Languages

Pages

Legal

Inovasi dan Daya SaingProduk Pertanian Indonesia

dalam Mendukung MEAProf. Dr. Bustanul Arifin

Guru Besar Ilmu Ekonomi Pertanian UNILADewan Pendiri dan Ekonom Senior INDEF

Ketua Perhimpunan Ekonomi Pertanian Indonesia

Seminar Nasional “Membangun Pertanian Modern dan Inovatif Berkelanjutan dalam Rangka Mendukung MEA“Balitbangda Jambi, BPTP Jambi, Universitas Jambi, BI Jambi dan PTP VI, tanggal 31 Mei 2016 di Jambi

Sistematika Pembahasan1. Update Ekonomi Global dan Ekonomi Nasional2. Pertanian Indonesia: Kapasitas Produksi Menurun3. Dari Keunggulan Komparatif ke Keunggulan Kompetitif4. Geo-Ekonomi Global: Kerangka ASEAN Community5. Dayasaing: Pertarungan Inovasi dan Business Model6. Rekomendasi: Perbaikan Ekosistem dan Kreativitas

Ekonomi Global Mengalami Perlambatandalam persen

Perekonomian 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Ekonomi Dunia 5,5 5,7 3,1 -0,0 5,4 4,2 3,4 3,4 3,4 3,1

Negara Maju 3,1 2,8 0,2 -3,4 3,1 1,7 1,2 1,4 1,8 1,9

Negara Berkembang 8,2 8,7 5,8 3,1 7,4 6,2 5,2 5,0 4,6 4,0

Ekonomi China 12,7 14,2 9,6 9,2 10,4 9,3 7,8 7,7 7,3 6,9

Harga Konomoditas(non-energi)

23,1 13,9 7,9 -15,8 26,5 17,9 -10,0 -1,2 -4,0 -17.4

Ekonomi Indonesia 5,5 6,3 6,0 4,6 6,4 6,2 6,0 5,6 5,0 4,8

PDB percapita (US$) 1.655 1.919 2.225 2.322 2.979 3.692 3.741 3.667 3.531 3.377

Sumber: Bank Dunia dan BPS, berbagai tahun

Pertumbuhan Ekonomi Indonesia, per Sektor

Sumber: BPS, 5 Februari 2016

Distribusi & Laju Pertumbuhan PDB Wilayah

Sumber: BPS, 5 Februari 2016

Pola Pergerakan Laju Inflasi, 2000-2016

Sumber: Bank Indonesia, 2016

TPI-TPID: Sinergi Program BI & Pemerintah

Sumber: Bank Indonesia, 2016

Pertanian Indonesia: Kapasitas Produksi Menurun• Kapasitas produksi pertanian pertanian sudah menurun,

baik sumberdaya alam, maupun sumberdaya manusia.• Peningkatan produksi pangan tidak banyak didorong oleh

perubahan teknologi pertanian dan adaptasi inovasi baru;• Total factor productivity (TFP) pertanian Indonesia 1%

(ASEAN 1,4%), lebih didorong perubahan efisiensi teknis(TEC), bukan perubahan teknologi (TC) (Suo, 2014);

• Pemerintahan membuat Upaya Khusus PeningkatanProduksi Padi, Jagung dan Kedelai (Upsus Pajale), yangbelum terbukti memecahkan masalah kapasitas produksi.

• Akibatnya, persoalan struktur dan tingkah laku pasarkomoditas pangan tidak tertangani secara sistematis.

Adopsi Teknologi Produksi Pertanian Lambat

Provinsi IR42 IR64 Ciherang Inpari13Tahun Rilis 1980 1986 2000 2009

Periode (thn) 35 29 15 6Jawa Timur (%) * 15,34 41,02 3,29Jawa Barat (%) * 3,29 46,51 0,88Sulawesi Selatan (%) * * 26,30 3,85Sumatera Barat (%) 18,25 3,43 7,93 *• Untuk menghasilkan satu varietas unggul padi perlu waktu 7-10 tahun• Adopsi varietas padi unggul sampai titik tertinggi perlu waktu 10-15 tahun.• Proses adopsi teknologi: lamban, memiliki siklus, dan spesifik lokasi.

Sumber: Suryana, 2015

Peluang Perkebunan: Kunggulan Komparatif?• Produksi CPO 2015: 32 juta ton, ekspor 26 juta ton. Tahun 2016

produksi CPO menembus 34 juta ton. Produk hilir mulai tumbuh.• Produksi kopi 2015: 700 ribu ton, ekspor 500 ribu ton. Tahun 2016

produksi kopi tidak banyak berubah, walau harga jual tidak turun.• Produksi kakao 2015: 840 ribu ton,ekspor 450 ribu ton.Tahun 2016

produksi stagnan. Cocoa Sustainability Partnership baru dimulai;• Produksi karet 2015: 3,2 juta ton, sebagian besar untuk ekspor.

Tahun 2016, produksi diprediksi turun, harga global anjlok drastis.

Peluang Perkebunan: Kunggulan Komparatif?• Produksi CPO 2015: 32 juta ton, ekspor 26 juta ton. Tahun 2016

produksi CPO menembus 34 juta ton. Produk hilir mulai tumbuh.• Produksi kopi 2015: 700 ribu ton, ekspor 500 ribu ton. Tahun 2016

produksi kopi tidak banyak berubah, walau harga jual tidak turun.• Produksi kakao 2015: 840 ribu ton,ekspor 450 ribu ton.Tahun 2016

produksi stagnan. Cocoa Sustainability Partnership baru dimulai;• Produksi karet 2015: 3,2 juta ton, sebagian besar untuk ekspor.

Tahun 2016, produksi diprediksi turun, harga global anjlok drastis.

Peluang Perkebunan: Kunggulan Komparatif?• Produksi CPO 2015: 32 juta ton, ekspor 26 juta ton. Tahun 2016

produksi CPO menembus 34 juta ton. Produk hilir mulai tumbuh.• Produksi kopi 2015: 700 ribu ton, ekspor 500 ribu ton. Tahun 2016

produksi kopi tidak banyak berubah, walau harga jual tidak turun.• Produksi kakao 2015: 840 ribu ton,ekspor 450 ribu ton.Tahun 2016

produksi stagnan. Cocoa Sustainability Partnership baru dimulai;• Produksi karet 2015: 3,2 juta ton, sebagian besar untuk ekspor.

Tahun 2016, produksi diprediksi turun, harga global anjlok drastis.

Fokus Dayasaing: Keunggulan Kompetitif?• Pembangunan pertanian Indonsia perlu megubah strategi

untuk lebih berbasis pada pengembangan dayasaingekonomi berbasis pengetahuan dan inovasi baru yangmensyaratkan empat aspek dari Porter’s Diamond:

1. Kondisi faktor produksi: ter-spesialisasi, tenaga terampil2. Kondisi permintaan: konsumen makin canggih (rewel?)3. Industri pendukung: kluster utuh, referensi, suplier4. Stretagi dan struktur organisasi: persaingan, rivalitas• Plus peran pemerintah dapat bersifat positif atau negatif• Plus kesempatan tertentu dapat mendorong dayasaing

Prinsip Dayasaing: Tingkat Mikro dan Makro

Dayasaing Bangsa: Ditentukan Iklim InvestasiTahun 2015 Indonesia Malaysia Thailand Vietnam Filipina SingapuraEase of DoingBusiness (world rank) 109 18 49 90 103 1

KemudahanMembuka Usaha 173 14 96 119 165 10

Izin Konstruksi 107 15 39 12 99 1

Akses Listrik 46 13 11 108 19 6PendaftaranBangunan (IMB) 131 38 57 58 112 17

Akses Kredit 70 28 97 28 109 19Perlindungan Investorminoritas 88 4 36 122 155 1

Pembayaran pajak 148 31 70 168 126 5Kepatuhan Kontrak 170 49 56 74 140 1

Paket kebijakan deregulasi dan debirokratisasi harusdimanfaatkan untuk meningkatkan dayasaing Indonesia Sumber: Bank Dunia (2015)

Rank Negara Skor Rank 20141 Swiss 5.76 12 Singapura 6.68 23 Amerika Serikat 5.61 34 Jerman 5.53 55 Belanda 5.50 86 Jepang 5.47 67 Hongkong SAR 5.46 78 Finlandia 5.45 49 Swedia 5.43 1010 Inggris Raya 5.43 918 Malaysia 5.23 2026 Korea Selatan 4.99 2628 China 4.89 2832 Thailand 4.64 3137 Indonesia 4.52 3447 Filipina 4.39 5255 India 4.31 7190 Kamboja 3.94 95124 Nigeria 3.46 127140 Guinea 2.84 144

Global Innovation Index, 2015 Global Competitiveness Index, 2015Rank Negara Skor Rank 2014

1 Swiss 68.30 12 Inggris Raya 62.42 23 Swedia 62.40 34 Belanda 61.58 55 Amerika Serikat 60.10 66 Finlandia 59.97 47 Singapura 59.36 78 Irlandia 59.13 119 Luksemburg 59.02 910 Denmark 57.70 814 Korea Selatan 56.26 1619 Jepang 53.97 2129 China 47.47 2932 Malaysia 45.98 3355 Thailand 38.10 4881 India 31.74 7683 Filipina 31.05 10097 Indonesia 29.79 87140 Togo 18.43 142141 Sudan 14.95 143

Sumber: INSEAD--The Business School for the World, 2015-2016 Sumber: WEF, Global Competitiveness Report, 2015-2016

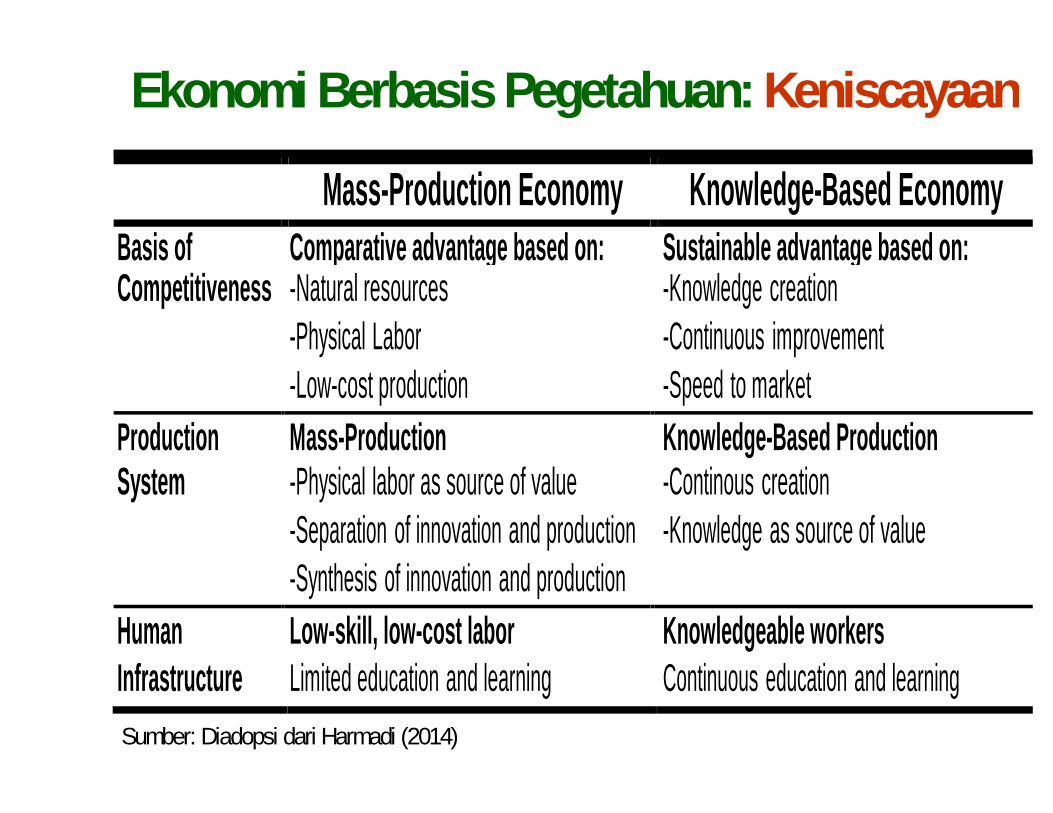

Ekonomi Berbasis Pegetahuan: Keniscayaan

Mass-Production Economy Knowledge-Based EconomyBasis of Comparative advantage based on: Sustainable advantage based on:Competitiveness -Natural resources -Knowledge creation

-Physical Labor -Continuous improvement-Low-cost production -Speed to market

Production Mass-Production Knowledge-Based ProductionSystem -Physical labor as source of value -Continous creation

-Separation of innovation and production -Knowledge as source of value-Synthesis of innovation and production

HumanInfrastructure

Low-skill, low-cost laborLimited education and learning

Knowledgeable workersContinuous education and learning

Sumber: Diadopsi dari Harmadi (2014)

ASEAN dalam Geo-Ekonomi Global

INTE

RGRA

TIO

NDE

EPEN

ING

Refresh: ASEAN Economic CommunityE N L A R G E M E N T

1967: INA, MALPHI, SIN,THA

1977: PTA

1992: CEPTAFTA

1984: BRU 1995:VN

1997: LAO, MYM

1999: CAM

2004:ASN-China

2006:ASN-KOR

2008:ASN-JAP

2009:ASN-ANZ;

EAFTA Study

CEPEA Study

1995:AFAS

1997:ASEANVision 2020

1998:AIA

2003: 3 Pillars of ASEAN Community 2020;11 Priority Integration Sectors (PIS)

2005: Logistics as PIS

2007:AEC 2015;ASEAN Charter;AEC Blueprint

ASN-India;ASN-China Investment;ASN Korea Investment

2010:ASEAN Plus WorkingGroups on ROO,TariffNomenclature, Customs,Economic Cooperation

2011:ASEAN Frameworkfor RegionalComprehensive Economic

2008: first year of AEC Blueprint;ASEAN Charter entered into force

Partnership

2009:ATIGA,ACIA,AEC Scorecard

2009: Roadmap for an ASEAN Community 2009-2015

2010: Connectivity Master PlanAEC 2015

2011:ASEAN Framework for EquitableEconomic Development

INTE

RGRA

TIO

NDE

EPEN

ING

Refresh: ASEAN Economic CommunityE N L A R G E M E N T

1967: INA, MALPHI, SIN,THA

1977: PTA

1992: CEPTAFTA

1984: BRU 1995:VN

1997: LAO, MYM

1999: CAM

2004:ASN-China

2006:ASN-KOR

2008:ASN-JAP

2009:ASN-ANZ;

EAFTA Study

CEPEA Study

1995:AFAS

1997:ASEANVision 2020

1998:AIA

2003: 3 Pillars of ASEAN Community 2020;11 Priority Integration Sectors (PIS)

2005: Logistics as PIS

2007:AEC 2015;ASEAN Charter;AEC Blueprint

ASN-India;ASN-China Investment;ASN Korea Investment

2010:ASEAN Plus WorkingGroups on ROO,TariffNomenclature, Customs,Economic Cooperation

2011:ASEAN Frameworkfor RegionalComprehensive Economic

2008: first year of AEC Blueprint;ASEAN Charter entered into force

Partnership

2009:ATIGA,ACIA,AEC Scorecard

2009: Roadmap for an ASEAN Community 2009-2015

2010: Connectivity Master PlanAEC 2015

2011:ASEAN Framework for EquitableEconomic Development

INTE

RGRA

TIO

NDE

EPEN

ING

Refresh: ASEAN Economic CommunityE N L A R G E M E N T

1967: INA, MALPHI, SIN,THA

1977: PTA

1992: CEPTAFTA

1984: BRU 1995:VN

1997: LAO, MYM

1999: CAM

2004:ASN-China

2006:ASN-KOR

2008:ASN-JAP

2009:ASN-ANZ;

EAFTA Study

CEPEA Study

1995:AFAS

1997:ASEANVision 2020

1998:AIA

2003: 3 Pillars of ASEAN Community 2020;11 Priority Integration Sectors (PIS)

2005: Logistics as PIS

2007:AEC 2015;ASEAN Charter;AEC Blueprint

ASN-India;ASN-China Investment;ASN Korea Investment

2010:ASEAN Plus WorkingGroups on ROO,TariffNomenclature, Customs,Economic Cooperation

2011:ASEAN Frameworkfor RegionalComprehensive Economic

2008: first year of AEC Blueprint;ASEAN Charter entered into force

Partnership

2009:ATIGA,ACIA,AEC Scorecard

2009: Roadmap for an ASEAN Community 2009-2015

2010: Connectivity Master PlanAEC 2015

2011:ASEAN Framework for EquitableEconomic Development

18

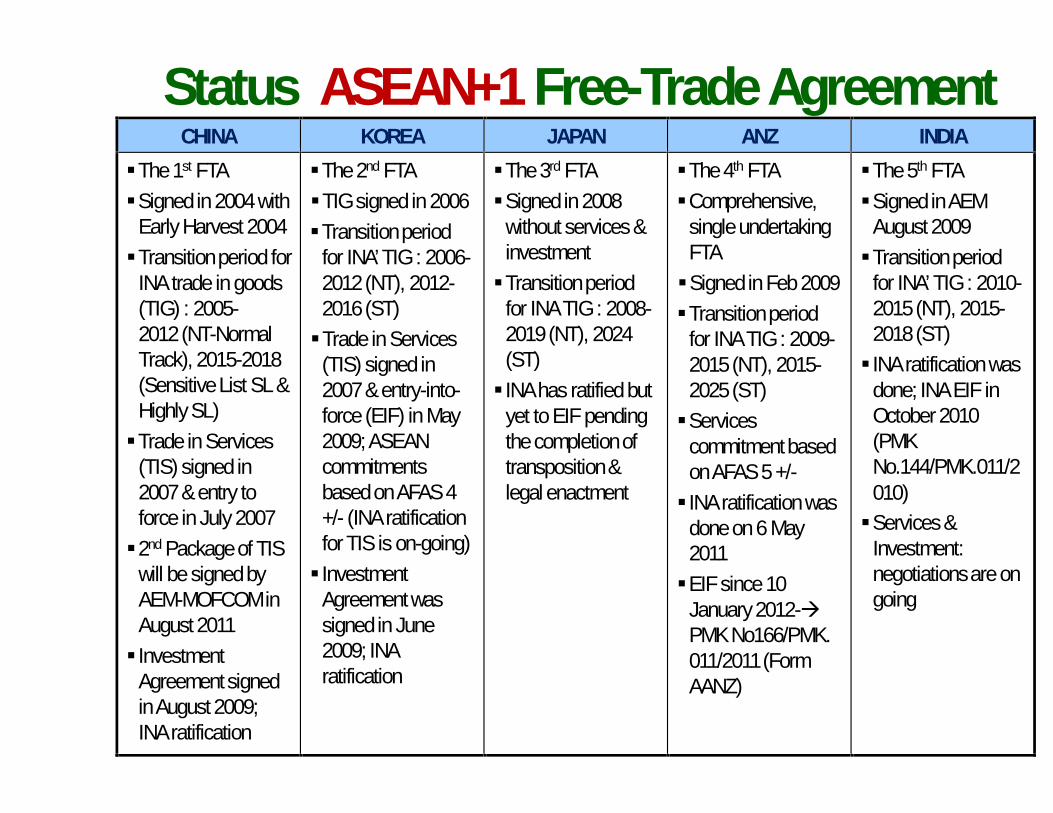

Status ASEAN+1 Free-Trade AgreementCHINA KOREA JAPAN ANZ INDIA

The 1st FTASigned in 2004 with

Early Harvest 2004Transition period for

INA trade in goods(TIG) : 2005-2012 (NT-NormalTrack), 2015-2018(Sensitive List SL &Highly SL)Trade in Services

(TIS) signed in2007 & entry toforce in July 20072nd Package of TIS

will be signed byAEM-MOFCOM inAugust 2011 Investment

Agreement signedin August 2009;INA ratification

The 2nd FTATIG signed in 2006Transition period

for INA’ TIG : 2006-2012 (NT), 2012-2016 (ST)Trade in Services

(TIS) signed in2007 & entry-into-force (EIF) in May2009; ASEANcommitmentsbased on AFAS 4+/- (INA ratificationfor TIS is on-going) Investment

Agreement wassigned in June2009; INAratification

The 3rd FTASigned in 2008

without services &investmentTransition period

for INA TIG : 2008-2019 (NT), 2024(ST) INA has ratified but

yet to EIF pendingthe completion oftransposition &legal enactment

The 4th FTAComprehensive,

single undertakingFTASigned in Feb 2009Transition period

for INA TIG : 2009-2015 (NT), 2015-2025 (ST)Services

commitment basedon AFAS 5 +/- INA ratification was

done on 6 May2011EIF since 10

January 2012-PMK No166/PMK.011/2011 (FormAANZ)

The 5th FTASigned in AEM

August 2009Transition period

for INA’ TIG : 2010-2015 (NT), 2015-2018 (ST) INA ratification was

done; INA EIF inOctober 2010(PMKNo.144/PMK.011/2010)Services &

Investment:negotiations are ongoing

18

Status ASEAN+1 Free-Trade AgreementCHINA KOREA JAPAN ANZ INDIA

The 1st FTASigned in 2004 with

Early Harvest 2004Transition period for

INA trade in goods(TIG) : 2005-2012 (NT-NormalTrack), 2015-2018(Sensitive List SL &Highly SL)Trade in Services

(TIS) signed in2007 & entry toforce in July 20072nd Package of TIS

will be signed byAEM-MOFCOM inAugust 2011 Investment

Agreement signedin August 2009;INA ratification

The 2nd FTATIG signed in 2006Transition period

for INA’ TIG : 2006-2012 (NT), 2012-2016 (ST)Trade in Services

(TIS) signed in2007 & entry-into-force (EIF) in May2009; ASEANcommitmentsbased on AFAS 4+/- (INA ratificationfor TIS is on-going) Investment

Agreement wassigned in June2009; INAratification

The 3rd FTASigned in 2008

without services &investmentTransition period

for INA TIG : 2008-2019 (NT), 2024(ST) INA has ratified but

yet to EIF pendingthe completion oftransposition &legal enactment

The 4th FTAComprehensive,

single undertakingFTASigned in Feb 2009Transition period

for INA TIG : 2009-2015 (NT), 2015-2025 (ST)Services

commitment basedon AFAS 5 +/- INA ratification was

done on 6 May2011EIF since 10

January 2012-PMK No166/PMK.011/2011 (FormAANZ)

The 5th FTASigned in AEM

August 2009Transition period

for INA’ TIG : 2010-2015 (NT), 2015-2018 (ST) INA ratification was

done; INA EIF inOctober 2010(PMKNo.144/PMK.011/2010)Services &

Investment:negotiations are ongoing

18

Status ASEAN+1 Free-Trade AgreementCHINA KOREA JAPAN ANZ INDIA

The 1st FTASigned in 2004 with

Early Harvest 2004Transition period for

INA trade in goods(TIG) : 2005-2012 (NT-NormalTrack), 2015-2018(Sensitive List SL &Highly SL)Trade in Services

(TIS) signed in2007 & entry toforce in July 20072nd Package of TIS

will be signed byAEM-MOFCOM inAugust 2011 Investment

Agreement signedin August 2009;INA ratification

The 2nd FTATIG signed in 2006Transition period

for INA’ TIG : 2006-2012 (NT), 2012-2016 (ST)Trade in Services

(TIS) signed in2007 & entry-into-force (EIF) in May2009; ASEANcommitmentsbased on AFAS 4+/- (INA ratificationfor TIS is on-going) Investment

Agreement wassigned in June2009; INAratification

The 3rd FTASigned in 2008

without services &investmentTransition period

for INA TIG : 2008-2019 (NT), 2024(ST) INA has ratified but

yet to EIF pendingthe completion oftransposition &legal enactment

The 4th FTAComprehensive,

single undertakingFTASigned in Feb 2009Transition period

for INA TIG : 2009-2015 (NT), 2015-2025 (ST)Services

commitment basedon AFAS 5 +/- INA ratification was

done on 6 May2011EIF since 10

January 2012-PMK No166/PMK.011/2011 (FormAANZ)

The 5th FTASigned in AEM

August 2009Transition period

for INA’ TIG : 2010-2015 (NT), 2015-2018 (ST) INA ratification was

done; INA EIF inOctober 2010(PMKNo.144/PMK.011/2010)Services &

Investment:negotiations are ongoing

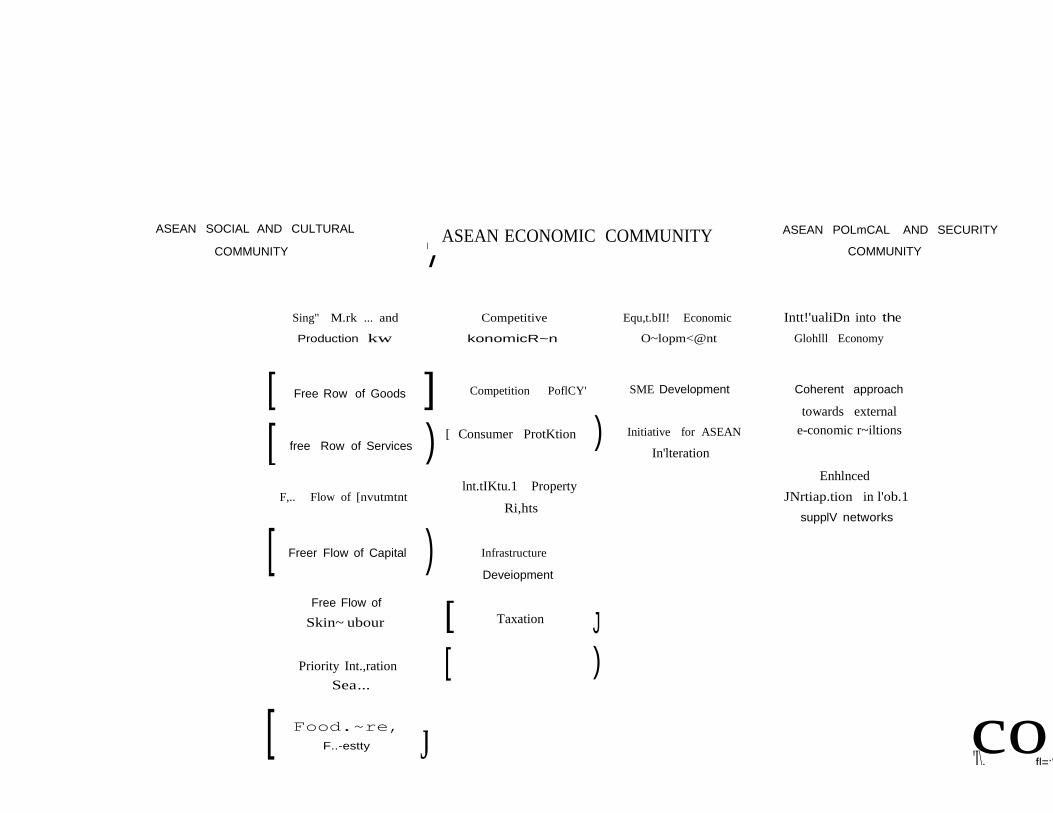

Kerangka Besar: ASEAN Community

[ ) )

[ J co

ASEAN SOCIAL AND CULTURAL

COMMUNITYASEAN ECONOMIC COMMUNITY

I

I

ASEAN POLmCAL AND SECURITY

COMMUNITY

Sing" M.rk ... and Competitive Equ,t.bII! Economic Intt!'ualiDn into the

Production kw konomicR~n O~lopm<@nt Glohlll Economy

[ Free Row of Goods ] Competition PoflCY' SME Development Coherent approach

towards external

[ Consumer ProtKtion Initiative for ASEAN e-conomic r~iltionsfree Row of Services In'lteration

lnt.tIKtu.1 PropertyEnhlnced

F,.. Flow of [nvutmtnt JNrtiap.tion in l'ob.1Ri,hts

[ Freer Flow of Capital ) Infrastructure

Deveiopment

supplV networks

Free Flow of

Skin~ ubour

Priority Int.,ration

Sea...

Food.~re,F..-estty

[ Taxation J[ )

'I\. fl=:'

Business Model: Perubahan Strategi (1)• Mempertahankan dayasaing secara abadi tentu sulit, baik

pada skala makro negara, maupun skala mikro bisnis.• Gaya hidup kaum urban mempengaruhi jatuh-bangun merek

kopi bubuk. Kedai Starbucks franchise fokus pada blending &cupping mengubah loyalitas konsumen pada merek kopi

Business Model: Perubahan Strategi (1)• Mempertahankan dayasaing secara abadi tentu sulit, baik

pada skala makro negara, maupun skala mikro bisnis.• Gaya hidup kaum urban mempengaruhi jatuh-bangun merek

kopi bubuk. Kedai Starbucks franchise fokus pada blending &cupping mengubah loyalitas konsumen pada merek kopi

Business Model: Perubahan Strategi (1)• Mempertahankan dayasaing secara abadi tentu sulit, baik

pada skala makro negara, maupun skala mikro bisnis.• Gaya hidup kaum urban mempengaruhi jatuh-bangun merek

kopi bubuk. Kedai Starbucks franchise fokus pada blending &cupping mengubah loyalitas konsumen pada merek kopi

Business Model: Perubahan Strategi (2)• Kedai Kopi Excelso: Adaptasi dari kopi merek Kapal Api

yang mulai terdesak. Berani head-to-head dgn Starbucks.

Business Model: Perubahan Strategi (2)• Kedai Kopi Excelso: Adaptasi dari kopi merek Kapal Api

yang mulai terdesak. Berani head-to-head dgn Starbucks.

Business Model: Perubahan Strategi (2)• Kedai Kopi Excelso: Adaptasi dari kopi merek Kapal Api

yang mulai terdesak. Berani head-to-head dgn Starbucks.

Business Model: Perubahan Strategi (3)• Modern Group (Fuji) harus belasan kali menyampaikan

business model menjadi Seven Eleven “warung anakmuda nongkrong”, beda dengan Alfamart dan Indomaret.

Rekomendasi: Perbaikan Ekosistem & Kreativitas• Inovasi dan dayasaing memerlukan perbaikan ekosistem inovasi

secara holistik, mulai dari manajemen usahatani, peningkatanproduktivitas, pendampingan intensif kepada petani (melibatkanuniversitas dan R&D) dengan memanfaatkan kearifan lokal;

• Rural non-farm employment (RNFE), produktivitas tenaga kerjaper sektor, integrasi proksimitas bahan baku, pusat-pusat pasar;

• Industrialisasi pedesaan, pemberdayaan sumber daya manusia,efisiensi tenaga kerja, keterkaitan desa-kota, sektor pendukung;

• Konsoldisasi lahan: skema contract-farming, kelembagaanmasyarakat, penguasaan aset, perluasan akses pasar;

• Teknologi informasi dan ekonomi kreatif: Inisiatif budaya kreatif,peningkatan nilai tambah, dan dukungan kebijakan memadai;