Banks under attack: Presentation to SEB Bank Baltics management about the #FinTech revolution

25

Banking Under Attack Startups that want to eat your business …. and what you might do to avoid it. 1 Andris K. Berzins April 2015 Image copyright of Home Box Office Inc.

-

Upload

andris-berzins -

Category

Business

-

view

550 -

download

1

Transcript of Banks under attack: Presentation to SEB Bank Baltics management about the #FinTech revolution

Banking Under AttackStartups that want to eat your business …. and what you might do to avoid it.

1

Andris K. Berzins April 2015

Image copyright of Home Box Office Inc.

Who is Andris K. Berzins?• MBA

• Consultant

• Entrepreneur

• Investor

• Advisor

• Volunteer

• NOT a banker

Text

The waves of changeComing to a bank near you

Mobile & data pervasive

• Smartphone penetration reaching saturation

• Always on • Apps and mobile

browsing maturing

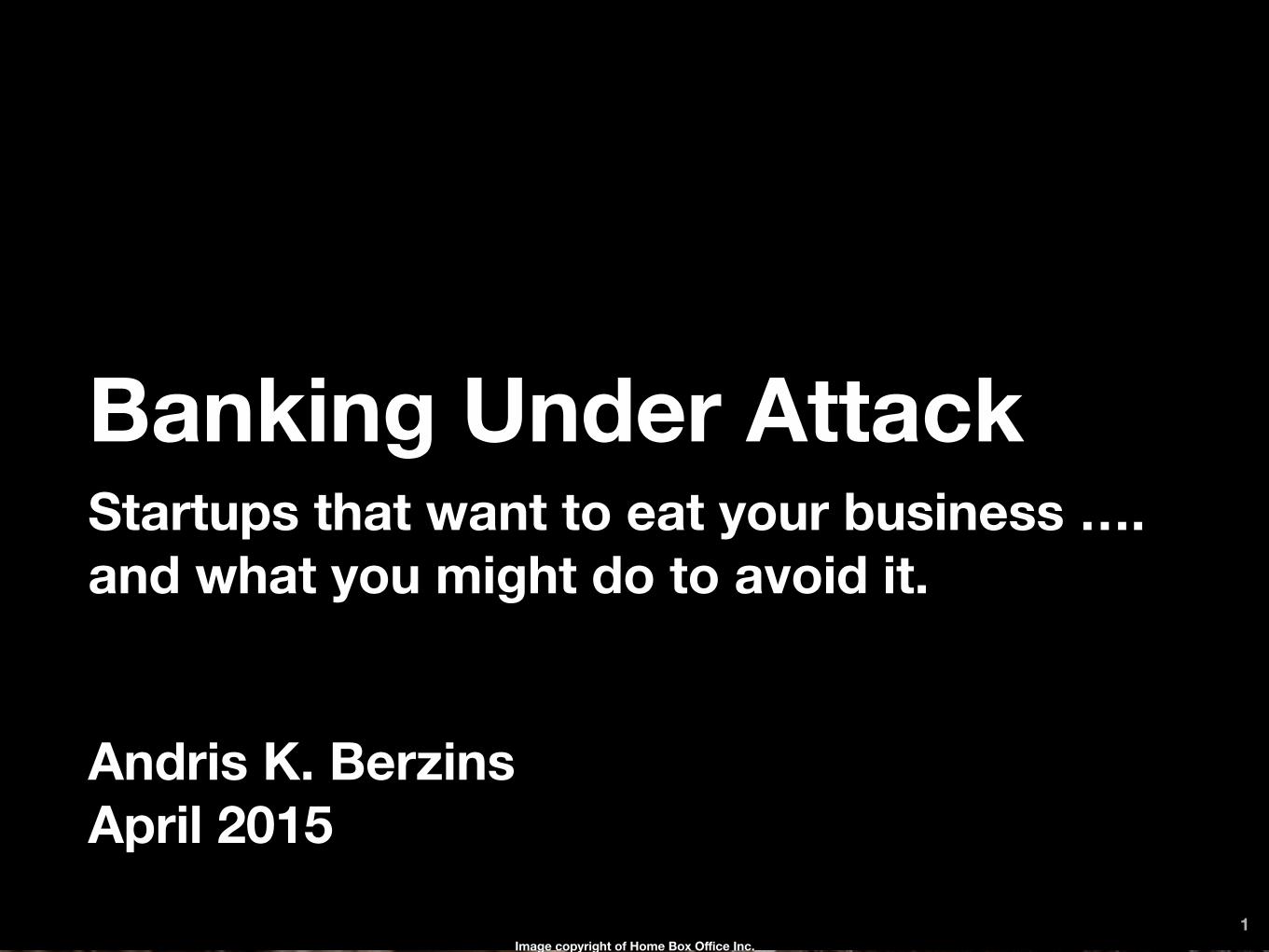

Mobile overtaking onlineM

obile

inte

ract

ions

as

% o

f tot

al

Online interactions as % of totalSource: Bain & Company presentation on digital reinvention in retail banking, 2015

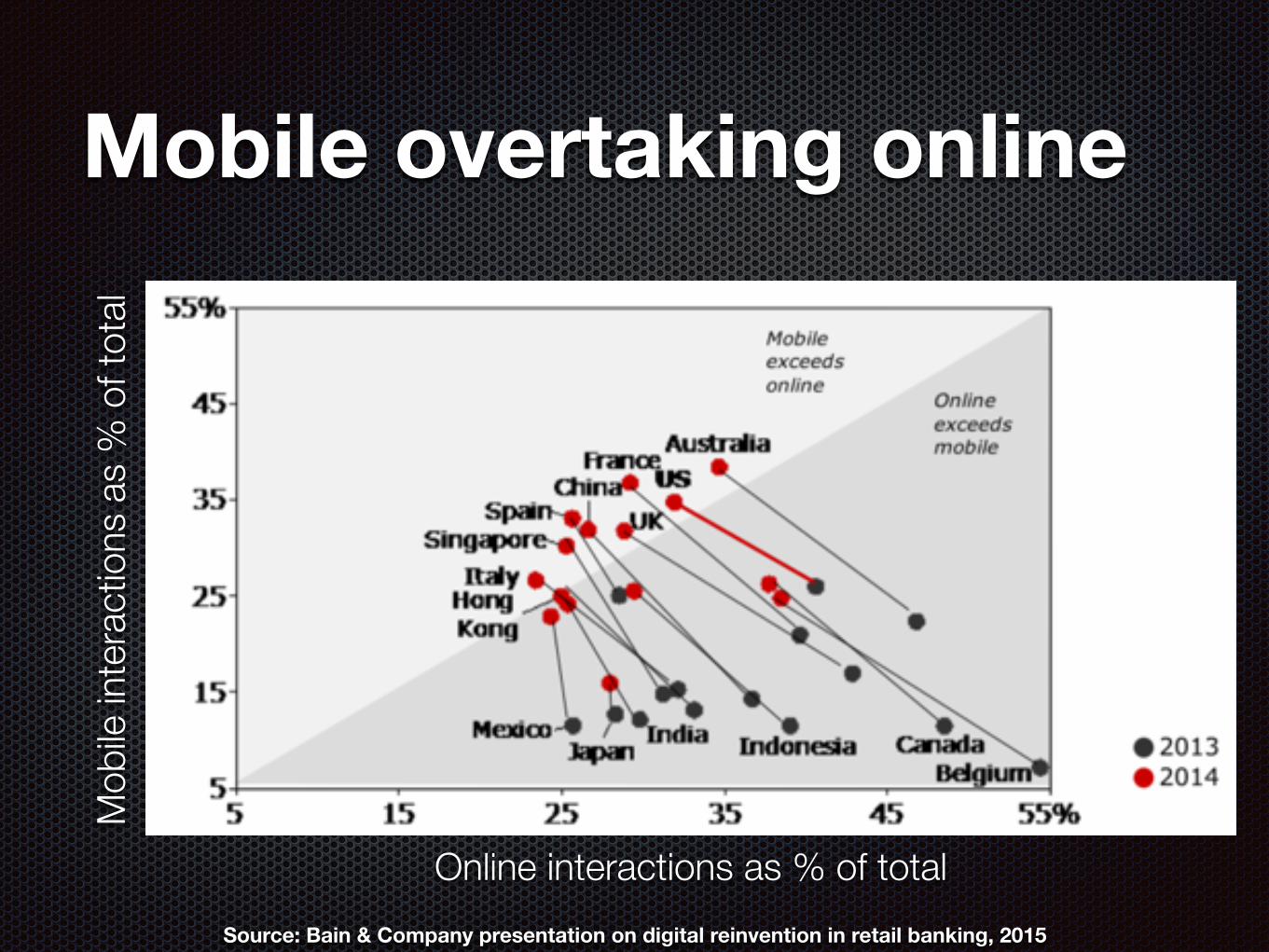

Personal identity device• The smartphone will

become THE identity device

• Viability driven by security improvements • Improved authentication • Device locking on theft • NFC and Bluetooth for

micro-location

Low trust in banks “to do what is right” dropping even further…… while technology companies enjoy very high trust.

0%

20%

40%

60%

80%

2009 2014

71%71%

29%34%

Bank

sTe

chno

logy

com

panie

sSource: Edelman Trustbarometer 2014 survey (EU)

Less trusted

% o

f EU

con

sum

ers

trus

t ind

ustr

y to

“do

wha

t is

right

”

Share of consumers using mobile apps rose 19% globally 2013-14Making every interaction ever more important

Less face time

Source: Bain report on banking customer loyalty (2014)

Expectations of speed of service and delivery are differentEspecially among younger consumers

Consumers want it now

The competition is different this time roundIncludes large technology companies and hungry startups

Fresh competition

Person-person micropayments are evolving rapidlyUsing smartphone and phone number as identity device is critical for this application

Venmo & Monea

Often deployed as a layer over traditional banking system - innovation is in user experience

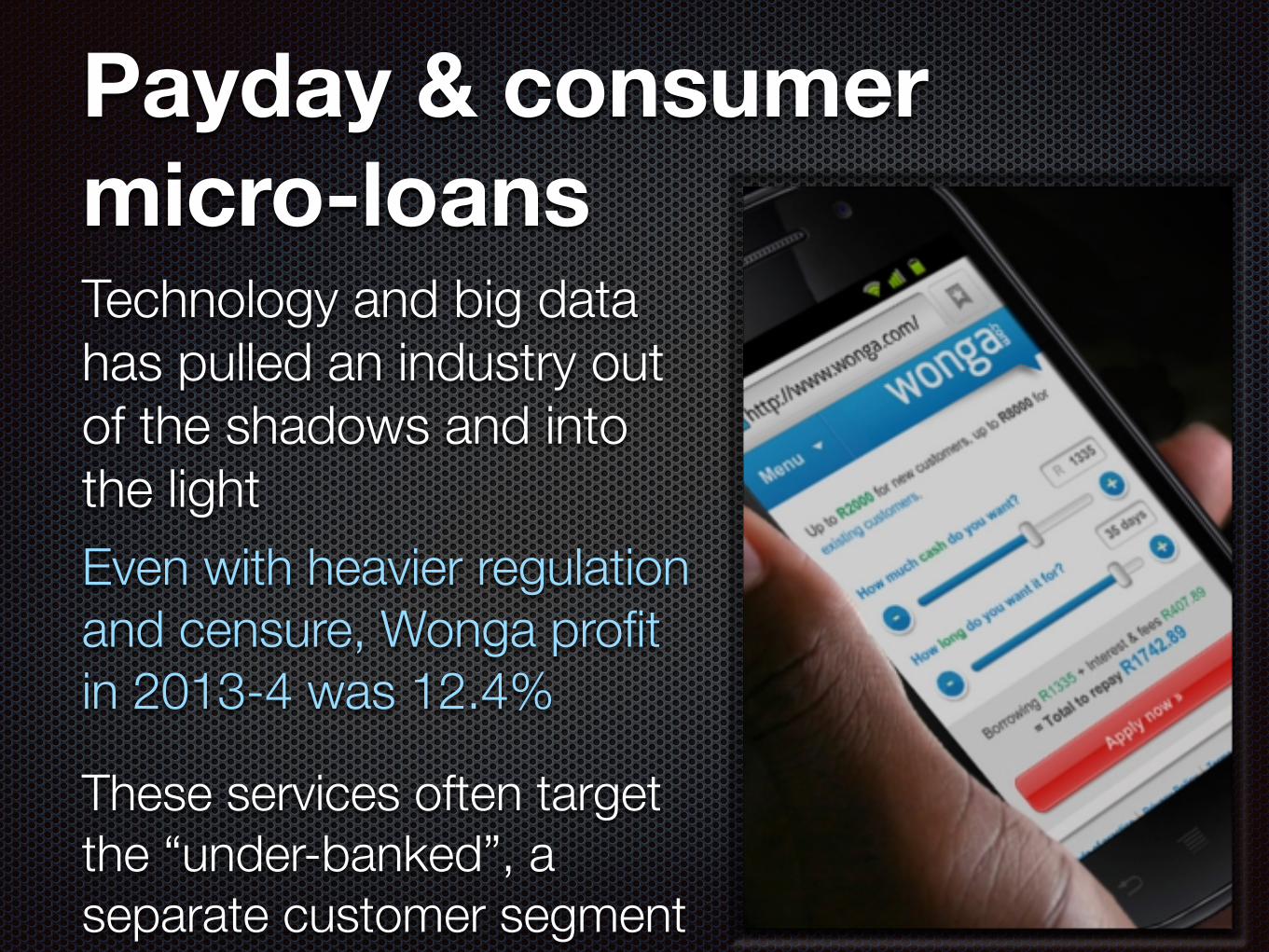

Technology and big data has pulled an industry out of the shadows and into the lightEven with heavier regulation and censure, Wonga profit in 2013-4 was 12.4%

Payday & consumer micro-loans

These services often target the “under-banked”, a separate customer segment

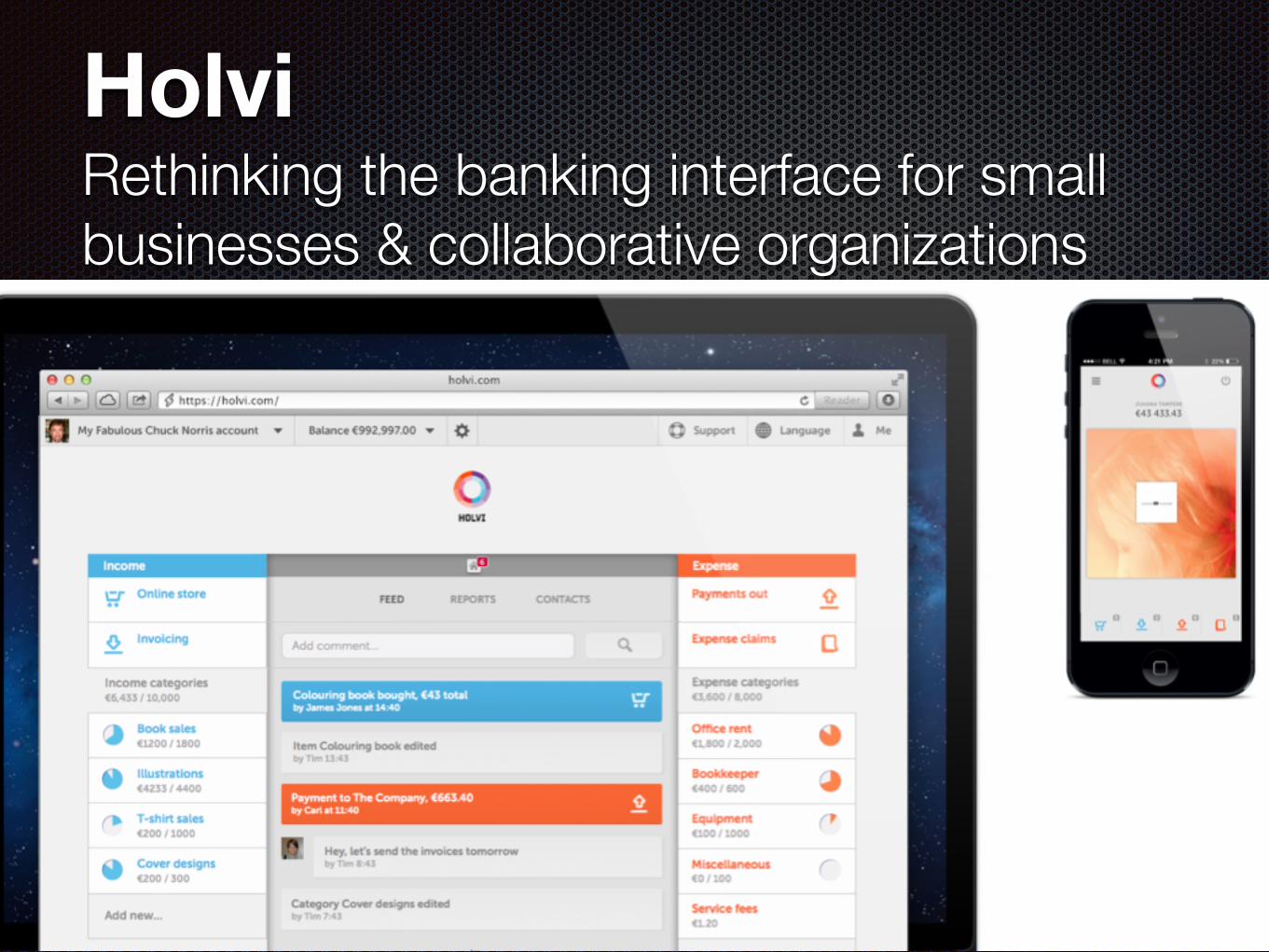

Rethinking the banking interface for small businesses & collaborative organizations

Holvi

Person-business loans enabled by big dataBondora & Mintos

Offers retail investors diversified loan portfolio with attractive rates

More mature US market shows where part of competitive advantage lies - in lower costs

Bondora & Mintos

These new players are able to “outsource compliance” and take advantage of “start from scratch” cost baseBut primary customer benefit is SPEED OF DECISION

Source: Goldman Sachs Future of Finance report, March 2015

Cost advantage merely allows profitability at much lower volume

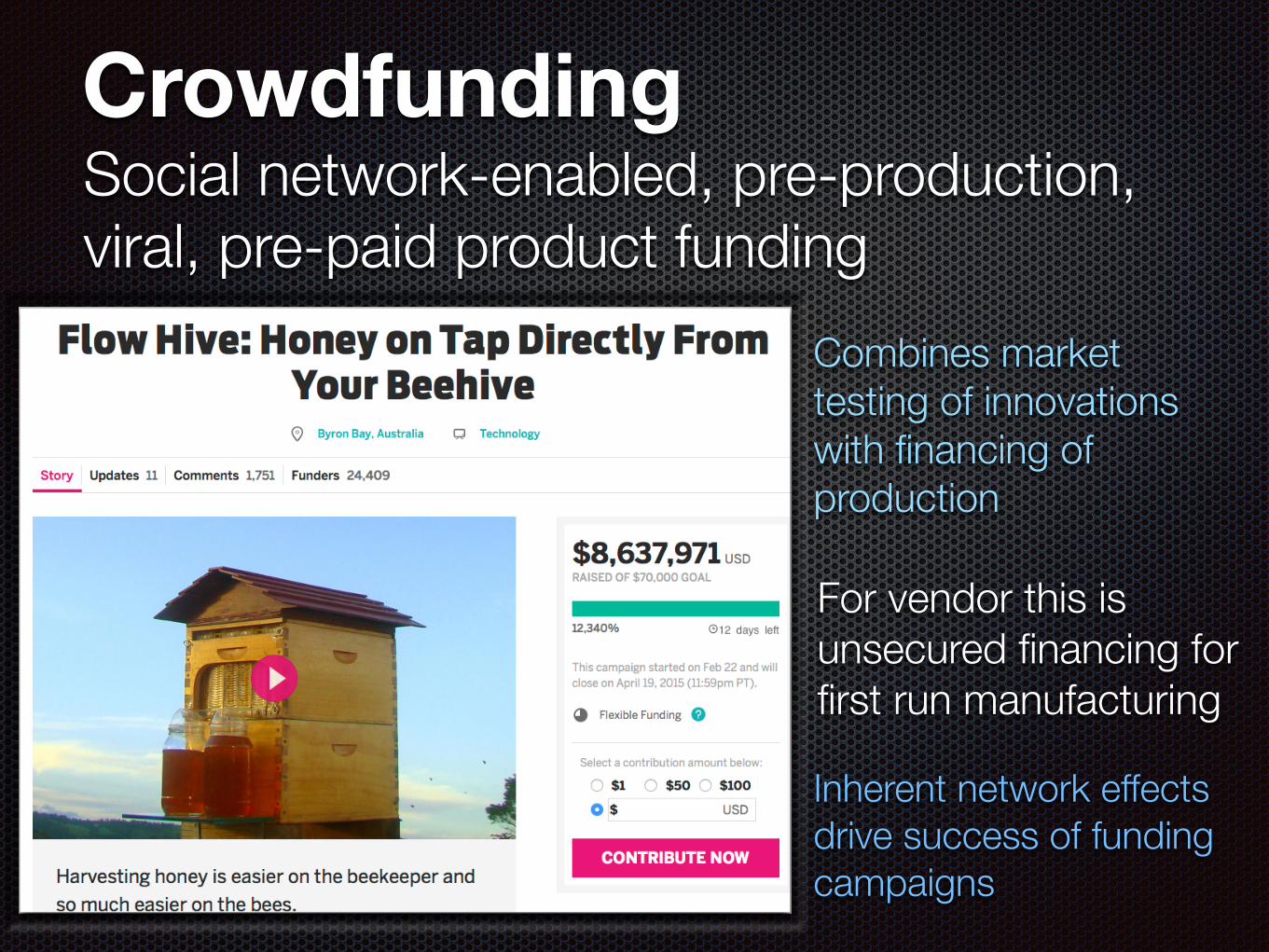

Social network-enabled, pre-production, viral, pre-paid product funding

Combines market testing of innovations with financing of production

Crowdfunding

For vendor this is unsecured financing for first run manufacturing

Inherent network effects drive success of funding campaigns

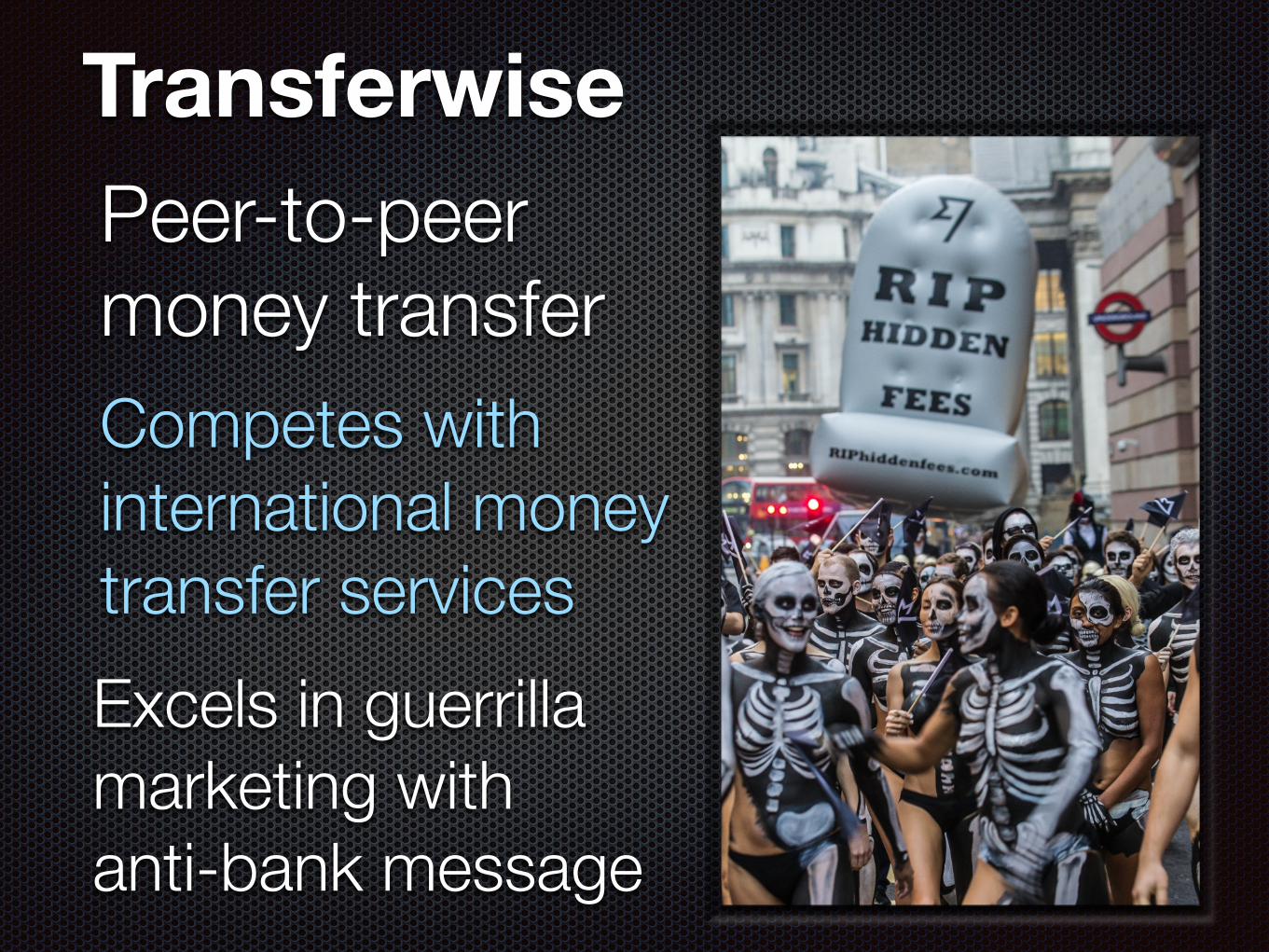

Peer-to-peer money transferCompetes with international money transfer services

Transferwise

Excels in guerrilla marketing with anti-bank message

Competing in this new race

Traditional banks have some distinct competitive advantages:• Big data • Customer service

organization • Branch networks • Low funding costs

Play to your strengths

• Fraud prevention • Account relationship management and awareness

• Spot issues related to corporate changes, market conditions

• Enhance customer relationships through positive interactions

• Proactive churn prevention • Analysis of historical pre-churn behavior can enable

warning and prevention service to be deployed • New income streams

• Advisory services for retailers using consumer spend data to improve retail locations and advertising targeting

Big Data Opportunity

Use your well-trained customer service staff but make sure they are empowered to make decisions to help clientsBranch visits are opportunities to WOW the customer and sell new products

Customer Service & Branches

Look for opportunities to make the service more convenient by allowing clients to avoid branch visits if they wishEven simple stand-alone technologies like Qminder can change the customer experience

The adoption of Bluetooth low energy beacons by the Apple and Android ecosystem brings huge opportunities

The mobile and physical experiences can now be brought together at a micro-location level

The iBeacon Opportunity

Think automated VIP priority queues, reinvention of the ATM experience, instant electronic document delivery…

Risk-taking is generally not rewarded in banking careers, to say the leastBut taking risks is essential to tackle the new competitive reality

Take more risks

Need to fund small risks, expand what succeedsNeed to change reward mechanisms and culture to encourage risk-taking and tolerate failure

Many new financial products may do better launched under a distinct brand

Think multiple brands & geographies

Banks may need to cannibalize their own products before competitors do, and better to do that under a separate brandSmaller country banks need to take advantage of licenses that allow them to sell financial products all over the EU, this is a great opportunity

Andris K. Berzins

+371 29568157

www.akberzins.com

Questions & Discussion