Cost of Quality

of 6

-

Upload

mina-maher-mikhail -

Category

Documents

-

view

9 -

download

0

description

Cost of Quality

Transcript of Cost of Quality

Cost of QualityWhen it comes to making decisions, most managers speakmoney. The Cost Of Quality theoryprovides the vocabulary to communicate between the quality professionalsand their managers.The Meaning of "Quality CostsThe term quality costs has different meanings to different people. Some equate quality costs with the costs of poor quality due tofinding and correcting defective work. Others equate the term with the costs to attain good quality. Others use the term to mean the costs of running the quality department. In mysite, the term "quality costs" means the cost of poor quality.Normally, quality-related costs run in the range of 10 to 30 percent of sales or 25 to 40 percent of operating expenses. Some of these costs arevisible and some hidden. The cost of quality not only includes factory operation, but the support operations significantlycontribute too.

Most companies can avoid quality costs. But these companies do not assign clear responsibility for action to reduce them. Nor do they create astructured approach for doing so.Tips You Must Know: The language of money is essential. Without the quality cost figures, communicating poor quality information to upper management is slow and ineffective.Quality cost measurement (only) does not solve quality problems. Some organizations publish it in the form of a scoreboard butthese efforts failbecauseoflackofaction.Don't limit the scope of quality costs. Most people focus quality cost only onthe cost of nonconformities. Quality costs include otherunmeasured costs such as lost sales due to poor quality. Wecall thisa hidden cost because we cannot easily measured it

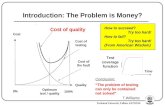

Categories ofCost of Quality:1- Internal Failure Costs The costs of deficiencies discovered before delivery. We associate deficiencies or nonconformitieswith the failure to meet explicit requirements or implicit needs of external or internal customers.

2- External Failure CostsThe costs associated with deficiencies found after product is received by the customer. These also includelost opportunities for sales revenue.3- Appraisal CostsThe costs incurred to determine the degree of conformance to quality requirements. For example inspection costs is an appraisal cost.4- Prevention CostsThe costs incurred to keep failure and appraisal costs to a minimum. For example product design or Poke Yoke costs are prevention costs.The total cost of quality is the sum of the four above categories.

Creating an Initial Quality Cost Study1. Review the literature on quality costs. Consult with others in similar industries who have had experience with applyingquality cost concepts.2. Select one organizational unit of the company to serve as a pilot site. This unit may be one plant, one large department, one product line, etc.3. Discuss the objectives of the study with the key people in the organization, particularly those in the accounting function. Two objectives are paramount...Determine the size of the quality problem and identify specific projects forimprovement.4. Collect whatever cost data are conveniently available from the accounting system. Use this information to gain management support to make a full cost of qualitystudy.5. The proposal should provide for a task force of all concerned parties. The task force will identify the work activities that contribute to the cost of poor quality. Use work records, job descriptions, flowcharts, interviews, and brainstorming to identify these activities.6. Publish a draft of the categories defining the cost of quality. Secure comments and revise.7. Finalize the definitions and secure management approval.8. Assignresponsibility for data collection and report preparation.9. Collect and summarize the data. Ideally, this should be done by accounting.10. Present the initial and final quality cost results from the quality improvement projectto management. Request authorization to proceed with a broader company wide program of measuring the costs and pursuing projects.

Clearly, the sequence must be tailored for each organization.

Capturing Quality Cost Tips1. Established expense accounts. Examples include inspection department appraisal activities and customer response warranty expenses.2. Define and analysis the ingredients of established expense accounts: For example, suppose an account called customer returns reports the cost of all goods returned. Some customers returned defective goods. Categorized these as cost of poor quality. Some customers return goods to reduce inventory. These are not cost of poor quality. You must break the customer returns into two separate expense accounts. To help distinguish the quality costs returns, someone must study of the return documents and classify all returns.3. Improve accounting documents: For example, some production department employees conduct product inspection. By securing their names, the associated payroll data, and inspection time youcan quantify these cost of quality.4. Include estimates: Input from knowledgeable personnel is clearly important.5. Use temporary records. For example, some production workers spend part of their time repairing defective product. Here you can create a temporary record to determine the repair time and thereby the repair cost. This cost can then be projected for the study time period.6. Utilize worksampling: Take random observations of activities. Within a few sampling you can calculate the percent of time spent in each of a number of predefined quality cost categories. Askemployees to record the observation as prevention, appraisal, failure, or first time work.7. Improve allocation of total resources: For example, some engineers are part-time engaged in making product failure analyses. The engineering department, however, makes no provision for charging engineering time to multiple accounts.Ask each engineer to make an estimate of time spent on product failure analysis. Do thisby keeping a temporary engineeringactivity log for several representative weeks. Categorized time spent due to a product failure as a failure cost.8. Track unit cost data: Here, the cost of correcting one error is estimated and multiplied by the number of errors per year. Examples include billing errors and scrap. Note that the unit cost per error may consist of corrections costs from several departments.9. Utilize market research data: Cost ofquality includes lost sales revenue due to poor quality. Although difficult to estimate, market research studies on customer satisfaction and loyalty can provide input data on dissatisfied customers and customer defections.