Cornerstone - British Polish Chamber of...

20

Cornerstone Building smart BIM as a risk management tool Blockchain: Redefining the future of real estate? Benelux at the crossroads of Europe Post-Brexit Investment Opportunities AECOM Quarterly Property Newsletter for Europe Issue No. 3 Q3, 2016 aecom.com

Transcript of Cornerstone - British Polish Chamber of...

Cornerstone

Building smartBIM as a risk management toolBlockchain: Redefining the future of real estate?Benelux at the crossroads of EuropePost-Brexit Investment Opportunities

AECOM Quarterly Property Newsletter for EuropeIssue No. 3 Q3, 2016

aecom.com

00101110 01101100 10100110 01011011 01100011 11111001 01101111 01100100 01111101 11110111 10101011 11100010 11001001 10100110 00011010 01001101 11000001 11101110 10010010 11101110 10111101 11100001 01111001 11100101 00110110 11000010 10101110 01110001 01010001 00101100 00011111 10101000 10010101 10000001 01100011 11000000 01110110 10111110 10100001 00010001 00010010 01010010 01111100 01100001 00000110 01011001 10111011 10111110 11011001 00111110 00010010 10101010 01100110 10110111 00000010 11001100 11000001 01101111 01100001 00011000 10111010 10110010 11000000 01000100 01101100 01110110 00001001 11111110 00011111 01001111 00011000 11011001 10010100 01111100 11000001 01000100 00100000 11001010 00001001 11000011 10111000 00000111 11000001 00111111 01101111 00100011 11100000 11001001 01111011 00111110 10111101 01100011 11000100 00011000 00100001 10100110 11010001 11001111 00110110 10110011 01011001 00011000 10010000 01011110 00001100 11101111 10110010 01011101 01100001 01110110 11000100 11110010 10011000 00110011 01001000 01101110 10101000 10111110 00110011 10101110 11111000 00011111 00010011 10110101 00101100 01001110 11011011 11011011 01000100 00010101 11001000 11010010 00111011 01001000 11110010 00000001 01101011 01011000 00110010 01110110 01100010 00100000 10001100 10101001 10011010 10000010 10101101 01111011 11001011 00111100 10010110 11001100 11010011 11110011 01100101 11100100 00001000 11111011 00100001 10100110 00011100 01111011 01001111 00101011 00010011 00010010 10111010 10010111 01001001 00000100 10110100 00010001 01110110 11100000 00111100 11110100 11001010 11001100 10010111 01101000 01110010 10110011 00010010 11010110 00010010 00000000 01110000 01001110 11010000 11111110 00100111 10111111 11000100 10100111 10111110 10100000 11001001 00011110 11000001 11011110 11111001 11010101 00001101 01100001 11111011 11100101 00010100 10101001 00110101 10011110 10110110 01111001 11001100 01011110 01001001 10101101 10000000 11100000 10011111 01001100 00110110 01001001 11011001 00011110

Post-brexit investment opportunities

Contact

Blockchain: redefining the future of real estate?

BIM as a risk management tool

Benelux at the crossroads of Europe

Building smart

Building smart

A fully integrated smart building connects this data to allow previously disparate systems and users to engage with the built environment in new and more effective ways. Appropriately deployed, a ‘smart’ building should become more efficient over time, continuously engaging the workforce and ultimately helping to reduce operational costs and increase occupant wellbeing and productivity.

Smart buildings are a bleeding edge technology integration

movement in the built environment. Based on the growing development of cloud computing and data management, a smart building links together multiple data sources, inputs, and user types into a cloud of useful information to create a more efficient, effective and engaging workplace.

Foundations for the futureThe foundation of a successful smart building is the ability to seamlessly merge hardware solutions that use economical and universal standards, software solutions that create useful information out of data analytics and bridge multiple platforms in two-way communications, and workforce change management that encourages occupants to adapt to their new smart environment. Ultimately, the critical measure of success in a smart building is the ability to function effectively over time; therefore the integration strategies of hardware, software and workforce must be robust, adaptable and flexible into the future.

Elements of a Smart Building

Productivity, comfort and wellbeingResearch shows that executive function is significantly improved in healthier buildings, improving decision making and reducing absenteeism. Using smart technology, occupancy, movement, lighting, humidity and temperature can all be continuously measured, allowing building systems to maximise effectiveness of energy use, thermal comfort and daylight balance.

Worker and workplace engagementWork environments are evolving. From smart transportation to collaborative technology, the office is becoming a place to interact and connect. Today’s workforce expects to be seamlessly connected in and out of the office, and flexible and customisable spaces allow individuals to make choices about where and how they work.

Safety, security and access controlIntegrated technologies and virtual environments are changing the traditional structure of building safety, security and access control. Physical Security Command and Control can be supplanted with a virtual, distributed and mobile one, changing how a building is planned and programmed. Automated Standard Operation Protocols can interpret events from multiple inputs and provide responses faster than a traditional security system, saving time and increasing response accuracy.

lighting

daylighting

temperature

humidity

sensing and integration

centralized command and

control

access control and management

video surveillance

asset management

emergency response and

communications

furniture and flexible work environments

utilization

technology and collaboration

food

health and wellness

opportunities for growth advancement

and feedback

smart transportation

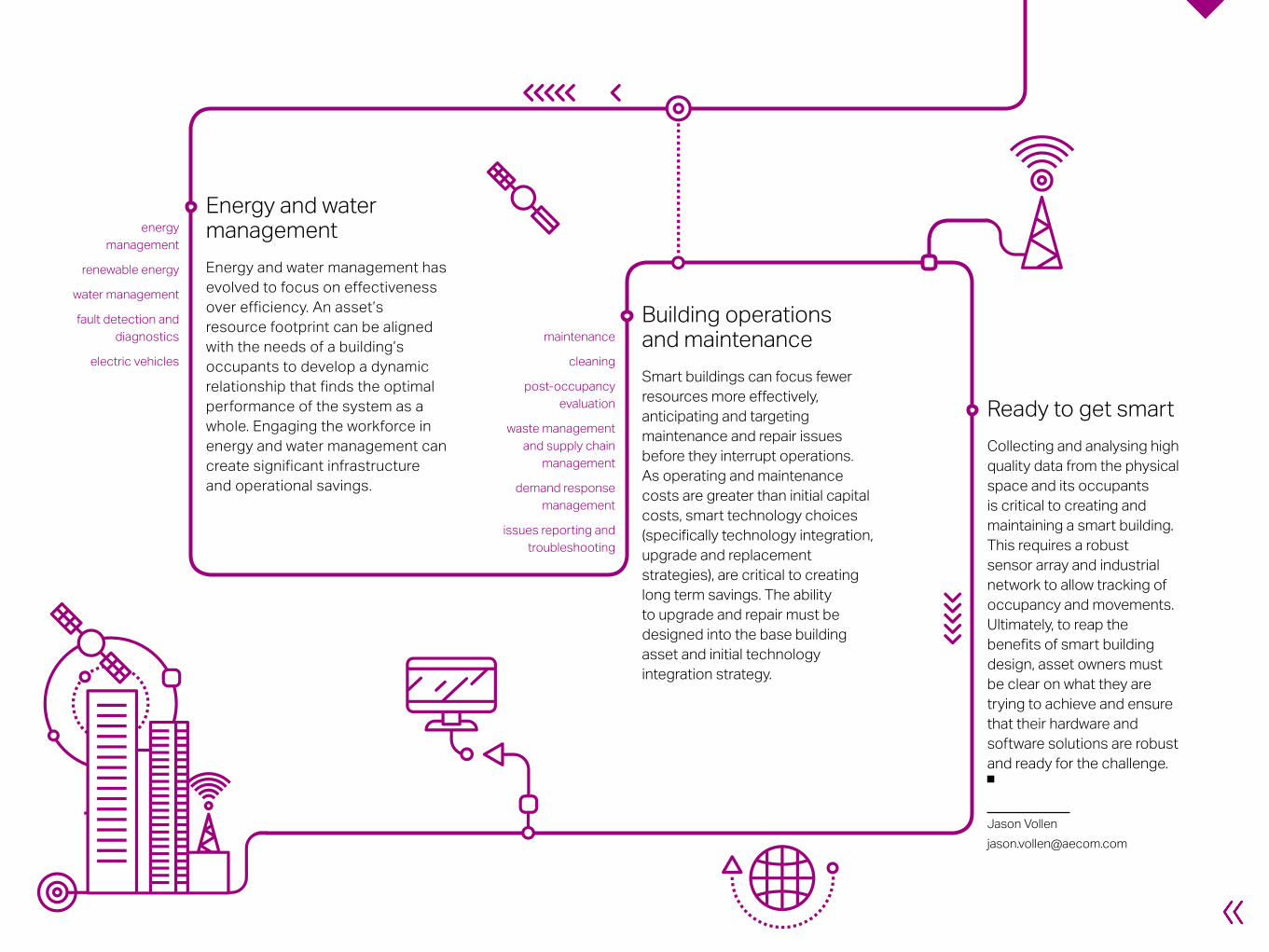

Energy and water managementEnergy and water management has evolved to focus on effectiveness over efficiency. An asset’s resource footprint can be aligned with the needs of a building’s occupants to develop a dynamic relationship that finds the optimal performance of the system as a whole. Engaging the workforce in energy and water management can create significant infrastructure and operational savings.

Building operations and maintenanceSmart buildings can focus fewer resources more effectively, anticipating and targeting maintenance and repair issues before they interrupt operations. As operating and maintenance costs are greater than initial capital costs, smart technology choices (specifically technology integration, upgrade and replacement strategies), are critical to creating long term savings. The ability to upgrade and repair must be designed into the base building asset and initial technology integration strategy.

Ready to get smartCollecting and analysing high quality data from the physical space and its occupants is critical to creating and maintaining a smart building. This requires a robust sensor array and industrial network to allow tracking of occupancy and movements. Ultimately, to reap the benefits of smart building design, asset owners must be clear on what they are trying to achieve and ensure that their hardware and software solutions are robust and ready for the challenge.

Jason Vollen [email protected]

energy management

renewable energy

water management

fault detection and diagnostics

electric vehicles

maintenance

cleaning

post-occupancy evaluation

waste management and supply chain

management

demand response management

issues reporting and troubleshooting

BIM as a risk management tool

Although these initiatives are driving innovation today, the next generation of BIM tools will focus on new ways of harnessing the geometry and data of the design models themselves, with risk management tools being the catalyst to a fully integrated delivery model.

Autodesk and Trimble have recently entered into an operability agreement that underlines the importance software providers are putting on more effective ways of connecting design and project management. The development of new bespoke project ecosystems which connect geometry and data together, allowing “real-time” interactions and analytics between design team members is becoming more common, for example:

Architects have been harnessing the

geometric aspects of BIM for many years resulting in a new generation of more complex building forms; but with ever increasing datasets, delivery cost is also being driven down as a consequence of BIM.

Microsoft’s Hololens immersive headsets being used on the design of the 2016 Serpentine Gallery

– Using ‘design to cost’ dashboards that provide architects with real-time cost data to allow the impact of design decisions to be instantly assessed and refined.

– Allowing the early examination of innovative construction approaches such as ‘flying factories’ and modular construction to help radically decrease assembly and construction time, whilst improving health and safety, cost and sustainability outcomes.

– Harnessing 3D tools as part of new coordination and design management processes, hence speeding up the iterative design process

Contractors are harnessing 4D (time) technologies linking their construction programmes to the design team’s BIM model, thus enabling varying construction strategies to be rehearsed, hence reducing site risk and optimising delivery.

Cost risk is also being managed by allowing commercial teams to more effectively link into the design model using 5D techniques that link into predefined templates that feed into historical cost databases.

Immersive technologies are radically changing the way we design, presenting better ways of communicating the developing designs to clients, shifting design team meetings and presentations away from the two dimensions of the meeting table. Meetings can be hosted inside design models with participants, and their avatars, joining in from around the world to discuss design issues in profoundly different ways, transitioning away from 2D information towards contemporary 3D connected environments.

Connecting project information in real-time significantly reduces project risks by minimising the time lag between issues, and the receipt and use of information. With an ever increasing number of parties using project information, real-time collaboration reduces the risk of any party using out of date information. Crucially, risks are managed by making sure the right information is available at the right time, and by connecting this information more effectively more rapid iterations of the design process are possible. For example, allowing a cost plan to be automatically updated upon receipt of the latest design team release, or enabling an engineer to rapidly assess the implications of a change in architectural specification.

Strategic project risks will continue to be managed in project workshops that identify key issues and determine who is best placed to own, manage, reduce and eliminate each risk as a project progresses. However, ultimately the aim is to fully enable project management teams to provide real-time feedback to the design team regarding the status of these risks, so as to speed up the process of resolution.

Harvesting the data

Design contentcreation

Project-wiseProalianceAPICEco-System

BIM 360 GlueRFI

3D WorkshopnavisBIM 360

Solibri

GIS IntegrationESRI Infraworks

Collaboration Validation

Manage

CommentImmersion

Geometry5D Cost x4D PrimaveraDATA Drofus6D Maximo

MEP AnalysisC&S Analysis

ARCH RevitMEP RevitC&S Revit

Data

VisualisationFly ThroughARVR

Looking to the future, likely key trends will be;

– The further automation of the design process using coding and scripting tools such as Grasshopper and Dynamo, which are currently used to define parametric geometry.

– The development of new quality assurance processes built around 3D workflow and coordination processes, offering the ability to automatically validate design models by checking against predetermined rulesets.

– The use of machine learning and other artificial intelligence techniques to improve decision-making.

BIM is taking construction on a journey from current analogue structures towards new digital working methodologies. Innovation that is not only driving efficiencies in delivery and out-turn cost, but also improving health and safety and risk management.

Dale Sinclair [email protected]

00101110 01101100 10100110 01011011 01100011 11111001 01101111 01100100 01111101 11110111 10101011 11100010 11001001 10100110 00011010 01001101 11000001 11101110 10010010 11101110 10111101 11100001 01111001 11100101 00110110 11000010 10101110 01110001 01010001 00101100 00011111 10101000 10010101 10000001 01100011 11000000 01110110 10111110 10100001 00010001 00010010 01010010 01111100 01100001 00000110 01011001 10111011 10111110 11011001 00111110 00010010 10101010 01100110 10110111 00000010 11001100 11000001 01101111 01100001 00011000 10111010 10110010 11000000 01000100 01101100 01110110 00001001 11111110 00011111 01001111 00011000 11011001 10010100 01111100 11000001 01000100 00100000 11001010 00001001 11000011 10111000 00000111 11000001 00111111 01101111 00100011 11100000 11001001 01111011 00111110 10111101 01100011 11000100 00011000 00100001 10100110 11010001 11001111 00110110 10110011 01011001 00011000 10010000 01011110 00001100 11101111 10110010 01011101 01100001 01110110 11000100 11110010 10011000 00110011 01001000 01101110 10101000 10111110 00110011 10101110 11111000 00011111 00010011 10110101 00101100 01001110 11011011 11011011 01000100 00010101 11001000 11010010 00111011 01001000 11110010 00000001 01101011 01011000 00110010 01110110 01100010 00100000 10001100 10101001 10011010 10000010 10101101 01111011 11001011 00111100 10010110 11001100 11010011 11110011 01100101 11100100 00001000 11111011 00100001 10100110 00011100 01111011 01001111 00101011 00010011 00010010 10111010 10010111 01001001 00000100 10110100 00010001 01110110 11100000 00111100 11110100 11001010 11001100 10010111 01101000 01110010 10110011 00010010 11010110 00010010 00000000 01110000 01001110 11010000 11111110 00100111 10111111 11000100 10100111 10111110 10100000 11001001 00011110 11000001 11011110 11111001 11010101 00001101 01100001 11111011 11100101 00010100 10101001 00110101 10011110 10110110 01111001 11001100 01011110 01001001 10101101 10000000 11100000 10011111 01001100 00110110 01001001 11011001 00011110 00110100 11110001 00001101 11111101 11010101 00010111 00101000 11100011 11001110 11111110 01110001 01111110 00000110 10001011 11000110 01001001 10101100 10010100 00110100 00001110 10000111 10000110 11100100 00100101 00101001 00000100 10011111 00111011 01100101 01010111 10110011 00101010 10010111 00111100 10010000 00000101 01010000 00010001 10011010 11010011 00010110 10110000 01001011 00001111 00110000 01100000 10101110 01100010 10000100 01100011 11010010 01100011 10001010 01100111 11011100 10111110 11011110 01100101 01000001 00111101 11100010 11101011 00100000 11001110 10100010 01011011 10101111 11010110 01101001 01011101 10010100 11000000 00101111 10101011 11111101 01101000 00000111 01000011 01010011 00100010 10101100 10001100 11101010 10100101 10110010 11100010 00111111 11100011 00001011 00000010 11001110 00001011 01001110 11110101 01100110 00100111 10011011 00011111 00111110 11000000 01111110 01101010 10011100 00000000 00100011 00011011 11001001 00100101 11110000 01100011 00100100 10101000 10101011 10100011 11000111 01001110 00101110 01100101 01110101 01100010 00111100 11101101 11101011 11100010 01001010 00011111 01011000 10010010 00011111 00011010 01000101 01111110 00100000 11110010 11000011 01001111 00000110 00000011 11111111 10000001 11101110 11001000 10001000 11101110 01011111 00010000 10010100 00101101 01111011 11101110 00011000 10101000 01000110 10110011 10011110 11111111 11010110 11100001 10000001 00101010 11000110 01010000 01111001 00000100 10111111 11100111 11010000 00000110 10000111 01100110 11110110 10010100 10111001 01010101 10100111 00101011 10011111 01001110 11001001 10100111 10111010 00110111 00110010 00011101 00000010 01111001 00111000 01011101 01111001 10111111 10011101 10110001 10101111 10101010 11000100 00010101 11001001 11001001 01011110 01100111 10101101 11001011 00001111 10010011 00100011 11001010 11011110 00111100 01100010 00101110 00101011 11011101 11011111 01101010 00101100 11000001 00011010 10010100 10101110 10010111 10110111 01100100 10110110 00100100 00001100 10101100 00111110 11110010 01110001 00011101 10101100 10011100 01101010 01010100 10100101 01011001 00111000 00111110 10010110 01011000 00111100 11000100 00010100 00010000 10100111 01001011 10011011 00011000 10111100 11001000 01110110 11111101 11000011 00000011 00101110 00100001 00110000 10101101 01110110 01111110 00101100 00111111 11101110 00101101 00100110 10011001 10101111 00110110 00011011 11001001 00110100 01011110 01010100 01000101 00110000 01010001 00111011 11001001 00110100 01011110 00101110 01101100 10100110 01011011 01100011 11111001 01101111 01100100 01111101 11110111 10101011 11100010 11001001 10100110 00011010 01001101 11000001 11101110 10010010 11101110 10111101 11100001 01111001 11100101 00110110 11000010 10101110 01110001 01010001 00101100 00011111 10101000 10010101 10000001 01100011 11000000 01110110 10111110 10100001 00010001 00010010 01010010 01111100 01100001 00000110 01011001 10111011 10111110 11011001 00111110 00010010 10101010 01100110 10110111 00000010 11001100 11000001 01101111 01100001 00011000 10111010 10110010 11000000 01000100 01101100 01110110 00001001 11111110 00011111 01001111 00011000 11011001 10010100 01111100 11000001 01000100 00100000 11001010 00001001 11000011 10111000 00000111 11000001 00111111 01101111 00100011 11100000 11001001 01111011 00111110 10111101 01100011 11000100 00011000 00100001 10100110 11010001 11001111 00110110 10110011 01011001 00011000 10010000 01011110 00001100 11101111 10110010

Blockchain: redefining the future of real estate?

Whilst the acquisition of property using virtual currency such as

Bitcoin still seems like a far-fetched concept, commercial real estate could be on the verge of adopting peer-to-peer cryptographic technology in the form of blockchain.

A wants to send money to B

How a blockchain works

The money moves from A to B

The transaction is represented online as a ‘block’

The block is broadcast to every party in the network

Those in the network approve the transaction is valid

The block then can be added to the chain, which provides an indelible and transparent record of transactions

Delivering trust In essence, blockchain is a database that allows people and organisations, who may not trust or indeed know one another, to share a set of verified, time-stamped records, typically financial. Trust delivered by way of cryptography.

Blockchain records who exactly acted in a particular way, and when. It provides a means of comprehensively tracking and ensuring the accuracy of information and can bring considerable value to procedures such as the registry of ownership title.

Financial peace of mind Imagine a world where the details of every office rental payment could be checked at the click of a button – the peace-of-mind, and power, of having a verified, accurate history of a property’s Net Operating Income since its first day of operation; a transparent, unchallengeable understanding of financial performance.

Blockchain could also have the potential to deliver highly efficient investment valuations using anonymised, comparable data. Complex, independent property valuations could become the exception rather than the norm, with elaborate financial due diligence and valuation procedures being replaced by a simple blockchain ledger.

There is considerable support for the theory that blockchain could also

eventually deliver incremental gains in property values. The power of blockchain’s cryptographic technology to preserve history has the potential to significantly drive down transaction costs and even add transparency to the property sales process.

Operational efficiency Allowing every operational transaction to be time-stamped, verified and allocated between tenants automatically, a live Service Charge reconciliation 365 days a year, 24 hours a day, all at the click of a mouse, is a powerful promise.

And blockchain is also revolutionizing physical access control systems by offering access via GPS enabled smartphones. This provides an unquestionable audit trail across worldwide property portfolios, accurately recording

who was where, and when – letting the right people into the right locations.

Embracing the future Blockchain is a very different way of doing things, it is about self-enforcement and diversifying trust. It’s about transparency and speed, a relentless drive for efficiency. Whether the change is driven by the regulators, financial institutions or asset managers themselves, ultimately, the commercial property world needs to ask whether it can afford not to embrace this change. With the promise of blockchain, the bricks-and-mortar world of commercial property could, finally, embrace the full power of our newly connected world.

Ian Church [email protected]

How blockchain works

Benelux at the crossroads of Europe

Benelux: Key facts Belgium The Netherlands Luxembourg

Population (thousands, 2016) 11 372 16 980 576Capital city Brussels Amsterdam - the capital Luxembourg City

The Hague - the seat of government Surface area (sq km) 30 528 37 354 2 586Head of State King Philippe King Willem-Alexander Grand Duke HenriHead of Government Charles Michel Mark Rutte Xavier BettelDate of next legislative election 2018 March 2017 2018Languages Dutch, French, German Dutch, Frisian Luxembourgish, French, German Currency Euro (EUR) Euro (EUR) Euro (EUR)GDP per capita (2015, current prices, US$) 44 383 48 326 102 101GDP growth (2015) 1,4 2,0 4,8Unemployment (2015) 8,5% 6,9% 6,5%Inflation (CPI) (2015) 0,6% 0,6% 0,5%FDI inflows (US$ million) 31 029 72 649 24 596EUR vs. USD exchange rate 1.0872 (as of 26/10/2016) 1.0872 (as of 26/10/2016) 1.0872 (as of 26/10/2016)

We are living in an extraordinary century of

urbanization and globalization. In an age where expansive networks of cities are becoming more important than nations, we often have more in common with cities thousands of kilometres away than we do with our hinterlands a few hundred or even a few dozen kilometres away.

As leaders, investors, and citizens, we ask ourselves: what kinds of new opportunities and challenges are we facing? Are the fortunes of existing cities and regions guaranteed?

Major shifts are transforming the prospects of our region. For starters, on a global basis, we are tilting eastward; at present all of Asia (including China and India) accounts for 30% of global middle-class consumption, but by 2050, Asian activity will represent 70% of the global economy.

We are also living longer; for the first time in history, we have regularly four generations in the workforce, and this demographic widening also broadens our values and the nature of our multi-ethnic communities. Of course there are also technological shifts; the digitalization of the workplace and the rise of machine intelligence are destroying established

customs and creating entirely new ideas about work, habitation, education, and leisure. The successful future city will embrace these astonishing and ongoing changes.

The Benelux (Belgium, Netherlands and Luxembourg) countries are particularly exposed to these shifts through their multi-facing windows on the world – the ports of Rotterdam, Antwerp, Ghent and Zeebruges, or Schiphol and both Brussels airports. The region interacts with the East by exporting large amounts of high-end goods from the Belgian, Dutch, German and French industrial heartlands, as well as importing commodity goods from the East to the consumption centres in the Benelux / Rhineland megapolis. These windows, production and consumption centres are well (inter)connected with crowded highways, railways and waterways. Benelux is truly at the crossroads of Europe.

Tees & Hartlepool (UK)

Immingham (UK)

Milford Haven (UK)

London (UK)

Southampton (UK)

Le Havre (FR)Dunkerque (FR)

Antwerpen (BE)

Rotterdam (NL)

Amsterdam (NL)

Bremenhaven (DE)

Hamburg (DE)

Gothenburg (SE)

Algeciras (ES)

Barcelona (ES)

Valencia (ES)

Marseille (FR)

Genova (IT)

Trieste (IT)

Taranto (IT)

75

54

34

82

42

42

35

40

396

41

114

5871

16534

59

38

60

4044

The EU 20 main cargo ports (in million tonnnes, 2011)

Source: Impact assesment, European Commission, 2013

As a consequence of being one of Europe’s key domestic hubs, as well as a gateway to the wider world, the logistics and distribution sector is an exceptionally important part of the regional economy. Belgium and the Netherlands have long since been recognized for their multi-modal accessibility, with activity in Belgium particularly focused around the Brussels, Antwerp and Ghent triangle, and Charleroi airport.

With retail clients and increasingly e-commerce continuing to drive occupier demand, there is impressive absorption across a range of asset types, hence pushing down vacancy levels in the most popular locations. Coupled with limited new supply, but with a plethora of investors seeking exposure to the robust fundamentals of both the region and the logistics sector, investment yields are undergoing compression.

Speculative warehouse development is slowly on the increase, however build-to-suit projects continue to form a significant proportion of new construction. Together with the increasingly complex requirements of the e-commerce sector, new insights and approaches on how to design, construct and future-proof warehouse properties are coming to the fore; advanced racking and picking systems, non-standard

ceiling configurations, smaller out-bound loading bays for vans rather than trucks, and real-time IT-systems for supply and picking are all very much the norm.

Staff facilities continue to evolve, with designing to minimum statutory requirements no longer enough for highly efficient picking facilities and shift work. Functional, efficient operations-led, process-oriented, design is key, and rather than minimising investment costs – operational effectiveness is becoming a key factor in maintaining investment value longevity.

With investment values in the logistics sector continuing to improve, and strong occupier fundamentals fueling both the supply of new product and rents, the thriving Benelux crossroads continues to become an attractive destination for both development and investment.

Emmanuel Raskin [email protected]

74% of EU trade goes by ship.Ports in Europe are directly connected to 848 ports in the Far East and 629 in Central and South America.

Africa 348

North America 340

South America 629

Asia 848

Middle East 89

Post-brexit investment opportunities

In the weeks that followed, property transactions were halted as investors’ renegotiated deals or pulled out altogether. A pause was inevitable amidst a shock that was political rather than economic. A few deals did go through albeit at reduced prices and shielded deal structures.

As the dust settles, it is becoming increasingly clear that the impact was less than feared and that markets have weathered the political uncertainty with surprising resilience. Since the referendum, financial markets have generally recovered and volatility has diminished.

The long-term outlook for the market is unclear and caution remains as there is still considerable uncertainty over the process by which the UK might leave the EU, and the implications of this. However, the rebound seems to indicate that the impact is unlikely to be enough to fundamentally change the underlying positive significantly of property markets in the United Kingdom and throughout the Eurozone.

The UK economy is in a fairly resilient shape. A new government is already in place and the central bank has provided several stimulus measures. The dip in currency should provide support to exports and has helped attract inward investment. In Europe, monetary policy and an improving labour market should continue to support its economy.

Economic conditions are expected to improve once uncertainty subsides. A downturn is expected with a gradual upturn resuming from

2018 onwards. Thereafter, growth is expected to resume as supply shortages should continue to cause prices to rise faster than earnings.

Whereas the investment market has seen a shift from panic to greater confidence as time has passed, the occupier market has seen a different dynamic. The forecast from the real estate industry is positive given the levels of activity and transaction volumes which point to a general level of confidence in the economy.

There is a solid underpinning of global appetite for yield and real assets. As a result, property should grow more attractive against competing assets like fixed income and equity supported by monetary policy and a flattening yield curve.

The weakening currency has made real estate more attractive, with the vote adding to the pressure for core investing. While the uncertainty surrounding Brexit will affect investor’s confidence, the market has a wide investor base. With the economic recovery set to continue, property is expected to remain an attractive investment.

A correction in asset pricing is bound to yield attractive investment opportunities. In an environment of heightened uncertainty and more conservative lending the focus is likely to be placed on core asset classes that are considered the most resilient. This creates opportunities for counter-cyclical investment strategies that take advantage of the dislocation in capital markets.

The result of the British referendum

on EU membership was a surprise that few anticipated with effects being felt throughout the Eurozone and beyond. The victory of the leave campaign led to the resignation of the prime-minister in the United Kingdom and to a sudden drop in the value of the currency and stock market.

-

5

10

15

20

25

Q2 0

7

Q2 0

8

Q2 0

9

Q2 1

0

Q2 1

1

Q2 1

2

Q2 1

3

Q2 1

4

Q2 1

5

Q2 1

6

Q4 0

7

Q4 0

8

Q4 0

9

Q4 1

0

Q4 1

1

Q4 1

2

Q4 1

3

Q4 1

4

Q4 1

5

The market was already slowing from the strong double digit growth of recent years. The referendum should accentuate the slowdown.

Source: LSH Research, Property Data, Property Archive

UK investment volume (£BN) Opportunity in adversityThe market was already slowing from the strong double digit growth of recent years. The referendum should accentuate the slowdown. This will put upward pressure on yields and slow rental growth, particularly in the more EU-dependent sectors such as London offices.

London’s office market was affected, but less than expected. London’s financial services have a global focus that is only partially impacted by the vote. The city continues to enjoy several structural advantages in these markets, which will not dissipate.

The referendum vote will delay some activity and the UK is set to be less favoured by some investors and occupiers, with other locations in Europe gaining at its expense. In the short term, the result is more likely to affect activity rather than values with the later supported by limited supply and lower interest rates.

Other European cities will aim to improve their status as financial centres. However it is unlikely that one will emerge. Rather, jobs that will potentially leave London are likely to be dispersed across a number of European cities, with Dublin,

Frankfurt, Paris and Amsterdam all likely to benefit.

Lending is likely to be more conservative and costs may rise, resulting in an even more pronounced two tier lending market favouring core opportunities. However pressure will remain for banks to lend, from central banks but also from owners. Banks will likely apply an additional risk premium in their spread when lending to non-core property.

A period of uncertainty with reduced liquidity will bring the stability of long-term equity and debt into greater focus. As banks reduce lending ratios and redirect funds to core properties, the opportunity that appears to elicit agreement amongst observers is for alternative lenders and equity investors to fill the funding gap left in the capital structure.

The mainstream residential sector should continue to offer attractive price growth, as the population continues to grow, regardless of migration and regulatory supply constraints which remain unaddressed. The pause should provide opportunities to acquire development sites for residential projects at attractive land basis.

Furthermore, the residential market is benefitting from structural changes that have been accentuated by Brexit. Uncertainty is expected to impact the willingness to buy, resulting in a fall in transaction volumes. Demand should be pushed into the private rented sector which will increasingly become an attractive alternative for both buyers and institutional investors looking for current income as well as capital appreciation.

Investment in Europe is likely to focus on stabilised assets in core markets, potentially redirecting capital from higher-yielding secondary cities. Core markets may face higher demand across the board as uncertainty and quantitative easing drives buyers and pushes down prime yields.

As a result, pricing may become more attractive in higher growth secondary European markets, which in some cases are already trading above historical average spreads to primary markets, with top-line rent growth forecasted as well.

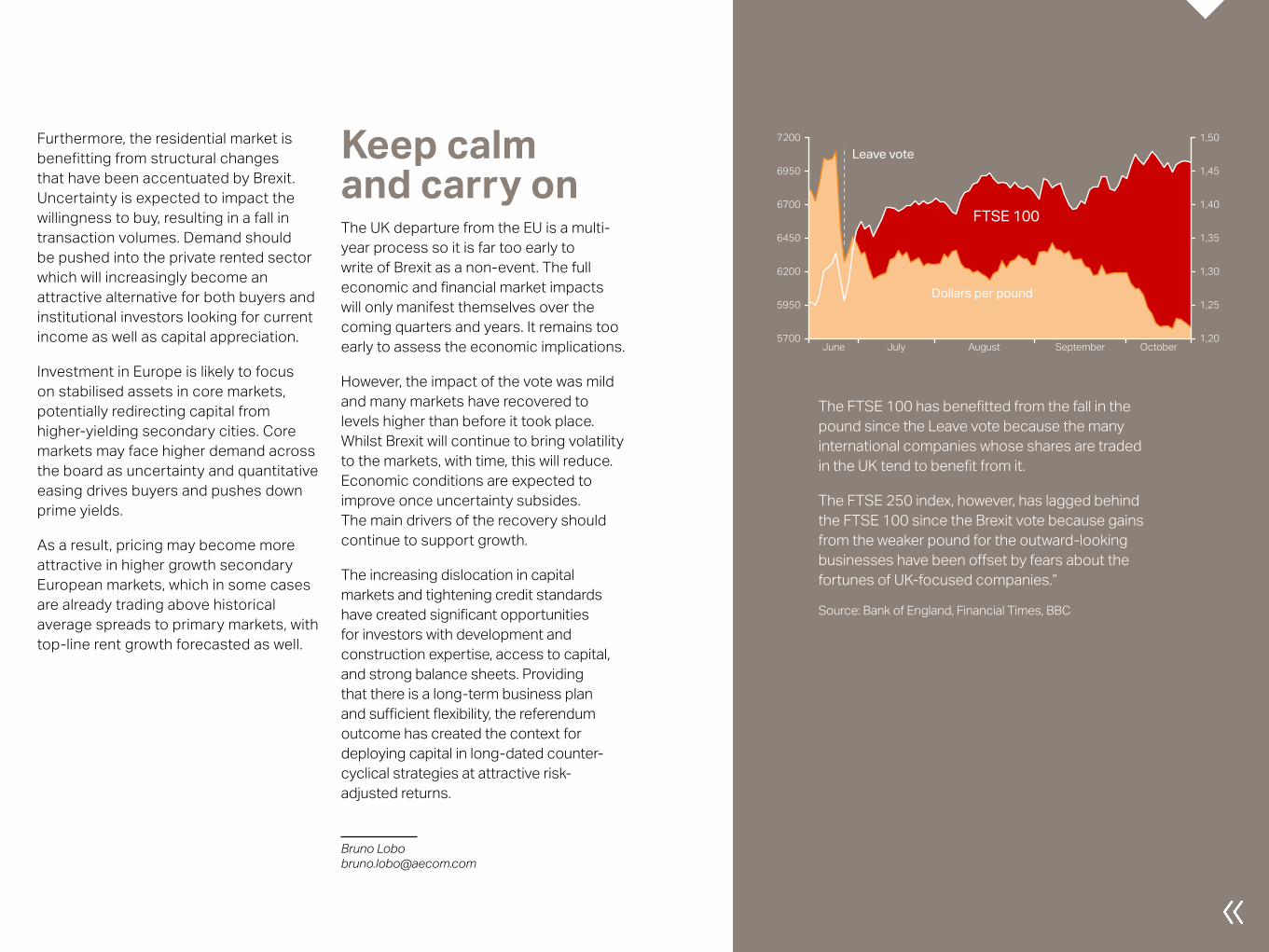

Keep calm and carry onThe UK departure from the EU is a multi-year process so it is far too early to write of Brexit as a non-event. The full economic and financial market impacts will only manifest themselves over the coming quarters and years. It remains too early to assess the economic implications.

However, the impact of the vote was mild and many markets have recovered to levels higher than before it took place. Whilst Brexit will continue to bring volatility to the markets, with time, this will reduce. Economic conditions are expected to improve once uncertainty subsides. The main drivers of the recovery should continue to support growth.

The increasing dislocation in capital markets and tightening credit standards have created significant opportunities for investors with development and construction expertise, access to capital, and strong balance sheets. Providing that there is a long-term business plan and sufficient flexibility, the referendum outcome has created the context for deploying capital in long-dated counter-cyclical strategies at attractive risk-adjusted returns.

Bruno Lobo [email protected]

1,20

1,25

1,30

1,35

1,40

1,45

1,50

Dollars per pound

OctoberAugust SeptemberJulyJune5700

5950

6200

6450

6700

6950

7200

FTSE 100

Leave vote

The FTSE 100 has benefitted from the fall in the pound since the Leave vote because the many international companies whose shares are traded in the UK tend to benefit from it.

The FTSE 250 index, however, has lagged behind the FTSE 100 since the Brexit vote because gains from the weaker pound for the outward-looking businesses have been offset by fears about the fortunes of UK-focused companies.”

Source: Bank of England, Financial Times, BBC

ContactContact us at [email protected]

The contents of Cornerstone are for general information. The opinions expressed in this publication do not necessarily reflect those of the editorial board, do not constitute advice and should not be relied upon in making (or refraining from making) any decision. The information contained within is provided on an “AS IS” basis, and all warranties, expressed or implied of any kind, regarding any matter pertaining to any information, advice or replies are disclaimed and excluded. Cornerstone, AECOM and its associates shall not be liable, at any time, for damages (including, without limitation, damages for loss of any kind) arising in contract, tort or otherwise from the Cornerstone contents, or from any action taken (or refrained from being taken) as a result of using the Cornerstone contents. ©2016 AECOM

About AECOMAECOM is built to deliver a better world. We design, build, finance and operate infrastructure assets for governments, businesses and organisations in more than 150 countries. As a fully integrated firm, we connect knowledge and experience across our global network of experts to help clients solve their most complex challenges. From high-performance buildings and infrastructure, to resilient communities and environments, to stable and secure nations, our work is transformative, differentiated and vital. A Fortune 500 firm, AECOM companies have annual revenue of approximately US$18 billion. See how we deliver what others can only imagine at aecom.com and @AECOM.

aecom.com