Estate Magazine 1-2016 (english)

53

N°1 2016 BIG MONEY SEEKS SAFE HAVENS NORWEGIAN REAL ESTATE: - OSLO IS UNDERPRICED LOOK TO NORWAY - THE INTEREST IN NORWAY WILL CONTINUE FOREVER - A LOT OF DRY GUNPOWDER - 2016 will be an exciting year ARCHITECTURE: -It left me breathless Investing in Norwegian Real Estate Tax and corporate law considerations The magazine for real estate professionals The edge of the risk scale The low interest rate level forces Olav Chen, one of Norway´s major pensions managers, onto the risk scale. This makes Norwegian commercial property an interesting investment opportunity.

-

Upload

estate-media -

Category

Documents

-

view

229 -

download

9

description

Â

Transcript of Estate Magazine 1-2016 (english)

1ESTATE MAGASIN | N°1 2016

N°1 2016

BIG MONEYSEEKS SAFE HAVENS

NORWEGIAN REAL ESTATE:- OSLO IS UNDERPRICED

LOOK TO NORWAY- THE INTEREST IN NORWAY WILL CONTINUE FOREVER

- A LOT OF DRY GUNPOWDER- 2016 will be an exciting year

ARCHITECTURE:-It left me breathless

Investing in Norwegian Real EstateTax and corporate law considerations

The magazine for real estate professionals

The edge of the risk scaleThe low interest rate level forces Olav Chen, one of Norway´s

major pensions managers, onto the risk scale. This makes Norwegian commercial property an interesting investment opportunity.

MANAGEMENT SERVICES FOR COMMERCIAL REAL ESTATE

History has taught us that it is difficult to navigate in unknown waters. Risks can belarger then they first appear. Yet the Nordic market is a solid safe haven in otherwiserough sea.

If you are looking to enter the Nordics, Basale is a solid partner with a proven trackrecord within asset, property and company management. We know the local waters, can guide you through the obstacles and avoid unnecessary risk. We have helped many foreign investors enter what can appear to be a closed market.

OBOS Basale AS is the largest independent manager of commercial propertyin Norway. With over 25 years of experience, we provide a complete range of real estate management and advisory services for financial investors and real estate funds.

We are a team of more than 235 specialists with a passion for real estate. Our team comprises of Property Managers, Brokers, Analysts, Auditors, Accountants, Engineersand Attorneys working together for the interest of our clients and their tenants.

If you are looking to enter the Nordic market, then get a serious partner.

Hilmar Auran +47 924 53 053 [email protected] CEO

Inger Eriksen +47 934 49 912 [email protected] CLO

Gjermund Fossnes +47 930 94 891 [email protected] Regional Director

NORWAY | SWEDEN | DENMARK www.basale.com

How to navigate the Nordics

MANAGEMENT SERVICES FOR COMMERCIAL REAL ESTATE

History has taught us that it is difficult to navigate in unknown waters. Risks can belarger then they first appear. Yet the Nordic market is a solid safe haven in otherwiserough sea.

If you are looking to enter the Nordics, Basale is a solid partner with a proven trackrecord within asset, property and company management. We know the local waters, can guide you through the obstacles and avoid unnecessary risk. We have helped many foreign investors enter what can appear to be a closed market.

OBOS Basale AS is the largest independent manager of commercial propertyin Norway. With over 25 years of experience, we provide a complete range of real estate management and advisory services for financial investors and real estate funds.

We are a team of more than 235 specialists with a passion for real estate. Our team comprises of Property Managers, Brokers, Analysts, Auditors, Accountants, Engineersand Attorneys working together for the interest of our clients and their tenants.

If you are looking to enter the Nordic market, then get a serious partner.

Hilmar Auran +47 924 53 053 [email protected] CEO

Inger Eriksen +47 934 49 912 [email protected] CLO

Gjermund Fossnes +47 930 94 891 [email protected] Regional Director

NORWAY | SWEDEN | DENMARK www.basale.com

How to navigate the Nordics

004 ESTATE MAGASIN | N°1 2016

URBANISM

HOME

MEETING PLACE

WELL-BEING

GREEN LUNGS

WORKPLACE

SUSTAINABILITY

SPACE

INFRASTRUCTURE

E N D L E S S P O S S I B I L I T I E S

N O R WAY: OSLO - B ER G EN - S TAVAN G ER - T R O N D H EIM - FR ED R IK S TAD - S TO R D S W E D E N : S TO CK H O L M - M AL M Ö - UM E Å - FAL KÖ PIN G - L ID KÖ PIN G - T R O L L HÄT TAN

D E N M A R K : CO PEN HAG EN L I N K A R K I T E K T U R .CO M

A city is not an accident but the result of coherent visions and aims. – Leon Krier

Pho

to: H

undv

en- C

lem

ents

Pho

togr

aphy

. Ill

ustr

atio

n: B

rick

Visu

al /

MIR

/ L

INK

arki

tekt

ur A

S

Creating a vibrant neighbourhood or local centre requires homes, buildings where people can work and study, cultural institutions, sports facilities and good health services. But what lies between the buildings is at least as important. If we as architects

are unable to think holistically, imaginatively and pragmatically about the development of an area, the venue in question will never be capable of at-tracting people. The task is this simple, and also this difficult!

LEF T: FORNEBU SENTRUM, SNARØYA. BELOW: BISPE VIK A SYD, FELT 9B, OSLO // B ILDØY - V ISJON K YSTBY, SOTRA // BANKPL ASSEN, OSLOAGORA, KRISTIANSAND // BRUPARKEN, DRAMMEN

005ESTATE MAGASIN | N°1 2016

URBANISM

HOME

MEETING PLACE

WELL-BEING

GREEN LUNGS

WORKPLACE

SUSTAINABILITY

SPACE

INFRASTRUCTURE

E N D L E S S P O S S I B I L I T I E S

N O R WAY: OSLO - B ER G EN - S TAVAN G ER - T R O N D H EIM - FR ED R IK S TAD - S TO R D S W E D E N : S TO CK H O L M - M AL M Ö - UM E Å - FAL KÖ PIN G - L ID KÖ PIN G - T R O L L HÄT TAN

D E N M A R K : CO PEN HAG EN L I N K A R K I T E K T U R .CO M

A city is not an accident but the result of coherent visions and aims. – Leon Krier

Pho

to: H

undv

en- C

lem

ents

Pho

togr

aphy

. Ill

ustr

atio

n: B

rick

Visu

al /

MIR

/ L

INK

arki

tekt

ur A

S

Creating a vibrant neighbourhood or local centre requires homes, buildings where people can work and study, cultural institutions, sports facilities and good health services. But what lies between the buildings is at least as important. If we as architects

are unable to think holistically, imaginatively and pragmatically about the development of an area, the venue in question will never be capable of at-tracting people. The task is this simple, and also this difficult!

LEF T: FORNEBU SENTRUM, SNARØYA. BELOW: BISPE VIK A SYD, FELT 9B, OSLO // B ILDØY - V ISJON K YSTBY, SOTRA // BANKPL ASSEN, OSLOAGORA, KRISTIANSAND // BRUPARKEN, DRAMMEN

006 ESTATE MAGASIN | N°1 2016

In our editorial column one year ago, we wrote that it looked as if there would be a high level of activity in the Norwegian market for commercial property in the period ahead, as financing terms were reasonable and investment options few.

That turned out to be the understatement of all times. The 2015 transaction volume ended at around 125 billion kroner, ie. more than double the 2014 transaction volume which represented an average of the annual volumes in the peak years 2006-2007.

The prices have also gone up in the residential market in 2015 – as they have done in the last few years. So far this year, there is little to indicate that this development will come to a halt as the big cities experience a strong migration influx and the construction industry is unable to meet the demand for new housing.

This trend is particularly noticeable in Oslo. We constantly hear that living in a city is not a basic human right. We have never claimed that it is. It is all about somet-hing quite different, namely to pave the way for the brainiest and this is where the authorities must be more actively involved. If housing becomes so expensive that only the highly paid can afford to live in the big cities, workplaces will lose access to employees other than those at the top of the pay scale. The fact is that a workplace needs people from all categories and at all pay levels.

However, back to the commercial property market where 2015 was a very good year. Several Norwegian banks have implemented restrictions with regard to the financing of commercial property but many of the foreign players will not be affe-cted by this measure as they have backing from their own banks and shareholders. Foreign investors accounted for approximately 40 per cent of last year’s total transa-ction volume, and according to those close to the market, still more foreign property investors wish to get in on the Norwegian market.

Lately, we have seen significant unrest in the Norwegian as well as the internati-onal stock exchanges. This will probably lead to even more interest in property as an investment, and we therefore venture to claim that the Norwegian property market will be attractive in 2016 as well. Still, we do not foresee a transaction volume like last year’s because a great number of large property portfolios changed ownership in 2015, and there is a limit as to how many of these are available in the market.

The reason why we believe that the transaction volume will go down is the pro-blems experienced by the oil industry. The oil price has gone down considerably over the last year and at this point in time, there is little indication of an imminent upswing of any significance. The falling oil price has led to reduced activity in the oil service businesses, and several thousand people have been laid off temporarily or made redundant. This is particularly noticeable in oil intensive regions like the county of Rogaland, not to mention the oil city Stavanger.

The consequences will, however, be noticeable all over Norway. The oil is a corner stone in the Norwegian economy and it is therefore obvious that continued unrest in the oil industry will be reflected in the economy of the country as a whole.

We predict that we will see a total volume of around 75 billion kroner in 2016, ie. a turnover well below that of 2015 but still higher than the previous years. The foreign investors will still be highly visible, perhaps even more so than before.

Still attractive

THOR ARNE BRUN

Editor-in-Chief

EDITOR-IN-CHIEF: Thor Arne Brun, mobile: +47 95 86 56 56 e-mail: [email protected] JOURNALISTS:Thor Arne Brun, mobile: +47 958 65 656 e-mail: [email protected] Hagøy, mobile: +47 997 47 171 e-mail: [email protected] Rønne, mobile: +47 9082 9393e-mail: [email protected] Årdal, mobile: +47 915 38 544 e-mail: [email protected]

ADVERTISING , CONTACT: Jan Erik Pedersen, mobile: +47 901 58 211e-mail: [email protected] Nessem mobile: +47 958 35 865 e-mail: [email protected] Hugo Øren, mobile: +47 928 16 111e-mail: [email protected] Boisen, mobile: + 47 9513 7283e-mail: [email protected] S. Matheson, mobile: + 47 995 53 059e-mail: [email protected] CEO: Trond Valle, mobile: +47 911 23 334e-mail: [email protected]

LAYOUT AND PRODUCTION: Estate ReklameMarion Nævestad, [email protected]

PRESS:UnitedPress Poligrafija corporation, Latvia

Cover photo: André Clemetsen

Copyright: Estate Media AS

RESPONSIBLE PUBLISHER:Estate Media AS, Rådhusgata 26, N-0151 Oslo, Phone: +47 22 42 43 42e-mail: [email protected] 1503-559X. All rights Estate Media AS.

N°1 2016

ESTATE MEDIA

C.J. Hambros plass 2D, 0164 Oslo, Norway | +47 21 93 10 [email protected] | www.foyentorkildsen.no

C.J. Hambros plass 2D, 0164 Oslo, Norway | +47 21 93 10 [email protected] | www.foyentorkildsen.no

008 ESTATE MAGASIN | N°1 2016008

CONTENT

content6 Editorial Still attractive

10 Look to Norway - Norway is of course in a difficult position with today s low oil price but the oil price will not necessarily remain low

14 Believes foreign investors will turn their backs on Norway - Norway is no longer a safe haven

16 - A lot of gunpowder - We truly believe that 2016 will be an exciting year

18 - 2015 was a fantastic year - In terms of revenue it was our best year ever

20 Multiplied by five in 2015 - We owe the high activity to low interest rates, a weak krone and a

strong will among foreign investors to invest

22 Norway s biggest property law firm - It was a busy year with great activity for the property group in general

24 - Big money seeks safe havens - Our expectations for the transaction market are positive

24 - Property is of course not a super-liquid asset class - But at the same time pension assets are by definition long term, and that makes it natural to invest in property, Storebrand Asset Management s Olav Chen says

36 Modernistic principles - It was almost like déjà vu but it still left me breathless

44 Boosting Norwegian transaction market - I think our legal framework is very liberal and transparent, easy to access and easy to navigate in

48 Investing in Norwegian real estate Tax and corporate considerations

26

14

36

44

009ESTATE MAGASIN | N°1 2016

THOMMESSEN RIGHT ON TARGETReal estate investors around the world are looking to Norway. Our lawyers assist in creating value – from acquisition through exit.

ADVOKATFIRMAET THOMMESSEN AS

thommessen.no

OSLOChristian Müller +47 23 11 11 07 [email protected]

Even Bratsberg +47 23 11 12 46 [email protected]

BERGENVidar Havsgård + 47 55 30 61 32 [email protected]

LONDONLars Eirik Gåseide Røsås +44 (20) 7920 3008 [email protected]

“ I like working with the firm very much. It is right on target, has a lot of hands-on experience, not only in law, but in the industry too and is very good at understanding technical issues.

Profilannonse Estate Magasin helside 2-16.indd 1 11.02.2016 13:52:38

010 ESTATE MAGASIN | N°1 2016

NNEWSTore Å[email protected]

Norwegians are not only known for being fast on the ski track. In Norway, properties have been sold at such a speed that foreign

investors have hardly had time to start on their research. Nick Laird in Anvil believes that this will change.

Look to Norway

Nick Laird was one of the lecturers at Eiendoms-dagene organised by Estate Media at Norefjell in January. The roughly 300 people present were greatly amused when he presented his own outline of the time lapse in connection with the sale of Norwegian property:

The property owner, while skiing in “marka” at 7.00 a.m. decides to sell and at 8.15 a.m., he calls his broker. It is not necessary to spend much time on the rest of the process before a closing dinner at 7.00 p.m.

FASTER THAN THE SWEDES- This is of course extreme but property sales in Norway happen much faster than what foreign investors are used to. Even the Swedes say that, Nick Laird says to Estate Magasin.

He is partner in Anvil AS, operating partner of Starwood Capital in Norway. Laird, original-ly from Boston, worked in New York for many years and moved to Norway in 2007.

NO SECRETS- Property sales happen fast in Norway because it is a small country. There are fewer players, fewer brokers and everybody knows everybody else. Consequently, there are no big secrets in the market, he says.

- If the bid on a property is high enough, the owner will wish to close the sale as soon as pos-sible. This has scared off some foreign investors, especially Americans who are used to spending a long time on research and due diligence.

MUST HAVE TIME FOR RESEARCHAccording to Laird, an American investment firm might spend one year on research before doing business in a new country. This applies to research on all aspects of the country as well as the property market.

- Previously, many Norwegian property owners probably thought that since foreign in-vestors weren’t fast enough, they were probably

NEWS

011ESTATE MAGASIN | N°1 2016

ATTRACTIVE: - With the prospect of low long-term interest rates, enormous sums of international capital are waiting to be in-vested across borders. In this picture, Norway is a very attractive market, says Nick Laird, partner in Anvil AS who is operating partner of Starwood Capital in Norway.

012 ESTATE MAGASIN | N°1 2016

NEWS

not serious. This is about to change. Conside-ring the high amount of international players who were involved in large transactions last year, I believe that the owners will now make sure that as many as possible have the oppor-tunity to view the property before it is sold, he says.

LARGE PROPERTIESThe properties must however be of a certain size before foreign investors take an inte-rest. Laird thinks that investment firms that have not done business in Norway before are typically looking for properties valued at 500 million kroner or more. If they have already done business in Norway, they might be looking for properties from 300 million kroner and upwards.

Still, he does not doubt that the Norwegian property market is attractive.

A GROWING POPULATIONLaird points out that Norway is one of the richest countries in the world, it has political stability, a growing population, no national debt and the world’s biggest piggybank.

- Norway is of course in a difficult position with today’s low oil price but the oil price will

not necessarily remain low. Moreover, Norway has a busy agenda with its highly educated population and a great deal of competence to develop new industry, Laird says.

WILL BE BACK- How long will the good, Norwegian market last?

- I think the interest in Norway will con-tinue forever. Foreign players who invested in Norwegian property in 2015 will be looking for new opportunities. Many of those who lost in the bidding rounds last year will also be back since they have now done their research on Norway. This will contribute to maintaining the price level in Norway, he replies.

- Debt is the fuel of the property market. With the prospect of low long-term interest rates, enormous sums of international capital are waiting to be invested across borders. In this picture, Norway is a very attractive market.

OSLO IN UNIQUE POSITIONLaird has great faith in the property market in Oslo in particular.

- Oslo is very diversified and at the same time, it is easier to understand the capital than

other cities. Consequently, foreign investors will always start in Oslo, he thinks.

As for the different types of property, Laird thinks that foreign players will show an in-terest in high-end retail, logistics and office space with long leases.

- Investments are very often made in cooperation with a Norwegian player, thus en-suring that the investor gets local competence backing in connection with the investment.

MORE OPPORTUNISTSLaird also thinks that we will see more oppor-tunistic, international players in the Norwegi-an property market in the future.

- Up until now, foreign players have prima-rily been interested in fully developed proper-ties with long leases. It may however also be profitable to improve a property, by either by upgrading an office building or converting a building into housing, he says.

Laird points out that the practice of con-verting buildings into housing started in New York 20 years ago. This will therefore be an interesting option in Norway.

PROMT EXECUTION: This is Nick Laird’s summing up of how a property sale used to come about in Norway.

7.00 PM

7.00 AM 9.00 AM

12.00 PM

1.00 PM

Property owner, while skiing in “ marka”,

decides to sell

Due Diligence Completed Closing dinnerWinning bid selected

Property tour arranged

Calls Broker8:15 AM

How international investors perceive the Norwegian sale process

5.00 PM

3.00 PM

Documents signedBroker calls Stordalen, Ringnes, Thon, KLP, Storebrand and the

Syndicates

013ESTATE MAGASIN | N°1 2016

PANGEA PROPERTY PARTNERS– NORDIC EXPERTISE

STOCKHOLM Norrlandsgatan 15, 7th floor

Stockholm, SWEDEN

+46 8 545 25 780

pangeapartners.se

OSLOTjuvholmen Allé 3, 8th floor

Oslo, NORWAY

+47 21 95 80 70

pangeapartners.no

LONDONBerkeley Square House, Berkeley Square London

W1J 6BD, GREAT BRITAIN

+44 20 788 713 74

en.pangeapartners.se

OSLO – STOCKHOLM – LONDON – HELSINKINEW

Acquisition of shopping centre company (34 assets) in Norway

Seller: Sektor Gruppen

EUR 1.5bn

Financial adviser and placement agent to Slättö IV

Not disclosed

Sale of residential portfolio in Luleå, Sweden

Seller: Lulebo

SEK 1.6bn

Sale of Quality Hotel Friends in Stockholm, Sweden

Buyer: Home Properties

SEK 1.0bn

Acquisition of several residential projects (~1,200 apartments) across Sweden.

Seller: Several

SEK ~2bn

Sale of 6 residential properties in Tranås, Sweden

Buyer: Boningsfastigheter

Not disclosed

Sale of residential portfolio in Östersund, Sweden

Byuer: Rikshem

SEK 1.1bn

Sale of Oslo City shopping centre in Oslo, Norway

Buyer: Entra and Steen&Strøm

NOK 5.0bn

Sale of hotel properies in Sweden

Seller: Midstar

SEK 850m

Acquisition of property companies Fortin in Norway and Sveareal in Sweden

Seller: DNB Nor Eiendomsinvest I

NOK ~11bn

Sale of 20 mixed-use properties in northern Sweden

Buyer: NP3

SEK 432m

KlarInvest

Sale of office portfolio in Sollentuna, Stockholm.

Buyer: Profi Fastigheter

Not disclosed

Acquisition of residential portfolio in Luleå.

Seller: Lulebo

SEK ~1.6bn

Sale of 5 city properties in Skellefteå, Sweden.

Buyer: Diös

SEK ~650m

Sale of residential portfolio in Härnösand and garage property in Umeå, Sweden.

Buyer: Amasten, NP3

SEK ~225m

Sale of shopping centre company (19 assets) in Norway

Buyer: Schage Eiendom

NOK 5bn

Sale of retail property 21,000 sqm (part of Hansa City) in Kalmar, Sweden

Buyer: Niam

Not disclosed

Acquisition of offshore oil base Mongstad in Bergen, Norway

Seller: Wimoh Invest

Sale of public sector property Kunnskapsveien 55 in eastern Oslo

Buyer: Hemfosa

Not disclosed

Sale of bank properties in Umeå, Söderhamn and Söderköping, Sweden

Buyer: Several

Not disclosed

Not disclosed

Acquisition of storage property outside Stockholm with the National Library of Sweden as single tenant

Seller: Stendörren

Not disclosed

Sale of newly developed office, Fornebuporten in Oslo, Norway (Gross area ~80,000 sqm)

Buyer: Syndicate

NOK ~3.2bn

Sale of big box retail portfolio across Norway

Buyer: Tristan Capital Partners

NOK 1.2bn

Sale of Royal Christiania Hotel in Oslo, Norway

Buyer: Anker Properties, Varner Invest

NOK 1.9bn

SEK 1.8bn

Sale of Radisson Blu Waterfront in Stockholm, Sweden

Buyer: KLP Eiendom

pangea property partners is an independent Nordic corporate finance and transaction advisory firm focusing on the real estate

sector. The company has offices in Stockholm, Oslo and London with over 30 employees. In addition, we have a close cooperation

with Mrec in Finland. In 2015, we have advised on some 50 transactions with an underlying property value close to EUR 7bn.

The mandates include divestments and acquisitions of single assets and portfolios as well as large corporate transactions, develop-

ment projects, financing mandates and capital raisings. In particular, Pangea has a long tradition of bringing international capital and

Nordic real estate together and some 40% of our deals are cross-border.

NEW

014 ESTATE MAGASIN | N°1 2016

Photo: shutterstock

NEWS

015ESTATE MAGASIN | N°1 2016

Believes foreign investors will turn their backs on Norway

For years, Norway has appeared to be a safe haven for property investments. That is over now.

- We anticipate that the foreign portion of the Norwegian transaction market will be significantly lower in 2016 than what it was in 2015, says analyst in DNB Markets, Simen Mortensen.

FROM 40 TO 20 PER CENTIn 2015, foreign investors represented 40 per cent of the total transaction volume. In kroner, this amounts to as much as 48 billion kroner of a total volume of 120 – 130 billion kroner. Thus, DNB Markets anticipate a sig-nificant drop in the foreign portion of the Norwegian volume in 2016.

- We think it will drop to around 20 per cent. They will still be there but mostly because of the currency, which gives them a discount in Norway, says Mortensen.

DOWN BY 35 BILLIONDNB Markets do not operate with estimates of the transaction volume and therefore they

cannot give any indication of how much 20 per cent of the volume will mean in kroner. A number of brokerage firms have however estimated a significant drop in this year’s volume. Some have estimated between 60 and 70 billion kroner. Twenty per cent of that comes to between 12 and 14 billion kroner. In other words, the drop from 48 billion is sig-nificant.

- Norway is no longer a safe haven. There is increased uncertainty in the Norwegian private sector. The Norwegian government is of course a safe tenant, but they cannot rent all of it, says Mortensen.

FEAR WILL STRIKEDNB Markets believe that the market will be characterised by an even more restrictive banking market.

- Most of the banks have already signal-led that they will raise the price of corporate loans, and commercial property constitutes a large portion of this, says Mortensen.

He also points out that the uncertainty in Norwegian business and industry has incre-ased.

- So far, this has not had an effect on the transaction market but we believe that 2016 will be the year when fear will strike. The fear of increased vacancy in the property market will affect the transaction market, says Mor-tensen.

DEMANDING FOR A LONG TIME TO COMESome reports indicate economic growth in 2017, but DNB Markets hold this outlook to be too optimistic.

- We believe that we will see a downward revision of GNP in 2017 also, and we envi-sage a shift in the expected growth in the economy. This will affect the letting market which we believe will be demanding also in 2017, says Mortensen.

WILL AFFECT : - The fear of increased vacancy in the property market will affect the market, says Simen Mortensen, analyst in DNB Markets.

NNEWSTorgeir Hågø[email protected]

016 ESTATE MAGASIN | N°1 2016

- A lot of dry gunpowderHead of transactions in Newsec, Håkon Styrvold,

says that there are many who have a lot of dry gunpowder that they will burn in 2016.

- We truly believe that 2016 will be an exci-ting year, says Håkon Styrvold.

He will not try to predict the total volume, but points out that a lot of people made a lot of money in both 2014 and 2015.

- A number of investors have been sitting on the fence watching the market go up and values increase, they have kept their gun-powder dry for investing now that they see opportunities in the market. That goes for both Norwegian and foreign players. It is not unthinkable that they want to go in in 2016, Styrvold says.

CHALLENGING FINANCINGThe transaction year 2015 broke all records. The volume estimates vary between 120 and 130 billion kroner. Most players think that even 2016 will be a good year but eve-ryone believes that in comparison to 2015 the volume will drop.

For many investors, the greatest problem will perhaps be financing. The banks have tightened the belt considerably, and both DNB and Nordea have signalled that they are not very eager to participate in new projects.

- If you are big enough, you will get funding. The banks, however, have a re-strictive attitude, which means that they

will be focusing strongly on the possibility of financing by loan capital. More than before will turn to the bond market, also in connection with lower volumes than before. Players who don’t have to make fi-nancing reservations in 2016 are in a very strong position, says Styrvold.

BELIEVES IN REPRICINGStyrvold thinks that in the course of 2016 we will also see a reprising of more inferior objects.

- Objects with short cash f low, located outside the big cities and with insecure tenants are the objects where we will see a higher yield in the time to come. If, for example, you have an older building on the outskirts of Bergen with one tenant in the oil service industry, I don’t think the bank will pat you on the back and give you a bag of money on your way out. The question is whether you will get any funding at all. We saw examples of this in processes at the turn of the year, says Styrvold.

NNEWSTorgeir Hågø[email protected]

STRONG COMPETITORS: - Players who don’t have to make financing reservations in 2016 are in a very strong position in a tender process, says Håkon Styrvold, head of transactions in Newsec.

NEWS

017ESTATE MAGASIN | N°1 2016

Wikborg Rein has an impressive track record in assisting leading Norwegian and foreign investors in a variety of transaction forms, including the most complex and largest corporate real estate transactions. 2015 was no exception. We have the expertise, the experience, the capacity and a proven methodology for assisting in successful transactions.

Our real estate team consists of 20 highly dedicated and experienced lawyers, and you can meet the team’s representatives at MIPIM.

Line [email protected] +47 952 23 394

Gøran Mjelde [email protected] +47 908 45 263

Wikborg Rein is one of Norway’s leading law firms with over 200 lawyers in Oslo, Bergen, London, Singapore, Kobe, and Shanghai. The firm’s long-standing presence overseas distinguishes Wikborg Rein as the Norwegian law firm with most international experience and expertise.

Meet us at MIPIM

Trusted advisor

PH

OTO

: IL

JA H

EN

DE

L

MIPIM Estate Februar 2016.indd 1 15.02.2016 15:59:30

018 ESTATE MAGASIN | N°1 2016

Acted as consultant in sales of infrastructure properties

Development projects and consultancy work connected with the buying and selling of a number of large infrastructure

properties marked the year for Selmer.

NNEWSTorgeir Hågø[email protected]

ASSISTED IN THE COOP SALE TO TRISTAN: Sverre Nordlie in the law firm Selmer.

- 2015 was a fantastic year. In terms of revenue it was our best year ever, and sales in the property department in 2015 came to around 95 million kroner, says Sverre Nordlie in Selmer.

- That is up from approximately 85 million in 2014, ie. a growth of around 10 million kroner.

DEVELOPMENT AND SALE OF INFRASTRUCTUREIn 2015, Selmer was involved in more than 50 transactions valued at more than 50 million kroner. Acccording to Nordlie, they have participated in transactions totalling around 25 billion kroner.

- We have probably not been involved in the largest portfolios in 2015, and the total transaction volume in kroner does not

really reflect the number of transactions or the complexity of the work we have done, says Nordlie.

The values only include the land value of acquired development projects, but the actual project value is of course far higher. He says that the year has been characte-rised by buying and selling development projects as well as larger infrastructure properties.

- We have been involved in a good number of acquisitions of land for develop-ment as well as in partnership projects. We also participated in the sale of Herøya in-dustrial estate and assisted EQT in the ac-quisition of the infrastructure at Mongstad outside Bergen, says Nordlie.

OTHER PROBLEMSAccording to Nordlie, acting as consultant in the selling of this kind of infrastructure properties is slightly different from regular commercial properties.

- It often involves a large number of employees, and buildings etc. are often of a different type and quality than more recent office properties, and this must be taken into consideration. Often, a number of properties, customers and agreements in addition to a series of “assets” other than the actual property provide the revenues. This creates a number of issues different

from those connected with general proper-ty transactions, says Nordlie.

He adds that they also assisted Coop in their sale of a property portfolio to Tristan Capital Partners.

- It was a big transaction. I cannot tell you how big but we are talking of billions. That much I can tell you, Nordlie says.

NEWS

019ESTATE MAGASIN | N°1 2016

Advokatfirmaet BA-HR DATjuvholmen allé 16, NO-0252 Oslo | PO Box 1524 Vika, NO-0117 OsloT: +47 21 00 00 50 | F: +47 21 00 00 51 | E: [email protected] | www.bahr.no

“The firm is very business-minded. A business partner more than a legal adviser. Simply the best”

Chambers Europe 2015

ERIKLANGSETHPARTNER

+47 412 16 634

ANNE SOFIE BJØRKHOLTPARTNER

+47 970 22 193

SAM E. HARRISPARTNER

+47 928 81 426

STIG L. BECHPARTNER

+47 913 72 668

LARS KRISTIANSANDEPARTNER

+47 908 58 464

CAMILLA H.SOLHEIMSENIORADVOKAT

+47 932 19 017

LARS DAVIDRÅMUNDDALSENIORADVOKAT

+47 917 04 760

ELIN MACKLØVDALSENIORADVOKAT

+47 911 43 487

OLE ANDREAS DIMMENSENIORADVOKAT

+47 414 38 821

ØYSTEIN MYREBREMSETSENIORADVOKAT

+47 415 62 122

020 ESTATE MAGASIN | N°1 2016

Multiplied by five in 2015The law firm Advokatfirmaet Thommessen can look

back on a very good year in 2015. The firm increased its transaction volume by 40 billion compared to 2014, ie.

an increase of 400 per cent.

- After having closed the books on 2015 and updated the figures with transactions handled by our Bergen office, we ended up at almost 50 billion kroner in 2015. Transa-ctions where we assisted with for instance financing come in addition, says Christian Müller in Advokatfirmaet Thommessen.

VERY GOOD UPSWINGMost law firms can look back on a very good year, and most of them report of very good transaction figures, often with a twofold increase or more. None can, however, show a growth as considerable as Thommessen. Whereas in 2014 the firm participated in transactions of around 10 billion kroner, the figures for 2015 are almost 50 billion kroner. That is an increase of 400 per cent and means in practice that they have multiplied last year’s volume by five.

- The number of transactions was 65 and a little more than in 2014, but clearly more large transactions took place in 2015 than in 2014, thus giving us a very good upswing in transa-ction volume, says Müller.

THIS IS WHAT THEY PARTICIPATED INMüller is supported by Chris Borch and Even Bratsberg who are also partners in the property department at Thommessen. According to them, figures like this have never been seen before – not even during the last boom in 2006 and 2007.

- We owe the high activity to low interest rates, a weak krone and a strong will among foreign investors to invest. There is a definite increase in international players, but our Nor-wegian clients are clearly just as important as before, says Bratsberg.

Among the transactions they have been in-volved in is the sale of Promenaden Property AS to the international property investment fund Meyer Bergman, in which Thommessen assisted Søylen. They also assisted Gjensidige Forsikring ASA in the sale of 50 per cent of the shares in the property investment company Oslo Areal AS to the Swedish pension insuran-ce company AMF Pensionsförsäkring AB. In addition, they aided Trond Mohn/Arctic in the acquisition of DNB’s headquarters in Bjørvika for around 4 billion and GC Rieber Eiendom in connection with the sale of the DNB building in Bergen for around 1.5 billion kroner.

IN THE PICTURE EVEN IN 2016They assisted Tristan Capital Market in buying a COOP portfolio with a property value of around 1.1 billion.

- Not surprisingly, we were involved in more transactions with foreign players in 2015 compared to 2014. We expect that the foreign investors will be in the picture in 2016 as well, even though the macro picture with falling oil prices, rising unemployment etc. is looking so-mewhat rough just now, says Müller.

BELIEVES IN CONTINUED FOREIGN INTEREST:- We owe the high activity to low interest rates, a weak krone and a strong will among foreign investors to invest, says Christian Müller in Advokatfirmaet Thommessen..

NNEWSTorgeir Hågø[email protected]

NEWS

021ESTATE MAGASIN | N°1 2016

OUR ECO LIGHTHOUSE CUTS COSTS AND MAKES YOU AN ECO WINNER!ISS Eiendom is one of Norway’s biggest property managers. Our portfolio includes over 3,500,000 m2 of floorspace across more than 6,500 buildings.

ISS has established its own Eco Lighthouse as part of ISS Green Management.

Our Eco Lighthouse is a hyper-modern control centre using the very latest in environmental technologies and monitoring systems. The control centre helps us measure and monitor overall energy consumption in a property. The result is big savings for the property owner.

There are also significant environmental benefits to be gained. This can boost the building’s environmental rating and increase the value of the property.

WE GUARANTEE THAT WE WILL BE ABLE TO FIND SAVINGS!

Kontakt ISS Green Management: 815 55 155

022 ESTATE MAGASIN | N°1 2016

Norway’s biggest property law firm

- Last year, we had a total transaction volume of 112 billion and that only included direct assistance to seller or buyer in transactions signed or closed in 2015. Norwegian pro-perties accounted for 80 billion, properties abroad owned by Norwegian structures accounted for the remaining 32 billion, says property lawyer and partner in BA-HR, Stig Bech.

UP BY 344 PER CENTThis is of course a formidable volume and it means that the law firm was involved in just about every large transaction that took place in 2015. Next on that list is Advokat-firmaet Schjødt. They also had a very good year. They report a total volume of 60 billion kroner, up from 13 – 14 billion kroner in 2014, ie. a growth of as much as 344 per cent, or between four and five times more than in 2014.

Advokatfirmaet BA-HR has a unique position when it comes to property transactions. Last year, their volume totalled as much as 112 billion, more

than doubled from 2014.

NNEWSTorgeir Hågø[email protected]

HAAVIND: Christian Bjørn Hansen.

NEWS

023ESTATE MAGASIN | N°1 2016

BA-HR: Stig Bech.

- It was a busy year with great activity for the property group in general and for those of us who work with property transacti-ons. We participated in a number of buying processes, worked with national and inter-national clients and continued to develop the positive trend from previous years, says head of the property group at Advokatfirma-et Schjødt, Ditlef A. Thaulow.

GOOD GROWTH FOR MANYThe third largest law firm in property transactions is Advokatfirmaet Thommes-sen. They participated in transactions to-talling 50 billion kroner, up from 10 billion in 2014. In other words, Thommessen increased their transaction volume five times.

Haavind is yet another firm that did very well. Last year was an all-time high in both sales and transaction volume.

- The highlight was carrying out more than 50 transactions valued at more than 50 million kroner. In some of the cases, we did extensive restructuring in advance, which meant a great deal of work, and at times you just had to hang on as best you could, says Christian Bjørn Hansen in Haavind.

Their transaction volume ended at around 25 billion. They were for instance involved in the sale of several properties for Statoil ASA, among others the sale of the headquarters in Stavanger and two office buildings in Trondheim for just over 4 billion kroner.

- The sale of Radisson Blue at Garder-moen was another highlight, says Bjørn

Hansen, adding that the outlook for 2016 is positive and that they are currently invol-ved in transactions amounting to around 4 billion.

STABLE FOR WIKBORG REIN2016 was a good year for Wikborg Rein but they cannot show the same growth as some of their competitors.

- Last year, we were involved in around 75 transactions totalling 22.3 billion. We had, in other words, a busy transaction year with more transactions than in the previous years, whereas the total transacti-on volume was roughly the same as before, says Gøran Mjelde Aarvik in Wikborg Rein.

They were participating in transactions of about 22 billion kroner in 2014, so the description «roughly the same as before» is in other words accurate.

- The activity early this year also shows that the market is still very active and th-erefore we have already started working on several new transactions in addition to a few “left-overs” from 2015, says Mjelde Aarvik.

Firm: 2015 2014 2013 2012BA-HR 112 44,5 23 26 Haavind: 25 7-8 4-4,5 -Kluge: ? ? 3,5 2,85Schjødt 60 13-14 14 20Selmer 25 36 13 20Steenstrup Stordrange ? 5,1 3 6Thommessen 50 10 13 20Wikborg Rein 22,3 22 16 21Hammervoll Pind 1 - - -

TRANSACTION VOLUME 2015

WIKBORG REIN: Gøran Mjelde Aarvik.

WIKBORG REIN: Gøran Mjelde Aarvik.

024 ESTATE MAGASIN | N°1 2016

- Big money seeks safe havens

The newcomer in the property market, Carnegie, believes in a good transaction year even in 2016.

Our expectations for the transaction market are positive. There is still a lot of money about, looking for safe havens, but we don’t expect to see the same volumes as we did in 2015, says head of project finance in Carnegie in Norway, Fredrik Bø.

WILL BE A DECENT COMPETITORCarnegie established themselves in the commercial property market in autumn 2015. The new team was however not in place until a couple of months into the new year. A total of five people will be working with syndica-tion and facilitation of the firm’s property projects.

- It is our ambition to be a decent compe-titor to the players already in the market, says Bø.

He himself came from DNB Markets where he also was head of corporate finance real estate.

- We want our fair share of this market, says Bø.

CAN TAKE A QUICK PROFITHe believes that some of the players who in-vested in property a few years back may have had such a decent appreciation in value that they might decide to sell in 2016.

- Some will probably think it is ok to take a profit, and we see that foreign investors experience a positive effect of the depreciati-on of the Norwegian currency. We therefore believe that 2016 is going to be a good transa-ction year, says Bø.

PAN-NORDIC EFFORTSCarnegie is a financial advisory firm with 600 employees in eight countries, among them Sweden, Denmark and Norway. It is not yet clear how big the Norwegian unit is going to be, but according to Begby, they expect to end up with a staff of just under ten people.

- Four to five people will be working with syndication of properties and we also plan to have a corporate finance department. On the website EstateNyheter.no, head of

Carnegie in Norway, Christian Begby, previo-usly stated, “We expect to end up with a staff of around eight to nine people”.

So far, Carnegie have been concentrating their activity on other asset classes but the commitment to property is part of a wider pan-Nordic strategy and priority.

- This is part of a long-term commitment in the Nordic countries. From the outside it may look as if we are going in at the peak of a market, which is always a worry, but this is part of a long-term strategy and commit-ment, says Begby.

NNEWSTorgeir Hågø[email protected]

NEWS

025ESTATE MAGASIN | N°1 2016

Colliers International AS is specializing in advising international investors acquiring commercial real estate in Norway. Our broad contacts and over 20 years of experience in the Norwegian commercial real estate market ensures you that we will find the best investment opportunity within most sectors in Norway.Our focus is both single assets and larger portfolios, including portfolios stretching all over Nordics.

Read more about us and our services on:www.colliers.com/no

PROPERTY INVESTMENTS NORWAY

Accelerating success.

026 ESTATE MAGASIN | N°1 2016

PORTRAIT

HECTIC PERIOD: It is not only the press calling Olav Chen whenever there is a downturn in the market. In his capacity of senior portfolio manager in Storebrand Asset Management, he must also bear the brunt when customers call.

027ESTATE MAGASIN | N°1 2016

The low interest rate level forces Olav Chen, one of Norway’s major pensions managers, and several other investors onto the risk scale. This makes Norwegian commercial property an

interesting investment opportunity.

By: Tore Årdal, [email protected]: André Clemetsen

The oil price just plummeted below 40 dollars a barrel, the NOK exchange rate is historically low, the interest rate is approaching zero. Olav Chen can barely squeeze football practice with Storebrand’s office team into his schedule.

It is not only the press calling Olav Chen for comments whenever there is a downturn in the market. In his capacity of senior portfo-lio manager in Storebrand Asset Management, he must also bear the brunt when clients call for an explanation of events.

MUST STAY UPDATED. In order to be able to respond properly to clients and the press, Chen must keep himself updated 24/7. Since the US fi-nancial parameters are extremely important to Norwegian economy, he must at least check Bloomberg and other channels at 10 p.m. Nor-wegian time, when the New York Stock Exchange closes. And pretty soon thereafter the Asian stock exchanges open.

- This is not a 9 to 4 job but at the same time, it allows me a more flexible workday. Besides, it was worse during the financial crisis when there was a lot happening at weekends as well. There were

• Born in Kongsvinger, Norway, in 1977.• Senior Portfolio Manager in Storebrand Asset Management since 2003.• Economist and risk controller in Storebrand 2003.• Corporate Trainee in Storebrand 2001 – 2003.• Master of Philosophy University of Oslo (M.Phil.) - Cand. Oecon, Economics, Mathematics 1996 – 2000.• The London School of Economics and Political Science (LSE), Master of Science (MSc), Economics 2000-2001.

OLAV CHEN

THE EDGE OF THE RISK SCALE

028 ESTATE MAGASIN | N°1 2016

PORTRAIT

EFFORTS YIELD RESULTS: - In Norway, it is preferable to be clever without putting a lot of effort into it. Only in sports the opposite is accepted, says Chen, who has had a Chinese upbringing and who is used to working hard.

numerous emergency meetings where politicians were trying to find solutions and it was vital to keep up, says Olav Chen.

FRAGMENTED IN COMMERCIAL PROPERTY. Estate Magasin meets him at Storebrand’s head office in Lysaker, just outside Oslo. This is where the West corridor from the capital starts, where the letting market for office space is beginning to get heavy.

- The market for commercial property will be very fragmented in the period ahead. I would stay well clear of the West Country, as em-ployment growth must be the basis. The oil industry has experienced powerful cuts, resulting in a challenging letting market. We see the same trend here in the West corridor, as several oil service companies are located here.

OSLO IN EXCEPTIONAL POSITION. The situation is completely different in the centre of Oslo.

- There are many public sector tenants there, who are not affected by the downturn in the oil industry. We also see that unemployment in Oslo has in fact gone down in the last 12 months, whereas unem-ployment in Norway as a whole has gone up. The commercial pro-perty market in Oslo is characterized by the fact that this is where the jobs are, but eventually the downturn will probably be felt a little there too, he says.

UNDESIRED EFFECTS. According to Chen, the thousand kroner qu-estion is how increased unemployment, as well as increased fear of losing one’s job, will affect consumer consumption and savings. This “second round” effect may result in new undesired effects in the Nor-wegian economy.

- Norway is fortunate in that it has more opportunities for action than other countries. Thank goodness for the fiscal rule (handlings-regelen) which has prevented Norway from spending an unnecess-

029ESTATE MAGASIN | N°1 2016

ary amount of money from the Government pension Fund Global (The Fund) in good times. In periods of depression, Erna Solberg, the Prime Minister, has the opportunity to spend money on the building of roads and other infrastructure if a proper crisis should emerge.

INDUSTRIOUS AND HARD WORKING. Olav Chen was born and brought up in Kongsvinger. His parents are from Shanghai and have mainly applied Chinese values in the upbringing of their son. This meant being industrious and hard working – especially when it came to schoolwork.

- I have probably been less exposed to the Jante Law than most people. I have no problem with being good or best, he em-phasizes.

HAD TO DOWNPLAY EFFORT. Both in primary, lower secondary and upper secondary school Chen felt that many of the pupils had to downplay their efforts prior to tests: “No, I haven’t done much studying.”

- In Norway, it is preferable to be clever without putting a lot of effort into it. Only in sports, the opposite is accepted. Look at Martin Johnsrud Sundby (leading Norwegian cross-co-untry athlete, ed. com.) who trains more than anyone else and becomes a number one in cross-country skiing. He is cheered. You are however considered a nerd and a climber if you spend Friday nights in the university reading room.

FRIDAY NIGHTS IN THE READING ROOM. Chen spent many a Friday night in the reading room when he was studying at the University of Oslo. He found it liberating to start his studies at The London School of Economics and Political Science.

- There the mentality was the complete opposite from Norway. If you didn’t sit in the reading room on a Friday night, you were considered a “free rider”. You might be taken to be the child of an oil sheik, who did not have to make an effort with the studies to be successful. To me, there is a clear connection between effort and results.

NATURAL TO INVEST IN PROPERTY. Storebrand Asset Manage-ment is among Norway’s largest pension management firms, and property is an important part of a balanced portfolio.

- Property is of course not a super-liquid asset class but at the same time pension assets are by definition long term, and that makes it natural to invest in property, he says.

The portfolio includes wholly as well as jointly owned office space and shopping centres in Norway.

ATTRACTIVE TO FOREIGNERS. – Because of the low interest rates. we and others are now being forced onto the risk scale. This is what the central bank wants, instead of keeping money in the bank, we should invest it or spend it. Then, commercial property becomes an interesting investment opportunity, says Chen.

Also, the low krone exchange rate makes it even more at-tractive for foreign investors to buy commercial property in Norway.

Thank goodness for the fiscal rule (handlingsrege-len) which has prevented Norway from spending an unnecessary amount of money from the Oil Fund in good times.

030 ESTATE MAGASIN | N°1 2016

PORTRAIT

- Foreign investors now achieve an exchange efficacy of 20 – 30 per cent in the short term. This contributes to keeping the price level of commercial property high, at least in Oslo, although the total space vacancy in Norway is increasing.

CYCLICAL IN HOUSING. As to housing prices, Chen indicates that a lot is cyclical.

- Jobs are currently to be found in Oslo but the labour im-migration might easily reverse. The weakened krone makes labour immigration less attractive, which again might result in a reduced demand for housing.

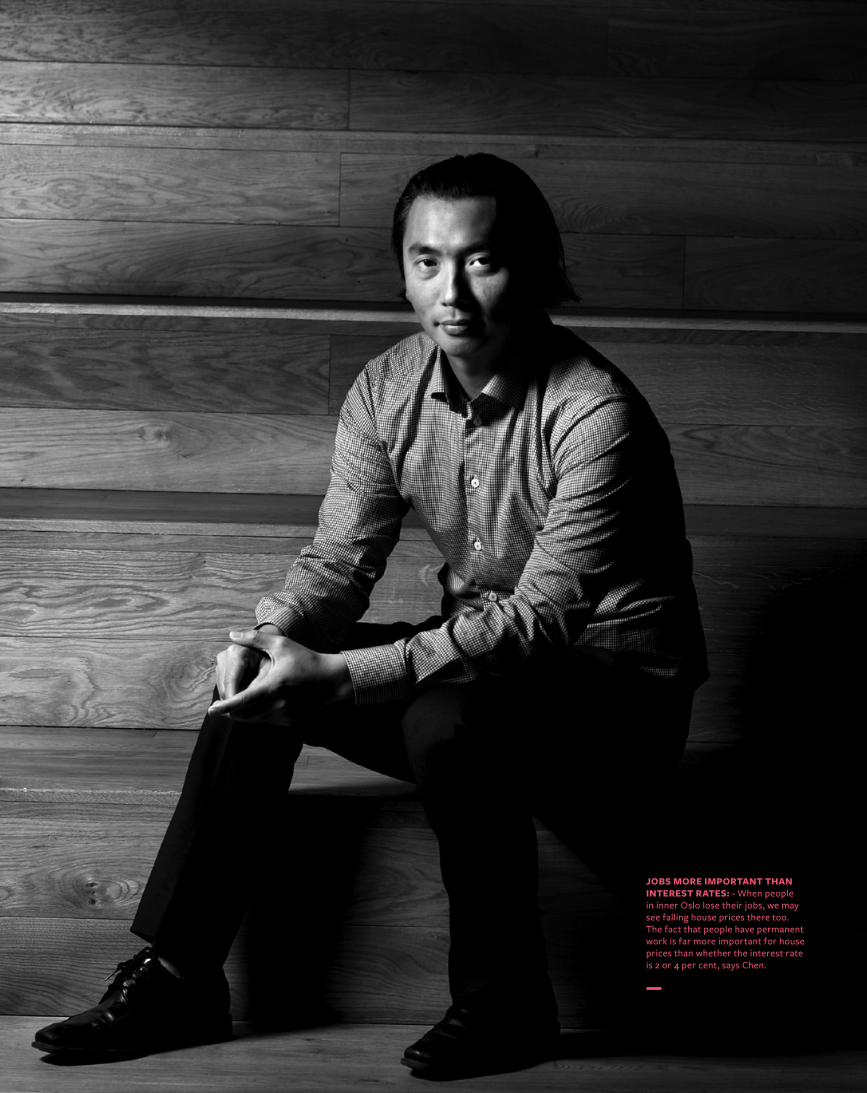

- When people in inner Oslo lose their jobs, we will see falling house prices there too. The fact that people have per-manent work is far more important for house prices than whether the interest rate is 2 or 4 per cent.

THE DOUBLE EFFECT. Chen deduces that whenever large cuts take place in the oil service industry, there will gradually be less work for, for instance, financiers and lawyers in and around Aker Brygge as well. The consequence being fewer restaurant visits and less shopping.

- If households do start to tighten their belts, the double effect comes in. Then, we may have a crisis in Norway, he warns.

Chens thinks that the flood of refugees into Norway might to a certain degree compensate for this, as the moun-tain resort hotels will suddenly have a high occupancy and the rate of employment and the general activity in the local environment will go up – refugees do after all shop in the local shops. This effect will however be short-term.

INNATE INTEREST IN CHINA. Since his parents come from Shanghai, Chen does not only travel to China at least once a year, he also has an innate interest in China and the coun-try’s role in international economy.

- China is becoming increasingly important from an econ-omic point of view and for me in connection with the invest-ments we make. The previous correction in the stock market did after all start in Asia. We will hear more and more about China in the future, he says.

RAPID CHANGES. Things happen fast in China, according to Chen.

- That is the advantage of a totalitarian state and a command economy; you don’t have to spend 10 years discus-sing things like the Fornebu tube. They simply decide and the following year they start building, he smiles.

China has used the last 10 years to improve the infrastru-cture and this has resulted in a great demand for raw mate-rials from countries like Russia and Australia, as well as a number of the so-called emerging economies.

Foreign investors now achieve an exchange effi-cacy of 20 – 30 per cent in the short term. This con-tributes to keeping the price level of commercial property in Norway high.

031ESTATE MAGASIN | N°1 2016

JOBS MORE IMPORTANT THAN INTEREST RATES: - When people in inner Oslo lose their jobs, we may see falling house prices there too. The fact that people have permanent work is far more important for house prices than whether the interest rate is 2 or 4 per cent, says Chen.

032 ESTATE MAGASIN | N°1 2016

PORTRAITPORTRETT

033ESTATE MAGASIN | N°1 2016

CUTTING EACH OTHER’S HAIR. – In principle, China now goes from buying raw materials from other countries to cutting each other’s hair. China is fast becoming a domestic economy where the service sector will grow more than traditional manufacturing, and this may have major consequences for other countries, he says.

- Those who were relying on exportation to China will see this as a major setback.

NORWEGIAN ICY FRONT TOWARDS CHINA. In 2010, Liu Xiaobo was awarded the Nobel Peace Prize “for his long and non-violent struggle for fundamental human rights in China”.

- He has been a strong spokesman for the application of fun-damental human rights also in China, said the then leader of the Nobel Committee and former prime minister in Norway, Torbjørn Jagland.

This peace price did not only lead to an icy front growing up between Norway and China, it also lead to a political debate in Norway as to whether this was a wise decision.

THE GOVERNMENT PENSION FUND GLOBAL CAN FORGET CHINA. – What do you think of this peace price?

- I think it was unnecessary and very unfortunate in view of the good relationship Norway and China had had over a long period of time, economically as well as politically. Nothing is happening now, the relationship is perhaps at the present time poorer than ever. It seems as if Norway is digging in, thinking it will pass, but I don’t think that will happen. I think a possible solution lies in the hands of Norway, Chen replies at the very moment when the Tunisian Natio-nal Dialogue Quartet is in Oslo to receive the 2015 Peace Price.

- The Oil Fund is a substantial property investor now showing an interest in the Asian market. Can we envision the Fund acquiring pro-perty in China?

- No, in view of the current political relationship between the two countries that is not possible.

MASTERS SHANGHAI-CHINESE. Chen masters Shanghai-Chinese. There is however one Norwegian word he is unable to translate.

The raw material exporting countries are now in for a blow, and Norway is not unique in this connection.

034 ESTATE MAGASIN | N°1 2016

The word is «skippertak» , and for the readers of Estate Magasin: The expression dates back to the time when many Norwegians worked as seamen. On long voyages, there was not a lot to do but whenever the ship was entering or leaving a harbour, everyone, including the captain, had to work hard. Today, the expression is used in connection with work but is perhaps best known in connection with studying, ie. the stu-dents read most of the curriculum right before the exams.

- Is there a Chinese sign for skippertak?- No, I think the word skippertak only exists in the Nor-

wegian language, he smiles.

NEW AND CHALLENGING SITUATION. Norway has an open and exposed economy. The oil price affects the global economy and Norway is affected by both the oil price and the global economy.

- The 2008 financial crisis affected all countries, but Norway to a lesser degree because of the oil revenues. During the national debt crisis a few years later, we were saved by the oil investments. Now, the raw material exporting countries are in for a blow and Norway is not unique in this connection. This is a new and challenging situation for Norway.

What was your first job?- My parents opened the first Chinese restaurant in Kongsvin-ger in the county of Hedmark in the 1970s. I worked there a lot. When studying at Blindern I was seminar leader and computer room guard.

Your first property?- A 40 square metre flat in Grünerløkka. I am very fond of Grü-nerløkka; it is less homogenous than other parts of Oslo. (Chen has since moved to a larger flat in Grünerløkka, ed.com.).

What do you listen to?- Spotify, he replies as he opens the app to find out that he last listened to Coldplay. - I will listen to anything.

What do you read?- I read mostly on the internet, the websites of Bloomberg, Eco-nomist, Wall Street Journal and Financial Times. As to books, I mostly read quasi-professional literature. The last book I read was “Flash Boys” by Michael Lewis.

What do you do in your spare time?- I play a little company football in addition to working out at SATS. I also spend time skiing and snowboarding, as well as on social activities.

What annoys you?- Traffic jams. I will do anything to get out of the queue and find an alternative route. And drivers who consequently drive in the left lane even though there is plenty of space in the right lane. Put that at the top of the list. That really is annoying.

What puts you in a good mood?- Sunshine, summer, sea and beaches. I am definitely a summer person and have recently bought myself a boat.

How do you so far rate the present government?- I like Erna Solberg – she is doing a great job. Otherwise, it varies a little. But I think they should be allowed a little more time to get on top of things.

EIGHT QUICK ONES

FOLLOWS CHINA CLOSELY: - China is fast becoming a domestic economy where the service sector will grow more than tra-ditional manufacturing, and this may have major consequences for other countries, says Chen, who follows the economic superpower closely.

PORTRAIT

035ESTATE MAGASIN | N°1 2016

A broader perspective

%

The solution to your challenges lies in our combined knowledge and experience. Deloitte has a broader perspective that makes the difference.

Auditor of some of Norway’s largest real estate business groups

Optimizing and structuring real estate projects

Valuation and financial advisory

Among Norway’s leading real estate lawyers

Real estate lawyers in more than 50 countries

Planning and executing successful transactions

www.deloitte.no

One of the world’s largest supplier of professional services. 225 000

employees in over 150 countries, with a global network within the Real Estate industry.

036 ESTATE MAGASIN | N°6 2013

ARCHITECTURE

«It was almost like déjà vu but it still left me breathless. Entering from the enclosed back of the house and seeing how it opened up towards the city below was very special.”

Modernistic principles

038 ESTATE MAGASIN | N°1 2016038

ARCHITECTURE

She recalls how they arrived while it was still daylight and stayed until darkness fell, and how the house and the place changed in pace with the city, that they did not want to leave, simply stay there and quietly enjoy the view.When Maren Bjerkeng, architect and partner in Grape Architects, was on a field trip to Los Angeles in 2011, she visited Stahl House for the first time. The house, which is clinging to one of the least buildable pieces of land in Hollywood Hills, is a spectator of the city. - Architecture must be experienced and Stahl House is no exception. The building is iconic and can be said to have achieved its “fame and fortune” through Julius Shul-man’s fabulous picture of it – not least as a backdrop in a number of films, series and advertisements, but nothing measures up to seeing it in real life, says Bjerkeng.- In addition to the spectacular location, the house is incredibly beautiful: the pure and simple shape, the logical and orderly layout, and the honest use of materials. To me, however, the history of the house is also

what makes it more interesting and even more beautiful, she continues.

AHEAD OF ITS TIMEThe house was built in 1960 as number 22 in a series of “Case Study House” projects in post-war America. These projects were sponsored by the Art & Architecture maga-zine to explore new forms of housing based on modernistic principles. It was at the same time an interesting experiment enabling or-dinary people to live in buildings that were architectural masterpieces, designed by the most famous architects of that time.- Admittedly, the owner, Buck Stahl, was exceptionally active in the development of the project. He acquired a site no one else would have, and envisioned a modernistic house of glass and steel with a 270 degree panoramic view of LA. He built the terrain and foundations from recycled concre-te, which he had collected from building sites all over the city. The architect Pierre Koening did not join the project until 1957, Bjerkeng explains.The architect is particularly impressed with how Stahl House with its pure and simple aesthetics challenged both the conventio-nal form and the structuring of housing.- For example, by it being so transparent and open it required the biggest sheets of glass possible to make at that time, she says.The house has an L-shaped form with one wing containing bedrooms, the swimming pool located at the intersection and one wing housing the common areas such as kitchen and living room.- The logical and simple layout is perfectly adjusted to the location and the functions. The most private zone towards the road at the back is more enclosed and introvert. You are automatically drawn to the open and transparent part of the house with different overlapping zones defined by fixed furnitu-re. The kitchen is situated at the back, the two living room zones are separated by the fireplace and the outermost zone is more open, focusing on the city, making it part of the interior. The furniture has probably been changed and replaced over time but it

A

ARCHITECTURESilje Rø[email protected]

039ESTATE MAGASIN | N°1 2016 039

Stahl House , also known as Case Study House # 22, is a modernist house designed by architect Pierre Koenig in the Hollywood Hills , Los Angeles.

ARCHITECTURE

Stahl House , also known as Case Study House # 22, is a modernist house designed by architect Pierre Koenig in the Hollywood Hills , Los Angeles.

has been kept in line with the house’s aest-hetics, emphasising it, she explains.

MERCILESS ARCHITECTUREThe challenging topography of the site is an important element in the architecture. The architect and the owner set high aesthetical standards and omitted unsightly balustra-des along the cliff edge. The swimming pool, the centre of the house, is also unsecured. - Thus, the house challenges conventions related to security. I have been told that instead of a fence along the escarpment, the family established a “baby catcher” in the form of a slightly sloping horizontal fence just below the escarpment, and that the children wore life vests in their early years. However, the precautions turned out to be unnecessary as the children automatically adjusted and lived with the house. Perhaps not an example to follow but nevertheless an interesting example of a lack of compro-mise, which in this case worked, the archite-ct says with a smile.What Bjerkeng finds most inspiring is the history and the vision. Having a vision, challenging conventions and seeing oppor-tunities others do not see, has been a great source of inspiration to her, and this is also the aim of Grape Architects and what they wish to achieve in their projects.

AMERICAN BEAUTY- Location is an important part of the wow factor and as a supporting element in Stahl’s vision, it makes the house truly unique. Sitting in the living room which hangs over LA, looking at the city with its endless rows of illuminated streets is beautiful and incre-dibly evocative, she says.The orientation of the house follows the grid of the city and it is easily understood why the city has been given such an important role in the house.- Today, it may seem something of a paradox that the beautiful view is towards Los Angeles, USA’s largest city with close to four million people. The “feeling of infinity” is due to an extreme form of dense, urban sprawl – a city structure that is both enclo-sed and scattered. What is beautiful and gives you a special kind of tranquillity when looking through the large windows of Stahl House, appears quite different when you are actually in the city, which is polluted, not very accessible and where it is difficult and unnatural to move about on foot, the archi-tect explains.- To me, this illustrates that beautiful things may have many and often conf licting facets and layers, and that context, scale, perspective and situation have an impact on whether or not it is beautiful, and that

“To me, this illustra-tes that beautiful things may have many and often con-flicting facets and layers, and that con-text, scale, perspecti-ve and situation have an impact on wheth-er or not it is beauti-ful, and that beauty can also sometimes be misleading. This is what makes it uni-que and interesting – and beautiful.”

ARCASA arkitekter asArcasa arkitekter AS. Sagveien 23c III, 0459 Oslo.

Telefon 22 71 70 70. [email protected]. www.arcasa.no.

VISUALISERING og tydelig design skaper bedre forståelse av ditt prosjektVi liker utfordringer i prosjektene og har lang erfaring med komplekse og krevende prosesser. Sammen med vårt datter-selskap Blår AS viser vi hvordan det ferdige resultatet kan bli, både for utvikler og fremtidige brukere.

Snakk med oss om:

• Reguleringsplaner

• Næringseiendom

• Boliger

• Design og Interiør

• Visualisering i 3D

Vi bidrar gjerne med visualisering av dine prosjekter også!

www.blaar.no

Kilenkollen, Selvaag Bolig

042 ESTATE MAGASIN | N°1 2016

ARCHITECTURE

NAME: MAREN BJERKENGAGE: 38

• Position: Partner in Grape Architects

• Education: The Oslo School of Architeture and Design, UniRoma3; Faculty of Architecture and Fine Art, The Royal Danish Academy of Fine Arts and the University of Oslo, Faculty of Law.

• Selected projects: Ruseløkkveien street plan, Fornebuporten, Aker Solutions Curitiba, Aker Solutions Tromsø, carpenter building/admi-nistrative building Aker Brygge.

Huset ble ferdigstilt i 1959 for Buck Stahl, og eies fortsatt av familien. Det er et kjent fra både filmer, reklamer, TV-serier og musikkvideoinnspillinger.

beauty can also sometimes be misleading. This is what makes it unique and interesting – and beautiful, she continues.

TAKE RESPONSIBILITY!Bjerkeng has always been attracted to big cities, of widely different character, and she finds it extremely exciting to see how history leaves its mark and explains each city’s layout and building structure, and how this triggers different sentiments.- LA is a fascinating city. It appears to be relatively green, surrounded by green hills, and it houses a great number of archite-ctural pearls. It has, however, also serious environmental problems and few pleasant urban spaces, the exception possibly being a few areas around Venice, which has a completely different and more accessible scale, she says. - LA is characterised by a density that is evenly smeared out, without distinct centres or hubs. You are therefore comple-tely dependent on having a car, and from an environmental perspective, the city is a horrifying example of urban development, the architect continues.

LA ranks as number two on the list of Ame-rican cities with the highest Co2 emissions, beaten only by Houston where action is being taken in the form of various initia-tives such as Megacities Carbon Project, aiming to make changes that can contribute to reducing the emissions.- I think that we as architects have a re-sponsibility to join in fulfilling the ambi-tions and give them a physical expression, to test, challenge and give substance to the possibilities available in overall plans and regulations. This is something I am stron-gly committed to. If we are good at thinking anew and see the possibilities, we can, by creating good and beautiful buildings and urban spaces in the right places, contribu-te to making the city beautiful, not only to look at but also to be in, she concludes.

Photo: Kirsti Mørch

CONTACT:

Audun L Bollerud, [email protected] Anders Utne, [email protected]

Andreas Frislid, [email protected]

Ambitious and skilled real estate developers and investors need ambitious and skilled real estate lawyers.

Looking to invest in Norway?

Let us help you with the acquisition, the structuring, tax and financing issues.

ADVOKATFIRMA RÆDER Henrik Ibsens gate 100, Oslo, Norway. Phone: +47 23 27 27 00, Email: [email protected]

www.raeder.no

Foto: Damian H

einisch Design: Mission AS

043ESTATE MAGASIN | N°1 2016

CONTACT:

Audun L Bollerud, [email protected] Anders Utne, [email protected]

Andreas Frislid, [email protected]

Ambitious and skilled real estate developers and investors need ambitious and skilled real estate lawyers.

Looking to invest in Norway?

Let us help you with the acquisition, the structuring, tax and financing issues.

ADVOKATFIRMA RÆDER Henrik Ibsens gate 100, Oslo, Norway. Phone: +47 23 27 27 00, Email: [email protected]

www.raeder.no

Foto: Damian H

einisch Design: Mission AS

044 ESTATE MAGASIN | N°1 2016

NNEWSTorgeir Hågø[email protected]

The Norwegian transaction market had its best year ever in 2015, and the activity in early 2016 continues at the same level.

Boosting Norwegian transaction market

Partners Anne Sofie Bjørkholt and Stig Bech in BA-HR became one of the largest legal players in the European market, advising clients on real estate transactions for more than NOK 112 billion during the year, divided between NOK 80 billion on Norwegian properties and the remaining 32 on international portfolios.

- Having this massive input from the 2015 transactions, how does the Norwegian legal fra-mework suit the international buyers?

- I think our legal framework is very liberal and transparent, easy to assess and easy to navi-gate in, Bech says.

- The main reason is that most of the Norwegi-an background legislation can be waived between professionals. The market both for the sale and purchase and for leases of commercial real estate in Norway is from a legal perspective characteri-sed by the important role of background legislati-on and a broad use of standard agreements.

- The background legislation will be used to fill in unregulated areas in the agreements and will also affect the interpretation of the wording of an agreement. The Norwegian contracts for both leases and the sale and purchase of real estate are less comprehensive than their equivalents in, for instance, Anglo-American jurisdictions.

- Most of sale and purchase contracts are based on standard texts, although with individu-al adjustments as a result of negotiations, Bjørk-holt says.

- Key real estate organisations such as the Real Estate Agents Association, together with, among others, the law firm BA-HR, issue a set of stan-dard agreements for sale of property every two to three years in accordance with market practice,

legislative amendments etc. These standards are used as a basis for 80–90% of all leases and real estate transactions.

SHARE DEALS THE MAIN RULE- Are share deals the main rule for purchase of real estate?

- Yes, Bech says.- Capital gains on the sale of shares in a limited

liability companies are tax free for a corporate shareholder. This is in contradiction to the sale of assets that are taxable at 25% of the gain. In addition, a share deal will assume no stamp duty on the property, as opposed to a real estate asset deal. Stamp duty is 2.5% of the market value of the property. Thus, around 90% of commercial real estate transactions are carried out through the sale of the shares in property owning compa-nies (SPVs).

- Having said that, there are also a considera-ble number of real estate transactions structured otherwise – both as asset sales or through sale of parts in general partnerships, limited partners-hips and silent partnerships, Bjørkholt fills in.

- How is the calculation of the purchase price in share deals handled?

- The seller and the purchaser agree on the property value that forms the basis for the cal-culation of the purchase price of the shares in the target company, Bjørkholt explains.

The purchase price is normally calculated as follows:Property value with the addition of• the cash and receivables on the balance sheet of the company,• an agreed share of the deferred tax benefit re-

NEWS

045ESTATE MAGASIN | N°1 2016

Øyvind Hovland are partner and lawyer in EY Advokatfirma. Kristian Råum are senior manager and lawyer in EY Advokatfirma.

046 ESTATE MAGASIN | N°1 2016

presented by any loss carry forward (to the extent the buyer is willing to pay for this)• any other assets in the company s balance sheet that the parties agree to include and with deduction of • all liabilities on the balance sheet of the company • 9-10% (normally, based on practice from 2015) of the difference between the proper-ty value after the deduction of the estima-ted market value of the land (because the land does not qualify for any depreciations) and the basis for tax depreciation on the property as per closing.

- The rationale behind the latter dedu-ction, is that in a share deal, the buyer does not obtain a step up in the tax basis for the property, but takes over the tax basis in the target company. Thus, the buyer will not be able to depreciate with tax effect the dif-ference between the agreed property value and the tax basis in the target company, Bech says.

THE LAND VALUE- What do you do with respect to the land value?

- There is no depreciation on the land, as opposed to the building which can be depreciated by 2% plus 10% on the fixed te-chnical installations. The market value of the land is subject to discussions/negotiati-ons, but is often agreed as being 20–25% of the property value for properties in central areas.

- Often, the fixed technical installa-tions will amount to around 40% of the building’s total tax value for a newly built building. Warehouses, hotels etc. are de-preciated by 4% on the building and 10 % on technical installations, Bech says.

- And the price deduction to compensate for lower depreciation in a share deal?

- The net present value of the lower de-preciation can be calculated individually, but is normally defined as a lump sum being 9-10% of the difference between the agreed property value of the building and the tax value of the same. Because of a decrease in the general tax rate (from 27% to 25%), we assume that we might see a decrease of the percentage going forward.

- This is the case if the building is de-preciated by 2% annually, which is the rate applicable to office buildings for a building depreciated by 4% annually, such as a ware-house building, the deduction is normally agreed at 12-16%. This lump sum equals the percentage reached by using a discount rate of 6%, and assuming a 60/40 split between

building and technical installations. - In this respect it is important to be

aware of that under Norwegian market practice, the buyer is thus not compensa-ted for the full latent capital gains tax on the property, i.e. the total tax saving for the seller. Such compensation would have equalled the net present value of 25% of the difference between the taxable value of the building and land and the agreed pro-perty value, discounted over the gain and loss account by 20% each year (declining balance method), Bjørkholt explains.