Micro finance and enterprenurship

40

Submitted By: Akshay Gattani, Aarzoo Khandelwal, Aastha Mathur

-

Upload

ak-maheshwari -

Category

Small Business & Entrepreneurship

-

view

81 -

download

3

Transcript of Micro finance and enterprenurship

Submitted By:Akshay Gattani, Aarzoo Khandelwal,Aastha Mathur

Resources:

Wikipedia

And some other websites

What is Microfinance?

Poor people are not able to access loans from commercial banksnormally because of lack in guarantee and collateral. But there are manyother reasons also involved for which commercial banks were not willingto finance poor

“Microfinance has evolved as an economic developmentapproach intended to benefit low-income Population. The termrefers to the provision of financial services to low –income clients,including the self employed.”

“Microfinance is the provision of a broad range offinancial services such as deposits, loans, payment services,money transfers, and insurance to poor and low-incomehouseholds and, their microenterprises.”

Microfinance Activities

Economic activities base upon sellers and buyer and theircapacity. Sellers, before market their product, look at buyer intentionand capacity. On the other hand, banking activities depend on bothsellers and buyers.

Microfinance usually don’t invest in consumer finance, butgive finance only for micro enterprise. MFIs encourage people to liftup their standards by doing businesses and earning from them andthis is a consistent and sustainable way.

Microfinance is dedicated only to poor and explicitly forbusiness activities. But with this, there are some indirect impacts ofmicrofinance on the micro borrower which are alleviation of poverty,improvement in healthcare, increase in literacy and other socialimpacts.

Microfinance standards and principles

Poor people borrow from informal moneylenders andsave with informal collectors. They receive loans and grantsfrom charities. They buy insurance from state-ownedcompanies. They receive funds transfers through formal orinformal remittance networks. It is not easy to distinguishmicrofinance from similar activities.

Ensuring financial services to poor people is bestdone by expanding the number of financial institutionsavailable to them, as well as by strengthening the capacity ofthose institutions. In recent years there has also beenincreasing emphasis on expanding the diversity ofinstitutions, since different institutions serve differentneeds.

Some of the principles are : Poor people need not just loans but also savings, Insurance and money transfer

services. Microfinance must be useful to poor households: helping them raise income, build

up assets and/or cushion themselves against external shocks. "Microfinance can pay for itself . Subsidies from donors and government are scarce

and uncertain and so, to reach large numbers of poor people, microfinance mustpay for itself.

Microfinance means building permanent local institutions. Microfinance also means integrating the financial needs of poor people into a

country's mainstream financial system. "The job of government is to enable financial services, not to provide them. "Donor funds should complement private capital, not compete with it. "The key bottleneck is the shortage of strong institutions and managers. Donors

should focus on capacity building. Interest rate ceilings hurt poor people by preventing microfinance institutions from

covering their costs, which chokes off the supply of credit. Microfinance institutions should measure and disclose their performance—both

financially and socially.

Economic activity by commercial banking

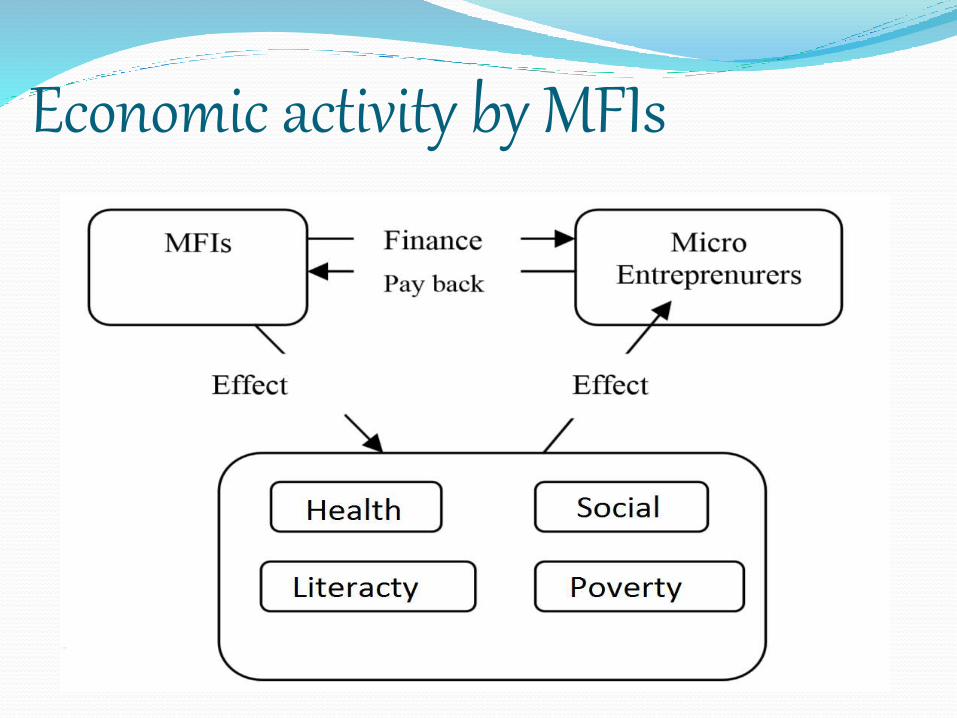

Economic activity by MFIs

Activities and characteristics are included in microfinance Some are:

• Small and short term loans • Social collateral rather than financial collateral • Access to larger amount of loan if repayment performance is positive • Search and access the real poor and their business demand • Continuous monitoring of business • Loan on higher interest rates due expensive financial transactions and risk factor

To be Continued…• Easy way to access finance, therefore not too muchpaper work, and easy and short procedures• Offering saving services to borrowers even forsmallest amount• Offer training services to borrower’s businessdevelopment• Literacy training to borrowers so that they cancome up with competence to daily businessproblems and its solutions• Health care, social services and other skill trainingservices to provide borrower a sustainable base fortheir business development

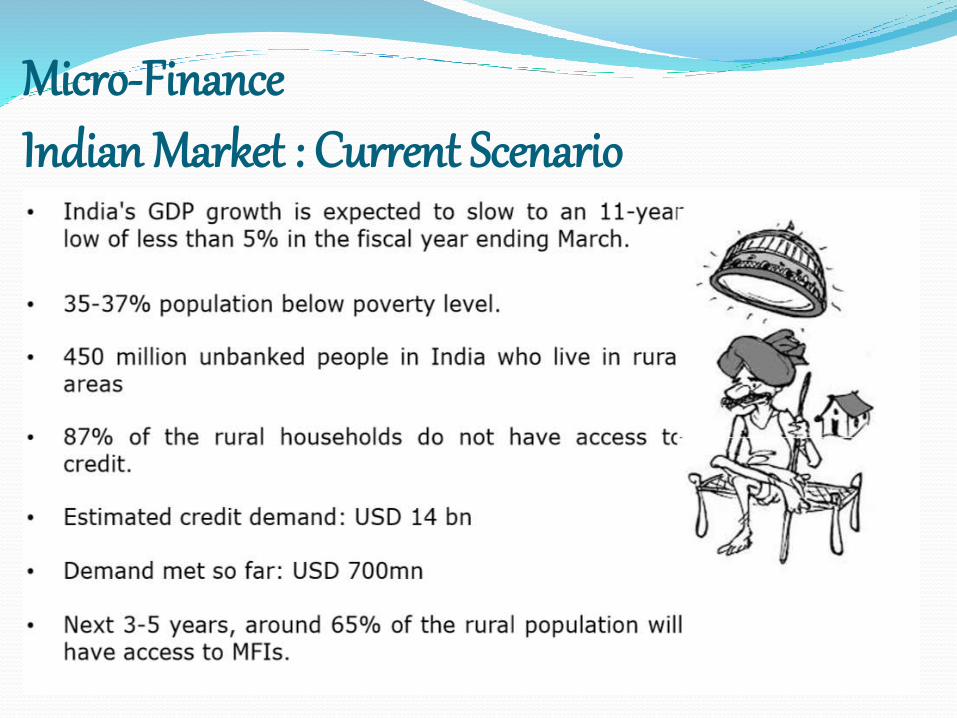

Micro-FinanceIndian Market : Current Scenario

Current Micro-Finance industry

Current Scenario Microfinance Industry

Micro finance models

SWOT Analysis -Strength

SWOT Analysis: Weaknesses

Opportunities

Threats

ENTERPRENEURSHIP

What is Entrepreneurship?

The Capacity and willingness to develop,

organize and manage a business venture along

with any of its risks in order to make a profit.

The most obvious example of

entrepreneurship combined with land, labor,

natural, resources and capital can produce

profit.

Characteristics of entrepreneur Desire for responsibility

Preference for moderate risk (risk eliminators)

Confidence in their ability to succeed

Desire for immediate feedback

High level of energy

Future orientation (serial entrepreneurs)

Skill in organization

Value of achievement over money

High degree of commitment

Willingness to accept risk, work hard and take action

Flexibility

Growth of entrepreneurship Young Entrepreneurs

Women Entrepreneurs

Minority Enterprises

Immigrant Entrepreneurs

Part-time Entrepreneurs

Home-Based Businesses

Family Businesses

Copreneurs

Corporate Castoffs

Corporate Dropouts