The MRO Market & Key Trends - aviationsuppliers.org · THE MRO MARKET & KEY TRENDS ASA Annual...

37

ICF proprietary and confidential. © ICF 2018 THE MRO MARKET & KEY TRENDS ASA Annual Conference 26 June 2018 Richard Brown Principal [email protected]

Transcript of The MRO Market & Key Trends - aviationsuppliers.org · THE MRO MARKET & KEY TRENDS ASA Annual...

ICF proprietary and confidential. © ICF 2018

THE MRO MARKET & KEY TRENDSASA Annual Conference26 June 2018

Richard BrownPrincipal

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

Today’s Agenda

1. Industry Context

2.MRO Market

3.Trends to watch

226 June 2018

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

Industry

Context

326 June 2018

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

Global airline industry achieved a record profitability of $38B USD in 2017, which is forecast to decrease to $33.8B in 2018

INDUSTRY CONTEXT

GLOBAL AIRLINE PROFITABILITY, 1998 – 2018F

-$30

-$20

-$10

$0

$10

$20

$30

$40

$USD

Billions

Europe, $8.6B

Africa, -$0.1B

North America, $15.0B

Asia Pacific, $8.2B

Middle East, $1.3BLatin America, $0.9B

$33.8B

4

Source: IATA/ ICF Analysis

26 June 2018

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

…but many airlines continue to struggle though North America has been a bright spot and was leading the way in 2017

INDUSTRY CONTEXT

-1.8%

-4.7%

0.1%

2.3%

1.0%

-0.9%

3.4%

4.7%

0.7%1.5%

3.0%

-0.4%

12.9%

5.2%

4.5%

2.9%

0.7%

-3.6%-5%

0%

5%

10%

15% 2008 2012 2017 2018F

Source: IATA/ ICF Analysis

GLOBAL AIRLINE EBIT MARGIN BY REGION

526 June 2018

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jan

-10

Apr-

10

Jul-

10

Oct-

10

Jan

-11

Apr-

11

Jul-

11

Oct-

11

Jan

-12

Apr-

12

Jul-

12

Oct-

12

Jan

-13

Apr-

13

Jul-

13

Oct-

13

Jan

-14

Apr-

14

Jul-

14

Oct-

14

Jan

-15

Apr-

15

Jul-

15

Oct-

15

Jan

-16

Apr-

16

Jul-

16

Oct-

16

Jan

-17

Apr-

17

Jul-

17

Oct-

17

Jan

-18

Apr-

18

Traffic growth driven by low fuel prices is slowly reversing, as 2018 has shown YTD growth of ~6.0%

INDUSTRY CONTEXT

Source: EIA; IATA

Fuel prices

declined ~50%

Air traffic growth rates increased from 5%

annually to >7.5% …

… but YTD growth limited at 6.0%

Jet fuel spot

price

($ per gallon)

Air traffic annual

growth rate

Fuel edging

back up

26 June 2018 6

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

0%

10%

20%

30%

40%

50%

60%

70%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

COMMERCIAL AIRCRAFT OEM PRODUCTION BACKLOG DRIVERS OF OEM BACKLOG

Backlog more than doubled

between 2010 and 2014,

driven by:

– Emerging market growth

– Very low interest rates and

plentiful capital

– High oil and commodity

prices

– Introduction of new

technology aircraft/engines

In 2017, total backlog

decreased for the first time

since 2009 as deliveries ramp-

up and orders slowdown

Commercial aircraft OEM production backlog remains at historical highs

INDUSTRY CONTEXT

Source: CAPA, ICF Analysis

Order

BacklogBacklog/

% Active Fleet

# of aircraft

726 June 2018

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

MRO Market

826 June 2018

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

NarrowbodyJet

WidebodyJet

Turboprop

Regional Jet

55%

13%

19%

13%

The current commercial air transport fleet consists of ~29,100 aircraft; ~8,500 are located in North America

MRO MARKET

2017 GLOBAL COMMERCIAL AIR TRANSPORT FLEET

Source: ICF Analysis: CAPA 2017

BY AIRCRAFT TYPE

~29,100

Aircraft

BY GLOBAL REGION

29%

29%

24%

7%

6%5%

Latin America

Africa North

America

(~8,500)

Asia

Pacific

Middle East

~29,100

Aircraft

Europe

926 June 2018

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

29%35%

37%

29%

23%

20%24%

23%

22%

7%

8%

8%

7%

7%

5%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2017 2027 2037

Africa, 3.5%

Middle East, 5.6%

South America, 3.6%

Europe, 2.5%

North America, 0.8%

Asia Pacific, 5.0%

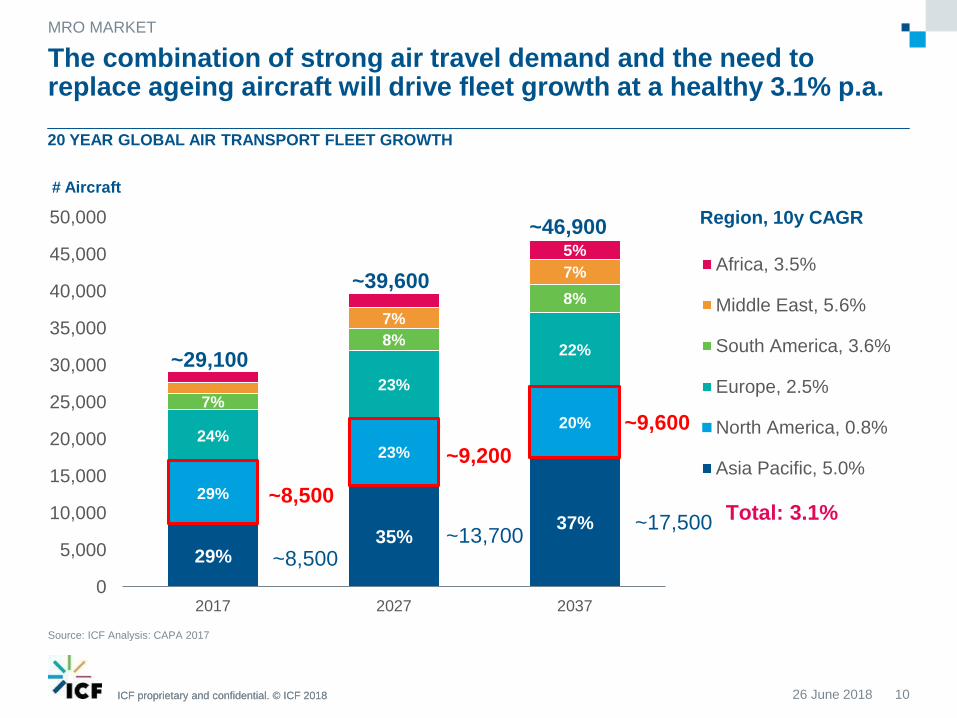

The combination of strong air travel demand and the need to replace ageing aircraft will drive fleet growth at a healthy 3.1% p.a.

MRO MARKET

20 YEAR GLOBAL AIR TRANSPORT FLEET GROWTH

Source: ICF Analysis: CAPA 2017

~29,100

~39,600

Region, 10y CAGR

Total: 3.1%

# Aircraft

~46,900

10

~9,600

~17,500

~8,500

~8,500

~9,200

~13,700

26 June 2018

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

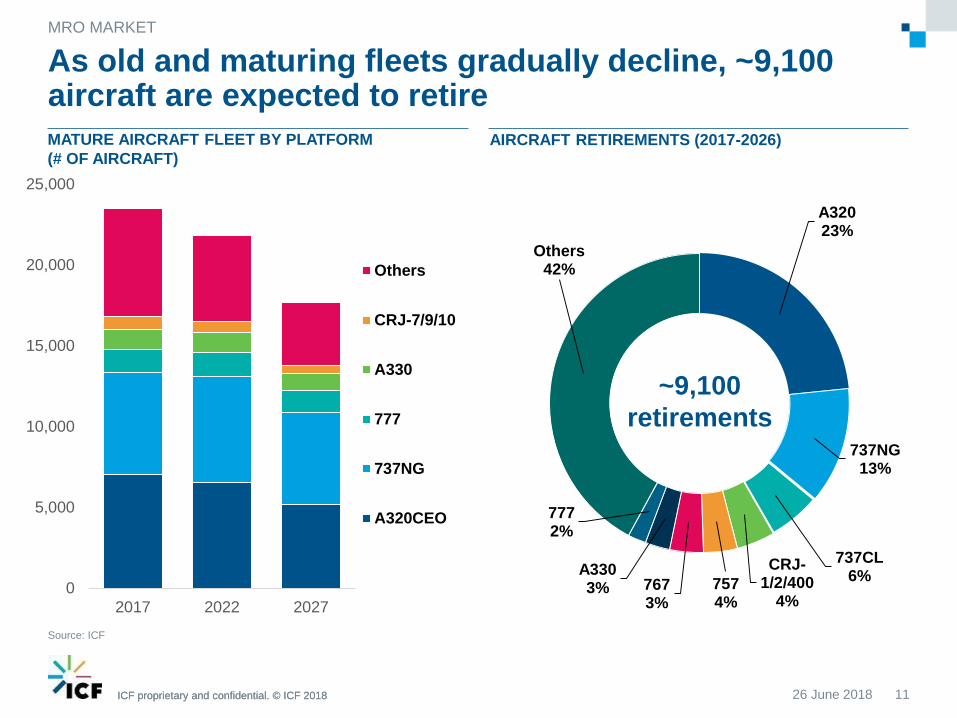

A32023%

737NG13%

737CL6%

CRJ-1/2/400

4%7574%

7673%

A3303%

7772%

Others42%

As old and maturing fleets gradually decline, ~9,100 aircraft are expected to retire

MRO MARKET

MATURE AIRCRAFT FLEET BY PLATFORM

(# OF AIRCRAFT)

AIRCRAFT RETIREMENTS (2017-2026)

0

5,000

10,000

15,000

20,000

25,000

2017 2022 2027

Others

CRJ-7/9/10

A330

777

737NG

A320CEO

Source: ICF

~9,100

retirements

26 June 2018 11

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

Engines

Components

Line

Airframe

Modifications

42%

13%

17%

7%

2017 commercial air transport MRO demand is $75.5B; Asia is now larger than North America and Europe in market size

MRO MARKET

2017 COMMERCIAL AIR TRANSPORT GLOBAL MRO DEMAND

Source: ICF Analysis: CAPA 2017

BY MRO SEGMENT

$75.5B

BY GLOBAL REGION

31%

26%

25%

8%

6% 4%Middle

East

Africa

Asia

Pacific

North America

$19.4B

South

America

$75.5B

Europe

21%

1226 June 2018

ICF proprietary and confidential. © ICF 2018

42%

45%46%

21%

20%

20%

17%

15%

14%

13%

12%

11%

8%

8%

8%

$0

$20

$40

$60

$80

$100

$120

$140

2017 2027 2037

Modfications, 5.8%

AHM, 3.5%

Line, 3.3%

Component, 4.3%

Engine, 5.2%

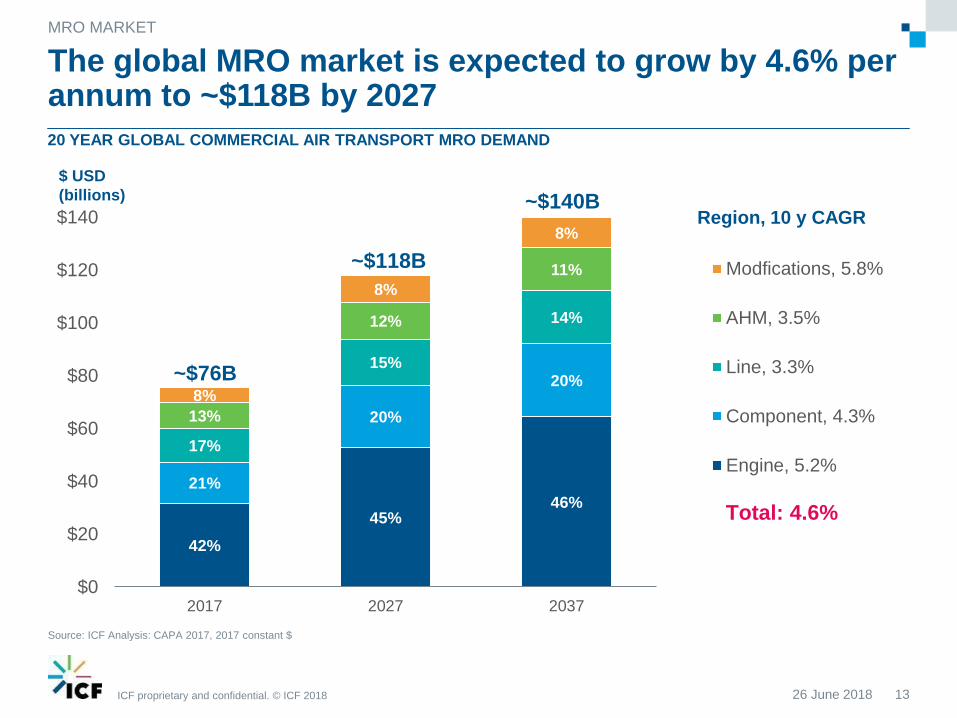

The global MRO market is expected to grow by 4.6% per annum to ~$118B by 2027

MRO MARKET

20 YEAR GLOBAL COMMERCIAL AIR TRANSPORT MRO DEMAND

Source: ICF Analysis: CAPA 2017, 2017 constant $

~$76B

~$118B

Total: 4.6%

$ USD

(billions) ~$140BRegion, 10 y CAGR

1326 June 2018

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

31%

36%38%

26%

19%

18%

25%

23%

21%

8%

11%

10%

6%

7%

7%

5%

$0

$20

$40

$60

$80

$100

$120

$140

2017 2027 2037

Africa, 6.1%

South America, 5.7%

Middle East, 7.9%

Europe, 3.3%

North America, 1.7%

Asia Pacific, 6.1%

Asia continues to grow strongly and will generate 38% of MRO demand by 2037…

MRO MARKET

20 YEAR GLOBAL COMMERCIAL AIR TRANSPORT MRO DEMAND

Source: ICF Analysis: CAPA 2017, 2017 constant $

~$76B

~$118B

Total: 4.6%

$ USD

(billions) ~$140BRegion, 10y CAGR

14

~$24.6B

~$19.3B

~$22.9B

26 June 2018

ICF proprietary and confidential. © ICF 2018

40%42% 43%

20%

21%21%17%

16%15%

16%

14%13%

8%

7%

8%

$0

$5

$10

$15

$20

$25

2017 2027 2037

Modifications, 1.3%

Airframe, 0.7%

Line, 1.0%

Component, 1.9%

Engine, 2.4%

North American MRO spend exhibits marginal growth, increasing by 1.7% per annum to $22.9B by 2027

MRO MARKET

20 YEAR NORTH AMERICAN COMMERCIAL AIR TRANSPORT MRO DEMAND

Source: ICF Analysis: CAPA 2017, 2017 constant $

Category, 10y CAGR

Total: 1.7%

$ USD

(billions)

$19.3B

$22.9B

$24.6B

26 June 2018 15

ICF proprietary and confidential. © ICF 2018

49%

58% 57%

31%

30%29%16%

9%12%

$0

$5

$10

$15

$20

$25

2017 2027 2037

Turboprop, -1.5%

Regional Jet, -3.8%

Widebody Jet, 1.5%

Narrowbody Jet, 3.3%

North American MRO spend exhibits marginal growth, increasing by 1.7% per annum to $22.9B by 2027

MRO MARKET

20 YEAR NORTH AMERICAN COMMERCIAL AIR TRANSPORT MRO DEMAND

Source: ICF Analysis: CAPA 2017, 2017 constant $

Category, 10y CAGR

Total: 1.7%

$ USD

(billions)

$19.3B

$22.9B

$24.6B

26 June 2018 16

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

Trends To

Watch

1726 June 2018

ICF proprietary and confidential. © ICF 2018

PMA Outlook

26 June 2018 18

ICF proprietary and confidential. © ICF 2018

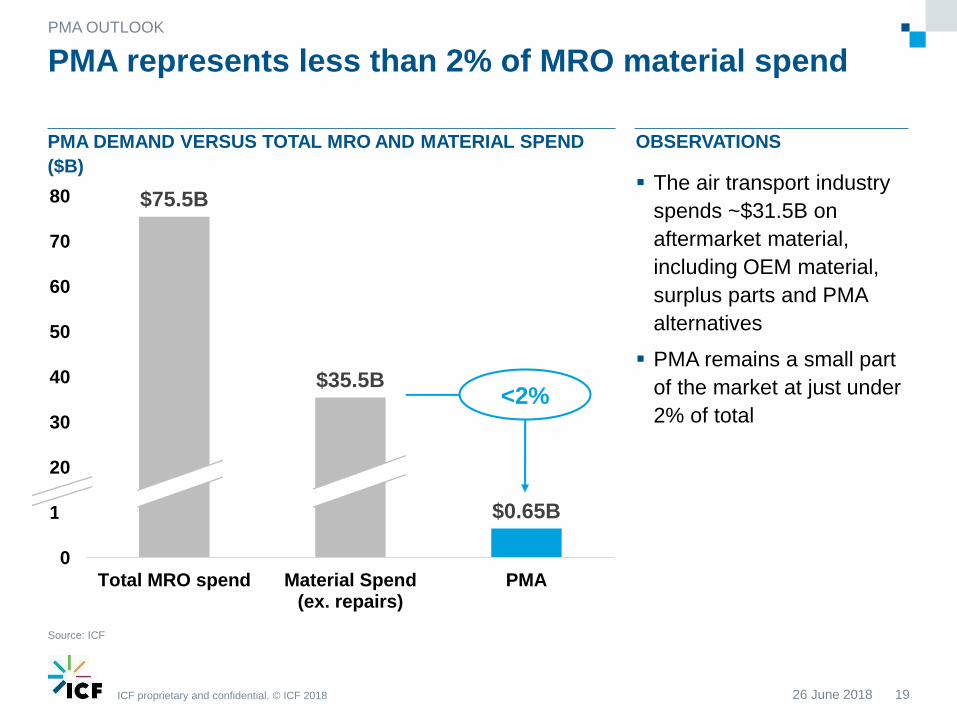

OBSERVATIONS

The air transport industry

spends ~$31.5B on

aftermarket material,

including OEM material,

surplus parts and PMA

alternatives

PMA remains a small part

of the market at just under

2% of total

PMA represents less than 2% of MRO material spend

26 June 2018 19

PMA OUTLOOK

Source: ICF

$75.5B

$35.5B

$0.65B

0

10

20

30

40

50

60

70

80

Total MRO spend Material Spend(ex. repairs)

PMA

PMA DEMAND VERSUS TOTAL MRO AND MATERIAL SPEND

($B)

<2%

ICF proprietary and confidential. © ICF 2018

Cabin & Components

Engine

Airframe

2017 commercial air transport PMA demand was ~$650M, N. America and Europe remain the key regions

PMA OUTLOOK

2017 COMMERCIAL AIR TRANSPORT GLOBAL PMA DEMAND

Source: ICF

BY MRO SEGMENT BY GLOBAL REGION

37%

27%

23%

5%5%3%Middle

East

Africa

Asia

Pacific

North

America

South

America

Europe

26 June 2018 20

60%

33%

7%

~$650M ~$650M

ICF proprietary and confidential. © ICF 2018

16,37336,202

61,439

220,074

356,683

468,689

107,737

0

100,000

200,000

300,000

400,000

500,000

<1991 1991 - 1995 1996 - 2000 2001 - 2005 2006 - 2010 2011 - 2015 2016-18YTD

Volume of PMA approvals has steadily grown since 1990; the pace appears to have slowed in 2016 and 2017

26 June 2018 21

PMA OUTLOOK

FAA APPROVED PMA PART NUMBERS BY APPROVAL YEAR

Source: Federal Aviation Administration – PMA Database extract June 2018

ICF proprietary and confidential. © ICF 2018

$654

$1,158

0

200

400

600

800

1,000

1,200

2017 2027

Airframe, 5%

Engine, 0.2%

Cabin &Components, 8.1%

PMA is set to grow significantly over the next decade, growing at a 5.8% CAGR to >$1.15B by 2027

PMA OUTLOOK

10 YEAR GLOBAL COMMERCIAL AIR TRANSPORT PMA DEMAND (CONSTANT 2017 US$)

Source: ICF, 2017 constant $

PMA Part Category, CAGR

Total: 5.8%

$ USD

(millions)

26 June 2018 22

ICF proprietary and confidential. © ICF 2018 23

M&A Activity

26 June 2018

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

Consolidation continues among System OEMs

TRENDS TO WATCH

Melrose acquires GKN

2018

Splits off 2 divisions,

keeps Aerospace

2017Rockwell Collins

acquires B/E

Aerospace

2016

Safran acquires

Zodiac

2017

UTC plans to

acquires

Rockwell Collins

2017

?

24

Next?Acquisitions?

Divestments?

BOEING

Boeing announces

acquisition of KLX

2018

?

26 June 2018

ICF proprietary and confidential. © ICF 2018

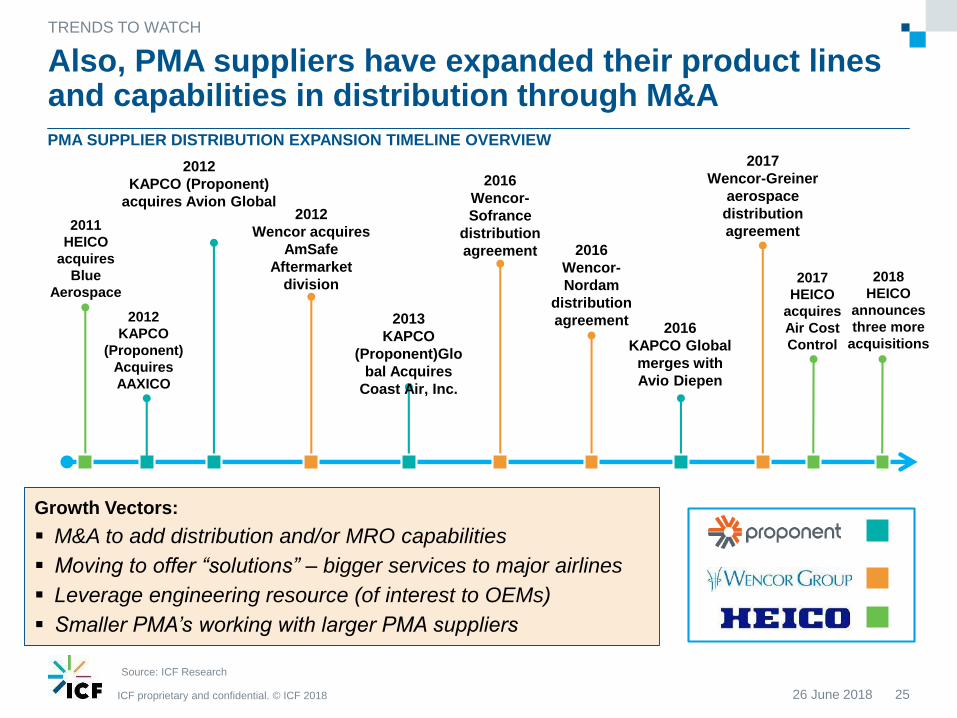

Also, PMA suppliers have expanded their product lines and capabilities in distribution through M&A

26 June 2018 25

TRENDS TO WATCH

PMA SUPPLIER DISTRIBUTION EXPANSION TIMELINE OVERVIEW

Source: ICF Research

2012

KAPCO

(Proponent)

Acquires

AAXICO

2012

KAPCO (Proponent)

acquires Avion Global

2013

KAPCO

(Proponent)Glo

bal Acquires

Coast Air, Inc.

2016

KAPCO Global

merges with

Avio Diepen

2017

HEICO

acquires

Air Cost

Control

2011

HEICO

acquires

Blue

Aerospace

2016

Wencor-

Nordam

distribution

agreement

2017

Wencor-Greiner

aerospace

distribution

agreement2012

Wencor acquires

AmSafe

Aftermarket

division

2016

Wencor-

Sofrance

distribution

agreement

Growth Vectors:

M&A to add distribution and/or MRO capabilities

Moving to offer “solutions” – bigger services to major airlines

Leverage engineering resource (of interest to OEMs)

Smaller PMA’s working with larger PMA suppliers

2018

HEICO

announces

three more

acquisitions

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

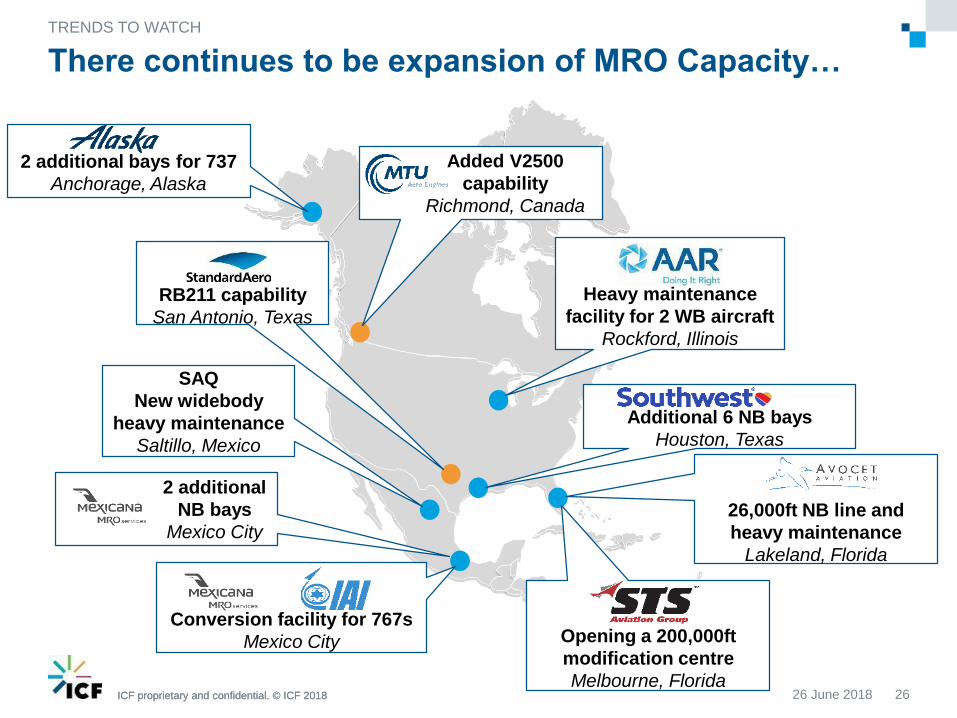

There continues to be expansion of MRO Capacity…

TRENDS TO WATCH

2 additional bays for 737

Anchorage, Alaska

Heavy maintenance

facility for 2 WB aircraft

Rockford, Illinois

2 additional

NB bays

Mexico City

SAQ

New widebody

heavy maintenance

Saltillo, Mexico

26,000ft NB line and

heavy maintenance

Lakeland, Florida

Additional 6 NB bays

Houston, Texas

Opening a 200,000ft

modification centre

Melbourne, Florida

Added V2500

capability

Richmond, Canada

Conversion facility for 767s

Mexico City

RB211 capability

San Antonio, Texas

2626 June 2018

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018 27

Impact of New

Technology

Aircraft

26 June 2018

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

~9k

17k

24k

~29k

~35k

~39k

0

10,000

20,000

30,000

40,000

2017 2022 2027

# aircraft

Limited AHM, -2.7%

AHM, 10.4%

ICF IN-SERVICE AIR TRANSPORT FLEET FORECAST OBSERVATION

ICF expects ~23,500 aircraft

will be equipped with Aircraft

Health Monitoring (AHM) by

2027, growing at 10.4% CAGR

This is driving a digitisation of

aircraft operations, which will

see high growth in the e-

enabled services and further

advances in health

management

The fleet of e-enabled aircraft is set to more than double over the next decade

28

IMPACT OF NEW TECHNOLOGY AIRCRAFT

Source: ICF

AHM adoption,

2017 – 2027

CAGR

TOTAL = 3.0%

~60%

~50%

~30%

26 June 2018

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

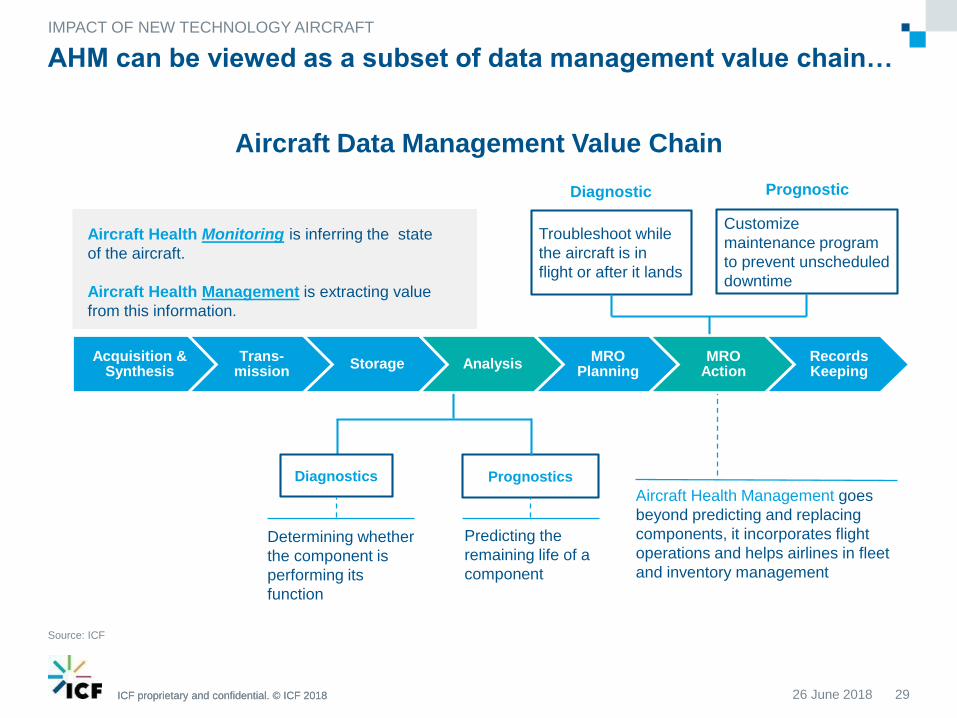

AHM can be viewed as a subset of data management value chain…

29

IMPACT OF NEW TECHNOLOGY AIRCRAFT

Source: ICF

Diagnostics Prognostics

Determining whether

the component is

performing its

function

Predicting the

remaining life of a

component

Troubleshoot while

the aircraft is in

flight or after it lands

Customize

maintenance program

to prevent unscheduled

downtime

Diagnostic Prognostic

Aircraft Health Monitoring is inferring the state

of the aircraft.

Aircraft Health Management is extracting value

from this information.

Aircraft Health Management goes

beyond predicting and replacing

components, it incorporates flight

operations and helps airlines in fleet

and inventory management

Acquisition & Synthesis

Trans-mission

Storage AnalysisMRO

PlanningMRO

ActionRecords Keeping

Aircraft Data Management Value Chain

26 June 2018

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

The race is on… new battlegrounds are emerging across the MRO market

30

IMPACT OF NEW TECHNOLOGY AIRCRAFT

Source: ICF

2017

AnalytX

BOEING

Avasio

2015

2015

Analytics

Division

Skywise

2017

2017

Aviatar2017

R2 Data Labs

2017

FlightPulse

2017

United

Technologies

Digital Division

Digital Solutions

2017

Prognos

2016

Availability

Centre

2017

EngineWise

2017

Predictive

Maintenance

Partnership

2018

2015

Digital

Collaboration

Centre in Dubai

26 June 2018

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

Digitisation could enable airlines to save in excess of $5B/year through lower fuel, maintenance and delay costs

31

IMPACT OF NEW TECHNOLOGY AIRCRAFT

Health Monitoring and Predictive Maintenance

Airline Industry savings: ~$3B (conservative estimate)

Driven by improved dispatch reliability, No Fault Found reduction, Inventory reduction

and Improved labour productivity

Fuel Cost Savings

Airline Industry savings: ~$1.7B (conservative estimate)

Continuous flight optimisation through live

weather updates, speed and altitude

optimisation…

Delay Reduction

Airline Industry savings:

~$0.8B (conservative

estimate)

Improved turnaround process,

in-flight routing optimisation

Source: ICF

26 June 2018

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

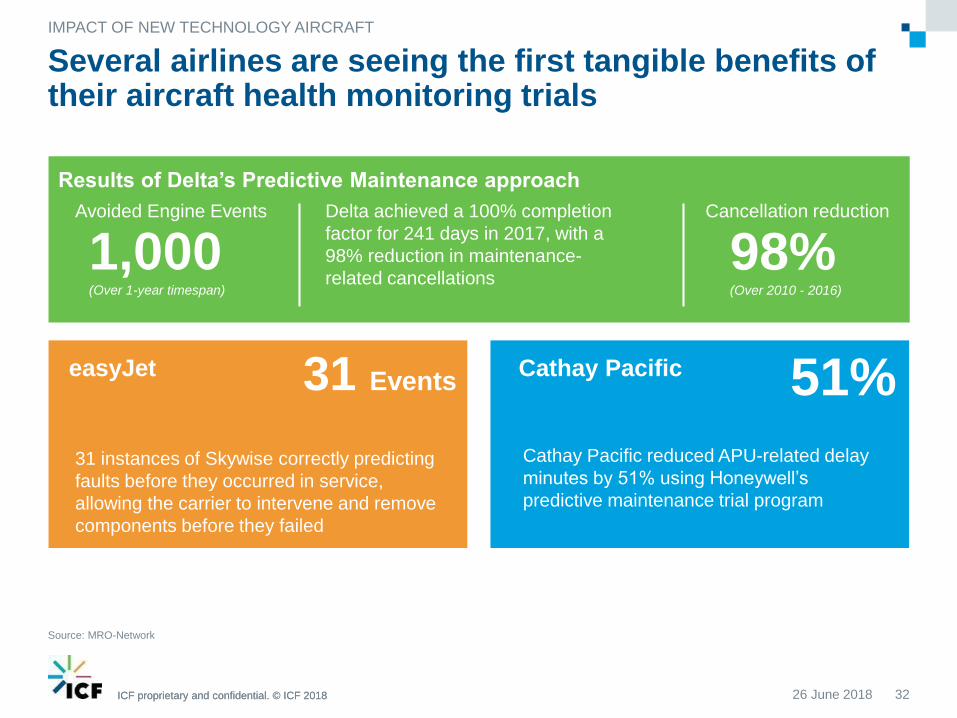

Several airlines are seeing the first tangible benefits of their aircraft health monitoring trials

IMPACT OF NEW TECHNOLOGY AIRCRAFT

Source: MRO-Network

Delta achieved a 100% completion

factor for 241 days in 2017, with a

98% reduction in maintenance-

related cancellations

Results of Delta’s Predictive Maintenance approach

1,000(Over 1-year timespan)

Drop in maintenance-related cancellations of…

Southwest to install AHM on complete 737 NG

fleet to improve performance

98%(Over 2010 - 2016)

Avoided Engine Events Cancellation reduction

31 Events

31 instances of Skywise correctly predicting

faults before they occurred in service,

allowing the carrier to intervene and remove

components before they failed

easyJet 51%

Cathay Pacific reduced APU-related delay

minutes by 51% using Honeywell’s

predictive maintenance trial program

Cathay Pacific

3226 June 2018

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

Considerations

3326 June 2018

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

In Conclusion…

CONSIDERATIONS

34

• The Global Air Transport MRO

market outlook remains robust at

$76B growing to $118B over the

next decade (an expected growth of

4.6% per annum)

• North America generates $19.4B of

MRO demand and will grow to $23B

by 2027

• New technology aircraft and engines

are creating both new challenges

and opportunities for aviation

stakeholders including how best to

leverage big data to reduce operator

costs, help increase efficiency and

increase reliability

26 June 2018

ICF proprietary and confidential. © ICF 201835

Let’s Make Big

Things PossibleConsulting for the

Global Aviation Industry

Airlines | Airports | Aircraft | Aerospace and Maintenance

Helping you manage assets and

operations, mitigate risk, and maximize

return on investment.

+44 7718 893 833

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

ICF supports clients across the aviation industry

Serving the

Aviation

Community

Since 1963

Broad Perspective.

Compelling Results. ICF offers our team of nearly 100 aviation experts dedicated to

strategic and operations consulting for the aviation industry. Our

aviation practice was founded as SH&E in 1963 and expanded with

the acquisition of AeroStrategy in 2011. Today we are one of the

world’s largest aviation consulting organizations. We provide objective,

independent commercial, financial, technical, and regulatory guidance

to aviation clients, including airlines, airports, lessors, financial

institutions, manufacturers, governments, and VIPs. From our offices

around the globe, ICF helps aviation clients manage assets and

operations, mitigate risk, and maximize return on investment.

Visit us online at icf.com/aviation.

ICF Aviation

Comprehensive Services:

Airlines

Fleet and network planning, pricing

and revenue management, OTP and

operational efficiency

Airports

Strategic planning, policy, route

development, concessions planning

Aircraft

Valuations, cash flow forecasts,

portfolio due diligence, market analysis,

technical services

Aerospace & MRO

Operations assessment, M&A support,

marketing analysis, strategy development

3626 June 2018

ICF proprietary and confidential. © ICF 2018ICF proprietary and confidential. © ICF 2018

Aerospace and MRO

ICF guides manufacturers, airlines, independent MROs, suppliers, and

the financial community through every step of the aerospace and MRO

supply chain to realize value and deliver strategies that drive growth.

We understand and focus on the key aspects of the industry, and have

the proprietary tools necessary for successful operations. Below, we

briefly describe our core aerospace & MRO services and proprietary

supporting products.

ICF focuses on

key aspects of the

industry that drive

value in both

revenue growth

and cost control.

Strategy Development

Leveraging years of aerospace and

MRO advisory experience as well as

proprietary market intelligence, ICF

delivers data-driven, objective insight

to underpin sustainable strategies.

Transaction Support

For clients’ investment decisions,

ICF combines global thought

leadership in aerospace and MRO

supply chain with accurate market

intelligence, operations expertise,

and unparalleled industry contacts.

Operations and Supply Chain

ICF’s proven tools and methodologies

offer improved performance and cost

reduction across manufacturing,

operations, and all phases of

make-buy supply chain planning

and execution.

MRO Business Improvement

For airlines, OEMs, and independent

MROs, ICF has deep experience in

comprehensive operational and

financial diagnostics based on

extensive proprietary benchmarks,

followed by results-oriented

improvement programs.

AEROSPACE AND MRO PRODUCTS

ICF’s suite of proprietary aerospace & MRO

tools, models, and databases helps

stakeholders navigate key business

challenges to their advantage.

Fleet &

MRO ForecastsValue

Database

MRO Best Practices

and Benchmarks

Proprietary, independent

forecasts for commercial and

business aviation, industrial

gas turbine, and military

markets.

Production value breakdown

by component category and

raw material content across

the aerospace supply chain.

Comprehensive, proprietary

databases on processes,

costs, and organization.

3726 June 2018