Global Market Perspective November 2010 Final

17

COPYRIGHT © JONES LANG LASALLE IP, INC. 2010. All Rights Reserved 1 Global Market Perspective November 2010 Real Estate Outlook for 2011 The final 2010 edition of Global Market Perspective provides our view on the likely shape of commercial real estate markets across the globe in 2011. Over the next 12 months we expect to see a much greater divergence in real estate activity and performance and our top 10 trends for 2011 are: 1. Global direct commercial real estate investment volumes will rise by 25-35% on 2010 levels. A significant weight of equity capital will target real estate and fresh capital-raising will further enliven the market 2. Banks and servicers will adopt a more aggressive approach to the disposal of non-performing assets, leading to the release of more secondary product 3. The CMBS market in the US will continue to gather pace, but will remain well below pre-Crisis levels 4. Leasing volumes will be at their highest level since the Global Financial Crisis, with corporate occupiers displaying greater confidence to do deals - but they will continue to push for the best possible terms 5. Asia Pacific will lead the upswing in leasing markets, ahead of Europe and North America 6. Prime property will continue to outperform secondary. Expect double-digit capital value growth for trophy assets in many of the world’s high-order business hubs 7. Shortages of prime product in Tier I cities will encourage investors to widen their search to Tier II 8. Latin America will continue to build momentum, attracting strong corporate occupier and investor interest 9. A lack of available Grade A stock in many markets will start to limit relocation options for corporate occupiers 10. The domestic corporate sector will come to the fore in Asia Pacific, particularly in India and China Highlights • A two-speed economic recovery persists • Asia Pacific leading the real estate upswing • Banks disposing of non-performing assets • Corporate occupiers face fewer relocation options • A market of trophy and trauma

-

Upload

christopher-chang -

Category

Documents

-

view

220 -

download

0

Transcript of Global Market Perspective November 2010 Final

8/6/2019 Global Market Perspective November 2010 Final

http://slidepdf.com/reader/full/global-market-perspective-november-2010-final 1/17

COPYRIGHT © JONES LANG LASALLE IP, INC. 2010. All Rights Reserved 1

Global Market Perspective November 2010

Real Estate Outlook for 2011

The final 2010 edition of Global Market Perspective provides our view on the likely shape of commercial real estate

markets across the globe in 2011. Over the next 12 months we expect to see a much greater divergence in real estate

activity and performance and our top 10 trends for 2011 are:

1. Global direct commercial real estate investment volumes will rise by 25-35% on 2010 levels. A significantweight of equity capital will target real estate and fresh capital-raising will further enliven the market

2. Banks and servicers will adopt a more aggressive approach to the disposal of non-performing assets, leading to

the release of more secondary product

3. The CMBS market in the US will continue to gather pace, but will remain well below pre-Crisis levels

4. Leasing volumes will be at their highest level since the Global Financial Crisis, with corporate occupiers

displaying greater confidence to do deals - but they will continue to push for the best possible terms

5. Asia Pacific will lead the upswing in leasing markets, ahead of Europe and North America

6. Prime property will continue to outperform secondary. Expect double-digit capital value growth for trophy

assets in many of the world’s high-order business hubs

7. Shortages of prime product in Tier I cities will encourage investors to widen their search to Tier II

8. Latin America will continue to build momentum, attracting strong corporate occupier and investor interest

9. A lack of available Grade A stock in many markets will start to limit relocation options for corporate occupiers

10.

The domestic corporate sector will come to the fore in Asia Pacific, particularly in India and China

Highlights

• A two-speed economic recovery persists • Asia Pacific leading the real estate upswing

• Banks disposing of non-performing assets

• Corporate occupiers face fewer relocation options

• A market of trophy and trauma

8/6/2019 Global Market Perspective November 2010 Final

http://slidepdf.com/reader/full/global-market-perspective-november-2010-final 2/17

COPYRIGHT © JONES LANG LASALLE IP, INC. 2010. All Rights Reserved 2

Global Market Perspective November 2010

Global Economy

Momentum continuing into 2011

The global economy is now more than 18 months into recovery and most forecasts point to the growth momentum

continuing into 2011, although at a decelerating pace. The IMF expects the global economy to grow at a healthy rate of

4.2% in 2011, but it highlights several downside risks relating to global economic imbalances and potential volatility infinancial, currency and commodity markets.

A two-speed economy

Economic prospects are likely to be uneven in 2011, which will be reflected in greater divergence in real estate activity

and performance. A subdued outlook for most advanced economies contrasts with a relatively strong year for many

emerging economies, where over half of the world’s 2011 economic growth is expected to occur. Most advanced

economies will still face major adjustments, particularly the need to strengthen household balance sheets, to stabilise

and reduce public debt and to repair their financial sectors. As a consequence, economic growth in North America,

Western Europe and Japan is projected to be muted, within a range of 1.0-2.5% in 2011. Moreover, ongoing periodic

tensions inEurope,

caused by the sovereign debt situation, will continue to unnerve the markets. Policy interest rates in

most advanced economies are likely to remain low in 2011 and fresh stimulus measures, to boost flagging economic

growth and ward off deflationary pressures, could further contribute to asset price inflation.

Asia Pacific - the star performer

In contrast, Asia Pacific is on a stronger foothold and will continue to outpace the world economy, with regional

economic growth in 2011 expected to be in the 6-7% range (excluding Japan). Robust growth in both China and India

of 8-9% will power the rest of the region. Hong Kong, Australia and Indonesia will also maintain healthy rates of

expansion. There are some potential bumps in the road however - currency appreciation is a concern which could

reduce competitiveness and affect trade and real estate capital flows. Asia Pacific is also facing inflationary pressures,

which are pushing up interest rates across the region.

Latin America will continue to build momentum in 2011 with Brazil taking the lead. There are also bright spots inEmerging Europe, notably Poland and Turkey, while Russia is now rebounding. Higher oil prices are driving a

recovery in some Middle Eastern economies, and there is increasing business interest in its two regional powerhouses,

Egypt and Saudi Arabia.

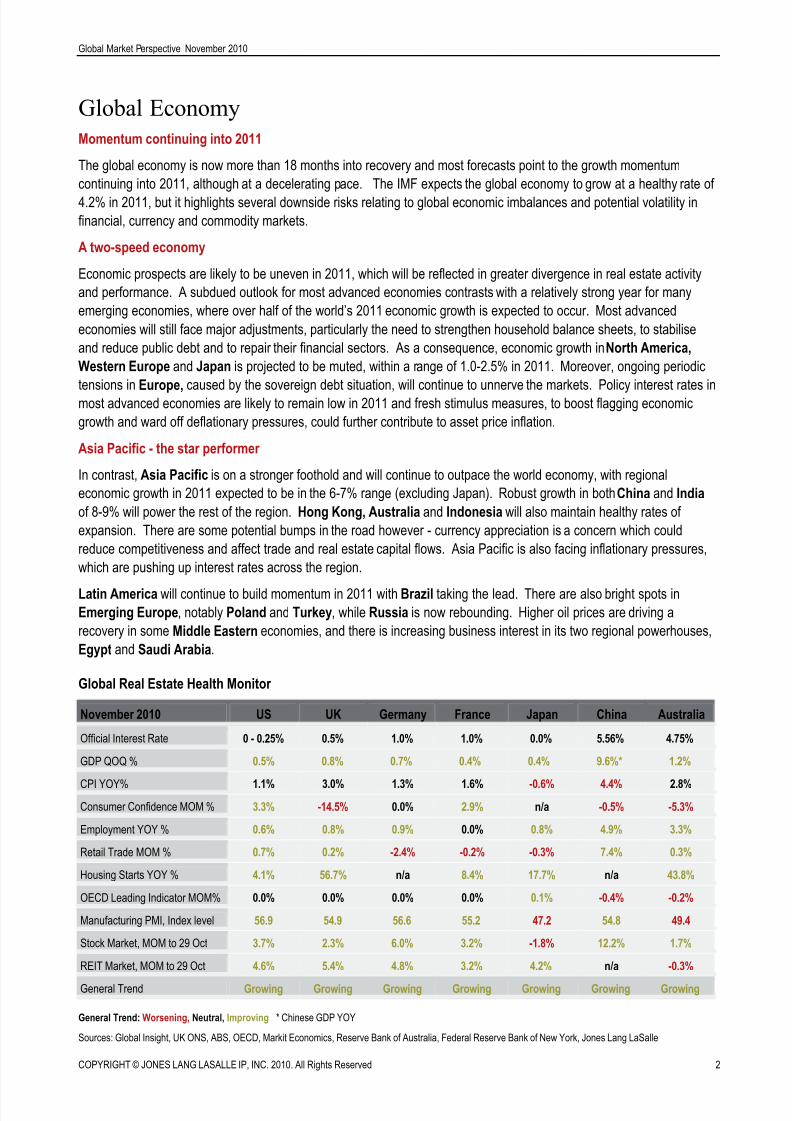

Global Real Estate Health Monitor

November 2010 US UK Germany France Japan China Australia

Official Interest Rate 0 - 0.25% 0.5% 1.0% 1.0% 0.0% 5.56% 4.75%

GDP QOQ % 0.5% 0.8% 0.7% 0.4% 0.4% 9.6%* 1.2%

CPI YOY% 1.1% 3.0% 1.3% 1.6% -0.6% 4.4% 2.8%

Consumer Confidence MOM % 3.3% -14.5% 0.0% 2.9% n/a -0.5% -5.3%

Employment YOY % 0.6% 0.8% 0.9% 0.0% 0.8% 4.9% 3.3%

Retail Trade MOM % 0.7% 0.2% -2.4% -0.2% -0.3% 7.4% 0.3%

Housing Starts YOY % 4.1% 56.7% n/a 8.4% 17.7% n/a 43.8%

OECD Leading Indicator MOM% 0.0% 0.0% 0.0% 0.0% 0.1% -0.4% -0.2%

Manufacturing PMI, Index level 56.9 54.9 56.6 55.2 47.2 54.8 49.4

Stock Market, MOM to 29 Oct 3.7% 2.3% 6.0% 3.2% -1.8% 12.2% 1.7%

REIT Market, MOM to 29 Oct 4.6% 5.4% 4.8% 3.2% 4.2% n/a -0.3%

General Trend Growing Growing Growing Growing Growing Growing Growing

General Trend: Worsening, Neutral, Improving * Chinese GDP YOY

Sources: Global Insight, UK ONS, ABS, OECD, Markit Economics, Reserve Bank of Australia, Federal Reserve Bank of New York, Jones Lang LaSalle

8/6/2019 Global Market Perspective November 2010 Final

http://slidepdf.com/reader/full/global-market-perspective-november-2010-final 3/17

COPYRIGHT © JONES LANG LASALLE IP, INC. 2010. All Rights Reserved 3

Global Market Perspective November 2010

Global Property

Asia Pacific leading the real estate upswing

Activity in the world’s major commercial real estate markets is expected to continue to strengthen during 2011, building

on the footholds established during 2010. The recovery, however, will be segmented by product type and geography,with prime property continuing to perform better than secondary, Tier I cities outperforming Tier II and III cities, and Asia

Pacific leading the upswing, ahead of Europe and North America.

More churn by corporate occupiers

Office leasing volumes in 2011 are projected to be at their highest level since the Global Financial Crisis, with corporate

occupiers displaying greater confidence to do deals. Higher churn will be helped by improved corporate profitability, but

occupiers will continue to push for the best possible terms and to strive for cost efficient space. Their focus will be on

better grades of space, leading to the eventual release of poorer quality second-hand property, which could potentially

overhang the market for several years.

In Asia Pacific, strong economic conditions and business confidence will boost office take-up in 2011. Relocation andupgrading are likely to underpin the bulk of demand, although with stronger hiring activity in markets such as Hong

Kong, Singapore, China and India, expansion demand is expected to accelerate as corporate occupiers equip

themselves for future growth. Net absorption across Asia Pacific’s Tier I office markets is projected to reach a record 4.5

million square metres in 2011, almost double the 2009 level and about 10% higher than the previous peak in 2007. Tier

I markets in India and China will see the highest net absorption rates, enhanced by rapidly-growing domestic corporate

sectors and expansion by multinational corporations (MNCs).

In both Europe and the US, take-up levels are expected to rise modestly on 2010 levels. Overall, net absorption is likely

to remain flat, although some core Tier I office hubs could register relatively strong absorption rates. German, Nordic

and CEE markets will also see strengthening demand. Conversely, most Tier II cities, suburban and Grade B segments

will continue to languish with levels of demand well below trend. A fully-fledged and sustained recovery in demandacross Western Europe and North America will not materialise until there is real and consistent jobs growth in office-

using sectors.

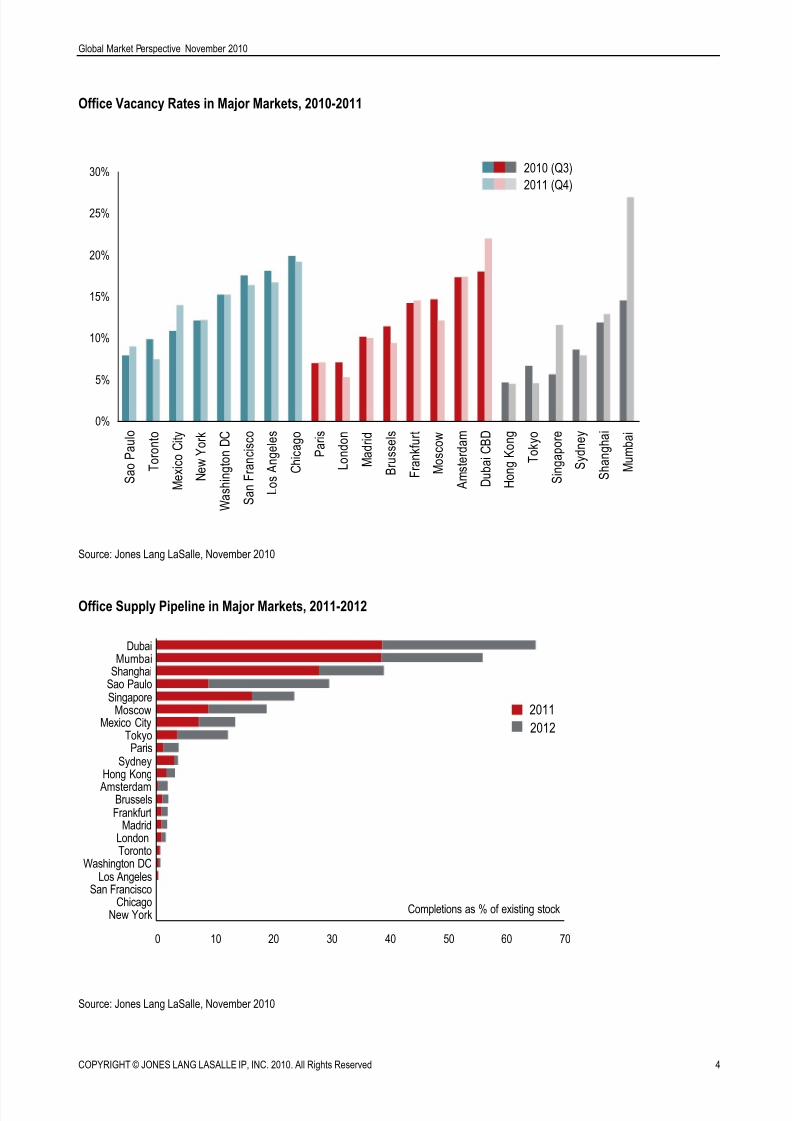

Vacancy rates trending down, but markets polarising

Overall office vacancy rates will gradually trend downwards during 2011. In Europe and the US, new office deliveries

are near historic lows and commencements are few and far between. This dynamic will intensify in 2011, leading to

increasing shortages of Grade A space. Most markets are still without speculative development finance and although

injections of funding have been seen in London, they have been focused on trophy tower schemes. A supply gap is

likely to emerge in many markets, with refurbishment and ‘green’ retrofits a logical strategy to exploit the lack of new

build. The market will increasingly polarise, with shortages of Grade A space and rising volumes of vacant secondaryspace.

By contrast, Asia Pacific will reach the peak of its development cycle in 2011 with a record additional 6.8 million square

metres of office space to be delivered. Nonetheless, strong corporate occupier demand will absorb much of the

additional space and, in most markets, vacancy rates will not rise significantly. The exceptions will be some Indian and

Chinese cities, and to a lesser extent Singapore, where large supply pipelines will force up vacancy rates. In markets

such as Hong Kong, Tokyo and Sydney, limited supply combined with strengthening demand should see vacancies

trend downwards.

Several major office markets in Latin America including Sao Paulo, Rio de Janeiro, Santiago and Panama City still

feature vacancy rates near or below equilibrium levels. With strong demand from MNCs for the highest-quality space,

many of these markets have chronic shortages of premier-grade offices. However, the construction pipelines are well-stocked and, while much of it will be absorbed, there is a risk of overbuilding in certain geographies over the short to

medium term.

8/6/2019 Global Market Perspective November 2010 Final

http://slidepdf.com/reader/full/global-market-perspective-november-2010-final 4/17

COPYRIGHT © JONES LANG LASALLE IP, INC. 2010. All Rights Reserved 4

Global Market Perspective November 2010

Office Vacancy Rates in Major Markets, 2010-2011

Source: Jones Lang LaSalle, November 2010

Office Supply Pipeline in Major Markets, 2011-2012

Source: Jones Lang LaSalle, November 2010

0%

5%

10%

15%

20%

25%

30%

S a o P a u l o

T o r o n t o

M e x i c o C i t y

N e w Y o r k

W a s h i n g t o n D C

S a n F r a n c i s c o

L o s A n g e l e s

C h i c a g o

P a r i s

L o n d o n

M a d r i d

B r u s s e l s

F r a n k f u r t

M o s c o w

A m s t e r d a m

D u b a i C B D

H o n g K o n g

T o k y o

S i n g a p o r e

S y d n e y

S h a n g h a i

M u m b a i

2010 (Q3)

2011 (Q4)

0 10 20 30 40 50 60 70

New YorkChicago

San FranciscoLos Angeles

Washington DCTorontoLondon

MadridFrankfurtBrussels

Amsterdam

Hong KongSydney

ParisTokyo

Mexico CityMoscow

SingaporeSao PauloShanghaiMumbai

Dubai

Completions as % of existing stock

2011

2012

8/6/2019 Global Market Perspective November 2010 Final

http://slidepdf.com/reader/full/global-market-perspective-november-2010-final 5/17

COPYRIGHT © JONES LANG LASALLE IP, INC. 2010. All Rights Reserved 5

Global Market Perspective November 2010

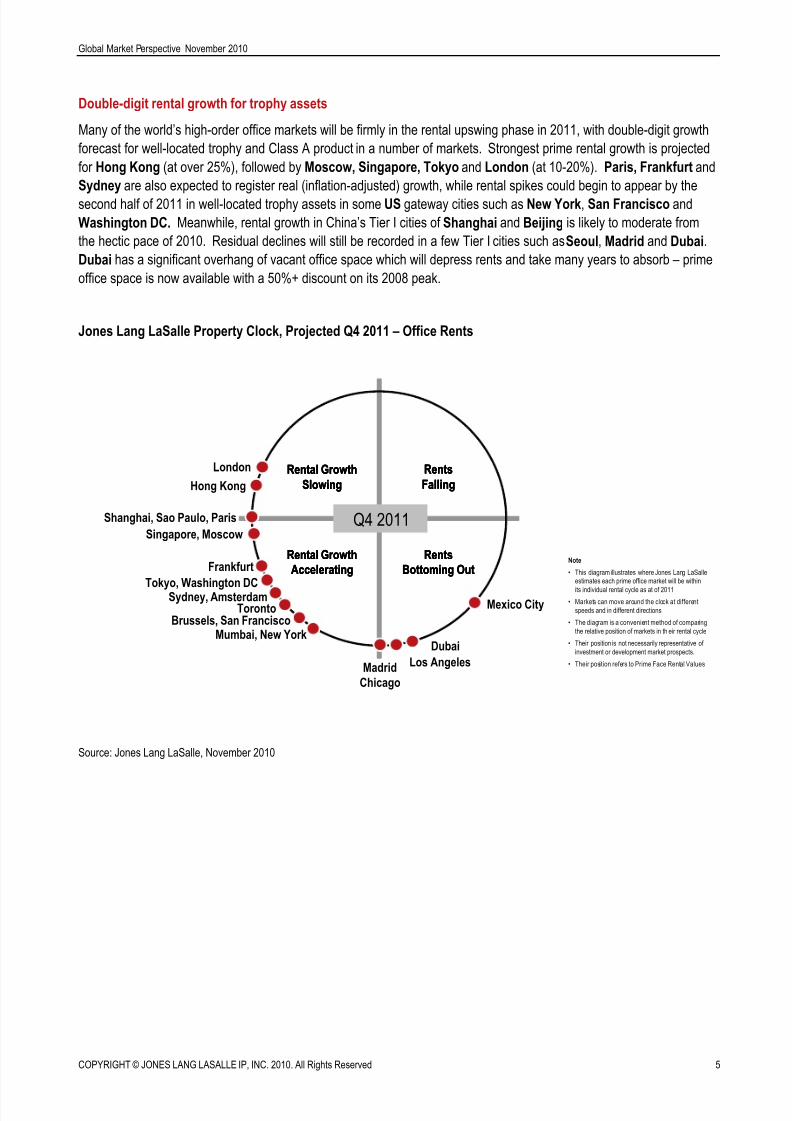

Double-digit rental growth for trophy assets

Many of the world’s high-order office markets will be firmly in the rental upswing phase in 2011, with double-digit growth

forecast for well-located trophy and Class A product in a number of markets. Strongest prime rental growth is projected

for Hong Kong (at over 25%), followed by Moscow, Singapore, Tokyo and London (at 10-20%). Paris, Frankfurt and

Sydney are also expected to register real (inflation-adjusted) growth, while rental spikes could begin to appear by the

second half of 2011 in well-located trophy assets in some US gateway cities such as New York, San Francisco and

Washington DC. Meanwhile, rental growth in China’s Tier I cities of Shanghai and Beijing is likely to moderate from

the hectic pace of 2010. Residual declines will still be recorded in a few Tier I cities such as Seoul, Madrid and Dubai.

Dubai has a significant overhang of vacant office space which will depress rents and take many years to absorb – prime

office space is now available with a 50%+ discount on its 2008 peak.

Jones Lang LaSalle Property Clock, Projected Q4 2011 – Office Rents

Source: Jones Lang LaSalle, November 2010

Note

• This diagram illustrates where Jones Lang LaSalle

estimates each prime office market will be within

its individual rental cycle as at of 2011

• Markets can move around the clock at different

speeds and in different directions

• The diagram is a convenient method of comparing

the relative position of markets in th eir rental cycle

• Their position is not necessarily representative of

investment or development market prospects.

• Their position refers to Prime Face Rental Values

Rental Growth

Slowing

Rents

Falling

Rental Growth

Accelerating

Rents

Bottoming Out

Rental Growth

Slowing

Rents

Falling

Rental Growth

Accelerating

Rents

Bottoming Out

Rental Growth

Slowing

Rents

Falling

Rental Growth

Accelerating

Rents

Bottoming Out

Sydney, Amsterdam

Brussels, San Francisco

Frankfurt

London

Madrid

Chicago

Singapore, Moscow

Dubai

Los Angeles

Mexico CityToronto

Mumbai, New York

Tokyo, Washington DC

Q4 2011

Hong Kong

Shanghai, Sao Paulo, Paris

8/6/2019 Global Market Perspective November 2010 Final

http://slidepdf.com/reader/full/global-market-perspective-november-2010-final 6/17

COPYRIGHT © JONES LANG LASALLE IP, INC. 2010. All Rights Reserved 6

Global Market Perspective November 2010

Retail – a mature versus emerging market story

In most mature retail markets prospects for 2011 are mixed. Retailers remain cautious in the light of persistently high

unemployment, the need to repair household balance sheets and concerns over the impact of austerity measures.

Nonetheless, demand for space in prime locations and well-established malls will be strong, and many large cross-border retailers are back in expansion mode. Shopping mall completions will be at very low levels in 2011, which should

support prime rents and, in the US, help to erode the excess inventory. Problems will persist in secondary locations,

with vacancy rates in many countries showing little sign of receding significantly in the short term. Some mature markets

are expected to outperform, notably where employment growth and consumer sentiment is comparatively healthy, such

as in Hong Kong, Australia, Germany and the Nordics.

A combination of favourable demographics, robust economic growth and buoyant consumer markets in 2011 will

continue to support dynamic retail markets in the ‘E7’ - China, India, Brazil, Turkey, Mexico, Russia and Indonesia.

Most of these markets are now in the middle of a major development cycle, however strengthening retailer demand is

expected to absorb much of the new stock. Demand for new mall space is expected to be particularly strong in China as

international brands continue to open new stores. For 2011, the largest increases in retail rents are expected in Greater China.

Industrial – boosted by recovery in global trade

Industrial market fundamentals are anticipated to improve in 2011 on the back of trade and retail sales growth. An

upturn in corporate occupier activity will be helped by the faster than expected recovery in global trade flows. The WTO

has predicted global trade to increase by 13.5% in 2010, which would be the fastest year-on-year growth registered

since records began in 1950. However, in general, rental growth prospects will remain subdued in 2011, with the

industrial markets of Greater China and Singapore likely to show the strongest rental growth (of 5-15%). In the US, the

industrial property sector still faces considerable slack from a demand overhang that has now lasted two years.Prospects for the US market in 2011 are expected to be relatively flat, although gateway ports and key distribution hubs

will outperform. The industrial market in Mexico is rebounding strongly, as US manufacturers shift production south of

the border.

Demand for logistics will be driven by structural changes in international supply chains, with corporate occupiers striving

for efficiency improvements in order to contain cost levels. This will result in ongoing merger and acquisition activity,

space consolidation and upgrading to modern stock.

8/6/2019 Global Market Perspective November 2010 Final

http://slidepdf.com/reader/full/global-market-perspective-november-2010-final 7/17

COPYRIGHT © JONES LANG LASALLE IP, INC. 2010. All Rights Reserved 7

Global Market Perspective November 2010

Real Estate Capital

Banks disposing of non-performing assets

2011 looks to be a promising year for investors seeking to take advantage of distressed opportunities in commercial

real estate. Banks and servicers are beginning to adopt a more aggressive approach to the disposal of non-performingor ‘distressed’ loans, r ecognising that the uptick in capital values is providing a window of opportunity. We are likelyto see an acceleration in the pace of liquidation activity, an increase in ‘big ticket’ disposals and a decline in the

amount of time that delinquent loans are allowed to languish. Significantly, banks will take more assertive actionoutside of their homelands.

This trend indicates that banks and servicers feel that the market has adequately recovered and that they can achieve

fair pricing. At the height of the Global Financial Crisis, as transaction volume collapsed and price discovery became

highly inefficient, there was a strong incentive to hang on to non-performing loans rather than liquidate in an opaque and

illiquid market. Counter intuitively, the anticipated increase in the share of ‘distressed sales’ is a positive trend and

signals the continued recovery of real estate capital markets.

The CMBS market gathering pace in the US

We finish 2010 on a relatively strong note for the global securitised markets. In the US, CMBS issuance for full-year

2010 is likely to be three times the total for 2009, and we anticipate 2011 issuance in the US could exceed US$30 billion.

But while the CMBS markets will continue to heal, volumes will remain low by historic measures and there remains a

vital need for debt capital. What has been learned over the past 12 months is that there is a strong appetitive for

‘straightforward’ CMBS. Foundations are in place for a steady expansion of CMBS which stays true to the principles of

risk diversification across all property types and all markets with a basis in sensible underwriting.

In Europe, reports that investment banks are returning to origination are premature, although there is no doubt that they

are working hard to create new CMBS-like structures. The only open market issuance of CMBS in the past two years

has been in long-dated, credit-linked transactions, where the tenant is responsible for the payment of the coupon andprincipal of the bond, regardless of the condition of the building.

Global CMBS Issuance, 2008-2010

Source: Credit Suisse

0

5

10

15

20

US Rest of World TOTAL

U S $ b i l l i o n s

2008 2009 Q1-Q3 2010

8/6/2019 Global Market Perspective November 2010 Final

http://slidepdf.com/reader/full/global-market-perspective-november-2010-final 8/17

COPYRIGHT © JONES LANG LASALLE IP, INC. 2010. All Rights Reserved 8

Global Market Perspective November 2010

Portfolio lenders continue to focus on prime - CMBS filling the void for secondary

So far in 2010, the US commercial real estate debt markets have averted the catastrophe that many strategists had

predicted last year. Distressed loans are being efficiently amended or liquidated through the markets freeing up

capacity, and demand for new loan originations is surprisingly high. Lenders became much more aggressive in 2010 asthey foresaw stabilisation in US property values. In addition, low interest rates have made lending on property highly

rewarding for banks as they can charge significant margins and still find plentiful demand. Currently, portfolio lenders

are offering 50 to 60% leverage at terms of 5 to 10 years at rates ranging from 3.5 to 5.0%. CMBS lenders are offering

upwards of 70% leverage at similar terms at rates of 4.5 to 5.5%. We expect leverage levels at portfolio lenders to

remain in the same range in 2011 but CMBS could inch up further to 75%. We also predict that portfolio lenders will

continue to focus on prime markets with exceptions for high-quality deals in secondary markets; however, we anticipate

CMBS will fill the void for secondary market product.

Concerns over impacts of Basel III regulations

Across Western Europe, there is a steady supply of funds available for core, low loan-to-value (LTV) lending, mainly

due to the ability of German lenders to access the Pfandbrief (covered bond) market. Most lending of this nature is sub

60% LTV, as the lenders are required to hold more regulatory capital on their balance sheet for higher LTV loans. This

will be an important feature in 2011 as lenders continue to be concerned about the impact of proposed Basel III

regulations upon their regulatory capital requirements. The cost of new senior loans varies from country to country, with

sub-60% LTV loans being available at sub-100 basis point margins in Germany, at circa 115-125 basis points margin in

France, and up to 150 basis points and above in the UK. However, with increases in LTV ratios, there will also be a

rapid rise in margins.

We envisage that lenders in 2011 will continue to focus on refinancing existing loans, at the same time taking the

opportunity to increase margins and charge additional fees. The market in Central and Eastern Europe appears to be

opening up, with banks having a local presence lending in Bulgaria, Romania and Poland. There is a significant supply

of mezzanine finance being provided by investors seeking exposure at ‘stretch-senior’ levels of 65-80% at mid-teens

returns. Investors are prepared to consider both acquisition finance and recapitalisation of existing facilities.

Asian banks increasing their risk tolerance

In Asia, banks are increasing their risk tolerance and loosening their underwriting criteria as the Asia Pacific economy

continues to outperform other regions. In 2011 we expect to see margins tightening to 100 to 150 basis points down from

the 200 to 300 basis points level witnessed in 2010. Loan-to-value ratios are edging upwards towards 60% from the

depths of 50%, and then only to longstanding clients. As much as all of this is good news, lenders are still nervous.

Balance sheet and club deals are likely to continue in 2011, spreading risk among parties at deal level. While banks are

becoming more confident in the external economic environment, at the deal level they still want to share the risk.

8/6/2019 Global Market Perspective November 2010 Final

http://slidepdf.com/reader/full/global-market-perspective-november-2010-final 9/17

COPYRIGHT © JONES LANG LASALLE IP, INC. 2010. All Rights Reserved 9

Global Market Perspective November 2010

Corporate Occupiers

Divergence – the underlying theme

Divergence will be the underlying theme among corporate occupiers for 2011. There will be increasing divergence in the

favourability of global market conditions as shown in our Global Markets Conditions Matrix; in conditions within individualmarkets, particularly between core and secondary sub-markets; in the growth trajectories and strategies of corporate

occupiers from different sectors; and in the routes that occupiers adopt to bring new order to their portfolios, manage the

twin pressures of growth and right-sizing, and to engage with the market.

Global Markets Conditions Matrix, 2011-2013

Source: Jones Lang LaSalle, November 2010

Real estate strategies for the medium term

2011 will bring growing corporate occupier activity across the globe, particularly in emerging markets, but this will be

against a continued backdrop of caution amid still fragile economic and operating conditions in many advanced

economies. There is mounting evidence that occupiers are now planning their real estate strategies for the medium term

with issues such as workplace strategy, sustainability, technology and cost avoidance escalating in influence. This will

provide a further stimulus to activity in the mature markets albeit based on churn resulting from consolidation and

rationalisation, rather than via growth.

Asia Pacific – a target for growth

In Asia Pacific the dynamic is markedly different with many global corporations actively targeting the region. This is

particularly true of the banking sector. Investment banks have taken advantage of bottoming markets in Asia Pacific to

acquire space to accommodate medium-term growth and retail banks are now following suit with branch growth on the

agenda. The pharmaceutical and life sciences sector, which has had an exceptionally active 2010, will continue on this

trajectory during 2011 as consolidation works through the sector.

Growing domestic corporate demand will also be a key feature of 2011. This is certainly true of markets such as India

and China, where companies that have relatively immature corporate real estate functions and previously limited

exposure in the markets are coming to the fore. They are now seeking to take advantage of market conditions andincreased revenues to enable competition on a global scale.

Tenant Favourable

Neutral Market

Landlord Favourable

MARKET MARKET MARKET

Chicago 2011 2012 2013 Amsterdam 2011 2012 2013 Hong Kong 2011 2012 2013

Los Angeles 2011 2012 2013 Brussels 2011 2012 2013 Mumbai 2011 2012 2013

New York 2011 2012 2013 Frankfurt 2011 2012 2013 Shanghai 2011 2012 2013

San Francisco 2011 2012 2013 London 2011 2012 2013 Singapore 2011 2012 2013

Toronto 2011 2012 2013 Madrid 2011 2012 2013 Sydney 2011 2012 2013

Washington DC 2011 2012 2013 Moscow 2011 2012 2013 Tokyo 2011 2012 2013

Mexico City 2011 2012 2013 Paris 2011 2012 2013

Sao Paulo 2011 2012 2013 Dubai 2011 2012 2013

TIMELINE TIMELINE TIMELINE

8/6/2019 Global Market Perspective November 2010 Final

http://slidepdf.com/reader/full/global-market-perspective-november-2010-final 10/17

COPYRIGHT © JONES LANG LASALLE IP, INC. 2010. All Rights Reserved 10

Global Market Perspective November 2010

Supply constraints will limit relocation options and push up costs

As corporate activity rises, supply dynamics will create a significant challenge for occupiers and push costs higher. In

Europe the lack of Grade A supply across many markets will limit relocation options. Vacancy rates, which are in

double-digits across much of the region, will belie this fact but are merely reflective of the disposal of poorer-quality

supply. In the US, occupier choice remains high with numerous direct, sub-lease and, in some markets, new

construction availabilities. However, a tale of two markets is emerging in the US as vacancy rates have declined in

many core CBD locations but remained high in most suburban markets. In Asia Pacific, rental costs are forecast to rise

with strong increases in a number of prime markets, such as Hong Kong, which will move rapidly through the property

cycle during the course of 2011. There are some outliers which are over-supplied, such as Seoul and certain markets in

India and China, but almost all markets in Asia will be in a period of mounting real estate costs and thus landlord-

favourable conditions during 2011.

Pressure on CREs to provide cost-effective solutions

The proactive and efficient management of real estate is being seen as an agent for change within corporations.

Following the Global Financial Crisis there is more visibility and scrutiny of real estate costs at the ‘C-suite’ level and this

is placing more pressure on corporate real estate (CRE) teams to respond and provide appropriate cost effective realestate solutions. The CRE function, which is typically under resource and headcount constraints, will need to be smarter,

more aligned to the business and more engaged with service providers in order to respond to the growing challenge.

8/6/2019 Global Market Perspective November 2010 Final

http://slidepdf.com/reader/full/global-market-perspective-november-2010-final 11/17

COPYRIGHT © JONES LANG LASALLE IP, INC. 2010. All Rights Reserved 11

Global Market Perspective November 2010

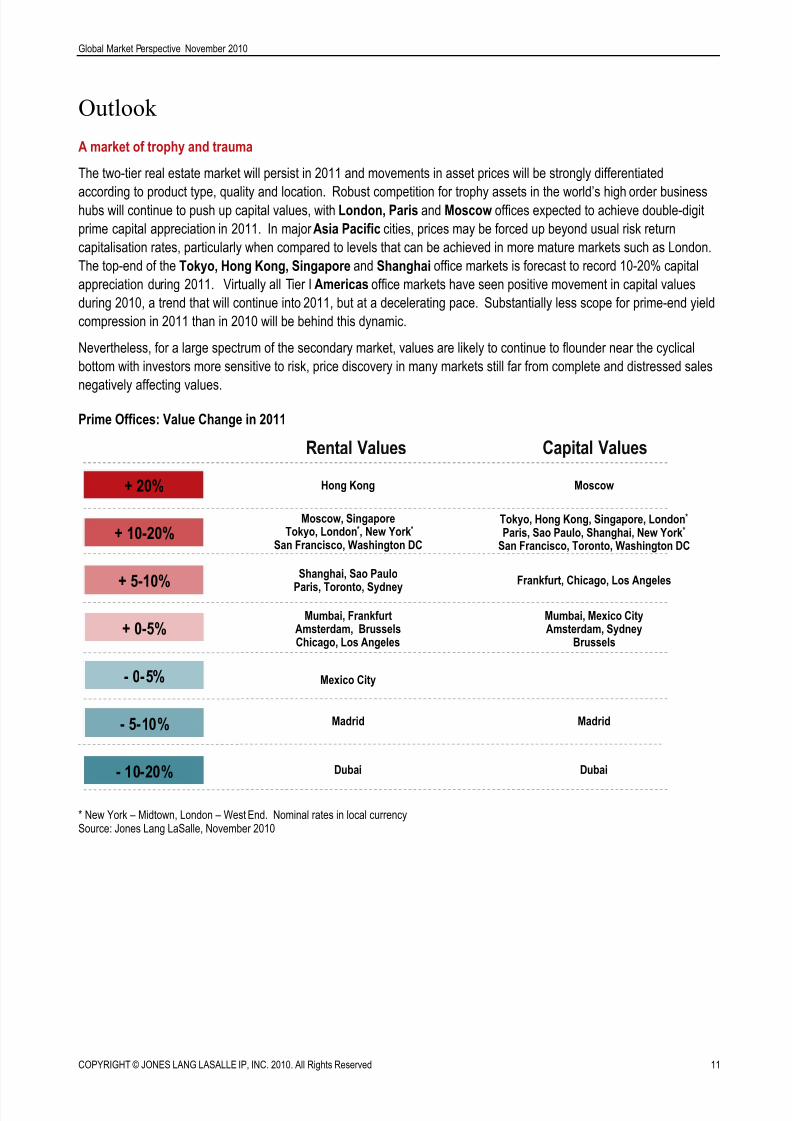

Outlook

A market of trophy and trauma

The two-tier real estate market will persist in 2011 and movements in asset prices will be strongly differentiated

according to product type, quality and location. Robust competition for trophy assets in the world’s high order businesshubs will continue to push up capital values, with London, Paris and Moscow offices expected to achieve double-digit

prime capital appreciation in 2011. In major Asia Pacific cities, prices may be forced up beyond usual risk return

capitalisation rates, particularly when compared to levels that can be achieved in more mature markets such as London.

The top-end of the Tokyo, Hong Kong, Singapore and Shanghai office markets is forecast to record 10-20% capital

appreciation during 2011. Virtually all Tier I Americas office markets have seen positive movement in capital values

during 2010, a trend that will continue into 2011, but at a decelerating pace. Substantially less scope for prime-end yield

compression in 2011 than in 2010 will be behind this dynamic.

Nevertheless, for a large spectrum of the secondary market, values are likely to continue to flounder near the cyclical

bottom with investors more sensitive to risk, price discovery in many markets still far from complete and distressed sales

negatively affecting values.

Prime Offices: Value Change in 2011

* New York – Midtown, London – West End. Nominal rates in local currencySource: Jones Lang LaSalle, November 2010

+ 10-20%

Capital ValuesRental Values

Moscow, SingaporeTokyo, London*, New York*

San Francisco, Washington DC

+ 5-10%

+ 0-5%

- 0-5%

- 5-10%

Shanghai, Sao Paulo

Paris, Toronto, Sydney

Mumbai, FrankfurtAmsterdam, BrusselsChicago, Los Angeles

Madrid

+ 20%

Tokyo, Hong Kong, Singapore, London*

Paris, Sao Paulo, Shanghai, New York*

San Francisco, Toronto, Washington DC

Moscow

Frankfurt, Chicago, Los Angeles

Mumbai, Mexico CityAmsterdam, Sydney

Brussels

Madrid

Hong Kong

- 10-20% Dubai Dubai

Mexico City

8/6/2019 Global Market Perspective November 2010 Final

http://slidepdf.com/reader/full/global-market-perspective-november-2010-final 12/17

COPYRIGHT © JONES LANG LASALLE IP, INC. 2010. All Rights Reserved 12

Global Market Perspective November 2010

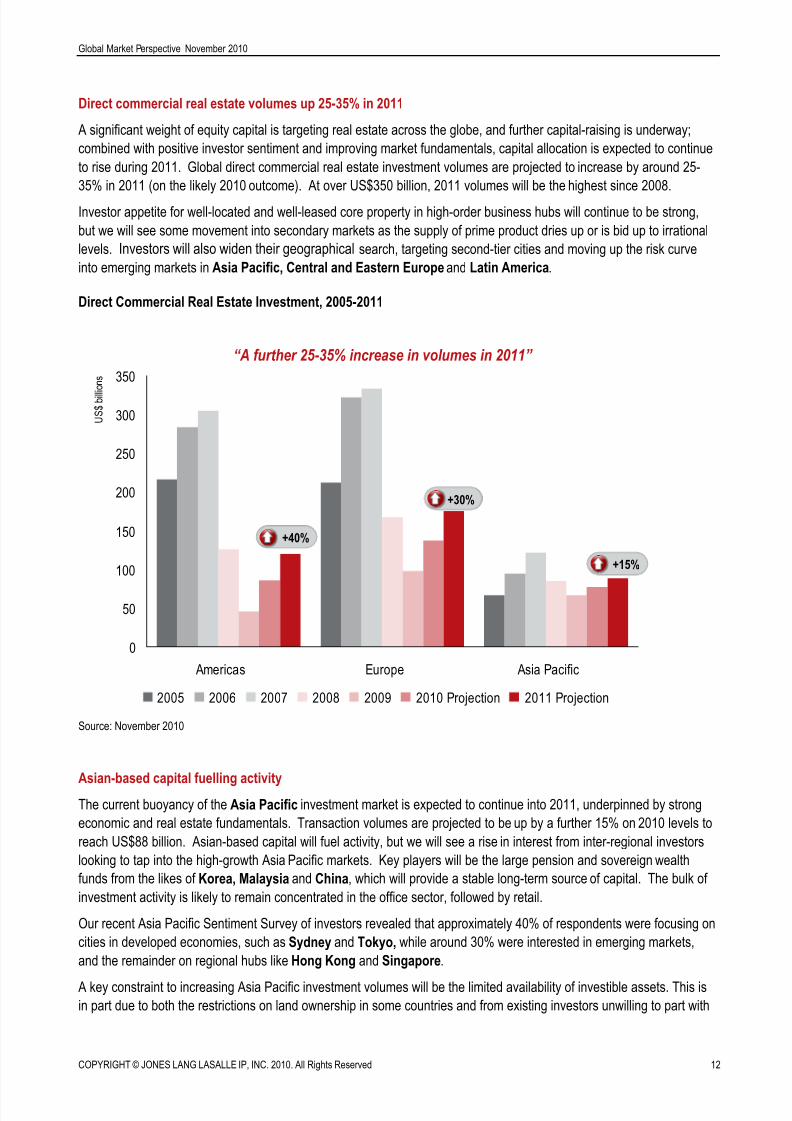

Direct commercial real estate volumes up 25-35% in 2011

A significant weight of equity capital is targeting real estate across the globe, and further capital-raising is underway;

combined with positive investor sentiment and improving market fundamentals, capital allocation is expected to continue

to rise during 2011. Global direct commercial real estate investment volumes are projected to increase by around 25-

35% in 2011 (on the likely 2010 outcome). At over US$350 billion, 2011 volumes will be the highest since 2008.

Investor appetite for well-located and well-leased core property in high-order business hubs will continue to be strong,

but we will see some movement into secondary markets as the supply of prime product dries up or is bid up to irrational

levels. Investors will also widen their geographical search, targeting second-tier cities and moving up the risk curve

into emerging markets in Asia Pacific, Central and Eastern Europe and Latin America.

Direct Commercial Real Estate Investment, 2005-2011

Source: November 2010

Asian-based capital fuelling activityThe current buoyancy of the Asia Pacific investment market is expected to continue into 2011, underpinned by strong

economic and real estate fundamentals. Transaction volumes are projected to be up by a further 15% on 2010 levels to

reach US$88 billion. Asian-based capital will fuel activity, but we will see a rise in interest from inter-regional investors

looking to tap into the high-growth Asia Pacific markets. Key players will be the large pension and sovereign wealth

funds from the likes of Korea, Malaysia and China, which will provide a stable long-term source of capital. The bulk of

investment activity is likely to remain concentrated in the office sector, followed by retail.

Our recent Asia Pacific Sentiment Survey of investors revealed that approximately 40% of respondents were focusing on

cities in developed economies, such as Sydney and Tokyo, while around 30% were interested in emerging markets,

and the remainder on regional hubs like Hong Kong and Singapore.

A key constraint to increasing Asia Pacific investment volumes will be the limited availability of investible assets. This isin part due to both the restrictions on land ownership in some countries and from existing investors unwilling to part with

0

50

100

150

200

250

300

350

Americas Europe Asia Pacific

U S $ b i l l i o n s

2005 2006 2007 2008 2009 2010 Projection 2011 Projection

+40%+40%

+30%+30%

+15%+15%

“A further 25-35% increase in volumes in 2011”

8/6/2019 Global Market Perspective November 2010 Final

http://slidepdf.com/reader/full/global-market-perspective-november-2010-final 13/17

COPYRIGHT © JONES LANG LASALLE IP, INC. 2010. All Rights Reserved 13

Global Market Perspective November 2010

their assets at a price buyers are prepared to pay. Currency appreciation, rising interest rates and increasing

government intervention to cool price growth may also dampen activity.

A broad range of investors targeting Europe

Investor sentiment across Europe is positive - a broad range of investors are targeting prime European real estate and

significant capital raising activity is underway. 2011 investment volumes are projected to be around €130 billion,representing a 30% increase on the likely 2010 outcome. Speed of execution is likely to accelerate, reflecting a growing

willingness to do deals. The large, liquid and transparent markets in the UK, France and Germany will attract the

majority of funds, with their focus being on London and Paris. Nonetheless, investors will widen their geographic

search, and we will see increased trading in the Nordic markets, Central and Eastern Europe and Moscow. Our

forecasts suggests little variation in returns at a sector level, but overall offices and retail will continue to have the

attention of most funds.

Transaction volumes could be held back by a lack of lending and continued low levels of trading in secondary assets

which, in most markets, are still considered too risky at current pricing levels. That said, we may see pricing

expectations on secondary assets shifting to become more realistic, in large part driven by disposals from the banks (or

from former bank stock held by NAMA). This will boost trading volumes.

Positive outlook for the Americas

The outlook for commercial investment sales activity is turning more positive across the Americas region. Volumes in

2010 are likely to be up by at least 90% over 2009, and the 2011 total is projected to increase by a further 40% over

2010 levels. However, volumes in 2011 may be slightly more back-ended than typical as investors take a measured

pause early in the year to digest pricing trends and to work out fair value given the tremendous capitalisation rate

compression in top-tier US office product during 2010.

There is approximately US$250 billion of equity earmarked for US real estate and, with most investors chasing core

office product in gateway cities, a significant scarcity premium has been created. The strong investor interest in core

gateway city product will continue, but we will see a greater push into cities such as Chicago, Seattle, Houston andDallas. Demand for multi-family product, from both domestic and international investors, is expected to strengthen.

Meanwhile, investor demand for retail assets will grow at a more cautious pace as the sector trails all others in the

bottoming-out of its market fundamentals.

International investors, who have avoided the broad debt market difficulties of the past few years, are returning to the US

market en masse. Buyers from Germany, the United Kingdom, Korea and Japan are seeking stable, well-located

assets in primary markets.

Prospects in Latin America, and particularly Brazil, will continue to brighten for investors, as the groundwork is laid for a

more definitive move from tenant to landlord-favourable markets.

Investor sentiment stabilising in MENA

In the MENA (Middle East and North Africa) region, investor sentiment is stabilising. Higher oil prices are resulting in

significant capital inflows into the region and, while most of these funds will be reinvested locally in infrastructure etc, a

proportion will find a home in international real estate. Jones Lang LaSalle’s recent Real Estate Investor Sentiment

Survey – Middle East & North Africa reveals that MENA real estate investors remain focused on Western Europe and

the UK in particular. The appetite for Asia real estate is increasing, although this has not yet been reflected in actual

transactions. Within MENA, there is growing interest in opportunities in North Africa, most particularly Egypt, and

Saudi Arabia. Both of these markets are benefiting from increasing demand from a large and growing population and a

shortage of high-quality modern real estate.

8/6/2019 Global Market Perspective November 2010 Final

http://slidepdf.com/reader/full/global-market-perspective-november-2010-final 14/17

COPYRIGHT © JONES LANG LASALLE IP, INC. 2010. All Rights Reserved 14

Global Market Perspective November 2010

Hotel Market Outlook

Sustained upturn in 2011

Across the globe most hotel investment markets are exhibiting stronger-than-expected signs of recovery. Tradingfundamentals continue to improve and investor confidence remains upbeat – setting the stage for a sustained upturn in

2011. For the full year 2010, we are now anticipating transaction volumes to increase by approximately 85% over 2009

to finish the year at US$17-18 billion1, substantially higher than our previous forecast of US$12-14 billion.

Barring any unforeseen circumstances, we are expecting another year of substantial growth in 2011. In the latest

November 2010 edition of Jones Lang LaSalle Hotels’ Hotel Investor Sentiment Survey (HISS), market optimism is

reflected in the notable increase in investor expectations for global short-term trading (+10.9% to 11.7%), with positive

short-term trading now expected in 61 of the 97 markets tracked. Yield requirements have also continued to firm up over

the past six months, with capitalisation rates falling 50 basis points to 8.3% and leveraged IRRs falling 110 basis points

to 17.0%.

Recovery led by the Americas

We expect the pace of recovery and growth will continue to be led by the Americas, particularly the US and Canada.

Investor ‘buy’ sentiments are strongest in the Americas (43%), and North American markets dominate the top 10 global

markets for buying - headed by Vancouver (77.8%), Boston (71.9%) and New York (71.1%).

Substantial equity seeking hotel real estate

Availability of capital, from both equity and debt sources, will continue to be a key driver of hotel investment activity in

2011. Globally, substantial equity is still available in the market waiting to be invested in hotel real estate, and a

significant proportion of acquisitions will continue to be completed with all equity or limited leverage. Debt liquidity for

both acquisitions and refinancings is also slowly improving along with lending terms, particularly in the US and WesternEurope. A few hotels-backed debt securitisations have been issued in 2010 and more are expected to surface during

the course of 2011. However, given continued regulatory changes/requirements we do not anticipate the availability of

debt to increase dramatically. On the other hand, the need to clean up balance sheets will mean that banks, lenders,

special servicers and inadvertent hotel owners are likely be the most motivated sellers in 2011.

Cross-border investors are expected to feature strongly again in 2011. As with 2010 we predict Asian-based investors to

continue to be among the most active cross-border players and we forecast increased cross-border capital flows to

originate from North America and the Middle East.

1 Excludes the US$3.9 billion paid by Blackstone, Paulson & Co, and Centerbridge Partners to bring the Extended Stay Americahotel chain out of bankruptcy in October 2010.

8/6/2019 Global Market Perspective November 2010 Final

http://slidepdf.com/reader/full/global-market-perspective-november-2010-final 15/17

COPYRIGHT © JONES LANG LASALLE IP, INC. 2010. All Rights Reserved 15

Global Market Perspective November 2010

Recent Key Transactions

Asia Pacific

Australia, Ayers Rock

The Ayers Rock Resort has been sold for A$300 million (circa US$300 million) to the Indigenous Land Corporation. Theresort is the country’s largest accommodation asset, and the sale represents one of Australia’s largest-ever single asset

hotel transactions.

Australia, Brisbane

Westscheme, a A$3.2billion (US$3.2 billion) superannuation fund, has disposed of its ownership interests in Brisbane

Square for A$300 million (US$300 million) to the Charter Hall Core Plus Office Fund and Telstra Super. The price of this

‘A’ grade commercial office tower located in the CBD reflected a 6.6% yield.

Australia, Melbourne

REST Industry Super has bought a new A$240 million (US$240 million) Docklands building, 717 Bourke Street, in

Melbourne’s largest office deal so far in 2010. The 37,000 square metre building was purchased from a joint venture

between Babcock & Brown and Melbourne Civic City at an 8% yield.

China, Shanghai

Grosvenor, an international property development, investment and fund management group, has recently bought the

Shanghai Changfeng international entertainment business centre for nearly RMB1.5 billion (US$225 million).

Hong Kong

An unidentified overseas buyer has paid HK$338 million (US$44 million) for a 1,228 square metre floor at The Center in

Central. Based on Land Registry data, the 79th floor was sold for HK$275,354 (US$35,530) per square metre,

representing a new record on a price per square metre basis for Hong Kong office space. The seller is Magic Ace Co, a

South Korean firm.

Japan, OsakaRREEF Investment has acquired a retail property on Shinsaibashisuji for around US$238 million from Japanese real

estate corporation, Socrates TMK.

Japan, Tokyo

Tokyu REIT has bought two office buildings for ¥8.6 billion (US$107 million) from real estate company GK Asok. The

listed company is paying ¥4.6 billion (US$57 million) for the Akihabara Sanwa Toyo Building and ¥4.0 billion (US$50

million) for the Kiba Eitai Building; both are 100% leased.

Singapore

City Developments Limited (CDL) has sold The Corporate Office, a 21-storey 10,200 square metre freehold office

building to a consortium led by Oxley Holdings group for S$215 million (US$165 million).

Singapore

Suntec REIT has acquired a one-third interest in a number of properties in Phase One of Marina Bay Financial Centre

(MBFC) for S$1.49 billion (US$1.15 billion). The vendors are Cheung Kong (Holdings) and Hutchison Whampoa of Hong

Kong.

South Korea, Seoul

Alpha Investment Partners’ Macro Trends Fund has invested US$210 million in the Seoul Square office building.

8/6/2019 Global Market Perspective November 2010 Final

http://slidepdf.com/reader/full/global-market-perspective-november-2010-final 16/17

COPYRIGHT © JONES LANG LASALLE IP, INC. 2010. All Rights Reserved 16

Global Market Perspective November 2010

Europe

France, Paris

Hammerson has sold 51% of its interest in the 90,000 square metre O’ Parinor Shopping Centre in Aulnay-sous-Bois

near Paris for a reported €224 million (c.US$305 million). The purchaser was the National Pension Service of Korea,advised by Rockspring Property Investment Managers.

Germany, Frankfurt

JP Morgan is reported to have acquired the OpernTurm trophy office building (67,000 square metres) from developer

Tishman Speyer for an estimated €600 million (c. $US840 million).

Netherlands, Amsterdam

German real estate fund, NordCapital has acquired the recently completed office building, Westgate II, from Lips Capital

Group for approximately €100 million (US$135 million) with a gross yield of 6.35%. The building is located in the

Riekerpolder area, comprises approximately 30,000 square metres and is fully let to PricewaterhouseCoopers as their

Dutch head office.

Nordic Region

Sweden-based hotel property company Pandox AB has acquired Norgani Hotels AS for NOK8.3 billion (US$1.4 billion).

Norgani's portfolio consists of 73 hotel properties totalling 12,900 rooms located in Sweden, Finland, Norway and

Denmark and one conference centre (in Helsinki).

Russia, Moscow

RBN Capital (a Russian investor) has acquired Domnikov Business Centre (two office buildings) for around €180 million

(c. US$250 million).

Sweden, Stockholm

Swedish pension fund AMF has sold City Cronan, a 41,700 square metre CBD office building to Deka Immobilien.

UK, LondonNorges Bank Investment Management, which manages the Norwegian Government Pension Fund Global, has agreed to

buy a 150-year lease on a 25% stake in The Crown Estate’s Regent Street properties for £448 million (US$720 million).

UK, London

The Employees Provident Fund (EPF), a major Malaysian government pension fund has acquired One Sheldon Square,

an 18,000 square metre office building on the Paddington Central development. The freehold was acquired from a

consortium of investors comprising Aviva Investors, Invista, Henderson Global Investors and US-based Liquid Realty

Partners for £157 million (US$250 million). This acquisition represents EPF’s first UK purchase following their

commitment alongside Kumpulan Wang Persaraan (KWAP), the other main Malaysian government pension fund, to

invest up to £1 billion (US$1.6 billion) in the UK property market

Americas

Brazil, Rio de Janeiro

Tishman Speyer has sold for R$680 million (US$400 million) a majority interest in its Ventura Corporate Tower II office

development to BR Properties. At a reported estimated yield of 11%, the interest sold represented 81% of the property.

Brazil, Sao Paulo

The Madison Building retail property has been sold for approximately R$52 million (US$30 million) to Eccelera at a

reported yield of 11.3%.

Canada, Calgary

A C$61 million (US$61 million) two-building office property has been traded on Quarry Park Boulevard in the Shepard

Industrial area. Standard Life purchased the property from Remington Properties.

8/6/2019 Global Market Perspective November 2010 Final

http://slidepdf.com/reader/full/global-market-perspective-november-2010-final 17/17

Global Market Perspective November 2010

Canada, Toronto

In the sub-market of Scarborough, Dundee REIT has purchased the Corporate Plaza office building for c. C$$31 million

(US$31 million).

Mexico, Mexico City

In the Polanco office sub-market, a private undisclosed owner has sold the Ejercito National 425 building for

approximately US$41 million to Operadora DI.

United States

The Blackstone Group, Paulson & Co and Centerbridge Partners have acquired Extended Stay America Inc, a chain of

about 680 hotels, for US$3.9 billion, bringing the company out of bankruptcy. In conjunction with this acquisition, the

purchasers lined up US$2 billion of debt from JP Morgan and Deutsche Bank that was securitised through a single loan

CMBS.

US, California

In Southern California’s Inland Empire, a 149,000 square metre distribution centre has been traded for approximately

US$85 million. LBA Realty bought the facility, with tenants including Ingram Micro and Ferguson Enterprises, from

Pacific Newport Properties.US, Chicago

In the suburban market, the 59,000 square metre Triangle Plaza office complex has been acquired by Commonwealth

REIT for approximately US$96 million and a reported yield of circa 7%. The vendor of the two-tower property was The

John Buck Company.

US, Hawaii

On Oahu, a joint venture of Glimcher Realty Trust and The Blackstone Group has acquired Pearlridge Center, a 111,000

square metre mall for about US$245 million. Northwestern Mutual Life has sold the mall at a reported 7.4% yield.

US, Los Angeles

The Wilshire Bundy Plaza office property in Westside has been sold for US$111 million. The purchaser, Douglas

Emmett Realty, also assumed the mortgage on the property from vendor Namco Capital Group.

COPYRIGHT © JONES LANG LASALLE IP, INC. 2010.

This report has been prepared solely for information purposes and does not necessarily purport to be a complete analysis of the topics discussed, which are inherentlyunpredictable. It has been based on sources we believe to be reliable, but we have not independently verified those sources and we do not guarantee that the information inthe report is accurate or complete. Any views expressed in the report reflect our judgment at this date and are subject to change without notice. Statements that are forward-looking involve known and unknown risks and uncertainties that may cause future realities to be materially different from those implied by such forward-lookingstatements. Advice we give to clients in particular situations may differ from the views expressed in this report. No investment or other business decisions should be made based solely on the views expressed in this report.