9M2014 FINANCIAL RESULTS

16

9M2014 RESULTS PRESENTATION 9 December, 2014

-

Upload

mechel- -

Category

Economy & Finance

-

view

4.620 -

download

0

Transcript of 9M2014 FINANCIAL RESULTS

9M2014 RESULTS PRESENTATION 9 December, 2014

DISCLAIMER

This presentation does not constitute or form part of and should not be construed as,

an offer to sell or issue or the solicitation of an offer to buy or acquire securities of

Mechel OAO (Mechel) or any of its subsidiaries in any jurisdiction or an inducement to

enter into investment activity. No part of this presentation, nor the fact of its

distribution, should form the basis of, or be relied on in connection with, any contract

or commitment or investment decision whatsoever. Any purchase of securities should

be made solely on the basis of information Mechel files from time to time with the U.S.

Securities and Exchange Commission. No representation, warranty or undertaking,

express or implied, is made as to, and no reliance should be placed on, the fairness,

accuracy, completeness or correctness of the information or the opinions contained

herein. None of the Mechel or any of its affiliates, advisors or representatives shall

have any liability whatsoever (in negligence or otherwise) for any loss howsoever

arising from any use of this presentation or its contents or otherwise arising in

connection with the presentation.

This presentation may contain projections or other forward-looking statements

regarding future events or the future financial performance of Mechel, as defined in

the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995.

We wish to caution you that these statements are only predictions and that actual

events or results may differ materially. We do not intend to update these statements.

We refer you to the documents Mechel files from time to time with the U.S. Securities

and Exchange Commission, including our Form 20-F. These documents contain and

identify important factors, including those contained in the section captioned “Risk

Factors” and “Cautionary Note Regarding Forward-Looking Statements” in our Form

20-F, that could cause the actual results to differ materially from those contained in

our projections or forward-looking statements, including, among others, the

achievement of anticipated levels of profitability, growth, cost and synergy of our

recent acquisitions, the impact of competitive pricing, the ability to obtain necessary

regulatory approvals and licenses, the impact of developments in the Russian

economic, political and legal environment, volatility in stock markets or in the price of

our shares or ADRs, financial risk management and the impact of general business

and global economic conditions.

The information and opinions contained in this document are provided as at the date

of this presentation and are subject to change without notice

2

FINANCIAL HIGHLIGHTS

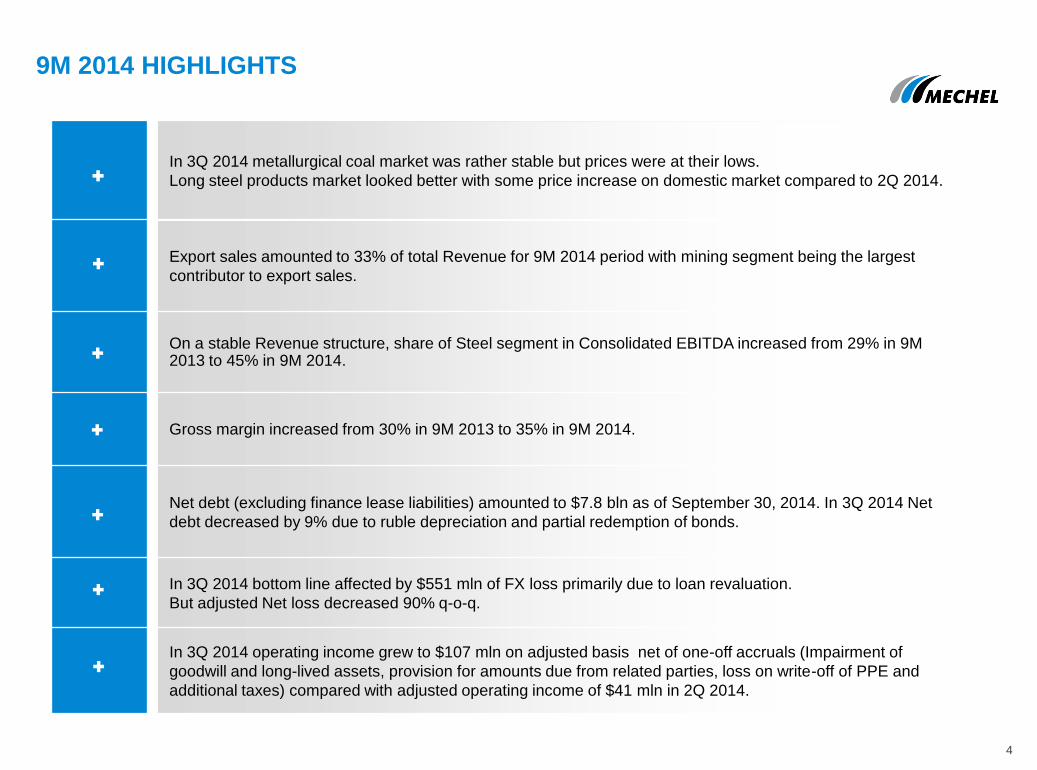

9M 2014 HIGHLIGHTS

4

In 3Q 2014 metallurgical coal market was rather stable but prices were at their lows.

Long steel products market looked better with some price increase on domestic market compared to 2Q 2014.

Export sales amounted to 33% of total Revenue for 9M 2014 period with mining segment being the largest

contributor to export sales.

On a stable Revenue structure, share of Steel segment in Consolidated EBITDA increased from 29% in 9M 2013 to 45% in 9M 2014.

Gross margin increased from 30% in 9M 2013 to 35% in 9M 2014.

Net debt (excluding finance lease liabilities) amounted to $7.8 bln as of September 30, 2014. In 3Q 2014 Net

debt decreased by 9% due to ruble depreciation and partial redemption of bonds.

In 3Q 2014 bottom line affected by $551 mln of FX loss primarily due to loan revaluation.

But adjusted Net loss decreased 90% q-o-q.

In 3Q 2014 operating income grew to $107 mln on adjusted basis net of one-off accruals (Impairment of

goodwill and long-lived assets, provision for amounts due from related parties, loss on write-off of PPE and

additional taxes) compared with adjusted operating income of $41 mln in 2Q 2014.

148

49

-4

193

83

34

11

121

63

-3

18

79 89

77

3

171

80

138

-7

219

Mining Steel Power Consolidated

3Q13 4Q13 1Q14 2Q14 3Q14

69

5

12

51

14

9

20

95

62

6

11

17

20

9

19

53

57

1

92

9

20

0

17

00

55

1

10

27

16

6

17

44

49

2

94

8

14

8

15

88

Mining Steel Power Consolidated

3Q13 4Q13 1Q14 2Q14 3Q14

10%

32% 58%

8%

32%

60%

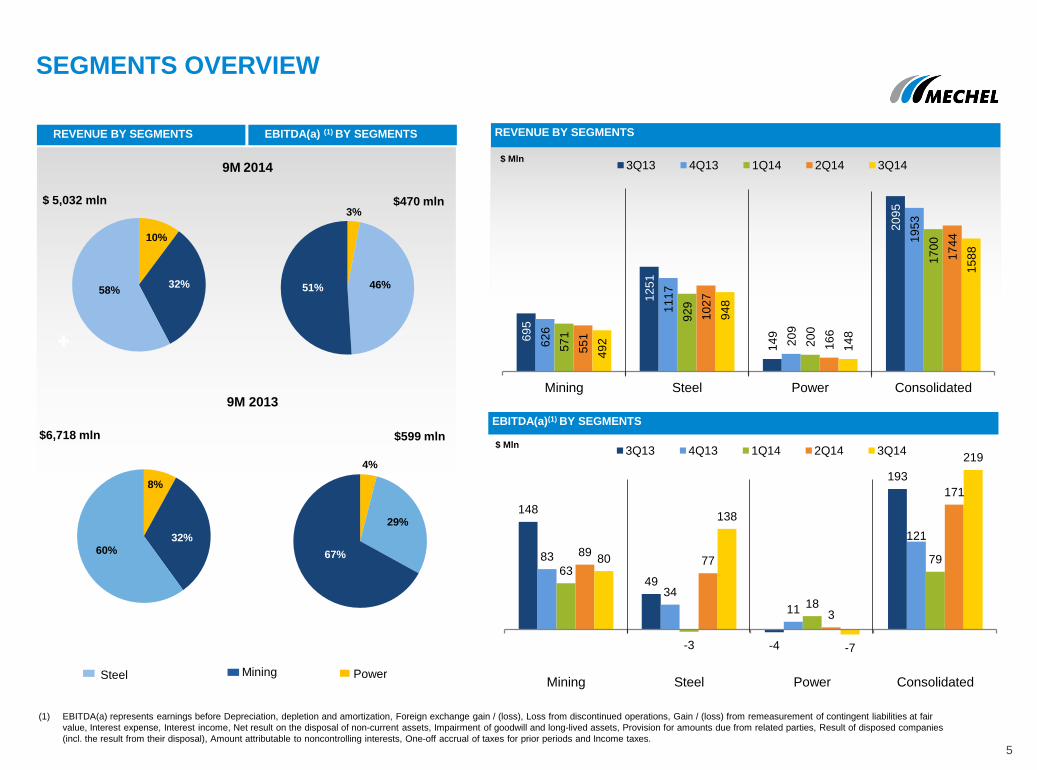

SEGMENTS OVERVIEW

REVENUE BY SEGMENTS

$ Mln

(1) EBITDA(a) represents earnings before Depreciation, depletion and amortization, Foreign exchange gain / (loss), Loss from discontinued operations, Gain / (loss) from remeasurement of contingent liabilities at fair

value, Interest expense, Interest income, Net result on the disposal of non-current assets, Impairment of goodwill and long-lived assets, Provision for amounts due from related parties, Result of disposed companies

(incl. the result from their disposal), Amount attributable to noncontrolling interests, One-off accrual of taxes for prior periods and Income taxes.

5

Steel Mining Power

EBITDA(a)(1) BY SEGMENTS

3%

46% 51%

9M 2014

4%

29%

67%

9M 2013

REVENUE BY SEGMENTS

$ Mln

EBITDA(a) (1) BY SEGMENTS

$ 5,032 mln $470 mln

$6,718 mln $599 mln

MINING SEGMENT

6

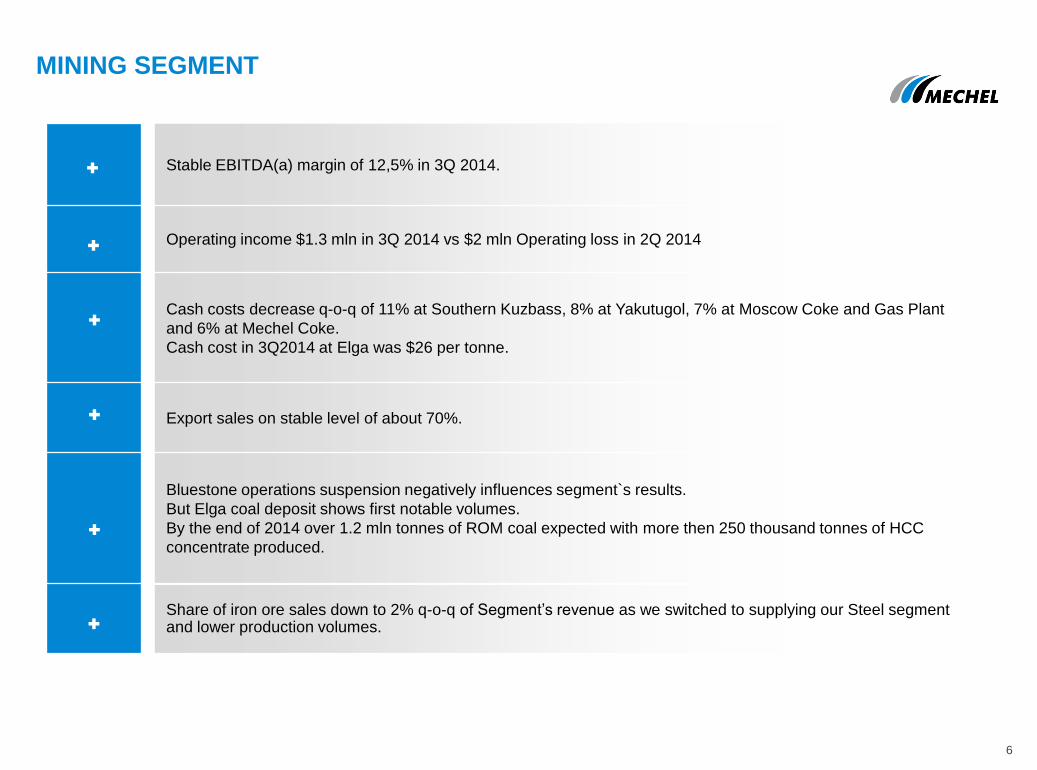

Stable EBITDA(a) margin of 12,5% in 3Q 2014.

Operating income $1.3 mln in 3Q 2014 vs $2 mln Operating loss in 2Q 2014

Cash costs decrease q-o-q of 11% at Southern Kuzbass, 8% at Yakutugol, 7% at Moscow Coke and Gas Plant

and 6% at Mechel Coke.

Cash cost in 3Q2014 at Elga was $26 per tonne.

Export sales on stable level of about 70%.

Bluestone operations suspension negatively influences segment`s results.

But Elga coal deposit shows first notable volumes.

By the end of 2014 over 1.2 mln tonnes of ROM coal expected with more then 250 thousand tonnes of HCC

concentrate produced.

Share of iron ore sales down to 2% q-o-q of Segment’s revenue as we switched to supplying our Steel segment and lower production volumes.

43%

23%

10%

16%

8%

9M2013 9M2014

Other

Depreciation and depletion

Energy

Staff costs

Raw materials and purchased goods

42%

26%

10%

16%

6%

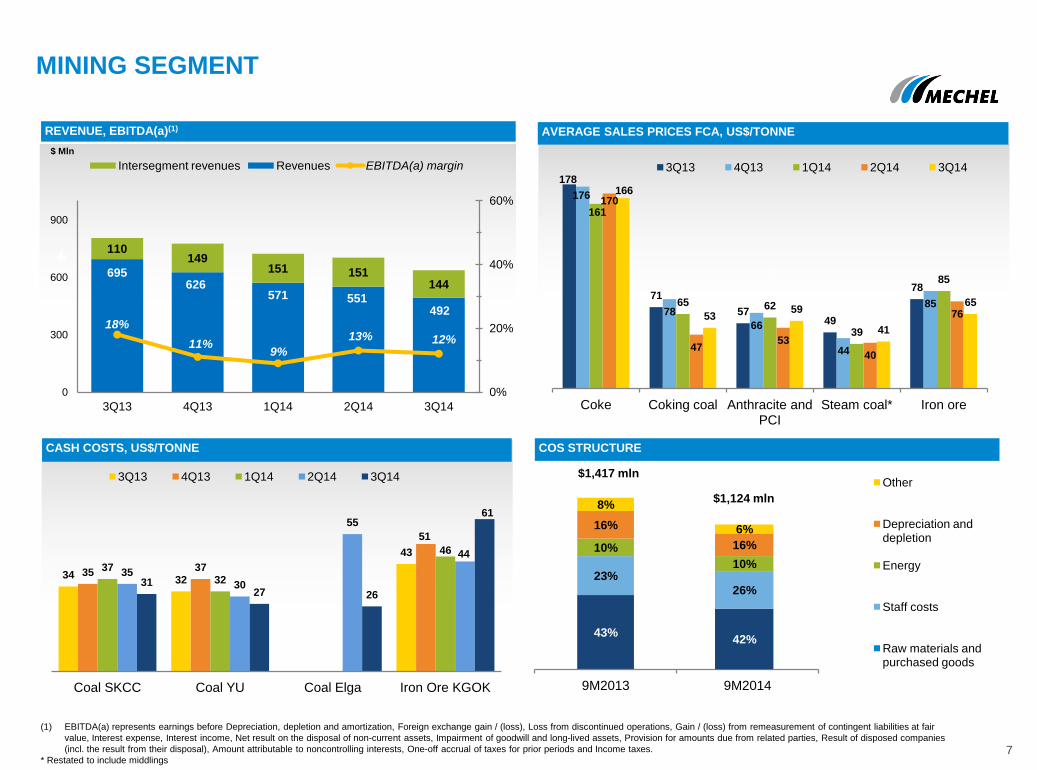

34 32

43

35 37

51

37 32

46

35 30

55

44

31 27 26

61

Coal SKCC Coal YU Coal Elga Iron Ore KGOK

3Q13 4Q13 1Q14 2Q14 3Q14

695 626

571 551 492

110 149

151 151 144

18%

11% 9%

13% 12%

0%

20%

40%

60%

0

300

600

900

3Q13 4Q13 1Q14 2Q14 3Q14

Intersegment revenues Revenues EBITDA(a) margin

0.

MINING SEGMENT

CASH COSTS, US$/TONNE

7

REVENUE, EBITDA(a)(1)

(1) EBITDA(a) represents earnings before Depreciation, depletion and amortization, Foreign exchange gain / (loss), Loss from discontinued operations, Gain / (loss) from remeasurement of contingent liabilities at fair

value, Interest expense, Interest income, Net result on the disposal of non-current assets, Impairment of goodwill and long-lived assets, Provision for amounts due from related parties, Result of disposed companies

(incl. the result from their disposal), Amount attributable to noncontrolling interests, One-off accrual of taxes for prior periods and Income taxes.

* Restated to include middlings

AVERAGE SALES PRICES FCA, US$/TONNE

COS STRUCTURE

$1,417 mln

$1,124 mln

178

71

57 49

78

176

78

66

44

85

161

65 62

39

85

170

47 53

40

76

166

53 59

41

65

Coke Coking coal Anthracite and PCI

Steam coal* Iron ore

3Q13 4Q13 1Q14 2Q14 3Q14

$ Mln

Coking coal 40%

Anthracites and PCI 28%

Coke 10%

Coking products

3%

Steam coal 11%

Iron ore 6%

Other 2%

Coking coal 39%

Anthracites and PCI

25%

Coke 8%

Coking products

2%

Steam coal 8%

Iron ore 16%

Other 2%

China 39%

Russia 28%

Europe 14%

Asia w/o China 10%

CIS 2%

Middle East 3%

USA 2%

Other 2%

MINING SEGMENT

8

REVENUE BREAKDOWN BY REGION

REVENUE BREAKDOWN BY PRODUCTS

9M 2013 9M 2014

9M 2013 9M 2014

China 36%

Russia 29%

Europe 15%

Asia w/o China 14%

CIS 3%

Middle East 3%

USA 0,15%

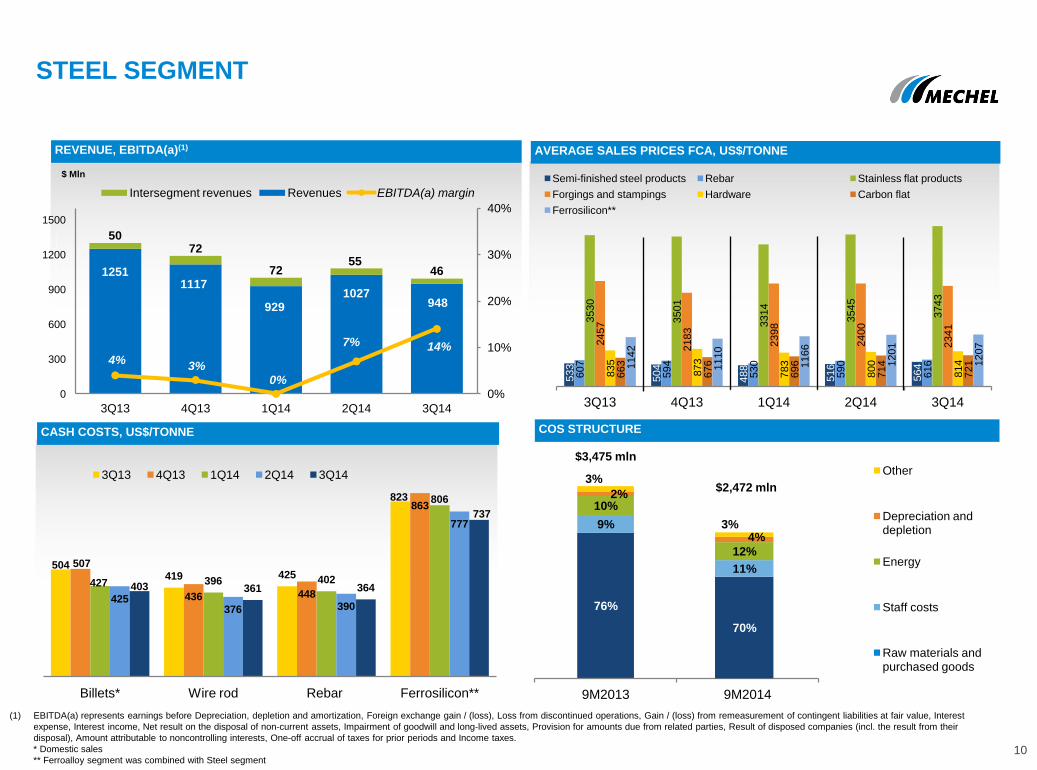

STEEL SEGMENT

9

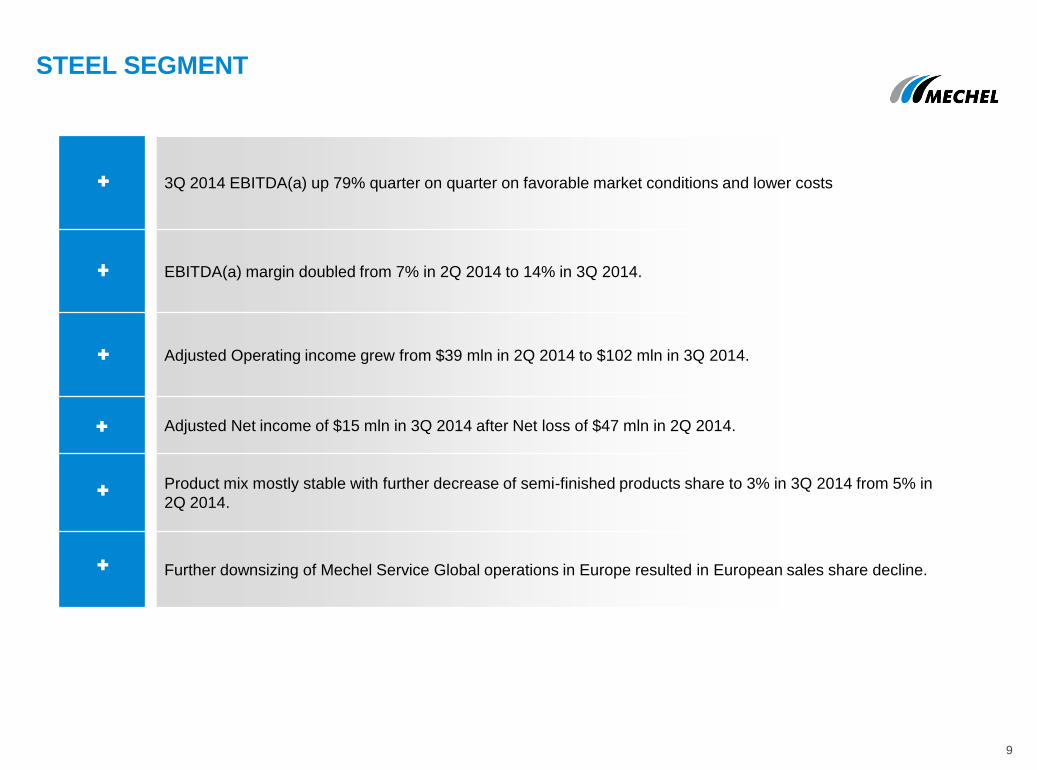

3Q 2014 EBITDA(a) up 79% quarter on quarter on favorable market conditions and lower costs

EBITDA(a) margin doubled from 7% in 2Q 2014 to 14% in 3Q 2014.

Adjusted Operating income grew from $39 mln in 2Q 2014 to $102 mln in 3Q 2014.

Adjusted Net income of $15 mln in 3Q 2014 after Net loss of $47 mln in 2Q 2014.

Product mix mostly stable with further decrease of semi-finished products share to 3% in 3Q 2014 from 5% in

2Q 2014.

Further downsizing of Mechel Service Global operations in Europe resulted in European sales share decline.

504 419 425

823

507

436 448

863

427 396 402

806

425 376 390

777

403 361 364

737

Billets* Wire rod Rebar Ferrosilicon**

3Q13 4Q13 1Q14 2Q14 3Q14

1251 1117

929 1027

948

50 72

72 55

46

4% 3%

0%

7% 14%

0%

10%

20%

30%

40%

0

300

600

900

1200

1500

3Q13 4Q13 1Q14 2Q14 3Q14

Intersegment revenues Revenues EBITDA(a) margin

533

504

488

516

564

607

594

530

590

616

3530

3501

3314

3545

3743

2457

2183

2398

2400

2341

835

873

783

800

814

663

676

696

714

721

1142

1110

1166

1201

1207

3Q13 4Q13 1Q14 2Q14 3Q14

Semi-finished steel products Rebar Stainless flat products

Forgings and stampings Hardware Carbon flat

Ferrosilicon**

76%

9%

10% 2%

3%

9M2013 9M2014

Other

Depreciation and depletion

Energy

Staff costs

Raw materials and purchased goods

70%

11%

12%

4% 3%

STEEL SEGMENT

10

CASH COSTS, US$/TONNE

REVENUE, EBITDA(a)(1)

$ Mln

(1) EBITDA(a) represents earnings before Depreciation, depletion and amortization, Foreign exchange gain / (loss), Loss from discontinued operations, Gain / (loss) from remeasurement of contingent liabilities at fair value, Interest

expense, Interest income, Net result on the disposal of non-current assets, Impairment of goodwill and long-lived assets, Provision for amounts due from related parties, Result of disposed companies (incl. the result from their

disposal), Amount attributable to noncontrolling interests, One-off accrual of taxes for prior periods and Income taxes.

* Domestic sales

** Ferroalloy segment was combined with Steel segment

AVERAGE SALES PRICES FCA, US$/TONNE

COS STRUCTURE

$3,475 mln

$2,472 mln

Semi-Finished Steel Products

5%

Rebar 29%

Stainless flat 2%

Carbon long products

19%

Forgings and stampings

9%

Hardware 16%

Carbon flat 8%

Ferrosilicon 2%

Other 10%

Semi-

Finished Steel

Products 11%

Rebar 28%

Stainless flat 3%

Carbon long

products 16%

Forgings and

stampings 8%

Hardware 15%

Carbon flat 8%

Ferrosilicon 1%

Other 10%

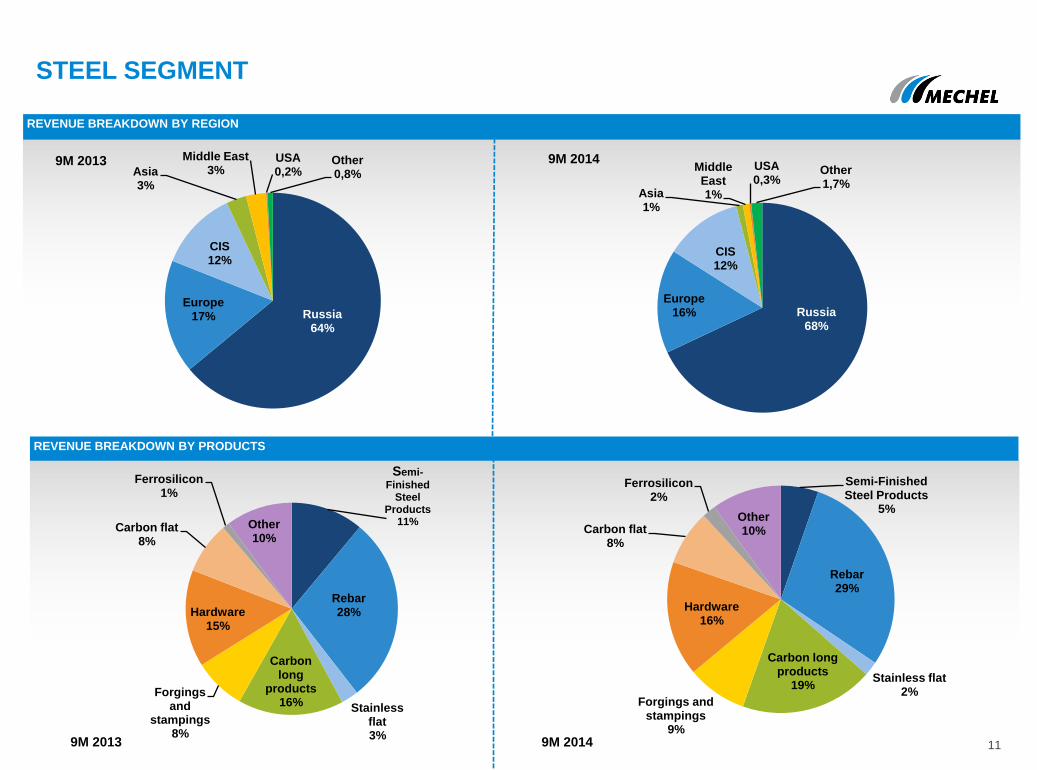

Russia 64%

Europe 17%

CIS 12%

Asia 3%

Middle East 3%

USA 0,2%

Other 0,8%

Russia 68%

Europe 16%

CIS 12%

Asia 1%

Middle East 1%

USA 0,3%

Other 1,7%

STEEL SEGMENT

11

REVENUE BREAKDOWN BY REGION

REVENUE BREAKDOWN BY PRODUCTS

9M 2014 9M 2013

9M 2014 9M 2013

87%

4%

7%

1% 1%

9M2013 9M2014

Other

Depreciation and depletion

Energy

Staff costs

Raw materials and purchased goods

89%

4%

5%

1% 1%

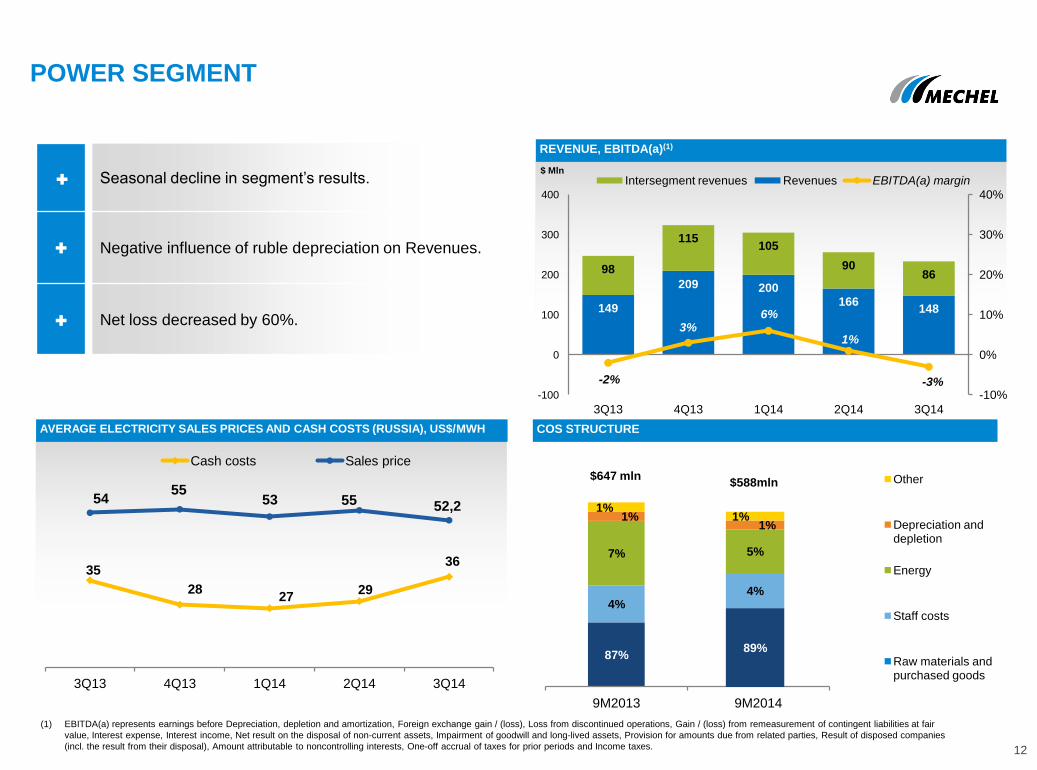

POWER SEGMENT

12

AVERAGE ELECTRICITY SALES PRICES AND CASH COSTS (RUSSIA), US$/MWH

REVENUE, EBITDA(a)(1)

$ Mln

(1) EBITDA(a) represents earnings before Depreciation, depletion and amortization, Foreign exchange gain / (loss), Loss from discontinued operations, Gain / (loss) from remeasurement of contingent liabilities at fair

value, Interest expense, Interest income, Net result on the disposal of non-current assets, Impairment of goodwill and long-lived assets, Provision for amounts due from related parties, Result of disposed companies

(incl. the result from their disposal), Amount attributable to noncontrolling interests, One-off accrual of taxes for prior periods and Income taxes.

COS STRUCTURE

$647 mln $588mln

Seasonal decline in segment’s results.

Negative influence of ruble depreciation on Revenues.

Net loss decreased by 60%. 149

209 200 166

148

98

115 105

90 86

-2%

3% 6%

1%

-3% -10%

0%

10%

20%

30%

40%

-100

0

100

200

300

400

3Q13 4Q13 1Q14 2Q14 3Q14

Intersegment revenues Revenues EBITDA(a) margin

35

28 27

29

36

54 55

53 55 52,2

3Q13 4Q13 1Q14 2Q14 3Q14

Cash costs Sales price

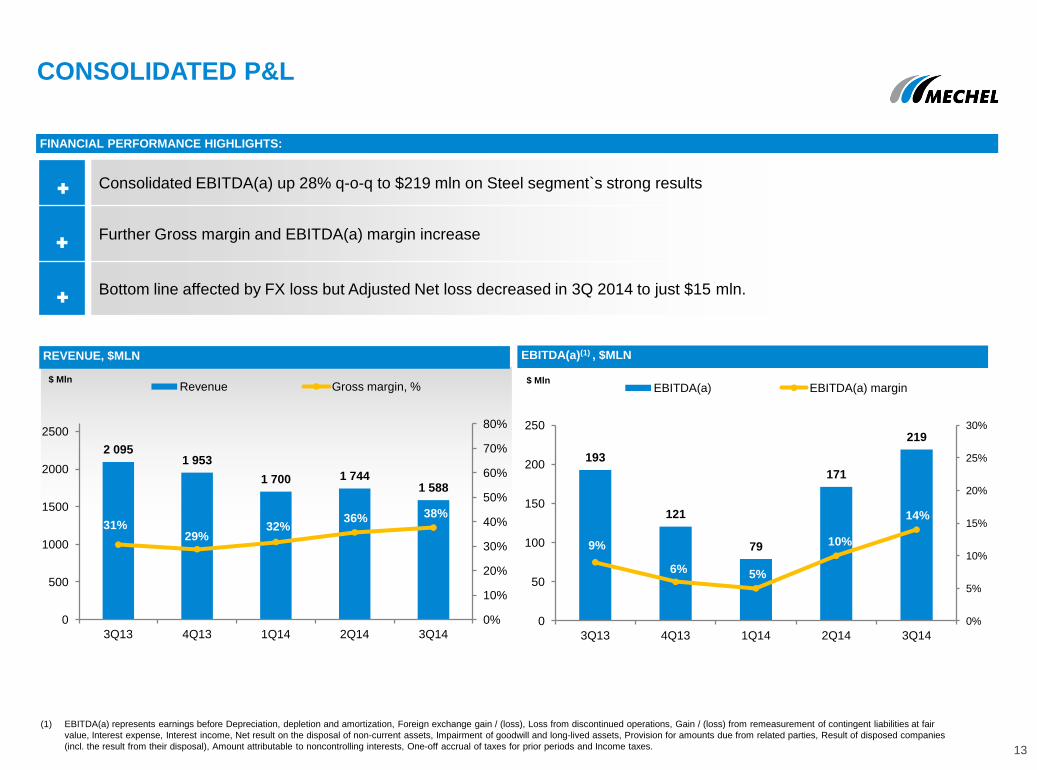

CONSOLIDATED P&L

13

REVENUE, $MLN

FINANCIAL PERFORMANCE HIGHLIGHTS:

$ Mln $ Mln

(1) EBITDA(a) represents earnings before Depreciation, depletion and amortization, Foreign exchange gain / (loss), Loss from discontinued operations, Gain / (loss) from remeasurement of contingent liabilities at fair

value, Interest expense, Interest income, Net result on the disposal of non-current assets, Impairment of goodwill and long-lived assets, Provision for amounts due from related parties, Result of disposed companies

(incl. the result from their disposal), Amount attributable to noncontrolling interests, One-off accrual of taxes for prior periods and Income taxes.

Consolidated EBITDA(a) up 28% q-o-q to $219 mln on Steel segment`s strong results

Further Gross margin and EBITDA(a) margin increase

Bottom line affected by FX loss but Adjusted Net loss decreased in 3Q 2014 to just $15 mln.

2 095 1 953

1 700 1 744 1 588

31% 29%

32% 36% 38%

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

500

1000

1500

2000

2500

3Q13 4Q13 1Q14 2Q14 3Q14

Revenue Gross margin, %

193

121

79

171

219

9%

6% 5%

10%

14%

0%

5%

10%

15%

20%

25%

30%

0

50

100

150

200

250

3Q13 4Q13 1Q14 2Q14 3Q14

EBITDA(a) EBITDA(a) margin

EBITDA(a)(1) , $MLN

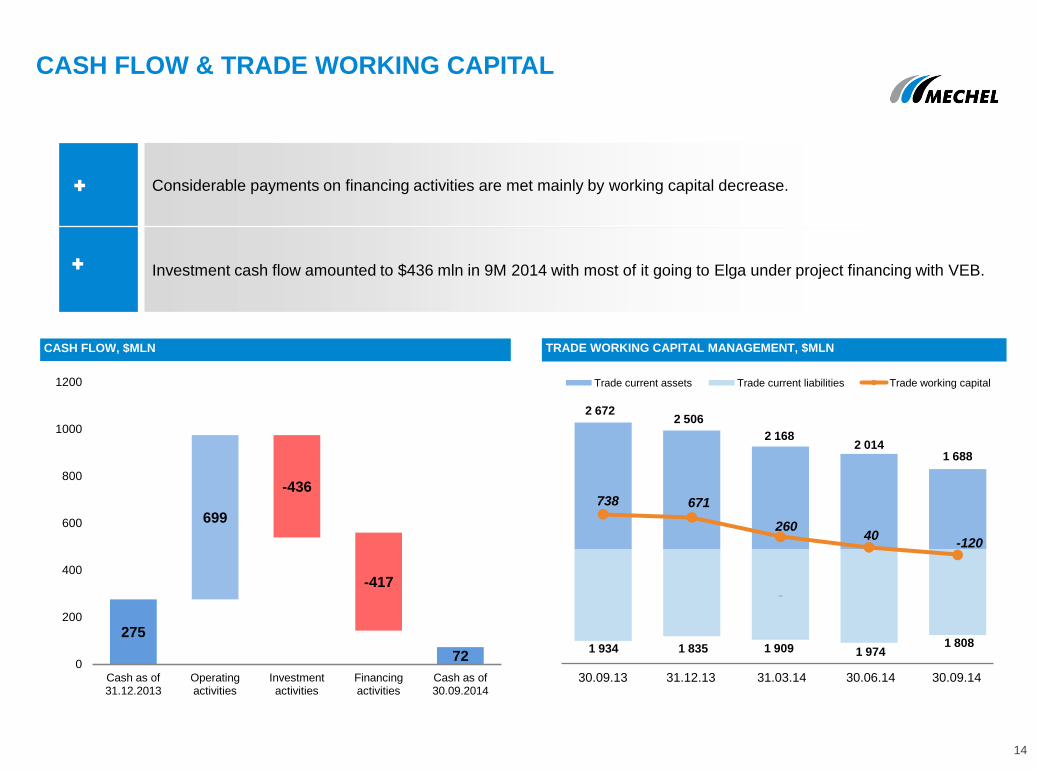

CASH FLOW & TRADE WORKING CAPITAL

14

CASH FLOW, $MLN

Considerable payments on financing activities are met mainly by working capital decrease.

Investment cash flow amounted to $436 mln in 9M 2014 with most of it going to Elga under project financing with VEB.

TRADE WORKING CAPITAL MANAGEMENT, $MLN

275

72

699

-436

-417

0

200

400

600

800

1000

1200

Cash as of 31.12.2013

Operating activities

Investment activities

Financing activities

Cash as of 30.09.2014

738 671

260 40

-120

Trade current assets Trade current liabilities Trade working capital

1 934 1 835 1 909 1 974 1 808

2 672 2 506

2 168 2 014

1 688

30.09.13 31.12.13 31.03.14 30.06.14 30.09.14

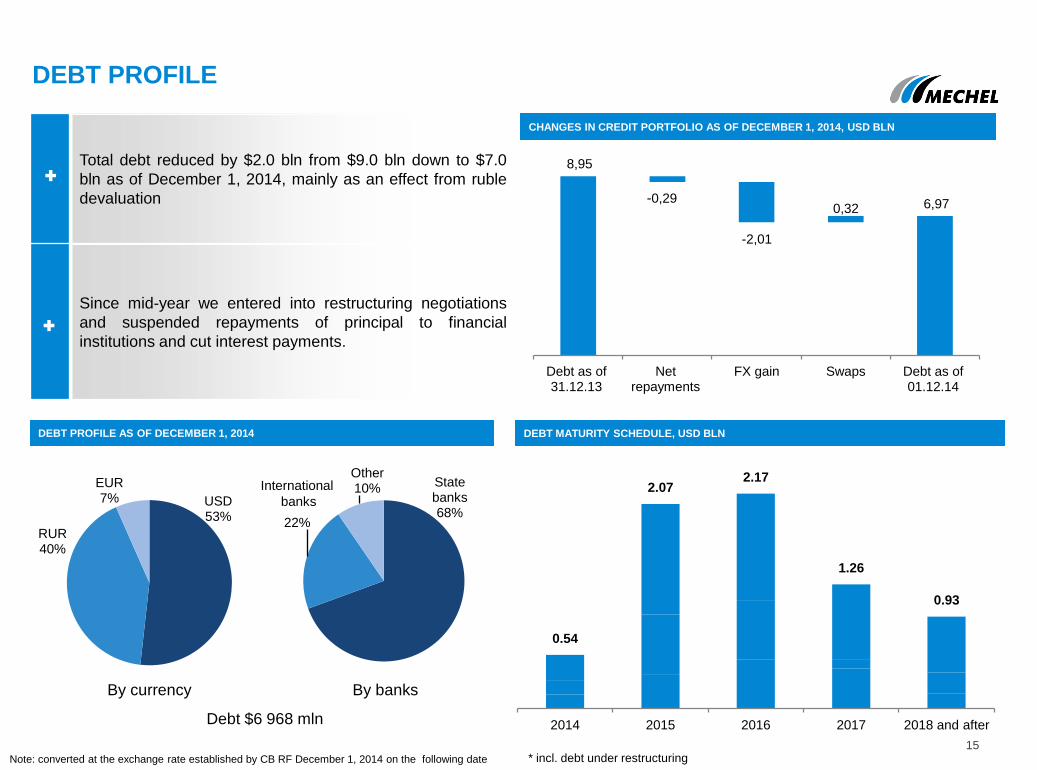

State banks 68%

22%

Other 10% International

banks

Total debt reduced by $2.0 bln from $9.0 bln down to $7.0

bln as of December 1, 2014, mainly as an effect from ruble

devaluation

Since mid-year we entered into restructuring negotiations

and suspended repayments of principal to financial

institutions and cut interest payments.

DEBT PROFILE

DEBT MATURITY SCHEDULE, USD BLN

CHANGES IN CREDIT PORTFOLIO AS OF DECEMBER 1, 2014, USD BLN

DEBT PROFILE AS OF DECEMBER 1, 2014

By currency By banks

15

0.54

2.07 2.17

1.26

0.93

2014 2015 2016 2017 2018 and after

* incl. debt under restructuring

Debt $6 968 mln

Note: converted at the exchange rate established by CB RF December 1, 2014 on the following date

8,95

0,29

2,01

0,32 6,97

Debt as of 31.12.13

Net repayments

FX gain Swaps Debt as of 01.12.14

-0,29

-2,01

USD 53%

RUR 40%

EUR 7%

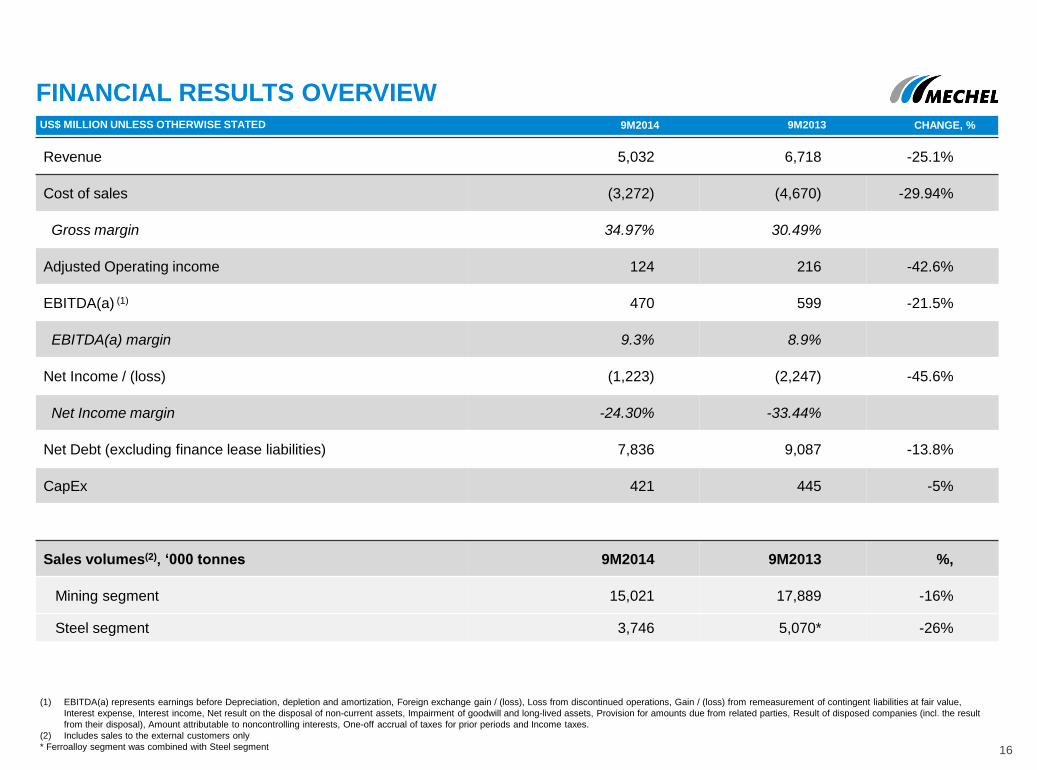

Revenue 5,032 6,718 -25.1%

Cost of sales (3,272) (4,670) -29.94%

Gross margin 34.97% 30.49%

Adjusted Operating income 124 216 -42.6%

EBITDA(a) (1) 470 599 -21.5%

EBITDA(a) margin 9.3% 8.9%

Net Income / (loss) (1,223) (2,247) -45.6%

Net Income margin -24.30% -33.44%

Net Debt (excluding finance lease liabilities) 7,836 9,087 -13.8%

CapEx 421 445 -5%

Sales volumes(2), ‘000 tonnes 9M2014 9M2013 %,

Mining segment 15,021 17,889 -16%

Steel segment 3,746 5,070* -26%

FINANCIAL RESULTS OVERVIEW

(1) EBITDA(a) represents earnings before Depreciation, depletion and amortization, Foreign exchange gain / (loss), Loss from discontinued operations, Gain / (loss) from remeasurement of contingent liabilities at fair value,

Interest expense, Interest income, Net result on the disposal of non-current assets, Impairment of goodwill and long-lived assets, Provision for amounts due from related parties, Result of disposed companies (incl. the result

from their disposal), Amount attributable to noncontrolling interests, One-off accrual of taxes for prior periods and Income taxes.

(2) Includes sales to the external customers only

* Ferroalloy segment was combined with Steel segment

US$ MILLION UNLESS OTHERWISE STATED 9M2014 9M2013 CHANGE, %

16