DIGITAL TRANSFORMATION IN 10 BUILDING...

4

october 2012 | TO BOOST CUSTOMER EXPERIENCE AND ROE DIGITAL TRANSFORMATION IN 10 BUILDING BLOCKS

-

Upload

phungduong -

Category

Documents

-

view

217 -

download

0

Transcript of DIGITAL TRANSFORMATION IN 10 BUILDING...

october 2012|

TO BOOST CUSTOMER EXPERIENCE AND ROE

DIGITAL TRANSFORMATION IN 10 BUILDING BLOCKS

1 | D IGITAL TRANSFORMATION IN 10 BUILDING BLOCKS

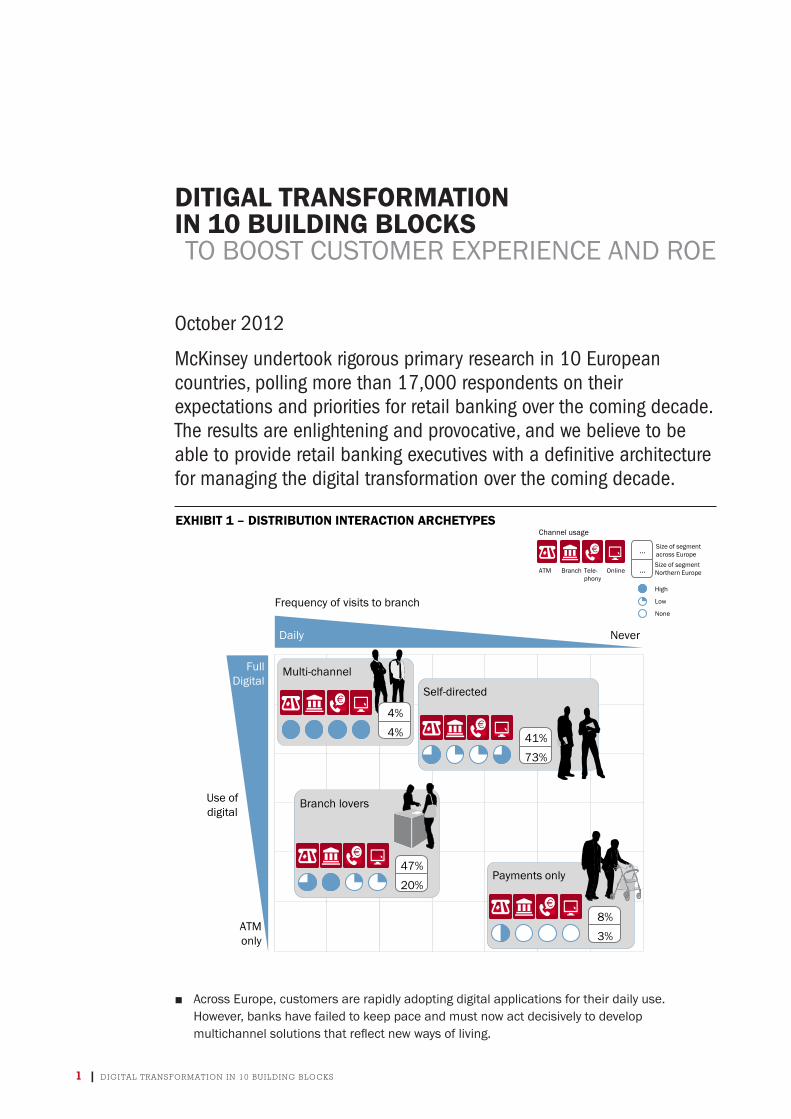

Frequency of visits to branch

Daily Never

Payments only

8%

3%

Branch lovers

47%

20%

Self-directed

41%

73%

Multi-channel

4%

4%

Use of digital

ATM only

Full Digital

Size of segment across Europe Size of segment Northern Europe

…

…

Channel usage

None

Low

High

ATM Branch Tele- phony

Online

EXHIBIT 1 – DISTRIBUTION INTERACTION ARCHETYPES

■ AcrossEurope,customersarerapidlyadoptingdigitalapplicationsfortheirdailyuse.However,bankshavefailedtokeeppaceandmustnowactdecisivelytodevelopmultichannelsolutionsthatreflectnewwaysofliving.

DITIGAL TRANSFORMATI0N IN 10 BUILDING BLOCKS TO BOOST CUSTOMER EXPERIENCE AND ROE

October 2012

McKinsey undertook rigorous primary research in 10 European countries, polling more than 17,000 respondents on their expectations and priorities for retail banking over the coming decade. The results are enlightening and provocative, and we believe to be able to provide retail banking executives with a definitive architecture for managing the digital transformation over the coming decade.

DIGITAL TRANSFORMATION IN 10 BUILDING BLOCKS | 2

summar y

Enablers 8. Outsource commodity technology and upgrade core systems (e.g., CRM) 9. Build digital marketing and sales skills (Big data, pricing, SEO, etc.) 10. Familiarize and educate employees and clients on digital banking; address security issues

Transforming to a Digital Bank

Offering 1. Launch new digital

services and products 2. Make current product

offer digital proof (rationalize portfolio, digital pricing)

3. Seamlessly integrate external applications and products with core offering (i.e., insurance)

Channel 4. Transform branch

footprint and performance

5. Invest in mobile and social media channels and expand functionalities of existing digital channels)

Process 6. Enable multi-channel

sales, transactions and services

7. Enable Remote advise and troubleshooting

EXHIBIT 2 – BUILDING BLOCKS FOR A DIGITAL TRANSFORMATION

■ Wehaveidentifiedfourdistinctcustomersegments:self-directed,multichannelusers,branchlovers,andATM/cardusers.(Exhibit1).

■ Althoughbranchloversarecurrentlythelargestsegment(47percentofsample),itisexpectedthattheself-directedsegment,whichismostadaptedtotheonlineworld,willaccountfor80percentofcustomersin10years.InNorthernEurope,theyalreadydoso.

■ Theriseoftheself-directedcustomersegmentcreatesauniqueopportunity forbankstoimproveeconomics

(20to40percentlesscostand2to5percentmarketsharegainforfirstmovers),allowingbankstoreducetheircost/incomeratiobyupto20p.p.

■ However,adigitaltransformationofcustomerexperiencesandbusinessmodelsisnecessary,requiringbankstooverhaultheirbusinessmodels.Thosethatsucceedwillreaprichrewards.

■ Basedonsegmentpreferencesandtheirimpactonbankeconomics,wehaveidentified10journeysthatbanksmustundertaketocapturevalueandboostearnings.(Exhibit2).

Makingthedigitaltransformationarealityrequiresathree-stepapproach,accompaniedbyactionstoensuresmoothimplementationandsustainedimpact.

■ Step1.Setyourmultichannelambition:banksmustbaselinecustomers’currentbehavior,identifycostreductionpotential,andprioritizetransformationjourneys.

■ Step2.Launch10digitaltransformationjourneystoboostcustomerexperienceandretailbankingeconomicsandputenablersinplaceforasuccessfultransformationjourney.

■ Step3.Monitordigitalbehaviorsandbepreparedtochangegearsswiftly.

Copyright © 2012

NopartofthispublicationmaybecopiedorredistributedinanyformwithoutthepriorwrittenconsentofEFMAand/orMcKinsey&Company.

Efmawww.efma.com

McKinsey & Companywww.mckinsey.com

Please contact the authors for access to more detailed consumer research, case examples for the building blocks, and/or to let us have your comments and feedback

VitoGiudici,Director,Milan [email protected]

RadboudVlaar,Principal,Amsterdam [email protected]

RemcoVlemmix,Principal,Amsterdam [email protected]

PhilippSiebelt,AssociatePrincipal,Cologne [email protected]

EwoutvanJarwaarde,EngagementManager,Amsterdam [email protected]