1 Ulrich Hege · Argentum Conference · September 5, 2012 Challenges for Private Equity From An...

27

1 Ulrich Hege · Argentum Conference · September 5, 2012 Challenges for Private Equity From An Academic Viewpoint Ulrich Hege - HEC Paris The Argentum Conference “Value of Private Equity” Bergen - September 5, 2012

-

Upload

joseph-merritt -

Category

Documents

-

view

217 -

download

0

Transcript of 1 Ulrich Hege · Argentum Conference · September 5, 2012 Challenges for Private Equity From An...

1 Ulrich Hege · Argentum Conference · September 5, 2012

Challenges for Private Equity From An Academic Viewpoint

Ulrich Hege - HEC Paris

The Argentum Conference “Value of Private Equity”

Bergen - September 5, 2012

2 Ulrich Hege · Argentum Conference · September 5, 2012

Academic research looks backwards. But in difficult times, searching in history can offer comfort

Disclaimer

3 Ulrich Hege · Argentum Conference · September 5, 2012

Reputation inside the industry: how important is it in private equity?

How credible is the private equity model for investors

portfolio companies and their stakeholders

public opinion, policy-makers and in the reshaping of the financial industry?

Reputation and Credibility

4 Ulrich Hege · Argentum Conference · September 5, 2012

I. Reputation: Experience and Risk-Taking

II. Credibility: Economic Effects

III. Credibility: Investor Relations

IV. Systemic Risk and Leverage in a Post-Crisis World

V. Transparency

VI. Conclusion

Overview

5 Ulrich Hege · Argentum Conference · September 5, 2012

I:Reputation:

Experience and Risk-Taking

6 Ulrich Hege · Argentum Conference · September 5, 2012

Reputation of PE funds prominent in academic research. Distinction between high- and low-reputation funds Quantitative measures of reputation by AUM, league

tables, past performance, age

Distinction between experienced and novice funds

Reputation-building is slow: fully established only after the third fund (Giot, Hege, Schwienbahcer, 2012)

Reputation: Experience

7 Ulrich Hege · Argentum Conference · September 5, 2012

Yes, experienced and novice funds invest differently: novice funds make larger investments they tend to invest at a slower pace they are less able to pick industries and timing

(Gompers, Kovner, Lerner, Scharfstein, 2008) they tend to pick up SBOs(Bonnini

High-reputation funds have access to better deal flow, e.g. to syndicated deals (Ljungqvist, Hochberg, Lu, 2007; 2010)

Evidence for performance persistence of top-quantile funds (Kaplan and Schoar, 2005; Phalippou and Gottschalg, 2009)

Does Reputation Matter?

8 Ulrich Hege · Argentum Conference · September 5, 2012

Regulators seem concerned and incentive effects like carry and clawbacks.

Giot, Hege and Schwienbacher (2012) use variation in implicit incentives: novice funds have a reputation to build (e.g. `grandstanding’; Gompers, 1996) and little to lose more prone to risk-taking

Findings: novice funds less diversified. But driven by access rather than risk-taking: they invest slowly, increase their pace, make large investment in VC not PE, underperform more with large investments

Probably an issue of lack of access to best (small) opportunities, not risk-shifting

Are PE Funds Risk-Takers?

9 Ulrich Hege · Argentum Conference · September 5, 2012

II:Credibility: Economic Effects

10 Ulrich Hege · Argentum Conference · September 5, 2012

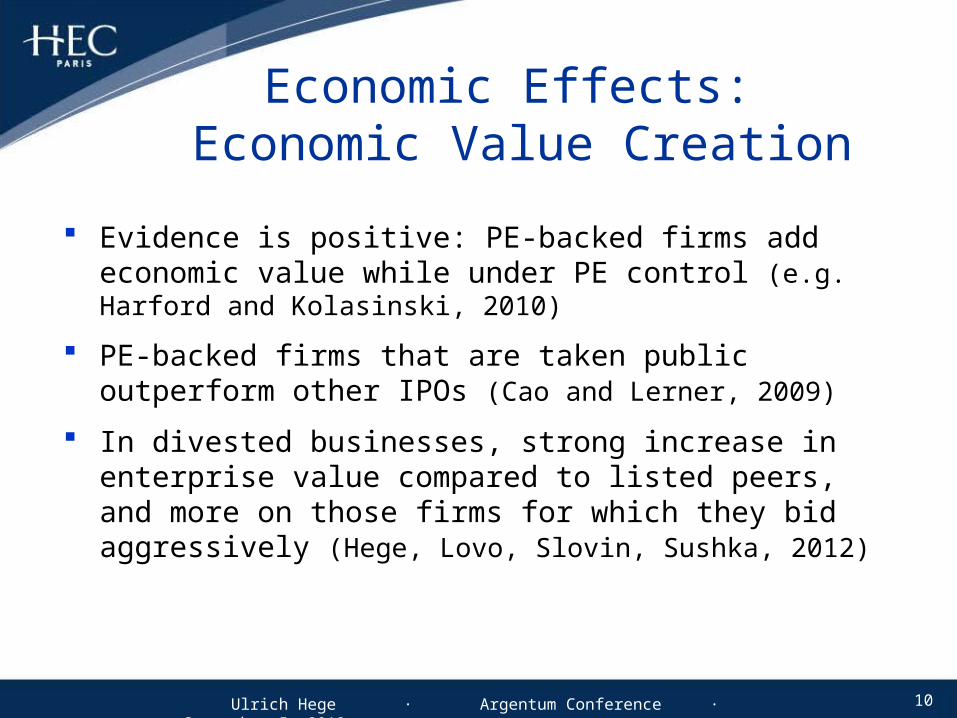

Evidence is positive: PE-backed firms add economic value while under PE control (e.g. Harford and Kolasinski, 2010)

PE-backed firms that are taken public outperform other IPOs (Cao and Lerner, 2009)

In divested businesses, strong increase in enterprise value compared to listed peers, and more on those firms for which they bid aggressively (Hege, Lovo, Slovin, Sushka, 2012)

Economic Effects: Economic Value Creation

11 Ulrich Hege · Argentum Conference · September 5, 2012

Evidence suggests positive effects on operating performance and investment

Private equity leads to higher investment and to growth in operating performance in USA (Kaplan, 1989; Lichtenberg and Siegel, 1990; Harris, Siegel, and Wright, 2005), but recent effect significantly weaker in p-to-p deals (Guo, Hotchkiss, and Song, 2011)

Positive investment effects in financially constrained small firms in France (Boucly, Sraer and Thesmar, 2011)

PE-backed firms invest in higher value R&D (Lerner, Sorensen, and Stromberg, 2011)

Economic Effects: Productivity and Investment

12 Ulrich Hege · Argentum Conference · September 5, 2012

In the US and UK, studies mostly show a decline in employment (e.g., Lichtenberg and Siegel, 1990; Arness and Wright, 2007)

Positive employment effects in France (Boucly, Sraer and Thesmar, 2011)

Creative job destruction: disaggregating by business units shows modest overall decline in US (1%); but large reductions in declining segments almost offset by increases in growth segments (sum 13%) (Davis, Haltiwanger, Jarmin, Lerner, Miranda, 2011)

Overall: the economic impact is overwhelmingly positive

Economic Effects: Employment

13 Ulrich Hege · Argentum Conference · September 5, 2012

III:Credibility: Investor Relations

14 Ulrich Hege · Argentum Conference · September 5, 2012

LP Returns and Conflicts of Interest

Overall performance probably disappointing for investors (Phalippou and Gottschalg, 2009)

Academic research showing outperformance for LPs suffers from selection bias (or suspicion thereof) (Harris, Kaplan, Jenkinson, 2011; Robinson and Sensoy, 2012)

Surprising homogeneity in fund compensation terms, hard to rationalize (Metrick and Yasuda, 2010; Robinson and Sensoy, 2011)

Clawbacks lead to perverse incentive effects Half of LPs say they have zombie funds in portfolio

(Coller Capital survey, 2012) transaction fees and conflicts of interest

15 Ulrich Hege · Argentum Conference · September 5, 2012

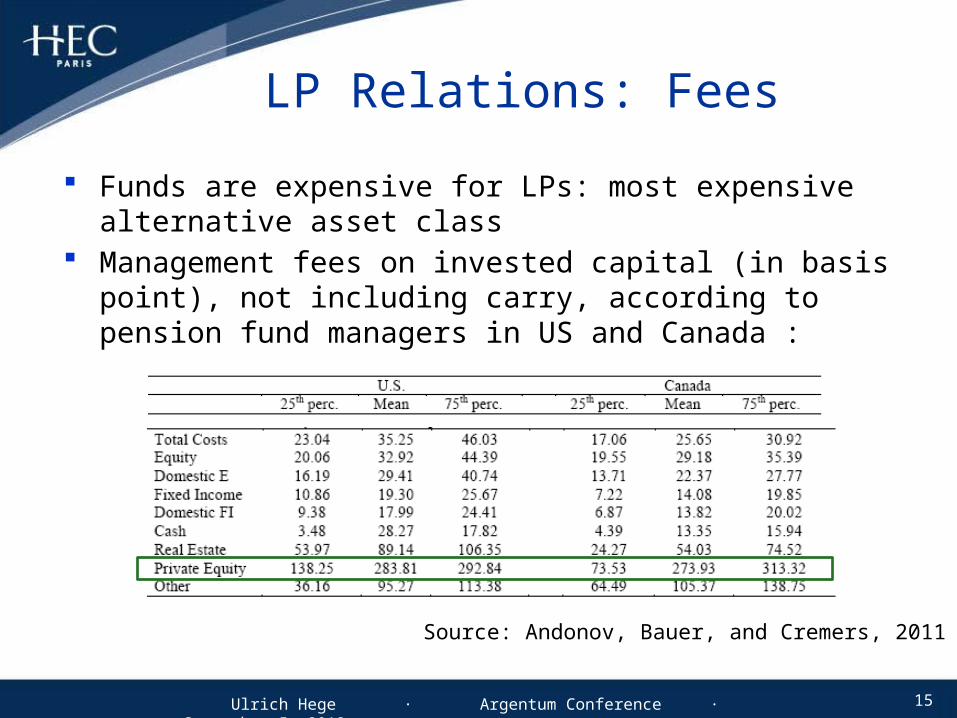

Funds are expensive for LPs: most expensive alternative asset class

Management fees on invested capital (in basis point), not including carry, according to pension fund managers in US and Canada :

LP Relations: Fees

Source: Andonov, Bauer, and Cremers, 2011

16 Ulrich Hege · Argentum Conference · September 5, 2012

IV:Systemic Risk and Leverage

in a Post-Crisis World

17 Ulrich Hege · Argentum Conference · September 5, 2012

Research shows that the use of LBO leverage is opportunistic: e.g., it changes dramatically with the credit spread (Axelson, Jenkinson, Strömberg, Weisbach, 2011)

Buyout boom until 2007 fuelled by mispriced debt, largely driven by securitization and thriving on opacity

Sudden halt in the securitization machinery in 2007/2008, and a drastic repricing of risky LBO debt

Boom and Bust in LBO Debt

18 Ulrich Hege · Argentum Conference · September 5, 2012

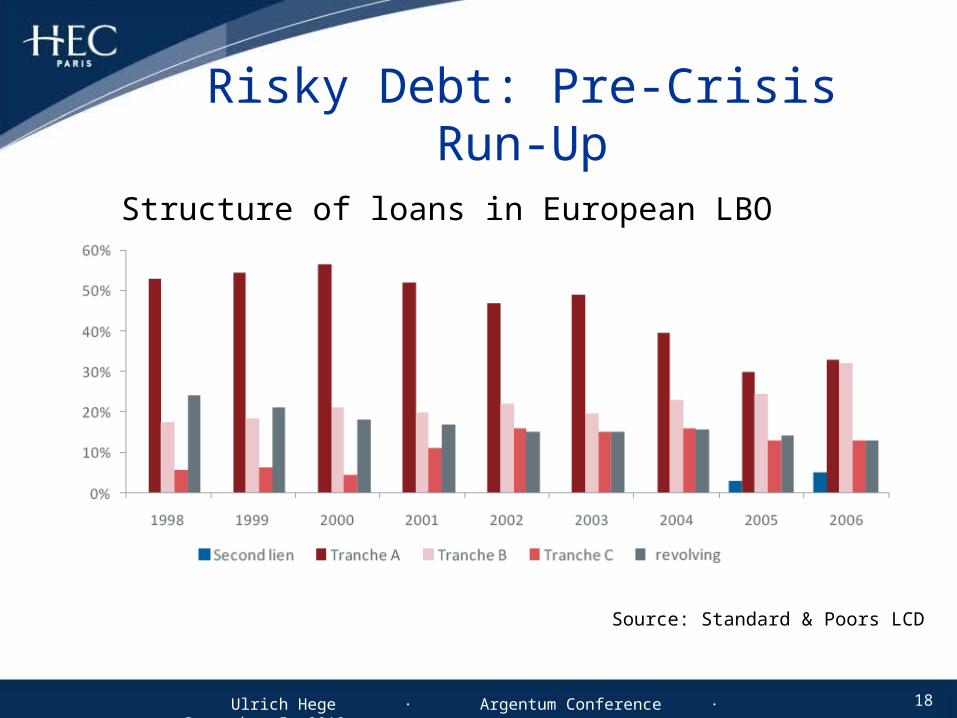

Structure of loans in European LBO transactions

Risky Debt: Pre-Crisis Run-Up

Source: Standard & Poors LCD

19 Ulrich Hege · Argentum Conference · September 5, 2012

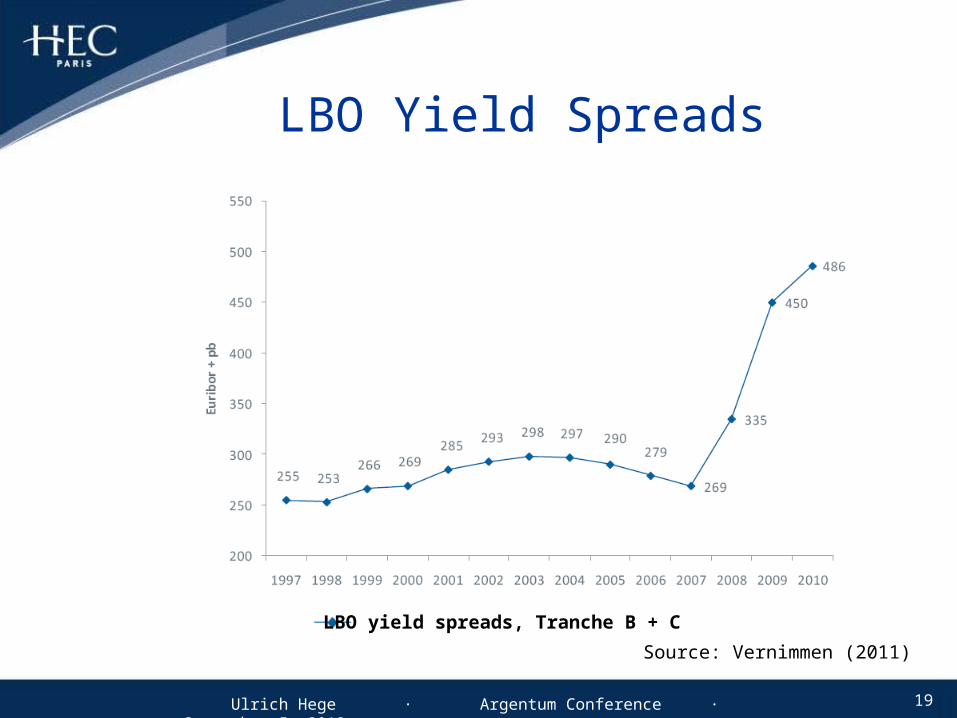

LBO Yield Spreads

LBO yield spreads, Tranche B + C

Source: Vernimmen (2011)

20 Ulrich Hege · Argentum Conference · September 5, 2012

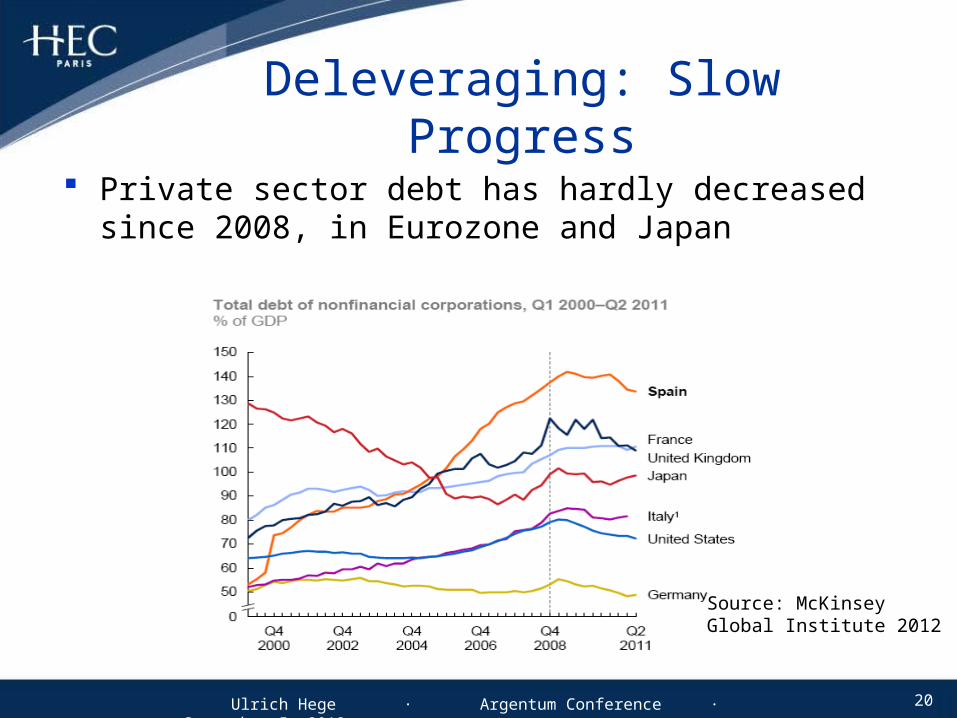

Private sector debt has hardly decreased since 2008, in Eurozone and Japan

Deleveraging: Slow Progress

Source: McKinsey Global Institute 2012

21 Ulrich Hege · Argentum Conference · September 5, 2012

Anecdotal evidence suggests: restructuring of LBO debt since 2009 has worked relatively smoothly unclear which part of LBO debt is definitely restructured,

which part is merely extended

Default rates of LBO-backed companies substantial, but fewer bankruptcies than feared

PE funds are bankruptcy experts (Hotchkiss, Smith and Strömberg, 2012)

Pricing of LBO debt indicates relative normalcy: Leveraged Loan average price indices maintain price level above 90% of par

Is LBO Debt a Systemic Risk Factor?

22 Ulrich Hege · Argentum Conference · September 5, 2012

PE Funds and (Systemic) Risk

No evidence of any contribution of the private equity industry to systemic risk during the crisis low beta estimates (1 to 1.3) reassuring (Franzoni, Nowak,

Phalippou, 2011). But ignores systemic risk effects

Lack of data prevents more thorough research, on leverage, debt overhang effects, restructuring

Deleveraging obliges PEs to look for true economic value

New disintermediation creates a trade-off for PE: banks drop out as loan arrangers, but less bank-centered financial system creates many opportunities

23 Ulrich Hege · Argentum Conference · September 5, 2012

V:Transparency

24 Ulrich Hege · Argentum Conference · September 5, 2012

(will we see the tax releases before November?)

An Image Problem

25 Ulrich Hege · Argentum Conference · September 5, 2012

“NY attorney general Schneiderman probes private equity tax strategy”, FT September 2, 2009, incl. Bain Capital, KKR, Apollo

Little knowledge on the true value of corporate tax shields in PE (Kaplan, 1989)

As large PE groups evolve into diversified financial services firms,

questions about governance of the business group and relationship between listed and unlisted parts of it

Transparency: Governance and Taxes

26 Ulrich Hege · Argentum Conference · September 5, 2012

Still no definite view about the overall performance of the PE industry, nor about its economic impact

The lack of reasonable data is largely to blame Many measurement and pervasive data problems

(Harris, Jenkinson, and Kaplan, 2011)

It is increasingly clear that the commercial data bases are being manipulated (Thomson – One Banker)

We need a Nordic sense of transparency in data availability

Transparency: Data

27 Ulrich Hege · Argentum Conference · September 5, 2012

Conclusion

PE funds need to look for sources of economic value beyond leverage

Disintermediation trade-off from the PE perspective

Credibility of PE model under siege. Nordic-style mandatory transparency on performance data, portfolio company financials, taxes, governance would help to r(re-)establish credibility