TDS Provisions For Payment to Non -residents - wirc … on payment to non-residents...Sec.197...

68

TDS Provisions For Payment to Non-residents Presented for: ICAI – WIRC By Mr. Kuntal Dave On January 29, 2011 At J. S. Lodha Auditorium, ICAI Bhawan, Cuffe Parade.

Transcript of TDS Provisions For Payment to Non -residents - wirc … on payment to non-residents...Sec.197...

TDS Provisions For Payment to Non-residentsto Non-residents

Presented for: ICAI – WIRCBy Mr. Kuntal Dave

On January 29, 2011At J. S. Lodha Auditorium, ICAI Bhawan, Cuffe

Parade.

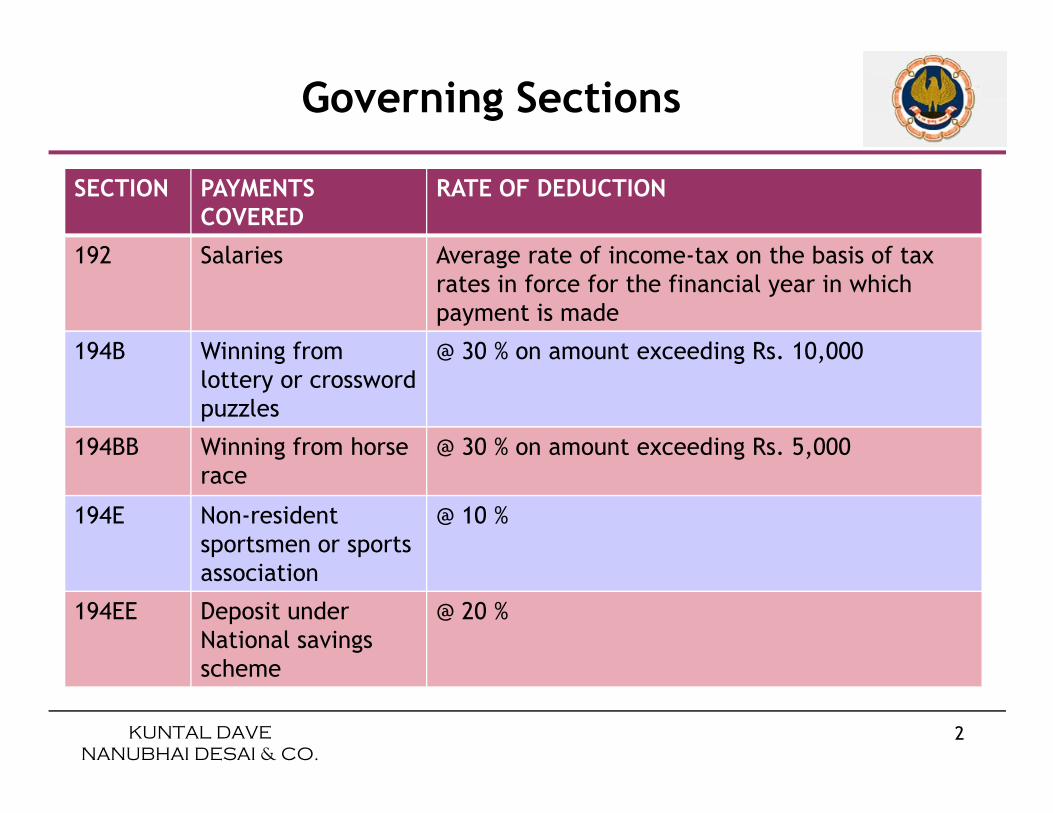

Governing Sections

SECTION PAYMENTS COVERED

RATE OF DEDUCTION

192 Salaries Average rate of income-tax on the basis of tax rates in force for the financial year in which payment is made

194B Winning from lottery or crossword puzzles

@ 30 % on amount exceeding Rs. 10,000

KUNTAL DAVE

NANUBHAI DESAI & CO.

2

puzzles

194BB Winning from horse race

@ 30 % on amount exceeding Rs. 5,000

194E Non-resident sportsmen or sports association

@ 10 %

194EE Deposit under National savings scheme

@ 20 %

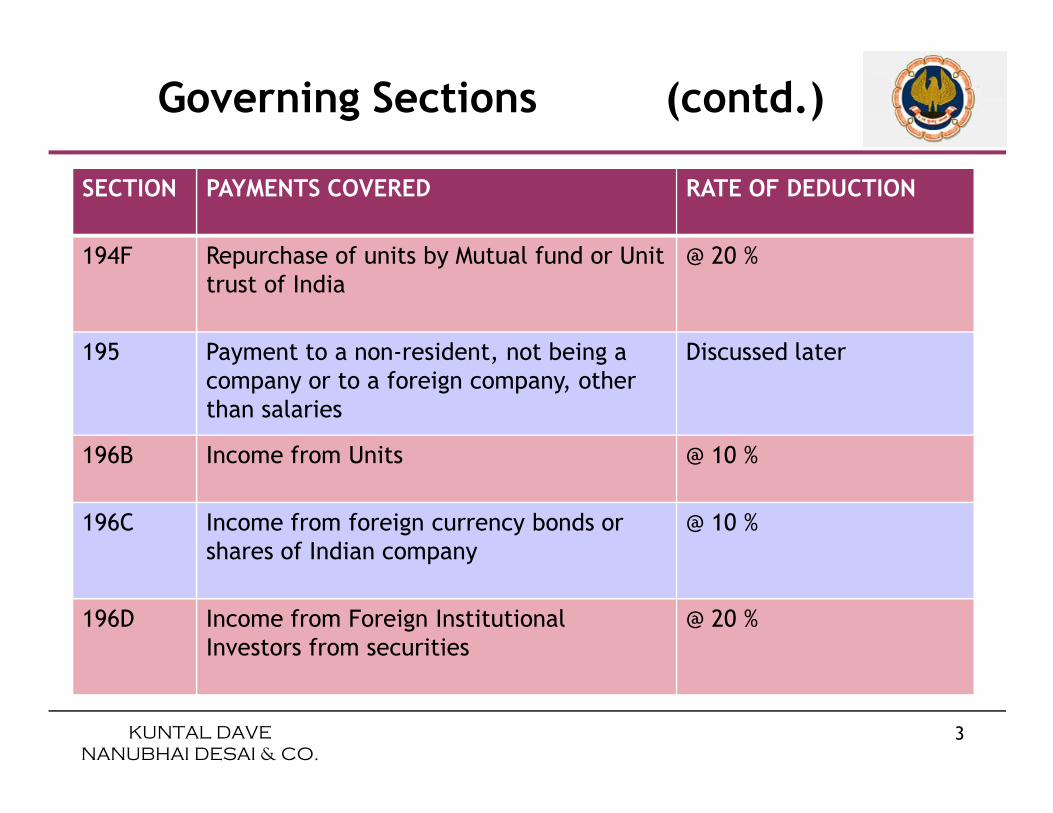

SECTION PAYMENTS COVERED RATE OF DEDUCTION

194F Repurchase of units by Mutual fund or Unit trust of India

@ 20 %

195 Payment to a non-resident, not being a company or to a foreign company, other than salaries

Discussed later

Governing Sections (contd.)

KUNTAL DAVE

NANUBHAI DESAI & CO.

3

than salaries

196B Income from Units @ 10 %

196C Income from foreign currency bonds or shares of Indian company

@ 10 %

196D Income from Foreign Institutional Investors from securities

@ 20 %

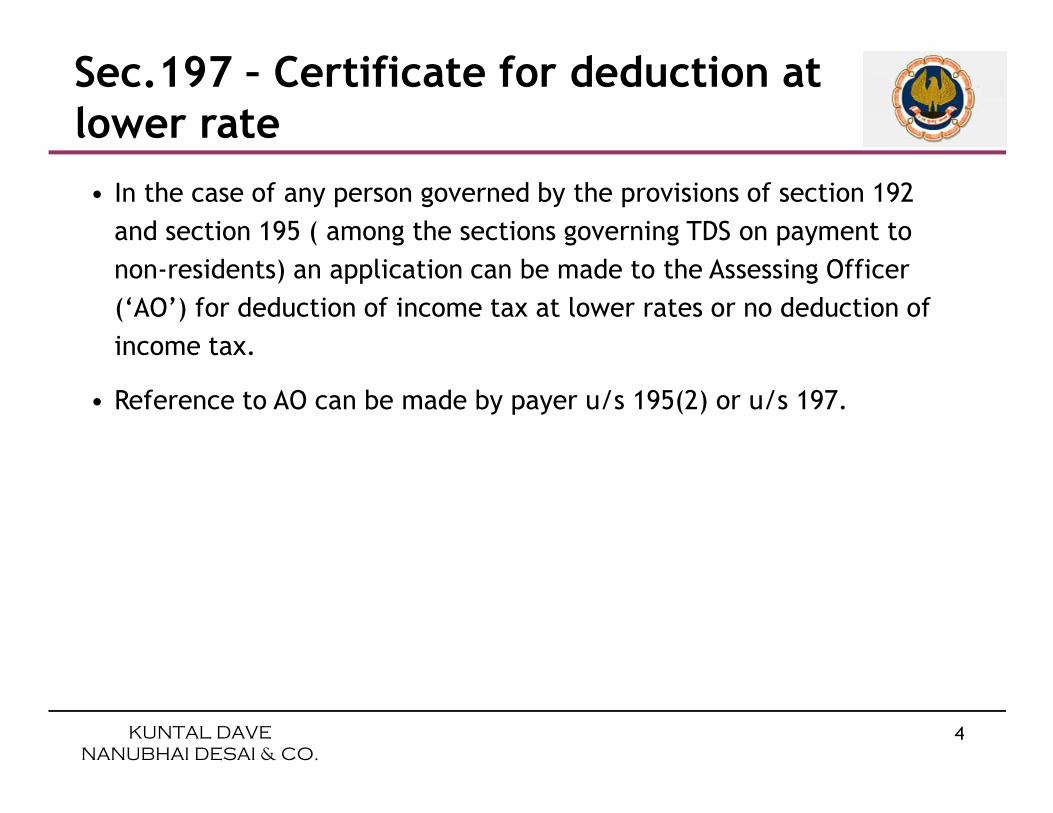

Sec.197 – Certificate for deduction at lower rate

• In the case of any person governed by the provisions of section 192

and section 195 ( among the sections governing TDS on payment to

non-residents) an application can be made to the Assessing Officer

(‘AO’) for deduction of income tax at lower rates or no deduction of

income tax.

• Reference to AO can be made by payer u/s 195(2) or u/s 197.

KUNTAL DAVE

NANUBHAI DESAI & CO.

4

• Reference to AO can be made by payer u/s 195(2) or u/s 197.

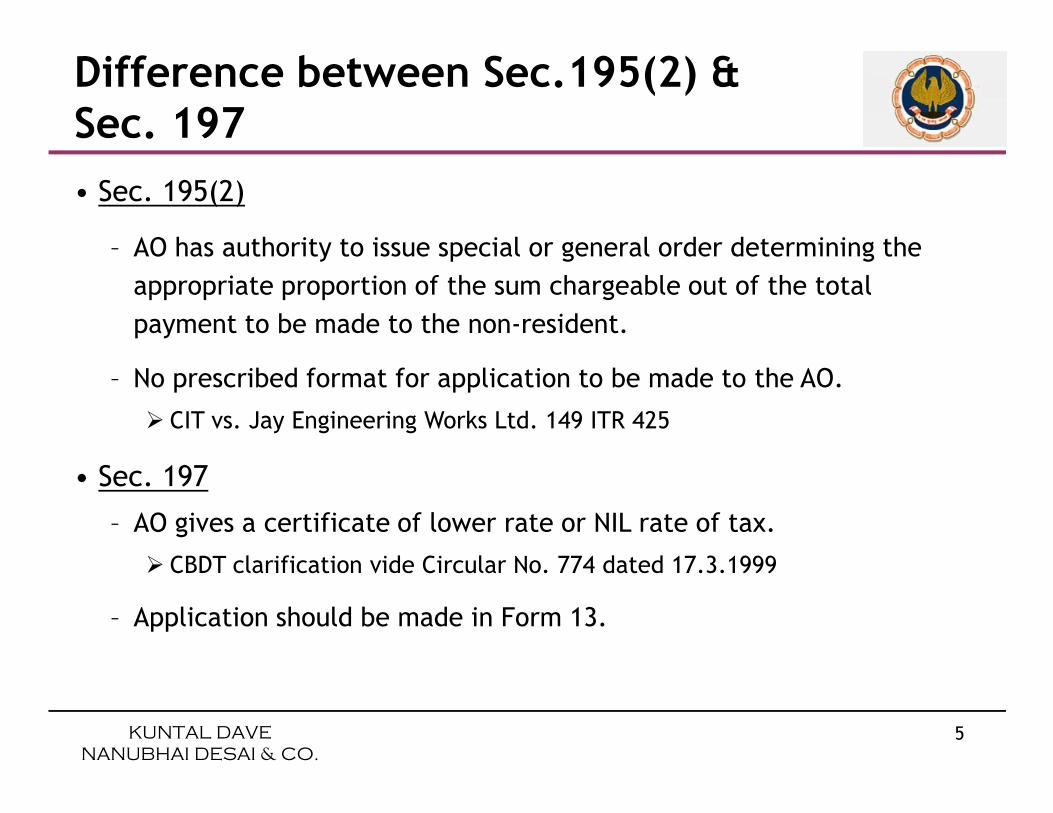

Difference between Sec.195(2) & Sec. 197

• Sec. 195(2)

– AO has authority to issue special or general order determining the

appropriate proportion of the sum chargeable out of the total

payment to be made to the non-resident.

– No prescribed format for application to be made to the AO.

� CIT vs. Jay Engineering Works Ltd. 149 ITR 425

KUNTAL DAVE

NANUBHAI DESAI & CO.

5

� CIT vs. Jay Engineering Works Ltd. 149 ITR 425

• Sec. 197

– AO gives a certificate of lower rate or NIL rate of tax.

� CBDT clarification vide Circular No. 774 dated 17.3.1999

– Application should be made in Form 13.

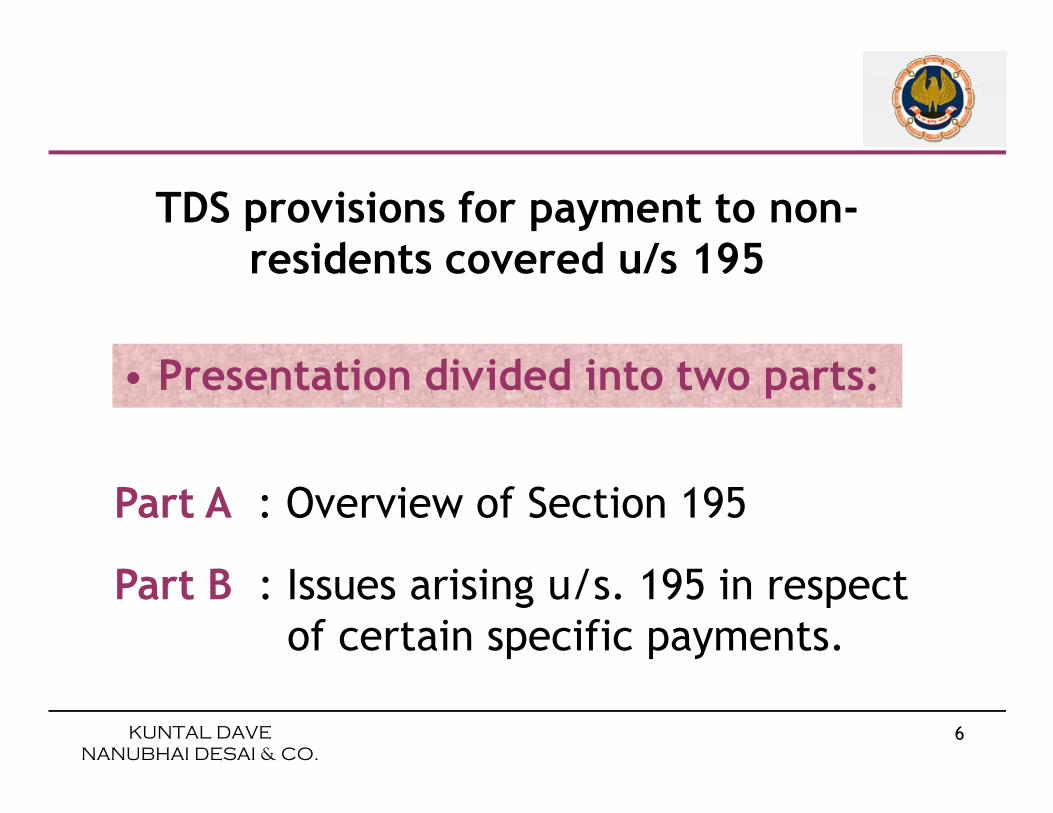

• Presentation divided into two parts:

TDS provisions for payment to non-residents covered u/s 195

KUNTAL DAVE

NANUBHAI DESAI & CO.

6

Part A : Overview of Section 195

Part B : Issues arising u/s. 195 in respect of certain specific payments.

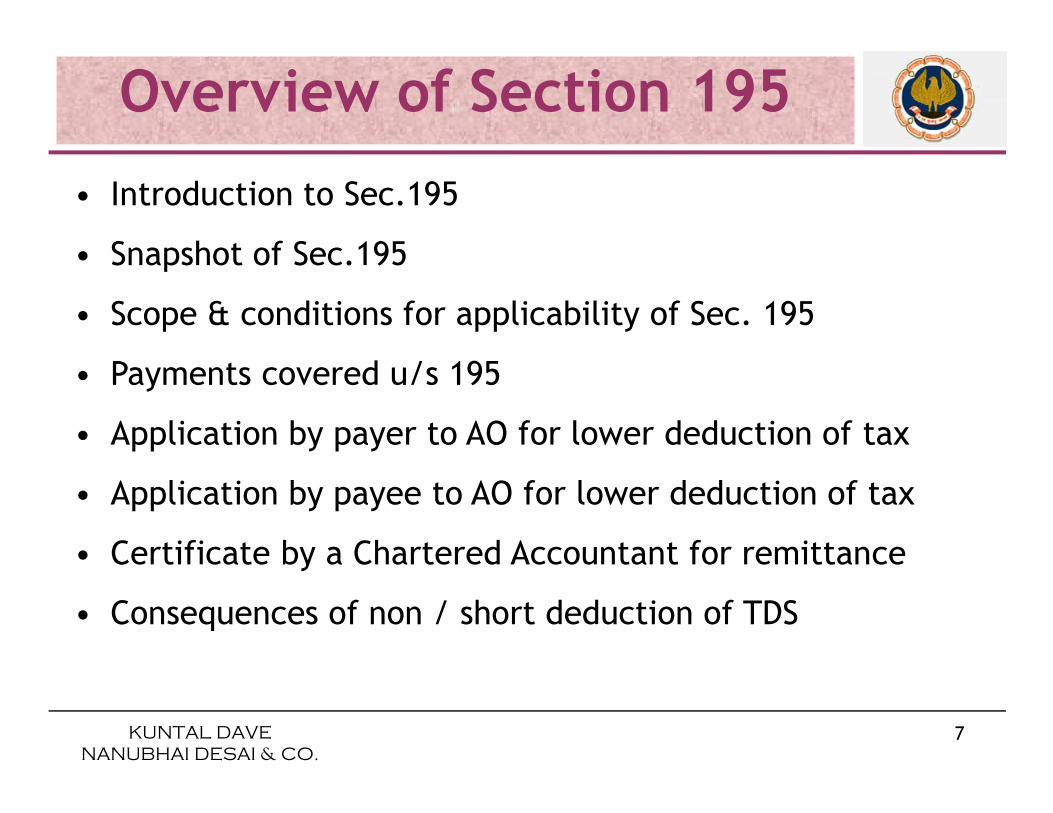

Overview of Section 195

• Introduction to Sec.195

• Snapshot of Sec.195

• Scope & conditions for applicability of Sec. 195

• Payments covered u/s 195

KUNTAL DAVE

NANUBHAI DESAI & CO.

7

• Application by payer to AO for lower deduction of tax

• Application by payee to AO for lower deduction of tax

• Certificate by a Chartered Accountant for remittance

• Consequences of non / short deduction of TDS

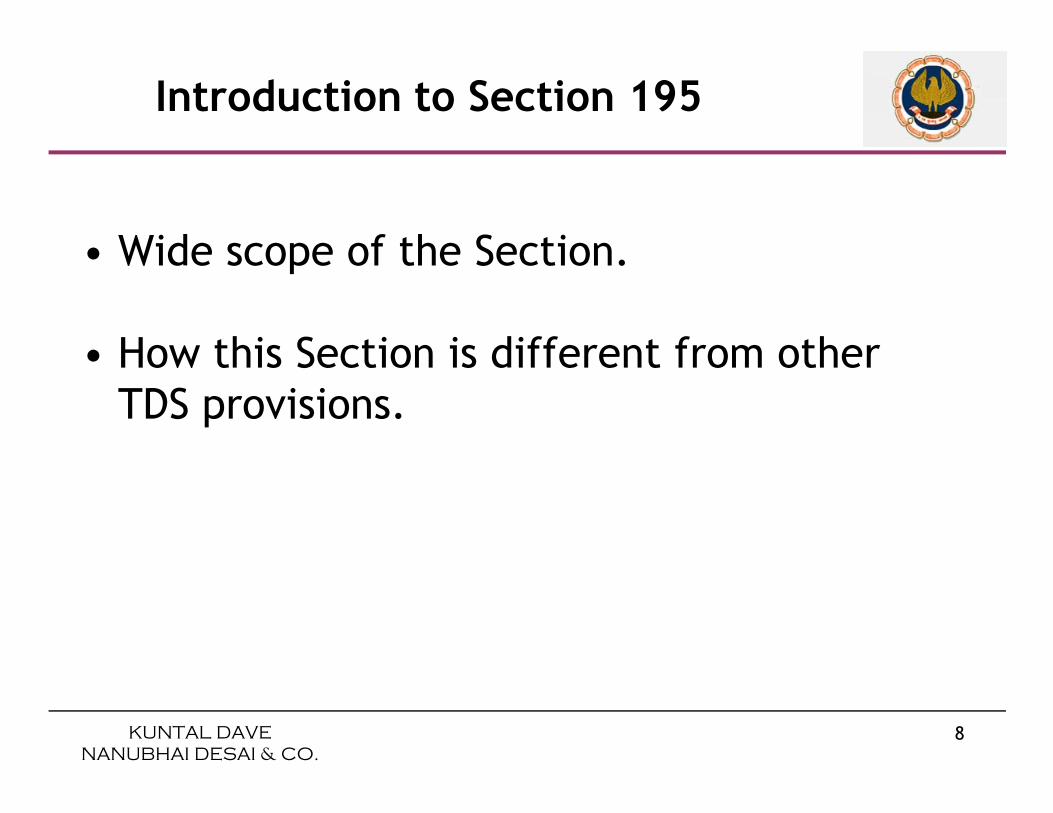

• Wide scope of the Section.

• How this Section is different from other TDS provisions.

Introduction to Section 195

KUNTAL DAVE

NANUBHAI DESAI & CO.

8

TDS provisions.

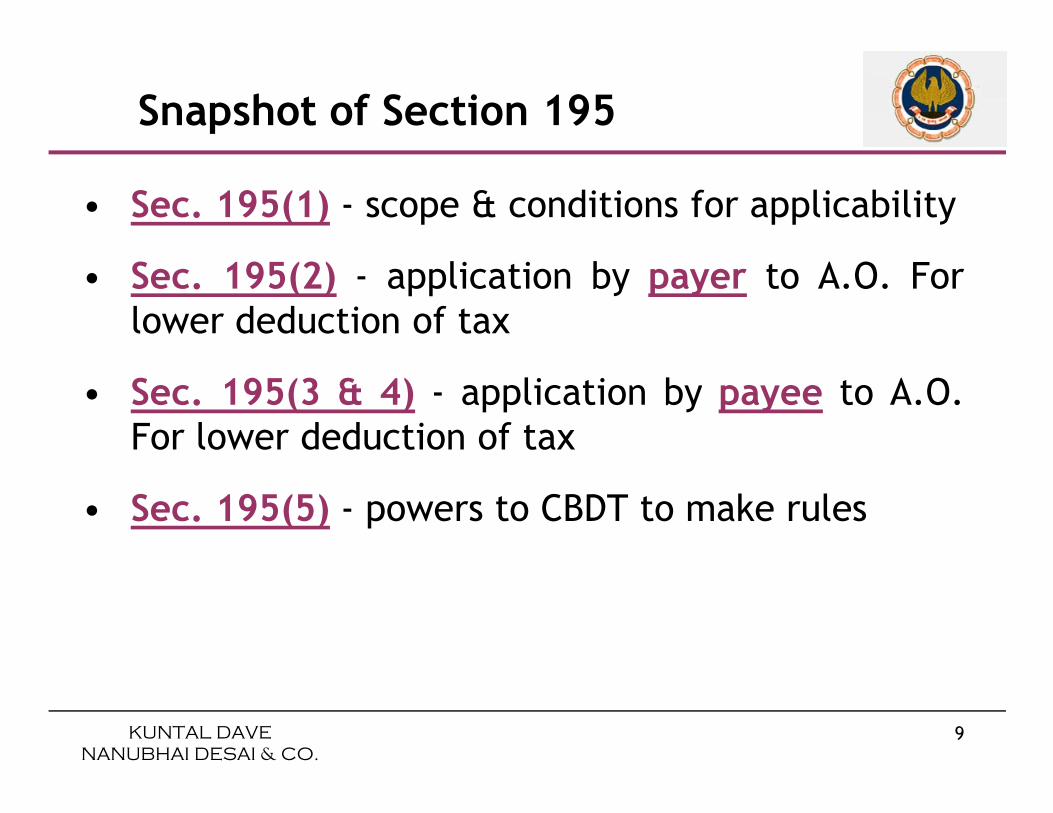

• Sec. 195(1) - scope & conditions for applicability

• Sec. 195(2) - application by payer to A.O. Forlower deduction of tax

• Sec. 195(3 & 4) - application by payee to A.O.

Snapshot of Section 195

KUNTAL DAVE

NANUBHAI DESAI & CO.

9

• Sec. 195(3 & 4) - application by payee to A.O.For lower deduction of tax

• Sec. 195(5) - powers to CBDT to make rules

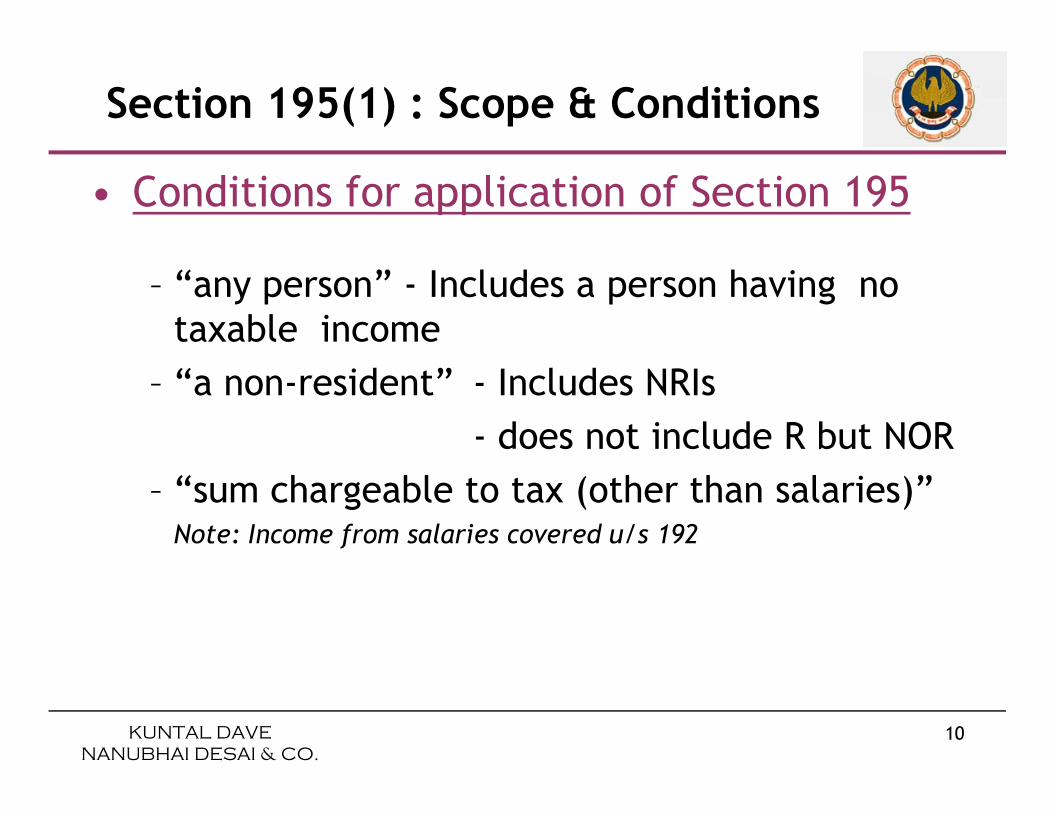

• Conditions for application of Section 195

– “any person” - Includes a person having no taxable income

– “a non-resident” - Includes NRIs

Section 195(1) : Scope & Conditions

KUNTAL DAVE

NANUBHAI DESAI & CO.

10

- does not include R but NOR

– “sum chargeable to tax (other than salaries)”Note: Income from salaries covered u/s 192

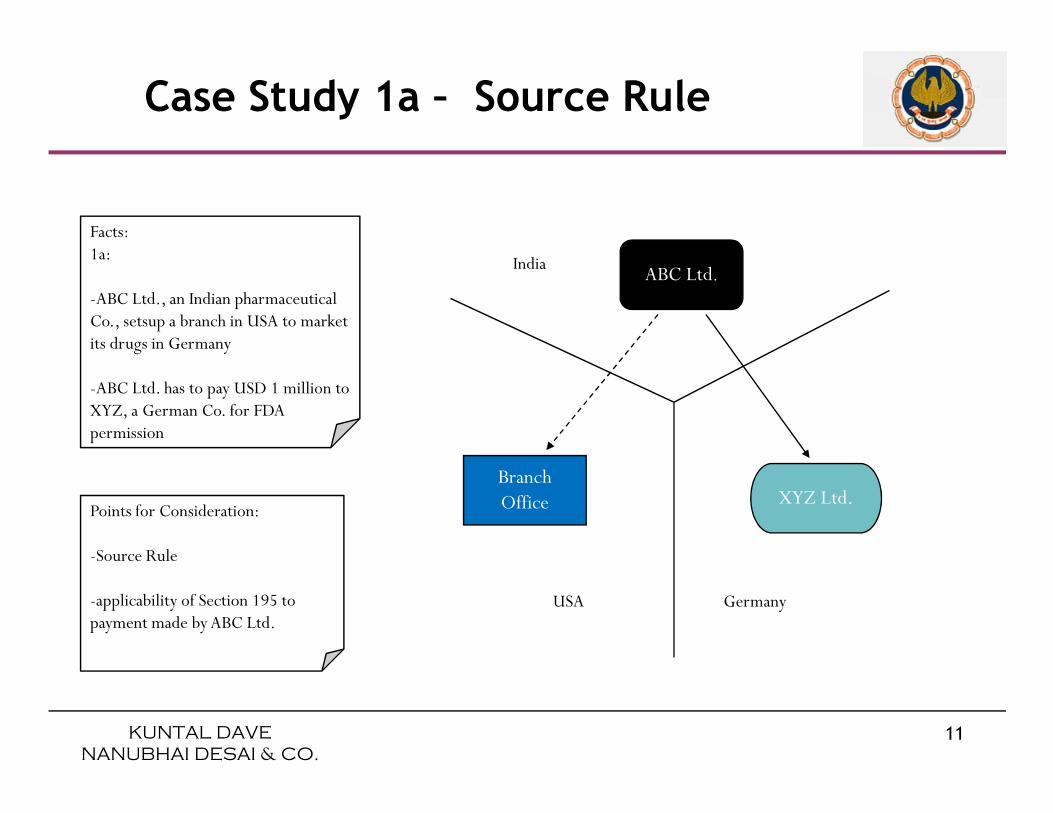

Case Study 1a – Source Rule

IndiaABC Ltd.

Facts:1a:

-ABC Ltd., an Indian pharmaceutical Co., setsup a branch in USA to market its drugs in Germany

-ABC Ltd. has to pay USD 1 million to XYZ, a German Co. for FDA

KUNTAL DAVE

NANUBHAI DESAI & CO.

11

USA Germany

BranchOffice XYZ Ltd.

XYZ, a German Co. for FDA permission

Points for Consideration:

-Source Rule

-applicability of Section 195 to payment made by ABC Ltd.

Case Study 1a – Source Rule (contd...)

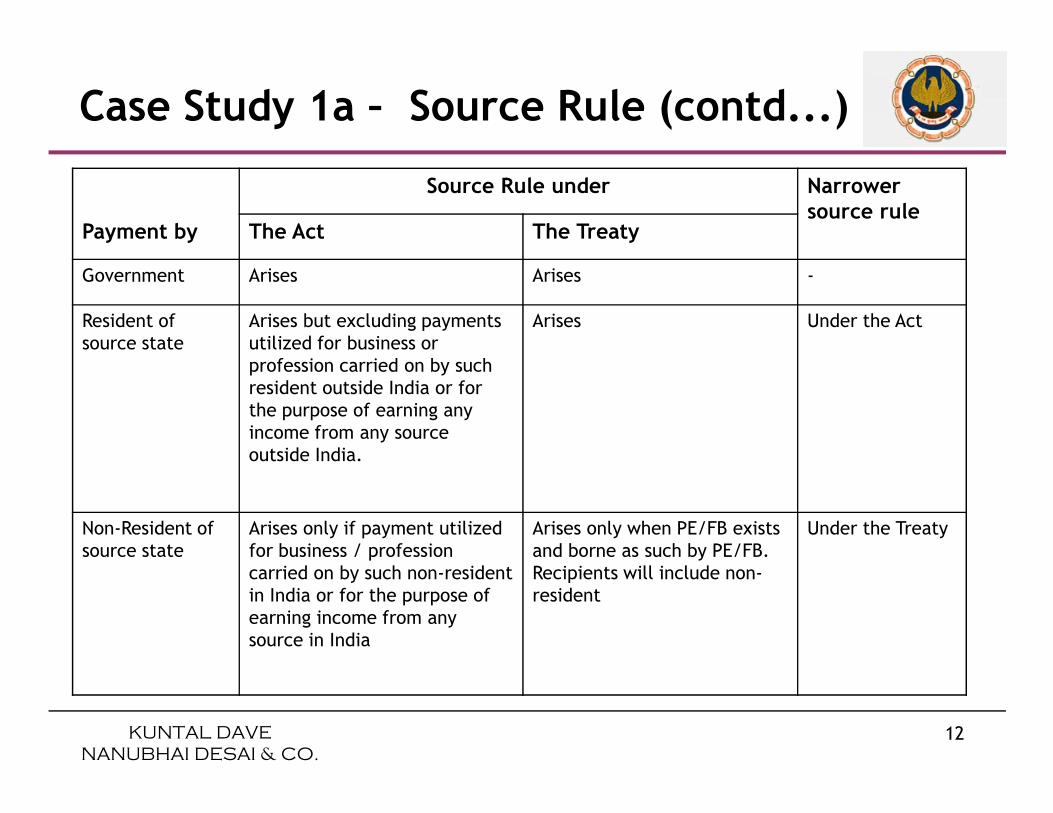

Source Rule under Narrower source rule

Payment by The Act The Treaty

Government Arises Arises -

Resident of source state

Arises but excluding payments utilized for business or profession carried on by such resident outside India or for the purpose of earning any

Arises Under the Act

KUNTAL DAVE

NANUBHAI DESAI & CO.

12

the purpose of earning any income from any source outside India.

Non-Resident of source state

Arises only if payment utilized for business / profession carried on by such non-resident in India or for the purpose of earning income from any source in India

Arises only when PE/FB exists and borne as such by PE/FB. Recipients will include non-resident

Under the Treaty

• Accrual – Source

– Source of income would not be the place where income accrues or arises

� CIT v Ahmedbhai Umarbhai & Co. – 018 ITR 472

� Anglo French Textile Co. Ltd. v CIT – 025 ITR 0027

• Section 9 (1) (vi) / (vii) of the Act deem royalty / FTS to accrue or arise in India where it is:

Case Study 1a – Source Rule (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

13

arise in India where it is:

– Payable by Government

– Payable by resident unless it is payable in respect of any right, property or information used or services utilized:

� For the purpose of or in the business or profession carried on by such resident outside India or

� For the purpose of making or earning any income from any source outside India

– Payable by non-resident only if it is payable in respect of any

right, property or information used or services utilized:

� For the purpose of or in the business or profession carried on by such

non-resident in India or

� For the purpose of making or earning any income from any source in

India

Case Study 1a – Source Rule (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

14

India

• Source Rule under the Treaty – Article 12

– Royalty / Fees for Technical Services are deemed to arise in India only if:

� Payer is a resident of India or

� Payer has a PE in India in connection with which the liability to pay royalty / fees for technical services has arisen and

� Such payment is borne by PE

Case Study 1a – Source Rule (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

15

• Place of Accrual (Section 5 & 9 of the Act):

– Accrue where service are utilized (SRK(230 ITR 206(AAR))

– Accrue where the payer is situated(238 ITR 296)

– Accrue where right to receive income arose (Rajiv Malhotra 284

ITR 564(AAR))

– Accrue in India if used in India

Case Study 1a – Source Rule (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

16

– Accrue in India if used in India

� Requirement of ‘rendered and used’ is no longer required in view of

retrospective amendment w.e.f. 1st June 1976 to Explanation to

Section 9(1) brought out by the Finance Act, 2010.

� Decision in Ishikawajma-Harima overruled by Ashapura Minechem Ltd.

vs. ADIT (ITAT Mumbai) ITA No.2508/Mum/08

– Lufthansa Cargo India (P.) Ltd. V DCIT (TDEL) – 091 ITD 133

– Payments from export proceeds – Madras HC

• Distinction between Service of providing employees & rendering

service through employees

� DDIT (IT) v Stock Engineer & Contractor B.V. (TBOM) – 121 TTJ 320

� Ind Telesoft P. Ltd., In Re. – 267 ITR 725 - The right to commission

arose in foreign country where development software was supplied

Case Study 1a – Source Rule (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

17

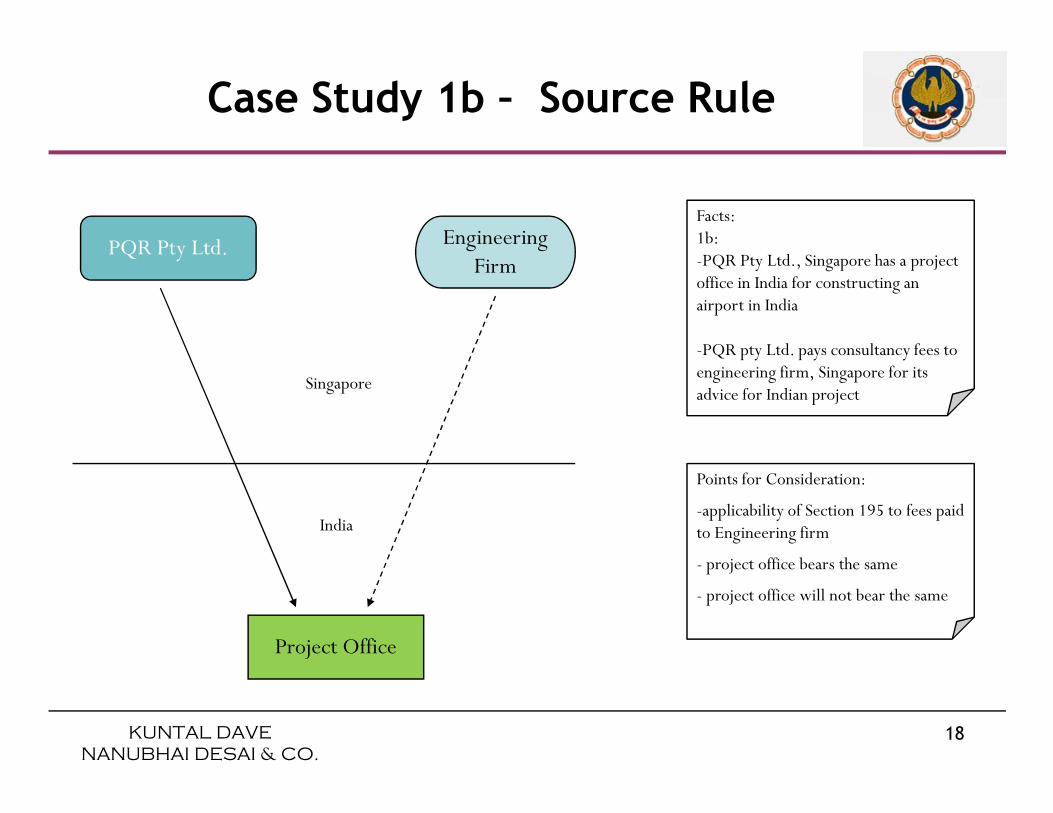

PQR Pty Ltd. Engineering Firm

Singapore

Facts:1b:-PQR Pty Ltd., Singapore has a project office in India for constructing an airport in India

-PQR pty Ltd. pays consultancy fees to engineering firm, Singapore for its advice for Indian project

Case Study 1b – Source Rule

KUNTAL DAVE

NANUBHAI DESAI & CO.

18

Project Office

India

Points for Consideration:

-applicability of Section 195 to fees paid to Engineering firm

- project office bears the same

- project office will not bear the same

• Most Indian tax treaties restrict the taxability in India of royalty /

fees for technical services from one non resident to other non

resident only to cases when the payer has a PE in India and the right,

property or contract in respect of which the royalties / fees for

technical services are paid is effectively connected with such PE

• In addition to the above the India-US treaty provides for taxability in

India of royalty / fees for technical services paid by one non resident

Case Study 1b – Source Rule (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

19

India of royalty / fees for technical services paid by one non resident

to another non resident, where the royalties relate to the use of, or

right to use, the right or property, or fees for included services relate

to services performed, in India [Article 12 (7) (b) of India-US tax

treaty]

• P.No.22 of 1996 [1996] 238 ITR 99 (AAR)

– Granting an Indian Co. the right to use trademark in India

– Held liable to tax - as royalty arises in India

• ‘Source’ is practical and not legal concept – All income accruing or arising from any ‘source of income in India’ is deemed to accrue or arise in India [Performing Right Society Ltd. v CIT 93 ITR 44]

Case Study 1b – Source Rule (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

20

ITR 44]

• Borne by:

– “allocable” – even when:

� The remuneration (eg: stock option) may not be deductible

� The remuneration is not actually deducted since PE is exempt from tax [DHV Consultants BV, In Re (AAR) – 277 ITR 0097]

– Economically incurred – remuneration that is capitalised

• Borne by (continued…):

– Commercially liable / actually paid – CIT v Dalhousie Properties Ltd. [149 ITR 708]

– Deductible

– Deducted

– Actually paid

Case Study 1b – Source Rule (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

21

• Whether applicable for:− Payments by a Branch of a foreign entity to its HO or

other Branches ? (Circular 740 & Circular 649)

− Payments by a resident to a branch in India of a foreignentity say Citibank? (Circular No. 20 dt. 3.8.1961)

− Payments by a resident to an “agent” of non-resident ?

Sec.195(1): Scope & Conditions (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

22

− Payments by a resident to an “agent” of non-resident ?(35 ITR 134).

“Any sum chargeable (other than salaries)”-meaning of:

− Scope of “income” of a non-resident (Section 5 & Section 9)

− TDS on “Gross Sum” or “income” element?

� 152 ITR 753; 239 ITR 587

� on Gross basis on Royalties / FTS / Investment Income / Lotteries etc.

Payments Covered U/s. 195

KUNTAL DAVE

NANUBHAI DESAI & CO.

23

• Is Tax deductible u/s 195 when:− Payments in kind (265 ITR 644)

− Decretal amount in favour of a non-resident

− (48 ITR 653) & (265 ITR 254)

− Interest U/s. 244A of Act ? (236 ITR 637)

− On income exempt u/s. 10 ? (188 ITR 749)

Payments Covered U/s.95 (Contd…)

KUNTAL DAVE

NANUBHAI DESAI & CO.

24

− On income exempt u/s. 10 ? (188 ITR 749)

• Is Tax deductible u/s 195 when: (Cont…)− When in doubt on taxability of the payment ? (Mumbai Tribunal in

Arthur Andersen’s case)

− Contrary decision in 76 ITD 37 – Hyd. ITAT

− On capital gains?

− On void agreement ? (81 ITD 77)

Payments Covered U/s.95 (Contd…)

KUNTAL DAVE

NANUBHAI DESAI & CO.

25

− On void agreement ? (81 ITD 77)

• “Rates in force” – meaning – (Section 2(37A)(iii); Circular 728)– what when difference in Act & Finance Act ? (Circular 740)

– Is surcharge to be added to Treaty rates ?

• Grossing up of tax (Section 195A)

Payments Covered u/s.195 (Contd…)

KUNTAL DAVE

NANUBHAI DESAI & CO.

26

• Grossing up of tax (Section 195A)– Not to be done in cases of presumptive Tax (264 ITR 340)

– Exchange Rate Applicable – (Rule 26)

• “Time of Deduction”

– On credit or payment whichever is earlier;

– Exception for interest payment by Government or PSB.

– When FEMA approval awaited ? (211 ITR 256)

– TDS when adjustment of amount payable to a non-resident against dues i.e. when no payment no credit ? (223 ITR 271)

Payments Covered u/s.195 (Contd…)

KUNTAL DAVE

NANUBHAI DESAI & CO.

27

i.e. when no payment no credit ? (223 ITR 271)

• Section 90(2); 222 ITR 551; 228 ITR 487

– “Liable to Tax” – meaning

� Emirates Fertilizer Trading Co. WLL (272 ITR 82) (AAR)

� Azadi Bachao Andolan (263 ITR 706) (SC)

� XYZ, in re (241 ITR 16)

Treaty Vs. Act

KUNTAL DAVE

NANUBHAI DESAI & CO.

28

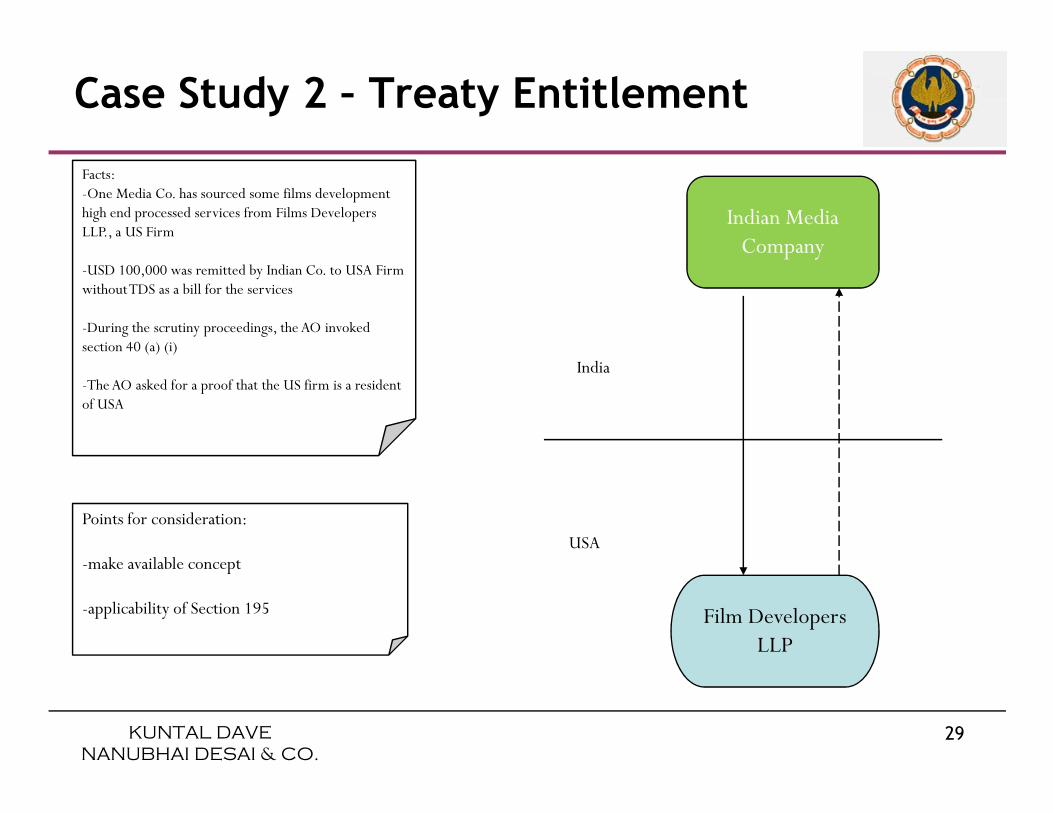

Case Study 2 – Treaty Entitlement

Facts:-One Media Co. has sourced some films development high end processed services from Films Developers LLP., a US Firm

-USD 100,000 was remitted by Indian Co. to USA Firm without TDS as a bill for the services

-During the scrutiny proceedings, the AO invoked section 40 (a) (i)

-The AO asked for a proof that the US firm is a resident of USA

Indian Media Company

India

KUNTAL DAVE

NANUBHAI DESAI & CO.

29

of USA

Points for consideration:

-make available concept

-applicability of Section 195 Film Developers LLP

USA

• Person – Article 3 (UN Model / OECD Model)

– Person includes:

� Individual

� Companies

� Body of persons

• Residence – Article 4 (UN Model / OECD Model)

– Category - 1

Case Study 2 – Treaty Entitlement (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

30

– Category - 1

� Entity is a person

� Person liable to tax by reasons of its Domicile/Residence/Place of management/Any other criterion of a similar nature/Citizenship

(additional criteria under US MC)/Place of incorporation (additional

criteria under UN MC & US MC)

� Liability to tax is under the laws of the state;

� Liability to tax not only in respect of income from sources or capital situated in that State

Case Study 2 – Treaty Entitlement (contd...)

• Residence – Article 4 (UN Model / OECD Model) (contd…)

– Category – 2

� Contracting State itself

– Category – 3

� Any political sub-division of, or a local authority

– only a person can be a resident

– Liable to tax

KUNTAL DAVE

NANUBHAI DESAI & CO.

31

– Liable to tax

� Where source of income is not taxable in State R

� Where entity is exempt from tax in State R

� Where entity is not covered by the tax law in State R

� Where the entity is not required to pay any tax in State R (loss making entity)

– Subject to tax

• India-UAE Treaty:

– Cyril Pereira

– M A Rafik

– Amendment to Treaty

• India-Mauritius Treaty:

– TRC

• India-US Treaty:

Case Study 2 – Treaty Entitlement (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

32

• India-US Treaty:

– General Electric Pension Trust, In Re – (280 ITR 425 – AAR)

• India-UK Treaty:

– Clifford Chance

– Person – excludes partnership

– Resident – covers person

– Article 15

�Individual – own capacity or as a member of a partnership

• India-US Treaty:

– Person also includes an estate, a trust and a partnership

– Resident of the contracting state means – a person under the laws of that state is “liable to tax”

– Partnership, estate & trusts – term “resident” shall apply only to the extent that income is “subject to tax” as the income of a resident, either in its hands or in the hands of its partners or beneficiaries

Case Study 2 – Treaty Entitlement (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

33

either in its hands or in the hands of its partners or beneficiaries

– A partnership is never taxed as such. Thus, for US tax purpose, the question of whether income received by a partnership is received by a resident is determined by residence of its partners rather than by the residence of partnership itself. To the extent the partners are subject to Us tax as residents of the United States, the income received by the partnership is treated as income received by a US resident

• Article 15 – IPS

– Firm of individuals

– Meaning of “Professional services”

• Article 12 – FIS

– Excludes amount paid to any individual or firm of individuals for professional services defined in Article 15

Case Study 2 – Treaty Entitlement (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

34

professional services defined in Article 15

Sec.195(2): Application by Payer to AO for lower deduction of tax

• Difference between Section 195(2) & Section 197

• Form for this application ?

• Rule 10

– percentage of turnover or

– proportion to total receipts or

– any other reasonable manner.

KUNTAL DAVE

NANUBHAI DESAI & CO.

35

– 44 B, 44 BB, 44 BBA, 44BBB – certificate by A.O to deduct 10% astax and 5% for adjustment in future – whether a valid certificate?

Sec.195(2) : Application by Payer to AO for lower deduction of tax (Contd…)

• Appeal against order u/s. 195(2) - Section 248

– within 30 days of payment of tax.

• Refund to deductor of tax deducted ?(Circular 790)

KUNTAL DAVE

NANUBHAI DESAI & CO.

36

Sec.195(3) : Application by payee for lower deduction of tax ?

• Rule 29B(2) – conditions

• “Certificate” by AO.

KUNTAL DAVE

NANUBHAI DESAI & CO.

37

Certificate by a Chartered Accountant for remittance

• Form of Certificate (Circular 10 of 2002)

• Clauses in Certificate of particular concern– Clause 1 – “name & address of beneficiary”

� “beneficiary” V/s. “beneficial owner”

– Clause 7 – Four Questions

KUNTAL DAVE

NANUBHAI DESAI & CO.

38

Consequences of non / short deduction of TDS

• Disallowance u/s. 40(a)(i) or Section 58(1)(a)(ii)

• Interest u/s. 201(1A)

– Cannot be levied if recipient has paid full tax (179 CTR121)

• Penalties - (Section 221; Section 271C)

KUNTAL DAVE

NANUBHAI DESAI & CO.

39

• Prosecution - (Section 276 B)

Mandatory PAN

• Section 206AA of the Income Tax Act, 1961 (“the Act”) has made itmandatory for payers to withhold tax at a higher rate if the payeedoes not provide its Permanent Account Number (“PAN”).

• With the above provision, if the recipient fails to provide the PAN,the withholding tax rate, if applicable, would be higher of thefollowing rates:

– Rate specified in the relevant section depending on the nature of

KUNTAL DAVE

NANUBHAI DESAI & CO.

40

– Rate specified in the relevant section depending on the nature ofpayment;

– Rates in force (rate specified in the ITA or under the tax treaty);

– Rate of 20%.

Mandatory PAN (contd...)

• The Revenue Officers are prohibited from issuing any certificate fornil withholding or lower withholding of taxes if the application filedfor this purpose does not contain the PAN of the payee.

• The PAN of the payee must be referred in all correspondence, bills,vouchers and other documents exchanged between the parties.

• CBDT has clarified that this requirement applies to non-residentpayees also.

KUNTAL DAVE

NANUBHAI DESAI & CO.

41

payees also.

ISSUES ARISING U/S. 195 IN RESPECT

KUNTAL DAVE

NANUBHAI DESAI & CO.

42

IN RESPECT OF CERTAIN

SPECIFIC PAYMENTS.

Issues arising u/s. 195 in respect of certain specific payments

• Section 9(1) (i): “Business Connection”

• Section 9 (1) (vi) & Section 9 (1) (vii)

KUNTAL DAVE

NANUBHAI DESAI & CO.

43

Section 9(1)(i)

• “Business Connection” – Interpretation

– Circular 23 of 1969 gave illustrative instances of ‘BusinessConnection’ and clarifications on applicability of Section 9.

– CBDT has issued Circular 7 of 2009 dated 22 October 2009 andwithdrawn circular 23 with immediate effect.

KUNTAL DAVE

NANUBHAI DESAI & CO.

44

Withdrawal of Circular 23

– Stated reason for withdrawal – Interpretation placed by sometaxpayers seeking to claim relief was not in accordance with theprovisions of the Act or the intention behind the circulars

– Clarifies that the withdrawal will in no way prejudice the followingarguments which the tax authorities have taken or may take in anyappeal, reference or petition

� Circular 23 does not apply to a particular case

KUNTAL DAVE

NANUBHAI DESAI & CO.

45

� Circular 23 cannot be interpreted to allow relief to the taxpayer whichis not in accordance with the provisions of section 9 or intentionbehind the issue of the circular

Impact of withdrawal of Circular 23

– Section 119 empowers CBDT to issue orders, instructions anddirections to subordinate authorities.

– CBDT issues circulars which have binding effect on tax authoritiesso long as they are not in conflict with the provisions of the Act orinterpretation provided by the Supreme Court.

– CBDT Circulars are in the nature of (contemporanea exposito) andaid in the proper construction and interpretation of statutory

KUNTAL DAVE

NANUBHAI DESAI & CO.

46

aid in the proper construction and interpretation of statutoryprovision.

– Principles laid down in section 9 and Supreme Court decision inR.D. Aggarwal and other decisions should prevail.

– Withdrawal does not necessarily mean that a non–residentautomatically is taxable in India in the situations describedcircular.

– Taxability evaluated independent of the provisions of the circular.

Does the withdrawal of the circular have retrospective operation?– Paragraph 3 of Circular 7 – Withdrawal of Circular 23 with

‘immediate effect’

– Paragraph 4 – Withdrawal shall in no way be prejudice that theDepartment ‘has taken’ or may take’

– Circulars issued under section 119 are in the nature of instructions/guidelines and do not constitute law. The withdrawal of these cantherefore operate only prospectively. Refer to UTI v. P.K. Unny (249

KUNTAL DAVE

NANUBHAI DESAI & CO.

47

therefore operate only prospectively. Refer to UTI v. P.K. Unny (249ITR 612) (Bom)

– Withdrawal should therefore operate prospectively and NOTretrospectively.

Section 9(1)(i) (contd...)

• Receipts of a non-resident

– Taxable only to the extent “reasonably attributable” to operations

in India.

– Specific exclusions – Explanation 1(b);1(c) & 1(d) of Section 9(1)(i)

– Specific inclusions – Explanation 2 to Section 9(1)(i)

KUNTAL DAVE

NANUBHAI DESAI & CO.

48

– treaty concept of dependent agent introduced in Act

� agent need not be in India but must Act in India.

• Other judicial rulings

– existence of some organization in India (223 ITR 416;108 ITR 874)

– Agency in India (239 ITR 879; 36 ITR 418; 120 ITR 887; etc)

(Note: Explanation 2 to Section 9(1)(i)) (refer 194 CTR 108 (AAR) )

Section 9(1)(i) (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

49

(Note: Explanation 2 to Section 9(1)(i)) (refer 194 CTR 108 (AAR) )

(Difference between “mainly” & “almost wholly”)

•Other judicial rulings (Cont…)

– Close relationship in India - (119 ITR 986)

– Asiasat’s case (85 ITD 478)

– Taxation of BPO units (Circular 5 of 2004)

– Difference between ‘Business Connection’ & ‘Permanent Establishment’ ?

Section 9(1)(i) (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

50

– Taxability of Reimbursement of Expenses� SRK (230 ITR 206 – AAR)

� Telco (245 ITR 823 (Bom)

� Contrary view – Cochin Refinery (222 ITR 354)

� Danfoss Industries (P) Ltd. (268 ITR 1(AAR)

� Timkin India Ltd. (273 ITR 67(AAR))

� Mahindra & Mahindra (1 SOT 896) (Mum)

– Taxability of FIIs� Fidelity Advisor Series VIII (271 ITR 1 (AAR))

� Morgan Stanley & co. (272 ITR 416 (AAR))

•Payment in nature of Royalty & FTS:

– These sub-sections override Sec. 9(1)(i) (167 ITR 884)

– Difference between “Royalty” & “FTS”

Section 9(1)(vi) & Section 9(1)(vii)

KUNTAL DAVE

NANUBHAI DESAI & CO.

51

– Difference between “Royalty” & “FTS”

– When are they deemed to accrue or arise in India ?� Place of accrual (230 ITR 206); (250 ITR 164); (262 ITR 513)

– “Royalty” - Act Vs. Treaty

– “FTS” - Act Vs. Treaty

– “Make available” definition of FTS

– Two specific issues with respect to rate for TDS

– TDS where FTS Article is missing in Treaty

Sec. 9(1)(vi) & Sec. 9(1)(vii) (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

52

– Indian Treaties where rates of tax lower than Act

• Consideration for designs & drawings– outright purchase not royalty (190 ITR 626) (Pfizer’s Case (271 ITR 101(AAR))

– when it forms part of composite contract for supply of machines (243 ITR 459; 259 ITR 248; 255 ITR 354) (contrary – 271 ITR 193(AAR))

– Services provided in course of business not FTS(237 ITR 142)(contrary –271 ITR 193 (AAR))

Sec. 9(1)(vi) & Sec. 9(1)(vii) (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

53

271 ITR 193 (AAR))

• Payment for initial know-how rendered from abroad (148 ITR 774; 145 ITR 84; 143 ITR 720 & 224 ITR 724 (SC))

• “information” – meaning

– HEG (263 ITR 230)

– Dun & Bradstreet Espana (272 ITR 99(AAR ))

– Wipro Ltd. (1 SOT 663) (contrary view – Payment for access of

CPU (238 ITR 296))

Sec. 9(1)(vi) & Sec. 9(1)(vii) (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

54

CPU (238 ITR 296))

• Payment for erection of machinery supplied – (262 ITR

110; & 251 ITR 348)

• Payment for training to Indian personnel

– In India – (224 ITR 203)

– Outside India

• Fees for deputing technicians to India - FTS (222 ITR 551)– Reimbursement of daily allowance treated as FTS (230 ITR 206)

• Payments for repairs– Sahara Airlines (79 TTJ 268)

Sec. 9(1)(vi) & Sec. 9(1)(vii) (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

55

– Sahara Airlines (79 TTJ 268)– Lufthansa Cargo (92 TTJ 837)– Airport Authority of India (193 CTR 487)– Contrary view – Mannesmann Demag (26 ITD 198)

• Payment for services related to GDR Issue (80 TTJ 120)

• Connectivity payment– Standard facilities - (80 TTJ 191; 251 ITR 53)– Satellites (80 TTJ 106), (78 TTJ 489) & (Raj TV (Unreported)

• Software / E-Commerce Payments

License to use Software or for electronic downloading of computer

programs / digital content may give rise to use of “copyright” as per

Sec. 9(1)(vi) & Sec. 9(1)(vii) (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

56

programs / digital content may give rise to use of “copyright” as perCopyright Act. Is it, thus, covered in “royalty”?

• FTS received by PE falling within 9 (1)(vii) but not in definition oftreaty. Deduction not restricted as per Section 44D (93 TTJ 293)

• The Test (OECD / IRS View) : What is the

consideration for ?– if for rights to use copyright then royalty;

– if use of copyright only incidental, then business profits;

– if for a copyrighted article then business profits;

Sec. 9(1)(vi) & Sec. 9(1)(vii) (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

57

– if for a copyrighted article then business profits;

• The Test (OECD / IRS View) : What is the consideration for ? (Cont)– if for rights in the copyright i.e. for transfer of ownership then Business

Income or Capital Gains.

– if for rights in relation to copyright – to use & make copies foroperation only within its business – then business profits.

Sec. 9(1)(vi) & Sec. 9(1)(vii) (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

58

– if Capital Gains a Mixed Payment i.e. sale of hardware with embeddedsoftware then break-up unless one part is the dominant part & otherparts are ancillary.

– Legal Decisions� Lucent Technologies (82 TTJ 163)� TCS (271 ITR 401)

• Payments for Shipping:

– Bare Boat

– Dry Lease

– Wet Lease

– Payment to Shipping Agent

• Payments for Services to Airlines:

– British Airways (73 TTJ 519)

Sec. 9(1)(vi) & Sec. 9(1)(vii) (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

59

– British Airways (73 TTJ 519)

– Lufthansa German Airline (83 TTJ 113)

Recent Judgments

• Vodafone International Holdings B. V. vs. Union of India and Anr (Mumbai High Court)

• M/s Microsoft Corporation vs. ADIT (Delhi Tribunal)

• Samsung Electronics judgement reversed by SC

KUNTAL DAVE

NANUBHAI DESAI & CO.

60

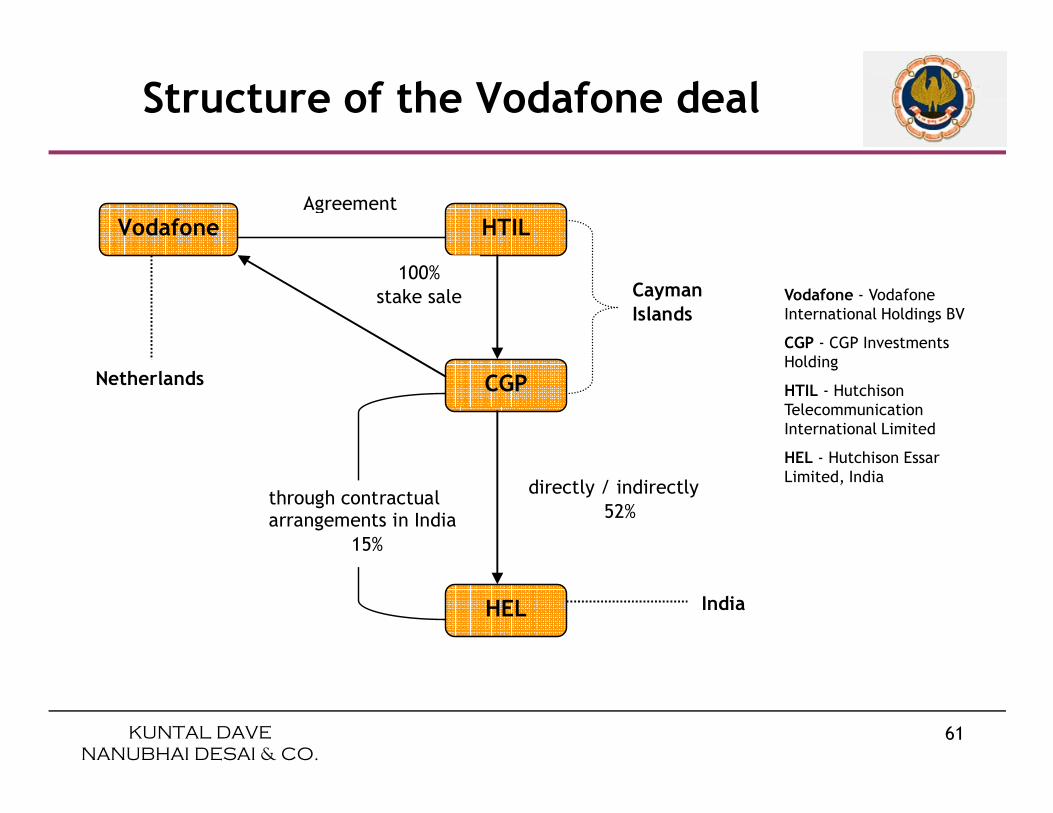

Structure of the Vodafone deal

Vodafone

CGP

HTIL Agreement

Cayman

Islands

Netherlands

100% stake sale Vodafone - Vodafone

International Holdings BV

CGP - CGP Investments Holding

HTIL - Hutchison Telecommunication

KUNTAL DAVE

NANUBHAI DESAI & CO.

61

HEL

directly / indirectly

52% through contractual arrangements in India

15%

India

Telecommunication International Limited

HEL - Hutchison Essar Limited, India

Vodafone case updates

• September 2007: Show cause notice by the department to Vodafone for failure to deduct

tax at source in relation to payments made to HTIL.

• October 2007: Vodafone moved the HC challenging the department’s jurisdiction to issue

the show cause notice.

• December 2008: The HC dismissed the writ petition against which Vodafone filed a special

leave petition before the SC.

KUNTAL DAVE

NANUBHAI DESAI & CO.

62

• January 23, 2010: The SC in its order dated January 23, 2010 directed that the

jurisdictional issue should be determined by the department after submission of

documents by Vodafone and that the department had right to seek the documentation to

come to a conclusion if it indeed had the jurisdiction. The SC order further stated that if

the jurisdictional issue was decided against Vodafone, it may move the Mumbai HC to

question the decision on the issue of jurisdiction and the SC left all questions of law open.

• May 31, 2010: In pursuance to the SC order, the department passed an order on May

31, 2010 after issuing fresh notices holding that it had valid, lawful and competent

jurisdiction to treat Vodafone as an assessee-in-default under section 201 of the Act.

Vodafone questioned the legality of the order by filing a petition before the HC under

Article 226 of the Constitution of India on the jurisdiction issue.

• September 8, 2010: The HC in its decision rendered on September 8, 2010, held that

the series of transaction in question had a ‘significant nexus’ with India since the

Vodafone case updates (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

63

essence of it was change in controlling interest in HEL, which constituted source of

income in India. The transaction between the parties covered within its ambit diverse

rights and entitlements and not merely offshore transfer of shares of CGP. The fact that

Vodafone had a nexus with Indian jurisdiction could be substantiated by diverse

agreements that it entered into with HTIL. In these circumstances, the HC concluded

that the proceedings which were initiated by the department could not be held as

lacking jurisdiction.

• Vodafone filed another appeal with the Supreme Court, with a hearing planned for

October 25, 2010.

• October 25, 2010 – Adjournment of hearing by SC to November 15, 2010.

• November 15, 2010 - The SC directed Vodafone to deposit $550 million within three

weeks in relation to the $2.5 billion tax dispute and a bank guarantee worth $1.9 billion

within eight weeks.

• Final hearing will begin from February 5, 2011

Vodafone case updates (contd...)

KUNTAL DAVE

NANUBHAI DESAI & CO.

64

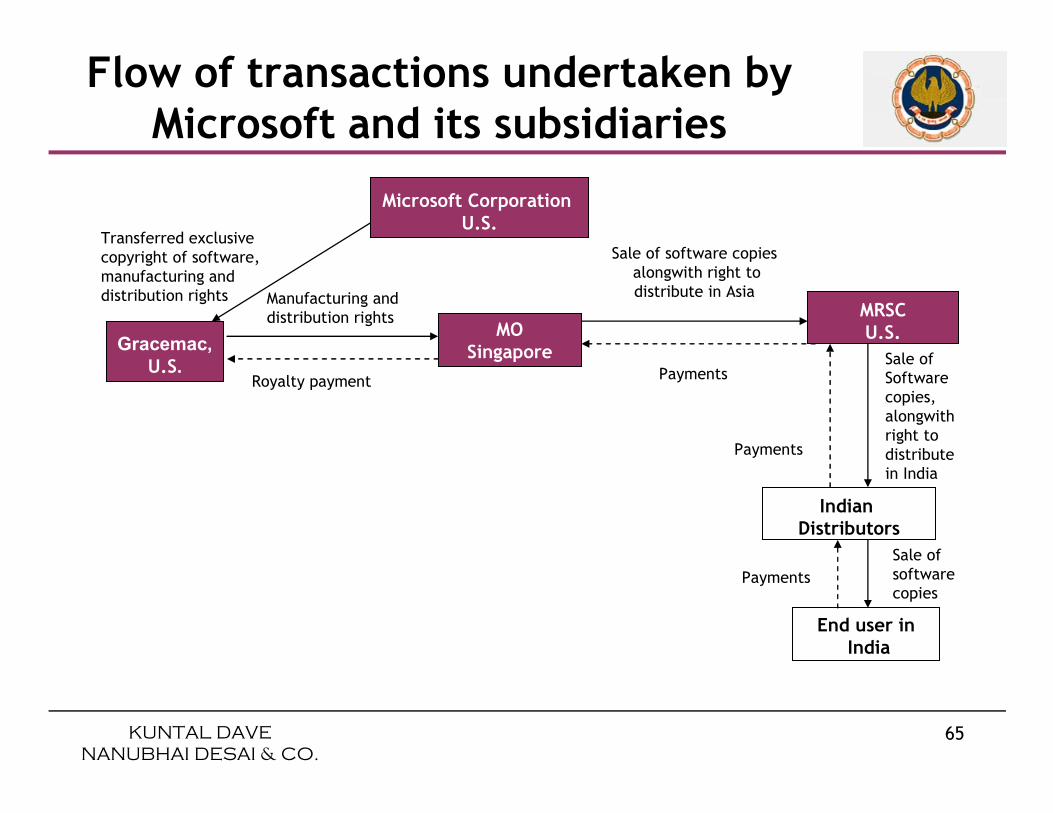

Flow of transactions undertaken by Microsoft and its subsidiaries

Microsoft Corporation U.S.

Gracemac,

U.S.

MOSingapore

MRSCU.S.

Transferred exclusive copyright of software, manufacturing and distribution rights Manufacturing and

distribution rights

Sale of software copiesalongwith right to distribute in Asia

Royalty payment PaymentsSale of Software copies, alongwith

KUNTAL DAVE

NANUBHAI DESAI & CO.

65

IndianDistributors

End user inIndia

Payments

Payments

alongwith right to distribute in India

Sale of software copies

Comments on Microsoft decision

• Significant departure from the rulings delivered by various benches, hence uncertainty for the software industry

• Uncertainty in the characterisation of income from supply of software

• No discussion on the applicability of Section 9(1)(vi)(c)

• Special Bench ruling on the applicability of ICA in characterising the

KUNTAL DAVE

NANUBHAI DESAI & CO.

66

• Special Bench ruling on the applicability of ICA in characterising the royalty income not followed

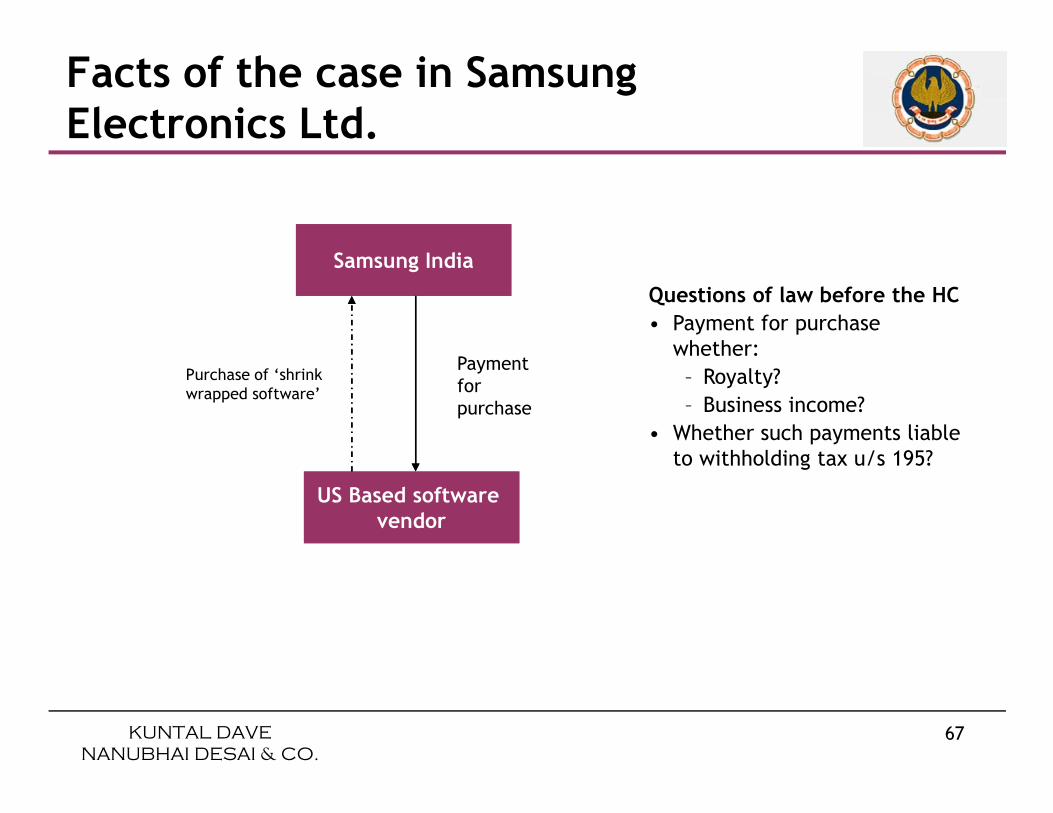

Facts of the case in Samsung Electronics Ltd.

Samsung India

Purchase of ‘shrink wrapped software’

Questions of law before the HC

• Payment for purchase whether:

– Royalty?

– Business income?

Payment for purchase

KUNTAL DAVE

NANUBHAI DESAI & CO.

67

US Based software vendor

– Business income?

• Whether such payments liable to withholding tax u/s 195?

purchase

Samsung Electronics Judgement Reversed By Supreme Court

• On September 9, 2010, the Supreme Court reversed the judgement of the Karnataka High Court in CIT vs. Samsung Electronics 320 ITR 209 where it was held that u/s 195 the payer was not entitled to consider whether the payment was chargeable to tax in the hands of the non-resident recipient or not.

• The appeals have been remanded to the High Court for a decision on whether or not the payments were taxable in the hands of the non-resident recipient. The judgement is awaited.

KUNTAL DAVE

NANUBHAI DESAI & CO.

68

resident recipient. The judgement is awaited.

• Impact of the judgement

A person making payment to a non resident will now have the option to decide whether income is chargeable to tax or not. That option was, most respectfully, erroneously withdrawn by the Karnataka High Court judgement.