PRESENTATION OF Q3 2015 RESULTS - Grupa...

53

PRESENTATION OF Q3 2015 RESULTS November 9th 2015

Transcript of PRESENTATION OF Q3 2015 RESULTS - Grupa...

PRESENTATION OF Q3 2015 RESULTS

November 9th 2015

Agenda Page

41

2

Overview of Grupa Azoty 3

Market overview 8

Grupa Azoty Group 14

Grupa Azoty PUŁAWY Group 23

Grupa Azoty POLICE Group 31

Grupa Azoty KĘDZIERZYN Group 39

Appendix 1 – Parent 45

OVERVIEW OF GRUPA AZOTY

1,016 1,322 1,899 2,767 517

0% 100%

Grupa Azoty S.A. Grupa Azoty ZAK Group Grupa Azoty POLICE Group Grupa Azoty PUŁAWY Group Other

4

FINANCIAL HIGHLIGHTS

JAN–SEP 2015 CONSOLIDATED REVENUE STRUCTURE

PERFORMANCE DRIVERS

OVERVIEW OF GRUPA AZOTY

↗ Higher production/sales of nitrogen and NPK

fertilizers as a result of effective sales policy

↗ Favourable trends in compound fertilizer prices

↗ Fall in prices of energy carriers

(gas, coal)

↗ Higher realised benzene-polyamide spread

↗ Stronger USD/PLN exchange rate

↗ AZOTY PRO Operational Excellence Programme

REVENUE PLN 7.5bn

REVENUE PLN 2.4bn

EBITDA PLN 1bn

EBITDA PLN 223m

NET PROFIT PLN 540m

NET PROFIT PLN 82m

3Q 2015 Jan–Sep 2015

EPS PLN 4.80

EPS PLN 4.80

NEW FERTILIZER COMPLEX

AT GRUPA AZOTY

PUŁAWY

5TH SCIENCE–BUSINESS–

AGRICULTURE

CONFERENCE

5

KEY DEVELOPMENTS IN Q3 2015

IMPLEMENTATION OF

STRATEGIC INVESTMENT

PROJECTS

10 YEARS OF

POLICE AND PUŁAWY

ON THE WSE

OVERVIEW OF GRUPA AZOTY

PARTNERSHIP WITH AGH

UNIVERSITY OF SCIENCE

AND TECHNOLOGY IN THE

DEVELOPMENT OF CLEAN

COAL-BASED

TECHNOLOGIES

EUROPEAN PARLIAMENT'S

RECOMMENDATIONS ON

THE TRANSATLANTIC

TRADE AND INVESTMENT

PARTNERSHIP (TTIP)

PIPELINE OF STRATEGIC INVESTMENT PROJECTS

CHP Plant

– PLN 600m (2019)

UAN production unit

– PLN 29.5m (2015)

Polyamide plant – PLN 320m (2016)

Mineral fertilizer granulation plant – PLN 140m (2016)

Puławy Power Plant

- PLN 1,125m (2019)

Extension of nitric acid unit

– PLN 695m (2021)

Nitrate mechanical granulation plant

two lines – PLN 385m (line 1 by 2018, line 2 by 2020)

Propylene production plant – PLN 1.7bn (2019)

Upgrade of the ammonia unit

- PLN 156m (by 2016)

Flue gas purification unit

and upgrade of the EC II CHP plant

- PLN 164m (by 2016)

2014–2020 PLN 7bn 68 investment projects

6 OVERVIEW OF GRUPA AZOTY

GRUPA AZOTY POLICE

GRUPA AZOTY KĘDZIERZYN

GRUPA AZOTY PUŁAWY

GRUPA AZOTY S.A.

KEY COMPANY DEVELOPMENTS IN Q3 2015

GRUPA AZOTY POLICE

Compared to Q3 2014:

• EBIT and net profit more than doubled

• net margin and ROCE up by over 100%

• revenue up by 19%

Establishment of PDH Polska S.A. in connection

with a project to construct Europe's largest and

most advanced PDH unit for propylene

production

GRUPA AZOTY S.A.

Launch of the new Mechanical Fertilizer

Granulation Plant project

Setting the groundbreaking plaque for the

New Polyamide 6 Production Plant

Grupa Azoty chosen the Best Investor of 2015

at the Tarnów Investment Forum

7 OVERVIEW OF GRUPA AZOTY

GRUPA AZOTY PUŁAWY

Launch of a unit for producing new solid

fertilizers – PULGRAN/PULGRAN S

Further work on the Puławy Power Plant project

Diversification of natural gas supply sources at

62% in Q3 2015

Publication of a report entitled ‘Poland as an

Attractive Food Producer and Food Supplier’

GRUPA AZOTY KĘDZIERZYN

WIKTORIA Business Quality award received in the

‘Heavy and Chemical Industry’ category

Diamond of the Polish Chemical Industry received

in the ‘Innovation Leader of the Year’ category

Fertilizer granulation technology transferred to

Grupa Azoty PUŁAWY

Oxoviflex® recognised at the 13th International

Oil, Gas and Chemicals Conference

MARKET OVERVIEW

STRONG POSITION IN TARGET MARKETS

90% of revenue derived from sales to EU markets

9

Poland

54%

+2%

Jan–Sep 2014

Jan–Sep 2015

South America

4%

+0.1%

Africa

2%

+0.1%

European Union 1

34%

-1% Asia

5%

-0.1%

Other Europe

1%

-1%

North America

0,3%

+0.1%

1 Excluding Poland

9 GRUPA AZOTY – MARKET OVERVIEW

Q3 2015 EXTERNAL FACTORS

PRICING TRENDS

0

200

400

600

DAP Ammonia Urea ASUSD/t

Q3 2014 Q3 2015

-10% -21%

-17%

-3%

0

500

1 000

1 500

2 000

2 500

CPL PA6 BenzeneEUR/t

Q3 2014 Q3 2015

-14% -17%

-35%

Source: EUROSTAT as at October 29th 2015.

0

500

1 000

1 500

2 000

2 500

3 000

Urea DAP NPK AS AN CAN UAN'000 tonnes

Jan–Aug 2014 Jan–Aug 2015

IMPORTS TO EU (28)

GRUPA AZOTY – MARKET OVERVIEW 10

EXTERNAL FACTORS

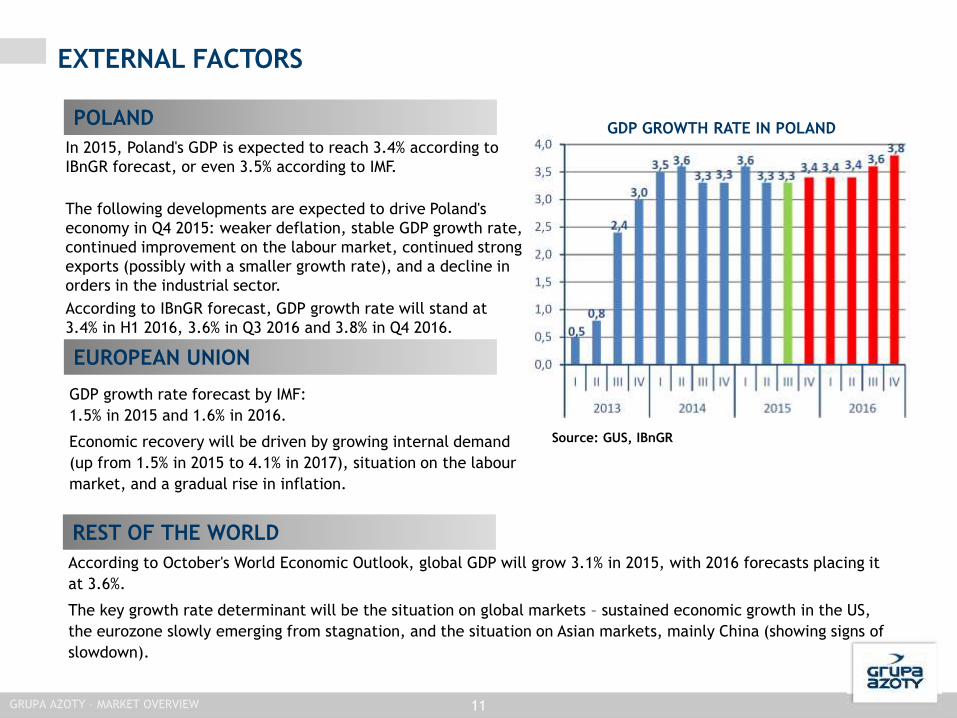

In 2015, Poland's GDP is expected to reach 3.4% according to

IBnGR forecast, or even 3.5% according to IMF.

The following developments are expected to drive Poland's

economy in Q4 2015: weaker deflation, stable GDP growth rate,

continued improvement on the labour market, continued strong

exports (possibly with a smaller growth rate), and a decline in

orders in the industrial sector.

According to IBnGR forecast, GDP growth rate will stand at

3.4% in H1 2016, 3.6% in Q3 2016 and 3.8% in Q4 2016.

According to October's World Economic Outlook, global GDP will grow 3.1% in 2015, with 2016 forecasts placing it

at 3.6%.

The key growth rate determinant will be the situation on global markets – sustained economic growth in the US,

the eurozone slowly emerging from stagnation, and the situation on Asian markets, mainly China (showing signs of

slowdown).

11

GDP GROWTH RATE IN POLAND

GRUPA AZOTY – MARKET OVERVIEW

POLAND

EUROPEAN UNION

GDP growth rate forecast by IMF:

1.5% in 2015 and 1.6% in 2016.

Economic recovery will be driven by growing internal demand

(up from 1.5% in 2015 to 4.1% in 2017), situation on the labour

market, and a gradual rise in inflation.

REST OF THE WORLD

Source: GUS, IBnGR

MARKET OUTLOOK FOR Q4 2015

12

FERTILIZERS

↗ Rise in food prices forecast from December 2015 – 1–2% higher than previous year's

↗ Direct subsidy payments to farmers give hopes of higher fertilizer demand in Q4 2015

↗ Urea prices on a growth trend until December 2015

↘ DAP market prices affected by weak demand ↗ The prices may grow driven by low stocks of DAP in

China

CHEMICALS

↘ Cautious procurement policy of customers purchasing OXO alcohols and plasticizers due to declining

raw material prices and stock optimisation measures

↘ Further decline in prices of alcohols and plasticizers caused by a downward trend in propylene prices

Average melamine price broadly flat on Q3 2015

↘ Usual decrease in titanium white demand and prices in Q4 – price adjustments depending on

macroeconomic conditions and stock reduction by customers

RAW

MATERIALS

↗ Average monthly TTF gas price forecast at around EUR 19/MWh, down year on year (according to

IHS)

↗ Forecast drop in crude oil prices and expected decline or stagnation in petroleum product prices

↘ Ammonia and sulfur prices expected to fall by ca. USD 16/t and USD 5-15/t, respectively

↘ Coal prices expected to grow by USD 2/t, to USD 57/t (according to IHS)

↗ Possible downward trend in prices of raw materials for titanium white production, with a larger

decline expected for titanium slag and smaller for ilmenite

PLASTICS ↘ Prices of plastics under pressure from seasonal stock optimisation in Q4

↗ Demand on target markets expected to grow, particularly in the automotive and textile sectors

GRUPA AZOTY – MARKET OVERVIEW

15

17

19

21

23

25

27

29

31

EUR/MWh

PGNiG tariff Average natural gas price paid by the Group TTF DA*

DIVERSIFICATION OF GAS SOURCES

GAS PRICES (EUR/MWh)

NATURAL GAS DEMAND

(BCM)

2015 Q3 2015

2.1 0.4

FROM OUTSIDE THE SYSTEM

Q3 2014 Q3 2015

60% 47%

13 GRUPA AZOTY – MARKET OVERVIEW

PGNIG'S NEW PRICING POLICY

The PGNiG Tariff sets a maximum gas price

The new discount scheme is linked to quoted

market prices of gas

Increased pricing differentiation, with prices

depending on the volumes and stability of gas

consumption over a gas year, reduces

diversification of gas sources

Source: ICIS.

* Day Ahead prices at Title Transfer Facility, a virtual trading point for natural gas in the Netherlands, no transfer costs.

GRUPA AZOTY

GROUP

GRUPA AZOTY GROUP: KEY FINANCIALS

* Adjusted for impairment loss on the phthalic anhydride unit recognised in 2014.

15 GRUPA AZOTY GROUP

2,269 2,556 2,839 2,281 2,401

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015

REVENUE

7,342

7,521

Jan–Sep 2014 Jan–Sep 2015

128 132

485

293 223

172

5.6% 5.2%

17.1%

12.9%

9.3

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015

EBITDA

EBITDA(adjusted)*

EBITDA MARGIN 695

1,001

Jan–Sep 2014 Jan–Sep 2015

9 21

306

152 82 54

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015

NET PROFIT

NET PROFIT* (adjusted) 250

540

Jan–Sep 2014 Jan–Sep 2015 (PLNm)

GRUPA AZOTY GROUP: EBITDA – KEY DRIVERS

16

695

1,001

342

198 26 3 6 51 89

111

positive effect on EBITDA

negative effect on EBITDA

GRUPA AZOTY GROUP

↘ lower selling prices of key products

↗ higher sales volume

↗ fall in prices of petroleum products and energy carriers

(PLNm)

GRUPA AZOTY GROUP: PERFORMANCE BY SEGMENT

CHANGE IN EBITDA – Q3 2014 VS. Q3 2015

Agro Fertilizers 61%

Plastics 12%

Chemicals 22%

Energy 2% Other

Activities 3%

REVENUE IN Q3 2015

17

SEGMENT (PLNm)

REVENUE EBITDA REVENUE EBITDA

Q3 2014 Q3 2015 Q3 2014 Q3 2015 Jan–Sep

2014

Jan–Sep

2015

Jan–Sep

2014

Jan–Sep

2015

Agro Fertilizers 1,210 1,468 73 169 4,066 4,522 459 725

Plastics 375 292 -6 -7 1,106 967 -17 8

Chemicals 602 534 19 19 1,915 1,744 110 112

Energy 47 49 15 16 142 151 56 58

Other 35 58 27 26 113 137 87 98

GRUPA AZOTY GROUP

-30

20

70

120

170

AgroFertilizers

Plastics Chemicals Energy Other(PLNm)

GRUPA AZOTY GROUP: AGRO FERTILIZERS

VOLUMES

18

GRAIN PRICES

'000 tonnes

Source: Ministry of Agriculture and Rural Development.

NITROGEN PRODUCT PRICES

Source: Profercy, ICIS.

(PLNm) Q3

2014

Q3

2015

Jan–

Sep

2014

Jan–

Sep

2015

CHANGE

Segment revenue,

including: 1,210 1,468 4,066 4,522 11% ↗

Nitrogen fertilizers

and ammonia 782 854 2,716 2,791 3% ↗

Compound

fertilizers 354 487 1,088 1,423 30% ↗

EBITDA 73 169 459 725 57% ↗

EBITDA margin 6% 12% 11% 16% ↗

0

1 000

2 000

3 000

Compound fertilizers Nitrogen fertilizersand ammonia

Jan–Sep 2014 Jan–Sep 2015

GRUPA AZOTY GROUP

200

250

300

100

300

500

700

EUR/t USD/t Ammonia USD/t

Urea USD/t

Ammonium sulfate AS USD/t

Calcium ammonium nitrate CAN EUR/t

0

1

2

3

4

5

6

0

500

1 000

1 500

2 000

2 500

1 kg N/1 kg milling wheat milling wheat (PLN/t)

fodder corn (PLN/t) rapeseed (PLN/t)

PLN/t 1 kgN

/1 kg

0

10

20

30

40

50

60

70

80

90

Polyamide Caprolactam

Jan-Sep 2014 Jan-Sep 2015

GRUPA AZOTY GROUP: PLASTICS

'000 tonnes

19

PRICES OF BENZENE, PHENOL, CPL, PA6

(PLNm) Q3

2014

Q3

2015

Jan–

Sep

2014

Jan–

Sep

2015

CHANGE

Segment revenue,

including: 375 292 1,106 967 -13% ↘

Polyamide 207 187 612 589 -4% ↘

Caprolactam 131 72 399 288 -28% ↘

EBITDA -6 -7 -17 8 147% ↗

EBITDA margin -2% -2% -2% 1% ↗

GRUPA AZOTY GROUP

400

900

1 400

1 900

2 400

EUR/t

Benzene EUR/t Liquid caprolactam EUR/t PA6 EUR/t Phenol EUR/t

VOLUMES

Source: ICIS, TECNON

0

100

200

300

400

Jan-Sep 2014 Jan-Sep 2015

GRUPA AZOTY GROUP: CHEMICALS

20

'000 tonnes

PRICES OF DEHP, 2-EH AND PROPYLENE

Source: ICIS.

(PLNm) Q3

2014

Q3

2015

Jan–

Sep

2014

Jan–

Sep

2015

CHANGE

Segment revenue

including: 602 534 1,915 1,744 -9% ↘

OXO products 179 93 552 352 -36% ↘

Urea (technical grade) 120 128 393 404 3% ↗

Melamine 85 99 274 294 7% ↗

Titanium white 74 55 236 205 -13% ↘

EBITDA 19 19 110 112 2% ↗

EBITDA margin 3% 3% 6% 6% ↗

GRUPA AZOTY GROUP

600

800

1 000

1 200

1 400

1 600

1 800

EUR/t

Propylene EUR/t DEHP EUR/t 2-EH EUR/t

VOLUMES

RATIOS Jan–Sep

2014

Jan–Sep

2015

Profitability ratios

EBIT margin (%) 4.0 8.5

EBITDA margin (%) 9.5 13.3

ROCE (%) 3.8 7.3

ROE (%) 3.9 7.7

Liquidity ratios

Current ratio 1.6 2.0

Debt ratios

Total debt ratio (%) 33.6 33.1

Net debt (PLNm) 455 410

Debt to equity ratio (%) 50.5 49.4

Sep 30

2014

Sep 30

2015 CHANGE

Non-current

assets 6,608 7,020 +6% ↗

Current

assets 3,142 3,434 +9% ↗

incl. cash and

cash equivalents

581 768 +32% ↗

TOTAL ASSETS 9,750 10,454 +7% ↗

GRUPA AZOTY GROUP: STATEMENT OF FINANCIAL POSITION

Sep 30

2014

Sep 30

2015 CHANGE

Equity 6,477 6,998 +8% ↗

Liabilities 3,273 3,455 +6% ↗

incl. borrowings 927 1,083 +17% ↗

other financial

liabilities 108 95 -12% ↘

TOTAL EQUITY AND

LIABILITIES 9,750 10,454 +7% ↗

(PLNm)

(PLNm)

21 GRUPA AZOTY GROUP

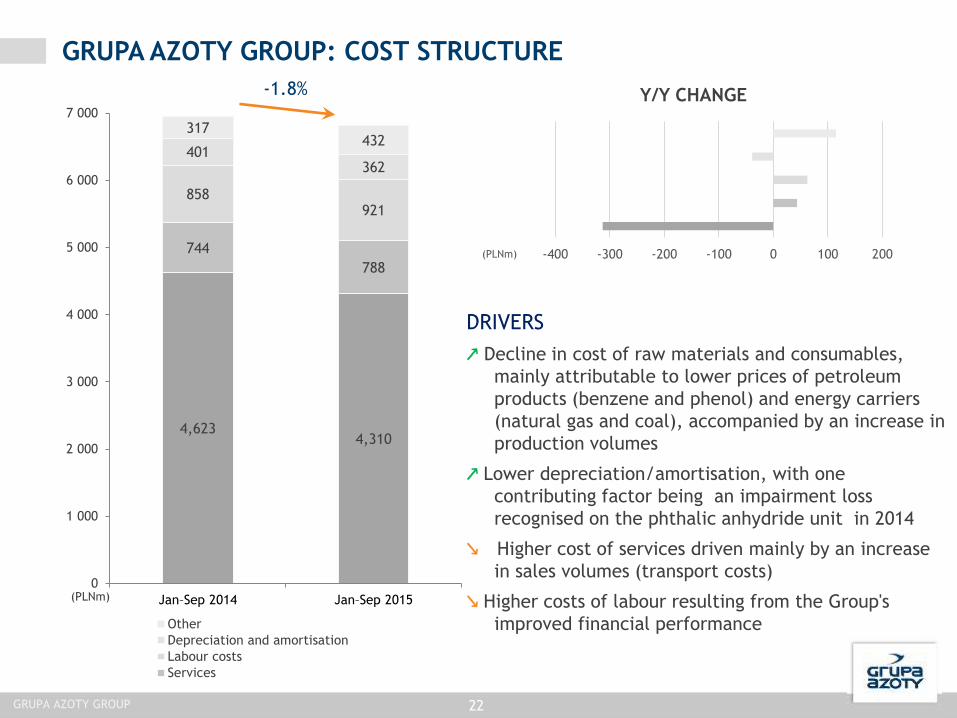

4,623 4,310

744

788

858 921

401 362

317 432

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

Jan–Sep 2014 Jan–Sep 2015

Other

Depreciation and amortisation

Labour costs

Services

GRUPA AZOTY GROUP: COST STRUCTURE

(PLNm)

DRIVERS

↗ Decline in cost of raw materials and consumables,

mainly attributable to lower prices of petroleum

products (benzene and phenol) and energy carriers

(natural gas and coal), accompanied by an increase in

production volumes

↗ Lower depreciation/amortisation, with one

contributing factor being an impairment loss

recognised on the phthalic anhydride unit in 2014

↘ Higher cost of services driven mainly by an increase

in sales volumes (transport costs)

↘ Higher costs of labour resulting from the Group's

improved financial performance

22

-400 -300 -200 -100 0 100 200(PLNm)

Y/Y CHANGE -1.8%

GRUPA AZOTY GROUP

GRUPA AZOTY PUŁAWY GROUP

GRUPA AZOTY PUŁAWY GROUP: KEY FINANCIALS

846 955 1,070 848 935

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015

REVENUE

40 86

227

144 118 4.8%

9.1%

21.3%

17.0%

12.6%

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015

EBITDA

EBITDA MARGIN

3 51

175

95 65

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015

NET PROFIT

PUŁAWY Group

174

334

9M 2014 9M 2015

308

490 11.3%

17.2%

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

0

100

200

300

400

500

600

9M 2014 9M 2015

2,709 2,854

0

500

1 000

1 500

2 000

2 500

3 000

9M 2014 9M 2015

24

(PLNm)

GRUPA AZOTY PUŁAWY GROUP: EBITDA – KEY DRIVERS

↗ increased sales volume

↗ lower prices of key strategic raw materials at the Parent

308 308 464 516 504 492 490 490

156

126 -74 -12 -12 -2

positive effect on EBITDA

negative effect on EBITDA

25

*Only the Parent.

PUŁAWY Group

(PLNm)

GRUPA AZOTY PUŁAWY GROUP: PERFORMANCE BY SEGMENT

Agro 67%

Chemicals 28%

Energy 2%

Other Activities

3%

26 PUŁAWY Group

SEGMENT (PLNm)

REVENUE EBITDA REVENUE EBITDA

Q3 2014 Q3 2015 Q3 2014 Q3 2015 Jan–Sep

2014

Jan–Sep

2015

Jan–Sep

2014

Jan–Sep

2015

Agro 508 629 63 121 1,698 1,871 341 461

Chemicals 308 264 6 17 910 875 41 92

Energy 13 17 6 8 44 51 26 31

Other 16 25 2 8 51 53 3 11

63

6 6 2

121

17 8 8

Agro Chemicals Energy Other

REVENUE IN Q3 2015

(PLNm)

CHANGE IN EBITDA – Q3 2014 VS. Q3 2015

0

400

800

1 200

1 600

Nitrogenfertilizers

Phosphate andcompoundfertilizers

Other Merchandise andmaterials

Jan–Sep 2014 Jan–Sep 2015

GRUPA AZOTY PUŁAWY GROUP: AGRO

Volumes (PLNm) Q3

2014

Q3

2015

Jan–

Sep

2014

Jan–

Sep

2015

CHANGE

Revenue 508 629 1,698 1,871 10.2%

Nitrogen fertilizers 380 464 1,378 1,507 9.4%

Phosphate and

compound

fertilizers

68 91 158 220 39.2%

Other goods and

services 32 18 55 40 -27.3%

Merchandise and

materials 28 56 107 104 -2.8%

EBITDA 63 121 341 461 35.2%

EBITDA margin 12.4% 19.3% 20.1% 24.7% 4.6

27

PRICES OF AN, UAN AND UREA

'000 tonnes

PUŁAWY Group

Source: Argus FMB

200

400

100

200

300

400

USD/t EUR/t

Ammonium nitrate AN EUR/t UAN EUR/t Urea USD/t

VOLUMES

0

50

100

150

200

Melamine Caprolactam Urea(PULREA®,PULNOX®for 100%solution

equivalent)

Other Merchandiseand

materials

Jan–Sep 2014 Jan–Sep 2015

GRUPA AZOTY PUŁAWY GROUP: CHEMICALS

(PLNm) Q3

2014

Q3

2015

Jan–Sep

2014

Jan–Sep

2015 CHANGE

Revenue 308 264 910 875 -3.8%

Melamine 85 99 274 294 7.3%

Caprolactam 131 64 366 279 -23.8%

Urea 62 67 191 208 8.9%

Other goods and

services 28 33 75 88 17.3%

Merchandise and

materials 2 1 4 6 50.0%

EBITDA 6 17 41 92 124.4%

EBITDA margin 1.9% 6.4% 4.5% 10.5% 6.0

28

'000

tonnes

PRICES OF MELAMINE AND CAPROLACTAM

GRUPA AZOTY PUŁAWY

0

1000

2000

3000

0

400

800

1200

1600

USD/t EUR/t

Melamine EUR/t Crystalline caprolactam USD/t

VOLUMES

Source: ICIS.

RATIOS

Jan-

Sep

2014

Jan-

Sep

2015

Profitability ratios

EBIT margin (%) 7.1 12.9

EBITDA margin (%) 11.3 17.2

ROCE (%) 6.6 11.6

ROE (%) 6.5 11.4

Liquidity ratios

Current ratio 2.4 2.6

Debt ratios

Total debt ratio (%) 22.5 21.8

Net debt (PLNm) -250 -281

Debt to equity ratio (%) 29.0 27.9

GRUPA AZOTY PUŁAWY GROUP: STATEMENT OF FINANCIAL POSITION

(PLNm) Sep 30

2014

Sep 30

2015 CHANGE

Equity 2,680 2,927 9.2%

Liabilities 778 817 5.0%

incl. borrowings

11 24 118.2%

other financial

liabilities 767 793 3.4%

TOTAL EQUITY AND

LIABILITIES 3,457 3,744 8.3%

29

(PLNm) Sep 30

2014

Sep 30

2015 CHANGE

Non-current

assets 2,106 2,204 4.7 %

Current

assets 1,351 1,540 14.0%

incl. cash and

cash equivalents

261 306 17.2%

TOTAL ASSETS 3,457 3,744 8.3 %

GRUPA AZOTY PUŁAWY

1,621 1,561

283 277

274 294

115 122

192 209

0

500

1 000

1 500

2 000

2 500

Jan–Sep 2014 Jan–Sep 2015

Other

Depreciation and amortisation

Employee benefits expense

Services

Raw materials and consumables used

GRUPA AZOTY PUŁAWY GROUP: COST STRUCTURE

PLNm

DRIVERS

In January-September 2015, total costs fell slightly

year on year, by approximately 1.0% (or PLN 24m).

The main changes included:

lower cost of gas consumption (down by ca. PLN

48m)

lower cost of other raw material and

consumables used (down by ca. PLN 12m)

higher cost of labour (up by ca. PLN 20m)

higher cost of advertising and entertainment

(up by ca. PLN 15m)

-1%

30 Grupa Azoty PUŁAWY

-80 -60 -40 -20 0 20 40(PLNm)

Y/Y CHANGE

GRUPA AZOTY POLICE GROUP

6 7

51 56

15

1.2% 1.0%

6.8% 8.0%

2.5%

0

10

20

30

40

50

60

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015

NET PROFIT

NET MARGIN

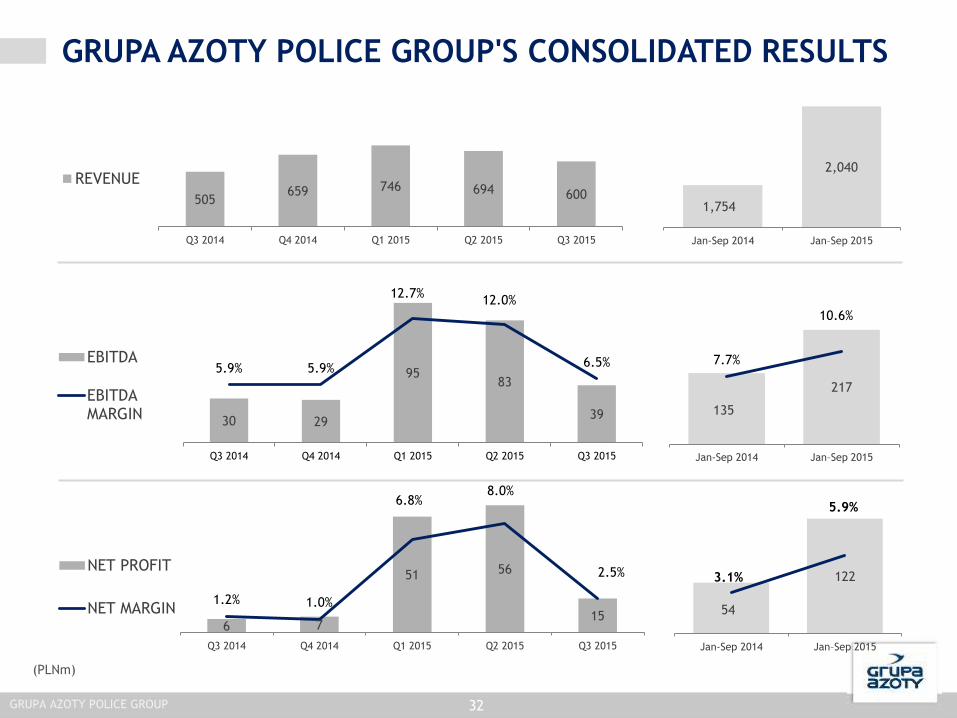

GRUPA AZOTY POLICE GROUP'S CONSOLIDATED RESULTS

(PLNm)

505 659 746 694 600

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015

REVENUE

30 29

95 83

39

5.9% 5.9%

12.7% 12.0%

6.5%

0102030405060708090

100

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015

EBITDA

EBITDAMARGIN

1,754

2,040

Jan-Sep 2014 Jan–Sep 2015

135

217

7.7%

10.6%

0

50

100

150

200

250

Jan-Sep 2014 Jan–Sep 2015

54

122 3.1%

5.9%

0

20

40

60

80

100

120

140

Jan-Sep 2014 Jan–Sep 2015

GRUPA AZOTY POLICE GROUP 32

GRUPA AZOTY POLICE GROUP: EBITDA – KEY DRIVERS

↗ Higher volume of sales and more favourable prices of compound fertilizers

↗ Increased production of compound fertilizers

135

217

166

101 99 20

37

28

EBITDA Jan–Sep 2014

Sales volumes Product prices Raw materialvolumes

Selling anddistribution

expenses, fixedcosts

Raw materialprices

other EBITDA Jan–Sep 2015

positive effect on EBITDA

negative effect on EBITDA

33 GRUPA AZOTY POLICE GROUP

(PLNm)

GRUPA AZOTY POLICE: PERFORMANCE BY SEGMENT

EBITDA

34

Fertilizers 88%

Pigments 9%

Other 3%

SEGMENT (PLNm)

REVENUE EBITDA REVENUE EBITDA

Q3 2014 Q3 2015 Q3 2014 Q3 2015 Jan–Sep

2014

Jan–Sep

2015

Jan–Sep

2014

Jan–Sep

2015

Fertilizers 416 528 18 37.2 1,481 1,789 95 206

Pigments 77 57 7 0.4 243 213 28 5

Other 12 15 5 1.4 30 38 12 6

GRUPA AZOTY POLICE GROUP

18

7 5

37

0.4 1.4

Fertilizers Pigments Other

REVENUE IN Q3 2015 CHANGE IN EBITDA – Q3 2014 VS. Q3 2015

(PLNm)

0

300

600

900

Compound fertilizers Urea Ammonia Other

Jan–Sep 2014 Jan–Sep 2015

GRUPA AZOTY POLICE: FERTILIZERS

(PLNm) Q3

2014

Q3

2015

Jan–

Sep

2014

Jan–

Sep

2015

CHANGE

Revenue 416 528 1,481 1,789 21%

Compound

fertilizers 297 414 957 1,251 31%

Urea 71 60 292 270 -8%

Ammonia 37 35 205 216 5%

Other 11 19 26 52 101%

EBITDA 18 37 95 206 117%

EBITDA margin 4% 7% 6% 12% 6% '000

tonnes

50

100

150

200

250

300

350

400

450

200

300

400

500

600

700

USD/t USD/t

NPK DAP Phosphate rock Potassium chloride

Source: WFM, FERTECON, Profercy.

PRICES OF NPK, DAP, PHOSPHATES, POTASSIUM CHLORIDE

GRUPA AZOTY POLICE GROUP

VOLUMES

35

0

10

20

30

Titanium white Other

Jan–Sep 2014 Jan–Sep 2015

GRUPA AZOTY POLICE: PIGMENTS

Volumes

(PLNm)

Q3

2014

Q3

2015

Jan–

Sep

2014

Jan–

Sep

2015

CHANGE

Revenue 77 57 243 213 -12%

Titanium white 74 55 235 204 -13%

Other 3 2 8 9 13%

EBITDA 7 0.4 28 5 -82%

EBITDA margin 9% 1% 12% 2% -10%

36

'000

tonnes

0

500

1000

1500

2000

0

1000

2000

3000

USD/t EUR/t

Titanium white Ilmenite Titanium slag

Source: ICIS, CCM

PRICES OF TITANIUM WHITE, ILMENITE AND TITANIUM SLAG

GRUPA AZOTY POLICE GROUP

RATIOS Jan–Sep

2014

Jan–Sep

2015

Profitability ratios

EBIT margin 4% 8%

EBITDA margin 8% 11%

Return on capital employed 5% 10%

ROE 5% 10%

Liquidity ratios

Current ratio 1.3 1.3

Debt ratios

Total debt ratio 44% 42%

Net debt (PLNm) 189 241

Equity-to-debt ratio 128% 137%

(PLNm) Sep 30

2014

Sep 30

2015 CHANGE

Non-current

assets 1,313 1,459 11% ↗

Current

assets 641 595 -7% ↘

incl. cash and

cash equivalents

45 52 15% ↗

TOTAL ASSETS 1,955 2,053 5% ↗

GRUPA AZOTY POLICE: STATEMENT OF FINANCIAL POSITION

(PLNm) Sep 30

2014

Sep 30

2015 CHANGE

Equity 1,098 1,186 8% ↗

Liabilities 856 867 1% ↗

incl. borrowings

225 285 27% ↗

other financial

liabilities 9 8 -14% ↘

TOTAL EQUITY

AND

LIABILITIES

1,955 2,053 5% ↗

37 GRUPA AZOTY POLICE GROUP

1,143

1,297

116

130 207

229 68

63

96

114

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

Jan–Sep 2014 Jan–Sep 2015

Other Depreciation and amortisation

Labour costs Services

Raw materials and consumables used

GRUPA AZOTY POLICE: COST STRUCTURE

(PLNm)

12.4%

38

DRIVERS

↘ Increased production of compound fertilizers

↗ Lower gas consumption costs following price

reduction

↘ Higher cost of services due to increased sales to

own unit responsible for transport operations

-10 30 70 110 150(PLNm)

Y/Y CHANGE

GRUPA AZOTY POLICE GROUP

GRUPA AZOTY

ZAKŁADY AZOTOWE KĘDZIERZYN S.A.

39

491 522 543 397 435

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015

REVENUE

GRUPA AZOTY KĘDZIERZYN: KEY FINANCIALS

31 20

93

27 35

60

6.3

11.5

17.2

6.8 8.1

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

16,0

18,0

20,0

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015

EBITDA

AdjustedEBITDA*

EBITDA MARGIN

9

0

60 12 14 33

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015

NET PROFIT

Adjusted NET PROFIT*

* One-off item: impairment loss on phthalic anhydride unit of PLN 40m

40 GRUPA AZOTY KĘDZIERZYN

1,534 1,375

Jan–Sep 2014 Jan–Sep 2015

78 87

Jan–Sep 2014 Jan–Sep 2015

155 156

Jan–Sep 2014 Jan–Sep 2015

(PLNm)

RATIOS

Jan–

Sep

2014

Jan–

Sep

2015

Profitability ratios

EBIT margin (%) 5.9% 7.2%

EBITDA margin (%) 10.1% 11.3%

ROCE (%) 7.5% 7.5%

ROE (%) 7.4% 8.0%

Liquidity ratios

Current ratio 1.47 1.43

Debt ratios

Total debt ratio 31.5% 34.5%

Net debt (PLNm) -45 -33

Debt to equity ratio (%) 46.1% 52.7%

(PLNm) Sep 30

2014

Sep 30

2015 CHANGE

Non-current

assets 1,027 1,168 141 ↗

Current

assets 523 492 -31 ↘

incl. cash and

cash equivalents

99 145 46 ↘

TOTAL ASSETS 1,550 1,660 110 ↘

GRUPA AZOTY KĘDZIERZYN: STATEMENT OF FINANCIAL POSITION

(PLNm) Sep 30

2014

Sep 30

2015 CHANGE

Equity 1,061 1,087 26 ↗

Liabilities 489 573 84 ↘

incl. borrowings 50 108 58 ↘

other financial

liabilities 4 4 -0.3 ↘

TOTAL EQUITY AND

LIABILITIES 1,550 1,660 110 ↘

41 GRUPA AZOTY KĘDZIERZYN

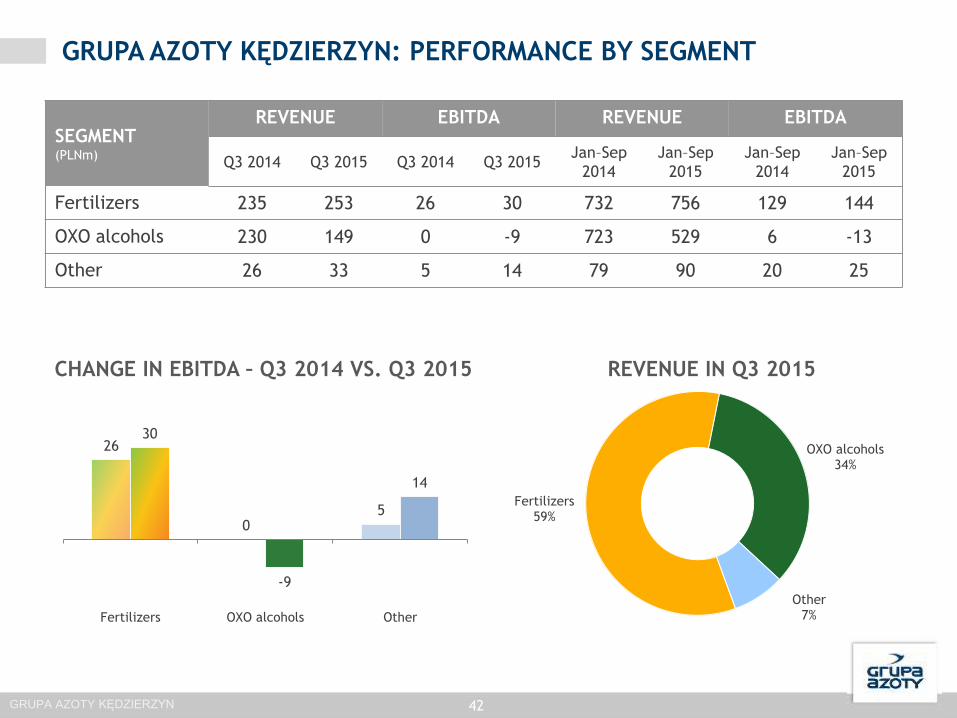

GRUPA AZOTY KĘDZIERZYN: PERFORMANCE BY SEGMENT

Fertilizers 59%

OXO alcohols 34%

Other 7%

42

SEGMENT (PLNm)

REVENUE EBITDA REVENUE EBITDA

Q3 2014 Q3 2015 Q3 2014 Q3 2015 Jan–Sep

2014

Jan–Sep

2015

Jan–Sep

2014

Jan–Sep

2015

Fertilizers 235 253 26 30 732 756 129 144

OXO alcohols 230 149 0 -9 723 529 6 -13

Other 26 33 5 14 79 90 20 25

GRUPA AZOTY KĘDZIERZYN

26

0 5

30

-9

14

Fertilizers OXO alcohols Other

REVENUE IN Q3 2015 CHANGE IN EBITDA – Q3 2014 VS. Q3 2015

DISCLAIMER

The information presented below has been prepared by the Grupa Azoty Group (the “Group”) solely for the purpose of presentation to investors and market analysts on

November 9th 2015 (the “Presentation”). By participating in the meeting at which the Presentation is presented or by referring to the following Presentation, you agree to

the following specific restrictions and disclaimers.

This presentation does not constitute or form any part of, and should not be considered as, an offer to sell or as an offer to subscribe for, or as a guarantee to purchase or

acquire in other way, any securities of any company of the Group. Neither this Presentation nor any part hereof may form the basis of, or be relied upon in connection with,

any subscription for any securities of the Group, or their acquisition. Neither this Presentation nor any part hereof may form the basis of, or be relied upon in connection

with, any investment agreement, commitment or decision relating to securities of the Group companies. This Presentation does not constitute a recommendation regarding

any securities of the Group companies.

No statement or assurance, expressed or implied, has been made by or on behalf of the Group or any of its shareholders, members of its bodies, officers, employees, agents

or advisers or any other person, as to the accuracy, completeness or reliability of information or opinions contained in this Presentation.

This Presentation may contain forward-looking statements. Forward-looking statements are different from statements of historical facts. Statements containing such words as

"expects", "intends", "plans", "believes", "anticipates", "will", "aims", "can", "would", "could", "continues" or similar words are examples of such forward-looking statements.

Forward-looking statements include statements about the financial performance, business strategy, plans and objectives of the Group (including development plans relating

to the Group). All forward-looking statements contained in this Presentation relate to matters involving known and unknown risks, issues that are impossible to predict, and

other factors. Actual results and achievements of the Group may be materially different from those described in statements concerning the past, and from the results and

achievements of the Group in the past. Forward-looking statements are made based on various assumptions of future events, including numerous assumptions regarding

present and future business strategies of the Group and its future business environment. Although the Group believes that its estimates and assumptions are reasonable, they

may prove to be incorrect. The information, opinions and forward-looking statements contained herein are valid only on the date of this Presentation and are subject to

change without notice. The Group and its advisers are not obliged to publish any updates or modify any information, data or statements contained in this Presentation in the

event of a change of strategy or the intentions of the Group, or of facts or circumstances that will have an impact on the strategy or intentions of the Group, unless such an

obligation arises under law. Please note that the only reliable source of data on the Group's financial results, forecasts, events and indicators of the Group are the current

and periodic reports released by the Group as part of its disclosure obligations under Polish law.

Neither the Group nor any of its shareholders, members of its bodies, officers, employees, agents or advisers nor any other person shall be liable for any loss arising from the

use of this Presentation or its contents or otherwise arising in connection with this Presentation.

Neither the Group nor any of its shareholders, members of its bodies, officers, employees, agents or advisers nor any other person shall be required to provide the recipients

of this Presentation with any additional information or to update this Presentation.

This Presentation contains information on the chemical industry in Poland and globally, including information on market shares of the Company and some of its competitors.

The source of this information is always provided in this Presentation and the Group or any other entity acting on behalf of the Group has independently verified the

information referred to above.

This Presentation is not intended for distribution to or use by any person or any entity in any jurisdiction where such distribution or use would be contrary to local law or

oblige the Group or any of its affiliates to obtain an authorization or licence, or to comply with the registration requirements under applicable laws. Neither this Presentation

nor any part hereof may be copied or transmitted into the United States of America, and cannot be disseminated, directly or indirectly, in the United States of America.

Failure to comply with this restriction may constitute a violation of U.S. securities laws. Persons who come into possession of this Presentation are required to inform

themselves of, and to observe all of the above restrictions. None of the securities referred to herein have been or will be registered under the U.S. Securities Act of 1933.

Any such securities may not be offered or sold in the United States of America, except pursuant to an exemption or in a transaction not required to be registered under the

Act.

43

Thank you for your attention. For more information, visit www.grupaazoty.com.

APPENDIX 1

PARENT

-200

-100

0

100

200

300

400

500

600

700

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

EBITDA AND NET DEBT

Net debt EBITDA

KEY RATIOS SINCE IPO 2008, QUARTERLY*

*Grupa Azoty Group

-100

0

100

200

300

400

500

-500

0

500

1 000

1 500

2 000

2 500

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

REVENUE AND NET PROFIT

Revenue Net profit (right axis)(PLNm)

(PLNm)

46 GRUPA AZOTY S.A.

GRUPA AZOTY S.A.: KEY FINANCIALS

464 470 500 371 468

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015

REVENUE

9 5

53

17 21 2% 1%

11%

5% 5%

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015

EBITDA

EBITDA MARGIN

-18 -23

18

218

-6 -12

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015

NET PROFIT/LOSS

NET PROFIT/LOSS (adjusted)

NET PROFIT was adjusted for dividend received (in all periods)

47

1,377

1,339

Jan–Sep 2014 Jan–Sep 2015

238 230

-32 -1

Jan–Sep 2014 Jan–Sep 2015

58

92

Jan–Sep 2014 Jan–Sep 2015

GRUPA AZOTY S.A.

(PLNm)

GRUPA AZOTY S.A.: RESULTS BY SEGMENT

Fertilizers 50%

Plastics 47%

Energy 1%

Other Activities

2%

48

SEGMENT (PLNm)

REVENUE EBITDA REVENUE EBITDA

Q3 2014 Q3 2015 Q3 2014 Q3 2015 Jan–Sep

2014

Jan–Sep

2015

Jan–Sep

2014

Jan–Sep

2015

Fertilizers 195 236 -5 7 586 608 11 43

Plastics 258 219 9 10 753 690 29 33

Energy 7 5 3 2 18 16 10 9

Other 5 8 2 2 21 25 8 7

GRUPA AZOTY S.A.

-5

9

3 2

7

10

2 2

Fertilizers Plastics Energy Other

(PLNm)

REVENUE IN Q3 2015 CHANGE IN EBITDA – Q3 2014 VS. Q3 2015

GRUPA AZOTY S.A.: FERTILIZERS

PRICES OF AMMONIA, AMMONIUM SULFATE AND CALCIUM AMMONIUM NITRATE

VOLUMES

49

Source: Argus FMB, ICIS

(PLNm) 32Q

2014

32Q

2015

Jan–

Sep

2014

Jan–

Sep

2015

CHANGE

Segment revenue

including 195 236 586 608 4%

Nitrogen fertilizers 178 218 517 546 6%

EBITDA -5 7 11 43 291%

EBITDA margin -3% 3% 2% 7% 0

100

200

300

400

500

600

700

Nitrogen fertilizers

Jan–Sep 2014 Jan–Sep 2015

'000

tonnes

GRUPA AZOTY S.A.

200

220

240

260

280

100

200

300

400

500

600

700

EUR/t USD/t

Ammonia USD/t Ammonium sulfate AS USD/t Calcium ammonium nitrate CAN EUR/t

GRUPA AZOTY S.A.: PLASTICS

VOLUMES

50

PRICES OF BENZENE, PHENOL, CPL, PA6

(PLNm) Q3

2014

Q3

2015

Jan–

Sep

2014

Jan–

Sep

2015

CHANGE

Segment revenue

including 258 219 753 690 -8% ↘

Polyamide 183 159 506 498 -2% ↘

Caprolactam 19 13 89 41 -54% ↘

EBITDA 9 10 29 33 14% ↗

EBITDA margin 3% 5% 4% 5% ↗

GRUPA AZOTY S.A.

400

900

1 400

1 900

2 400

EUR/t

Benzene EUR/t Liquid caprolactam EUR/t PA6 EUR/t Phenol EUR/t

0

20

40

60

80

Polyamide Caprolactam

Jan–Sep 2014 Jan–Sep 2015

Source: ICIS, TECNON

GRUPA AZOTY S.A.: COST STRUCTURE

(PLNm)

51

901

789

203

220

127

141

68

68

44

58

0

200

400

600

800

1 000

1 200

1 400

Jan–Sep 2014 Jan–Sep 2015 Other

Depreciation and amortisation

Labour costs

Services

Raw materials and consumables used

-150 -100 -50 0 50(PLNm)

Y/Y CHANGE

DRIVERS

↘ Decline in cost of raw materials and

consumables attributable to lower prices of

petroleum products (benzene down 37%

and phenol down 30%) and energy carriers

(natural gas down 6% and coal down 12%)

↗ Higher cost of services driven by a change in

terms of sale (transport costs)

↗ Increase in the 'Other' line item following

reclassification of the cost of rights to CO2

emissions (last year disclosed under 'Raw

materials and consumables used')

-5%

GRUPA AZOTY S.A.

STOCK PRICE – NEW HIGH

0,00

10,00

20,00

30,00

40,00

50,00

60,00

70,00

80,00

90,00

100,00

0

500

1 000

1 500

2 000

2 500

3 000

Jun 08 Dec 08 Jun 09 Dec 09 May 10 Nov 10 May 11 Oct 11 Apr 12 Oct 12 Apr 13 Oct 13 Apr 14 Sep 14 Mar 15 Sep 15

Trading volume Price

Growth from Jun 30 2008:

Growth from Jan 1 2015:

High (Aug 11 2015)

Low (Feb 3 2009)

475 %

45%

PLN 96.90

PLN 6.00

52 GRUPA AZOTY S.A.