ING Property Trust November 2009 - Argosy

23

ING Property Trust Interim Results Presentation November 2009 ING Property Trust Interim results presentation November 2009

Transcript of ING Property Trust November 2009 - Argosy

ING Property TrustInterim Results Presentation

November 2009

ING Property TrustInterim results presentationNovember 2009

1

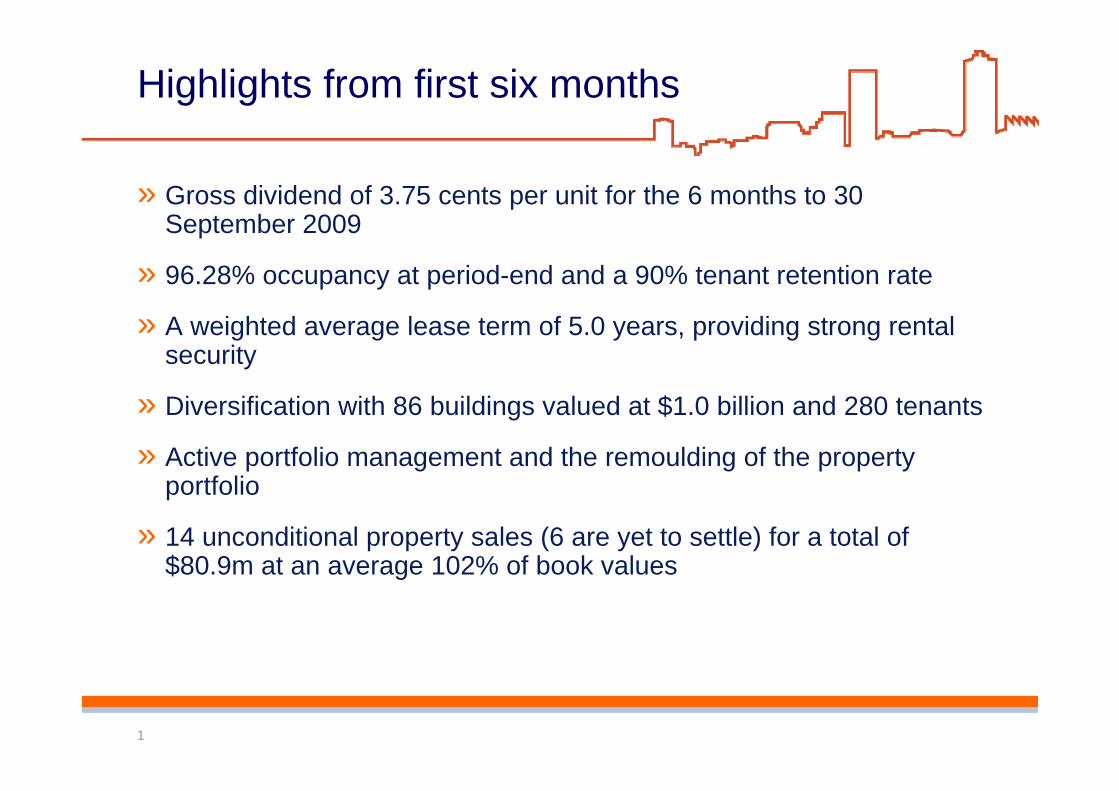

Highlights from first six months

» Gross dividend of 3.75 cents per unit for the 6 months to 30 September 2009

» 96.28% occupancy at period-end and a 90% tenant retention rate

» A weighted average lease term of 5.0 years, providing strong rental security

» Diversification with 86 buildings valued at $1.0 billion and 280 tenants

» Active portfolio management and the remoulding of the property portfolio

» 14 unconditional property sales (6 are yet to settle) for a total of $80.9m at an average 102% of book values

2

Trust basics

3

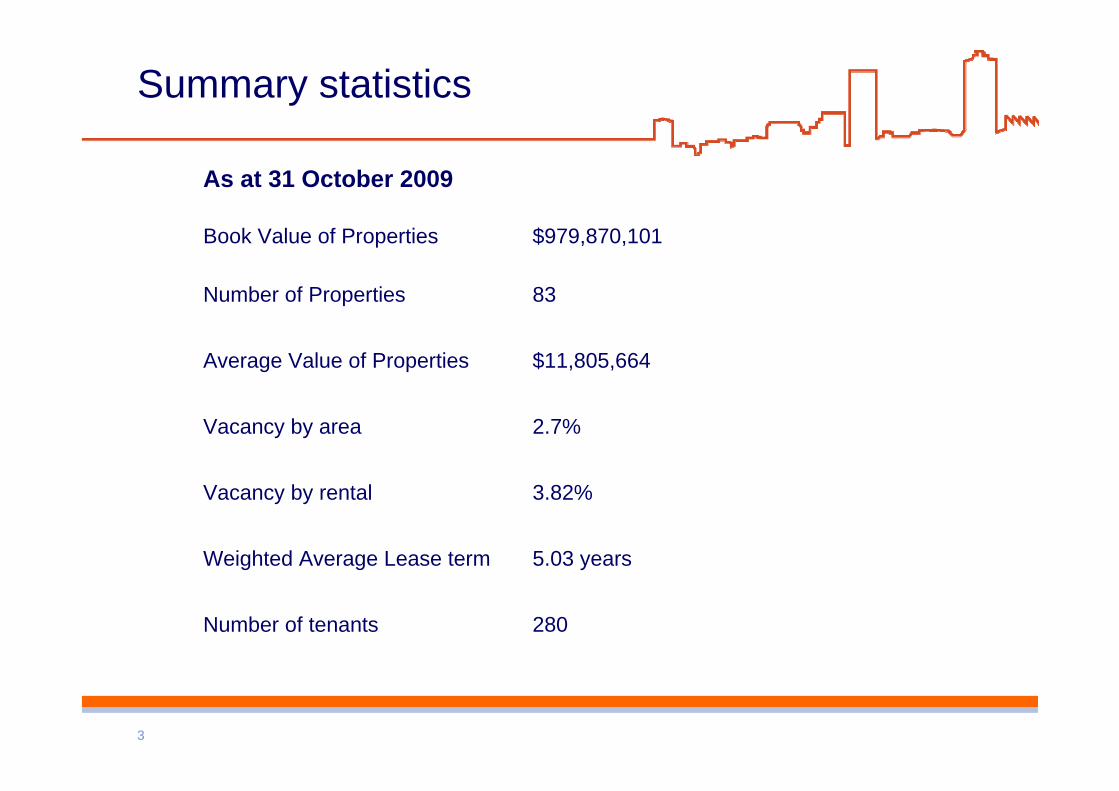

Summary statistics

280Number of tenants

5.03 yearsWeighted Average Lease term

3.82%Vacancy by rental

2.7%Vacancy by area

$11,805,664Average Value of Properties

83Number of Properties

$979,870,101Book Value of Properties

As at 31 October 2009

4

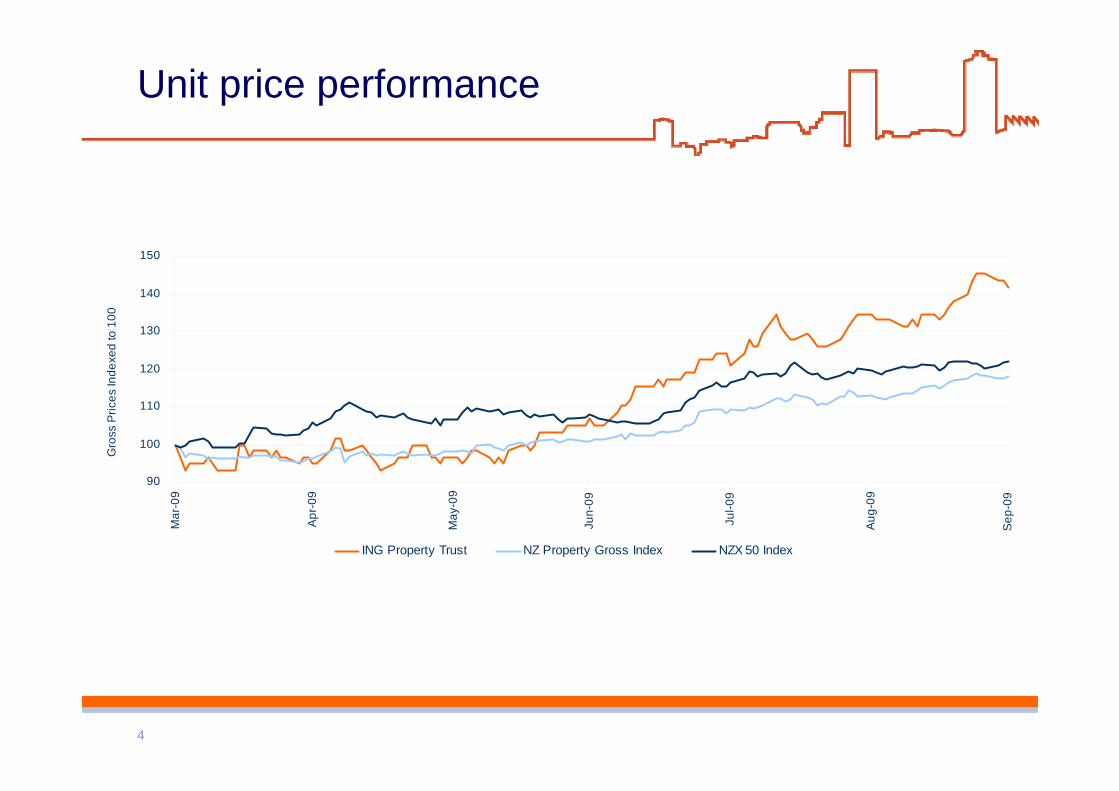

Unit price performance

90

100

110

120

130

140

150

Mar

-09

Apr

-09

May

-09

Jun-

09

Jul-0

9

Aug

-09

Sep

-09

Gro

ss P

rices

Inde

xed

to 1

00

ING Property Trust NZ Property Gross Index NZX 50 Index

5

Portfolio overview

6

Strategy

» Risk mitigation

» Debt Reduction

» Portfolio positioning for the future

7

Diversification

71%

10%

16%

3%

Auckland

Hamilton

Wellington

Regional

36%27%

37%

Office

Industrial

Retail

By sector By region

8

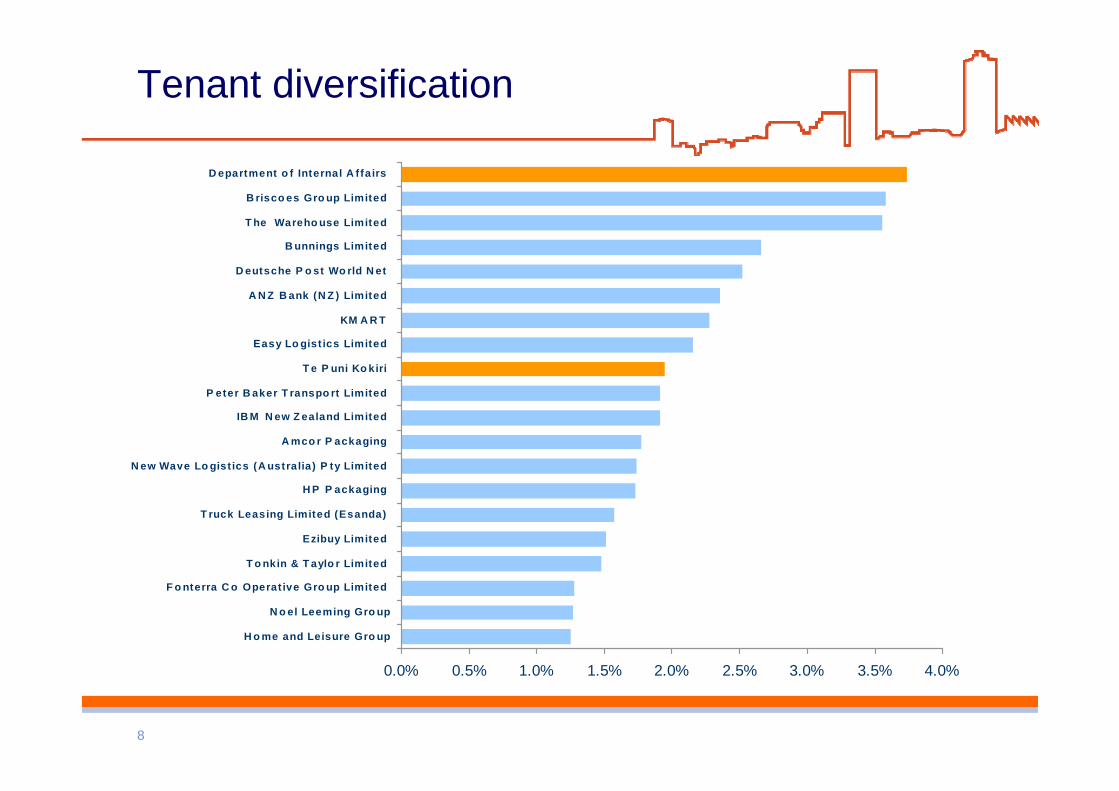

Tenant diversification

0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0%

H o me and Leisure Gro up

N o el Leeming Gro up

F o nterra C o Operat ive Gro up Limited

T o nkin & T aylo r Limited

Ezibuy Limited

T ruck Leasing Limited (Esanda)

H P P ackaging

N ew Wave Lo gist ics (A ustralia) P ty Limited

A mco r P ackaging

IB M N ew Z ealand Limited

P eter B aker T ranspo rt Limited

T e P uni Ko kiri

Easy Lo gist ics Limited

KM A R T

A N Z B ank (N Z ) Limited

D eutsche P o st Wo rld N et

B unnings Limited

T he Wareho use Limited

B risco es Gro up Limited

D epartment o f Internal A ffairs

9

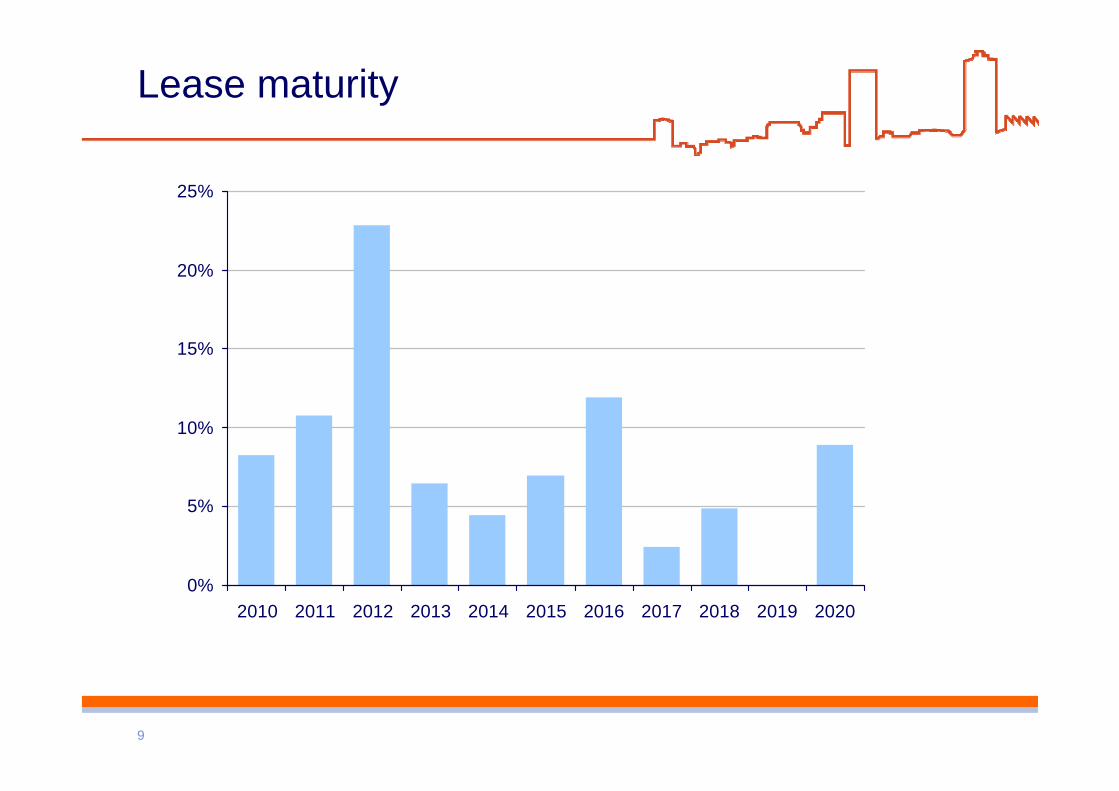

Lease maturity

0%

5%

10%

15%

20%

25%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

10

Property sales

102%$80,904,000$79,490,000

100%06 Dec 2009$13,700,000$13,700,000Croftfield Lane, Auckland

100%20 Jan 2010$4,050,000$4,050,000Khyber Pass Road (vacant)

100%20 Jan 2010$3,700,000$3,700,000Khyber Pass Road (vacant)

105%11 Jan 2010$2,000,000$1,900,00Maui Street, Hamilton (pending vacancy)

100%31 Mar 2010$6,850,000$6,850,000Port Hills Road, Christchurch

101%02 Nov 2009$1,750,000$1,730,000Maui Street, Hamilton (vacant)

100%30 Sep 2009$3,550,000$3,550,000Cryers Road, Auckland (pending vacancy)

103%11 Sep 2009$1,850,000$1,800.000Maui Street, Hamilton

100%21 Aug 2009$5,000,000$5,000,000Sir William Drive, East Auckland

99%31 Aug 2009$7,000,000$7,060,000Great South Road, Auckland (vacant)

112%03 Aug 2009$10,000,000$8,950,000Annie Huggan Grove, Wellington

100%31 Jul 2009$7,600,000$7,600,000London Street, Hamilton

100%01 Dec 2009$6,000,000$6,000,000Cavendish Drive, Manukau

103%19 Jun 2009$7,854,000$7,600,000College Hill, Auckland (pending vacancy)

Proportion of book value

Settlement date or expected settlement

dateSale PriceMarket value as

at 31/03/09Property

11

Positioning the portfolio for the future

» 18 new leases

» 27 lease extensions

» Sales of vacant property

» Sale of higher risk property

12

New lease to Dick Smith

» Eight year lease term

» Building upgrade at a cost of $2.15m

» Projected profit $700,000 at 8.5% cap

» Commences three months following vacation by Kmart

13

Valuations

» Sales show stability

» No requirement for interim valuation assessment

» Average size grants ability to transact in liquid part of the market

» There is a strong body of evidence to provide confidence in values

» Devaluation of Albany Block E assets

14

Manawatu Business Park

» Asset remains sound and activity is still a possibility

» Joint venture partner faces some challenges

» Good interest in the assets

» Agreement to sell $7m of investment property and $7.9m of vacantland

15

Financial overview

16

Financial performance

0.05(1.06)Post tax earnings per units (cents)$ 12.8m$(10.6m)$ 2.2m(Loss)/profit for the period - Comprehensive

$14.2m

-$ 0.1m

$13.6m

$ 1.5m

Revaluation losses – on investment property

- on construction

25.4%$18.0m$13.5mInterest expense

$ 1.9m$ 2.8m$ 0.9mCurrent taxation$ (6.8m)$ 5.7m$(1.1m)(Loss)/profit before income tax

$ 1.8m$ 7.3mLoss on derivatives

-6.3%$43.7m$40.9mNet rental income

$ 0.3m

$39.4m

HY09

$ (5.9m)

-12.7%

Change

$(5.6m)

$34.4m

HY10

(Loss)/profit for the period

Operating surplus (pre disposals, revals & tax)

17

Gross rental income

46.2

5.22.4

44.0

1.30.7

30.0

32.0

34.0

36.0

38.0

40.0

42.0

44.0

46.0

48.01H

09 G

ross

Ren

t

Sold

by

Mar

'09

Sold

by

Sept

'09

Ren

tin

crea

ses

E Bl

ock

1H10

Gro

ssR

ent

Dol

lars

(m)

In the period 30 September 2008 to 30 September 2009 there has been $150m of property sales settled. The following highlights the impact this has had on Gross Rental Income:

18

Interest rate management

» The Trust current interest rate hedge is 63% of its debt.» The interest rate paid (including margins and fees) in the first six

months of FY2010 was 6.36% (compared with 7.25% in 1H09).» The duration of the hedge portfolio is 4.3 years

Hedge expiry by year

17.0%

5.7% 7.6% 7.6%11.3%

17.0%

34.0%

0.0%

10.0%

20.0%

30.0%

2010 2011 2012 2013 2014 2015 2016

19

Distributable income

$(0.1m)$1.5mRevaluations losses/(gains) – construction$(0.4m)$0.1mInvestment disposal gains/(losses)

$1.8m$7.3mDerivative fair value adjustment$0.7m$0.7mManagement rights amortisation

4.28c4.13cGross distributable income per unit (cents)

$14.2m$13.6mRevaluations losses/(gains) – propertyAdjust for:

$21.9m$21.9mGross distributable income -$2.8m-$0.9mCurrent tax

$5.7m$(1.1m)(Loss)/profit before income tax

$19.0m$21.0mNet distributable income

3.73c3.95cNet distributable income per unit (cents)

HY09HY10

20

Financial position

5.7%42.0%39.6%Debt-to-total-assets ratio

23.9%$431.8m$404.9mBank debt

-17.7%$1,223.3m$1,006.9mTotal property value

-16.5%$673.1m$561.7mUnitholders’ funds

0.9%526.2m534.2mSecurities on issue

-19.7%131.7c105.8cNet asset backing per unit (cents)

HY09 ChangeHY10

21

Gearing

31 March 2009 to 30 September 2009

30

35

40

31 M

ar'0

9

Prop

erty

Sale

s

Cap

ex

Swap

Rev

al

30 S

ept'0

9

Unc

ondi

tiona

lsa

les

$40m

Addi

tiona

lSa

les

Gea

ring

%

Post 30 September 2009

22

Thank you