EvaluateMedTech_World_Preview_2013

22

World Preview 2013, Outlook to 2018 The Future of Medtech

-

Upload

spenceblack7999 -

Category

Documents

-

view

33 -

download

0

description

Medtech marketr report

Transcript of EvaluateMedTech_World_Preview_2013

World Preview 2013, Outlook to 2018

The Future of Medtech

Welcome to the EvaluateMedTech™ World Preview 2013, Outlook to 2018

Launched in October 2012, the EvaluateMedTech™ service is focused on the medical device and diagnostic industry. Powered by Evaluate’s proven platform and high quality market intelligence, it allows life science and healthcare companies, investment banks, management consultancies, service providers and others to easily track and benchmark the sector and perform rapid analysis.

Our second annual EvaluateMedTech™ World Preview brings together many of our analyses to provide a top level insight into the expected performance of the medtech industry between now and 2018. Based on EvaluateMedTech™’s coverage of the world’s leading medical device and diagnostic companies, the World Preview highlights trends in medtech including consensus sales forecasts of leading industry analysts by device area to 2018, the top 20 companies in 2018, R&D spend current and future, FDA approvals, M&A and venture financing and enterprise value & focus analysis.

About Evaluate Ltd.

Evaluate is the trusted source for high quality commercial market intelligence and exclusive consensus sales forecasts to 2018. Our services are EvaluatePharma®, EvaluateMedTech™ and EvaluateClinicalTrials™. Our award-winning editorial arm, EP Vantage, leverages our market intelligence and analysis to cut through the noise, providing daily opinion and insights. Evaluate’s services give you the insights you need to ask the right questions and get the right answers. That’s intelligence you can act on. For more information visit: www.evaluategroup.com. On Twitter: @evaluatepharma, @evaluatemedtech, @epclinicaltrial, @epvantage

� North America: Debbie Paul Tel: 1-617-573-9453 Email: [email protected]

� Rest of the World: Will Hau Tel: +44 (0)20 7377 0800 Email: [email protected]

� Asia Pacific: Hiroshi Yamazaki Tel: +81 (0)80 1164 4754 Email: [email protected]

� General inquiries about this report: Christine Lindgren Tel: 1-617-573-9458 Email: [email protected]

Disclaimer

All intellectual property rights in this report remain that of Evaluate Ltd and/or its respective third party licensors. Whilst all reasonable steps have been taken to ensure that the data presented are accurate, Evaluate Ltd cannot accept responsibility for errors or omissions. Neither does Evaluate Ltd warrant the accuracy, merchantability or fitness for a particular purpose of the data. Nothing in the reports shall constitute investment, financial or legal advice and the contents of the reports are provided for information purposes only. The data is not intended to amount to advice and should not be used as a determining factor in any investment decision. This report may not be lent, resold, hired out or otherwise disposed of by way of trade in any form of binding or cover other than that in which it is published, without the prior written consent of Evaluate Ltd. Copyright © 2013 Evaluate Ltd. All rights reserved.

September 2013

2Co

pyr

igh

t ©

201

3 Ev

alu

ate

Ltd

. All

rig

hts

res

erve

d.

n the second edition of the EvaluateMedTech™ World Preview we can reveal the medtech market is expected to grow at 4.5% per year (CAGR) between 2012 and 2018, achieving global sales of $455bn in 2018 (page 6). The analysis is based on in-depth forecast models for the top 180 global medtech companies available within EvaluateMedTech™. This sales forecast represents the only current consensus view from equity analysts of the medtech market.

Moving towards specialisation

Though the single biggest medtech company, Johnson & Johnson, is a conglomerate, the prevalent trend in the medtech industry is towards increased company specialisation. Following Abbott’s highly successful split into two separate companies, one medtech, one pharma, and Covidien shedding its pharma operations, we could see a trend in others following suit in order to become smaller and nimbler. Indeed, J&J itself is considering selling its slow-growing diagnostics business; it would not be surprising if broad-based companies such as Siemens or 3M were to separate into more specialised concerns.

Regulatory standards tightening

Both the US and European medtech markets are seeing tightening of the rules governing the approval of medical devices. The proposed changes to the CE marking process currently moving through the European Parliament could see device-makers having to meet higher standards to get their products on sale. In the US, the FDA is considering bringing laboratory-developed tests, currently sold without requiring direct regulatory oversight, under its control – and the agency’s requirements have been getting stricter overall as well. The FDA has approved just 14 new PMAs so far this year – a 42% decline compared with the same point last year (page 12).

VC squeeze

Both changes could potentially lengthen the approval process, and consequently could scare investors away. The medtech industry used to offer venture capitalists a relatively quick return on their investment; VCs will be less keen to stump up cash if they know they have longer to wait for their payday. The 14% drop in the total venture funding in 2012 compared with 2011 suggests this may already be happening (page 19).

Growth and maturing

In vitro diagnostics is not only the largest segment within medtech, with predicted worldwide sales of $58.8bn in 2018, it is also one of the fastest growing, at a rate of 5.1% (page 13). The huge potential of companion diagnostics is one of the drivers here, and the advent of advanced molecular diagnostics is also contributing. If the proposed changes at the FDA take effect they could also spur growth in this market by forcing the withdrawal of many competing laboratory-developed tests from sale.

Elsewhere, though, markets are maturing from a period of fast expansion to one of slower growth. The cardiology, imaging and orthopedic sectors are all growing more slowly than the industry average, and higher regulatory bars and decreased investment could militate against the advent of transformative new technologies.

Ian Strickland Product Manager, EvaluateMedTech™

I

3

EvaluateMedTech™ Foreword

Co

pyr

igh

t ©

201

3 Ev

alu

ate

Ltd

. All

rig

hts

res

erve

d.

EvaluateMedTech™ World Preview 2013, Outlook to 2018 – Analysis Highlights

� Worldwide medtech sales forecast to grow by 4.5% (CAGR 2012 to 2018), reaching $455bn by 2018

� Medtech set to outperform the prescription drug market with a CAGR of 4.5% vs. 3.8% between 2012 and 2018 – but pharma forecast to catch up, with both industries estimated to grow by approximately 5% per year from 2015 to 2018

� Johnson & Johnson forecast to be the clear market leader in 2018 with medtech sales of $33.4bn

� In vitro diagnostics expected to be the world’s largest medtech segment in 2018, with sales of $58.8bn

� Global medtech R&D spend set to grow by 3.9% (CAGR) to $26.7bn in 2018

� Siemens predicted to be the top medtech R&D spender in 2018, with investment in new programmes forecast to reach $2bn, but Abbott’s spending is increasing fast following the AbbVie split

� Number of 1st time PMAs decreases 5% to 41 in 2012; 510(k) clearances up 1% to 3,185

� FDA approves 14 new PMAs in 2013 to end of August, representing a 42% decline compared with the same point last year

� Roche maintains leading position within in vitro diagnostics with sales of $11.3bn in 2018, and market share of 19.3%

� Medtronic maintains top spot in cardiology to 2018 with sales of $9.9bn and a 20% market share

� Johnson & Johnson set to dominate the slow-growing orthopedics market with 2018 market share of 26.6% and sales of $10.6bn

� M&A deal value falls by a startling 79% in H1 2013 vs. H1 2012 and deal count drops 15%

� Total deal value of medtech venture financing falls 14% to $3.8bn in 2012 vs. 2011 but expands 6% to $2.5bn in H1 2013 vs. H1 2012

4Co

pyr

igh

t ©

201

3 Ev

alu

ate

Ltd

. All

rig

hts

res

erve

d.

Johnson & Johnson forecast to be the clear market leader in 2018

Table of Contents

6 Worldwide Medtech Sales by Device Area in 2018

7 Worldwide Medtech Sales in 2018: Top 20 Companies

8 Worldwide Medtech vs. Prescription Drug Sales (2005-18)

9 Worldwide Medtech R&D Spend (2005-2018)

10 Medtech R&D Spend in 2018: Top 20 Companies

11 FDA Device Approval Analysis: 2005 to 2012

12 2013 FDA First Time PMA and HDE Approvals

13 In Vitro Diagnostics (IVD) Market to 2018

14 Cardiology Market to 2018

15 Diagnostic Imaging Market to 2018

16 Orthopedics Market to 2018

17 Ophthalmics Market to 2018

18 M&A Analysis: 2008 to H1 2013

19 Venture Financing Analysis: 2008 to H1 2013

20 Enterprise Value & Focus Analysis: 2013 Latest vs. 2012

5Co

pyr

igh

t ©

201

3 Ev

alu

ate

Ltd

. All

rig

hts

res

erve

d.

6Co

pyr

igh

t ©

201

3 Ev

alu

ate

Ltd

. All

rig

hts

res

erve

d.

In Vitro Diagnostics (IVD)CardiologyDiagnostic Imaging

Orthopedics

OphthalmicsEndoscopy

Drug Delivery

General & Plastic Surgery

Dental

Wound Management

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

+3.0% +3.5% +4.0% +4.5% +5.0% +5.5% +6.0%

WW

Mark

et

Sh

are

%

% Sales Growth: CAGR 2012-18

Analysis on Top 10 Device Areas in 2018, Market Share & Sales Growth (2012-18)Source: EvaluateMedTech™ (23 SEP 2013)

Note: Bubble = WW Sales in 2018

Worldwide Medtech Sales Forecast to Grow by 4.5% (CAGR) to $455bn by 2018; In Vitro Diagnostics remains Number 1 in 2018EvaluateMedTech™ finds that the market for medtech products, based on the consensus forecast for the leading 180 medtech companies, will grow by 4.5% per year (CAGR) between 2012 and 2018, to $455bn.In vitro diagnostics is expected to be the world's largest medtech segment in 2018, with sales of $58.8bn, beating cardiology and diagnostic imaging to the top spot. The fastest growing of the top 15 segments is neurology, which is set to grow at 6.9% per year (CAGR) between 2012 and 2018, to reach $8bn. Diabetic care and orthopedics are forecast to be the slowest growing segments within the top 15, expanding 3.4% per year (CAGR) between 2012 and 2018.

6

Worldwide Medtech Sales Forecast to Grow by 4.5% (CAGR) to $455bn by 2018; In Vitro Diagnostics remains Number 1 in 2018

EvaluateMedTech™ finds that the market for medtech products, based on the consensus forecast for the leading 180 medtech companies, will grow by 4.5% per year (CAGR) between 2012 and 2018, to $455bn.

In vitro diagnostics is expected to be the world’s largest medtech segment in 2018, with sales of $58.8bn, beating cardiology and diagnostic imaging to the top spot. The fastest growing of the top 15 segments is neurology, which is set to grow at 6.9% per year (CAGR) between 2012 and 2018, to reach $8bn. Diabetic care and orthopedics are forecast to be the slowest growing segments within the top 15, expanding 3.4% per year (CAGR) between 2012 and 2018.

Note: Analysis is based on the top 180 medtech companies. Sales in 2012 based on company reported data. Sales forecasts to 2018 based on a consensus of leading equity analysts’ estimates for segmental sales.

Worldwide MedTech Sales by Device Area in 2018

7Co

pyr

igh

t ©

201

3 Ev

alu

ate

Ltd

. All

rig

hts

res

erve

d.

Worldwide Medtech Sales in 2018: Top 20 Companies

WW Medtech Sales (2012/18): Top 20 Companies & Total Market

2018 Change Rank

Company Country 2012 2018 % CAGR 12-18 vs. Sep 12 ($bn) 2012 2018 Chg. (+/-) Chg. (+/-)

1 Johnson & Johnson USA 27.4 33.4 +3% -4.5 7.9% 7.3% -0.5pp -

2 Siemens Germany 17.7 21.7 +3% +1.6 5.1% 4.8% -0.3pp -

3 Medtronic USA 16.6 19.9 +3% -0.5 4.8% 4.4% -0.4pp -

4 Roche Switzerland 11.0 13.7 +4% +0.4 3.1% 3.0% -0.1pp -

5 General Electric USA 9.8 13.3 +5% -0.2 2.8% 2.9% +0.1pp -

6 Abbott Laboratories USA 9.6 12.7 +5% +0.4 2.8% 2.8% +0.0pp +1

7 Covidien USA 9.6 12.4 +4% -0.3 2.8% 2.7% -0.0pp -1

8 Philips The Netherlands 9.6 12.0 +4% +0.4 2.8% 2.6% -0.1pp -

9 Stryker USA 8.7 11.4 +5% +0.0 2.5% 2.5% +0.0pp -

10 Essilor International France 5.7 9.6 +9% +0.6 1.6% 2.1% +0.5pp +5

11 Novartis Switzerland 6.7 9.0 +5% -0.7 1.9% 2.0% +0.1pp -

12 Danaher USA 6.7 8.7 +5% +0.5 1.9% 1.9% +0.0pp -

13 B. Braun Melsungen Germany 6.5 8.7 +5% +0.3 1.9% 1.9% +0.0pp +1

14 Baxter International USA 5.1 8.6 +9% +1.2 1.4% 1.9% +0.5pp +3

15 Becton Dickinson USA 6.6 8.5 +4% +0.4 1.9% 1.9% -0.0pp -2

16 Boston Scientific USA 7.2 8.3 +2% +0.2 2.1% 1.8% -0.2pp -6

17 Olympus Japan 4.8 7.4 +8% +0.8 1.4% 1.6% +0.3pp +2

18 3M USA 5.0 6.4 +4% +0.1 1.4% 1.4% -0.0pp -

19 St. Jude Medical USA 5.5 6.3 +2% -1.0 1.6% 1.4% -0.2pp -3

20 Fresenius Germany 3.7 5.9 +8% +1.0 1.1% 1.3% +0.2pp +5

Total Top 20 183.5 237.9 +4% +0.7 52.6% 52.3% -0.2pp

Other 165.5 216.7 +5% 47.4% 47.7% +0.2pp

Total 349.0 454.6 +5% 100.0% 100.0%

Source: EvaluateMedTech™ (23 SEP 2013)

WW Market Share WW Medtech Sales ($bn)

33.4

21.719.9

13.7 13.3 12.7 12.4 12.0 11.49.6

0

5

10

15

20

25

30

35

40

Johnson &Johnson

Siemens Medtronic Roche GeneralElectric

AbbottLaboratories

Covidien Philips Stryker EssilorInternational

WW

Med

tech

Sale

s (

$b

n)

WW Medtech in 2018: Top 10 Companies Source: EvaluateMedTech™ (23 SEP 2013)

Note: Analysis is based on the top 180 medtech companies. Sales in 2012 based on company reported data. Sales forecasts to 2018 based on a consensus of leading equity analysts' estimates for segmental sales.2018 Change vs. Sep 12 ($bn) column represents the change in the consensus forecast since September 2012.

Johnson & Johnson Forecast to be Clear Market Leader in Medtech Sales in 2018EvaluateMedTech™ finds that Johnson & Johnson is forecast to be number one medtech company in terms of global medtech sales, with $33.4bn in sales in 2018. Nonetheless its share of the medtech market is expected to fall, from 7.9% in 2012 to 7.3% in 2018.The fastest growing of the top 20 companies follow two very different business strategies. Lens maker Essilor has a very narrow focus, whereas Baxter is active in many disparate areas including dialysis, drug delivery, wound management and regenerative medicine.Between 2012 and 2018 Boston Scientific is forecast to fall six ranking places, from 10th to 16th. With a CAGR of 2% between 2012 and 2018, the company looks likely to struggle to replace sales from its flagging cardiology businesses.

(-) (-) +1 -1 (-) (-) +5

Sales ($bn)CAGR 2012-18 (%)

Ranking Change 2012-18

+3%

+5%

+3%

+4%

+5%+5% +4% +4%

+9%

(-) (-) (-)

+3%

7

Johnson & Johnson Forecast to be Clear Market Leader in Medtech Sales in 2018

EvaluateMedTech™ finds that Johnson & Johnson is forecast to be number one medtech company in terms of global medtech sales, with $33.4bn in sales in 2018. Nonetheless its share of the medtech market is expected to fall, from 7.9% in 2012 to 7.3% in 2018.

The fastest growing of the top 20 companies follow two very different business strategies. Lens maker Essilor has a very narrow focus, whereas Baxter is active in many disparate areas including dialysis, drug delivery, wound management and regenerative medicine.

Between 2012 and 2018 Boston Scientific is forecast to fall six ranking places, from 10th to 16th. With a CAGR of 2% between 2012 and 2018, the company looks likely to struggle to replace sales from its flagging cardiology businesses.

Note: Analysis is based on the top 180 medtech companies. Sales in 2012 based on company reported data. Sales forecasts to 2018 based on a consensus of leading equity analysts’ estimates for segmental sales.

2018 Change vs. Sep 12 ($bn) column represents the change in the consensus forecast since September 2012.

Worldwide Medtech Sales in 2018: Top 20 Companies

8Co

pyr

igh

t ©

201

3 Ev

alu

ate

Ltd

. All

rig

hts

res

erve

d.

Worldwide Medtech vs. Prescription Drug Sales (2005-18)

WW Medtech vs. Prescription Drug Sales (2005-18)

WW Sales ($bn)

Year 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

WW Medtech Sales 219 241 267 295 299 316 340 349 357 374 394 414 434 455

Growth per Year +9.9% +11.0% +10.5% +1.2% +5.7% +7.9% +2.5% +2.2% +4.8% +5.3% +5.1% +4.9% +4.7%

Medtech as % of Rx 44.3% 44.5% 44.6% 45.5% 45.0% 46.1% 47.0% 49.0% 50.0% 50.7% 50.9% 51.0% 50.9% 51.0%

WW Prescription (Rx) 495 542 599 650 664 684 725 713 713 736 773 812 852 891

Growth per Year +9.4% +10.6% +8.4% +2.2% +3.0% +5.9% -1.7% +0.1% +3.3% +5.0% +5.0% +5.0% +4.6%

Source: EvaluateMedTech™ & EvaluatePharma® (23 SEP 2013)

CAGR 12-18

WW Medtech Sales

WW Prescription Drug Sales

+4.5%

+3.8%

219 241267

295 299 316340 349 357 374 394 414 434 455

495542

599650 664 684

725 713 713 736773

812852

891

0

100

200

300

400

500

600

700

800

900

1,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

WW

Med

tech

& R

x S

ale

s (

$b

n)

WW Medtech vs Prescription Drug Sales 2005-18 Source: EvaluateMedTech™ and EvaluatePharma® (23 SEP 2013)

WW Medtech Sales: +4.5% CAGR 2012-18

Medtech Set to Outperform Prescription Drug Market with 4.5% (CAGR) Growth vs. 3.8% between 2012 and 2018, But Pharma Forecast to Catch UpEvaluateMedTech™ consensus forecast finds that the worldwide market for medtech products is set to outperform the prescription drug market growth with 4.5% growth per year (CAGR) between 2012 and 2018, versus 3.8% for pharmaceuticals. However, from 2015 onwards growth in the prescription drug market is forecast to catch up, with annual growth of 5% forecast each year from 2015 to 2018 for both industries. Overall in 2018 the medtech industry will be 51.0% of the size of the prescription drug market, up from 44.3% in 2005.

Note: Prescription drug sales based on top 500 pharmaceutical and biotech companies from EvaluatePharma®.Sales to 2012 based on company reported sales data. Sales forecasts to 2018 based on a consensus of leading equity analysts' estimates for segmental sales.

10%11% 10%

1%

6%

8%

3% 2%

5%5% 5% 5% 5%

9%11%

8%

2%

3%

6%

-2%

0%

3%

5% 5% 5% 5%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

WW

Sale

s G

row

th %

WW Growth Rate: Medtech vs. Prescription Drug Sales 2006-18

Medtech Growth per Year

Prescription (Rx) Growth per Year

WW Prescription Sales: +3.8% CAGR 2012-18

2012: Euro crisis impacts euro sales converted to dollars.

2009: World economy contracted -2.2%

8

Medtech Set to Outperform Prescription Drug Market with 4.5% (CAGR) Growth vs. 3.8% between 2012 and 2018, But Pharma Forecast to Catch Up

EvaluateMedTech™ consensus forecast finds that the worldwide market for medtech products is set to outperform the prescription drug market growth with 4.5% growth per year (CAGR) between 2012 and 2018, versus 3.8% for pharmaceuticals. However, from 2015 onwards growth in the prescription drug market is forecast to catch up, with annual growth of 5% forecast each year from 2015 to 2018 for both industries. Overall in 2018 the medtech industry will be 51.0% of the size of the prescription drug market, up from 44.3% in 2005.

Note: Prescription drug sales based on top 500 pharmaceutical and biotech companies from EvaluatePharma®.

Sales to 2012 based on company reported sales data. Sales forecasts to 2018 based on a consensus of leading equity analysts’ estimates for segmental sales.

Worldwide Medtech vs. Prescription Drug Sales (2005-18)

9Co

pyr

igh

t ©

201

3 Ev

alu

ate

Ltd

. All

rig

hts

res

erve

d.

Worldwide Medtech R&D Spend (2005-2018)

WW Medtech R&D Spend by Medtech Companies (2005-2018)

WW Medtech R&D & Medtech Sales ($bn)

Year 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Medtech R&D Spend 12.8 14.6 17.0 18.7 18.4 19.4 20.9 21.3 21.9 22.7 23.7 24.7 25.7 26.7

Growth per Year +14.2% +16.4% +9.6% -1.3% +5.5% +7.8% +1.5% +2.9% +4.0% +4.3% +4.2% +4.1% +3.9%

WW Medtech Sales 219 241 267 295 299 316 340 349 357 374 394 414 434 455

R&D as % of Medtech Sales 5.8% 6.1% 6.4% 6.3% 6.2% 6.2% 6.1% 6.1% 6.1% 6.1% 6.0% 6.0% 5.9% 5.9%

R&D as % of Medtech Sales (Top 20 in 2018) 8.0% 7.6%

Source: EvaluateMedTech™ (23 SEP 2013) CAGR 12-18 on Medtech R&D Spend

Cumulative 5 year R&D Spend (2008-12) $99bn

CAGR 08-12 on Medtech R&D Spend +3.3%

+3.9%

1315

1719 18

1921 21 22

2324

2526

27+14.2%

+16.4%

+9.6%

-1.3%

+5.5% +7.8%

+1.5%

+2.9%+4.0% +4.3% +4.2% +4.1% +3.9%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

5

10

15

20

25

30

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

R&

D S

pen

d G

row

th %

WW

Me

dte

ch

R&

D S

pe

nd

($

bn

)

Worldwide Total Medtech R&D Spend in 2005-18Source: EvaluateMedTech™ (23 SEP 2013)

Global Medtech R&D Spend Set to Grow by 3.9% (CAGR) to $26.7bn by 2018EvaluateMedTech™ consensus forecast finds that worldwide medtech R&D is expected to grow at a healthy 3.9% per year (CAGR) between 2012 and 2018 to $26.7bn. The overall R&D investment rate is expected to be around 5.9% of sales in 2018, slightly down from the 6.1% observed in 2012, perhaps due to companies conserving their cash as payers squeeze prices. Within the top 20 companies the reinvestment rate is higher at 7.6% in 2018, but still down on the 8.0% seen in 2012.

Note: Analysis is based on the Top 180 medtech companies. R&D spend in 2012 based on company reported data. Forecast medtech R&D spend based on a consensus of leading equity analysts' estimates for company level R&D spend, extrapolated to medtech R&D when a company has non-medtech R&D activity.Medtech R&D is not disclosed by a number of companies and this analysis is limited to those companies with sufficient disclosure.

+3.9% CAGR 2012-18

9

Global Medtech R&D Spend Set to Grow by 3.9% (CAGR) to $26.7bn by 2018

EvaluateMedTech™ consensus forecast finds that worldwide medtech R&D is expected to grow at a healthy 3.9% per year (CAGR) between 2012 and 2018 to $26.7bn. The overall R&D investment rate is expected to be around 5.9% of sales in 2018, slightly down from the 6.1% observed in 2012, perhaps due to companies conserving their cash as payers squeeze prices. Within the top 20 companies the reinvestment rate is higher at 7.6% in 2018, but still down on the 8.0% seen in 2012.

Note: Analysis is based on the top 180 medtech companies. R&D spend in 2012 based on company reported data.

Forecast medtech R&D spend based on a consensus of leading equity analysts’ estimates for company level R&D spend, extrapolated to medtech R&D when a company has non-medtech R&D activity.

Medtech R&D is not disclosed by a number of companies and this analysis is limited to those companies with sufficient disclosure.

Worldwide Medtech R&D Spend (2005-2018)

10Co

pyr

igh

t ©

201

3 Ev

alu

ate

Ltd

. All

rig

hts

res

erve

d.

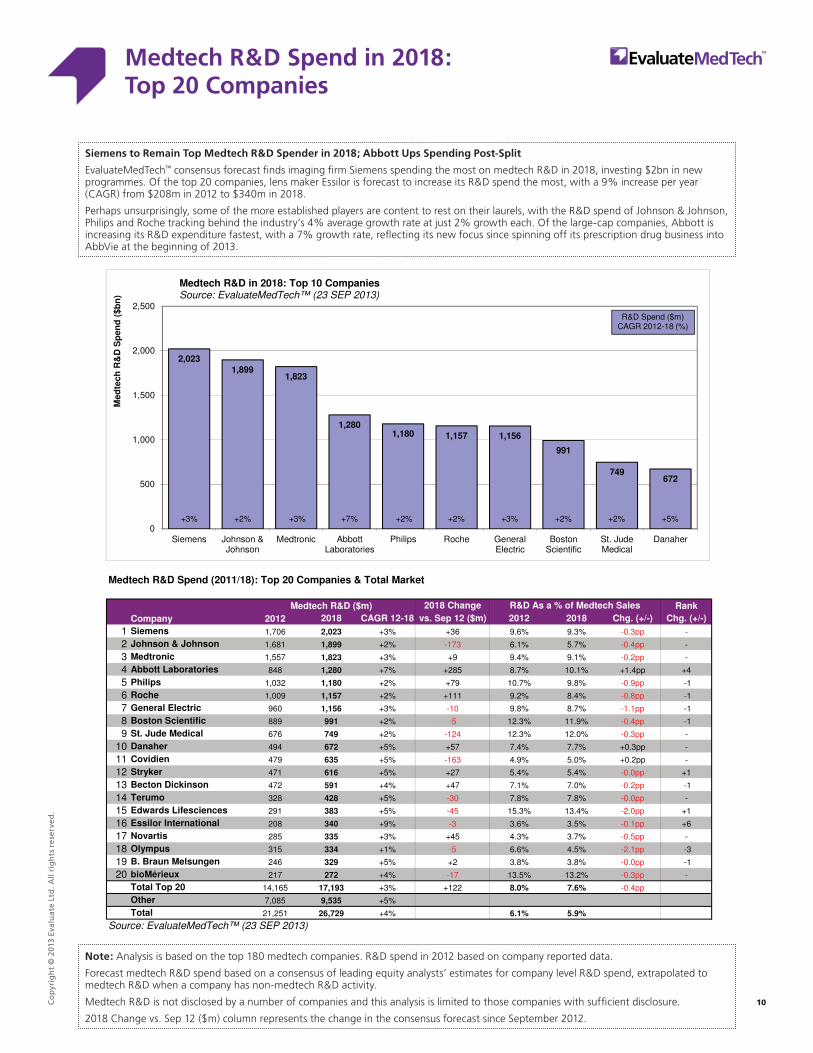

Medtech R&D Spend in 2018: Top 20 Companies

Medtech R&D Spend (2011/18): Top 20 Companies & Total Market

2018 Change Rank

Company 2012 2018 CAGR 12-18 vs. Sep 12 ($m) 2012 2018 Chg. (+/-) Chg. (+/-)

1 Siemens 1,706 2,023 +3% +36 9.6% 9.3% -0.3pp -

2 Johnson & Johnson 1,681 1,899 +2% -173 6.1% 5.7% -0.4pp -

3 Medtronic 1,557 1,823 +3% +9 9.4% 9.1% -0.2pp -

4 Abbott Laboratories 848 1,280 +7% +285 8.7% 10.1% +1.4pp +4

5 Philips 1,032 1,180 +2% +79 10.7% 9.8% -0.9pp -1

6 Roche 1,009 1,157 +2% +111 9.2% 8.4% -0.8pp -1

7 General Electric 960 1,156 +3% -10 9.8% 8.7% -1.1pp -1

8 Boston Scientific 889 991 +2% -5 12.3% 11.9% -0.4pp -1

9 St. Jude Medical 676 749 +2% -124 12.3% 12.0% -0.3pp -

10 Danaher 494 672 +5% +57 7.4% 7.7% +0.3pp -

11 Covidien 479 635 +5% -163 4.9% 5.0% +0.2pp -

12 Stryker 471 616 +5% +27 5.4% 5.4% -0.0pp +1

13 Becton Dickinson 472 591 +4% +47 7.1% 7.0% -0.2pp -1

14 Terumo 328 428 +5% -30 7.8% 7.8% -0.0pp -

15 Edwards Lifesciences 291 383 +5% -45 15.3% 13.4% -2.0pp +1

16 Essilor International 208 340 +9% -3 3.6% 3.5% -0.1pp +6

17 Novartis 285 335 +3% +45 4.3% 3.7% -0.5pp -

18 Olympus 315 334 +1% -5 6.6% 4.5% -2.1pp -3

19 B. Braun Melsungen 246 329 +5% +2 3.8% 3.8% -0.0pp -1

20 bioMérieux 217 272 +4% -17 13.5% 13.2% -0.3pp -

Total Top 20 14,165 17,193 +3% +122 8.0% 7.6% -0.4pp

Other 7,085 9,535 +5%

Total 21,251 26,729 +4% 6.1% 5.9%

Source: EvaluateMedTech™ (23 SEP 2013)

R&D As a % of Medtech SalesMedtech R&D ($m)

2,0231,899

1,823

1,2801,180 1,157 1,156

991

749672

0

500

1,000

1,500

2,000

2,500

Siemens Johnson &Johnson

Medtronic AbbottLaboratories

Philips Roche GeneralElectric

BostonScientific

St. JudeMedical

Danaher

Med

tech

R&

D S

pen

d (

$b

n)

Medtech R&D in 2018: Top 10 CompaniesSource: EvaluateMedTech™ (23 SEP 2013)

Note: Analysis is based on the top 180 medtech companies. R&D spend in 2012 based on company reported data. Forecast medtech R&D spend based on a consensus of leading equity analysts' estimates for company level R&D spend, extrapolated to medtech R&D when a company has non-medtech R&D activity.Medtech R&D is not disclosed by a number of companies and this analysis is limited to those companies with sufficient disclosure.2018 Change vs. Sep 12 ($m) column represents the change in the consensus forecast since September 2012.

Siemens to Remain Top Medtech R&D Spender in 2018; Abbott Ups Spending Post-SplitEvaluateMedTech™ consensus forecast finds imaging firm Siemens spending the most on medtech R&D in 2018, investing $2bn in new programmes. Of the top 20 companies, lens maker Essilor is forecast to increase its R&D spend the most, with a 9% increase per year (CAGR) from $208m in 2012 to $340m in 2018.Perhaps unsurprisingly, some of the more established players are content to rest on their laurels, with the R&D spend of Johnson & Johnson, Philips and Roche tracking behind the industry’s 4% average growth rate at just 2% growth each. Of the large-cap companies, Abbott is increasing its R&D expenditure fastest, with a 7% growth rate, reflecting its new focus since spinning off its prescription drug business into AbbVie at the beginning of 2013.

+2% +7% +2%+2%+3% +2% +3% +2%

R&D Spend ($m)CAGR 2012-18 (%)

+5%+3%

10

Siemens to Remain Top Medtech R&D Spender in 2018; Abbott Ups Spending Post-Split

EvaluateMedTech™ consensus forecast finds imaging firm Siemens spending the most on medtech R&D in 2018, investing $2bn in new programmes. Of the top 20 companies, lens maker Essilor is forecast to increase its R&D spend the most, with a 9% increase per year (CAGR) from $208m in 2012 to $340m in 2018.

Perhaps unsurprisingly, some of the more established players are content to rest on their laurels, with the R&D spend of Johnson & Johnson, Philips and Roche tracking behind the industry’s 4% average growth rate at just 2% growth each. Of the large-cap companies, Abbott is increasing its R&D expenditure fastest, with a 7% growth rate, reflecting its new focus since spinning off its prescription drug business into AbbVie at the beginning of 2013.

Note: Analysis is based on the top 180 medtech companies. R&D spend in 2012 based on company reported data.

Forecast medtech R&D spend based on a consensus of leading equity analysts’ estimates for company level R&D spend, extrapolated to medtech R&D when a company has non-medtech R&D activity.

Medtech R&D is not disclosed by a number of companies and this analysis is limited to those companies with sufficient disclosure.

2018 Change vs. Sep 12 ($m) column represents the change in the consensus forecast since September 2012.

Medtech R&D Spend in 2018: Top 20 Companies

11Co

pyr

igh

t ©

201

3 Ev

alu

ate

Ltd

. All

rig

hts

res

erve

d.

FDA Device Approval Analysis: 2005 to 2012

FDA Approval Count (1st PMAs/ HDEs/ Supplementary PMAs/ 510(k)s)

Year 2005 2006 2007 2008 2009 2010 2011 2012

1st Time PMA/ HDE/ PDP 34 44 32 30 18 22 43 41

% Chg. +29% -27% -6% -40% +22% +95% -5%

Supplementary PMA/ PDP 735 1,062 1,117 1,488 1,498 1,841 2,192 2,380

% Chg. +44% +5% +33% +1% +23% +19% +9%

510(k) 3,205 3,257 3,035 3,102 3,044 2,850 3,150 3,185

% Chg. +2% -7% +2% -2% -6% +11% +1%

Total 3,974 4,363 4,184 4,620 4,560 4,713 5,385 5,606

% Chg. +10% -4% +10% -1% +3% +14% +4%

2012: FDA Approval Count (1st Time PMAs/ HDEs/ PDPs/ 510(k)s) & Medtech R&D Spend

Company

1 Medtronic

2 Boston Scientific

3 Abbott Laboratories

4 Johnson & Johnson

5 St. Jude Medical

6 Roche

7 Edwards Lifesciences

8 Siemens

9 Novartis

10 Stryker

TotalSource: EvaluateMedTech™ (23 SEP 2013)

0 45

471

41 2,380

0 5 43

3,185

R&D Spend

($m)

1,557

889

848

1,706

285

1 26

1 73

1,681

676

1,009

291

1 114

5 195

2 96

1 158

PMA/ HDEs -

First Approval

PMA/ PDPs -

Suppl.

510(k)

Clearance

Total

Approvals

2 461

1 573

35

45

173

119

81

66

619

498

218

197

52

48

5,606

18

82

14

21

39

7

7

34 44 32 30 18 22 43 41

3,205 3,257

3,035 3,102 3,0442,850

3,150 3,185

735

1,062 1,117

1,488 1,498

1,841

2,1922,380

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0

10

20

30

40

50

60

2005 2006 2007 2008 2009 2010 2011 2012

No

. o

f S

up

PM

As

/ 5

10

(k)s

No

. o

f 1

st

PM

A/

HD

E/ P

DP

FDA Approval Count: 1st PMA/HDE/PDPs, 510(k)s & Supplementary PMA/PDPs Per Year Source: EvaluateMedTech™ (23 SEP 2013)

1st Time PMA/ HDE/ PDP 510(k) Supplementary PMA/ PDP

Number of 1st Time PMAs Decreases 5% to 41; 510(k) Approvals Up 1% to 3,185EvaluateMedTech™ found that the FDA approved 41 new PMAs/HDEs/PDPs (first time approvals) in 2012, a decrease of 5% from the 2011 figure of 43. In 2012 Abbott had the most first PMA/HDE approvals with five, whilst Medtronic had the most overallapprovals with 619. 510(k) clearances held steady, increasing by just 1% year-on-year to 3,185 in 2012.

Note: Based on Devices@FDA data. PMA (Pre-market Approval): a class III device which is a ‘life-sustaining or life-supporting implantable device'; usually require trials. 510(k): "substantially equivalent” to a legally marketed Class I, II, III device (where PMA not required). HDE (Humanitarian Device Exemption): a device for treating or diagnosing a disease/condition that affects <4,000 individuals

11

Number of 1st Time PMAs Decreases 5% to 41; 510(k) Approvals Up 1% to 3,185

EvaluateMedTech™ found that the FDA approved 41 new PMAs/HDEs/PDPs (first time approvals) in 2012, a decrease of 5% from the 2011 figure of 43. In 2012 Abbott had the most first PMA/HDE approvals with five, whilst Medtronic had the most overall approvals with 619. 510(k) clearances held steady, increasing by just 1% year-on-year to 3,185 in 2012.

Note: Based on Devices@FDA data.

PMA (Pre-market Approval): a class III device which is a ‘life-sustaining or life-supporting implantable device’; usually require trials.

510(k): “substantially equivalent” to a legally marketed Class I, II, III device (where PMA not required).

HDE (Humanitarian Device Exemption): a device for treating or diagnosing a disease/condition that affects <4,000 individuals in the US per year.

FDA Device Approval Analysis: 2005 to 2012

12Co

pyr

igh

t ©

201

3 Ev

alu

ate

Ltd

. All

rig

hts

res

erve

d.

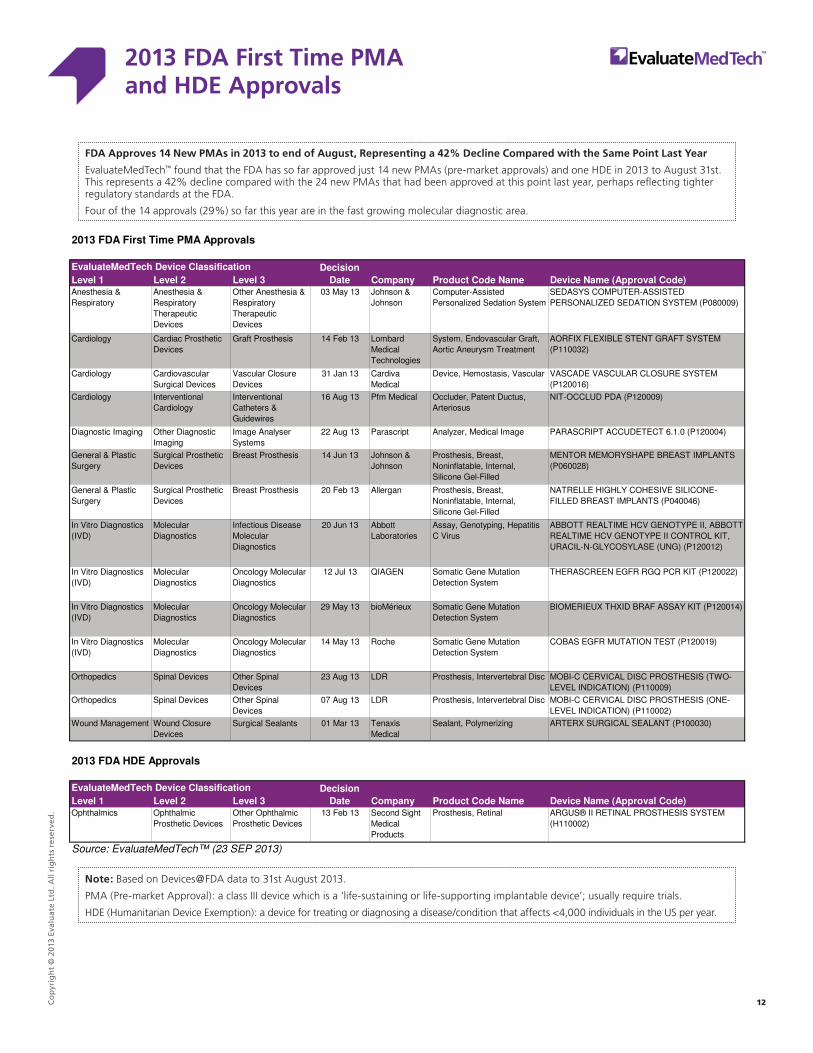

2013 FDA First Time PMA and HDE Approvals

2013 FDA First Time PMA Approvals

Level 1 Level 2 Level 3 Company Product Code Name Device Name (Approval Code)Anesthesia &

Respiratory

Anesthesia &

Respiratory

Therapeutic

Devices

Other Anesthesia &

Respiratory

Therapeutic

Devices

03 May 13 Johnson &

Johnson

Computer-Assisted

Personalized Sedation System

SEDASYS COMPUTER-ASSISTED

PERSONALIZED SEDATION SYSTEM (P080009)

Cardiology Cardiac Prosthetic

Devices

Graft Prosthesis 14 Feb 13 Lombard

Medical

Technologies

System, Endovascular Graft,

Aortic Aneurysm Treatment

AORFIX FLEXIBLE STENT GRAFT SYSTEM

(P110032)

Cardiology Cardiovascular

Surgical Devices

Vascular Closure

Devices

31 Jan 13 Cardiva

Medical

Device, Hemostasis, Vascular VASCADE VASCULAR CLOSURE SYSTEM

(P120016)

Cardiology Interventional

Cardiology

Interventional

Catheters &

Guidewires

16 Aug 13 Pfm Medical Occluder, Patent Ductus,

Arteriosus

NIT-OCCLUD PDA (P120009)

Diagnostic Imaging Other Diagnostic

Imaging

Image Analyser

Systems

22 Aug 13 Parascript Analyzer, Medical Image PARASCRIPT ACCUDETECT 6.1.0 (P120004)

General & Plastic

Surgery

Surgical Prosthetic

Devices

Breast Prosthesis 14 Jun 13 Johnson &

Johnson

Prosthesis, Breast,

Noninflatable, Internal,

Silicone Gel-Filled

MENTOR MEMORYSHAPE BREAST IMPLANTS

(P060028)

General & Plastic

Surgery

Surgical Prosthetic

Devices

Breast Prosthesis 20 Feb 13 Allergan Prosthesis, Breast,

Noninflatable, Internal,

Silicone Gel-Filled

NATRELLE HIGHLY COHESIVE SILICONE-

FILLED BREAST IMPLANTS (P040046)

In Vitro Diagnostics

(IVD)

Molecular

Diagnostics

Infectious Disease

Molecular

Diagnostics

20 Jun 13 Abbott

Laboratories

Assay, Genotyping, Hepatitis

C Virus

ABBOTT REALTIME HCV GENOTYPE II, ABBOTT

REALTIME HCV GENOTYPE II CONTROL KIT,

URACIL-N-GLYCOSYLASE (UNG) (P120012)

In Vitro Diagnostics

(IVD)

Molecular

Diagnostics

Oncology Molecular

Diagnostics

12 Jul 13 QIAGEN Somatic Gene Mutation

Detection System

THERASCREEN EGFR RGQ PCR KIT (P120022)

In Vitro Diagnostics

(IVD)

Molecular

Diagnostics

Oncology Molecular

Diagnostics

29 May 13 bioMérieux Somatic Gene Mutation

Detection System

BIOMERIEUX THXID BRAF ASSAY KIT (P120014)

In Vitro Diagnostics

(IVD)

Molecular

Diagnostics

Oncology Molecular

Diagnostics

14 May 13 Roche Somatic Gene Mutation

Detection System

COBAS EGFR MUTATION TEST (P120019)

Orthopedics Spinal Devices Other Spinal

Devices

23 Aug 13 LDR Prosthesis, Intervertebral Disc MOBI-C CERVICAL DISC PROSTHESIS (TWO-

LEVEL INDICATION) (P110009)

Orthopedics Spinal Devices Other Spinal

Devices

07 Aug 13 LDR Prosthesis, Intervertebral Disc MOBI-C CERVICAL DISC PROSTHESIS (ONE-

LEVEL INDICATION) (P110002)

Wound Management Wound Closure

Devices

Surgical Sealants 01 Mar 13 Tenaxis

Medical

Sealant, Polymerizing ARTERX SURGICAL SEALANT (P100030)

2013 FDA HDE Approvals

Level 1 Level 2 Level 3 Company Product Code Name Device Name (Approval Code)Ophthalmics Ophthalmic

Prosthetic Devices

Other Ophthalmic

Prosthetic Devices

13 Feb 13 Second Sight

Medical

Products

Prosthesis, Retinal ARGUS® II RETINAL PROSTHESIS SYSTEM

(H110002)

Source: EvaluateMedTech™ (23 SEP 2013)

EvaluateMedTech Device Classification Decision

Date

EvaluateMedTech Device Classification Decision

Date

FDA Approves 14 New PMAs in 2013 to end of August, Representing a 42% Decline Compared with the Same Point Last YearEvaluateMedTech™ found that the FDA has so far approved just 14 new PMAs (pre-market approvals) and one HDE in 2013 to August 31st. This represents a 42% decline compared with the 24 new PMAs that had been approved at this point last year, perhaps reflecting tighter regulatory standards at the FDA.Four of the 14 approvals (29%) so far this year are in the fast growing molecular diagnostic area.

Note: Based on Devices@FDA data to 31st August 2013.PMA (Pre-market Approval): a class III device which is a ‘life-sustaining or life-supporting implantable device'; usually require trials. HDE (Humanitarian Device Exemption): a device for treating or diagnosing a disease/condition that affects <4,000 individuals in the US per year.

12

FDA Approves 14 New PMAs in 2013 to end of August, Representing a 42% Decline Compared with the Same Point Last Year

EvaluateMedTech™ found that the FDA has so far approved just 14 new PMAs (pre-market approvals) and one HDE in 2013 to August 31st. This represents a 42% decline compared with the 24 new PMAs that had been approved at this point last year, perhaps reflecting tighter regulatory standards at the FDA.

Four of the 14 approvals (29%) so far this year are in the fast growing molecular diagnostic area.

Note: Based on Devices@FDA data to 31st August 2013.

PMA (Pre-market Approval): a class III device which is a ‘life-sustaining or life-supporting implantable device’; usually require trials.

HDE (Humanitarian Device Exemption): a device for treating or diagnosing a disease/condition that affects <4,000 individuals in the US per year.

2013 FDA First Time PMA and HDE Approvals

13Co

pyr

igh

t ©

201

3 Ev

alu

ate

Ltd

. All

rig

hts

res

erve

d.

In Vitro Diagnostics (IVD) Market to 2018

Top 10 Companies & Total WW In Vitro Diagnostics Sales 2012-18

CAGR 2018 Change Rank Chg.

Rank Company 2012 2018 2012-18 vs. Sep 12 ($m) 2012 2018 2012-18

1 Roche 8,216 11,329 +6% +586 18.8% 19.3% -

2 Abbott Laboratories 4,292 6,292 +7% +647 9.8% 10.7% +2

3 Danaher 4,628 6,197 +5% +452 10.6% 10.5% -

4 Siemens 5,153 6,073 +3% +330 11.8% 10.3% -2

5 Thermo Fisher Scientific 2,912 3,749 +4% -58 6.7% 6.4% -

6 Becton Dickinson 2,538 3,203 +4% +62 5.8% 5.4% -

7 Alere 2,110 2,808 +5% +33 4.8% 4.8% -

8 Sysmex 1,666 2,542 +7% -535 3.8% 4.3% +1

9 Johnson & Johnson 2,069 2,143 +1% -427 4.7% 3.6% -1

10 bioMérieux 1,609 2,064 +4% -27 3.7% 3.5% -

Top 10 35,194 46,400 +5% +1062 80.7% 78.9%

Other 8,421 12,389 +7% 19.3% 21.1%

Total Industry 43,614 58,789 +5.1% 100.0% 100.0%

Source: EvaluateMedTech™ (23 SEP 2013); Consensus sales from equity analysts' reports

WW Sales ($m) WW Market Share

0%

20%

40%

60%

80%

100%

120%

140%

0 0.2 0.4 0.6 0.8 1 1.2 1.4

WW

Mark

et

Sh

are

%

% Sales Growth: CAGR 2011-18

Takeda: Actos generic competition expected 2012.

Note: Bubble = WW Sales in 2018

Novo: Solid growth in its core insulin franchise, including Tresiba (insulin degludec), and GLP-1 Victoza (liraglutide).

Merck: Strong growth in DPP-IV inhibitor

0%

20%

40%

60%

80%

100%

120%

140%

0 0.2 0.4 0.6 0.8 1 1.2 1.4

WW

Mark

et

Sh

are

%

% Sales Growth: CAGR 2011-18

Takeda: Actos generic competition expected 2012.

Note: Bubble = WW Sales in 2018

Novo: Solid growth in its core insulin franchise, including Tresiba (insulin degludec), and GLP-1 Victoza (liraglutide).

Merck: Strong growth in DPP-IV inhibitor

Roche Maintains Leading Position within In Vitro Diagnostics Market; J&J FlagsEvaluateMedTech™ consensus forecast finds Swiss giant Roche is the clear market leader within in vitro diagnostics with sales of $11.3bn in 2018, and a 19.3% market share*. But arguably the real success story is Abbott, which is expected to jump two ranking places to second spot between 2012 and 2018, with 2018 sales of $6.3bn.Conversely, Johnson & Johnson's diagnostic business is the slowest growing of the top 10 companies, with sales growing 1% (CAGR) between 2012 and 2018, a factor that may have influenced its recent decision to look for a buyer for the flagging business.

Roche

Abbott LaboratoriesDanaherSiemens

Thermo Fisher Scientific

0%

5%

10%

15%

20%

25%

+0% +1% +2% +3% +4% +5% +6% +7% +8% +9%

WW

Mark

et

Sh

are

%

% Sales Growth: CAGR 2012-18Note: Bubble = WW Sales in 2018

Analysis on WW Sales, Market Share & Sales Growth (2012-18)Source: EvaluateMedTech™ (23 SEP 2013)

Note: *Excludes Glucose Test Systems which are included in Diabetic Care classification.2018 Change vs. Sep 12 ($m) column represents the change in the consensus forecast since September 2012.

Abbott: Strong growth from Point of Care and Molecular Diagnostics

13

Roche Maintains Leading Position within In Vitro Diagnostics Market; J&J Flags

EvaluateMedTech™ consensus forecast finds Swiss giant Roche is the clear market leader within in vitro diagnostics with sales of $11.3bn in 2018, and a 19.3% market share*. But arguably the real success story is Abbott, which is expected to jump two ranking places to second spot between 2012 and 2018, with 2018 sales of $6.3bn.

Conversely, Johnson & Johnson’s diagnostic business is the slowest growing of the top 10 companies, with sales growing 1% (CAGR) between 2012 and 2018, a factor that may have influenced its recent decision to look for a buyer for the flagging business.

Note: *Excludes Glucose Test Systems which are included in Diabetic Care classification.

2018 Change vs. Sep 12 ($m) column represents the change in the consensus forecast since September 2012.

In Vitro Diagnostics (IVD) Market to 2018

14Co

pyr

igh

t ©

201

3 Ev

alu

ate

Ltd

. All

rig

hts

res

erve

d.

Cardiology Market to 2018

Top 10 Companies & Total WW Cardiology Sales 2012-18

CAGR 2018 Change Rank Chg.

Rank Company 2012 2018 2012-18 vs. Sep 12 ($m) 2012 2018 2012-18

1 Medtronic 8,695 9,866 +2% -487 22.8% 20.2% -

2 St. Jude Medical 5,080 5,662 +2% -893 13.3% 11.6% -

3 Boston Scientific 5,008 5,319 +1% +197 13.1% 10.9% -

4 Abbott Laboratories 2,925 3,532 +3% -33 7.7% 7.2% -

5 Edwards Lifesciences 1,866 2,826 +7% -665 4.9% 5.8% +2

6 Johnson & Johnson 1,985 2,667 +5% +22 5.2% 5.5% -1

7 Getinge 1,934 2,626 +5% +21 5.1% 5.4% -1

8 Terumo 1,775 2,558 +6% -5 4.7% 5.2% -

9 Covidien 1,602 2,192 +5% -200 4.2% 4.5% -

10 Asahi Kasei 653 1,498 +15% +82 1.7% 3.1% +3

Top 10 31,522 38,747 +3% -1961 82.6% 79.5%

Other 6,627 9,991 +7% 17.4% 20.5%

Total Industry 38,149 48,738 +4.2% 100.0% 100.0%

Source: EvaluateMedTech™ (23 SEP 2013); Consensus sales from equity analysts' reports.

WW Sales ($m) WW Market Share

Takeda: Actos generic competition expected 2012.

Note: Bubble = WW Sales in 2018

Merck: Strong growth in DPP-IV inhibitor

Takeda: Actos generic competition expected 2012.

Note: Bubble = WW Sales in 2018

Merck: Strong growth in DPP-IV inhibitor

Medtronic Set to Maintain Number 1 Position in Cardiology to 2018 but Asahi Kasei Growing FastEvaluateMedTech™ consensus forecast finds that Medtronic will remain the world's number one cardiology company with global sales of $9.9bn in 2018 and a market share of 20%. Asahi Kasei is set to be the fastest growing cardiology company in the top 10 with expected 15% per year growth (CAGR) between 2012 & 2018, driven by its acquisition of ZOLL Medical in 2012.

Medtronic

St. Jude Medical

Boston Scientific

Abbott Laboratories

Edwards Lifesciences

0%

5%

10%

15%

20%

25%

30%

+0% +1% +2% +3% +4% +5% +6% +7% +8% +9%

WW

Ma

rke

t S

ha

re %

% Sales Growth: CAGR 2012-18Note: Bubble = WW Sales in 2018

Note: General Electric & Philips do not disclose cardiology sales.2018 Change vs. Sep 12 ($m) column represents the change in the consensus forecast since September 2012.

Edwards: Solid growth in transcatheter heart valves segment.

Analysis on WW Sales, Market Share & Sales Growth (2012-18)Source: EvaluateMedTech™ (23 SEP 2013)

14

Medtronic Set to Maintain Number 1 Position in Cardiology to 2018 but Asahi Kasei Growing Fast

EvaluateMedTech™ consensus forecast finds that Medtronic will remain the world’s number one cardiology company with global sales of $9.9bn in 2018 and a market share of 20%. Asahi Kasei is set to be the fastest growing cardiology company in the top 10 with expected 15% per year growth (CAGR) between 2012 & 2018, driven by its acquisition of ZOLL Medical in 2012.

Note: General Electric & Philips do not disclose cardiology sales.

2018 Change vs. Sep 12 ($m) column represents the change in the consensus forecast since September 2012.

Cardiology Market to 2018

15Co

pyr

igh

t ©

201

3 Ev

alu

ate

Ltd

. All

rig

hts

res

erve

d.

Diagnostic Imaging Market to 2018

Top 10 Companies & Total WW Diagnostic Imaging Sales 2012-18

CAGR 2018 Change Rank Chg.

Rank Company 2012 2018 2012-18 vs. Sep 12 ($m) 2012 2018 2012-18

1 Siemens 10,421 12,959 +4% +1031 28.9% 28.7% -

2 General Electric 8,414 11,353 +5% -178 23.3% 25.2% -

3 Philips 4,878 6,162 +4% +200 13.5% 13.7% -

4 Toshiba 4,522 4,806 +1% -1047 12.5% 10.6% -

5 Carestream Health 1,525 1,977 +4% -55 4.2% 4.4% -

6 Hitachi Medical 1,344 1,329 -0% -520 3.7% 2.9% -

7 Agfa-Gevaert 951 986 +1% +69 2.6% 2.2% -

8 Konica Minolta 880 869 -0% -287 2.4% 1.9% -

9 Varian Medical Systems 493 757 +7% +11 1.4% 1.7% +1

10 Shimadzu 667 741 +2% -112 1.8% 1.6% -1

Top 10 34,094 41,939 +4% -889 94.5% 92.9%

Other 1,985 3,200 +8% 5.5% 7.1%

Total Industry 36,079 45,139 +3.8% 100.0% 100.0%

Source: EvaluateMedTech™ (23 SEP 2013); Consensus sales from equity analysts' reports

WW Sales ($m) WW Market Share

Siemens and General Electric to Retain Leading Positions in 2018EvaluateMedTech™ consensus forecast finds that Siemens and General Electric remain the dominant forces in the diagnostic imaging industry in 2018, with a combined market share of 53.9%. Of the two, Siemens is forecast to be the world's leading diagnostic imaging company in 2018 – just as it was in 2012 – based on worldwide sales of $13bn and a 28.7% market share. General Electric is set to close the gap on Siemens, though, with sales expected to grow by 5% per year (CAGR) to $11.4bn in 2018. Overall, the diagnostic imaging market is set to grow at 3.8% per year (CAGR) to $45.1bn in 2018.

Siemens

General Electric

Philips

Toshiba

Carestream Health

0%

5%

10%

15%

20%

25%

30%

35%

40%

+0% +1% +2% +3% +4% +5% +6% +7%

WW

Mark

et

Sh

are

%

% Sales Growth: CAGR 2012-18Note: Bubble = WW Sales in 2018

Note: Segment sales include servicing of machines.FUJIFILM's Diagnostic Imaging sales are not available.2018 Change vs. Sep 12 ($m) column represents the change in the consensus forecast since September 2012.

Analysis on WW Sales, Market Share & Sales Growth (2012-18)Source: EvaluateMedTech™ (23 SEP 2013)

15

Siemens and General Electric to Retain Leading Positions in 2018

EvaluateMedTech™ consensus forecast finds that Siemens and General Electric remain the dominant forces in the diagnostic imaging industry in 2018, with a combined market share of 53.9%. Of the two, Siemens is forecast to be the world’s leading diagnostic imaging company in 2018 – just as it was in 2012 – based on worldwide sales of $13bn and a 28.7% market share. General Electric is set to close the gap on Siemens, though, with sales expected to grow by 5% per year (CAGR) to $11.4bn in 2018. Overall, the diagnostic imaging market is set to grow at 3.8% per year (CAGR) to $45.1bn in 2018.

Note: Segment sales include servicing of machines.

FUJIFILM’s Diagnostic Imaging sales are not available.

2018 Change vs. Sep 12 ($m) column represents the change in the consensus forecast since September 2012

Diagnostic Imaging Market to 2018

16Co

pyr

igh

t ©

201

3 Ev

alu

ate

Ltd

. All

rig

hts

res

erve

d.

Orthopedics Market to 2018

Top 10 Companies & Total WW Orthopedics Sales 2012-18

CAGR 2018 Change Rank Chg.

Rank Company 2012 2018 2012-18 vs. Sep 12 ($m) 2012 2018 2012-18

1 Johnson & Johnson 7,238 10,642 +7% -503 22.1% 26.6% -

2 Stryker 4,932 6,402 +4% +321 15.1% 16.0% -

3 Zimmer 4,234 5,274 +4% +91 12.9% 13.2% -

4 Biomet 2,796 3,360 +3% -84 8.5% 8.4% +1

5 Medtronic 3,131 3,244 +1% -82 9.6% 8.1% -1

6 Smith & Nephew 2,178 2,394 +2% -261 6.7% 6.0% -

7 Arthrex 1,080 1,575 +6% n/a 3.3% 3.9% +1

8 NuVasive 581 844 +6% -58 1.8% 2.1% +1

9 Globus Medical 386 746 +12% n/a 1.2% 1.9% +4

10 Wright Medical Group 484 706 +6% +118 1.5% 1.8% +1

Top 10 27,040 35,187 +4% -458 82.6% 88.0%

Other 5,684 4,815 -3% 17.4% 12.0%

Total Industry 32,724 40,003 +3.4% 100.0% 100.0%

Source: EvaluateMedTech™ (23 SEP 2013); Consensus sales from equity analysts' reports

WW Sales ($m) WW Market Share

Johnson & Johnson

Stryker

Zimmer

BiometMedtronic

0%

5%

10%

15%

20%

25%

30%

35%

+0% +1% +2% +3% +4% +5% +6% +7% +8% +9%

WW

Mark

et

Sh

are

%

% Sales Growth: CAGR 2012-18Note: Bubble = WW Sales in 2018Note: Bubble = WW Sales in 2018

Johnson & Johnson Set to Entrench Domination of Slow-Growing Orthopedics Market EvaluateMedTech™ consensus forecast finds that, despite high-profile failures with some of its joint products, Johnson & Johnson is due to be the clear dominant force in orthopedics. It is forecast to command an even greater market share in 2018, 26.6%, than the already-leading 22.1% in 2012, largely owing to its acquisition of Synthes in June 2012.Overall, the orthopedics market is set to grow at 3.4% per year (CAGR), slower growth than the medtech industry as a whole, reflecting a lack of technological breakthroughs in a maturing market.

Note: Bubble = WW Sales in 2018

JNJ: Acquired Synthes in June 2012 for $19.7bn.

Analysis on WW Sales, Market Share & Sales Growth (2012-18)Source: EvaluateMedTech™ (23 SEP 2013)

Note: 2018 Change vs. Sep 12 ($m) column represents the change in the consensus forecast since September 2012.

16

Johnson & Johnson Set to Entrench Domination of Slow-Growing Orthopedics Market

EvaluateMedTech™ consensus forecast finds that, despite high-profile failures with some of its joint products, Johnson & Johnson is due to be the clear dominant force in orthopedics. It is forecast to command an even greater market share in 2018, 26.6%, than the already-leading 22.1% in 2012, largely owing to its acquisition of Synthes in June 2012.

Overall, the orthopedics market is set to grow at 3.4% per year (CAGR), slower growth than the medtech industry as a whole, reflecting a lack of technological breakthroughs in a maturing market.

Note: 2018 Change vs. Sep 12 ($m) column represents the change in the consensus forecast since September 2012.

Orthopedics Market to 2018

17Co

pyr

igh

t ©

201

3 Ev

alu

ate

Ltd

. All

rig

hts

res

erve

d.

Ophthalmics Market to 2018

Top 10 Companies & Total WW Ophthalmics Sales 2012-18

CAGR 2018 Change Rank Chg.

Rank Company 2012 2018 2012-18 vs. Sep 12 ($m) 2012 2018 2012-18

1 Essilor International 5,716 9,591 +9% +632 24.2% 29.1% +1

2 Novartis 6,206 8,479 +5% -703 26.3% 25.7% -1

3 Johnson & Johnson 2,996 3,519 +3% -376 12.7% 10.7% -

4 HOYA 1,958 2,564 +5% -257 8.3% 7.8% -

5 Valeant Pharmaceuticals* 1,750 2,448 +6% new entry 7.4% 7.4% new entry

6 Carl Zeiss 1,745 2,056 +3% -202 7.4% 6.2% -

7 The Cooper Companies 1,189 1,744 +7% +46 5.0% 5.3% -

8 Abbott Laboratories 1,097 1,322 +3% -124 4.7% 4.0% -

9 TOPCON 376 538 +6% -1 1.6% 1.6% -

10 NIDEK 370 397 +1% -102 1.6% 1.2% -

Top 10 23,402 32,658 +6% -1085 99.2% 99.2%

Other 188 279 0.8% 0.8%

Total Industry 23,590 32,937 +5.7% 100.0% 100.0%

Source: EvaluateMedTech™ (23 SEP 2013); Consensus sales from equity analysts' reports

WW Sales ($m) WW Market Share

0%

20%

40%

60%

80%

100%

120%

140%

0 0.2 0.4 0.6 0.8 1 1.2 1.4

WW

Mark

et

Sh

are

%

% Sales Growth: CAGR 2011-18

Takeda: Actos generic competition expected 2012.

Note: Bubble = WW Sales in 2018

Novo: Solid growth in its core insulin franchise, including Tresiba (insulin degludec), and GLP-1 Victoza (liraglutide).

Merck: Strong growth in DPP-IV inhibitor

0%

20%

40%

60%

80%

100%

120%

140%

0 0.2 0.4 0.6 0.8 1 1.2 1.4

WW

Mark

et

Sh

are

%

% Sales Growth: CAGR 2011-18

Takeda: Actos generic competition expected 2012.

Note: Bubble = WW Sales in 2018

Novo: Solid growth in its core insulin franchise, including Tresiba (insulin degludec), and GLP-1 Victoza (liraglutide).

Merck: Strong growth in DPP-IV inhibitor

Essilor To Replace Novartis as Top Ophthalmics Company by 2018EvaluateMedTech™ consensus forecast finds that Essilor will take over from Novartis as the leading ophthalmics company in 2018 with global sales of $9.6bn. The French maker of optical lenses is expected to demonstrate strong year-on-year growth of 9% between 2012 and 2018.Elsewhere, a new player has entered the game: Valeant Pharmaceuticals debuts in the top 10 at number 5 following its August 2013 acquisition of Bausch & Lomb, with 2018 sales forecast to reach $2.4bn.

Essilor International

Novartis

Johnson & Johnson

HOYA Valeant Pharmaceuticals*

0%

5%

10%

15%

20%

25%

30%

35%

40%

+0% +2% +4% +6% +8% +10% +12%

WW

Ma

rke

t S

ha

re %

% Sales Growth: CAGR 2012-18Note: Bubble = WW Sales in 2018

Valeant: Entered the Ophthalmics space in 2013 following acquisition of Bausch + Lomb

Note: *2012 sales figure and market share for Valeant represent those of Bausch + Lomb prior to acquisition.2018 Change vs. Sep 12 ($m) column represents the change in the consensus forecast since September 2012.

Analysis on WW Sales, Market Share & Sales Growth (2012-18)Source: EvaluateMedTech™ (23 SEP 2013)

17

Essilor To Replace Novartis as Top Ophthalmics Company by 2018

EvaluateMedTech™ consensus forecast finds that Essilor will take over from Novartis as the leading ophthalmics company in 2018 with global sales of $9.6bn. The French maker of optical lenses is expected to demonstrate strong year-on-year growth of 9% between 2012 and 2018.

Elsewhere, a new player has entered the game: Valeant Pharmaceuticals debuts in the top 10 at number 5 following its August 2013 acquisition of Bausch & Lomb, with 2018 sales forecast to reach $2.4bn.

Note: *2012 sales figure and market share for Valeant represent those of Bausch + Lomb prior to acquisition.

2018 Change vs. Sep 12 ($m) column represents the change in the consensus forecast since September 2012.

Ophthalmics Market to 2018

18Co

pyr

igh

t ©

201

3 Ev

alu

ate

Ltd

. All

rig

hts

res

erve

d.

M&A Analysis: 2008 to H1 2013

Count of Medtech M&A Deals vs. Total Medtech M&A Value (2008 - H1 2013)

Year 2008 2009 2010 2011 2012 H1 2012 H1 2013

Deal Count 209 164 253 246 224 112 95

% Chg. -22% 54% -3% -9% -15%

Deal Value ($bn) 36 13 50 77 46 31 6

% Chg. -65% 293% 55% -41% -79%

Top 10 MedTech M&A Closed Deals in H1 2013: Ranked on Deal Value

Completion Deal

Target Country (Status) Acquiror Date Value ($m)

1 Conceptus USA (Listed) Bayer 05 Jun 13 1,100

2 Trauson China (Listed) Stryker 01 Mar 13 764

3 Technolas Perfect Vision Germany (Private) Bausch + Lomb 28 Jan 13 645

4 Verinata Health USA (Private) Illumina 21 Feb 13 450

5 BioMimetic Therapeutics USA (Listed) Wright Medical Group 01 Mar 13 380

6 Angiotech's Interventional Business Canada (-) Argon Medical Devices 15 Apr 13 363

7 Young Innovations USA (Listed) Consortium of Investors 31 Jan 13 314

8 HemoCue Sweden (-) Danaher 09 Apr 13 300

9 Palomar Medical Technologies USA (Listed) Cynosure 24 Jun 13 287

10 Epocal Canada (Private) Alere 04 Feb 13 242

Other 1,624

Total 6,468

Source: EvaluateMedTech™ (23 SEP 2013)

$36bn $13bn $50bn $77bn $46bn

209

164

253246

224

0

50

100

150

200

250

300

0

50

100

150

200

250

300

350

2008 2009 2010 2011 2012

De

al C

ou

nt

De

al V

alu

e (

$b

n)

Count of Pharma M&A Deals vs. Total Pharma M&A Value (2005 - 2009) Source: EvaluatePharma® (30 APR 2010)

Deal Value Deal Count

M&A Deal Value Falls by a Startling 79% in H1 2013; Deal Count Also DropsEvaluateMedTech™ found that total deal values from M&A of medtech companies decreased by a shocking 79% to $6bn in H1 2013, compared with $31bn in H1 2012. The number of deals also declined significantly, by 15%, with 95 deals closed in H1 2013 vs. 112 in H1 2012. The largest deal in H1 2013, and the only one worth over $1bn, was the acquisition of contraception specialist Conceptus by Bayer. The second half of the year has, however, started more positively thanks to the recent closing of Valeant’s $8.7bn acquisition of Bausch + Lomb and Baxter’s $3.9bn acquisition of Gambro.

2005FUJ [YAM] ($20.8bn)SAN [DAI] ($15.4bn)

2006SCH [BAY] ($21.3bn)

PFE Cons [JNJ] ($16.6bn)

2007Organon [SGP] ($15.6bn)

MEDI [AZN] ($15.6bn)Serono [Merck] ($13.8bn)

2008Alcon [NVS] ($10.4bn)

2009WYE [PFE] ($68.0bn)

DNA [Roche] ($46.8bn)SGP [MRK] ($41.1bn)

Target [Acquiror] (Deal Value)

173% Growth

$36bn $13bn $50bn $77bn $46bn $31bn $6bn

209

164

253246

224

112

95

0

50

100

150

200

250

300

0

10

20

30

40

50

60

70

80

2008 2009 2010 2011 2012 H1 2012 H1 2013

De

al

Co

un

t

Deal

Valu

e (

$b

n)

Count of Medtech M&A Deals vs. Total Medtech M&A Value (2008 - H1 2013) Source: EvaluateMedTech™ (23 SEP 2013)

Deal Value ($bn) Deal Count

2009 AM Optics [ABT] $2.8bn

Target [Acquiror] (Deal Value)

Note: Analysis based on closing date of deal.*Alcon & Genzyme included in analysis as >25% of company sales are derived from medtech.

2010Alcon* [NVS] $28bnev3 [COV] $2.6bn

2011Genzyme* [SAN]: $20.1bn

Alcon* [NVS] $9.6bnBeckman C [DHR] $6.8bn

Kinetic C (P. Equity) $6.1bn

H1 2012Synthes [JNJ] $19.7bn

2008Alcon* [NVS] $10.4bn

Respironics (Philips) $5.1bnVentana (Roche) $3.4bn

S. Goldway (Philips) $3bn

2012Synthes [JNJ] $19.7bn

Gen-Probe [HOL] $3.7bn

18

M&A Deal Value Falls by a Startling 79% in H1 2013; Deal Count Also Drops

EvaluateMedTech™ found that total deal values from M&A of medtech companies decreased by a shocking 79% to $6bn in H1 2013, compared with $31bn in H1 2012. The number of deals also declined significantly, by 15%, with 95 deals closed in H1 2013 vs. 112 in H1 2012.

The largest deal in H1 2013, and the only one worth over $1bn, was the acquisition of contraception specialist Conceptus by Bayer. The second half of the year has, however, started more positively thanks to the recent closing of Valeant’s $8.7bn acquisition of Bausch + Lomb and Baxter’s $3.9bn acquisition of Gambro.

Note: Analysis based on closing date of deal.

*Alcon & Genzyme included in analysis as >25% of company sales are derived from medtech.

M&A Analysis: 2008 to H1 2013

19Co

pyr

igh

t ©

201

3 Ev

alu

ate

Ltd

. All

rig

hts

res

erve

d.

Venture Financing Analysis: 2008 to H1 2013

Count of Medtech Venture Financing Deals & Value (2008 - H1 2013)

Year 2008 2009 2010 2011 2012 H1 2012 H1 2013

Deal Count 244 333 360 433 319 188 216

% Chg. 36% 8% 20% -26% 15%

Deal Value ($m) 3,119 3,605 4,502 4,480 3,845 2,337 2,481

% Chg. 16% 25% -1% -14% 6%

Top 10 Venture Financing Deals in H1 2013: Ranked on Deal Value

Company Country Financing Round Date Deal

Value ($m)

1 TearScience Ophthalmics USA Series Undisclosed 26 Feb 13 70

2 Proteus Digital Health Patient Monitoring USA Series F 01 May 13 63

3 Mevion Medical Systems Radiology USA Series Undisclosed 25 Jun 13 55

4 Natera In Vitro Diagnostics USA Series E 01 May 13 55

5 RTI Surgical Orthopedics USA PIPE 12 Jun 13 50

6 Nevro Neurology USA Series C 07 Mar 13 48

7 BioFire Diagnostics In Vitro Diagnostics USA Series Undisclosed 02 May 13 45

8 Avedro Ophthalmics USA Series D 05 Mar 13 43

9 EndoChoice Gastroenterology USA Series Undisclosed 04 Jan 13 43

10 ElectroCore Neurology USA Series A 09 Apr 13 40

Other 1,970

Total 2,481

Source: EvaluateMedTech™ (23 SEP 2013)

Primary Focus

Value of Venture Financing Expands 6% in H1 2013; Deal Count Increases 15%EvaluateMedTech™ found that in H1 2013 the total deal value of medtech venture financing increased by 6% to $2.5bn, whilst the number of venture financing deals increased by 15% to 216.Morrisville, North Carolina-based TearScience’s $70m funding was the largest single round seen in the first half of 2013. The cash is earmarked for commercialisation of the company’s dry eye therapy. This chimes with the relatively rapid growth seen in the ophthalmics sector.

$3,119m

$3,605m

$4,502m $4,480m

$3,845m

$2,337m$2,481m

244

333360

433

319

188216

0

100

200

300

400

500

600

700

0

1000

2000

3000

4000

5000

2008 2009 2010 2011 2012 H1 2012 H1 2013

De

al C

ou

nt

De

al V

alu

e (

$m

)

Count of Venture Financing Deals vs. Total Venture Financing Value (2008 - H1 2013) Source: EvaluateMedTech™ (23 SEP 2013)

Deal Value Deal Count

Note: Includes investments in medtech companies only. Does not include pharmaceutical or biotech companies. Includes Private Investment in Public Equity (PIPE).

H1 2013 vs.H1 2012

19

Value of Venture Financing Expands 6% in H1 2013; Deal Count Increases 15%

EvaluateMedTech™ found that in H1 2013 the total deal value of medtech venture financing increased by 6% to $2.5bn, whilst the number of venture financing deals increased by 15% to 216.

Morrisville, North Carolina-based TearScience’s $70m funding was the largest single round seen in the first half of 2013. The cash is earmarked for commercialisation of the company’s dry eye therapy. This chimes with the relatively rapid growth seen in the ophthalmics sector.

Note: Includes investments in medtech companies only. Does not include pharmaceutical or biotech companies. Includes Private Investment in Public Equity (PIPE).

Venture Financing Analysis: 2008 to H1 2013

20Co

pyr

igh

t ©

201

3 Ev

alu

ate

Ltd

. All

rig

hts

res

erve

d.

Enterprise Value & Focus Analysis: 2013 Latest vs. 2012

Top 20 Medtech Companies in 2013 (2018 Sales: >$1bn): Ranked by Enterprise Value

% '13 Sales

Company Country Medtech 2012 Latest % Growth 2012 Latest % Growth

1 General Electric USA 8% 507 497 -2% 20.99 23.78 +13%

2 Johnson & Johnson USA 40% 190 240 +26% 70.10 88.57 +26%

3 Roche Switzerland 22% 183 231 +26% 199.59 250.45 +25%

4 Novartis Switzerland 12% 165 188 +14% 63.30 76.20 +20%

5 Sanofi France 2% 135 139 +3% 45.79 47.96 +5%

6 Siemens Germany 18% 101 122 +21% 102.69 117.24 +14%

7 Bayer Germany 4% 87 102 +17% 93.63 111.50 +19%

8 3M USA 17% 65 83 +27% 92.85 118.60 +28%

9 Medtronic USA 100% 41 53 +30% 40.79 53.58 +31%

10 Abbott Laboratories USA 45% 109 52 -52% 30.98 34.87 +13%

11 Danaher USA 47% 42 50 +20% 55.90 69.76 +25%

12 Baxter International USA 38% 39 46 +17% 66.66 71.78 +8%

13 Kimberly-Clark USA 8% 38 42 +11% 84.43 95.69 +13%

14 Valeant Pharmaceuticals Canada 18% 27 41 +52% 56.44 99.20 +76%

15 Thermo Fisher Scientific USA 25% 29 39 +33% 63.78 91.11 +43%

16 Fresenius Germany 23% 34 35 +4% 14.23 15.08 +6%

17 Philips The Netherlands 31% 25 34 +39% 26.48 33.07 +25%

18 Toshiba Japan 6% 30 32 +5% 23.55 24.35 +3%

19 Covidien USA 100% 30 31 +1% 57.74 60.45 +5%

20 Allergan USA 14% 26 26 -1% 91.64 88.77 -3%

Total Top 20 1,903 2,083 +9% avg. +20%

Source: EvaluateMedTech™ (23 SEP 2013)

Enterprise Value ($bn) Share Price ($ ADR)

$497bn

$240bn $231bn

$188bn

$139bn$122bn

$102bn$83bn

$53bn $52bn

+13%

+26% +25%

+20%

+5%

+14%

+19%

+28%

+31%

+13%

+0%

+5%

+10%

+15%

+20%

+25%

+30%

+35%

+40%

0

100

200

300

400

500

600

Gen

era

lE

lectr

ic

Joh

nson

&Joh

nson

Ro

che

No

vart

is

Sa

no

fi

Sie

men

s

Ba

yer

3M

Med

tro

nic

Ab

bo

ttL

ab

ora

tori

es

Sh

are

Pri

ce P

erf

orm

an

ce Y

TD

(%

)

En

terp

rise V

alu

e (

$b

n)

WW Ranking on Enterprise Value in 2013 (Latest)Source: EvaluateMedTech™ (23 SEP 2013)

General Electric Number 1 in Latest Enterprise Value RankingsEvaluateMedTech™ found US giant General Electric to be the largest company by enterprise value operating in the medtech space, with a figure of $497bn. General Electric is expected to derive 8% of its 2013 revenues from its medtech segment.The analysis includes only medtech companies that are forecast to have sales in excess of $1bn in 2018. The analysis reveals the extent to which large diversified companies operate within the medtech space. Only two of the top 20 companies derive more than 50% of sales from medtech: Medtronic and Covidien. Even Johnson & Johnson, the clear market leader in medtech, only generates 40% of group sales from medtech.

Note: Includes companies with >$1bn medtech sales in 2018.Valuation based on share price close and valuation on 13th September 2013.

S&P 2013 YTD Return: +18%

20

General Electric Number 1 in Latest Enterprise Value Rankings

EvaluateMedTech™ found US giant General Electric to be the largest company by enterprise value operating in the medtech space, with a figure of $497bn. General Electric is expected to derive 8% of its 2013 revenues from its medtech segment.

The analysis includes only medtech companies that are forecast to have sales in excess of $1bn in 2018. The analysis reveals the extent to which large diversified companies operate within the medtech space. Only two of the top 20 companies derive more than 50% of sales from medtech: Medtronic and Covidien. Even Johnson & Johnson, the clear market leader in medtech, only generates 40% of group sales from medtech.

Note: Includes companies with >$1bn medtech sales in 2018.

Valuation based on share price close and valuation on 13th September 2013.

Enterprise value for Abbott drops YTD following the spin-out of AbbVie on 1 January 2013.

Enterprise Value & Focus Analysis: 2013 Latest vs. 2012

Evaluate’s Solutions for the Life Science IndustryAt Evaluate, our focus is on the business success of our clients.Our services are delivered via online subscriptions and through custom solutions. Contact us today to find out more.

Leader in consensus forecasts and analysis of pharma and biotech

� Consensus sales forecasts of leading equity research analysts, currently to 2018

� Must-have data in an integrated, standardized platform

� Interactive NPV discount cash flow model for asset valuation and Calendar of Events tool

A new standard in medtech industry analysis via a consensus view

� Consensus sales forecasts of leading equity research analysts, currently to 2018

� Simplified medtech classification system correlated to FDA and company specified segments

� Six integrated FDA databases and EU CE Marks

High quality global clinical trial intelligence linked to essential information

� Full records of ClinicalTrials.gov, EudraCT and a Japanese Clinical Trials data source

� Integrated with in-depth EvaluatePharma product and indication information

� Unique search fields for custom analysis and reporting

Award-winning commentary and analysis by industry experts

� Daily round up of share price movements

� Future market events that will impact product value

� Searchable news and commentary powered by high quality Evaluate data

For more information please visit www.evaluategroup.com. On Twitter: @evaluate, @evaluatepharma, @evaluatemedtech, @epclinicaltrial, @epvantage.

21Co

pyr

igh

t ©

201

3 Ev

alu

ate

Ltd

. All

rig

hts

res

erve

d.

Evaluate – Headquarters – Evaluate Ltd, 11-29 Fashion Street, London E1 6PX United Kingdom

Tel: +44 (0)20 7377 0800 – Fax: +44 (0)20 7539 1801

Evaluate – North America – EvaluatePharma USA, Inc., 15 Broad Street, Suite 401, Boston, MA 02109 USA

Tel: 1-617 573-9450 – Fax: 1-617 573-9542

Evaluate – Japan – EvaluatePharma Japan KK, Tokyo, Japan

Tel: +81 (0) 80 1164 4754

www.evaluategroup.com

All intellectual property rights in this report remain that of Evaluate Ltd and/or its respective third party licensors. Whilst all reasonable steps have been taken to ensure that the datapresented are accurate, Evaluate Ltd cannot accept responsibility for errors or omissions. Neither does Evaluate Ltd warrant the accuracy, merchantability or fitness for a particular purpose of the data. Nothing in the reports shall constitute investment, financial or legal advice and the contents of the reports are provided for information purposes only. The data is not intended to amount to advice and should not be used as a determining factor in any investment decision. This report may not be lent, resold, hired out or otherwise disposed of by way of trade in any form of binding or cover other than that in which it is published, without the prior written consent of Evaluate Ltd. Copyright © 2013 Evaluate Ltd. All rights reserved.

Complimentary copies of our World Preview 2013, Outlook to 2018 Report can be downloaded at: www.evaluategroup.com/MedTechWP2013

Evaluate is the trusted source for high quality commercial market intelligence and exclusive consensus sales forecasts to 2018. Our services are EvaluatePharma®, EvaluateMedTech™ and EvaluateClinicalTrials™. Our award-winning editorial arm, EP Vantage, leverages our market intelligence and analysis to cut through the noise, providing daily opinion and insights. Evaluate’s services give you the insights you need to ask the right questions and get the right answers. That’s intelligence you can act on. For more information visit: www.evaluategroup.com. On Twitter: @evaluatepharma, @evaluatemedtech, @epclinicaltrial, @epvantage.

EVALMTWP2013

General inquires about this report: Christine Lindgren Tel: 1-617-573-9458 Email: [email protected]