The complete-idiots-guide-to-business-plans-120609033902-phpapp02

338

by Gwen Moran and Sue Johnson A member of Penguin Group (USA) Inc. Business Plans

-

Upload

truong-trung-thinh -

Category

Education

-

view

28 -

download

0

Transcript of The complete-idiots-guide-to-business-plans-120609033902-phpapp02

by Gwen Moran and Sue Johnson

A member of Penguin Group (USA) Inc.

Business Plans

by Gwen Moran and Sue Johnson

A member of Penguin Group (USA) Inc.

Business Plans

This book is dedicated to the brave, visionary people who start and run the businesses that power our nation’s economy.

ALPHA BOOKSPublished by the Penguin Group

Penguin Group (USA) Inc., 375 Hudson Street, New York, New York 10014, USA

Penguin Group (Canada), 90 Eglinton Avenue East, Suite 700, Toronto, Ontario M4P 2Y3, Canada (a division ofPearson Penguin Canada Inc.)

Penguin Books Ltd., 80 Strand, London WC2R 0RL, England

Penguin Ireland, 25 St. Stephen's Green, Dublin 2, Ireland (a division of Penguin Books Ltd.)

Penguin Group (Australia), 250 Camberwell Road, Camberwell, Victoria 3124, Australia (a division of PearsonAustralia Group Pty. Ltd.)

Penguin Books India Pvt. Ltd., 11 Community Centre, Panchsheel Park, New Delhi—110 017, India

Penguin Group (NZ), 67 Apollo Drive, Rosedale, North Shore, Auckland 1311, New Zealand (a division of PearsonNew Zealand Ltd.)

Penguin Books (South Africa) (Pty.) Ltd., 24 Sturdee Avenue, Rosebank, Johannesburg 2196, South Africa

Penguin Books Ltd., Registered Offices: 80 Strand, London WC2R 0RL, England

Copyright © 2005 by Gwen Moran and Sue JohnsonAll rights reserved. No part of this book shall be reproduced, stored in a retrieval system, or transmitted by any means,electronic, mechanical, photocopying, recording, or otherwise, without written permission from the publisher. Nopatent liability is assumed with respect to the use of the information contained herein. Although every precaution hasbeen taken in the preparation of this book, the publisher and authors assume no responsibility for errors or omissions.Neither is any liability assumed for damages resulting from the use of information contained herein. For information,address Alpha Books, 800 East 96th Street, Indianapolis, IN 46240.

THE COMPLETE IDIOT’S GUIDE TO and Design are registered trademarks of Penguin Group (USA) Inc.

Library of Congress Catalog Card Number: 2005928079

Note: This publication contains the opinions and ideas of its authors. It is intended to provide helpful and informativematerial on the subject matter covered. It is sold with the understanding that the authors and publisher are not engagedin rendering professional services in the book. If the reader requires personal assistance or advice, a competent profes-sional should be consulted.

The authors and publisher specifically disclaim any responsibility for any liability, loss, or risk, personal or otherwise,which is incurred as a consequence, directly or indirectly, of the use and application of any of the contents of this book.

Publisher: Marie Butler-KnightProduct Manager: Phil KitchelSenior Managing Editor: Jennifer BowlesSenior Acquisitions Editor: Mike SandersDevelopment Editor: Ginny Bess MunroeProduction Editor: Megan Douglass

Copy Editor: Jan ZoyaCartoonist: Jody Shaeffer

Indexer: Heather McNeillLayout: Becky Harmon

Book Designer: Trina Wurst

ISBN: 1-4406-9085-5

Contents at a GlancePart 1: Getting Started 1

1 According to Plan 3How your plan can help you

2 Figuring Out the Financing 15Understanding your business’s financial needs

3 Business Writing Basics 29Tips and pitfalls to consider while writing your plan

Part 2: Putting Together Your Plan 37

4 Ready, Set, Write 39Putting your business ideas on paper

5 Getting Down to Business 47How to put your best business foot forward

6 Industry Overview 61Describing your industry and its climate

7 Who Are You? 75Your people are your primary asset; how to showcase yourdream team

8 Analyzing Your Business in the Market 87Explaining how your business will perform in the market

9 Getting the Word Out 105Positioning and promoting your business for the best possibleresults

10 Sales Plan and Forecast 119Explaining how you’ll sell your stuff

11 Operation Success 129Making the most of your day-to-day business activities

12 Money, Money 141Financial statements you’ll need to know for your plan

13 Show Your Documents 159Supporting your claims with all the right backup documents

14 Executive Summary 169What you’re going to tell them in this critical part of yourplan

Part 3: Putting Your Plan to Work 175

15 Financing Considerations to Include in Your Plan 177How to use your plan for investment or lending purposes

16 Using Your Plan as a Management Tool 189How your plan can help everyone in the business get on thesame page

17 Keeping Your Plan Current 205How to keep your plan up to date and relevant

Appendixes

A Business Terms Glossary 215

B Sample Plans 221

C Resources 301

Index 307

Contents

Part 1: Getting Started 11 According to Plan 3

Business Owner Basics ..................................................................3Types of Business Plans ................................................................4

Securing Financing or Investors ....................................................5Strengthening Operations ............................................................5Preparing for a Sale ....................................................................5

How Can a Plan Help? ..................................................................5Establishing a Vision and Direction ..............................................6Keeping on Course ........................................................................6Setting Goals and Benchmarking Success ......................................6Outlining Operations ..................................................................7Fiscal Fitness ................................................................................7Checking the Ego ........................................................................7Thorough Research ......................................................................8Marketing Plan ..........................................................................8Feasibility ....................................................................................8Future Expansion ........................................................................8Exit Strategy ..............................................................................8

Your USP ......................................................................................9Finding Your USP Through Feedback ..........................................9

Doing It Yourself or Getting Help? ............................................10Finding Free or Low-Cost Help ..................................................11Hiring Help ..............................................................................11

Getting Soft ................................................................................12

2 Figuring Out the Financing 15Understanding Debt and Equity ................................................16

Debt ..........................................................................................16Equity ........................................................................................16

Money Sources ............................................................................16Grants ......................................................................................17Personal Resources ......................................................................17Loans ........................................................................................19

Selecting a Lender ......................................................................21Angel Investors ............................................................................21Other Funding Sources ..............................................................22

The Complete Idiot’s Guide to Business Plansvi

EDA ..........................................................................................22Community Development Centers ..............................................22Trade or Business Groups ..........................................................22

What Lenders and Investors Want ............................................23Capacity to Repay ......................................................................23Capital to Invest ........................................................................23Collateral ..................................................................................24Conditions of Use of Money ........................................................24Character of Owners ..................................................................24Credit Rating ............................................................................24

Credit-Reporting Bureaus ..........................................................25Your Credit Score ........................................................................26Assessing Your Report ................................................................26

Increasing Your Score ................................................................27Beware of Quick Credit Fixes ....................................................28

3 Business Writing Basics 29Effective Business Writing ..........................................................29

Targeting Your Audience ............................................................30Language and Tone ....................................................................30Grammar ..................................................................................31Cutting the Fluff ......................................................................32Avoiding Clichés ........................................................................33Presenting Your Information ......................................................33Capitalizing and Punctuating Properly ......................................34Writing, then Rewriting ............................................................35

Avoiding Writer’s Block ..............................................................35Speaking and Writing Well ........................................................36

Part 2: Putting Together Your Plan 374 Ready, Set, Write 39

From Dream to Document ........................................................39Being Organized ........................................................................40Knowing Your Stuff ..................................................................40Supporting Your Claims ............................................................41

Getting to the Goal ....................................................................41Obtaining Financial Assistance ..................................................41Attract Business Partners ..........................................................43Operation Benchmark ................................................................43

Contents

Obtain Assistance ........................................................................43Iterative Process ..........................................................................44

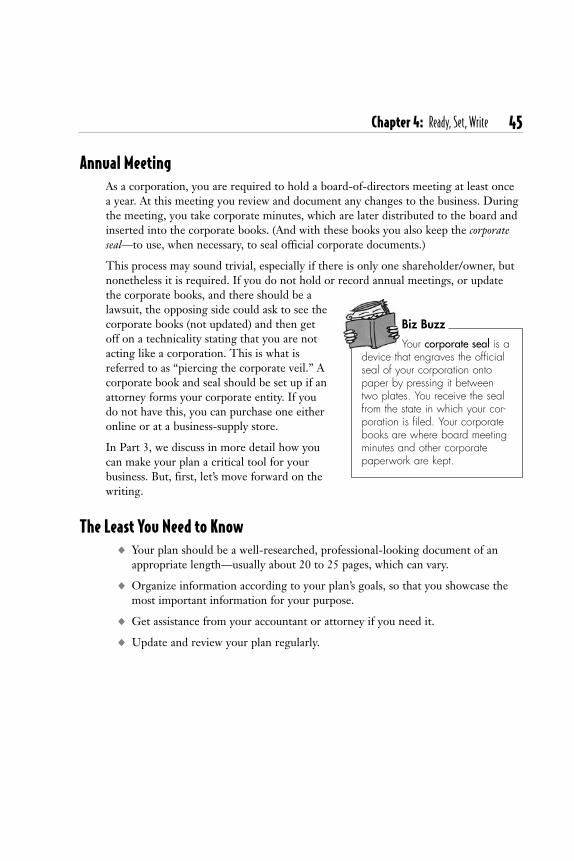

Staying Updated ........................................................................44Analysis ....................................................................................44Annual Meeting ........................................................................45

5 Getting Down to Business 47Getting Off on the Right Foot ..................................................48Title Page ....................................................................................50Table of Contents ........................................................................52Confidentiality Agreement ..........................................................52Executive Summary ....................................................................55Purpose ........................................................................................55

Business Description ..................................................................55Structure ..................................................................................55Owners ......................................................................................56Location ....................................................................................56Hours of Operation ....................................................................56Season’s Greetings ......................................................................56

What Is It? ..................................................................................57We’re on a Mission ......................................................................57

Mission Statement ......................................................................58Vision Statement ........................................................................58Values Statement ........................................................................59

6 Industry Overview 61Industrial Strength ......................................................................61Understanding Market Research ................................................62

Interviews ..................................................................................63Surveys ......................................................................................63Focus Groups ..............................................................................63Online Focus Groups ..................................................................64Observation ................................................................................64

Understanding the Industry ........................................................64Industry Life Cycle ....................................................................64

Industry Economics and Trends ................................................66Opportunities and Obstacles ......................................................67

Innovations ................................................................................67Regulations ................................................................................68Economic Factors ........................................................................68

vii

The Complete Idiot’s Guide to Business Plansviii

Price Comparisons ......................................................................69Location ....................................................................................69

Competition ................................................................................69Business Performance ..................................................................71

7 Who Are You? 75Internal Assets ..............................................................................76Owners and Partners ..................................................................76Staffing ........................................................................................77

Management Team ....................................................................77Outsourcing and Consultants ......................................................79

Employee or Contractor? ............................................................79Who Is an Independent Contractor? ............................................80Who Is a Common-Law Employee? ............................................80Who Is an Employee? ................................................................81Statutory Employees ..................................................................81Statutory Nonemployees ..............................................................82

Organizational Chart ..................................................................82Salaries ........................................................................................83Strategic Partners ........................................................................83Professional Resources ................................................................84

CPA ..........................................................................................84Attorney ....................................................................................84Bank ..........................................................................................84Insurance Professionals ..............................................................84Other ........................................................................................85

8 Analyzing Your Business in the Market 87Getting Down to Strategy ..........................................................88Targeting Your Customers ..........................................................89Demographic Profiles ..................................................................90

Income and Spending Habits ......................................................90Personal Characteristics ..............................................................90Standard of Living ....................................................................90Household Characteristics ..........................................................91

Getting Psychographic ................................................................91Opinions and Values ..................................................................91Political Views ............................................................................91Style and Taste ..........................................................................92

Contents ix

Defining Business-to-Business Customers ................................92Type of Business and Ownership ..................................................92Sector ........................................................................................92Geography ................................................................................93Psychographic Characteristics ......................................................93

Who Is Your Perfect Customer? ................................................93Why Do They Buy? ....................................................................95

Do They Need It or Want It? Can They Afford It? ....................95What’s Important to Them? ......................................................95For Whom Are They Buying? ....................................................95Who Are Your Customers’ Influencers? ......................................95Are They Brand Loyal or Price Driven? ....................................96How Do They Buy? ....................................................................96

Creating Profiles ..........................................................................96Innovators ..................................................................................97Thinkers ....................................................................................97Achievers ..................................................................................97Experiencers ..............................................................................98Believers ....................................................................................98Strivers ......................................................................................98Makers ......................................................................................99Survivors ..................................................................................99

Why You Shouldn’t Service Every Customer ............................99Evaluating Market Segments ....................................................100Defining Your Market Strategy ................................................101The SWOT Approach ..............................................................101

Strengths ................................................................................101Weaknesses ..............................................................................102Opportunities ..........................................................................102Threats ....................................................................................102

Predicting Market Share ..........................................................103

9 Getting the Word Out 105Positioning Your Business in the Market ..................................105Explaining Your Marketing Strategy ........................................106

Price ........................................................................................107Place (Distribution) ..................................................................107Promotion ................................................................................107

Putting Together the Marketing Plan ......................................113Being Clear About Goals ..........................................................114Planning the Action ................................................................114

The Complete Idiot’s Guide to Business Plansx

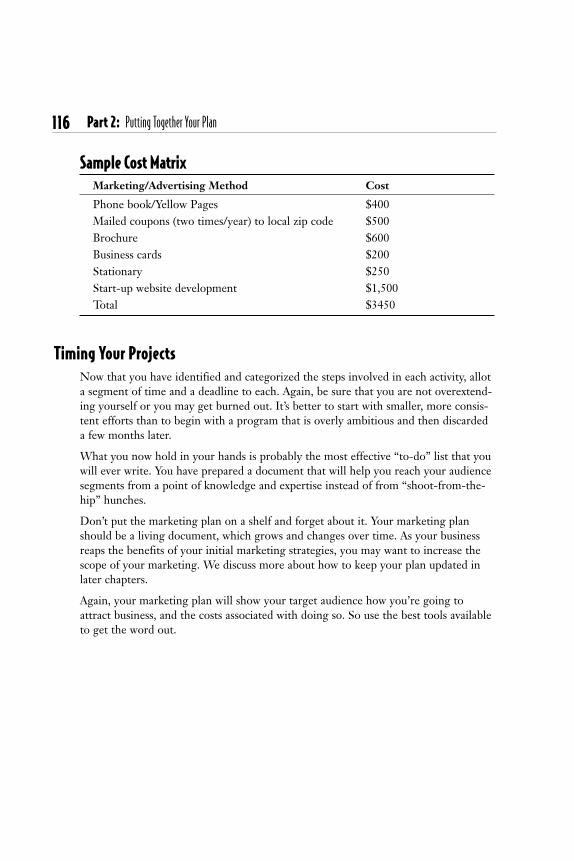

Budgeting Your Resources ........................................................115Creating a Marketing-Cost Matrix ..........................................115Timing Your Projects ................................................................116

10 Sales Plan and Forecast 119Selling Yourself ..........................................................................119Your Channels ............................................................................120

Direct Selling ..........................................................................120Manufacturer’s Representatives ................................................120Wholesalers ..............................................................................120Retailers ..................................................................................121Catalogs ..................................................................................121E-tailing ..................................................................................121Affiliate Programs ..................................................................121

Sales Tools ..................................................................................122Database ..................................................................................122Technological Tools ....................................................................122Trade Shows ............................................................................122

Territories ..................................................................................123Finding Prospects ......................................................................123

Referral Systems ......................................................................123Vendor Contacts ......................................................................123Expanding Existing Customers ................................................123Joining In ................................................................................124Offering a Better Price ............................................................124

Sales Cycles and Strategies ........................................................124AIDA ......................................................................................125Sales Cycle ..............................................................................125

Sales Forecast ............................................................................127Outlining Your Assumptions ....................................................127Considering Your Marketing Reach ..........................................127Past Sales or Similar Industries ................................................127

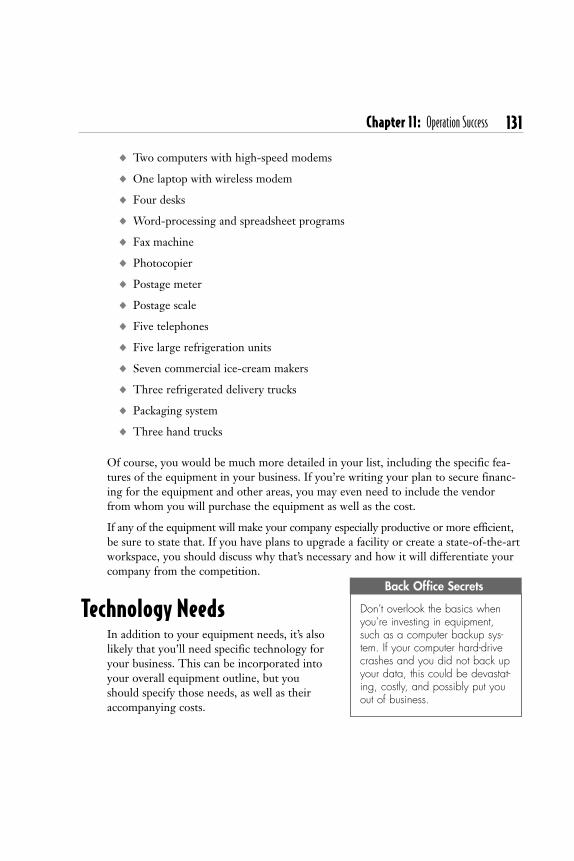

11 Operation Success 129Business Operations ..................................................................129Equipment ................................................................................130Technology Needs ....................................................................131Equipment Leases ......................................................................132Building Leases ..........................................................................132

Price ........................................................................................132Length of Lease ........................................................................133

Contents xi

Location and Traffic ................................................................133Potential for Growth ................................................................133

Utilities and Services ................................................................134Production/Service Provision Methods ....................................135Quality Control ........................................................................135Inventory and Supply ................................................................136

Managing Inventory ................................................................136Purchasing Policies ..................................................................137Suppliers ..................................................................................137Handling Orders and Deliveries ..............................................137

Vendor Agreements or Letters of Intent ..................................138Customer-Service Policies ........................................................139

12 Money, Money 141Start-Up Costs ..........................................................................142Creating an Operating Budget ..................................................143Source and Use of Funds ..........................................................144Managing Cash Flow ................................................................145Creating a Cash-Flow Statement ..............................................145Understanding Profit-and-Loss Statements ............................147Understanding the Balance Sheet ............................................149Determining Profitability with Financial Tools ......................151

Are You Profitable? ..................................................................151Break-Even Point ....................................................................152Outlining Repayment/ROI ......................................................152

Analysis of Financial Facts ........................................................153Determining How Much Financing Is Needed ..........................153How Much Owners Are Investing ............................................154

Insurance Needs ........................................................................154Cover Me ................................................................................155Prove It ..................................................................................156

13 Show Your Documents 159Back Me Up ..............................................................................159Resumés or Bios ........................................................................160Personal Financial Statements and Tax Returns ......................162Business Structure (Articles of Incorporation) ........................162Loans ..........................................................................................163Credit Reports ..........................................................................163Franchise or Acquisition Agreements ......................................163Leases or Mortgage ..................................................................164

The Complete Idiot’s Guide to Business Plansxii

Licenses ......................................................................................164Letters of Intent ........................................................................165Market Analysis ..........................................................................166Other ..........................................................................................166

14 Executive Summary 169In Summary ..............................................................................169What’s in the Executive Summary ............................................170Selling in Your Summary ..........................................................171

Company Overview ..................................................................171Operations Overview ................................................................171Market Overview ....................................................................172Financial Overview ..................................................................172

Paring It Down ..........................................................................173What Not to Put in the Executive Summary ..........................174

Part 3: Putting Your Plan to Work 17515 Financing Considerations to Include in Your Plan 177

The Money Plan ........................................................................178Who’s Got the Cash? ................................................................178What Lenders Want to See ......................................................179Knocking a Lender’s Socks Off ................................................180Negotiating Your Financing ......................................................181Types of Loans ..........................................................................182

Transaction Loans ....................................................................182Line of Credit ..........................................................................182Term ........................................................................................182Government-Secured Loans ......................................................183Lease ........................................................................................183

What to Expect During the Loan Process ..............................183Finding Investors ......................................................................185Money Online ............................................................................186What Investors Want ................................................................187Other Financial Uses for the Plan ............................................187

16 Using Your Plan as a Management Tool 189Planning to Run ........................................................................189Planning Findings ......................................................................190

Solidifying Your Philosophy ......................................................190Developing a Strategic Vision ..................................................190

Contents

Identifying Improvements ........................................................191Preventing Distractions ............................................................191Avoiding Misunderstandings ....................................................192

Implementing Your Plan ..........................................................192Providing Strong Leadership ....................................................192Stating Clear Expectations ......................................................193Creating Actionable Steps ........................................................193Being Ready for Barriers ..........................................................193

All Aboard ..................................................................................194Creating an Advisory Board ....................................................194Identifying and Building Relationships ......................................196Strategic Partners ....................................................................196

Staffing Up ................................................................................198Keeping Them Motivated ........................................................198Creating Employee Incentives ..................................................199Getting Employees Onboard with Your Plan ............................201

Managing the Future ................................................................202

17 Keeping Your Plan Current 205Keeping It Going ......................................................................205Measuring Your Company’s Success ........................................206Getting Information ..................................................................207

Your Financial Statements ........................................................207Your Customer Database or Sales Figures ................................207Your Employees ........................................................................208

What Do Customers Really Think? ........................................209Using the Information You Find ..............................................210When It’s Time to Go, It’s Time to Go ..................................210Going Forward ..........................................................................212

AppendixesA Business Terms Glossary 215

B Sample Plans 221

C Business Resources 301

Index 307

xiii

ForewordI have written dozens of business plans. I have read thousands of them. After almost20 years of building companies, I have come to realize that the actual business plan-ning document is almost always meaningless. That’s right. The final written productwe call “the plan” is actually almost worthless.

As a serial entrepreneur and angel investor, every business plan I ever read says the samething: “We get rich in year five.” Each plan states that this new company addresses a“billion dollar untapped market” and furthermore, its financial projections are “con-servative.” Let’s face it. These are both lies. If publicly traded companies are unable tounfailingly predict the financial goals they are able to hit next quarter, how can thenew business owner predict what business will be like in year two?

However, the process of researching and writing a plan for your business is valuable andessential to building a profitable company. President Dwight Eisenhower said, “I havealways found that plans are useless, but planning is indispensable.” A business plan that is notproperly researched or that is not regularly revisited and integrated into the company’soperations is useless. In business, as in most of life, things almost never happen theway we plan them. However, the actual process of considering all of the possibilities iscritical. It teaches you essential survival techniques at all phases of your business.

Stop searching for the perfect business plan format. There are no absolutely rightanswers. Don’t look for magic in pricey consultants. You need to write the first draftyourself because the process is a key learning step. Focus on the guidelines in thisbook as best you can. Write simply. Leave the cool buzz words and fancy jargon out.Build your projections from the ground up. Figure out what it will cost to make yourproduct or deliver your service. How will you acquire new customers? How muchbusiness can you expect per customer? When you consider these questions, is yournew business even feasible? These are some of the most valuable questions to answer!The work you do to find the answers is what matters, not how perfectly constructedthe final plan is.

After you have worked hard to put together the best plan you can, stop typing,researching, and surveying. Instead, get out of your chair and actually talk to peoplewho might be real customers and are in a position to buy your product or servicetoday. Are they willing to part with their cash to solve a problem they have? What isthe Unique Selling Proposition (USP) you can offer prospective customers? You willnot know the real answer until you ask someone to buy what you are selling.

Although planning is essential, premeditated business can be a dangerous thing. Ifyou create your plan and stick by it no matter what, you could doom your business to

failure by being inflexible. Write your plan, and revisit it regularly to change what’snot working. Too many small business owners set a goal and try to reach it no matterwhat. Sometimes, that tenacity is the backbone of their success. But sometimes, whenthey fail to see the signs that the goal might not be the best direction for the business,that lack of flexibility can be a business death sentence.

What do businesses need most? Not a perfectly written business plan, but a well-researched plan. Companies need enough cash to grow and thrive, which a good plancan help land. They need to manage that cash through constant analysis of cash flow.They need a management team that can execute the plan. They need a marketing anddistribution component so prospects can access the product or service. Finally, theyneed repeat customers and referrals.

Read this book. Write your plan. Keep talking to customers. And then modify yourplan to make the most of what’s working and to stop wasting effort on what’s notworking. These are the steps that will get your business off to a great start.

—Barry Moltz, www.moltz.com

Chicago, Illinois

June 2005

IntroductionThere’s no feeling like starting your own business. Opening a fresh box of businesscards with “Your Name, Owner” on them, or sitting in your brand-new office for thefirst time—it’s heady stuff and an achievement about which many only dream.

But you’re different. You’ve taken the plunge, or are making the plans to do so. Becauseyou’re holding this book in your hands, you’re also more likely than the average start-up to succeed.

Why? You’ve realized the critical importance of creating a business plan. Whetheryou’re in need of financing, or simply need a road map to guide your business, a well-prepared and properly targeted business plan will help you to achieve the goals thatyou’ve set for your business by documenting the goals, resources, and processes thatwill propel your business forward.

There’s an old adage that says, “Failing to plan is planning to fail.” That is nevermore true than when it is applied to a business plan. We have seen this phenomenonfirsthand, consulting with and counseling scores of businesses. Those ventures thatoperate without a solid game plan in place are much more at risk to fail than thosethat take the time to plan.

Because we’ve both been in the trenches as entrepreneurs, we know how valuable yourtime is. As we’ve written this book, we assume that you know the basics—how to choosewhich business is right for you, how to structure it, how to staff it, and the like. We’vewritten this book to show you how to take the facts about your business and put themon paper in a way that will interest lenders, business partners, or other decision-makers,and how to create a plan that will become a critical management tool for your busi-ness. So we’re going to dive into the nuts and bolts of crafting your plan. (If you doneed to brush up on start-up basics, be sure to read The Complete Idiot’s Guide toStarting Your Own Business, Fourth Edition, by Edward Paulson.)

And, again, because we have been entrepreneurs like you, we’ll share the best tips,secrets, and tactics that we’ve learned on our own. We know the amount of courage,resolve, and commitment it takes to do what you’re doing. We want to help you makethat investment pay off.

Who This Book Is ForThe Complete Idiot’s Guide to Business Plans is for anyone who is starting or acquiring abusiness and wants to go the extra mile to ensure its success. Whether you’re usingyour plan to map out management and marketing strategies or going after big bucks,we’ll show you how to put the best possible words and numbers on paper.

The Complete Idiot’s Guide to Business Plans

What You Need to Know Before You StartThe Complete Idiot’s Guide to Business Plans assumes that you’ve got basic businessknowledge. We won’t explain the nuts and bolts of how to run your business becauseyou already know the difference between a balance sheet and a budget.

We assume that you have a solid business idea or prospect in mind. This book takes youthrough the process of extracting the information you need in an acceptable business-plan format to secure financing or to strengthen your business operations, management,and marketing. Anytime you put a series of goals and objectives, as well as a plan forfulfilling them, on paper, you vastly increase the chances of achieving those goals andobjectives. That’s what we’ll help you to do.

While we recommend a format and order for the information, you may find that mix-ing up that order works best for your business. That’s fine. You’ll see in the samplebusiness plans that business plans come in many forms and formats. Write the planthat feels most comfortable for you and fulfills the purpose you need to achieve.

What You’ll Find in This BookThe Complete Idiot’s Guide to Business Plans is organized to walk you through the processof writing your business plan in a step-by-step sequence. Because there are some sec-tions that you’ll write out of order, we mention them within the sequence and thenpay more attention to them when you’re at the point at which you need to write it.

The book has four sections:

Part 1, “Getting Started”: This is where we give you the basics, a few facts that you’llneed to know, and a briefing of what you’ll need to write your plan more easily. We’vealso included a chapter on business-writing basics that will help you with some of thecommon issues of structure, composition, grammar, and punctuation that often plaguethose who don’t regularly write for a living (and that sometimes plague those who do).

Part 2, “Putting Together Your Plan”: Here is where the majority of the book’sfocus lies. We’ll walk you through the planning process, including how to set goalsfor your plan and how to write it to achieve those goals. Throughout, we’ve wovensections of real-life business plans to show you how it’s done.

Part 3, “Putting Your Plan to Work”: Once you’ve put your plan together, don’tjust put it on a shelf or in a drawer! In this part, we’ll show you how to make yourplan an important part of your business, how to keep it updated, and how to use it toobtain financing.

xviii

Introduction

Appendixes: This isn’t your garden-variety “stuff at the back of the book.” Our lastsection is chock-full of sample business plans from various types of businesses, rang-ing from retailers to consultants to manufacturing firms and more. Our glossary willbrief you on the terms you need to know, and our list of business resources will showyou where to turn for help, information, and advice.

Together, these four sections will tell you just about everything you need to knowabout writing a knock-their-socks-off business plan. And while we know that follow-ing these directions will leave you with a solid plan, it is our sincere hope that it willalso leave you with a better understanding of and vision for your business.

So let’s get ready to write.

How to Get the Most out of This BookTo get the most out of this book, read it through first and examine the sample busi-ness plans. You can also head online to examine other sample business plans to choosethe format that works best for you and your business.

Once you’re familiar with the content, use the book as a guide to help you write yourplan. By tackling each of the parts in this book, you can then use the order that wesuggest, or reorganize the information the way that you see fit, or in the way that’srequired by your lender, investors, or consultants. Either way, this book will help youget to the heart of the most important information more quickly.

In Part 3, we also address the issues of using your plan as a tool. No business plan isworthwhile if it just sits in a desk or on a hard drive. We show you how to make yourplan into a real tool for your business, as well as how to integrate it into your opera-tions to keep it current and relevant to your business.

Pay particular attention to the sidebars and margin notes, which include tips, warn-ings, secrets, and money-saving tidbits. These notes may be short in format, butyou’ll find great value in how they can shorten your learning curve and boost yourbottom line!

xix

Because time is money, thesetips will help save you both asyou write your plan.

Bottom Line BoosterIn business, mistakes

can cost you. These sidebars willgive you fair warning aboutpotential pitfalls to avoid.

Red Zone

The Complete Idiot’s Guide to Business Plans

Let Us Know What You ThinkFor updates on the book and additional information about small-business resources,visit Gwen Moran’s website (www.gwenmoran.com).

We welcome your feedback and success stories. If you have suggested resources or ifthis book has helped you, let us know at [email protected] or [email protected].

AcknowledgmentsWe’d like to thank the folks at Alpha Books, including the amazing team who workedon this book: Mike Sanders, Ginny Bess, Megan Douglass, Jan Zoya, and the produc-tion team. Thanks to our agent, Bob Diforio, for all of his help, support, and constantcontact through his Blackberry!

Gwen would like to thank her family and friends for their support, advice, and assis-tance in writing this book. Thanks to her parents, Thomas and Jeanice Moran, whoraised four individuals who are unafraid to open the door when opportunity knocks.Thanks to her brothers, Shaun, Brian, and Eric Moran, who are a great group ofbusiness advisors. And thanks to Joseph Raymond, who taught Gwen about the thingsthat are possible when we choose our own paths.

Thanks, also, to the many business owners Gwen has taught, with whom she’s worked,and about whom she’s written over the years—their spirit, tenacity, and energy nevercease to inspire her. And special thanks to the entrepreneur who shares her homeaddress—her husband, Henry Nonnenberg Jr.—and their daughter, Abigail.

Sue would like to thank her mother and late father, Susan and Albert Mahalske, foralways encouraging her by saying, “You can accomplish anything you want by puttingyour mind to it.” Thanks also to her loving husband, Bob Johnson, for supporting herthrough all of her crazy and wonderful ideas, ventures, and businesses, as well as toher two sons, Bobby and Chris, for all of their love and for being the wonderfulyoung adults that they are.

xx

The world of businessand writing business plans can beconfusing. These sidebars providedefinitions for the trickier terms.

Biz BuzzIn these sidebars, we’ll make youprivy to the tips, tricks, and little-known facts that will help youwrite your plan and run yourbusiness.

Back Office Secrets

Introduction

She would like to extend special thanks to Bill Harnden and Vicki Lynne Morgan fortheir time and input to some of the material in this book. Bill is the Assistant Directorof the Small Business Development Center (SBDC). After a long and distinguishedcareer in finance, he is currently employed at Raritan Valley Community College pro-viding financial counseling to many small businesses through the SBDC. Vicki Lynneowns Animal Brands, a marketing and sales representation agency, as well as RussmorMarketing Group, which focuses on private consulting, counseling, mentoring, andcoaching for businesses, and is an SBDC counselor.

Thanks to the great people she works with at SBDC and RVCC, especially Bill Harndenand Allison O’Neil for their team efforts and contributions, to their local SBDC, inassisting small businesses. Thanks, also, to the many wonderful small-business ownersshe has met and has had the opportunity to assist in their journey of pursuing theirdreams. Thanks, also, to Gwen for reaching out to her to co-author of this book!

A special thanks go to two very special businesses—Let’s Eat! started by owner DomenickCelentano and Stellar Academy started by two sisters, Mary Matthews and Dr. MargaretBuley—who have allowed us to use their business plans (modified for confidentiality) inthis book to benefit and assist other future small-business owners. Through the SmallBusiness Development Center, Sue Johnson had counseled with each of these businesses.

TrademarksAll terms mentioned in this book that are known to be or are suspected of beingtrademarks or service marks have been appropriately capitalized. Alpha Books andPenguin Group (USA) Inc. cannot attest to the accuracy of this information. Use of aterm in this book should not be regarded as affecting the validity of any trademark orservice mark.

xxi

1Here’s what you need to know before you begin drafting your plan, includ-ing the financial and basic company information you should have on hand.This part also includes a few tips on business writing basics. In Chapter 1, wediscuss plan basics, such as how your plan can help you run your businessas well as give you an overview of what you can expect during the process.In Chapter 2, we give you an overview of financing options and help youunderstand the financing needs of your business. Chapter 3 gives you ahead start on business writing basics to help make the process of writingmuch less intimidating.

Part

Getting Started

1According to Plan

In This Chapter◆ Entrepreneurship in the United States

◆ How your business plan can help you

◆ Your Unique Selling Point

◆ Do it yourself or get help?

You’re finally acting on that great idea you’ve had for ages. Or perhapsyou decided that you’ve just had enough of the commuter lifestyle andwant to start a business of your own, closer to home. Whatever the reasonyou’re starting or acquiring a business, you’re already further ahead thanmost because you understand the importance of a good business plan.Your business plan can be an invaluable management and financial tool,keeping your business on track and helping you to grow. But there are anumber of things you need to know before you start writing. So let’s dive in.

Business Owner BasicsEntrepreneurship is a big part of the American dream, and more people thanever are starting up their own enterprises as full-time ventures or as side-line operations. In 2003, there were approximately 23.7 million businesses

Chapter

Part 1: Getting Started

in the United States, according to the Small Business Administration (SBA). Of those,572,900 were brand new.

In fact, each year, hundreds of thousands of businesses open their doors, includingstart-ups, acquisitions, and franchises. Major factors that determine whether a companyremains viable include an ample supply of capital, sizable enough to have employees,

the owner’s education level, and the owner’s reasonfor starting the business in the first place, such asfreedom for family life or the desire to be one’s ownboss. The companies that had the clearest sense ofpurpose—and a solid plan for survival—are the onesthat are still open today. The plan for survival is mosteffective when it takes the form of a written businessplan.

Beyond the organizational benefits, business plans can offer a financial benefit as well.More than 75 percent of small firms use some form of credit in their start-up or opera-tions. Companies use many different sources of capital, including their own savings,loans from owners’ family and friends, and business loans from financial institutions.Credit cards, credit lines, and vehicle loans are the most common types of credit. Someother business owners turn to commercial banks, who are the leading suppliers of credit,followed by owners and finance companies. Some businesses turn to venture capital.

Whatever the form of financing, the lender will want to see a solid business planbefore making loans available to your business. In the upcoming chapters, we helpyou present your business in the best possible way, which can make the differencewhen you’re trying to secure financing or credit for your business.

Types of Business PlansBusiness plans come in several varieties, and it’s important to know why you’re writingthe plan before you begin. A business plan can range from about 5 pages to 60 or morepages, although an average business plan usually falls in the range of 20 to 30 pages.If you’re writing a business plan to attract capital, then your plan may be longer andfilled with more documentation than if you’re using it as an internal managementtool. The length and form of your business plan depends on you and your goals foryour business. The following sections look at some of the common varieties of busi-ness plans.

4

An entrepreneur issomeone who launches a for-profit venture or business.

Biz Buzz

Chapter 1: According to Plan

Securing Financing or InvestorsPlans with financial goals place heavy emphasis on the business numbers—what are itssales, assets, projected revenue and income growth, and other factors that make thebusiness a good financial risk? Lenders and investors want to be sure that their invest-ment will be worthwhile, so you’ll want to put your best foot forward, emphasizingyour management strengths, financing plan, profit margins, and potential sales growth.

Strengthening OperationsIf your plan will be used as an internal tool to help you grow your business, you’ll wantto spend more effort examining how the business is structured, how products andservices are delivered, and how the company markets itself. That way, you can fullyoutline and measure the success and growth of your business, beyond the bottom line.

Preparing for a SaleIf you are looking for a way to sell your company, a business plan can help you streamlineoperations and find flaws that might make your business less attractive to potentialbuyers.

If your business is a partnership, you have toclearly lay out your expectations for the saleof the business, including the selling priceand how the proceeds are to be divided. It’s agood idea to consult an attorney to execute apartnership agreement or buy/sell agreementthat spells out these details.

How Can a Plan Help?The good news is that a thorough business plan can help you avoid many of the commonchallenges that new businesses face. How? A business plan is a road map of your busi-ness, both in context and in financial terms. A written business plan is an extremelyimportant tool for any business. It can be used to provide analysis and milestones forthe business owner. It serves as a means of communication with accountants, attorneysand others, and as preparation for financial needs and loans. It also acts as an iterativeprocess of a working plan for your ongoing business.

5

A partnership agree-ment is a document that outlinesthe terms and conditions of twopersons or entities entering into abusiness agreement.

Biz Buzz

Part 1: Getting Started

Writing a business plan enables you to assemble all of the components of your busi-ness together and document them. This process will ensure that you’ve considered themajor aspects, expenses, and revenue potential of your business, as well as the staffing,location, and other needs it will have. It will also help you determine the long-termoutlook and help you decide whether this is an endeavor that will fit your lifestyle.

After you have written a business plan, it can serve as a guide for your business’sprogress. With constant review and updates of the plan, it will give you a solid basison which to make decisions, implement changes, and take action. As your businessprogresses, you will continue to learn more facts that can be implemented into yourplan. Some of the purposes that your business plan can serve are discussed in moredetail in the following sections.

Establishing a Vision and DirectionYour business plan requires that you document what your vision is for your business.It’s a blueprint that takes the resources with which you’re starting, adds the experienceof the key players and the strategy for making the business work, and filters all of thatthrough the financial realities of the business. Done right, it’s a way to test the businesson paper before making a significant investment of time and money in a new venture.

Keeping on CourseYour business plan can also act as a compass, keeping you on the path that you origi-nally set for your business. All too often, businesses get sidetracked from their coremissions, leading to a slowdown in growth because resources are diverted to otherefforts. Your business plan can serve to remind you of exactly how your goals shouldbe focused.

Setting Goals and Benchmarking SuccessYour business plan will help you set the short- and long-term goals that will bench-mark the progression of your business. By putting these goals down on paper andexplaining how they will be accomplished, you map out the steps you need to take tomake your business successful.

Your business plan will also have projections about growth, revenue, and accomplish-ments. You can use these projections as measurements, to determine how well yourbusiness is performing. If you find that your business consistently fails to meet the

6

Chapter 1: According to Plan

goals that were set, then it’s a sure sign that you either need to ramp up some of thesectors of your business or you need to take a look at the measurement mechanismsyou’ve put in place to determine if they are realistic.

Outlining OperationsA large portion of your business plan will be devoted to the operations of your busi-ness, or how it will work. Who will be responsible for various business functions andhow will the work get done? Outlining these responsibilities on paper may show youwhere improvements could be made, where you can save money and time, and ifyou’re overlooking a key component of how your business will get its tasks done.

Fiscal FitnessAs noted earlier, another key factor of a business plan is to obtain money from debt(lenders) or equity (interest in the company) funding. Your business plan is your keyto convincing a lender that you have a viable business idea in which they shouldinvest. These money gatekeepers look for research—facts, figures, and demographics.However, they also look for intangibles, such as ingenuity, dedication, and manage-ment experience. So it’s critical that you include all of your assets, knowledge, andexpertise in this document. The more complete the business plan, the more likely youwill obtain funding.

Your business plan can also serve as a working budget, to ensure that income is spentproperly. Sure, it would be great to rent prime space and spend thousands on luxedécor for your new office. And when you get a fat check from a lender, it can betempting to splurge on a few things. However, by outlining the cash flow that will bethe lifeblood of your business, you’ll be less tempted to take money that should gotoward growth rather than spend it on a too-lavish grand-opening party.

Checking the EgoStarting your own business can be a heady experience. Suddenly, you’re the boss, andyou may have employees who rely on you to be their leader. You’re the one responsi-ble for decisions for a business that is largely the result of your talent and ability.With so many people turning to them for answers, many entrepreneurs get caught upin thinking that they know it all. A business plan helps you to understand the realitiesof your business and helps you stay focused on what needs to be done in the bestinterest of growing your venture.

7

Part 1: Getting Started

Thorough ResearchThe process of writing a business plan will mean that you’ll need to do the necessaryhomework. That means researching your business idea and the marketplace to see ifthey’re a good fit. Research can take many forms and range from studying data fromtrade associations to conducting your own market research by talking to potentialcustomers, vendors—and even competitors.

If you ignore the research component of starting your business, you do so at yourperil. A business plan that saves you from a business that fails because it was neverviable in the first place is also a successful plan.

Marketing PlanThe marketing component of your plan will set a clear course for getting the wordout about your business, products, and services. Beyond that, your marketing planwill determine how your product is positioned, priced, and distributed, relative toyour competition’s, giving you more insight into how your business will be successful.

FeasibilityThroughout your plan, you’ll be reinforcing why your business is a good idea, wherethe market for your products and services will be, and, overall, how feasible yourbusiness really is. While some businesses simply hang a shingle and call themselveslaunched, your plan will force you to think through exactly how your business will besuccessful and exactly why people or businesses will want to become your customers.

Future ExpansionYour business plan will explore how and when youwill grow your business, including the staff, facilities,and revenue that you’ll need to do so.

Exit StrategyBecause no one can run a business forever, goodbusiness plans also include exit strategies—gameplans for leaving the business or selling it. Investorsneed to know the business will have longevity afterthe entrepreneur leaves for any reason.

8

Many people use rev-enue and income interchange-ably, but they are actually twodifferent things. Revenue is yourgross income, before any deduc-tions. Income refers to the amountof money that remains after yourbusiness expenses, but beforeincome taxes are paid.

Biz Buzz

Chapter 1: According to Plan

Your USPIn the context of your business plan, you also need to show your unique selling propo-sition, or USP. Focusing on developing a USP isn’t a new concept, but it’s a criticalone. Setting your business apart from the competition means having a strong plat-form to do so. If you can’t articulate why customers should buy from your companyand not your competitors’, then you’re going to run into problems in selling yourself.

Without a strong differentiation that makes your company the clear choice, you’llfind yourself often competing on price or constantly having to settle for customersthat might not be the best fit for your company (or the selling cycle—the time framein which you sell your products or services—will be vastly increased!).

So what qualifies as a unique selling point? Following are some qualifications:

◆ New: If you’re first to market, then you have a unique selling point by default—no one else does what you do.

◆ Improved: If you can clearly state how you’ve improved upon the existing prod-ucts or services in your sector, then you have a strongly unique selling point.

◆ Convenience: Does your offering save people time or effort? If your product orservice is more convenient to use or provides some savings of time or effort, thatcan be a strongly unique selling point.

◆ Specialization: Is your product or service better for a specific niche of the mar-ketplace? For instance, are your widgets manufactured for industrial use or isyour service better suited toward more established businesses?

◆ Better quality: Do you do what you do better than the competition? Qualityconsistently ranks ahead of price in surveys of why customers buy. So if yourproduct is more durable, your service more reliable, or you’re otherwise headand shoulders above the competition, let your customers and prospects know.

Finding Your USP Through FeedbackA good way to determine what your unique selling points are, if you’re already inbusiness, is to ask your customers. Institute some mechanism, such as a survey thatdetermines their level of satisfaction, to gather their feedback and ask them why theybuy from you. It’s usually better if you gather the information through some sort ofanonymous means. For instance, you can conduct surveys at checkout counters, or

9

Part 1: Getting Started

send surveys in the mail after the client buys from you, as you’ll get more reliable datathat way. Some ways to do this include the following:

◆ Sending a survey to customers with an incentive to return the survey, such as adiscount coupon or chance of being entered into a drawing for a worthwhile gift.

◆ Including a short questionnaire with monthly invoices.

◆ Creating a suggestion box—this could be a physical drop-box or an anonymousform on your website.

Another idea is to teach employees to make note of anecdotal feedback that customersrelay. For instance, if a customer says that a new display or service works really well,have a method of capturing that information. It could be as simple as a notebook inwhich these sorts of comments can be recorded. For more technical-savvy businesses,an e-mail report or entry into a shared database or contact management program canbe more effective.

Look for ways that you interact with your customers and try to integrate short, non-invasive methods of information gathering.

The key to successful gathering of feedback is to keep questionnaires and surveys to amanageable length. This varies depending on your type of business, but the generalrule is that shorter is better—five to six questions is ideal. Use a format of both multiple-choice and open-ended questions for best results.

Doing It Yourself or Getting Help?There are a number of business-plan writing services out there, as well as business-plantemplate software. Should you hire someone, or use software to write your plan for you?

We don’t think so—at least not for the first draft. Theprocess of writing your plan is an exercise that willhelp solidify the direction of your business. By goingthrough the process yourself, even if you’re not agood writer, you’ll be forced to think through variousscenarios and learn more about how your business willrun, market, staff, and grow. By hiring someone to dothat for you, you’ll lose out on the benefits gainedfrom that process. However, if you’re not confident in

10

If your plan needs an editorialonce-over, hire a business orcommunications student to helpyou fine-tune it. The student willget valuable resumé fodder

and you’ll get the benefit of abudding wordsmith who can putyour ideas into captivating prose.

Bottom Line Booster

Chapter 1: According to Plan

your writing skills and feel like you need someone to edit your plan before it goes tolenders or equity partners, it’s fine to hire someone for the final draft.

Finding Free or Low-Cost HelpIf you are still skittish about tackling your business plan on your own, you may wantto consider getting some help. There are a number of resources to which you can turnto get that help for free (or almost free). If your plan needs just a bit of a kick-start,there are plenty of low- or no-cost resources to turn to for help. Try one of the fol-lowing:

◆ Check out your local Small Business Development Center, which can providefree and confidential counseling with assistance and review of your businessplan, as well as many other free counseling services to existing and beginningbusinesses. These services cover marketing, financing, and much more. Visitwww.asbdc-us.org for the center nearest you.

◆ Call SCORE (Counselors to America’s Small Business), which offers free coun-seling to start-up or established business owners. Find out more at www.score.org.

◆ Visit the U.S. Small Business Administration online at www.sba.gov for a varietyof small business information, suggestions, and tips offered in English and inSpanish.

◆ Contact your local college. If you can offer a meaty assignment, you may be ableto attract a business student to intern with your company in exchange for creditor a small stipend. If not, see if the college has a business club that can help.

◆ Virtually all industries and professions have trade associations. These associa-tions offer assistance, statistics, and research that can help you refine your busi-ness plan ideas. Visit the association’s website or call for help.

Hiring HelpIn addition to low-cost help, there are others who can help you write a business plan.Remember that bigger isn’t necessarily better. Don’t be seduced by a “big name” con-sulting firm, especially if your business is small. Instead, consider hiring a freelancewriter or marketing consultant, rather than a management-consulting firm. In mostcases, the soloist’s fees will be more affordable than hiring a company with lots of over-head. To save even more money, write the first draft yourself and hire a copyeditor orfreelance writer to polish up the grammar and language.

11

Part 1: Getting Started

Other tips for hiring providers include the following:

◆ Seek recommendations. Ask other business owners who they would use or callyour local Chamber of Commerce or business association.

◆ Interview a few. Speak with more than one provider to get a sense of pricing andservice levels.

◆ Get and check references. Don’t just settle for an impressive list of clients—choose specific companies from that list to call, instead of just settling for thereferences that are offered. And do call—you’ll sometimes be surprised at whatthe references really have to say!

◆ Review samples. Business plans are proprietary, so the professional may not beable to share other plans (be wary if he or she does). However, you should stilllook at the provider’s portfolio. Does it suit your style? Oftentimes writing willbe somewhat subjective—if you don’t like how the provider’s previous worklooks or reads, chances are that you won’t like what he or she will do for you.

Getting SoftThere are a number of business-plan software packages on the market today. Thesepackages will lead you step-by-step through the process of writing your plan. Some ofthe more popular packages include these:

◆ Business Plan Pro 2005 by Palo Alto Software (www.businessplanpro.com)

◆ Plan Write by Business Resource Software (www.brs-inc.com)

◆ Biz Plan Builder by Jian Tools for Sales (www.jian.com)

12

If you hire a writer to complete your plan, he or she should have business planexperience, as well as a thorough understanding of how a business plan is constructed.Because business plans are proprietary, the writer may not be able to show you otherplans that he or she has written. However, the writer should be able to produce at leasttwo appropriate writing samples. In this case, it really pays to check references.

Red Zone

Chapter 1: According to Plan

◆ Business Plan 12.0 by Out of Your Mind … And Into the Marketplace(www.business-plan.com)

◆ Anatomy of a Business Plan by Linda Pinson (www.business-plan.com/anatomy.html)

This list doesn’t constitute an endorsement, and we think that you can write yourbusiness plan just fine without spending the money on software. However, these pro-grams do make formatting convenient by providing step-by-step, fill-in-the-blanktemplates for writing a plan. The trouble is that your plan will look like that of every-one else who used the software. The choice is yours—it may save you some time, butonly you will know whether the software is worth it.

In this chapter, we covered the basics of why you need a plan. As we move forward,we’ll walk you through the process of putting the plan together. Take a deep breath—and let’s go!

The Least You Need to Know◆ Businesses that have a solid business plan succeed more frequently than those

that do not.

◆ Revenue is not the same as income.

◆ A business plan can help you secure financing, grow your business, or accom-plish other goals.

◆ Write your business plan yourself to get the most out of the process. Hire some-one to help you clean up the prose later—for much less expense than writing itfrom scratch.

◆ Business-plan software can be a great convenience or an unnecessary expense,depending on your writing skills. Check out whether it will work for you beforeyou spend your money.

13

2Figuring Out the Financing

In This Chapter◆ Equity versus debt financing

◆ Types of financial resources available

◆ Types of lenders and investors

◆ What lenders want

◆ Understanding credit

Whatever the purpose of your plan, the financing portion will be animportant part of it. You’ll need to figure out how much money it willrealistically take to start or acquire your business, as well as how muchmoney you’ll need to sustain it until it becomes profitable.

It’s easy to underestimate the amount of money you’re going to need—andthat’s a major reason why many businesses fail. Undercapitalization willconstrict your cash flow and limit the opportunities you have to grow yourbusiness. You will also need enough money on the personal side to carryyou through the start-up phase. Sometimes business owners run out ofcash to cover their own expenses even when the business is viable.

In later chapters, we discuss the specific financial statements that you’regoing to need to develop. In this chapter, we address the broader strokesof making your plan appealing to financiers.

Chapter

Part 1: Getting Started

Understanding Debt and EquityAs you examine the capital needs of your business, and consider using your plan toobtain that capital, you’ll first need to understand the two primary forms of financing:debt financing and equity financing.

DebtDebt financing means that you obtain money from a lender at a certain interest rateand term and then have to repay a set amount that includes interest and any fees thathave been added to the principal amount. When you borrow money, the lender hasno ownership stake or say in the decision-making processes, and you keep control ofyour business.

EquityEquity financing is when an investor purchases a part-ownership of your business inexchange for a certain amount of money. The investor and the business owner usuallydecide on the parameters of ownership rights to which the investor will be entitled.The biggest concern here is that investors usually want substantial control and inputin the business to ensure that the business will be successful and get the type of returnon their investments that they anticipate. Of course the negative is that you lose con-trol over what you thought was your business. Just be careful with the negotiations.In addition, the investor usually maintains a percentage ownership stake in the busi-ness, and may be entitled to a percentage of profits from the business, which is theinvestor’s return on investment.

The investor usually wants a buyout point that is stated up front, because they arelooking for a return on their investment over a certain period of time. The period oftime can differ between businesses and industries, but frequently it is less than five years.

Money SourcesWhen you’re looking for money to launch your business, there are a number ofoptions available, depending on the type of business you want to start, the collateralyou have, and the amount of money you wish to borrow. These include grants, per-sonal resources, savings, credit cards, and several different types of loans.

16

Chapter 2: Figuring Out the Financing

GrantsDespite some infomercials that tout the availability of grants for virtually any business,grants for garden-variety ventures such as hair salons or restaurants are actually rela-tively rare. Sometimes you can find special one-time grants online, if you regularlysearch around, but that may require more than a bit of luck.

Still, if you find a grant that matches your business venture, by all means apply for it.Grants are terrific because they don’t need to be repaid as long as you fulfill the obli-gation that you set forth when applying for the grant. The searching and applying canbe time-consuming, however, and often grant matches are not found.

More commonly, grants are available for bio-life science and high-tech businesses, oftenoffered through various states to cultivatethose types of businesses. Federal grants forthese types of companies are offered throughthe Small Business Innovative Research(SBIR) and Small Business TechnologyTransfer (STTR) programs. Both govern-ment programs seek innovative and uniqueideas. If your business qualifies, it couldreceive a grant for as much as $750,000 forthe start-up phase and up to $1 million forthe growth phase.

Personal ResourcesMost lenders and investors want to see that you’ve invested some of your own resourcesin the business. After all, if your money is on the line, you’re more likely to be cautiousabout risking that investment. The following sections discuss some of the personalresources that bootstrapping entrepreneurs have used to start and fund their ventures.

SavingsPersonal savings, including money in savings and checking accounts, CDs, mutualfunds, and other investment vehicles, are often tapped for new ventures. The benefit isthat there is no interest due on this money, but you also want to be careful that youdon’t jeopardize your ability to pay personal expenses, such as mortgage, car, creditcard, and other payments, not to mention having a few bucks left over for groceries,clothes, and other essentials.

17

Because navigating the government-grant process can be tricky, youmight want to seek help from yourlocal Small Business DevelopmentCenter (SBDC). SBDCs throughoutthe nation have consultants whocan assist you with the applicationprocess. For SBDC locations nearyou, go to their national websiteat www.asbdc-us.org.

Back Office Secrets

Part 1: Getting Started

Home-Equity Loans or Lines of CreditA number of entrepreneurs have borrowed against their largest assets—their homes—in order to fund their businesses. This is a surefire way to get cash, and the interestmay be tax-deductible; however, you need to be sure that you’re going to be able torepay this additional loan on your home, or you could end up losing it.