Languages

Pages

Legal

Broken Markets or Broken Rhetoric?

James J. Angel, Ph.D. CFA Visiting Associate Professor

The Wharton School University of Pennsylvania

Associate Professor McDonough School of Business

Georgetown University [email protected]

About #GUFinProf • Studies financial markets and regulation

– Visited over 70 exchanges around the world – Former Chair of Nasdaq Economic Advisory Board – Public member of Direct Edge Board of Directors – 10 patents on trading technology – Warned SEC 5 times in writing in year before

Flash Crash that markets were vulnerable to major technical glitches

– Testified 5 times before U.S. Congress • B.S. Caltech, MBA Harvard, Ph.D. Berkeley • At Georgetown since 1991 • At Wharton 2012-2014 • [email protected] • 202 687 3765 • Twitter: #GuFinProf

2

Key points • Lots of rhetoric about a “broken” market structure • Internal industry infighting has spilled into the public arena

– The media loves a good fight! • My take on it: Our markets are (mostly) better, but they are different than

before. – Different imperfections

• Fail in different ways • Need to work on these rough edges!

• What is broken – Need better containment against technical failures – The decline in the number of public companies: Need to experiment!

• Let issuers pick their own tick sizes – they have the incentives to get it right. – Regulation: Push SEC to hire experienced market people and move SEC to NY. – Volume drought

• Need more companies, more splits, longer trading hours for most active stocks.

3

We are under attack.

4

Some people just hate us.

5

It’s not just from the tinfoil hats

6

Public perception

• “Of 878 students at 18 high schools across 11 different states surveyed by the Financial Literacy Group, three-quarters of them said they agreed with this statement: ‘The stock market is rigged mostly to benefit greedy Wall Street bankers.’”

• New York Times, Andrew Ross Sorkin, – http://dealbook.nytimes.com/2012/08/06/why-

are-investors-fleeing-equities-hint-its-not-the-computers/

7

Thousands of complaints to SEC

• http://www.sec.gov/comments/s7-21-09/s72109-42.htm

8

This is not new

• “Meanwhile, individual investors are coming to the realization that the stock market is rigged against them.” – New York Times, January 17, 1988.

– “The money market is manipulated down just as the

stock market is manipulated up, the two manipulations being complementary and part of the some dark plot.”

– New York Times, The Financial Situation, November 20, 1904

9

Misleading Media Reports

• http://www.nytimes.com/2009/07/24/business/24trading.html?_r=4&adxnnl=1&ref=business&adxnnlx=1255964744-hsGxQ2eMFrQcW2cnqFYOtw

10

And the politicians rise to the occasion

11

The regulators listen.

12

And the regulators act

13

So what’s going on?

• Are the markets really broken? • Or is it just broken rhetoric?

• Is it just the usual whining or is there really a

broken-market wolf out there?

14

Whenever there is a meltdown…

• There is a call to “arrest the usual suspects”

15

This is routine • Whenever markets go down…

– Anyone who made money gets blamed • Either for causing the problem • Or for profiting from it.

• Calls for reform – To fix problems – And to punish the bloodsucking fascist insects that prey

upon the people.

• This has been going on for hundreds of years – Amsterdam attempted to ban short selling soon after

modern equity trading began.

16

Populist misunderstanding

• If I don’t understand it, it must be bad. • If I lost money in the market, and someone

else is making money, then they must have stolen it from me.

• And we want revenge!!!!!!!!!!!!!!!!!!!!!!!!

17

Long standing populist mistrust of financial markets.

18

The Al Berkeley Analogy

• Former Nasdaq President • Our markets today are like a 4-team soccer

game. – Buyers and sellers are competing with goals at

the North and South ends of the field. – Exchanges and ATS’s have goals on the East and

West sides. – You can’t tell the players from their jerseys. – They all want to control the ball.

19

Commercial disputes

• Players don’t hesitate to lobby regulators and legislators to come to their side.

• The media love a fight – Happy to let us box in public.

• We put nasty names on things we don’t like – “Dark” pools, “naked” short selling, “naked” access,

“predatory” algos…

– Media picks it up and dark names scare the public.

20

But this can backfire

• Reg NMS was the result of a previous NYSE lobbying campaign to protect the old trade-through rule which kept the ECNs from effectively competing in NYSE-listed stocks.

• But the SEC only protected “fast” markets. – NYSE forced to automate

• And forced to route orders to competition.

• Result: Massive erosion in NYSE market share.

21

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

Apr-04 Aug-05 Dec-06 May-08 Sep-09 Feb-11 Jun-12

NYSE-listed market shares

NYSE

NYSE-Arca

NasdaqOMX Group

BATS

Direct Edge

Other

Total

22

The allegations

• “Market fragmentation and HFT have scared away investors” – Co-location, HFT, “dark pools” allegedly steal

money from retail investors

• Excessive “fragmentation” leads to complexity – Complexity = risk

23

Where’s the proof?

• By traditional measures of market quality, things are better than ever for the individual investor.

• So why is there so much grumbling?

24

Our markets are mostly better now

• Lower transactions costs benefit retail investors.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Sep-

01

Mar

-02

Sep-

02

Mar

-03

Sep-

03

Mar

-04

Sep-

04

Mar

-05

Sep-

05

Mar

-06

Sep-

06

Mar

-07

Sep-

07

Mar

-08

Sep-

08

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Mar

-12

U.S

. cen

ts

Effective Bid-Ask Spreads from Rule 605 Reports

NYSE-Listed

Nasdaq-listed

25

Executions are faster

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Sep-

01

Jan-

02

May

-02

Sep-

02

Jan-

03

May

-03

Sep-

03

Jan-

04

May

-04

Sep-

04

Jan-

05

May

-05

Sep-

05

Jan-

06

May

-06

Sep-

06

Jan-

07

May

-07

Sep-

07

Jan-

08

May

-08

Sep-

08

Jan-

09

May

-09

Sep-

09

Jan-

10

May

-10

Sep-

10

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Market Order Execution Speed

NYSE-listed Nasdaq-listed

26

If our market structure is so bad…

• Why are other nations copying us? – Monopoly exchanges deliver monopoly service

and cost. – Competition improves the breed. – Need for-profit incentives to bring in real

competition.

27

Institutional trading costs are low in the U.S.

0

20

40

60

80

100

120

140

US - small cap

Latin America

Emerging Markets

Africa and the Middle

East

US - mid cap

Japan Developed Asia ex-Japan

Canada UK Developed Europe ex-

UK

US - large cap

Basi

s poi

nts

Institutional Trading Costs (bps)

2 Q 2010

3 Q 2012

28

But… Some of the complaints have merit

29

What was scary about the Flash Crash

• 1. Flash Crash revealed that market had no shock absorbers to prevent chaotic behavior. – Revealed that nobody had the big picture in mind.

• 2. SEC could not deliver a credible story in a timely manner about what happened. – Even though practitioners were telling them

within hours.

30

Don’t be LULD into complacency

• Post Flash Crash reforms are steps in the right direction, but further refinement is needed. – Interactions of different circuit breakers not well

thought out! • Will break in some unexpected way when a real

tsunami of message traffic hits.

– Shock absorbers need to be based on data integrity as well as price.

31

And there will be another incident…

• We just don’t know where or when. • Tsunamis of message traffic are predictable in

times of great uncertainty. • Market barely withstood “Twitter Crash”

– But what if it had been real news?

32

Message traffic is still an issue that costs all of us money.

-

100

200

300

400

500

600

700

800

Jul-98 Apr-01 Jan-04 Oct-06 Jul-09 Apr-12

Quotes per minute per security

33

Quotes-to-trades are down from their peak.

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Jul-98 Apr-01 Jan-04 Oct-06 Jul-09 Apr-12

Quote-to-Trade Ratio

34

Other allegations have less merit.

• Excessive fragmentation?

• Do we have too many supermarkets?

35

“Excessive” Competition?

• Our “open architecture” market makes it easy for new innovative entrants to come in. – Competition has improved the markets.

• Consolidation is provided by smart routers. • The network of all buyers and sellers is the

market, rather than any one trading platform.

36

All HFT are not alike

• We need to get the message out that many HFTs do things that help the market – Market making – ETF arbitrage

37

Regulation is broken

• Over 100 different financial regulators at state and federal levels – Overlapping jurisdictions – Turf battles – Contradictory regulatory philosophies – Dysfunctional bureaucratic cultures that value

paperwork over common sense.

38

We have been penny wise and pound foolish in funding the SEC

• Cumulative SEC Budget in real dollars since 1934: About $21 billion

• Less than investor losses from one Enron or one Madoff!

39

The Result

• Failing to fund the SEC has resulted in a financial police force that only writes speeding tickets on Main Street while the criminals go on stealing.

40

Need for fundamental reform

• To change an organizations culture, need to change the people.

• Staff SEC with fewer lawyers, but more people with market experience.

• Every time the SEC testifies before Congress, they should be asked how many CFAs, MBAs, FINRA license holders, engineers, and IT professionals work for them in addition to JDs.

• How many have two or more years of work experience in the financial services industry?

41

Move SEC to New York City • The SEC does not understand markets.

– Located in DC, far from the markets. – DC labor pool mostly government types.

• Move SEC to NY to attract more market savvy employees.

• Put in same building as other financial regulators to facilitate information and people flow among agencies.

• More jobs for NY & NJ Congressional Districts = more support for SEC budget. – Move as much of SEC as possible to other Congressional

Districts. – Leave only a few Congressional liaisons in DC.

42

Our vocabulary is broken.

• Dark pools – Custom-display markets

• Naked anything • “Fragmented”

– Implies something is broken

43

Our supply of new companies is broken.

44

This is a crisis!

• Only 3,565 firms in Wilshire “5000” • As of March 31, 2013

– Used to have around 8,000.

• At current rate of decline, we will not have 500 public U.S. companies left for the S&P500 by 2060.

45

Numerous contributing factors

• Litigation mess – “If I go public, I get sued.”

• Compliance burdens – Sarbanes Oxley, etc.

• Market structure – Old NASDAQ very different from old NYSE – Wider spreads provided financial incentive for

industry to market smaller stocks – Now we have almost no differences between the two

exchanges.

46

We need to experiment!

• Industry and regulators need to be open to different ways of trading small stocks.

• Sponsored liquidity – Direct payments from issuers

• 12b-1 style fees? – 1 to 5 cents a share fee – Set by issuer – Could be used to pay for

• Market making • Research • Commission-free trading

47

Volume is broken. Why?

0

2,000

4,000

6,000

8,000

10,000

12,000

Jan-03 May-04 Sep-05 Feb-07 Jun-08 Nov-09 Mar-11 Aug-12

Mill

ions

of s

hare

s

Average Daily US Equity Share Volume

48

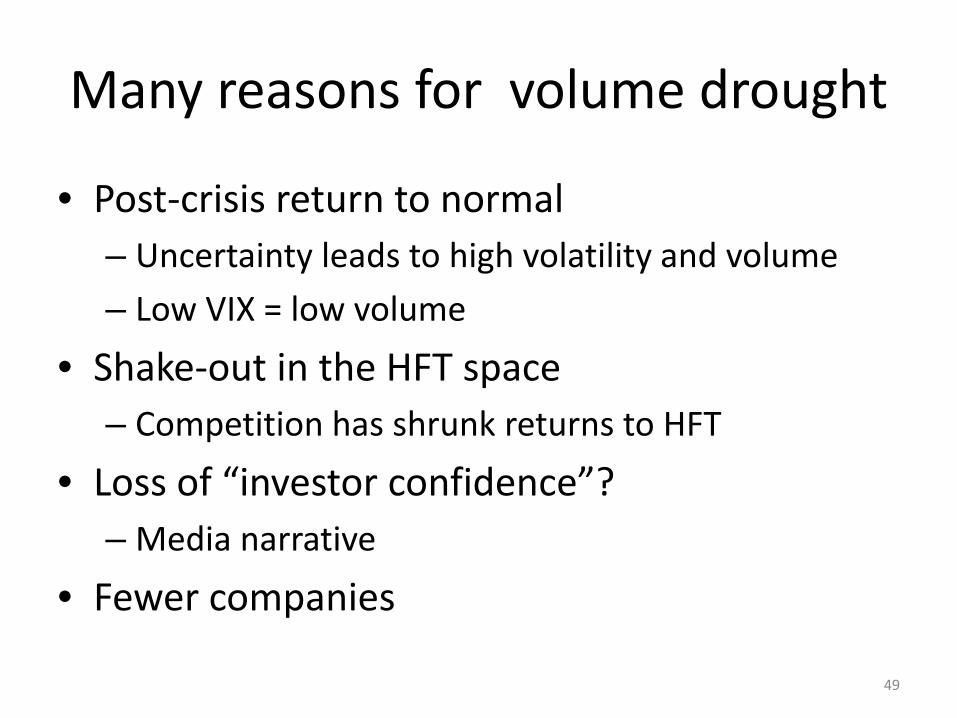

Many reasons for volume drought

• Post-crisis return to normal – Uncertainty leads to high volatility and volume – Low VIX = low volume

• Shake-out in the HFT space – Competition has shrunk returns to HFT

• Loss of “investor confidence”? – Media narrative

• Fewer companies

49

To increase volume

• More companies • More stock splits for high-priced stocks

– Over $100 stocks have more volatility than they should.

– NYSE and NASDAQ should stop charging fees for splits. • Extend trading hours in most active stocks

– Already good enough liquidity in many active stocks in extended trading like BAC.

– Start with Dow, Nasdaq100, S&P100 and largest ETFs & ADRs.

– Extend to 5PM ET and see what happens.

50

Summary

• Our markets are not “broken” but they can be improved. – Need better containments for technology failures and

data overloads. – Need willingness to experiment with different market

structures for small-cap stocks • Let issuers pick their ticks • 12b1 fees for equities

– Need more experienced regulators • Push SEC to hire experienced market plumbers and move to

NY.

51

Top Related