Broken Markets or Broken Rhetoric? - STANY€¦ · • “Market fragmentation and HFT have scared...

51

Broken Markets or Broken Rhetoric? James J. Angel, Ph.D. CFA Visiting Associate Professor The Wharton School University of Pennsylvania Associate Professor McDonough School of Business Georgetown University [email protected]

Transcript of Broken Markets or Broken Rhetoric? - STANY€¦ · • “Market fragmentation and HFT have scared...

Broken Markets or Broken Rhetoric?

James J. Angel, Ph.D. CFA Visiting Associate Professor

The Wharton School University of Pennsylvania

Associate Professor McDonough School of Business

Georgetown University [email protected]

About #GUFinProf • Studies financial markets and regulation

– Visited over 70 exchanges around the world – Former Chair of Nasdaq Economic Advisory Board – Public member of Direct Edge Board of Directors – 10 patents on trading technology – Warned SEC 5 times in writing in year before

Flash Crash that markets were vulnerable to major technical glitches

– Testified 5 times before U.S. Congress • B.S. Caltech, MBA Harvard, Ph.D. Berkeley • At Georgetown since 1991 • At Wharton 2012-2014 • [email protected] • 202 687 3765 • Twitter: #GuFinProf

2

Key points • Lots of rhetoric about a “broken” market structure • Internal industry infighting has spilled into the public arena

– The media loves a good fight! • My take on it: Our markets are (mostly) better, but they are different than

before. – Different imperfections

• Fail in different ways • Need to work on these rough edges!

• What is broken – Need better containment against technical failures – The decline in the number of public companies: Need to experiment!

• Let issuers pick their own tick sizes – they have the incentives to get it right. – Regulation: Push SEC to hire experienced market people and move SEC to NY. – Volume drought

• Need more companies, more splits, longer trading hours for most active stocks.

3

We are under attack.

4

Some people just hate us.

5

It’s not just from the tinfoil hats

6

Public perception

• “Of 878 students at 18 high schools across 11 different states surveyed by the Financial Literacy Group, three-quarters of them said they agreed with this statement: ‘The stock market is rigged mostly to benefit greedy Wall Street bankers.’”

• New York Times, Andrew Ross Sorkin, – http://dealbook.nytimes.com/2012/08/06/why-

are-investors-fleeing-equities-hint-its-not-the-computers/

7

Thousands of complaints to SEC

• http://www.sec.gov/comments/s7-21-09/s72109-42.htm

8

This is not new

• “Meanwhile, individual investors are coming to the realization that the stock market is rigged against them.” – New York Times, January 17, 1988.

– “The money market is manipulated down just as the

stock market is manipulated up, the two manipulations being complementary and part of the some dark plot.”

– New York Times, The Financial Situation, November 20, 1904

9

Misleading Media Reports

• http://www.nytimes.com/2009/07/24/business/24trading.html?_r=4&adxnnl=1&ref=business&adxnnlx=1255964744-hsGxQ2eMFrQcW2cnqFYOtw

10

And the politicians rise to the occasion

11

The regulators listen.

12

And the regulators act

13

So what’s going on?

• Are the markets really broken? • Or is it just broken rhetoric?

• Is it just the usual whining or is there really a

broken-market wolf out there?

14

Whenever there is a meltdown…

• There is a call to “arrest the usual suspects”

15

This is routine • Whenever markets go down…

– Anyone who made money gets blamed • Either for causing the problem • Or for profiting from it.

• Calls for reform – To fix problems – And to punish the bloodsucking fascist insects that prey

upon the people.

• This has been going on for hundreds of years – Amsterdam attempted to ban short selling soon after

modern equity trading began.

16

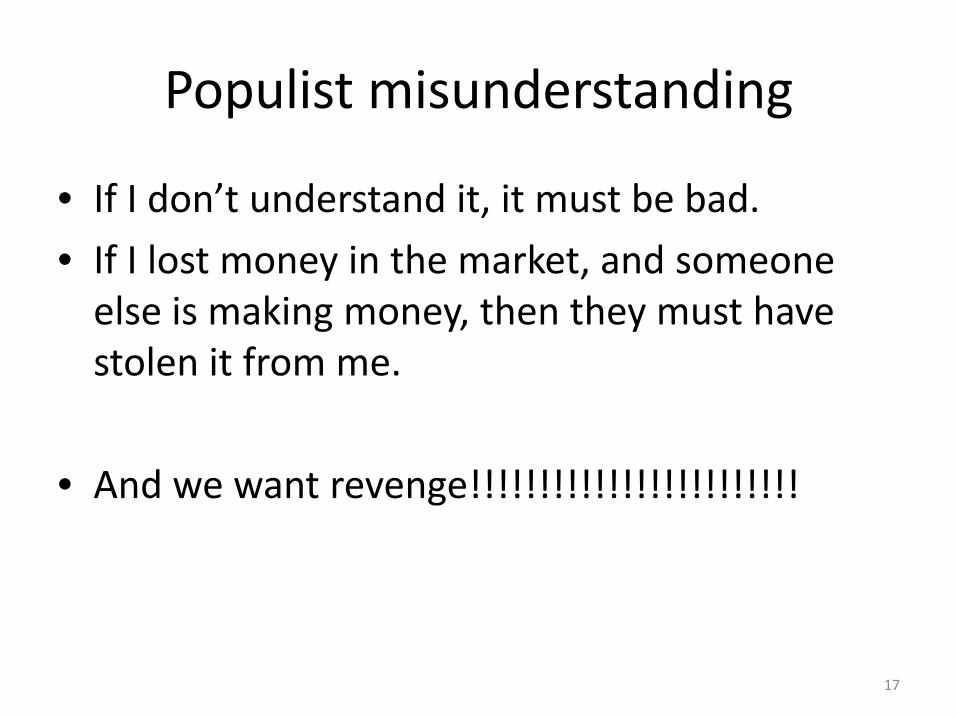

Populist misunderstanding

• If I don’t understand it, it must be bad. • If I lost money in the market, and someone

else is making money, then they must have stolen it from me.

• And we want revenge!!!!!!!!!!!!!!!!!!!!!!!!

17

Long standing populist mistrust of financial markets.

18

The Al Berkeley Analogy

• Former Nasdaq President • Our markets today are like a 4-team soccer

game. – Buyers and sellers are competing with goals at

the North and South ends of the field. – Exchanges and ATS’s have goals on the East and

West sides. – You can’t tell the players from their jerseys. – They all want to control the ball.

19

Commercial disputes

• Players don’t hesitate to lobby regulators and legislators to come to their side.

• The media love a fight – Happy to let us box in public.

• We put nasty names on things we don’t like – “Dark” pools, “naked” short selling, “naked” access,

“predatory” algos…

– Media picks it up and dark names scare the public.

20

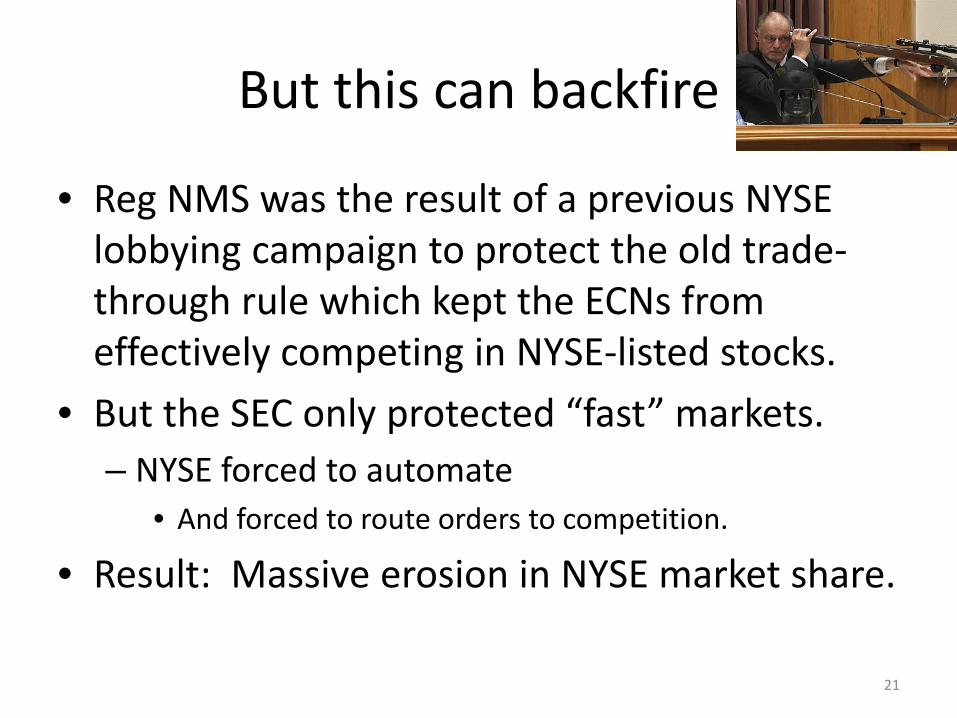

But this can backfire

• Reg NMS was the result of a previous NYSE lobbying campaign to protect the old trade-through rule which kept the ECNs from effectively competing in NYSE-listed stocks.

• But the SEC only protected “fast” markets. – NYSE forced to automate

• And forced to route orders to competition.

• Result: Massive erosion in NYSE market share.

21

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

Apr-04 Aug-05 Dec-06 May-08 Sep-09 Feb-11 Jun-12

NYSE-listed market shares

NYSE

NYSE-Arca

NasdaqOMX Group

BATS

Direct Edge

Other

Total

22

The allegations

• “Market fragmentation and HFT have scared away investors” – Co-location, HFT, “dark pools” allegedly steal

money from retail investors

• Excessive “fragmentation” leads to complexity – Complexity = risk

23

Where’s the proof?

• By traditional measures of market quality, things are better than ever for the individual investor.

• So why is there so much grumbling?

24

Our markets are mostly better now

• Lower transactions costs benefit retail investors.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Sep-

01

Mar

-02

Sep-

02

Mar

-03

Sep-

03

Mar

-04

Sep-

04

Mar

-05

Sep-

05

Mar

-06

Sep-

06

Mar

-07

Sep-

07

Mar

-08

Sep-

08

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Mar

-12

U.S

. cen

ts

Effective Bid-Ask Spreads from Rule 605 Reports

NYSE-Listed

Nasdaq-listed

25

Executions are faster

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Sep-

01

Jan-

02

May

-02

Sep-

02

Jan-

03

May

-03

Sep-

03

Jan-

04

May

-04

Sep-

04

Jan-

05

May

-05

Sep-

05

Jan-

06

May

-06

Sep-

06

Jan-

07

May

-07

Sep-

07

Jan-

08

May

-08

Sep-

08

Jan-

09

May

-09

Sep-

09

Jan-

10

May

-10

Sep-

10

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Market Order Execution Speed

NYSE-listed Nasdaq-listed

26

If our market structure is so bad…

• Why are other nations copying us? – Monopoly exchanges deliver monopoly service

and cost. – Competition improves the breed. – Need for-profit incentives to bring in real

competition.

27

Institutional trading costs are low in the U.S.

0

20

40

60

80

100

120

140

US - small cap

Latin America

Emerging Markets

Africa and the Middle

East

US - mid cap

Japan Developed Asia ex-Japan

Canada UK Developed Europe ex-

UK

US - large cap

Basi

s poi

nts

Institutional Trading Costs (bps)

2 Q 2010

3 Q 2012

28

But… Some of the complaints have merit

29

What was scary about the Flash Crash

• 1. Flash Crash revealed that market had no shock absorbers to prevent chaotic behavior. – Revealed that nobody had the big picture in mind.

• 2. SEC could not deliver a credible story in a timely manner about what happened. – Even though practitioners were telling them

within hours.

30

Don’t be LULD into complacency

• Post Flash Crash reforms are steps in the right direction, but further refinement is needed. – Interactions of different circuit breakers not well

thought out! • Will break in some unexpected way when a real

tsunami of message traffic hits.

– Shock absorbers need to be based on data integrity as well as price.

31

And there will be another incident…

• We just don’t know where or when. • Tsunamis of message traffic are predictable in

times of great uncertainty. • Market barely withstood “Twitter Crash”

– But what if it had been real news?

32

Message traffic is still an issue that costs all of us money.

-

100

200

300

400

500

600

700

800

Jul-98 Apr-01 Jan-04 Oct-06 Jul-09 Apr-12

Quotes per minute per security

33

Quotes-to-trades are down from their peak.

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Jul-98 Apr-01 Jan-04 Oct-06 Jul-09 Apr-12

Quote-to-Trade Ratio

34

Other allegations have less merit.

• Excessive fragmentation?

• Do we have too many supermarkets?

35

“Excessive” Competition?

• Our “open architecture” market makes it easy for new innovative entrants to come in. – Competition has improved the markets.

• Consolidation is provided by smart routers. • The network of all buyers and sellers is the

market, rather than any one trading platform.

36

All HFT are not alike

• We need to get the message out that many HFTs do things that help the market – Market making – ETF arbitrage

37

Regulation is broken

• Over 100 different financial regulators at state and federal levels – Overlapping jurisdictions – Turf battles – Contradictory regulatory philosophies – Dysfunctional bureaucratic cultures that value

paperwork over common sense.

38

We have been penny wise and pound foolish in funding the SEC

• Cumulative SEC Budget in real dollars since 1934: About $21 billion

• Less than investor losses from one Enron or one Madoff!

39

The Result

• Failing to fund the SEC has resulted in a financial police force that only writes speeding tickets on Main Street while the criminals go on stealing.

40

Need for fundamental reform

• To change an organizations culture, need to change the people.

• Staff SEC with fewer lawyers, but more people with market experience.

• Every time the SEC testifies before Congress, they should be asked how many CFAs, MBAs, FINRA license holders, engineers, and IT professionals work for them in addition to JDs.

• How many have two or more years of work experience in the financial services industry?

41

Move SEC to New York City • The SEC does not understand markets.

– Located in DC, far from the markets. – DC labor pool mostly government types.

• Move SEC to NY to attract more market savvy employees.

• Put in same building as other financial regulators to facilitate information and people flow among agencies.

• More jobs for NY & NJ Congressional Districts = more support for SEC budget. – Move as much of SEC as possible to other Congressional

Districts. – Leave only a few Congressional liaisons in DC.

42

Our vocabulary is broken.

• Dark pools – Custom-display markets

• Naked anything • “Fragmented”

– Implies something is broken

43

Our supply of new companies is broken.

44

This is a crisis!

• Only 3,565 firms in Wilshire “5000” • As of March 31, 2013

– Used to have around 8,000.

• At current rate of decline, we will not have 500 public U.S. companies left for the S&P500 by 2060.

45

Numerous contributing factors

• Litigation mess – “If I go public, I get sued.”

• Compliance burdens – Sarbanes Oxley, etc.

• Market structure – Old NASDAQ very different from old NYSE – Wider spreads provided financial incentive for

industry to market smaller stocks – Now we have almost no differences between the two

exchanges.

46

We need to experiment!

• Industry and regulators need to be open to different ways of trading small stocks.

• Sponsored liquidity – Direct payments from issuers

• 12b-1 style fees? – 1 to 5 cents a share fee – Set by issuer – Could be used to pay for

• Market making • Research • Commission-free trading

47

Volume is broken. Why?

0

2,000

4,000

6,000

8,000

10,000

12,000

Jan-03 May-04 Sep-05 Feb-07 Jun-08 Nov-09 Mar-11 Aug-12

Mill

ions

of s

hare

s

Average Daily US Equity Share Volume

48

Many reasons for volume drought

• Post-crisis return to normal – Uncertainty leads to high volatility and volume – Low VIX = low volume

• Shake-out in the HFT space – Competition has shrunk returns to HFT

• Loss of “investor confidence”? – Media narrative

• Fewer companies

49

To increase volume

• More companies • More stock splits for high-priced stocks

– Over $100 stocks have more volatility than they should.

– NYSE and NASDAQ should stop charging fees for splits. • Extend trading hours in most active stocks

– Already good enough liquidity in many active stocks in extended trading like BAC.

– Start with Dow, Nasdaq100, S&P100 and largest ETFs & ADRs.

– Extend to 5PM ET and see what happens.

50

Summary

• Our markets are not “broken” but they can be improved. – Need better containments for technology failures and

data overloads. – Need willingness to experiment with different market

structures for small-cap stocks • Let issuers pick their ticks • 12b1 fees for equities

– Need more experienced regulators • Push SEC to hire experienced market plumbers and move to

NY.

51