Skilled Labor Shortage in the Construction Industry? It's ...

35

Skilled Labor Shortage in the Construction Industry? It's Not Demonstrated in the Numbers Dale L. Belman School of Human Resources and Labor Relations Michigan State University Professor Belman can be reached at the School of Human Resources and Labor Relations, South Kedzie Hall, Rm 408 368 Farm Lane, Michigan State University East Lansing, Ml 48824 and at [email protected] Page 1of27

Transcript of Skilled Labor Shortage in the Construction Industry? It's ...

Skilled Labor Shortage in the Construction Industry?

It's Not Demonstrated in the Numbers

Dale L. Belman

School of Human Resources and Labor Relations

Michigan State University

Professor Belman can be reached at the School of Human Resources and Labor Relations, South Kedzie Hall, Rm 408 368 Farm Lane, Michigan State University East Lansing, Ml 48824 and at

Page 1of27

Page 2 of 27

Summarv1

Despite the construction industry's slow recovery from the Great Recession, some

construction stakeholders have expressed concern that the industry is facing an imminent

shortage of skilled workers. These concerns reflect the industry's long experience with wide

fluctuations in construction activity and the demand for construction workers. Even if

construction labor markets are not currently tight, stakeholders can be concerned with whether

in the near term future, one to two years, increased demand for construction will cause the

need for construction workers to rapidly outstrip the availability of qualified employees.

This report examines the current state of construction labor markets with respect to the

balance between the supply and demand for labor. Building on the work of Veneri {1999) and

Barnow, Trutko and Piatak (2013) we examine data on employment, job openings,

unemployment and wages since 2000. Although there are some indications that the

construction industry is coming out of the Great Recession, its recovery lags the recovery of the

overall economy. Specifically,

• Employment remains well below the levels of 2001-2006 and employment growth is

only slightly stronger than in the economy as a whole. As a result, there is a pool of

more than one million experienced construction workers who are either not currently

working or have found work in other industries. Such pools of experienced workers are

present not only for construction as a whole, but also for trades such as iron workers,

electricians and plumbers/pipefitters.

• Data on job openings and help wanted advertisements indicate that, although the

demand for construction workers has improved relative to its level during the Great

Recession, it is only returning to its historic relationship to the private economy in 2013.

Further, while the ratio of unemployment to help wanted advertising suggests that

there are 2.3 individuals actively seeking employment for each job advertised in the

private economy, the ratio in construction is 10 individuals actively seeking employment

for each job advertised.

• Unemployment among construction workers remains high both in its level and in

comparison to the entire the labor force. Although down from the high levels during

the Great Recession, unemployment among construction workers was 13.9% in 2012. In

addition, construction workers remain twice as likely to be unemployed than workers in

the entire labor force. Prior to the great recession, construction workers were only 70%

more likely to be unemployed.

1 The author of this report would like to thank Amy Tracy Wells and Ralph Gentile for valuable comments on earlier

versions of the report. Particular thanks to Carey Peters of the Construction Labor Research Council for providing OES data and comments. Any errors are the responsibility of the author.

Page 3 of 27

• An important indicator of tightening labor markets is rapidly rising wages. Data from

the Occupational Employment Survey and the Current Employment Survey indicate that

wage growth is no faster in construction, and somewhat slower in some trades, than in

the entire labor force. There is also no evidence that employers are required to pay

more for better skilled trades workers.

In sum, although there is evidence that the construction industry is slowly recovering from the

Great Recession, it remains far below the level of employment achieved between 2000 and

2006. The employment, job openings and unemployment data support the view that there is a

large pool of experienced workers available to the construction industry when the industry has

the jobs for those workers. The similarity of the pace of increase in construction wages and all

wages also suggests that the demand for construction labor is not outstripping its supply.

Page 4 of 27

Skilled Labor Shortage in the Construction Industry? It's Not Demonstrated in the Numbers

Introduction:

Construction industry stakeholders: employers, workers and owners (those who pay to

have buildings and infrastructure constructed), face wide fluctuations in demand. A boom in

construction today can quickly turn into a slump; and slumps can, in a relatively short period,

turn back into a boom. The industry is recovering from the Great Recession of 2007 - 2009 and

there is a steadily increasing volume of work in some construction sectors, notably energy and

energy related work. Evidence of a boom in construction spending is less evident in other

sectors of construction, but construction activity may be moving back toward a more normal

level of activity from the low levels during the Great Recession.

The prospective increase in construction spending has raised concerns among

stakeholders about whether there is an emergent shortage of skilled construction labor. This

concern derives both from past experience in obtaining labor during peaks in construction

spending and the national discussion of whether there is a shortage of skilled blue collar and

technical labor. Steven Sand her, chief executive officer of the Associated General Contractors

reflected this concern in stating,

"Between the challenges of attracting new recruits and retaining out-of-work ones, there aren't that many skilled workers waiting for a call-back in many parts of the country. If the industry continues to add

jobs, it won't be long before contractors in some parts of the country are scrambling to find enough skilled workers to meet demand." 2

2 From The Construction Index, Wednesday, July 3, 2013

Page 5 of 27

Similar concerns are expressed by the associate director of the Associated Builders and

Contractors, Geoffrey Burrs, in which he indicates that, given the prospective 32%

growth in demand for construction workers from 5.6 in 2013 to 7.4 million in 2020, a

guest worker program was needed to address future construction labor shortages. 3 4

Such concerns are finding regular expression in industry and national publications and,

in their regular appearance, creating an accepted view which, to date, has not been

based on a close analysis of construction labor markets.

This report examines national data on construction labor to determine whether

there is likely to be shortages of construction labor both in the near term, the next one

to two years, and the longer term, three to five years. Using national data on

employment, job openings unemployment, and compensation since 2000, we find that

the construction industry has yet to recover from the Great Recession and that there is a

pool of experienced construction workers who are either unemployed, underemployed

or have moved to other industries. Employment in construction remains almost 2.2

million workers lower than its peak in the middle of the last decade; unemployment

remains around 10% of the labor force even at the height of the construction season;

there are 10 construction workers for every job opening in the industry while the

economy wide ratio is 2 workers per opening.

3 Letter from Geoffrey Burr to Patrick Leahy, chair of the Senate Judiciary committee sent on May 14, 2013, see

http://www.abc.org/Porta ls/1/Documents/Newsl ine/2013/Senate Judiciary Immigration Letter ABC.pdf 4 As will be developed in section on employment, if the BLS projection is accurate, it will take almost seven years to

return close to the 2007 level of employment in the construction industry.

Page 6 of 27

The data suggest that the normal operation of construction labor markets and

actions by construction stakeholders and government to improve construction training

systems will be able to meet the foreseeable needs of construction labor. There is a

sufficient pool of immediately available workers to meet the needs of the industry over

the next one to two years. Current projections of labor force demand out to 2020 also

do not suggest that demand for construction workers will overwhelm the capacity of

construction labor markets to provide for that demand. BLS projections of demand for

construction workers through 2020 indicate that peak demand for labor will be less than

the number of workers in the construction labor force in 2005-2007. Even the highest

projections of non-residential labor force requirements suggest that peak demands for

construction labor will be no more than 13% above the level of 2005-2007.

As national demand for construction trade labor will not require exceptional

growth in the construction labor force, market processes should operate to reallocate

labor to meet the needs of the construction industry. Increased demand for trades

workers in localities and trades will, by raising wages and benefits, induce both an

increase in hours among incumbent workers and movement of those workers to

locations with better employment opportunities. In combination with increased

employment opportunities, improvements in compensation will also induce trades

workers who left the industry during the Great Recession to re-enter construction.

Higher compensation will attract individuals with skills that are compatible with

construction trades work to move into the construction industry and obtain the training

required to become fully skilled in their trade.

Page 7 of 27

While the normal operation of construction labor markets will address much of

the rising demand for construction labor, actions by construction stakeholders can do

much to speed the process of adjustment. Over the last five years, and possibly over

the last several decades, employers have become accustomed to obtaining workers with

needed skills when they were needed at a favorable price. These conditions will not

continue over the next four to five years. Successful operation in the developing

markets will require employers and owners to pay higher wages. These price signals are

central to bringing former construction employees back to the industry and in attracting

partially skilled employees from outside the industry. Employers will need to be willing

to hire lesser skilled employees and provide both formal and on-the-job training to bring

the employees up to desired levels of efficiency. Owners will no longer be able to count

on bids coming in below engineering estimates and will need to allow for increasing

labor and materials costs in their planning process.

Rather than view the improvements in construction labor markets as an

impending crises, construction stakeholders can use the strengthening of the market as

an opportunity to create a sustainable and highly skilled construction labor force which

is attractive to the quality of worker needed into the future . Emerging conditions can be

used to revitalize proven construction training programs. The industry has long

complained about not being able to attract better educated young workers. In

combination with strong employment opportunities and training, rising wages could

make construction a career of choice for capable, well educated but under-employed

Page 8 of 27

younger workers. Emerging improvements in the construction industry and labor

markets provide an opportunity to be grasped if the industry has the vision to do this.

What is a Labor Shortage?

There is no universal definition of a labor shortage. Barnow, Trutko and Piatak (2013) suggest

that the term "labor shortage" sometimes refers to an absolute shortfall in the number of

workers in a labor force while at other times it refers to a mismatch between worker

qualifications and the jobs which are available. Building on earlier analytic work on labor supply,

they define a labor shortage as

"A sustained market disequilibrium between supply and demand in which the quantity of workers demanded exceeds the supply available and willing to work at a particular wage and working conditions at a particular place and point in time." (pg. 3)

A critical element of this definition is that markets return to equilibrium slowly, resulting in an

ongoing excess of demand for workers over the supply of workers. The delays in a return to

equilibrium may be related to slowness in employer and employee recognition and response to

the shortage, or ongoing increases in the demand for workers.

What is the evidence for an occupational labor shortage? Analysts suggest that rapid

growth in employment and wages, large numbers of vacancies and low unemployment rates

are evidence of disequilibrium in the labor market. Veneri (1999) provides benchmarks for

employment, wages and unemployment

"For this analysis, occupations were evaluated to determine whether, for the 1992-97 period (for which data were available when the analysis was conducted), the occupation's employment growth rate was at least 50

percent faster than average employment growth, the wage increase was

Page 9 of 27

at least 30 percent faster than average, and the occupation's unemployment rate was at least 30 percent below average (in each case, "average" was defined by the total for all workers)." (pg. 18)

The benchmarks are established relative to economy wide developments. Rapid growth

in occupation wages is not in itself sufficient to indicate an occupational labor shortage; it is

rapid growth relative to the economy wide growth of wages.5 As Veneri indicates, the levels

she has established are arbitrary and open to discussion. This turns out to make little

difference in our analysis as construction's performance tends to be close to or below national

economic performance.

Employment

Employment and employment growth are central to assessing whether there is an

emerging labor shortage. Absent some absolute limit on the number of employees in an

occupation, labor shortages are marked by rapidly increasing employment. We consider

employment trends for the construction industry as a whole, as well as for trade occupations,

and compare these to national trends. If there is a shortage of construction employees, we

would expect to see rapid growth in construction employment relative to the balance of the

economy.

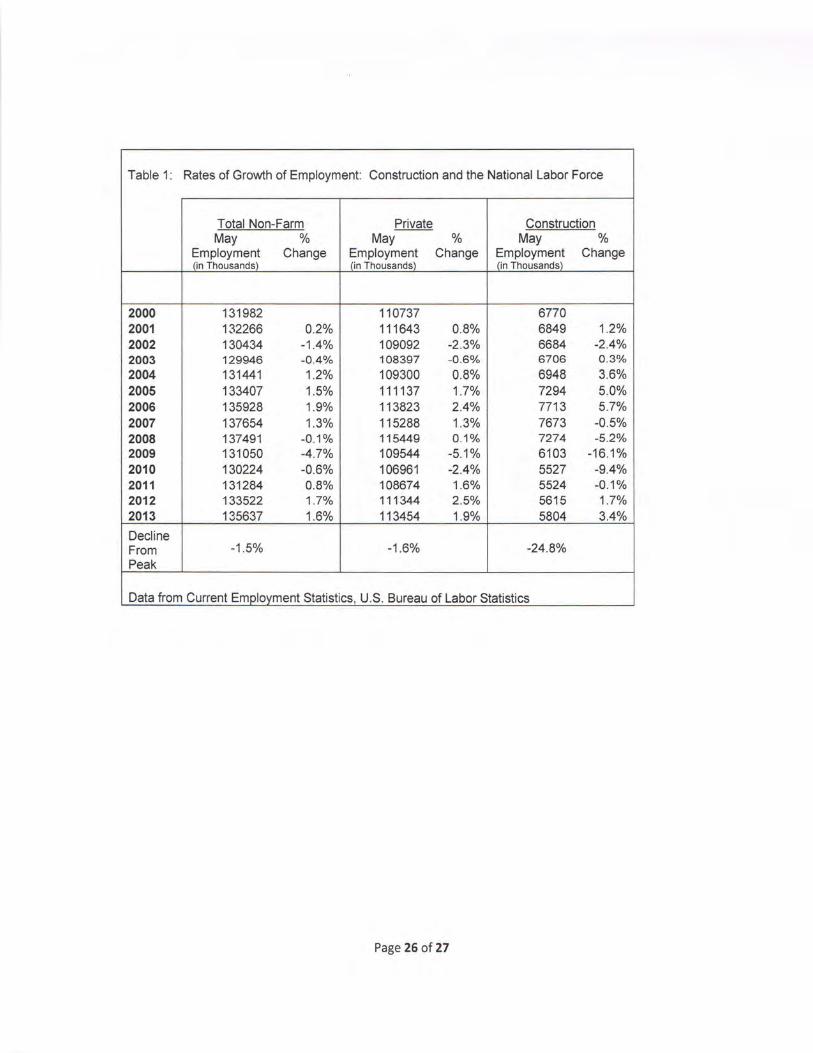

Table 1 compares employment levels and the annual rate of growth of employment for

the total non-farm labor force, the private labor force and the construction industry for 2000 to

2013 . We use the most current month available, May, rather than annualized employment, to

5 For example, during a period of rapid inflation, occupational wages are likely to grow rapidly without there being a shortage or surplus of labor. As wages through the economy will also be adjusting to inflation, benchmarking the occupations wages to national wages helps adjust for factors such as inflation.

Page 10 of 27

capture any recent trends in construction. The data is taken from the Current Employment

Statistics series and is limited to employees. For each labor force category, the left hand

column is total employment in millions, and the right hand column is the annual growth (or

decline) in employment in percent.

The construction industry was, and remains, deeply affected by the Great Recession.

Employment rose fairly steadily from 2000 to 2006, when it peaked at 7.7 million employees.

By 2010, the Great Recession had caused construction employment to decline 28%, to 5.5

million employees. By May 2013 modest improvements in the construction economy increased

construction employment to 5.8 million . Employment grew rapidly in the last year, by 3.4%,

but May 2013 employment remained 1.9 million, 24.8%, below the 2006 peak.

How does employment and employment growth in construction compare with the

balance of the economy? The Great Recession reduced employment in other sectors

substantially; employment in the private economy fell by from 115.5 to 109.5 million, or by

5.1%, between 2008 and 2009. The decline was not, however, as severe, and the recovery has

been more complete, than in construction. While construction employment remains almost

25% below its 2006 peak, employment in the private economy is 1.7% below its peak.

Construction has shown strong job growth over the last year. Jobs grew at a 3.4% rate

over the last year as construction added almost 200,000 employees. This compares favorably

with job growth in the private sector, 1.9%, or in the private and public sectors, 1.6%. However,

in the context of a sector which also suffers from very fast job decline, construction lost jobs at

more than three times the rate of the private economy in 2009, and remains almost two million

Page 11of27

employees below its peak employment in the decade of the 2000s. This means that, even if the

increased pace of job growth of the last year continues into the foreseeable future, the supply

of experienced construction workers is unlikely to be exhausted in the next two years. 6

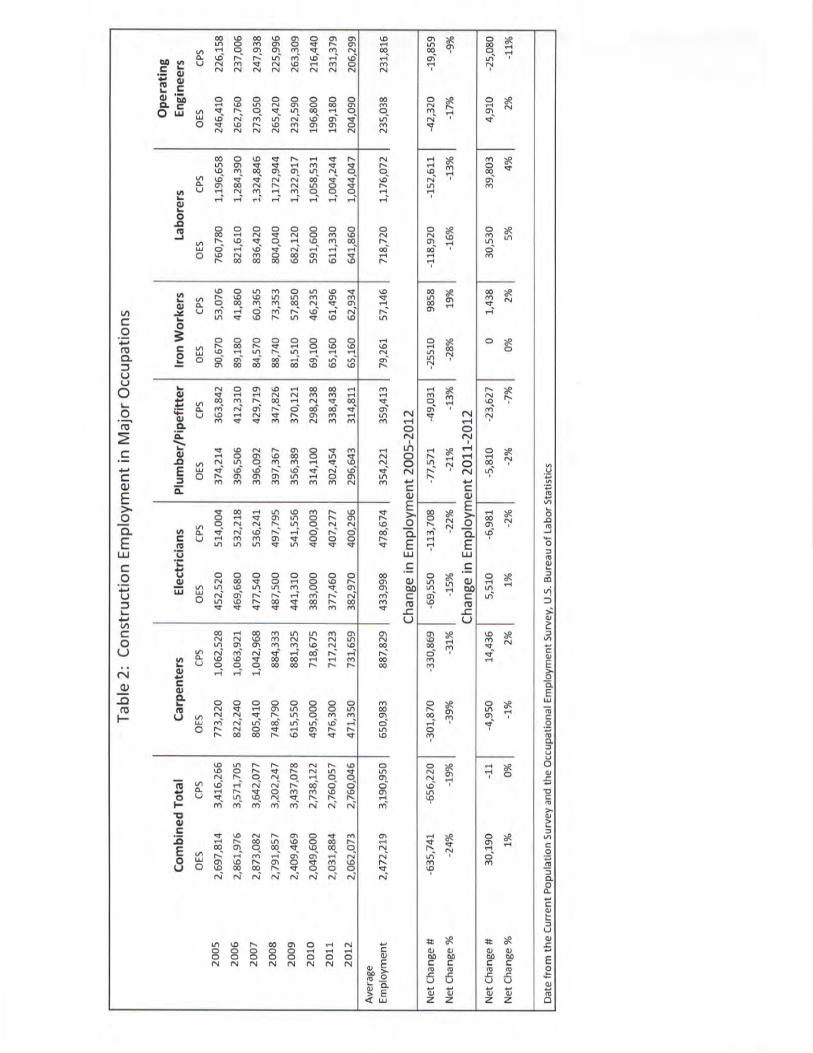

Employment by Trade

Issues with labor shortages in construction tend to be focused on specific highly skilled

trades such as pipefitters, electricians and welders. We consider the employment of

carpenters, electricians, plumbers/pipefitters, iron workers, laborers and operating engineers

from 2005 to 2012 in Table 2. Data from both the Occupational Employment Statistics (OES), a

survey of employers, and the Current Population Survey (CPS), a survey of individuals, are in the

left and right hand columns for each trade respectively. 7 The first set of columns combines the

data from the six trades to provide a consolidated portrait of employment from 2005. Turning

to the combined totals, both series show a large decline in employment between 2005 and

2012.8 These trades lost 635, 741 jobs (OES) and 656,220 employees (CPS), between 19% and

24% of all employment, over this period. Employment growth between 2011 and 2012 was

6 Construction employment has substantially greater variance than employment in the broader economy. While private sector employment grew between 1.3% and 2.4% between 2004 and 2007, construction grew between 3.6% and 5.7%. Similarly, the declines in construction are far more severe than the balance of the economy. While the largest annual decline in employment in the private sector during the great recession was 5.1%, construction employment fell by 16.1% in that year. The higher rate of growth of construction employment in 2012-2013 is then consistent with the greater variance of construction employment and may not be indicative of unusually fast growth relative to the broad economy. 7 The OES surveys employers about the number of positions in a particular occupation at that employer. The CPS

surveys households and collects, in addition to a variety of labor market measures, the occupation in which the

respondent is employed. Differences in concepts and surveys result in differences between the levels of

employment reported by the OES and CPS. These differences have been a subject of study and debate for some

years. In this instance, the trends in the two series are similar and provide a parallel understanding of changes in

construction employment and jobs.

8 Because employer was substantially greater in 2006 and 2007 than 2005 for most of the trades in Table 2, the

absolute and relative decline would have been greater had we measured against either of these years.

Page 12 of 27

weak, between 0% and 1% depending on the series used. Although large employment declines

occurred in all of the trades reported in Table 2, not all trades suffered equally. Between 31%

and 39% of carpentry employment was lost, operating engineers lost between 9% and 17% of

employment. Despite these differences, each of the trades' employment levels are currently

well below those of the mid-2000s. The pool of experienced workers has certainly been

reduced by retirements and some workers have found permanent employment in other

industries. Still, there appears to be a substantial pool of experienced construction workers

who are available to the industry if employment were available.

Job Openings

Job openings are a direct measure of labor shortages, indicating the degree to which

jobs are going unfilled . The two main sources of job openings data are the Job Openings and

Labor Turnover (JOLTS) survey of the U.S. Bureau of Labor Statistics and the Help Wanted On

Line (HWOL) data collected by the Conference Board. The former is derived from an employer

survey, the latter on the collection and analysis of on-line help wanted advertisements.

Neither, in its publicly available form, provides detailed information on trades occupations, but

both provide information on the construction industry as a whole.

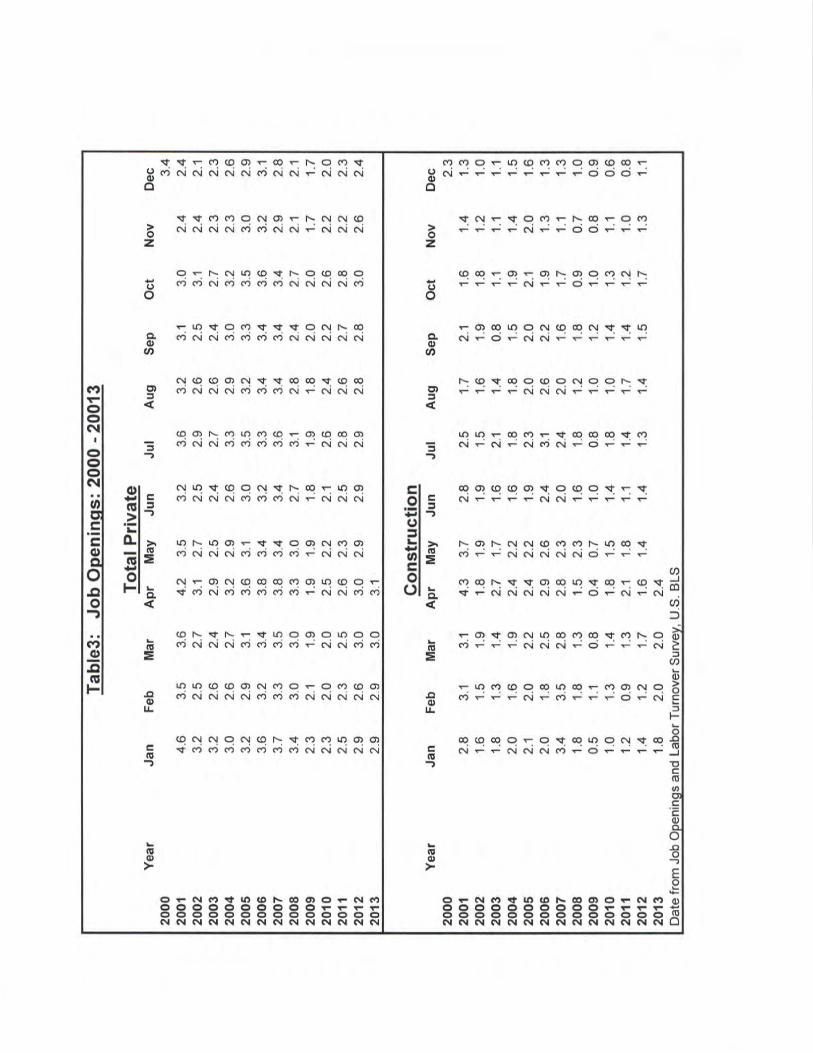

Table 3 and the accompanying chart summarize JOLTS data on job openings in the

private sector and construction from January, 2001 to April 2013. The JOLTS rate is a ratio of

the number of job openings to the sum of current employment plus job openings expressed as

a percent.9

Higher rates indicate more jobs are going unfilled. The severity of current unmet

9 The job openings rate is the number of job openings on the last business day of the month divided by the sum of the number of

Page 13 of 27

labor demand can be measured by comparing current job opening rates in construction to past

rates and by comparing the growth of job opening rates in construction with their growth in the

private economy.

The red line in Chart 1 shows the job openings rate as a percent of employment in

construction between 2001 and 2013. Current job openings in construction, at the far right of

the chart, are considerably below job openings in early 2001 and job openings in 2006 and

2007. Although greatly improved over the level of job openings during the Great Recession,

job openings remain well below their levels when construction activity was expanding rapidly.

Comparison of construction job openings to those in the private sector requires

benchmarking. The JOLTS ratio in construction is typically lower than the JOLTS ratio in the

private economy as a whole. Between 2001 and 2006, there were .64 openings in construction

for each job opening in the private sector. The ratio to date for 2013 is similar, .69, while the

average for 2012 and 2013, .54, is below the historic ratio. While construction had fewer than

normal job openings since 2012, there is evidence that demand for construction workers has

improved in 2013. However, this has only moved construction back toward its historic ratio

prior to the Great Recession. Construction labor markets are not tight relative to the private

economy.

The Conference Board' s Help Wanted On Line {HWOL) provides an alternative measure

of job openings. The June 5 press release (#5673) reported that 112,500 new help wanted ads

appeared for construction in May 2013 . This was up by 1,300 from the 111,200 ads in April and

employees who worked during or received pay for the pay period that includes the 12th of the month and the number of job openings on the last business day of the month.

Page 14 of 27

by 27,000 from May 2012. While the month to month increase is not large, the 31% increase

from the prior year is considerably above the 3.5% increase in all help wanted ads.

A second measure provided by the Conference Board suggests that, despite the rapid

increase in construction, the labor supply in construction is slacker than in most of the

economy. The Conference Board provides a supply/demand ratio, the number of individuals

who are unemployed to the number of help wanted ads. The ratio for the total workforce is 2.3;

that is, there are 2.3 unemployed workers actively seeking employment for every help wanted

ad. The ratio for construction is 10.3; that is, there are slightly more than ten construction

workers for every help wanted ad. This is consistent with a view that construction has a

considerable way to go before it recovers from the effects of the Great Recession. The increase

in demand is healthy, but considerable employment growth is needed to absorb those seeking

work and to return to prior levels of employment in construction.

Unemployment

Both the levels of unemployment, and the comparison of unemployment in the

construction industry to the national level of unemployment, are important benchmarks of

labor shortages. Veneri (1999) has suggested that unemployment rates which are 30 percent

lower than the national unemployment rate are consistent with the presence of a labor

shortage. While the unemployment data is less focused than desired, we have data on the

construction industry inclusive of trade and white collar employment.

The BLS calculates industry unemployment rates by asking the unemployed their last

industry of employment and then calculates the rate as the number of the unemployed who

Page 15 of 27

report an industry as their last industry of employment divided by the sum of employment and

unemployment in that industry. We compare the unemployment rate in construction with the

national unemployment rates of persons in the labor force 20 and older. We use age 20 and

older because the calculation of unemployment is limited to the experienced labor force, those

who have or have previously had a job. The experienced labor force in construct ion includes

very few individuals under the age of 20; therefore limiting the measures of national

unemployment to those age 20 and older improves the comparability of the unemployment

rates.

There is little evidence of an emerging labor shortage in the unemployment data (chart

2 and tables 4a and 4b). Construction unemployment in 2013 remains substantially above the

unemployment levels in construction between 2000 and 2006. While annual unemployment in

construction varied from 9.3 to 6.2% between 2000 and 2006, it ranged from 10.6% to 20.6% in

2008 to 2012. While unemployment in construction has declined considerably from its 2010

peak, unemployment in construction remained high, 13.9%, in 2012. The recent decline below

this level in April and May of 2013 appears to be a normal seasonal decline as the economy

moves into the construction season.

Comparison of unemployment in construction to unemployment in the U.S. labor force

also suggests that construction labor markets remain slack. While the annual rate of

unemployment in the labor force remained high at 7.4% in 2012, construction unemployment

was considerably above this at 13.9%. As Chart 2 shows, unemployment in construction has

historically run above unemployment in the broad economy. It is possible that construction

Page 16 of 27

labor markets might be very tight even if the construction unemployment rate is above the rate

for the labor force. We can adjust for this by considering the ratio of construction to national

unemployment. If this ratio is well below its "historical" level, there could be some concern

that construction labor markets are tightening. The ratio of construction unemployment to

national unemployment from 2000 to 2006 was 1.7, that is construction workers were 70%

more likely to report being unemployed than those in the private labor force. During the Great

Recession, this ratio rose to 2.3 and, in 2012, returned to 1.9. Between January and May 2013,

the ratio has averaged 2.0, that is construction workers are twice as likely to report being

unemployed as a typical worker. Construction unemployment remains above its historic

relationship with national unemployment and construction labor markets are lagging the broad

economy in recovering from the Great Recession.

Nothing in our results is consistent with an emergent near term shortage of

construction labor. The construction unemployment rate remains considerably above the

national unemployment rate. The ratio of the rates remains above the ratio prior to the Great

Recession. Further, the high unemployment rate suggests there are considerable numbers of

construction workers who are actively seeking employment at current wages but unable to find

employment.

Wages and Earnings

When demand and supply are out of equilibrium in competitive markets, they are

moved toward equilibrium by price adjustments. In instances when demand outstrips the

supply of employees in an occupation, the increase in the wage brings forth both an additional

Page 17 of 27

supply of labor and tamps down demand. Higher wages pull in employees who have left an

industry either for other work or are not working in the industry. It also encourages the current

labor force to work additional hours and those without requ isite skills to train so as to take

advantage of the higher wages. Given this market dynamic, wages in industries experiencing

labor shortages would be expected to rise considerably faster than wages through the economy

or among private sector employees.

We consider this with wage data from the Occupational Employment Survey (OES) and

the Current Employment Survey (CES) . The former is an annual survey which collects

information by occupation in May of each year. The latter is a monthly survey which collects

information by industry, but not by occupation. The OES data fits our purposes better than the

CES, but it is only available through May 2012, while the CES data is available through May of

2013 . Looking at both will provide information on wage trends in construction up to the very

recent past.

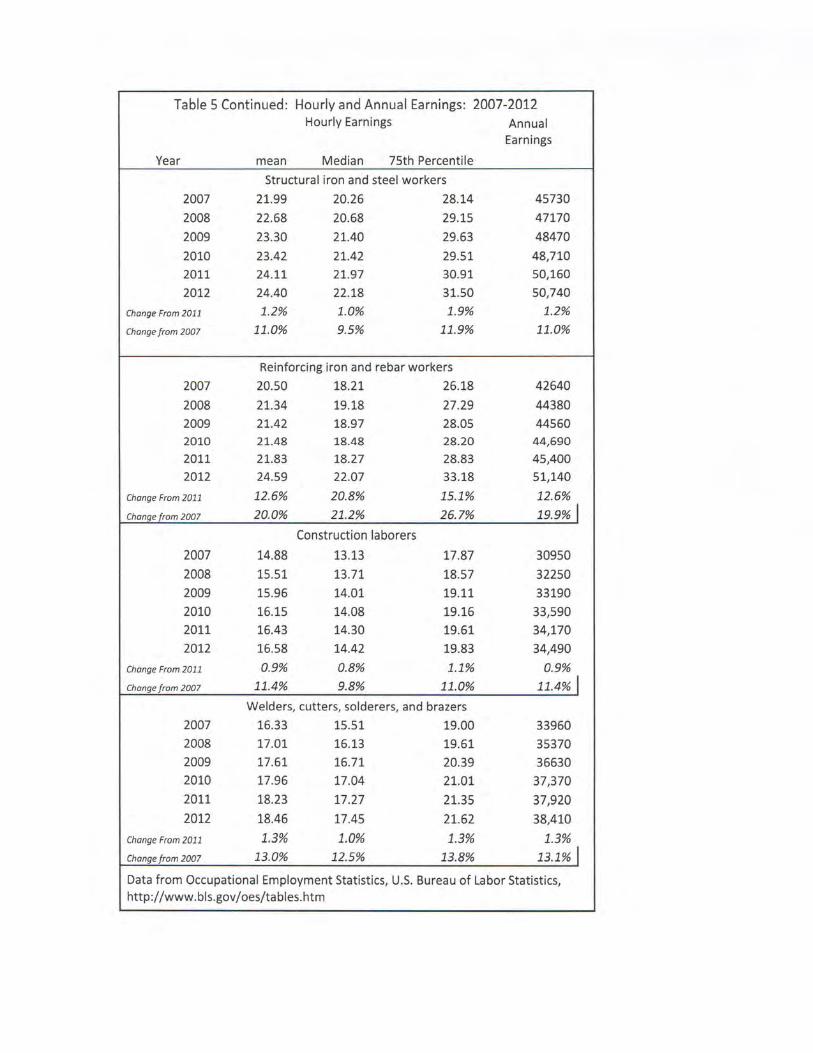

Information on mean and median hourly earnings as well as mean annual earnings for

all occupations and for several important construction occupations is found in Table 5. In

addition, the hourly wage at the 75th percentile of the wage distribution is included to

determine whether demand for the better skilled, and therefore better paid, employees is

causing wages at the 75th percentile to rise more rapidly than the typical wage. At the bottom

of each occupation's wage, there is a measure of the percent change in the wage since 2011

(the one year change) and since 2007.

Page 18 of 27

Initially considering all occupations, there is little difference in the measures of wage

change since 2011 or since 2006. Between 2011 and 2012 mean wages rose by 1.2% while

median wages rose by 0.8%. Mean annual earnings rose by 1.2% while earnings at the 75th

percentile rose by 1.3%. There is similarly little difference in the measures of wage change since

2006. Mean and annual wages rose by 12.5% while median wages rose somewhat more slowly,

at 10. 7%. Wages at the 75th percentile rose by 13.2%, suggesting that better skilled workers

received larger wage increases than typical employees.

With the exception of reinforcing iron and rebar workers, construction workers have not

done quite as well as the full labor force over either of these periods. 10 The one year and six

year rise in hourly and annual earnings of carpenters, electricians and construction laborers

have lagged behind the increases enjoyed by all occupations. While all occupations mean

hourly earnings rose by 1.2% between 2011 and 2012 and by 12.5% between 2007 and 2012,

carpenters mean hourly earnings rose by 0.4% and 7.9% since 2011 and 2007 respectively.

Similarly, electricians mean hourly earnings rose by 0.2% and 10.2% over the one and five year

period. Plumbers, pipefitters and steam fitters, construction laborers and structural steel

workers hourly earnings rose at rates very similar to those of all occupations. Individuals at the

75th percentile of the wage distribution did not do consistently better than the typical employee

in the trade.

10 The glaring exception to these conclusions is reinforcing iron and rebar workers whose earnings rose

dramatically in 2012. Although it is possible that this occurred, it is more likely to be a sampling issue. Further

evidence for issues with this data is that data from Current Employment Statistics for Poured Concrete Structures,

an industry which employs large numbers of rebar workers, does not show the same dramatic rise in 2012 or 2013 (see Table 6).

Page 19 of 27

As there is considerable discussion about shortages of welders, the OES data on

welder's earnings may be of particular interest. The evidence on hourly earnings suggests that

the increases in hourly earnings of welders have been very similar to that of all occupations in

the past year, and slightly better than all occupations since 2007. The gains relative to all

occupations falls far short of the 30% faster wage growth suggested by Veneri (1999) as

evidence of a labor shortage. Employment of welders, the first column in the table, has, similar

to other trades, declined substantially since 2007.

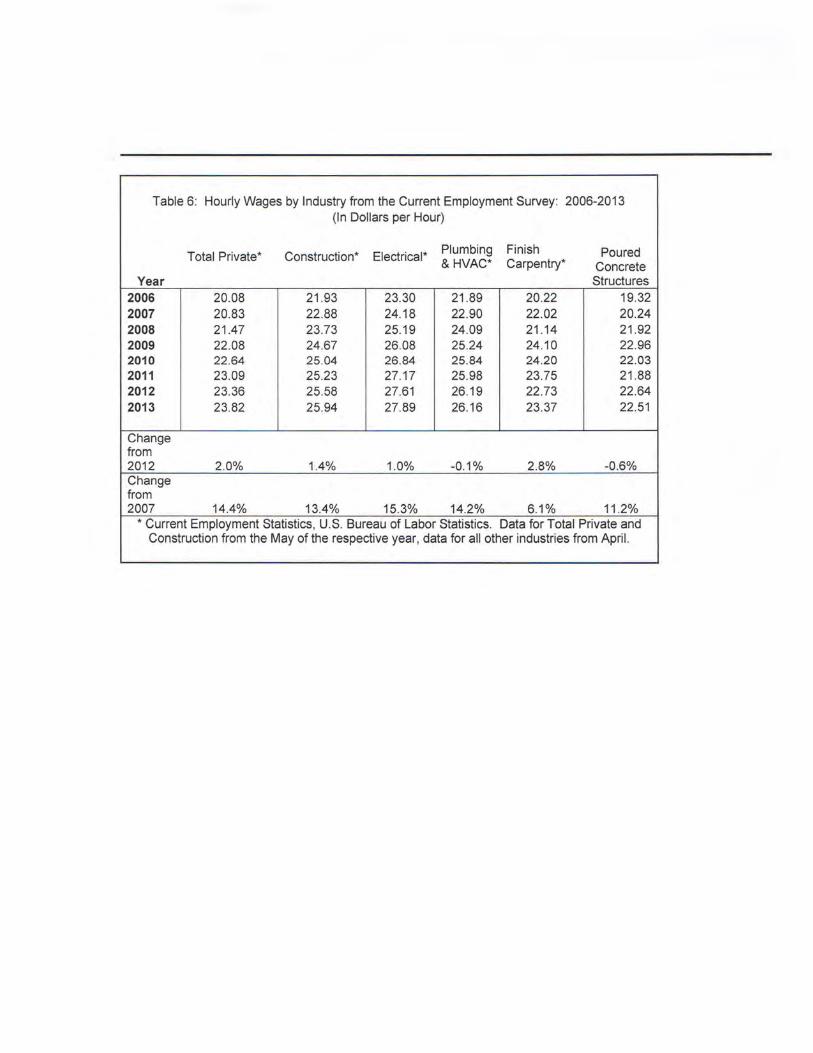

We turn to the Current Employment Survey (CES) to obtain more recent information on

wage change in construction. The CES is structured around detailed industries making it

possible to obtain data on hourly wages in sub-industries such as electrical and

plumbing/HVAC. The industries, and the wage measures, include non-trade workers such as

managers and administrators but the proportion of trade workers in the construction labor

force is very high. Because of this, if trade workers were receiving substantial wage increases,

we would expect to see average hourly wages rising even if other workers in the industry did

not receive wage increases.

Table 6 provides wage data on hourly wages for total private industries, for

construction, for the electrical, plumbing/HVAC, finish carpentry industries and poured

concrete structures (which employs many reinforcing iron workers) . Hourly wages in total

private industries rose by 2.0% between May 2012 and May 2013 and by 14.4% between May

2007 and May 2013. The increases for total construction were somewhat lower; 1.4% for the

last year and 13.4% since May 2007. Wage growth among the industries which comprise

Page 20 of 27

construction are scattered around but not greatly different than the wage growth in total

private industries. The one year increase for electrical, plumbing and steel and poured

concrete is lower than for total private industries while finish carpentry is somewhat above

total private industries. If the period since 2007 is considered, wage increases in electrical and

plumbing/HVAC tend to be at or slightly above total private industry, while finish carpentry and

poured concrete is considerably below total private industry.

Earnings in construction are not growing faster, and may be growing more slowly in

some trades, than earnings in the economy as a whole. This is consistent with construction

employment not having as fully recovered from the Great Recession as employment in the

broader economy. The large contraction in employment in construction during the Great

Recession allows employers to obtain workers with prior construction experience without

having to greatly increase their offers of compensation.

Conclusion

The evidence on national construction employment, job openings, unemployment and

wages does not support the concern that construction faces an imminent national labor

shortage in the next two years. Although the data shows that construction labor markets are

improving, employment remains well below its peak levels in the 2000s; unemployment

remains above historic levels, job openings remain low relative to the available labor force, and

wages are increasing no more rapidly than wages for the national labor force. None of this data

supports concerns about labor shortages now or in the near future.

Page 21of27

It is possible that there could be geographically local shortages in specific skills. In the

past, such shortages have been met through market processes. Construction has long

experience with attracting labor to meet local shortages with increased compensation and

there is every reason to believe that this will be an effective strategy in the near term future.

Given the low level of employment relative to historic levels, and the high rate of

unemployment, sufficient labor should be available without excessive increases in

compensation.

Could there be a shortage of skilled workers three or more years out? This is less

certain than a one to two year scenario as it requires projecting levels of demand for

construction labor and a more developed understanding of the flow of workers into and out of

the construction labor force. While a study of the long term sustainability of the construction

labor force should be undertaken to determine whether there is likely to be a shortage of

construction labor in the mid-term future and how any such shortages could best be addressed,

past experience and current conditions suggest that the increase in construction demand can

be successfully addressed. We provide several observations which point toward the industry's

ability to meet current and future demand if reasonable steps are taken to adjust to the

recovery of construction spending.

First, current projections of construction employment suggest that it will not rise

substantially above the levels of the mid-2000s. The BLS projections utilized by the Associated

Builders and Contractors suggest that construction employment will be 4% lower in 2020 than

in 2006. The projections of the Construction Labor Market Analyzer (CLMA) are less sanguine;

Page 22 of 27

they suggest that in 2017, non-residential employment will peak at 6.8 million employees, up

from 6 million prior to the Great Recession and from current non-residential employment of 4.5

to 5 million. Even with several years of retirements and some workers having permanently left

the labor force, it can be expected that, as employment once again becomes available, trades

workers will flow back into the industry. The 10% unemployment rate in construction and the

high unemployment to openings rate in the HWOL data both suggest that large numbers of

employees are immediately available to the industry.11 Given that those who left for other jobs

took jobs at the bottom of the Great Recession, there is every reason to believe that

construction employment will be attractive to many former construction employees.

Second, market adjustments both in wages and prices will reallocate resources toward

construction so long as the industry is willing to pay for that reallocation. Increases in wages

and benefits play a central role in attracting former and new employees to the industry. The

industrial welder working at $12 per hour may well be attracted away from that job to a

construction job which pays substantially more when these jobs become available. Higher

wages and benefits provide lesser skilled employees the resources needed to upgrade their

skills and provide those outside the industry with incentives to train for trades jobs. Likewise,

as labor costs and other costs rise, marginal projects will be dropped, dampening demand for

construction labor, or delayed, moving demand away from the peak. Between improved

wages increasing the flow of workers into construction labor markets, and reductions of

11 With unemployment at somewhat over 10%, and 5.8 million employees in the construction labor force, there

are 644,000 former construction employees actively seeking employment. Not all may be seeking employment in the construction industry.

Page 23 of 27

demand because of higher labor and materials prices, the peak demand for trades labor, and

any excess over supply, is likely to be more moderate that current discussion allows.

Third, it would not be good public policy to have a construction labor force which was so

large it could readily handle peak demand. As the data on construction employment show,

construction goes through very large swings in spending and employment. This is not surprising

as construction is investment activity. Given the large investment in time and money required

to train a skilled tradesperson, and the investment in equipment needed to support their work,

a labor force which was large enough to meet peak demand would find itself unemployed and

underemployed much of the time. Such over-investment would be wasteful of human and

physical capital and would result in economic hardship for the construction labor force.

All of this is not to argue that there is not a need for additional efforts to develop and

sustain the construction labor force. This is about training, but also about the quality of the

jobs in the industry. Too often discussions of attracting new employees into construction, and

complaints that younger workers just are not choosing construction, are deeply unrealistic

about the quality of construction employment. While construction can pay well, employment

can be, as is apparent in the data, very unstable and trades workers can face extended periods

of unemployment and underemployment. Construction work can be appealing to younger

workers, but too many construction workers lack benefits or have minimal benefits, are

exposed to dangerous conditions which threaten short and long term physical harm, and have

careers which are substantially shorter than their white collar counterparts. Addressing

construction labor shortages is fundamentally about the industry stakeholders discussing and

Page 24 of 27

taking the steps required to create a sustainable labor force that chooses construction over

other careers both because of the challenges and the knowledge that it is indeed a good career.

Page 25 of 27

Table 1: Rates of Growth of Employment: Construction and the National Labor Force

Total Non-Farm Private Construction May % May % May %

Employment Change Employment Change Employment Change (in Thousands) (in Thousands) (in Thousands)

2000 131982 110737 6770 2001 132266 0.2% 111643 0.8% 6849 1.2% 2002 130434 -1.4% 109092 -2.3% 6684 -2.4% 2003 129946 -0.4% 108397 -0.6% 6706 0.3% 2004 131441 1.2% 109300 0.8% 6948 3.6% 2005 133407 1.5% 111137 1.7% 7294 5.0% 2006 135928 1.9% 113823 2.4% 7713 5.7% 2007 137654 1.3% 115288 1.3% 7673 -0 .5% 2008 137491 -0.1% 115449 0.1% 7274 -5.2% 2009 131050 -4.7% 109544 -5.1% 6103 -16.1% 2010 130224 -0.6% 106961 -2.4% 5527 -9.4% 2011 131284 0.8% 108674 1.6% 5524 -0.1% 2012 133522 1.7% 111344 2.5% 5615 1.7% 2013 135637 1.6% 113454 1.9% 5804 3.4%

Decline From -1 .5% -1.6% -24.8% Peak

Data from Current Employment Statistics, U.S. Bureau of Labor Statistics

Page 26 of 27

Tab

le 2

: C

on

stru

ctio

n E

mp

loym

ent

in M

ajo

r O

ccu

pat

ion

s

Op

erat

ing

C

om

bin

ed T

ota

l C

arp

ente

rs

Ele

ctri

cian

s P

lum

ber

/Pip

efit

ter

Iron

Wo

rker

s L

abo

rers

E

ng

inee

rs

OES

C

PS

OES

C

PS

OES

C

PS

OES

C

PS

OES

C

PS

OES

C

PS

OES

C

PS

20

05

2,

697,

814

3,41

6,26

6 77

3,22

0 1,

062,

528

452,

520

514,

00

4

374,

214

363,

842

90,6

70

53,0

76

760,

780

1,19

6,65

8 24

6,41

0 22

6,15

8

20

06

2,

861,

976

3,57

1,70

5 82

2,24

0 1,

063,

921

46

9,6

80

53

2,21

8 39

6,50

6 41

2,31

0 89

,180

41

,860

82

1,61

0 1,

284,

390

262,

760

237,

006

20

07

2,

873,

082

3,64

2,07

7 80

5,41

0 1,

042,

968

477,

540

536,

241

396,

092

429,

719

84,5

70

60,3

65

836,

420

1,32

4,84

6 27

3,05

0 24

7,93

8

20

08

2,

791,

857

3,20

2,24

7 74

8,79

0 88

4,33

3 48

7,50

0 49

7,79

5 39

7,36

7 34

7,82

6 88

,740

73

,353

80

4,04

0 1,

172,

944

265,

420

225,

996

20

09

2,

409,

469

3,43

7,07

8 61

5,55

0 88

1,32

5 44

1,31

0 54

1,55

6 35

6,38

9 37

0,12

1 81

,510

57

,850

68

2,12

0 1,

322

,91

7

232,

590

263,

309

20

10

2,

049,

600

2,73

8,12

2 49

5,00

0 71

8,67

5 38

3,00

0 40

0,00

3 31

4,10

0 29

8,23

8 69

,100

46

,235

59

1,60

0 1,

058,

531

196,

800

216,

440

20

11

2,

031

,884

2,

760

,057

47

6,30

0 71

7,22

3 37

7,46

0 40

7,2

77

302,

454

338,

438

65,1

60

61,4

96

611,

330

1,00

4,24

4 19

9,18

0 23

1,37

9

20

12

2,

062,

073

2,76

0,04

6 47

1,35

0 73

1,65

9 38

2,97

0 40

0,29

6 29

6,64

3 31

4,81

1 65

,160

62

,934

64

1,8

60

1,

044,

047

204,

090

206,

299

Ave

rage

E

mp

loy

men

t 2,

472,

219

3,

190,

950

650,

983

887,

829

433,

998

478,

674

354,

221

359,

413

79,2

61

57,1

46

718

,720

1,

176,

072

235,

038

231,

816

Cha

nge

in E

mp

loym

ent

2005

-201

2

Net

Ch

ang

e#

-635

,741

-6

56,2

20

-301

,870

-3

30

,86

91

-6

9,55

0 -1

13

,70

81

-7

7,57

1 -4

9,03

1 I -

2551

0 9

85

81

-1

18,9

20

-152

.611

I -4

2,32

0 -1

9,85

9

Net

Ch

ang

e%

-24%

-1

9%

-39%

-3

1%

-15%

-2

2%

-21%

-1

3%

-28%

19

%

-16%

-1

3%

-17%

-9

%

Cha

nge

in E

mp

loym

ent

2011

-201

2

Net

Cha

ng

e#

3

0,1

90

-1

1 -4

,950

14

,436

1 5,

510

-6.9

81 I

-5,8

10

-23

,62

71

0

1,43

81

30,5

30

39

,80

31

4,

910

-25,

080

Net

Ch

ang

e%

1%

0%

-1%

2%

1%

-2

%

-2%

-7

%

0%

2%

5%

4%

2%

-11%

Dat

e fr

om

th

e C

urre

nt P

opul

atio

n S

urve

y an

d th

e O

ccup

atio

nal

Em

ploy

men

t S

urve

y, U

.S.

Bur

eau

of

Lab

or S

tati

stic

s

c 0

·.;:; u

ClJ 2 ..... ..... ro Ill

.::: c ... c:: 0

0 u ...., m I I u ~ QJ 0 V) N n-uer QJ I ... ~ - n-uer ca 0 > ·- 0 n -uer .... N c.. ot-uer

QJ c 60-uer .c 0 ...., - 80-uer c ....,

u Lo-uer ::::s V) .... 90-uer llO ....,

c V) so-uer c c 0 .. 170-uer

QJ u c. "'C rn-uer 0 c rn-uer ..c ca 0 .. w -uer - 0 0 C? 0 0 0

LJ"i '<f M N M 0 lUawA01dw3

10 iuaJJad 'd se s~u1uado qor

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

20

09

2010

20

11

2012

20

13

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

20

09

2010

20

11

2012

20

13

Ye

ar

Ye

ar

Jan

4.6

3.

2 3.

2 3.

0 3.

2 3.

6 3

.7

3.4

2.3

2.3

2.5

2.9

2.9

Jan

2.8

1.6

1.8

2.0

2.1

2.0

3.4

1.8

0.5

1.0

1.2

1.

4 1.

8

Tab

le3:

Jo

b O

pen

ing

s: 2

000

-200

13

Fe

b

3.5

2.5

2.6

2.6

2.9

3.2

3.3

3.

0 2.

1 2.

0 2.

3 2.

6 2.

9

Fe

b

3.1

1.

5 1.

3 1.

6 2.

0 1.

8 3.

5 1.

8 1.

1 1.

3 0.

9 1.

2 2.

0

Mar

3.6

2.7

2.4

2.7

3.1

3.4

3.

5 3.

0 1.

9 2.

0 2.

5 3.

0 3.

0

Mar

3.1

1.9

1.4

1.9

2.2

2.5

2.8

1.3

0.8

1.4

1.3

1.7

2.0

To

tal

Pri

vate

A

pr

May

Ju

n

4.2

3.5

3.1

2.7

2.9

2.5

3.2

2.9

3.6

3.1

3.8

3.4

3.8

3.4

3.3

3.0

1.9

1.9

2.5

2.2

2.6

2.3

3.0

2.9

3.1

3.2

2.5

2.4

2.6

3.0

3.2

3.4

2.7

1.8

2.1

2.5

2.9

Co

nst

ruct

ion

A

pr

May

Ju

n

4.3

3.

7 1.

8 1.

9 2

.7

1.7

2.4

2.2

2.4

2.2

2.9

2.6

2.8

2.3

1.5

2.3

0.4

0.7

1.

8 1.

5 2.

1 1.

8 1.

6 1.

4 2.

4

2.8

1.9

1.6

1.6

1.9

2.4

2.0

1.6

1.0

1.4

1.1

1.4

Jul 3.6

2.9

2.7

3.3

3.5

3.3

3.6

3.1

1.9

2.6

2.8

2.9

Jul 2.5

1.5

2.1

1.

8 2.

3 3

.1

2.4

1.8

0.8

1.8

1.4

1.3

Au

g

3.2

2.6

2.6

2.9

3.2

3.4

3.4

2.8

1.8

2.4

2.6

2.8

Au

g

1.7

1.6

1.4

1.8

2.0

2.6

2.0

1.2

1.0

1.0

1.7

1.4

Da

te fr

om

Job

Ope

nin

gs

an

d L

ab

or

Tu

rno

ver

Su

Ne

y, U

.S.

BL

S

Sep

3.1

2.5

2.4

3.0

3.3

3.4

3.4

2.4

2.0

2.2

2.7

2.8

Sep

2.1

1.9

0.8

1.5

2.0

2.2

1.6

1.8

1.2

1.4

1.4

1.5

Oct

3.0

3.1

2.7

3.2

3.5

3.6

3.4

2.7

2.0

2.6

2.8

3.0

Oct

1.6

1.8

1.1

1.9

2.1

1.

9 1.

7 0.

9 1.

0 1.

3 1.

2 1.

7

No

v 2.4

2.4

2.3

2.3

3.0

3.2

2.9

2.1

1.7

2.

2 2.

2 2.

6

No

v 1.4

1.2

1.1

1.4

2.0

1.3

1.

1 0

.7

0.8

1.1

1.0

1.3

De

c 3.4

2.4

2.1

2.3

2.6

2.9

3.1

2.8

2.1

1.7

2.

0 2.

3 2.

4

De

c 2.3

1.3

1.0

1.1

1.

5 1.

6 1.

3 1

.3

1.0

0.9

0.6

0.8

1.1

Ta

ble

4a

: C

on

stru

ctio

n U

ne

mp

loym

en

t: J

anua

ry 2

000

to M

ay,

2013

: In

div

idu

als

in t

he

exp

eri

en

ced

pri

vate

labo

r fo

rce

re

po

rtin

g c

urr

en

tly

em

plo

yed

or

tha

t th

eir

last

job

was

in t

he

co

nst

ruct

ion

in

du

stry

: Y

ear

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

20

09

2010

20

11

2012

20

13

Jan 9

.7

9.8

13

.6

14

.0

11

.3

11.8

9.

0 8

.9

11.0

18

.2

24

.7

22.5

1

7.7

1

6.1

S

erie

s L

NU

0403

2231

Feb 10

.6

9.9

12.2

14

.0

11.6

12

.3

8.6

10

.5

11.4

21

.4

27.1

21

.8

17.1

15

.7

Mar

8.7

8.4

11

.8

11.8

11

.3

10.

3 8

.5

9.0

12

.0

21.1

24

.9

20.0

17

.2

14.7

Apr

M

ay

5.8

5.

0 7.

1 5

.6

10.1

7.

4 9.

3 8.

4 9

.5

7.4

7.4

6.1

6.9

6.6

8.6

6

.9

11.1

8.

6 18

.7

19

.2

21.8

20

.1

17.8

16

.3

14.

5 1

4.2

13.2

10

.8

Jun 4.

6 5

.1

6.9

7.9

7.0

5.7

5.6

5.9

8.2

17.4

20

.1

15.6

12

.8

Jul

Aug

4

.4

5.1

4.9

5

.8

6.9

7.4

7.

5 7.

1 6.

4 6.

0 5

.2

5.7

6.

1 5.

9 5.

9 5.

3 8

.0

8.2

18

.2

16

.5

17.3

17

.0

13.6

13

.5

12.3

11

.3

Sep

4.6

5

.5

7.0

7.

6 6.

8 5

.7

5.6

5.8

9.9

17

.1

17.2

13

.3

11.9

Oct

4.9

6.

1 7

.7

7.4

6.9

5.

3 4.

5 6

.1

10.

8 18

.7

17.3

13

.7

11.4

Tab

le 4

b:

Un

em

plo

yme

nt o

f in

div

idu

als

20

and

old

er:

Janu

ary

2000

to

May

, 20

13:

Yea

r 20

00

2001

20

02

2003

20

04

2005

20

06

2007

20

08

2009

20

10

2011

20

12

2013

S

erie

s L

NU

0400

0024

Jan

4

.0

4.1

5.8

5

.9

5.7

5.

2 4.

6 4

.6

4.8

7.9

9.

9 9

.2

8.3

7

.9

Fe

b

3.8

4.0

5.

6 5.

8 5.

5 5

.2

4.6

4

.4

4.7

8.

3 9

.9

9.0

8

.2

7.5

Mar

3.

7 4.

0 5.

5 5.

6 5.

5 4

.8

4.3

4

.1

4.8

8.

5 9

.6

8.7

7.8

7.

1

Ap

r 3.2

3.

7 5.

2 5.

3 4.

8 4

.4

4.1

3.

8 4

.3

8.1

8

.9

8.1

7.

2 6.

6

May

3.

3 3.

6 4

.9

5.2

4.

7 4.

2 3.

9 3.

7 4.

6 8.

4 8

.6

8.2

7.

3 6.

6

Jun

3.

4 3.

9 5.

1 5.

6 5

.0

4.4

4.0

3.

9 4.

8 8

.7

8.7

8.

5 7

.6

Jul

Au

g

3.5

3.5

4

.0

4.3

5.2

5.1

5.

5 5

.5

4.9

4

.8

4.5

4.

3 4

.3

4.1

4

.3

4.1

5.

2 5

.5

8.9

8.9

8.

9 8

.9

8.6

8.

4 7.

8 7.

5

Sep

3

.2

4.2

4.

8 5

.2

4.6

4.4

3.8

4.0

5.

4 8.

8 8

.6

8.2

7

.0

Oct

3

.1

4.4

4.9

5

.0

4.5

4

.1

3.6

3.

9 5.

5 8.

8 8.

4 7.

9 6

.9

No

v 3.2

4.

7 5

.0

5.1

4.6

4.3

3.

8 4.

0 5

.9

8.7

8.

7 7

.6

6.8

No

v 5.7

7.6

8.5

7.8

7.4

5.

7 6

.0

6.2

12.7

19

.4

18

.8

13.1

12

.2

Dec

A

nn

ua

l 6

.8

6.2

9

.0

7.1

10.9

9.

2 9.

3 9

.3

9.5

8

.4

8.2

7.4

6.

9 6

.7

9.4

7.

4 15

.3

10.

6 22

.7

19.0

20

.7

20

.6

16.0

16

.4

13.5

13

.9

De

c A

nn

ua

l 3

.2

3.4

4.9

4

.2

5.2

5

.2

5.0

5.4

4.6

4

.9

4.2

4.5

3.

8 4

.1

4.3

4

.1

6.6

5.2

9

.1

8.6

8

.6

9.0

7

.8

8.3

7.1

7.4

V)

:::> M .. ~ Cl) 0 !N t'O

0:: 0 +"" 0 co CIJ N E > c 0 0 c. +""

E ~ QJ I..

c t; :::> c >o -U

..c "'C 1: c 0 t'O

~

n -Jd'v'

01-1nr

60-l:JQ

60-uer

80-Jd'v'

Lo-1nr

90-PO

90-uer

SO-Jd'v'

vo-1nr

EQ-PO

rn-uer

ZO-Jd'v'

10-1nr

oo-i:io oo-uer

c 0 ~ u 2 ti c 0 u

I + 0 N Q) tlO

1

Table 5: Hourly and Annual Earnings: 2007 - 2012 Hourly Earnings Annual

Earnings

75th Year Mean Median Percentile

All Occupations

2007 19.56 15.10 23 .87 40690

2008 20.32 15.57 24.78 42270

2009 20.90 15.95 25.44 43460

2010 21.35 16.27 26.08 44,410

2011 21.74 16.57 26.67 45,230

2012 22.01 16.71 27.02 45,790

Change From 2011 1.2% 0.8% 1.3% 1.2%

Change from 2007 12.5% 10.7% 13.2% 12.5%

Carpenters

2007 19.84 18.11 24.40 41260

2008 20.64 18.72 25.37 42940

2009 20.98 18.98 25.76 43640

2010 21.10 19.00 25.90 43,890

2011 21.31 19.24 26.23 44,330

2012 21.41 19.20 26.35 44,520

Change From 2011 0.5% -0.2% 0.5% 0.4%

Change from 2007 7.9% 6.0% 8.0% 7.9%

Electricians

2007 23.12 21.53 28.77 48100

2008 23 .98 22.32 29.88 49890

2009 24.45 22.68 30.35 50850

2010 24.91 23.20 30.71 51,810

2011 25.44 23.71 31.38 52,910

2012 25 .50 23.96 31.48 53,030

Change From 2011 0.2% 1.1 % 0.3% 0.2%

Change from 2007 10.3% 11.3% 9.4% 10.2%

Plumbers, Pipefitters, and Steamfitters

2007 22.76 21.20 28.51 47350

2008 23 .65 21.94 29.66 49200

2009 23.97 22.27 30.01 49870

2010 24.21 22.43 30.22 50,360

2011 24.92 22.96 31.15 51,830

2012 25.46 23 .62 31.75 52,950

Change From 2011 2.2% 2.9% 1.9% 2.2%

Change from 2007 11.9% 11.4% 11.4% 11.8%

Table 5 Continued: Hourly and Annual Earnings: 2007-2012 Hourly Earnings Annual

Earnings

Year mean Median 75th Percentile

Structural iron and steel workers

2007 21.99 20.26 28.14 45730

2008 22.68 20.68 29.15 47170

2009 23.30 21.40 29.63 48470

2010 23.42 21.42 29.51 48,710

2011 24.11 21.97 30.91 50,160

2012 24.40 22.18 31.50 50,740

Change Fram 2011 1.2% 1.0% 1.9% 1.2%

Change fram 2007 11.0% 9.5% 11 .9% 11.0%

Reinforcing iron and rebar workers

2007 20.50 18.21 26.18 42640

2008 21.34 19.18 27.29 44380

2009 21.42 18.97 28.05 44560 2010 21.48 18.48 28.20 44,690 2011 21.83 18.27 28.83 45,400 2012 24.59 22.07 33.18 51,140

Change Fram 2011 12.6% 20.8% 15.1% 12.6%

Change / ram 2007 20.0% 21.2% 26.7% 19.9% I Construction laborers

2007 14.88 13.13 17.87 30950

2008 15.51 13.71 18.57 32250

2009 15.96 14.01 19.11 33190

2010 16.15 14.08 19.16 33,590 2011 16.43 14.30 19.61 34,170

2012 16.58 14.42 19.83 34,490

Change From 2011 0.9% 0.8% 1.1% 0.9%

Change from 2007 11.4% 9.8% 11.0% 11.4% I Welders, cutters, solderers, and brazers

2007 16.33 15.51 19.00 33960 2008 17.01 16.13 19.61 35370 2009 17.61 16.71 20.39 36630 2010 17.96 17.04 21.01 37,370

2011 18.23 17.27 21.35 37,920

2012 18.46 17.45 21.62 38,410

Change Fram 2011 1.3% 1.0% 1.3% 1.3% Change f rom 2007 13.0% 12.5% 13.8% 13.1% I Data from Occupational Employment Statistics, U.S. Bureau of Labor Statistics, http://www.bis.gov/oes/tables.htm

Table 6: Hourly Wages by Industry from the Current Employment Survey: 2006-2013 (In Dollars per Hour)

Total Private* Construction* Electrical* Plumbing Finish Poured & HVAC* Carpentry* Concrete

Year Structures

2006 20.08 21 .93 23.30 21 .89 20.22 19.32 2007 20.83 22.88 24.18 22.90 22 .02 20.24 2008 21.47 23 .73 25.19 24.09 21 .14 21 .92 2009 22.08 24.67 26.08 25.24 24.10 22.96 2010 22.64 25.04 26.84 25.84 24.20 22.03 2011 23.09 25.23 27.17 25.98 23.75 21 .88 2012 23.36 25.58 27.61 26.19 22 .73 22.64 2013 23.82 25.94 27.89 26.16 23.37 22.51

Change from 2012 2.0% 1.4% 1.0% -0.1% 2.8% -0 .6% Change from 2007 14.4% 13.4% 15.3% 14.2% 6.1% 11 .2%

* Current Employment Statistics, U.S. Bureau of Labor Statistics. Data for Total Private and Construction from the May of the respective year, data for all other industries from Apri l.

Bibliography

Barnow, B. S., J. Trutko and J. S. Piatak, Occupational Labor Shortages: Concepts, Causes

Consequences and Cures, Kalamazoo: W. E. Upjohn Institute, 2013

Podgornik, G. "Job openings and hires continue to show modest changes in 2011" Monthly

Labor Review, September, 2012, pages 28 - 34

Veneri, C. M., "Can occupational labor shortages be identified using available data?", Monthly

Labor Review, March, 1999, pages 15 - 21.

Page 27 of 27