Dr. Rick Sibbel - Pharmaceutical Industry Perspective of the Impacts of the Regulatory Environment

Pharmaceutical Market Perspective

Policy Dialogue on Universal Health Care & Access to Medicines

25 July 2013

Disclaimer

IMS does not warrant that the information contained herein shall meet the present or future needs or objectives of the recipient, who assumes sole responsibility for the use, selection, and suitability of the said information to its needs and objectives. IMS shall not be liable for any expressions of opinion, evaluations, or forecasts contained in the said information. For Services or deliverables provided by IMS Health which contain forward-looking statements or projections, it is acknowledged by the Parties that such forward-looking statements or projections are subject to known and unknown risks, uncertainties, and other factors which could cause the actual results or performance to differ from such projections, and IMS shall not be responsible for and disclaims any liability arising from any such differences. IMS does not accept or assume responsibility to any person or third party for any matter contained in or referred to in the information provided in accordance with these Services or for any reliance placed on the information contained in this presentation or deliverables resulting from these Services.

Agenda

• The Philippine pharma market (size & growth)

• Market share trends

• Ethical vs. OTC

• Retail vs. hospital sectors

• Innovators vs. branded generics vs. unbranded generics

• Philippines

• Comparator Asian countries

• Post-MDRP/GMAP scenario (snapshots for select molecules)

• Summary: Prospects for the Philippine pharma market

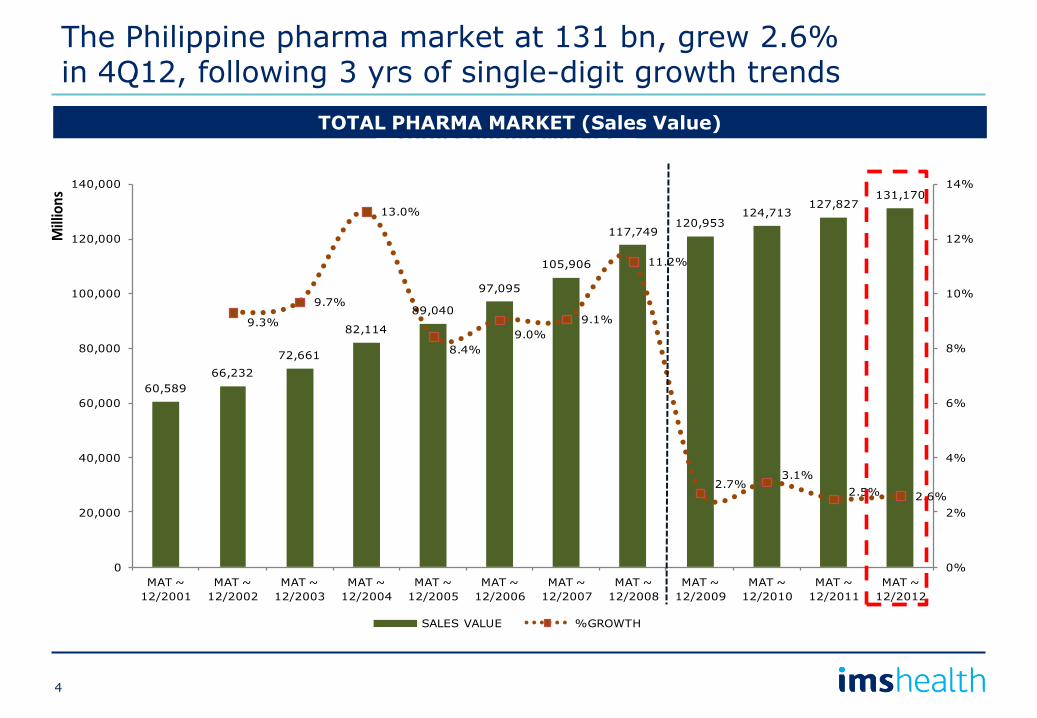

60,589

66,232

72,661

82,114

89,040

97,095

105,906

117,749120,953

124,713127,827

131,170

9.3%

9.7%

13.0%

8.4%

9.0%

9.1%

11.2%

2.7%3.1%

2.5% 2.6%

0%

2%

4%

6%

8%

10%

12%

14%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

MAT ~

12/2001

MAT ~

12/2002

MAT ~

12/2003

MAT ~

12/2004

MAT ~

12/2005

MAT ~

12/2006

MAT ~

12/2007

MAT ~

12/2008

MAT ~

12/2009

MAT ~

12/2010

MAT ~

12/2011

MAT ~

12/2012

Millions

Total Pharma Marketin Sales Value

SALES VALUE %GROWTH

TOTAL PHARMA MARKET (Sales Value)

The Philippine pharma market at 131 bn, grew 2.6% in 4Q12, following 3 yrs of single-digit growth trends

4

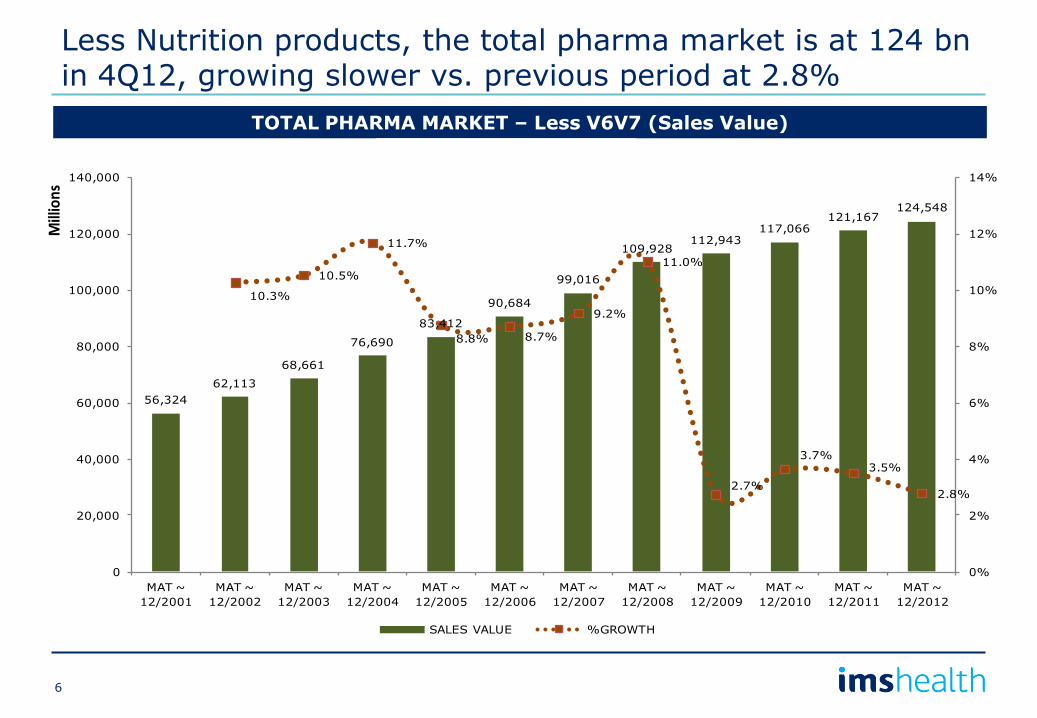

56,324

62,113

68,661

76,690

83,412

90,684

99,016

109,928112,943

117,066121,167

124,548

10.3%

10.5%

11.7%

8.8% 8.7%

9.2%

11.0%

2.7%

3.7%3.5%

2.8%

0%

2%

4%

6%

8%

10%

12%

14%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

MAT ~

12/2001

MAT ~

12/2002

MAT ~

12/2003

MAT ~

12/2004

MAT ~

12/2005

MAT ~

12/2006

MAT ~

12/2007

MAT ~

12/2008

MAT ~

12/2009

MAT ~

12/2010

MAT ~

12/2011

MAT ~

12/2012

Millions

Total Pharma Market less V6V7in Sales Value

SALES VALUE %GROWTH

TOTAL PHARMA MARKET – Less V6V7 (Sales Value)

Less Nutrition products, the total pharma market is at 124 bn in 4Q12, growing slower vs. previous period at 2.8%

6

Agenda

• The Philippine pharma market (size & growth)

• Market share trends

• Ethical vs. OTC

• Retail vs. hospital sectors

• Innovators vs. branded generics vs. unbranded generics

• Philippines

• Comparator Asian countries

• Post-MDRP/GMAP scenario (snapshots for select molecules)

• Summary: Prospects for the Philippine pharma market

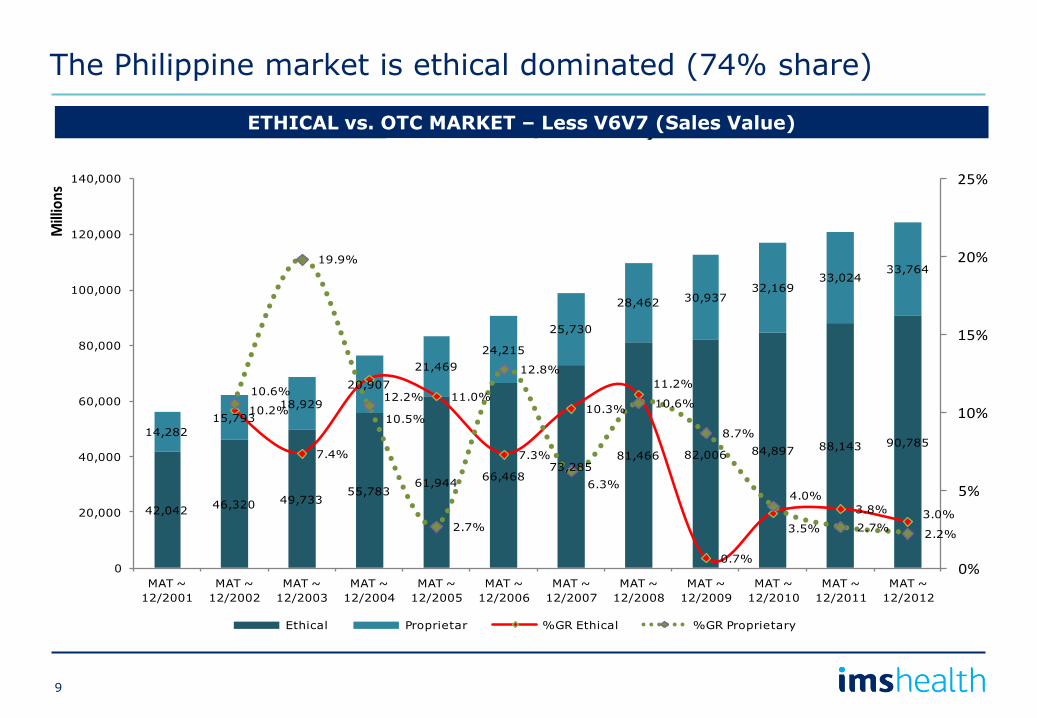

42,04246,320 49,733

55,78361,944

66,46873,285

81,466 82,006 84,897 88,143 90,78514,282

15,793

18,929

20,907

21,469

24,215

25,730

28,462 30,93732,169

33,02433,764

10.2%

7.4%

12.2% 11.0%

7.3%

10.3%

11.2%

0.7%

3.5%

3.8% 3.0%

10.6%

19.9%

10.5%

2.7%

12.8%

6.3%

10.6%

8.7%

4.0%

2.7%2.2%

0%

5%

10%

15%

20%

25%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

MAT ~

12/2001

MAT ~

12/2002

MAT ~

12/2003

MAT ~

12/2004

MAT ~

12/2005

MAT ~

12/2006

MAT ~

12/2007

MAT ~

12/2008

MAT ~

12/2009

MAT ~

12/2010

MAT ~

12/2011

MAT ~

12/2012

Millions

Ethical vs. OTC (less V6V7)in Sales Value

Ethical Proprietar %GR Ethical %GR Proprietary

ETHICAL vs. OTC MARKET – Less V6V7 (Sales Value)

The Philippine market is ethical dominated (74% share)

9

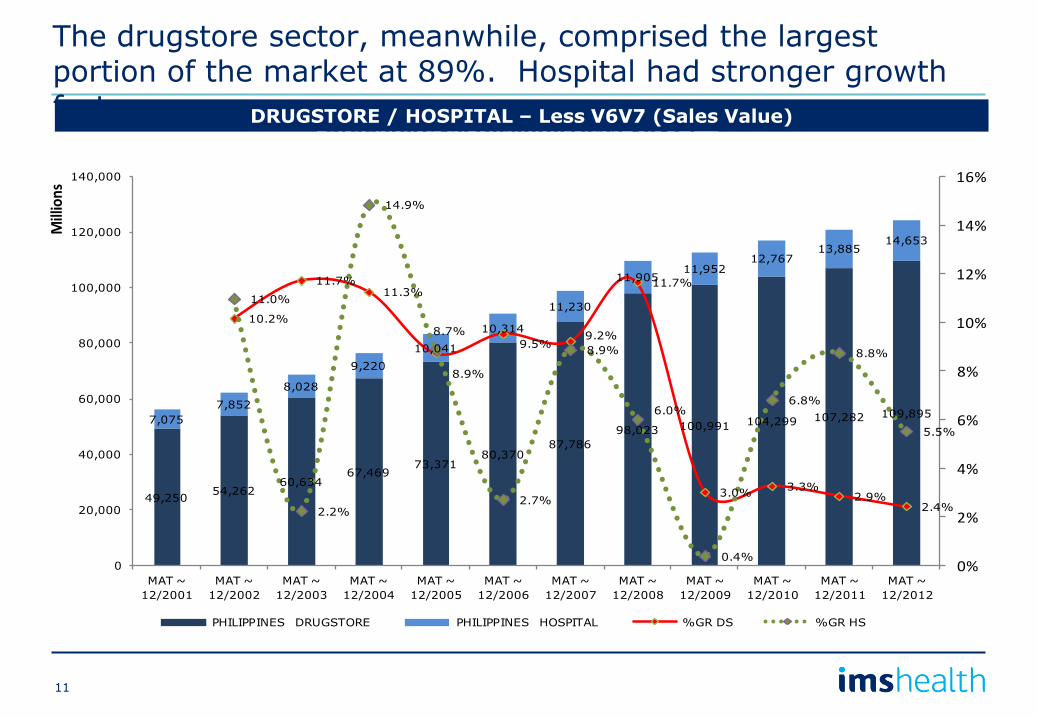

49,25054,262

60,63467,469

73,37180,370

87,786

98,023 100,991 104,299 107,282 109,8957,075

7,852

8,028

9,220

10,041

10,314

11,230

11,90511,952

12,76713,885

14,653

10.2%

11.7%11.3%

8.7%9.5%

9.2%

11.7%

3.0%3.3%

2.9%2.4%

11.0%

2.2%

14.9%

8.9%

2.7%

8.9%

6.0%

0.4%

6.8%

8.8%

5.5%

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

MAT ~

12/2001

MAT ~

12/2002

MAT ~

12/2003

MAT ~

12/2004

MAT ~

12/2005

MAT ~

12/2006

MAT ~

12/2007

MAT ~

12/2008

MAT ~

12/2009

MAT ~

12/2010

MAT ~

12/2011

MAT ~

12/2012

Millions

Drugstore vs. Hospital (less V6V7)in Sales Value

PHILIPPINES DRUGSTORE PHILIPPINES HOSPITAL %GR DS %GR HS

DRUGSTORE / HOSPITAL – Less V6V7 (Sales Value)

The drugstore sector, meanwhile, comprised the largest portion of the market at 89%. Hospital had stronger growth faster

11

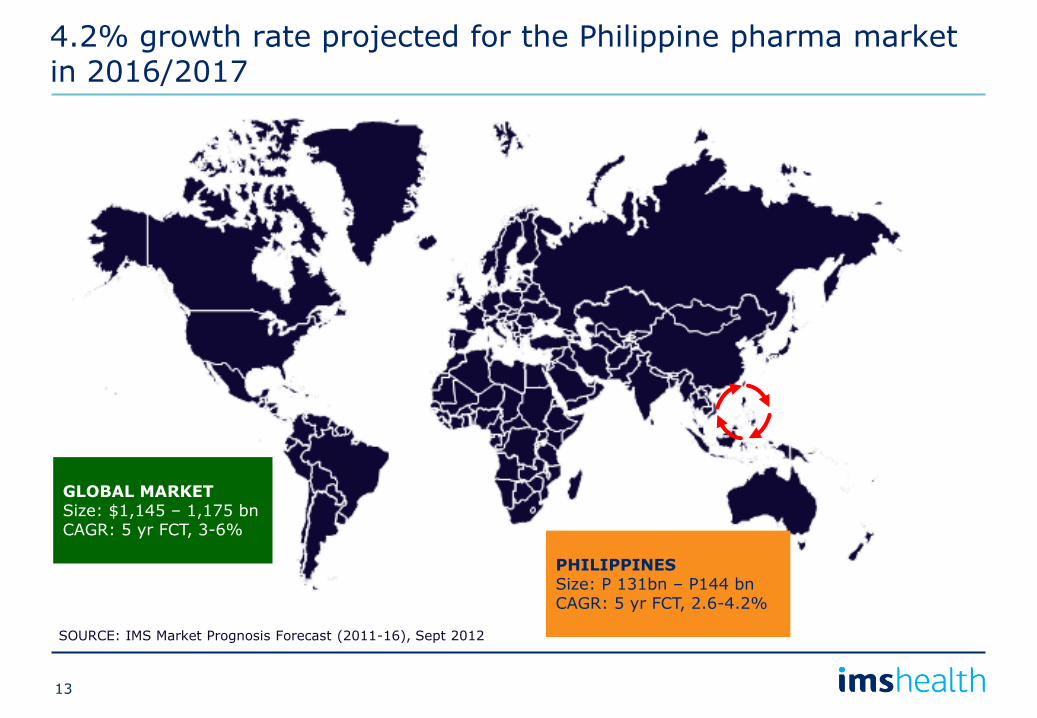

4.2% growth rate projected for the Philippine pharma market in 2016/2017

SOURCE: IMS Market Prognosis Forecast (2011-16), Sept 2012

GLOBAL MARKET Size: $1,145 – 1,175 bn CAGR: 5 yr FCT, 3-6%

PHILIPPINES Size: P 131bn – P144 bn CAGR: 5 yr FCT, 2.6-4.2%

13

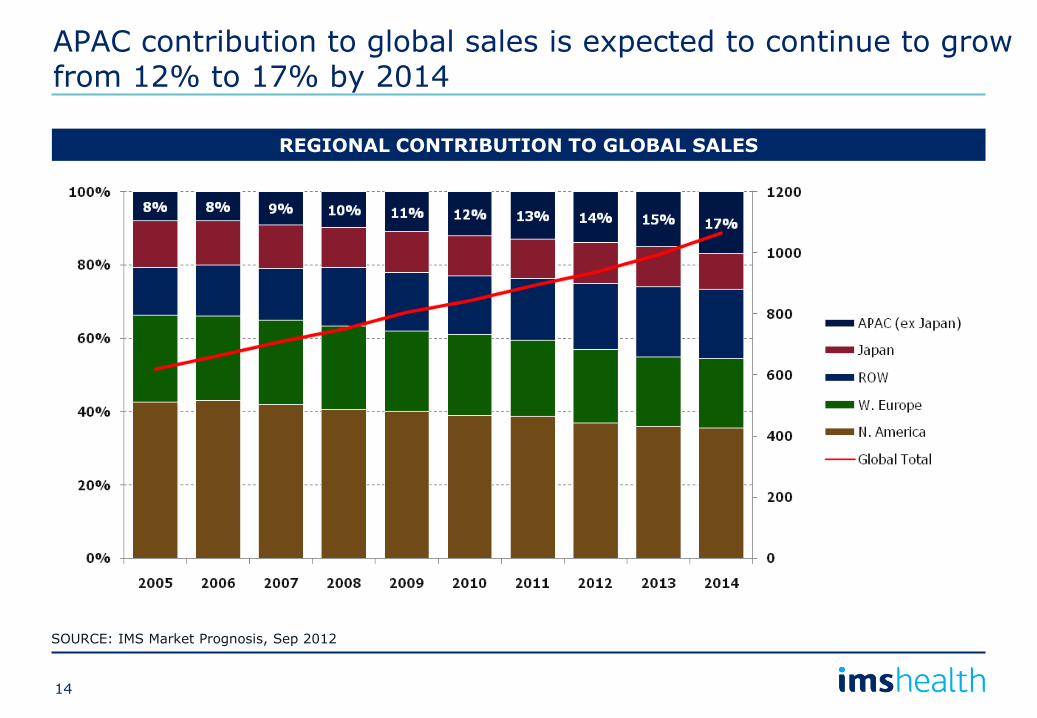

APAC contribution to global sales is expected to continue to grow from 12% to 17% by 2014

SOURCE: IMS Market Prognosis, Sep 2012

REGIONAL CONTRIBUTION TO GLOBAL SALES

14

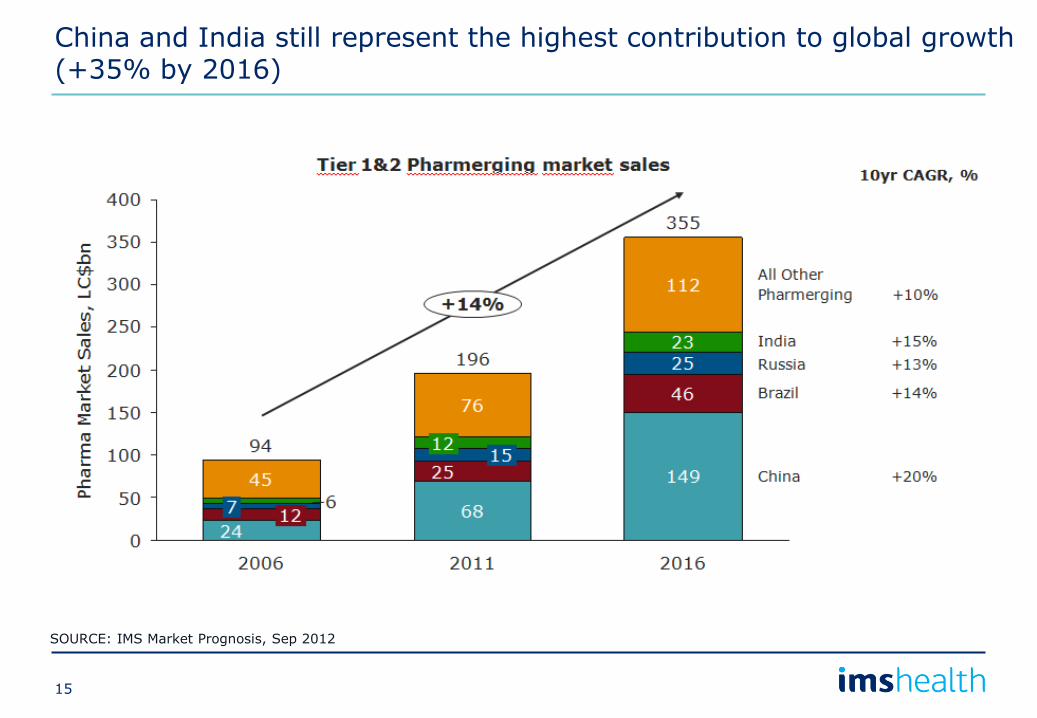

China and India still represent the highest contribution to global growth (+35% by 2016)

SOURCE: IMS Market Prognosis, Sep 2012

15

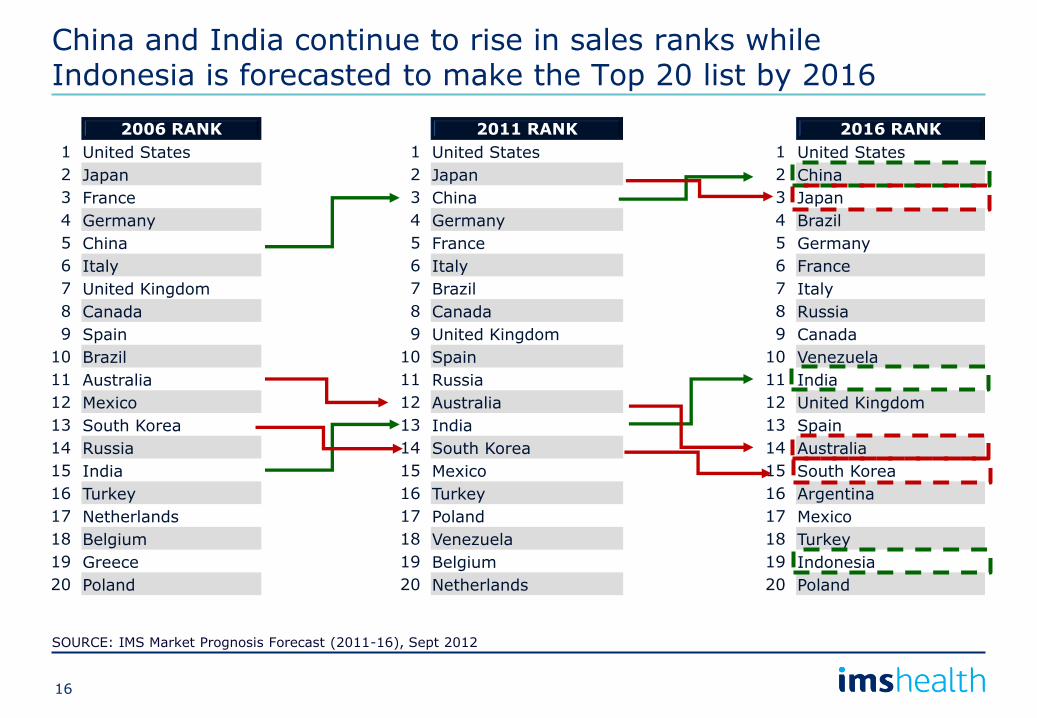

China and India continue to rise in sales ranks while Indonesia is forecasted to make the Top 20 list by 2016

2006 RANK 2011 RANK 2016 RANK

1 United States 1 United States 1 United States

2 Japan 2 Japan 2 China

3 France 3 China 3 Japan

4 Germany 4 Germany 4 Brazil

5 China 5 France 5 Germany

6 Italy 6 Italy 6 France

7 United Kingdom 7 Brazil 7 Italy

8 Canada 8 Canada 8 Russia

9 Spain 9 United Kingdom 9 Canada

10 Brazil 10 Spain 10 Venezuela

11 Australia 11 Russia 11 India

12 Mexico 12 Australia 12 United Kingdom

13 South Korea 13 India 13 Spain

14 Russia 14 South Korea 14 Australia

15 India 15 Mexico 15 South Korea

16 Turkey 16 Turkey 16 Argentina

17 Netherlands 17 Poland 17 Mexico

18 Belgium 18 Venezuela 18 Turkey

19 Greece 19 Belgium 19 Indonesia

20 Poland 20 Netherlands 20 Poland

SOURCE: IMS Market Prognosis Forecast (2011-16), Sept 2012

16

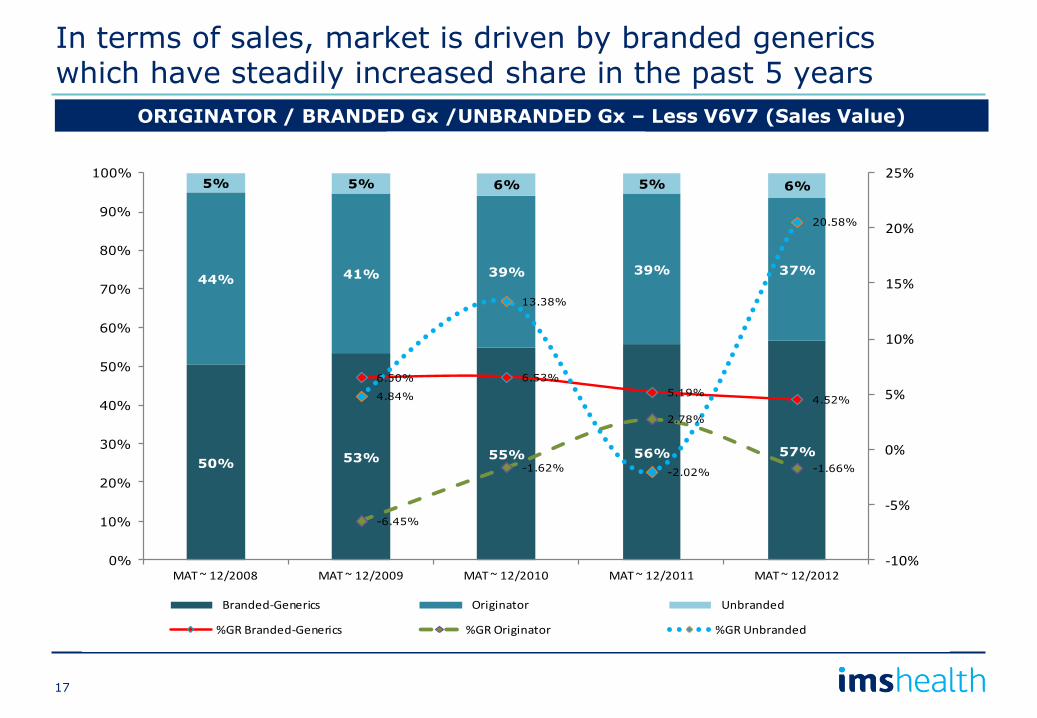

50% 53% 55% 56% 57%

44% 41% 39% 39% 37%

5% 5% 6% 5% 6%

6.50% 6.53%

5.19%4.52%

-6.45%

-1.62%

2.78%

-1.66%

4.84%

13.38%

-2.02%

20.58%

-10%

-5%

0%

5%

10%

15%

20%

25%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

MAT ~ 12/2008 MAT ~ 12/2009 MAT ~ 12/2010 MAT ~ 12/2011 MAT ~ 12/2012

Ethical Market less V6V7Share Trend in Sales Value

Branded-Generics Originator Unbranded

%GR Branded-Generics %GR Originator %GR Unbranded

ORIGINATOR / BRANDED Gx /UNBRANDED Gx – Less V6V7 (Sales Value)

In terms of sales, market is driven by branded generics which have steadily increased share in the past 5 years

17

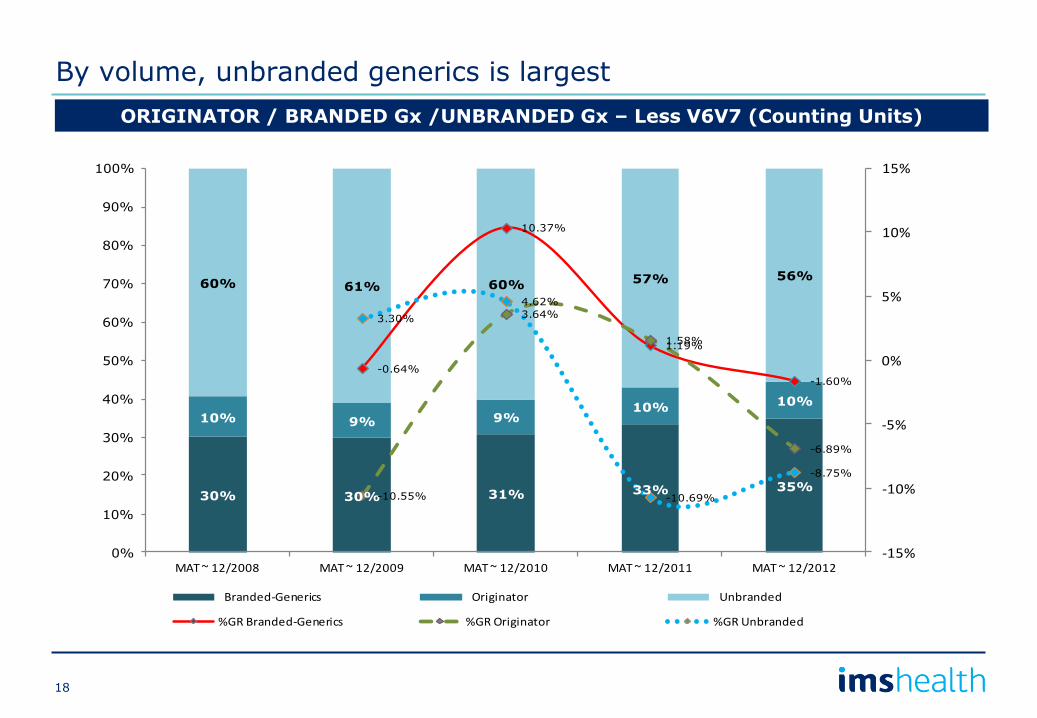

30% 30% 31% 33% 35%

10% 9% 9%10%

10%

60% 61% 60% 57% 56%

-0.64%

10.37%

1.19%

-1.60%

-10.55%

3.64%

1.58%

-6.89%

3.30%

4.62%

-10.69%

-8.75%

-15%

-10%

-5%

0%

5%

10%

15%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

MAT ~ 12/2008 MAT ~ 12/2009 MAT ~ 12/2010 MAT ~ 12/2011 MAT ~ 12/2012

Ethical Market less V6V7Share Trend in Counting Units

Branded-Generics Originator Unbranded

%GR Branded-Generics %GR Originator %GR Unbranded

ORIGINATOR / BRANDED Gx /UNBRANDED Gx – Less V6V7 (Counting Units)

By volume, unbranded generics is largest

18

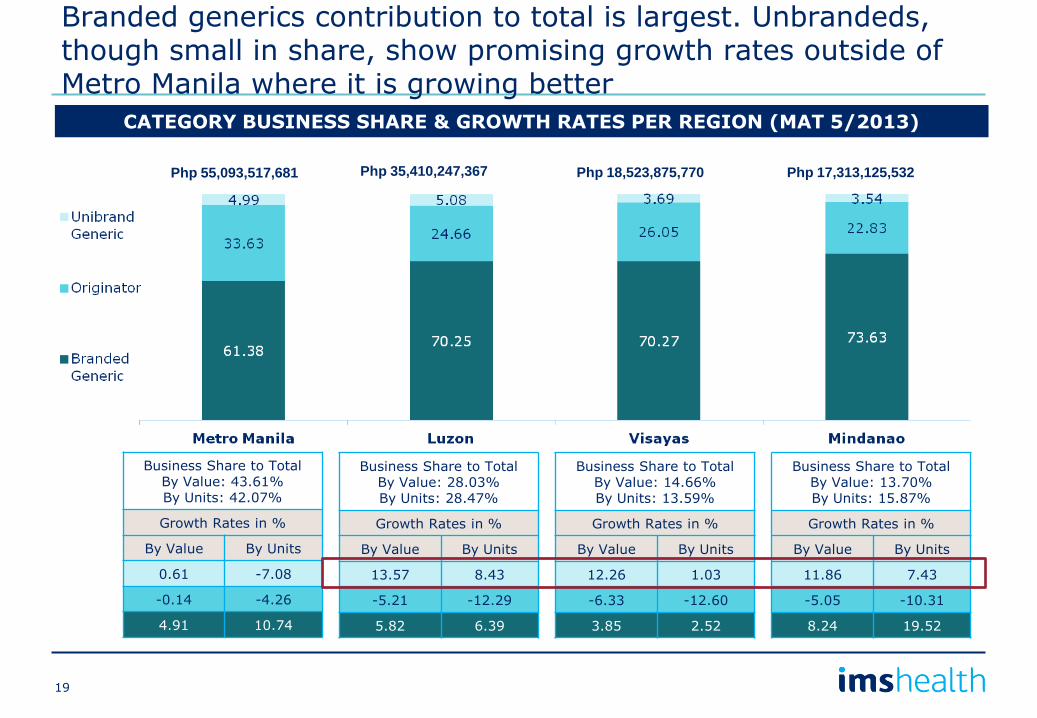

Branded generics contribution to total is largest. Unbrandeds, though small in share, show promising growth rates outside of Metro Manila where it is growing better

Business Share to Total By Value: 43.61% By Units: 42.07%

Growth Rates in %

By Value By Units

0.61 -7.08

-0.14 -4.26

4.91 10.74

Business Share to Total By Value: 28.03% By Units: 28.47%

Growth Rates in %

By Value By Units

13.57 8.43

-5.21 -12.29

5.82 6.39

Business Share to Total By Value: 14.66% By Units: 13.59%

Growth Rates in %

By Value By Units

12.26 1.03

-6.33 -12.60

3.85 2.52

Business Share to Total By Value: 13.70% By Units: 15.87%

Growth Rates in %

By Value By Units

11.86 7.43

-5.05 -10.31

8.24 19.52

Php 55,093,517,681 Php 35,410,247,367 Php 18,523,875,770 Php 17,313,125,532

CATEGORY BUSINESS SHARE & GROWTH RATES PER REGION (MAT 5/2013)

19

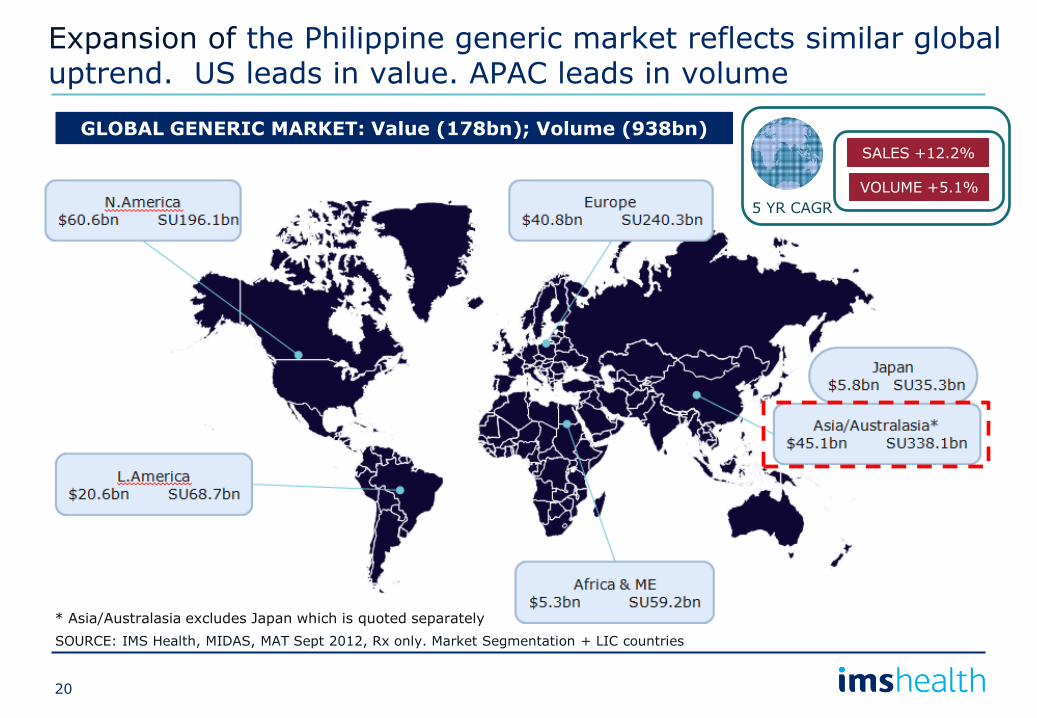

Expansion of the Philippine generic market reflects similar global uptrend. US leads in value. APAC leads in volume

SOURCE: IMS Health, MIDAS, MAT Sept 2012, Rx only. Market Segmentation + LIC countries

* Asia/Australasia excludes Japan which is quoted separately

5 YR CAGR

SALES +12.2%

VOLUME +5.1%

GLOBAL GENERIC MARKET: Value (178bn); Volume (938bn)

20

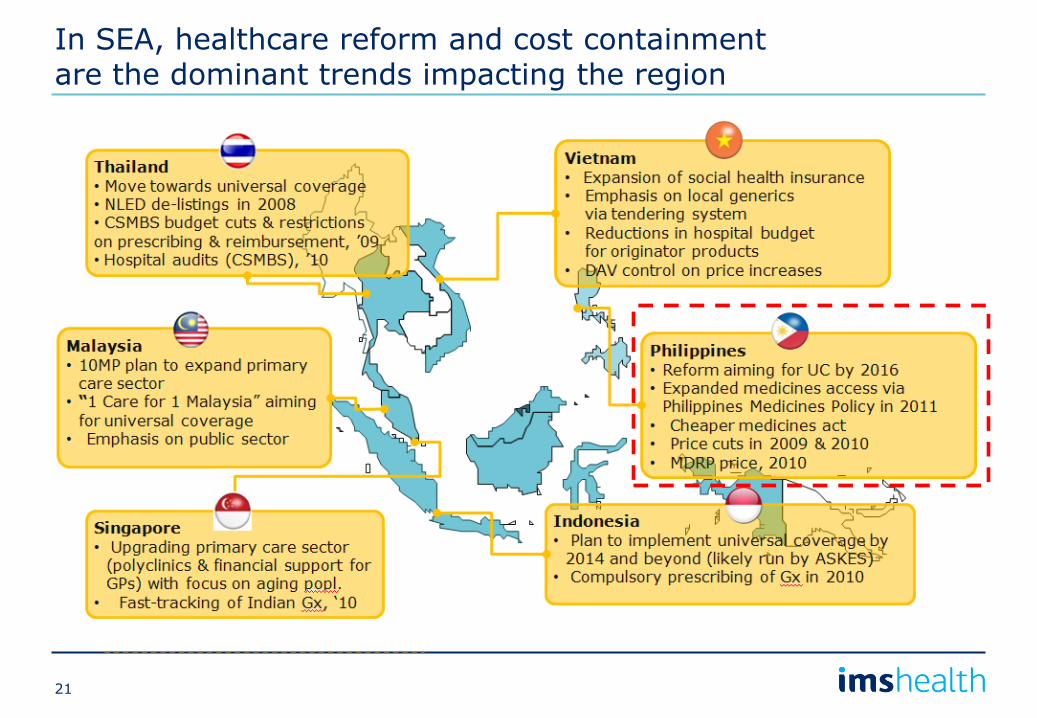

In SEA, healthcare reform and cost containment are the dominant trends impacting the region

21

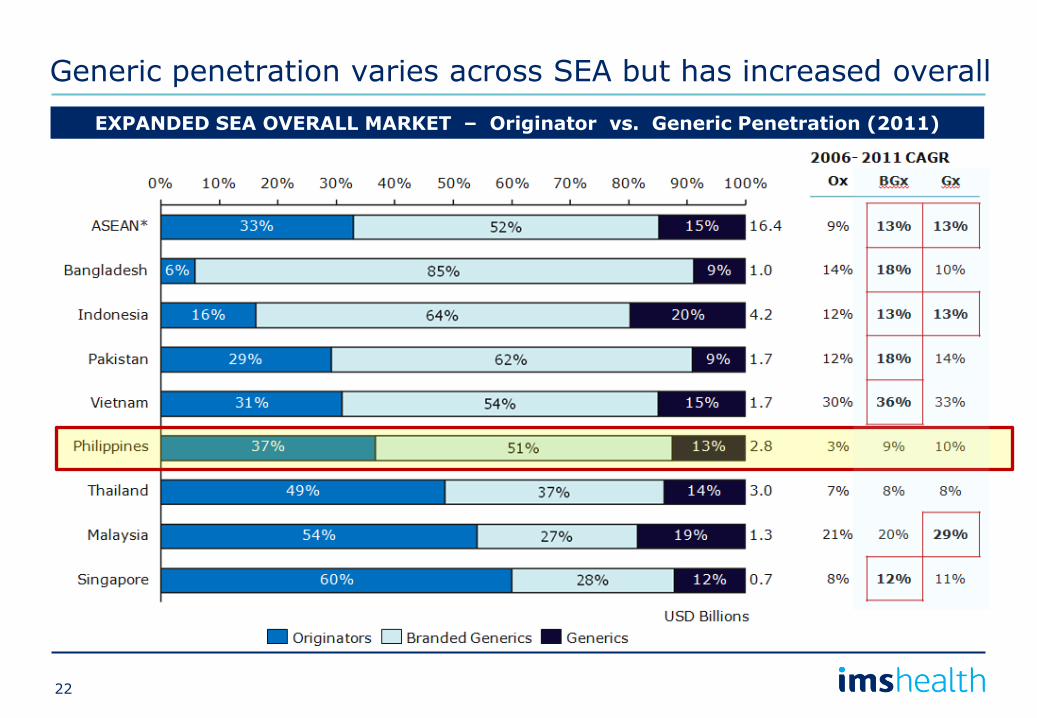

Generic penetration varies across SEA but has increased overall

EXPANDED SEA OVERALL MARKET – Originator vs. Generic Penetration (2011)

22

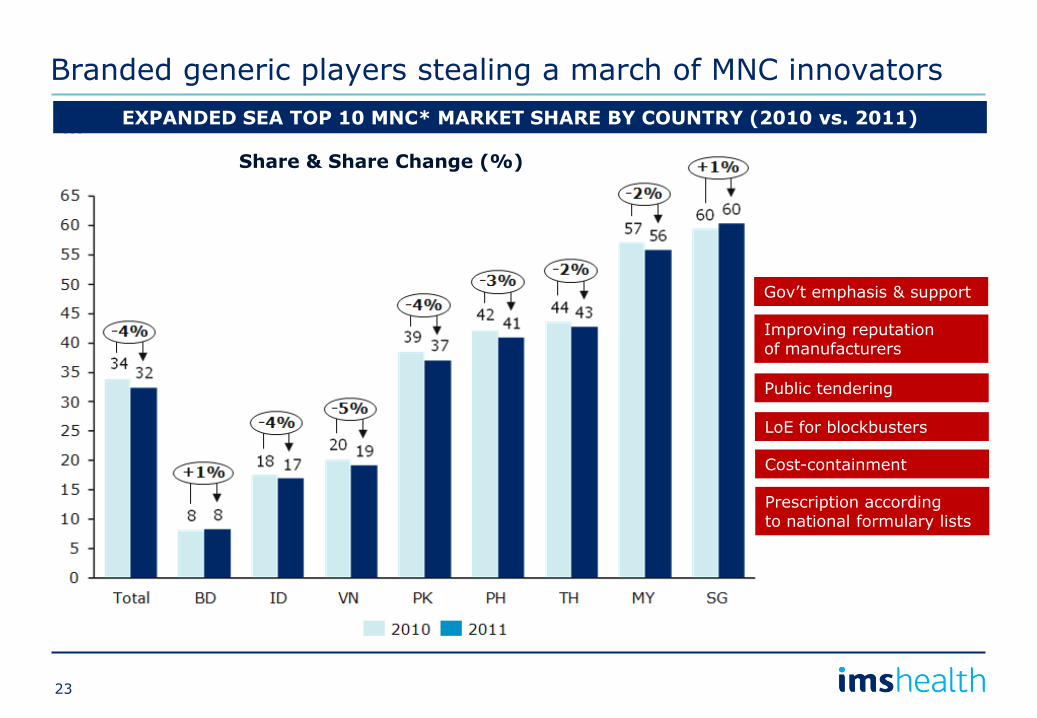

Branded generic players stealing a march of MNC innovators

…

SOURCE:

EXPANDED SEA TOP 10 MNC* MARKET SHARE BY COUNTRY (2010 vs. 2011)

Gov’t emphasis & support

Improving reputation of manufacturers

Public tendering

LoE for blockbusters

Cost-containment

Prescription according to national formulary lists

Share & Share Change (%)

23

Agenda

• The Philippine pharma market (size & growth)

• Market share trends

• Ethical vs. OTC

• Retail vs. hospital sectors

• Innovators vs. branded generics vs. unbranded generics

• Philippines

• Comparator Asian countries

• Post-MDRP/GMAP scenario (snapshots for select molecules)

• Summary: Prospects for the Philippine pharma market

0

500

1,000

1,500

2,000

2,500

3,000

3,500

MAT ~

12/2001

MAT ~

12/2002

MAT ~

12/2003

MAT ~

12/2004

MAT ~

12/2005

MAT ~

12/2006

MAT ~

12/2007

MAT ~

12/2008

MAT ~

12/2009

MAT ~

12/2010

MAT ~

12/2011

MAT ~

12/2012

Thousands

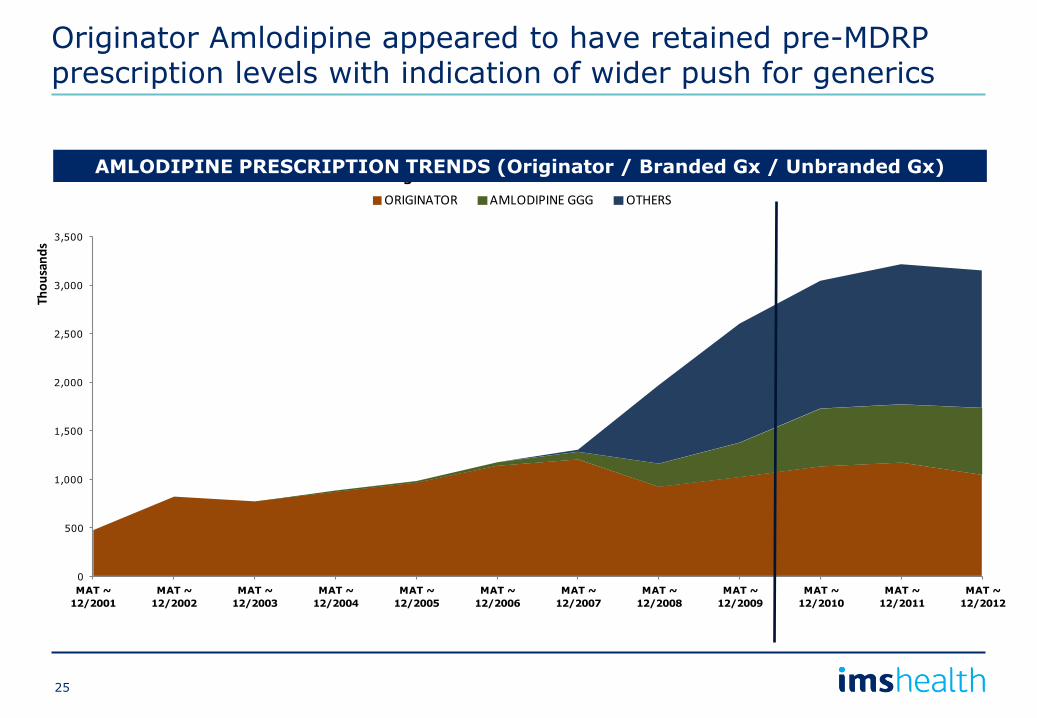

Amlodipine PrescriptionOriginator vs Generic Rx vs Others

ORIGINATOR AMLODIPINE GGG OTHERS

Originator Amlodipine appeared to have retained pre-MDRP prescription levels with indication of wider push for generics

AMLODIPINE PRESCRIPTION TRENDS (Originator / Branded Gx / Unbranded Gx)

25

40 43 44 43 40

34

57

7383 89

4

10

15

20

35

1,982

1,648

1,101 1,075

996

503716

833

9371,011

58137

187

230

376

0

500

1000

1500

2000

2500

3000

0

20

40

60

80

100

120

140

160

180

MAT~12/2008(19 Products)

MAT~12/2009(26 Products)

MAT~12/2010(33 Products)

MAT~12/2011(43 Products)

MAT~12/2012(44 Products)

Millions

Millions

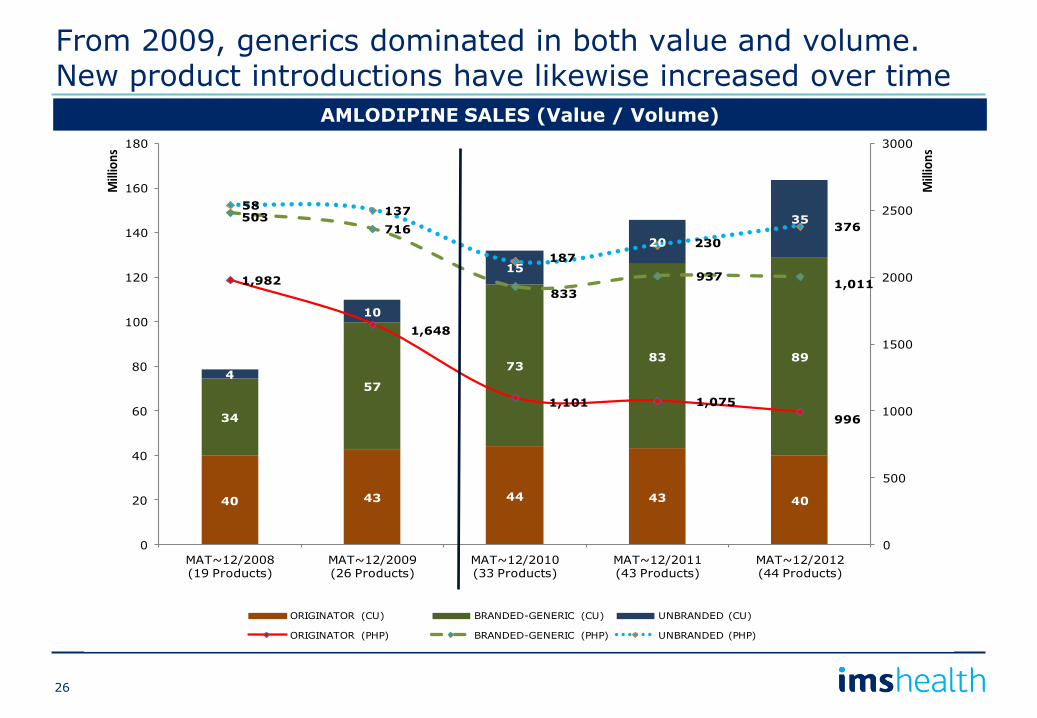

Amlodipine

ORIGINATOR (CU) BRANDED-GENERIC (CU) UNBRANDED (CU)

ORIGINATOR (PHP) BRANDED-GENERIC (PHP) UNBRANDED (PHP)

From 2009, generics dominated in both value and volume. New product introductions have likewise increased over time

AMLODIPINE SALES (Value / Volume)

26

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

MAT ~

12/2001

MAT ~

12/2002

MAT ~

12/2003

MAT ~

12/2004

MAT ~

12/2005

MAT ~

12/2006

MAT ~

12/2007

MAT ~

12/2008

MAT ~

12/2009

MAT ~

12/2010

MAT ~

12/2011

MAT ~

12/2012

Thousands

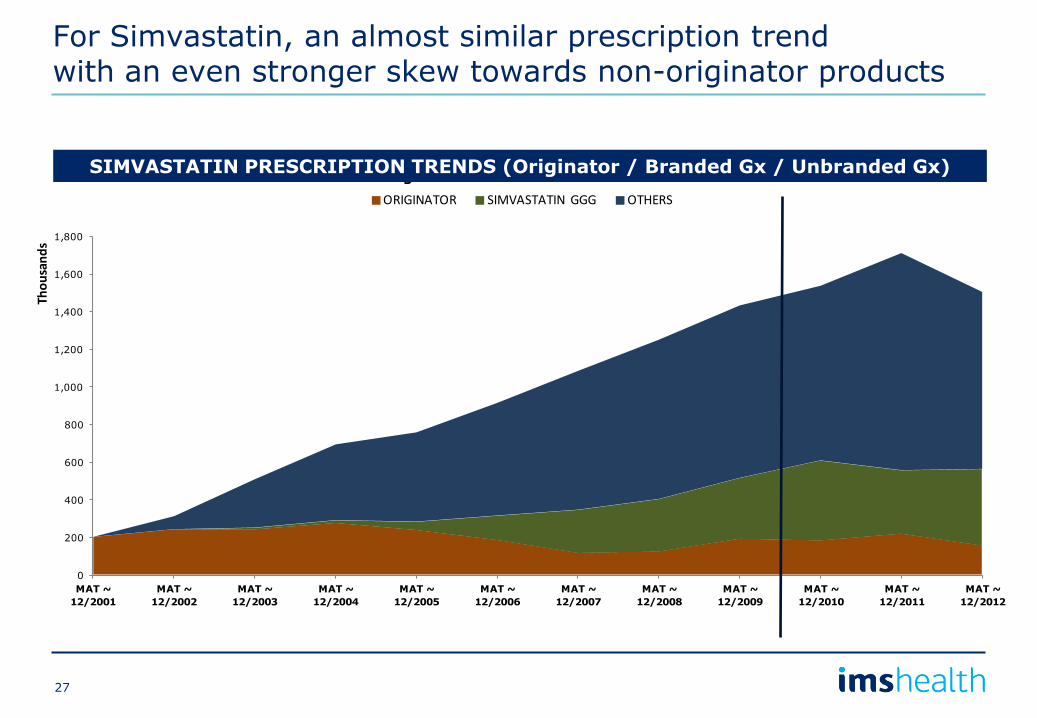

Simvastatin PrescriptionOriginator vs Generic Rx vs Others

ORIGINATOR SIMVASTATIN GGG OTHERS

For Simvastatin, an almost similar prescription trend with an even stronger skew towards non-originator products

SIMVASTATIN PRESCRIPTION TRENDS (Originator / Branded Gx / Unbranded Gx)

27

3 4 4 4 3

29

3236

32

28

9

10

13

14 22

83 115 113 111 96

682

695 662

587

539

160

175200

209

321

0

200

400

600

800

1000

1200

0

10

20

30

40

50

60

MAT~12/2008(36 Products)

MAT~12/2009(43 Products)

MAT~12/2010(45 Products)

MAT~12/2011(44 Products)

MAT~12/2012(41 Products)

Millions

Millions

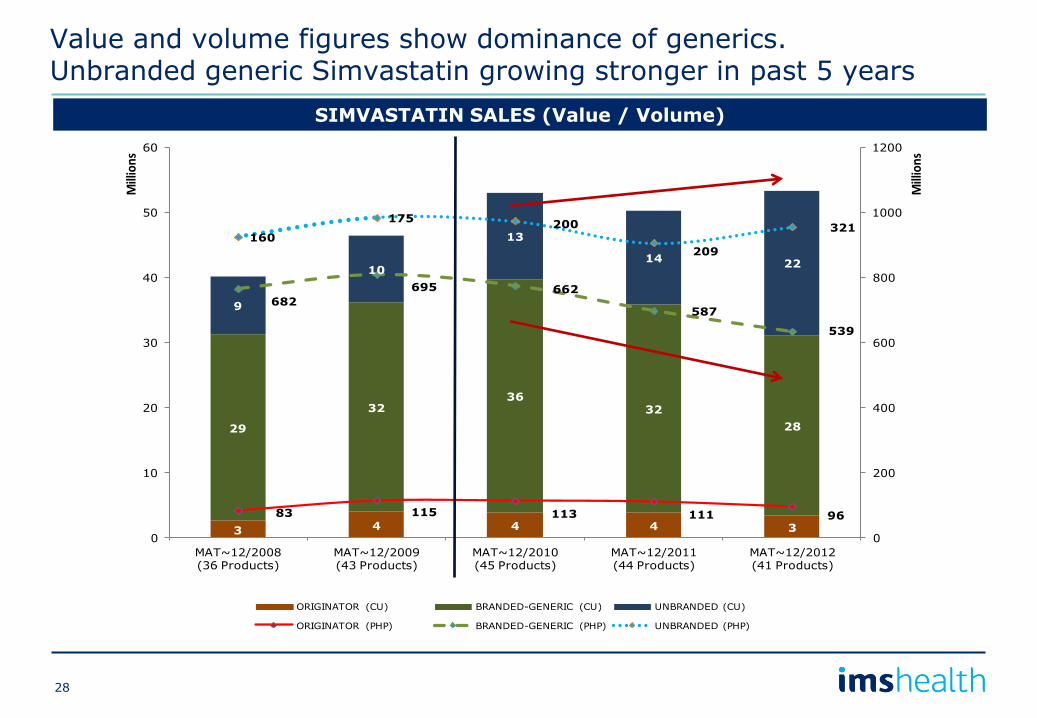

Simvastatin

ORIGINATOR (CU) BRANDED-GENERIC (CU) UNBRANDED (CU)

ORIGINATOR (PHP) BRANDED-GENERIC (PHP) UNBRANDED (PHP)

Value and volume figures show dominance of generics. Unbranded generic Simvastatin growing stronger in past 5 years

SIMVASTATIN SALES (Value / Volume)

28

0

10

20

30

40

50

60

70

80

90

MAT ~

12/2001

MAT ~

12/2002

MAT ~

12/2003

MAT ~

12/2004

MAT ~

12/2005

MAT ~

12/2006

MAT ~

12/2007

MAT ~

12/2008

MAT ~

12/2009

MAT ~

12/2010

MAT ~

12/2011

MAT ~

12/2012

Thousands

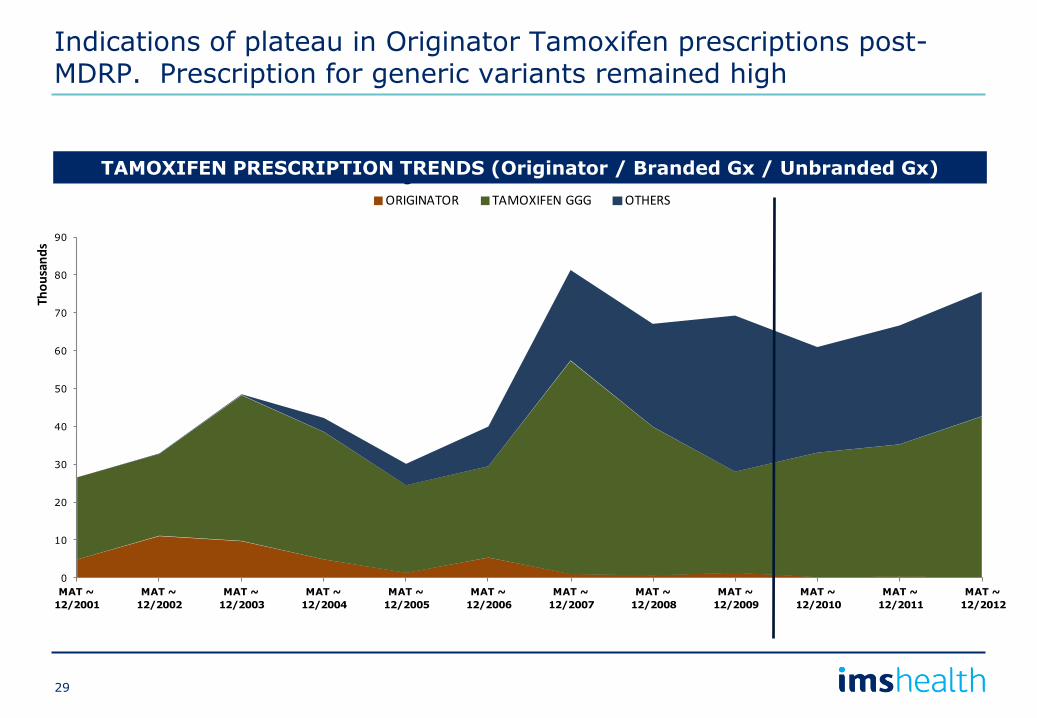

Tamoxifen PrescriptionOriginator vs Generic Rx vs Others

ORIGINATOR TAMOXIFEN GGG OTHERS

Indications of plateau in Originator Tamoxifen prescriptions post-MDRP. Prescription for generic variants remained high

TAMOXIFEN PRESCRIPTION TRENDS (Originator / Branded Gx / Unbranded Gx)

29

163 148 188 209438

2,5672,714 2,686

2,535

1,832

117

98

8 75 5

11

114

106

9284

43

3

3

0

20

40

60

80

100

120

140

0

500

1,000

1,500

2,000

2,500

3,000

3,500

MAT~12/2008(7 Products)

MAT~12/2009(7 Products)

MAT~12/2010(6 Products)

MAT~12/2011(6 Products)

MAT~12/2012(7 Products)

Millions

Thou

sand

sTamoxifen

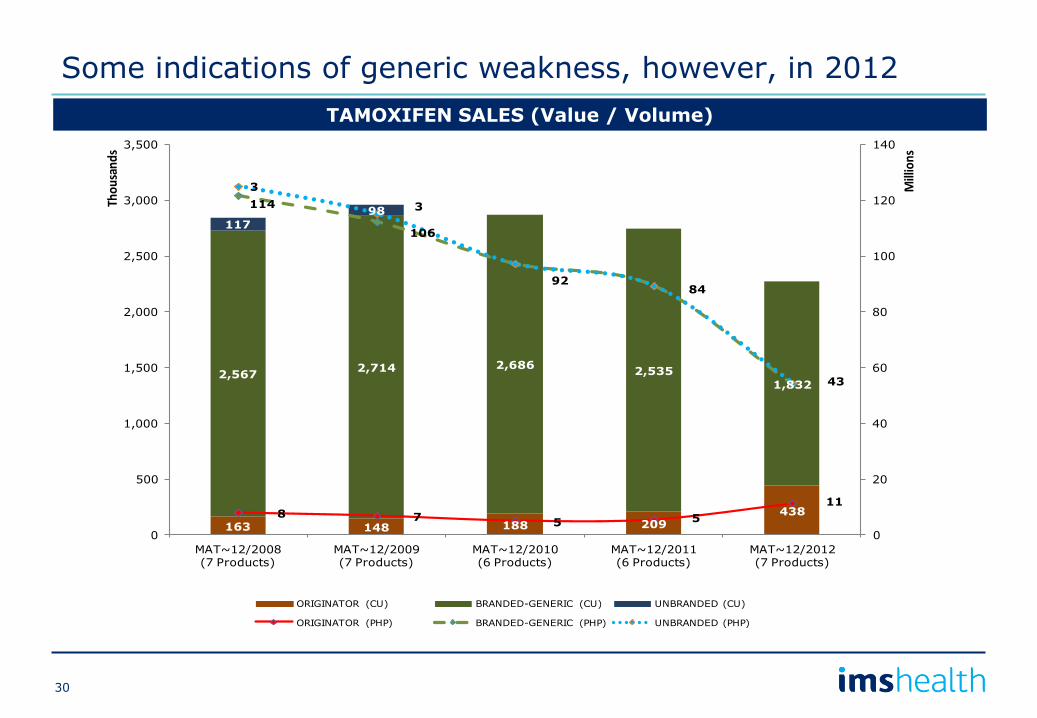

ORIGINATOR (CU) BRANDED-GENERIC (CU) UNBRANDED (CU)

ORIGINATOR (PHP) BRANDED-GENERIC (PHP) UNBRANDED (PHP)

Some indications of generic weakness, however, in 2012

TAMOXIFEN SALES (Value / Volume)

30

Agenda

• The Philippine pharma market (size & growth)

• Market share trends

• Ethical vs. OTC

• Retail vs. hospital sectors

• Innovators vs. branded generics vs. unbranded generics

• Philippines

• Comparator Asian countries

• Post-MDRP/GMAP scenario (snapshots for select molecules)

• Summary: Prospects for the Philippine pharma market

PHILIPPINE

PHARMA/

HEALTHCARE

INDUSTRY

Players

Product

Channel

Therapy

class

Market

Promotion

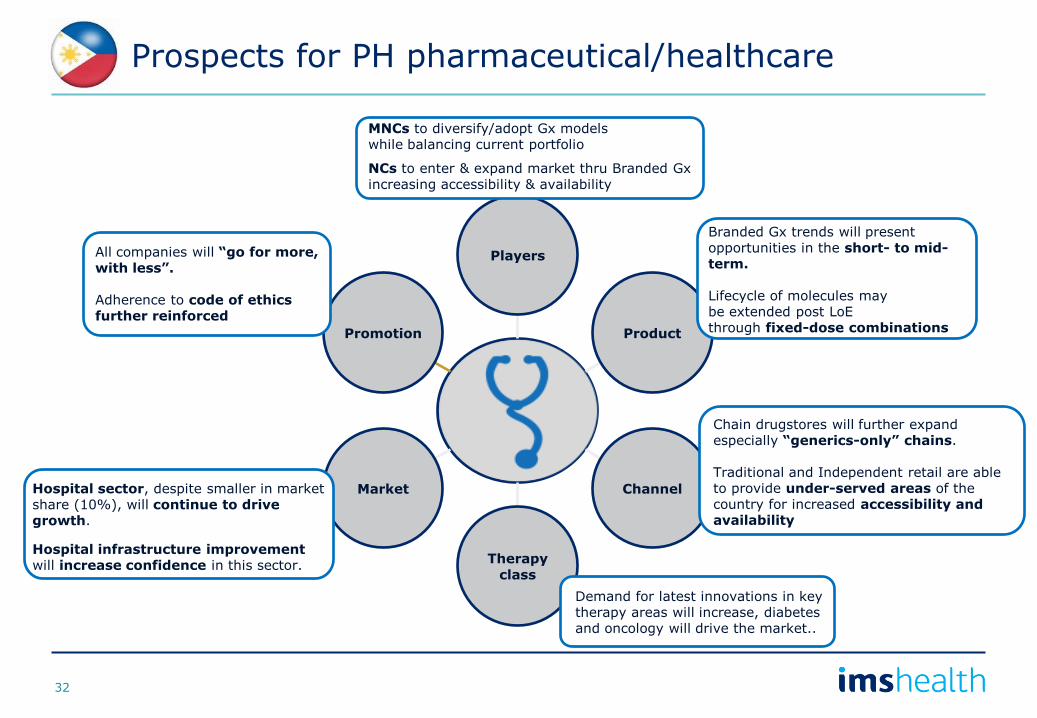

Prospects for PH pharmaceutical/healthcare

MNCs to diversify/adopt Gx models while balancing current portfolio

NCs to enter & expand market thru Branded Gx increasing accessibility & availability

Chain drugstores will further expand especially “generics-only” chains. Traditional and Independent retail are able to provide under-served areas of the country for increased accessibility and availability

All companies will “go for more, with less”. Adherence to code of ethics further reinforced

Hospital sector, despite smaller in market share (10%), will continue to drive growth.

Hospital infrastructure improvement will increase confidence in this sector.

Branded Gx trends will present opportunities in the short- to mid-term. Lifecycle of molecules may be extended post LoE through fixed-dose combinations

Demand for latest innovations in key therapy areas will increase, diabetes and oncology will drive the market..

32

Deejay Cromwell V. Sanqui Product Manager – Philippines & Indonesia

+632 5885407 / +917 5535970

IMS Health

Thank you very much.

![Secondary Pharmaceutical Patents: A Global Perspective · Secondary Pharmaceutical Patents: A Global Perspective Kenneth C. Shadlen (LSE) [Bhaven N. Sampat (Columbia)] WHO-WIPO-WTO](https://static.fdocuments.net/doc/165x107/5ea3393d0f1a3a0d1948b29f/secondary-pharmaceutical-patents-a-global-perspective-secondary-pharmaceutical.jpg)