THE CHAMBER OF TAX CONSULTANTS TDS … Sushil Lakhani...THE CHAMBER OF TAX CONSULTANTS TDS UNDER...

50

THE CHAMBER OF TAX CONSULTANTS TDS UNDER SECTION 195 ON PAYMENT TO NON-RESIDENTS September 12, 2015 By Sushil Lakhani

-

Upload

hoangkhuong -

Category

Documents

-

view

229 -

download

1

Transcript of THE CHAMBER OF TAX CONSULTANTS TDS … Sushil Lakhani...THE CHAMBER OF TAX CONSULTANTS TDS UNDER...

THE CHAMBER OF TAX CONSULTANTS

TDS UNDER SECTION 195 ON PAYMENT TO NON-RESIDENTS

September 12, 2015

By Sushil Lakhani

OVERVIEW OF SECTION 195

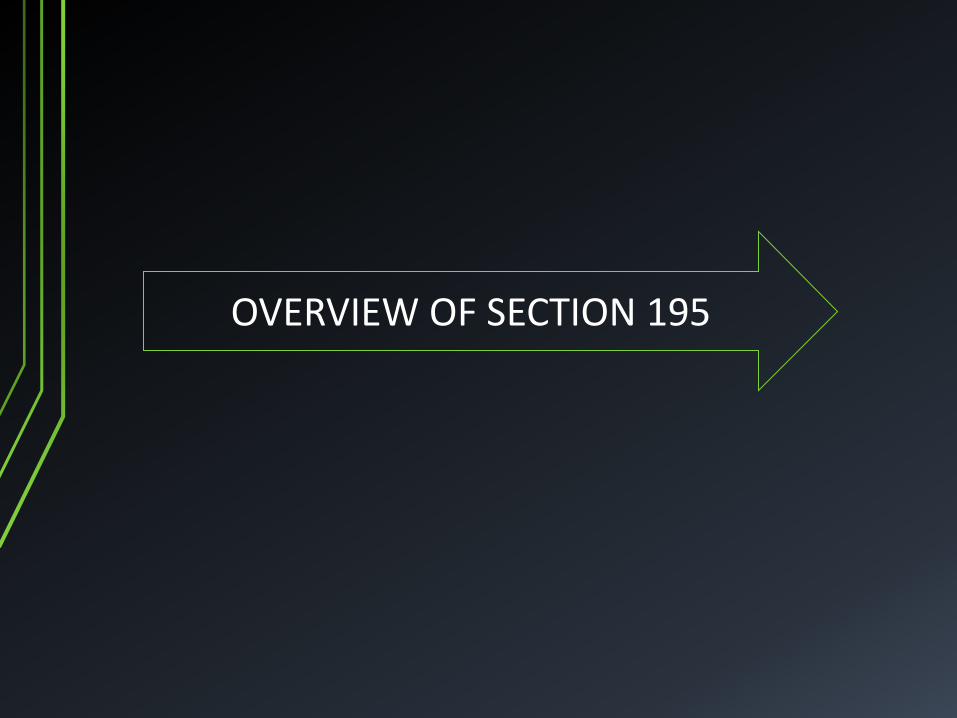

Section Provisions

195(1) Scope and conditions of applicability

195(2) Application by the “payer” to the AO

195(3) Application by the “payee” to the AO

195(4) Validity of certificate issued by the AO

195(5) Powers of CBDT to issue Notifications

195(6) Furnish the information relating to the payment of any sum

195(7) Power of CBDT to specify class of persons or cases where application to AO u/s 195(2) compulsory.

195A Grossing up of tax

206AA Permanent Account Number

90 (4) Tax Residency Certificate

172 Payment for carriage of passengers, livestock, mail or goods shipped at post in India (occasional shipping). Rate is on deemed profit 7.5%.

OVERVIEW OF RELEVANT PROVISIONS

12/9/2015 Sushil Lakhani 3

Section Applicable to Rate

194 LB Interest to non-resident by an Infrastructure Debt fund 5%

194 LC Interest to non-resident by an Indian company or a business trust under approved loan agreements or on long term Infra Bonds

5%

194LD Interest to FIIs or QFIS on rupees denominated bonds or government Security

5%

195 Any sum chargeable under the Act other than salaries & other than sums covered by other TDS provisions

Different for each type of Income (Sec. 111A to Sec. 115AD)

196A Income on respect of mutual fund units 20%

196B Long Term Capital Gains and/or other income in respect of mutual funds held by an offshore fund

10%

196C Interest, dividend or long term capital gains from Bonds or GDRs

10%

196D Interest on dividend or capital gains of FIIs (other than Income covered by Section 194LD)

20%

12/9/2015 Sushil Lakhani 4

Other TDS Provisions for payments to Non-residents

12/9/2015 Sushil Lakhani 5

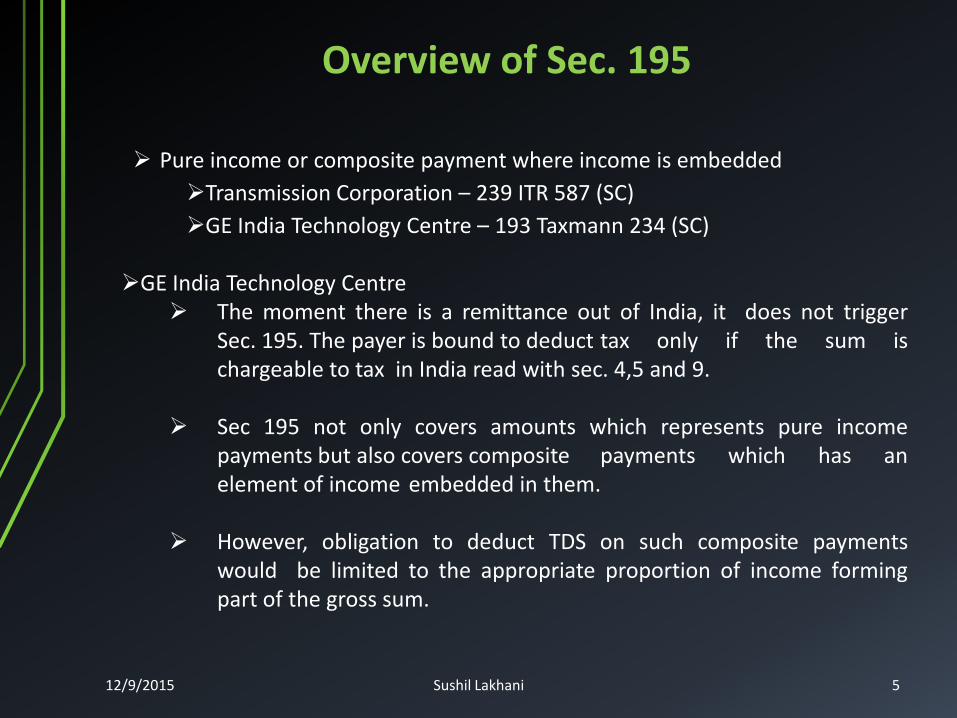

Overview of Sec. 195

Pure income or composite payment where income is embedded

Transmission Corporation – 239 ITR 587 (SC)

GE India Technology Centre – 193 Taxmann 234 (SC)

GE India Technology Centre The moment there is a remittance out of India, it does not trigger Sec. 195. The payer is bound to deduct tax only if the sum is chargeable to tax in India read with sec. 4,5 and 9.

Sec 195 not only covers amounts which represents pure income payments but also covers composite payments which has an element of income embedded in them.

However, obligation to deduct TDS on such composite payments would be limited to the appropriate proportion of income forming part of the gross sum.

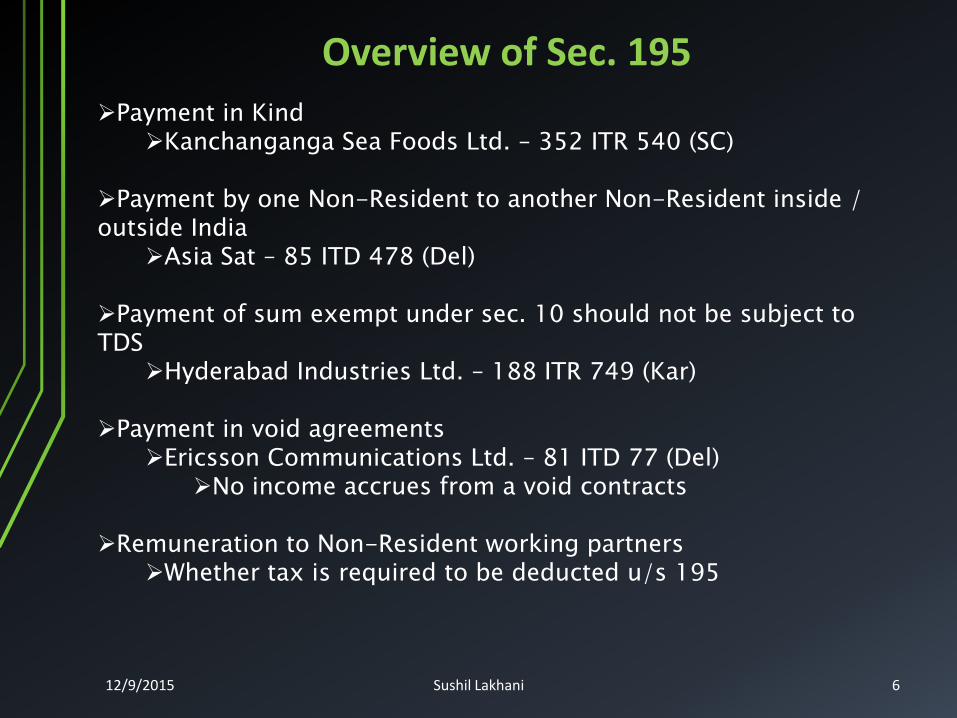

Payment in Kind Kanchanganga Sea Foods Ltd. – 352 ITR 540 (SC)

Payment by one Non-Resident to another Non-Resident inside / outside India

Asia Sat – 85 ITD 478 (Del)

Payment of sum exempt under sec. 10 should not be subject to TDS

Hyderabad Industries Ltd. – 188 ITR 749 (Kar)

Payment in void agreements Ericsson Communications Ltd. – 81 ITD 77 (Del)

No income accrues from a void contracts

Remuneration to Non-Resident working partners Whether tax is required to be deducted u/s 195

12/9/2015 Sushil Lakhani 6

Overview of Sec. 195

PART - A

SECTION 195(6)---UPLOADING FORM 15CA AND CERTIFICATE IN FORM 15CB BY CA FOR REMITTANCE

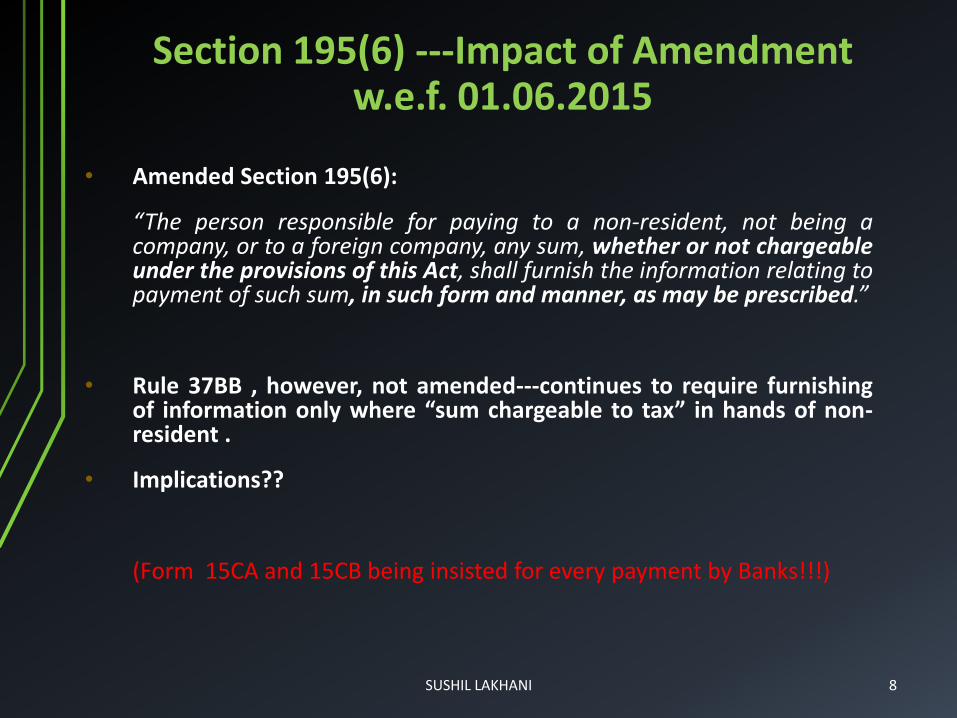

Section 195(6) ---Impact of Amendment w.e.f. 01.06.2015

• Amended Section 195(6):

“The person responsible for paying to a non-resident, not being a company, or to a foreign company, any sum, whether or not chargeable under the provisions of this Act, shall furnish the information relating to payment of such sum, in such form and manner, as may be prescribed.”

• Rule 37BB , however, not amended---continues to require furnishing of information only where “sum chargeable to tax” in hands of non-resident .

• Implications??

(Form 15CA and 15CB being insisted for every payment by Banks!!!)

SUSHIL LAKHANI 8

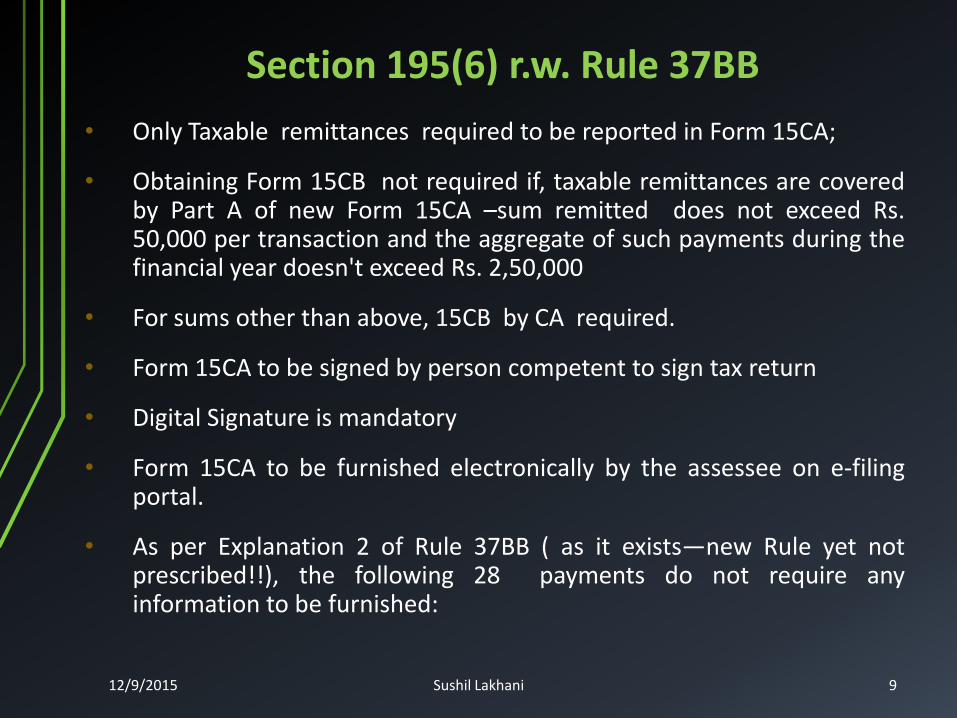

Section 195(6) r.w. Rule 37BB

• Only Taxable remittances required to be reported in Form 15CA;

• Obtaining Form 15CB not required if, taxable remittances are covered by Part A of new Form 15CA –sum remitted does not exceed Rs. 50,000 per transaction and the aggregate of such payments during the financial year doesn't exceed Rs. 2,50,000

• For sums other than above, 15CB by CA required.

• Form 15CA to be signed by person competent to sign tax return

• Digital Signature is mandatory

• Form 15CA to be furnished electronically by the assessee on e-filing portal.

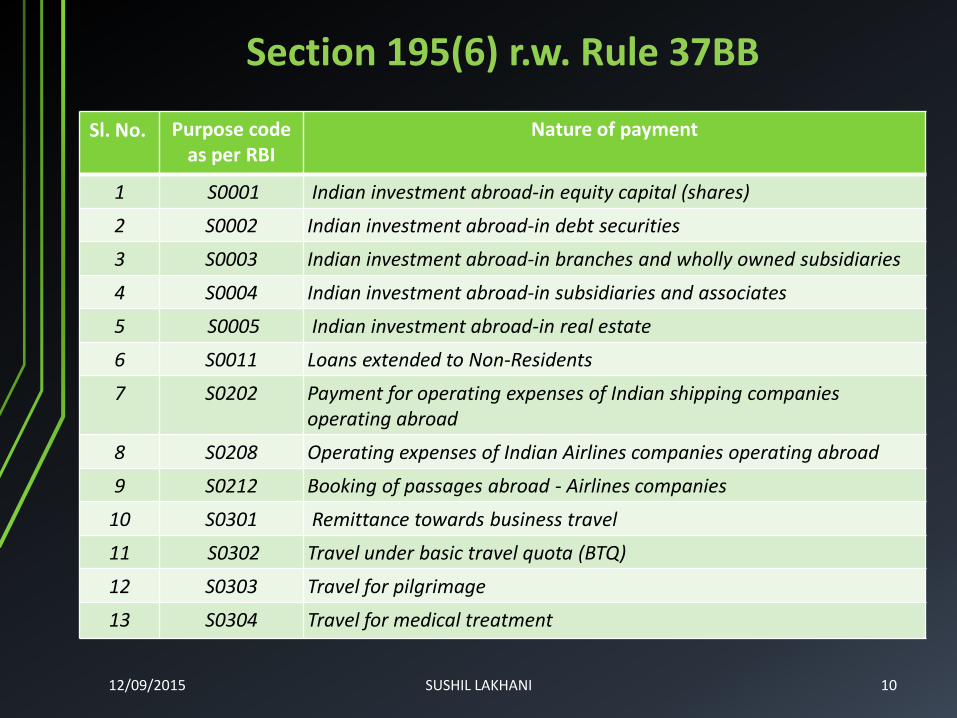

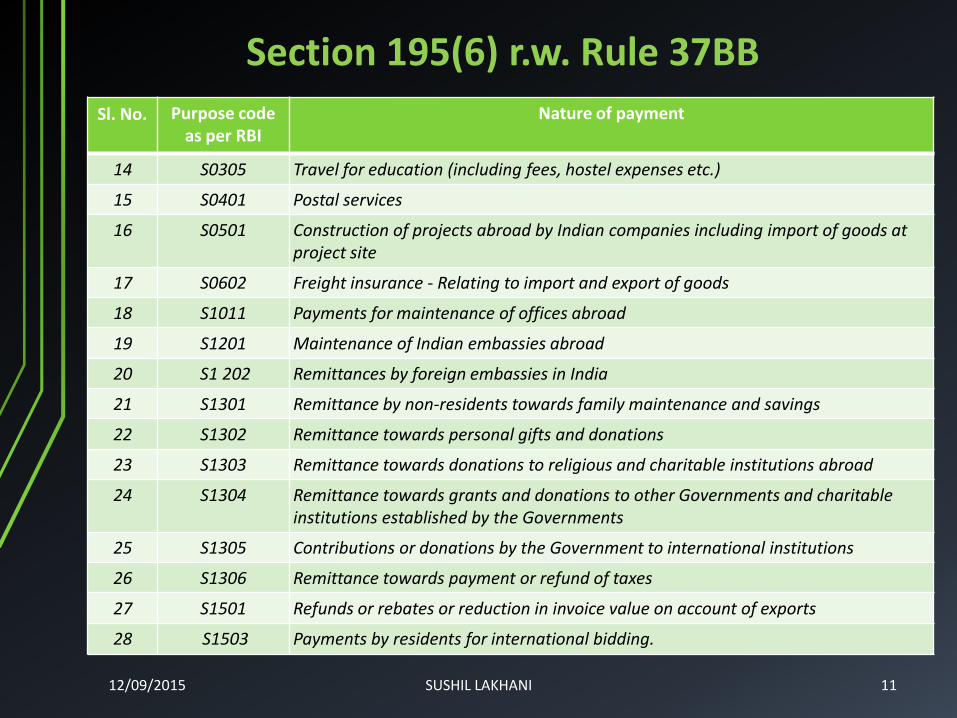

• As per Explanation 2 of Rule 37BB ( as it exists—new Rule yet not prescribed!!), the following 28 payments do not require any information to be furnished:

12/9/2015 Sushil Lakhani 9

Sl. No. Purpose code as per RBI

Nature of payment

1 S0001 Indian investment abroad-in equity capital (shares)

2 S0002 Indian investment abroad-in debt securities

3 S0003 Indian investment abroad-in branches and wholly owned subsidiaries

4 S0004 Indian investment abroad-in subsidiaries and associates

5 S0005 Indian investment abroad-in real estate

6 S0011 Loans extended to Non-Residents

7 S0202 Payment for operating expenses of Indian shipping companies operating abroad

8 S0208 Operating expenses of Indian Airlines companies operating abroad

9 S0212 Booking of passages abroad - Airlines companies

10 S0301 Remittance towards business travel

11 S0302 Travel under basic travel quota (BTQ)

12 S0303 Travel for pilgrimage

13 S0304 Travel for medical treatment

12/09/2015 SUSHIL LAKHANI 10

Section 195(6) r.w. Rule 37BB

Sl. No. Purpose code as per RBI

Nature of payment

14 S0305 Travel for education (including fees, hostel expenses etc.)

15 S0401 Postal services

16 S0501 Construction of projects abroad by Indian companies including import of goods at project site

17 S0602 Freight insurance - Relating to import and export of goods

18 S1011 Payments for maintenance of offices abroad

19 S1201 Maintenance of Indian embassies abroad

20 S1 202 Remittances by foreign embassies in India

21 S1301 Remittance by non-residents towards family maintenance and savings

22 S1302 Remittance towards personal gifts and donations

23 S1303 Remittance towards donations to religious and charitable institutions abroad

24 S1304 Remittance towards grants and donations to other Governments and charitable institutions established by the Governments

25 S1305 Contributions or donations by the Government to international institutions

26 S1306 Remittance towards payment or refund of taxes

27 S1501 Refunds or rebates or reduction in invoice value on account of exports

28 S1503 Payments by residents for international bidding.

12/09/2015 SUSHIL LAKHANI 11

Section 195(6) r.w. Rule 37BB

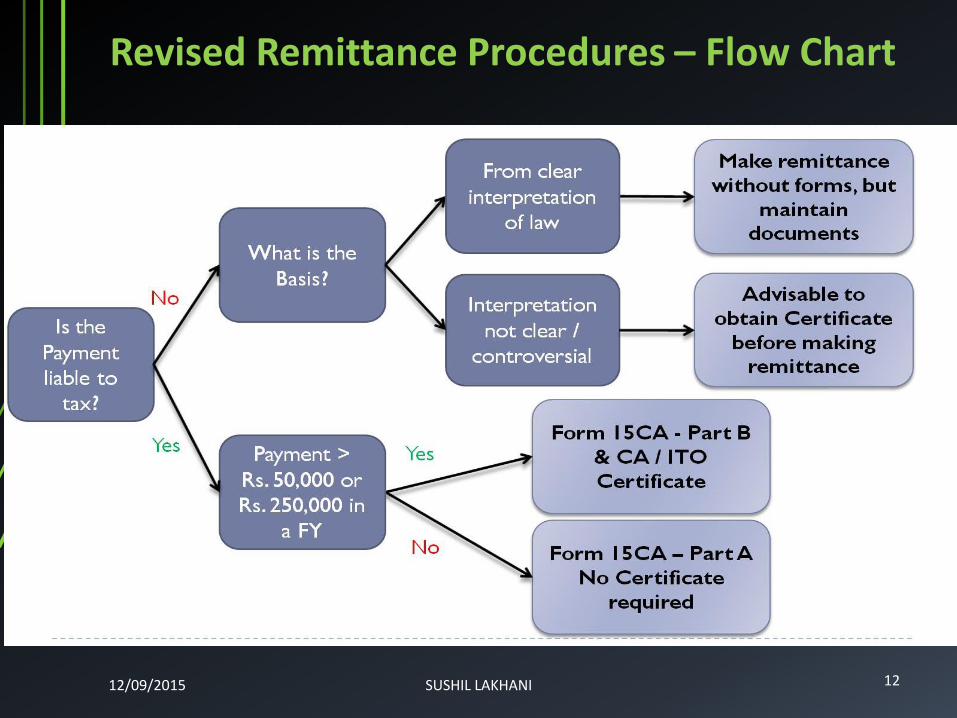

Revised Remittance Procedures – Flow Chart

12/09/2015 SUSHIL LAKHANI 12

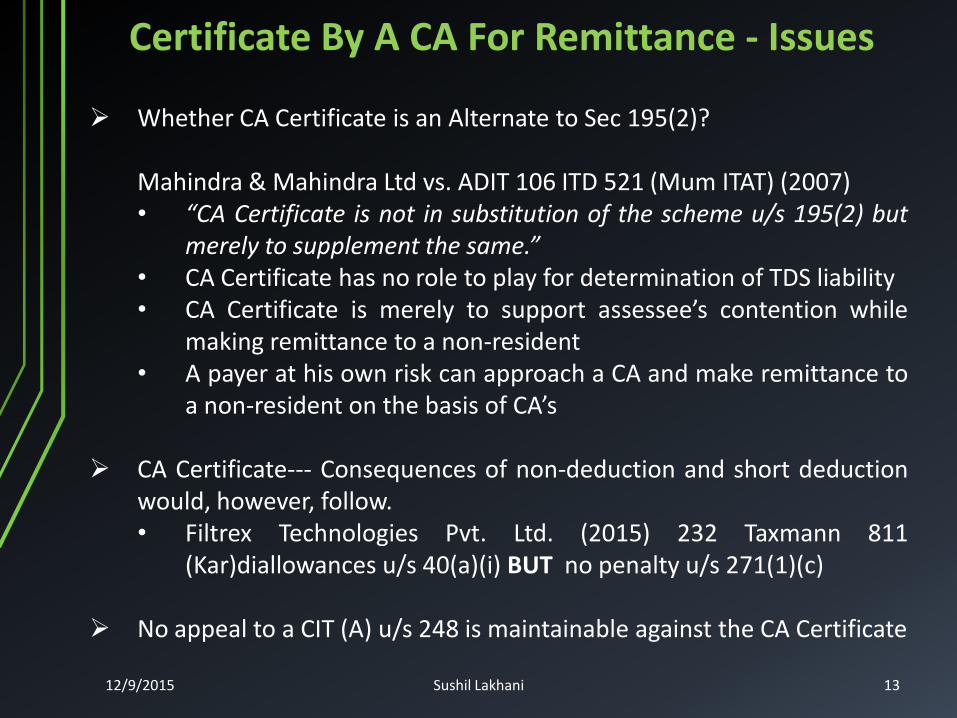

Whether CA Certificate is an Alternate to Sec 195(2)?

Mahindra & Mahindra Ltd vs. ADIT 106 ITD 521 (Mum ITAT) (2007) • “CA Certificate is not in substitution of the scheme u/s 195(2) but

merely to supplement the same.” • CA Certificate has no role to play for determination of TDS liability • CA Certificate is merely to support assessee’s contention while

making remittance to a non-resident • A payer at his own risk can approach a CA and make remittance to

a non-resident on the basis of CA’s

CA Certificate--- Consequences of non-deduction and short deduction would, however, follow. • Filtrex Technologies Pvt. Ltd. (2015) 232 Taxmann 811

(Kar)diallowances u/s 40(a)(i) BUT no penalty u/s 271(1)(c)

No appeal to a CIT (A) u/s 248 is maintainable against the CA Certificate

Certificate By A CA For Remittance - Issues

12/9/2015 Sushil Lakhani 13

PART - B

TAX RESIDENCY CERTIFICATE (S. 90(4)) AND

IMPLICATIONS OF SECTION 206AA

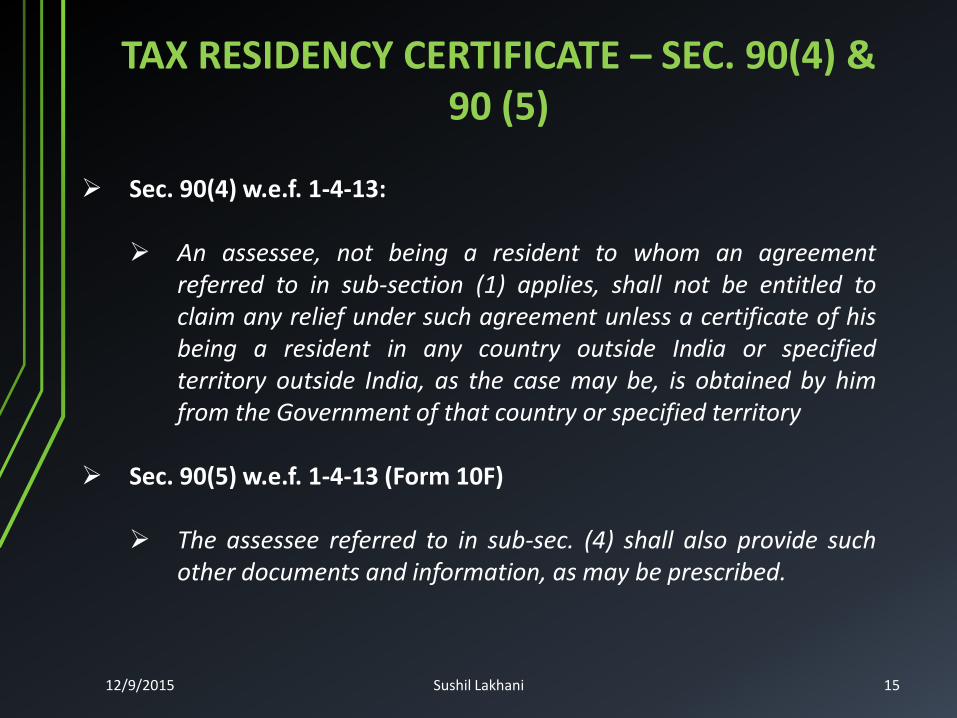

TAX RESIDENCY CERTIFICATE – SEC. 90(4) & 90 (5)

Sec. 90(4) w.e.f. 1-4-13:

An assessee, not being a resident to whom an agreement referred to in sub-section (1) applies, shall not be entitled to claim any relief under such agreement unless a certificate of his being a resident in any country outside India or specified territory outside India, as the case may be, is obtained by him from the Government of that country or specified territory

Sec. 90(5) w.e.f. 1-4-13 (Form 10F)

The assessee referred to in sub-sec. (4) shall also provide such other documents and information, as may be prescribed.

12/9/2015 Sushil Lakhani 15

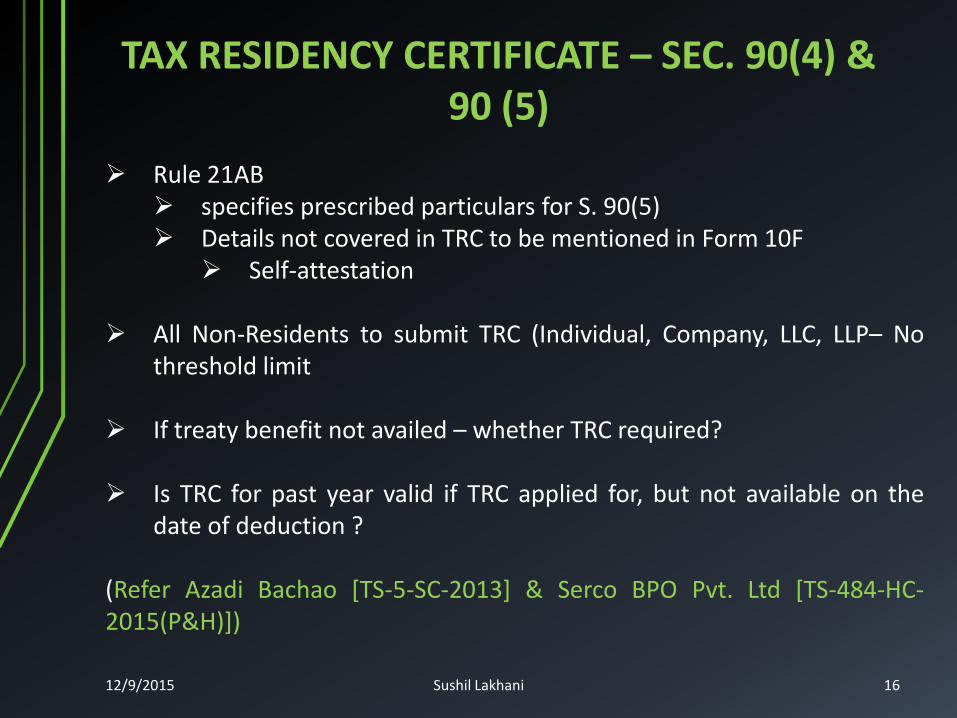

Rule 21AB specifies prescribed particulars for S. 90(5) Details not covered in TRC to be mentioned in Form 10F

Self-attestation

All Non-Residents to submit TRC (Individual, Company, LLC, LLP– No threshold limit

If treaty benefit not availed – whether TRC required?

Is TRC for past year valid if TRC applied for, but not available on the

date of deduction ? (Refer Azadi Bachao [TS-5-SC-2013] & Serco BPO Pvt. Ltd [TS-484-HC-2015(P&H)])

12/9/2015 Sushil Lakhani 16

TAX RESIDENCY CERTIFICATE – SEC. 90(4) & 90 (5)

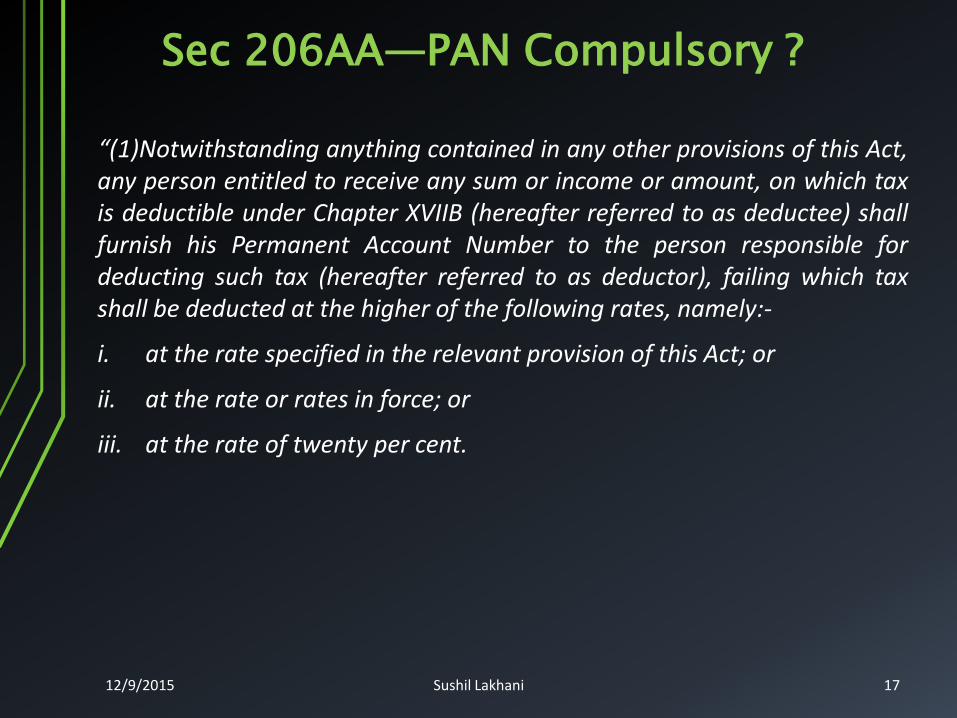

Sec 206AA—PAN Compulsory ?

“(1)Notwithstanding anything contained in any other provisions of this Act, any person entitled to receive any sum or income or amount, on which tax is deductible under Chapter XVIIB (hereafter referred to as deductee) shall furnish his Permanent Account Number to the person responsible for deducting such tax (hereafter referred to as deductor), failing which tax shall be deducted at the higher of the following rates, namely:-

i. at the rate specified in the relevant provision of this Act; or

ii. at the rate or rates in force; or

iii. at the rate of twenty per cent.

12/9/2015 Sushil Lakhani 17

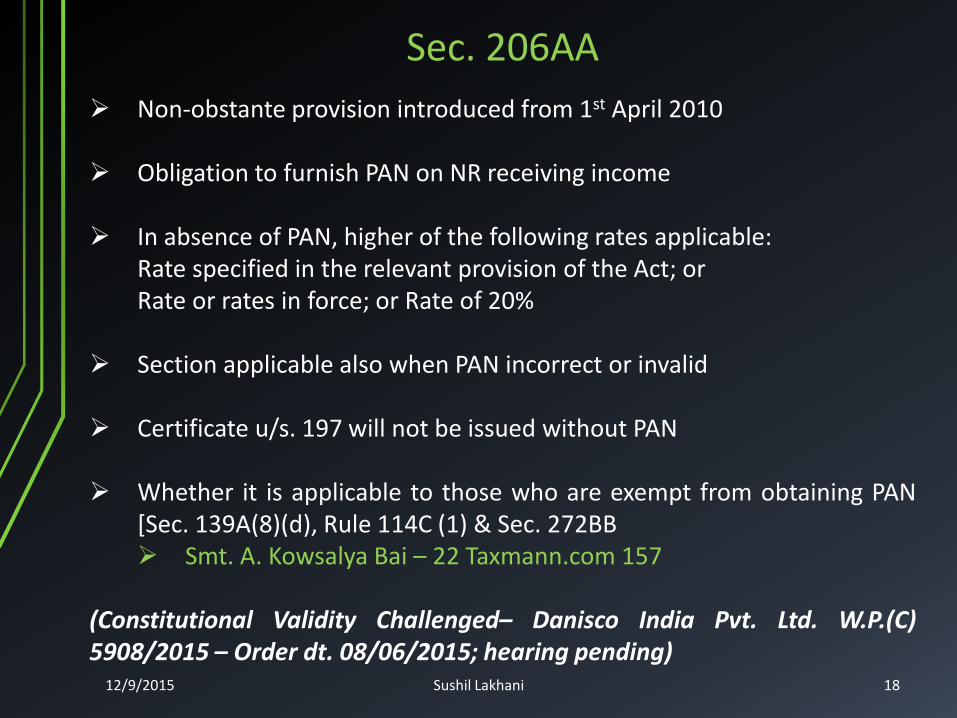

Sec. 206AA

Non-obstante provision introduced from 1st April 2010

Obligation to furnish PAN on NR receiving income In absence of PAN, higher of the following rates applicable: Rate specified in the relevant provision of the Act; or Rate or rates in force; or Rate of 20%

Section applicable also when PAN incorrect or invalid Certificate u/s. 197 will not be issued without PAN

Whether it is applicable to those who are exempt from obtaining PAN

[Sec. 139A(8)(d), Rule 114C (1) & Sec. 272BB Smt. A. Kowsalya Bai – 22 Taxmann.com 157

(Constitutional Validity Challenged– Danisco India Pvt. Ltd. W.P.(C) 5908/2015 – Order dt. 08/06/2015; hearing pending)

12/9/2015 Sushil Lakhani 18

Sec 206AA - Issues

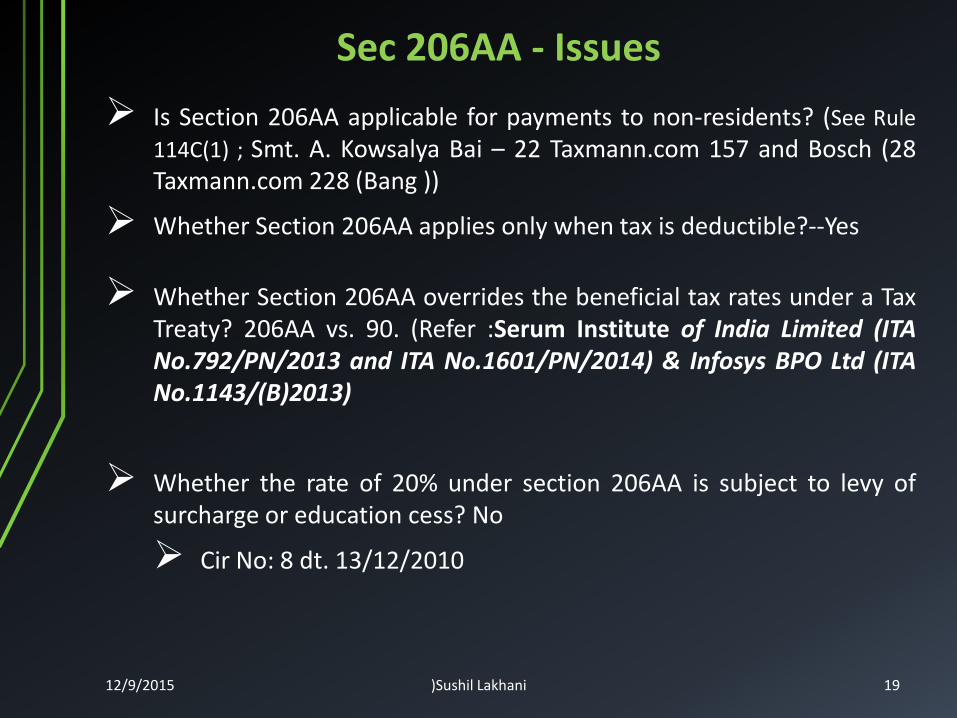

Is Section 206AA applicable for payments to non-residents? (See Rule

114C(1) ; Smt. A. Kowsalya Bai – 22 Taxmann.com 157 and Bosch (28 Taxmann.com 228 (Bang ))

Whether Section 206AA applies only when tax is deductible?--Yes

Whether Section 206AA overrides the beneficial tax rates under a Tax Treaty? 206AA vs. 90. (Refer :Serum Institute of India Limited (ITA No.792/PN/2013 and ITA No.1601/PN/2014) & Infosys BPO Ltd (ITA No.1143/(B)2013)

Whether the rate of 20% under section 206AA is subject to levy of surcharge or education cess? No

Cir No: 8 dt. 13/12/2010

12/9/2015 )Sushil Lakhani 19

Sec. 206AA r.w. Sec. 195A

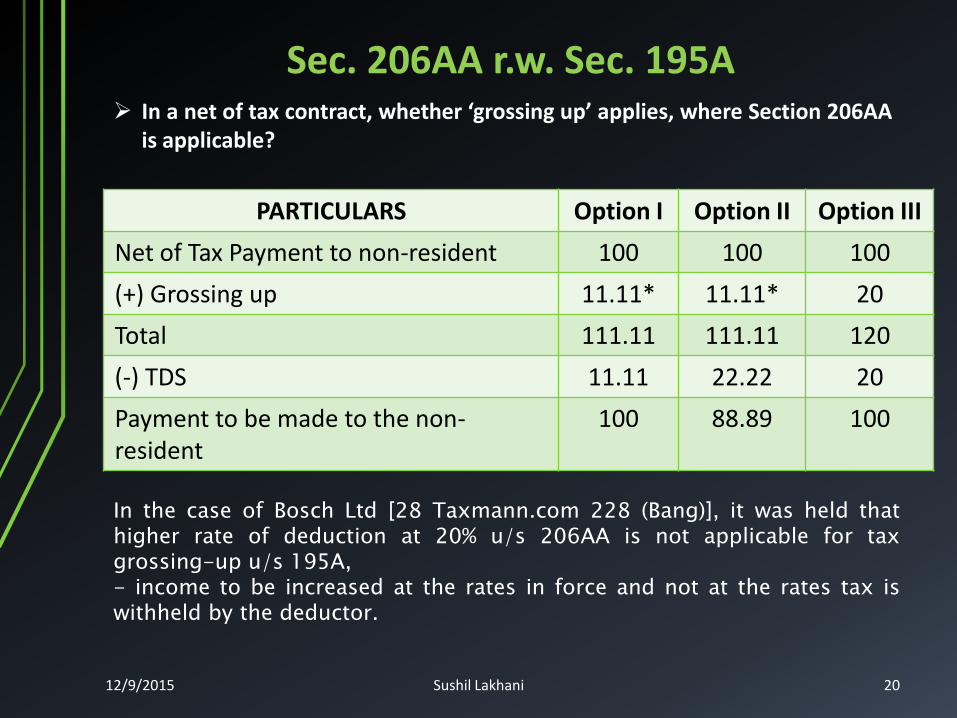

PARTICULARS Option I Option II Option III

Net of Tax Payment to non-resident 100 100 100

(+) Grossing up 11.11* 11.11* 20

Total 111.11 111.11 120

(-) TDS 11.11 22.22 20

Payment to be made to the non-resident

100 88.89 100

12/9/2015 Sushil Lakhani 20

In the case of Bosch Ltd [28 Taxmann.com 228 (Bang)], it was held that higher rate of deduction at 20% u/s 206AA is not applicable for tax grossing-up u/s 195A, - income to be increased at the rates in force and not at the rates tax is withheld by the deductor.

In a net of tax contract, whether ‘grossing up’ applies, where Section 206AA is applicable?

Yes

No

• No

No

Yes

Yes

No

No

Yes Yes Yes

No

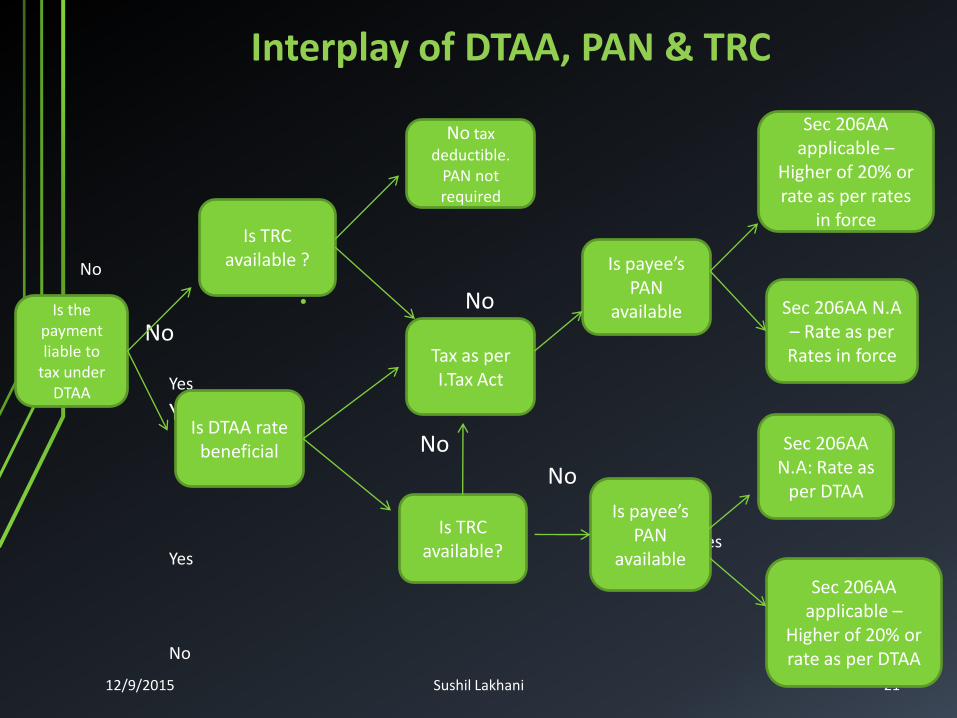

12/9/2015 Sushil Lakhani 21

Is the payment liable to

tax under DTAA

Is TRC available ?

No tax deductible.

PAN not required

Is DTAA rate beneficial

Tax as per I.Tax Act

Is TRC available?

Is payee’s PAN

available

Is payee’s PAN

available

Sec 206AA N.A: Rate as

per DTAA

Sec 206AA applicable –

Higher of 20% or rate as per DTAA

Sec 206AA applicable –

Higher of 20% or rate as per rates

in force

Sec 206AA N.A – Rate as per Rates in force

Interplay of DTAA, PAN & TRC

PART - C

Some Issues with respect to taxability of Non-residents

12/9/2015 Sushil Lakhani 23

SOURCE RULE

1. Business Profits Taxable if Business Connection in India or property or asset or source in India or transfer of a capital asset situated in India.{New retrospective Explanations 4 and 5 to section 9(1)(i) for meaning of “through” and to cover indirect transfers}

2. Salaries Taxable if services are rendered in India [Section 9(1)(ii)] (Refer Eli Lilly (SC))

3. Dividends Taxable if paid by an Indian Company [Section 9(1)(iv)]- (At present exempt)

4. Capital Gains on Shares / Property

Taxable if situs of Shares / Property in India

5. Rental from Properties Taxable if situs of Property in India

6. Interest/Royalty/FTS Taxable if sourced from India

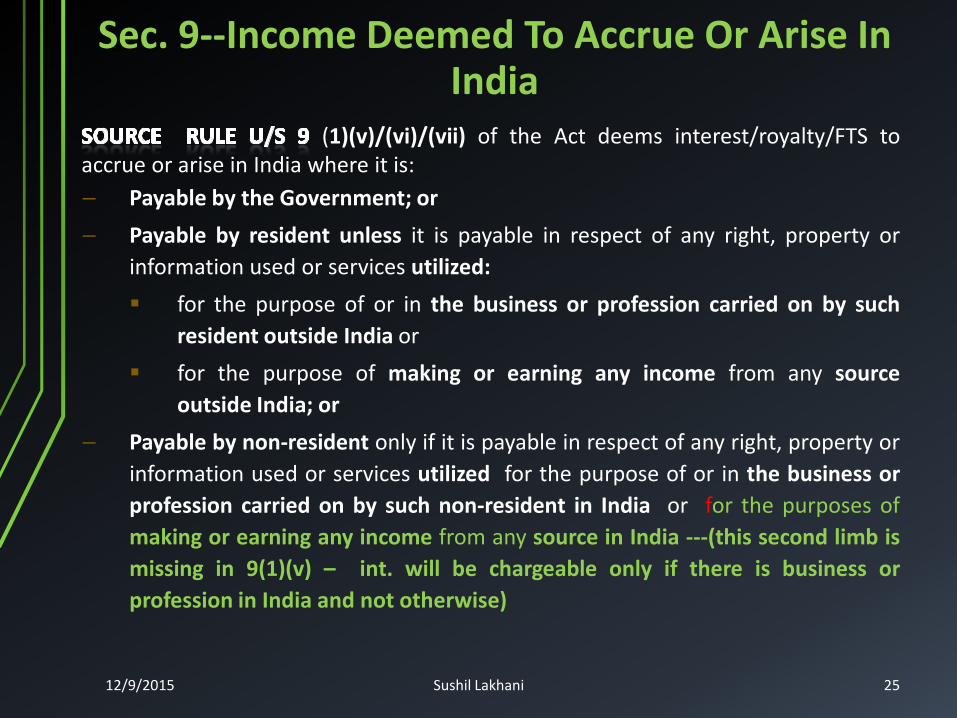

Sec. 9--Income Deemed To Accrue Or Arise In India

12/9/2015 Sushil Lakhani 24

(1)(v)/(vi)/(vii) of the Act deems interest/royalty/FTS to accrue or arise in India where it is:

– Payable by the Government; or

– Payable by resident unless it is payable in respect of any right, property or

information used or services utilized:

for the purpose of or in the business or profession carried on by such

resident outside India or

for the purpose of making or earning any income from any source

outside India; or

– Payable by non-resident only if it is payable in respect of any right, property or

information used or services utilized for the purpose of or in the business or

profession carried on by such non-resident in India or for the purposes of

making or earning any income from any source in India ---(this second limb is

missing in 9(1)(v) – int. will be chargeable only if there is business or

profession in India and not otherwise)

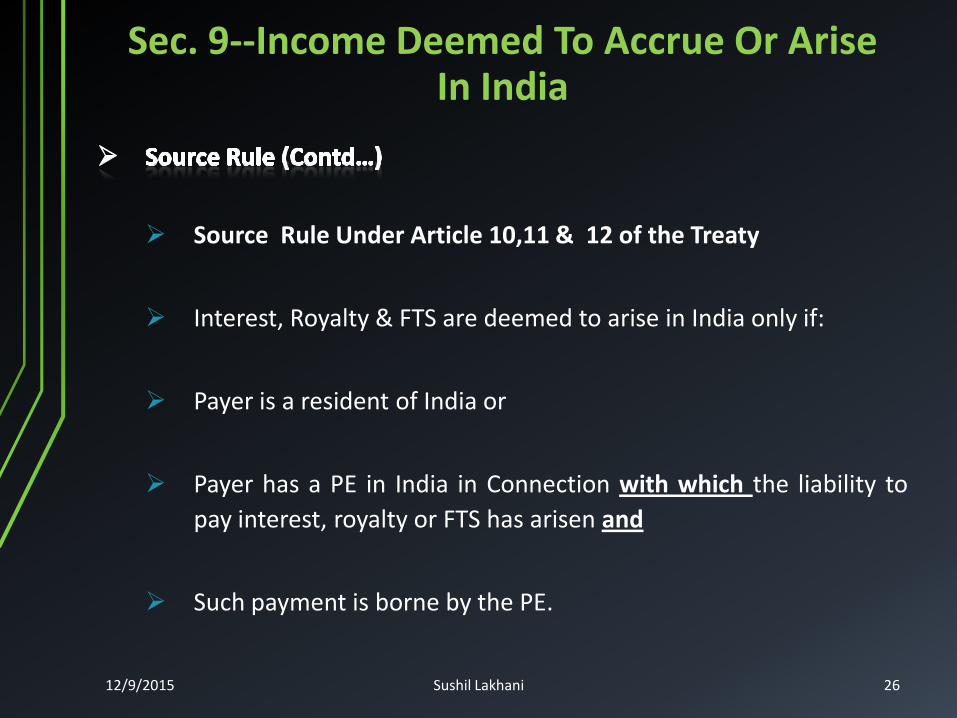

Sec. 9--Income Deemed To Accrue Or Arise In India

12/9/2015 Sushil Lakhani 25

Source Rule Under Article 10,11 & 12 of the Treaty

Interest, Royalty & FTS are deemed to arise in India only if:

Payer is a resident of India or

Payer has a PE in India in Connection with which the liability to

pay interest, royalty or FTS has arisen and

Such payment is borne by the PE.

Sec. 9--Income Deemed To Accrue Or Arise In India

12/9/2015 Sushil Lakhani 26

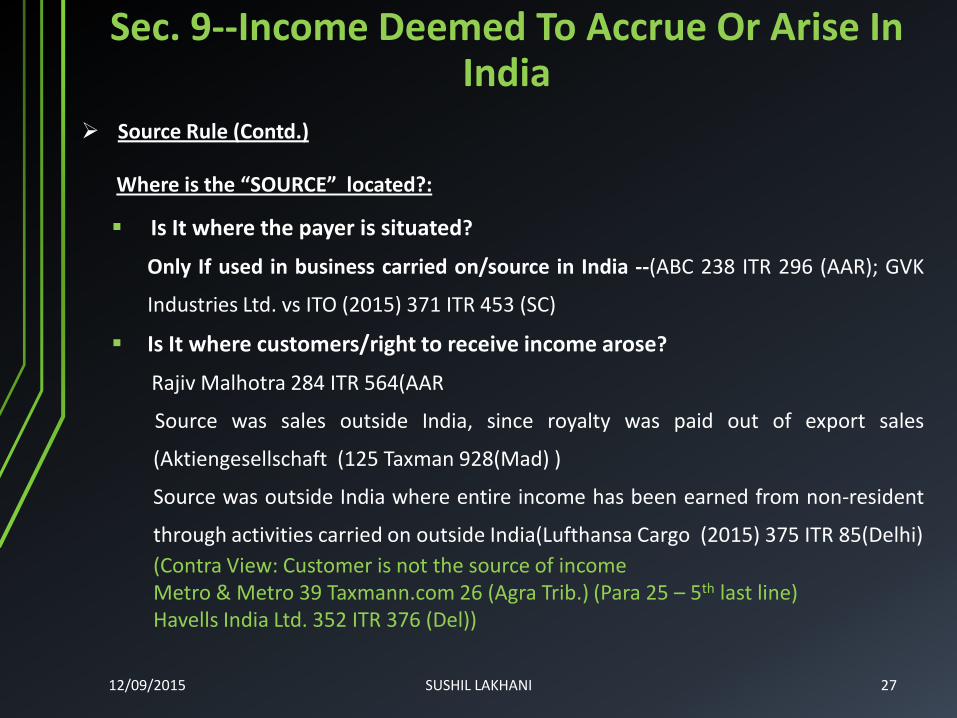

Source Rule (Contd.)

Where is the “SOURCE” located?:

Is It where the payer is situated?

Only If used in business carried on/source in India --(ABC 238 ITR 296 (AAR); GVK

Industries Ltd. vs ITO (2015) 371 ITR 453 (SC)

Is It where customers/right to receive income arose?

Rajiv Malhotra 284 ITR 564(AAR

Source was sales outside India, since royalty was paid out of export sales

(Aktiengesellschaft (125 Taxman 928(Mad) )

Source was outside India where entire income has been earned from non-resident

through activities carried on outside India(Lufthansa Cargo (2015) 375 ITR 85(Delhi)

(Contra View: Customer is not the source of income Metro & Metro 39 Taxmann.com 26 (Agra Trib.) (Para 25 – 5th last line) Havells India Ltd. 352 ITR 376 (Del))

27 12/09/2015 SUSHIL LAKHANI

Sec. 9--Income Deemed To Accrue Or Arise In India

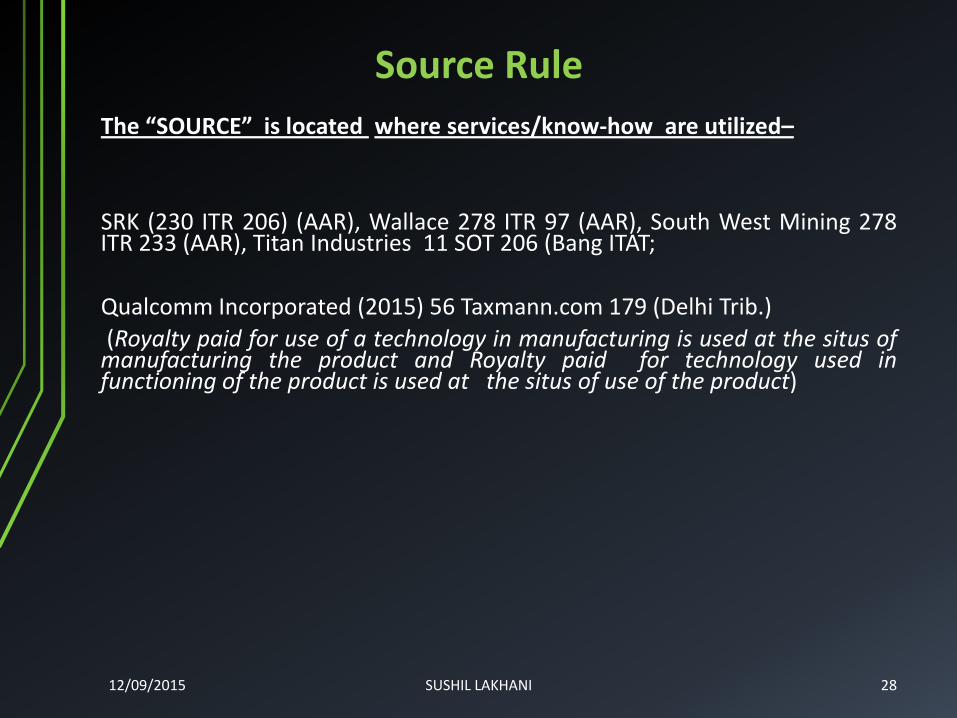

Source Rule

The “SOURCE” is located where services/know-how are utilized–

SRK (230 ITR 206) (AAR), Wallace 278 ITR 97 (AAR), South West Mining 278 ITR 233 (AAR), Titan Industries 11 SOT 206 (Bang ITAT;

Qualcomm Incorporated (2015) 56 Taxmann.com 179 (Delhi Trib.)

(Royalty paid for use of a technology in manufacturing is used at the situs of manufacturing the product and Royalty paid for technology used in functioning of the product is used at the situs of use of the product)

28 12/09/2015 SUSHIL LAKHANI

12/9/2015 Sushil Lakhani 29

Implications w.r.t. explanation to section 195 (1)

Implications w.r.t. explanation to section 195 (1)

• New Explanation 2 added retrospectively:

“For the removal of doubts, it is herby clarified that the obligation to comply with sub section (1) and to make deduction thereunder applies and shall be deemed to have always applied and extends and shall be deemed to have always extended to all persons, residents or non-residents, whether or not the non-resident person has-

• A residence or place of business connection in India; or

• Any other presence in any manner whatsoever in India”.

• Does not override exclusion limb of section 9(1)(v), (vi), (vii)

• Prithvi Information Solutions Ltd. – 47 Taxmann.com 214 (Hyd. Trib.)

• Lufthansa Cargo India (2015) 375 ITR 85 (Del)

12/9/2015 Sushil Lakhani 30

12/9/2015 Sushil Lakhani 31

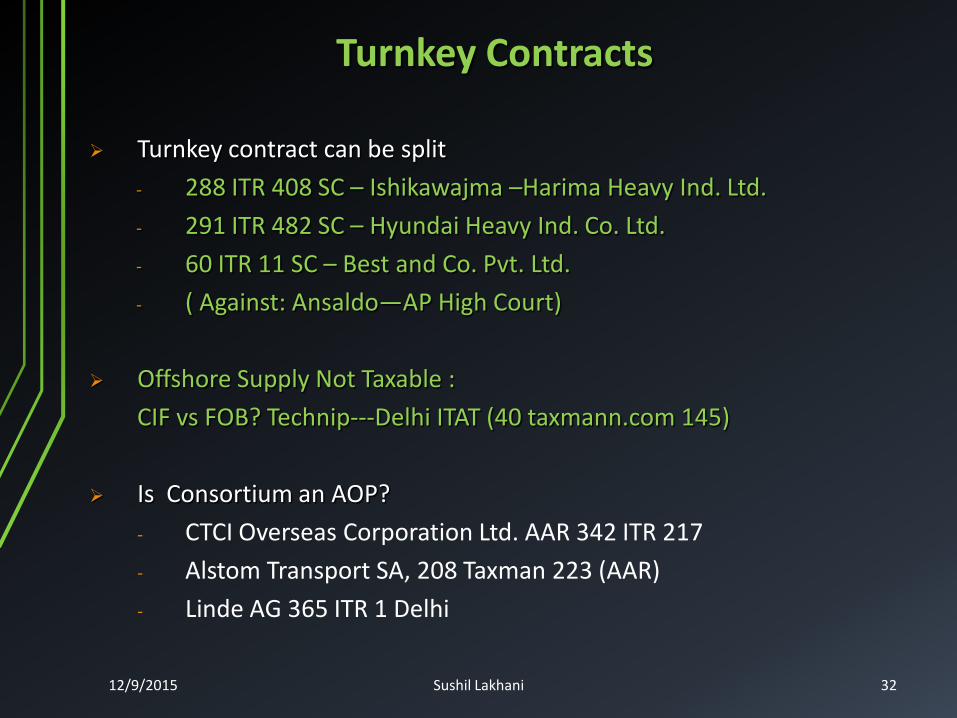

TURNKEY CONTRACTS

Turnkey Contracts

Turnkey contract can be split

- 288 ITR 408 SC – Ishikawajma –Harima Heavy Ind. Ltd.

- 291 ITR 482 SC – Hyundai Heavy Ind. Co. Ltd.

- 60 ITR 11 SC – Best and Co. Pvt. Ltd.

- ( Against: Ansaldo—AP High Court)

Offshore Supply Not Taxable :

CIF vs FOB? Technip---Delhi ITAT (40 taxmann.com 145)

Is Consortium an AOP?

- CTCI Overseas Corporation Ltd. AAR 342 ITR 217

- Alstom Transport SA, 208 Taxman 223 (AAR)

- Linde AG 365 ITR 1 Delhi

12/9/2015 Sushil Lakhani 32

Consortium – Turnkey Contract

• TDS on payment by consortium to members – section 40ba

Payments to the partners not in their capacity as partners, but made for the specific services rendered by them - CIT v. Rajam Ramaswamy and Sons [2008] 298 ITR 325 (Mad) HC

- CIT v. Gemini Productions [1977] 110 ITR 847 Mad.

- CIT v. Chitra Kalpana [1988] 169 ITR 678 AP

12/9/2015 Sushil Lakhani 33

12/9/2015 Sushil Lakhani 34

EXPORT COMMISSION

Export Commission • Not taxable

• Transformers & Electricals Kerala Ltd. – 50 Taxmann.com 454

• Sumit Gupta – 50 Taxmann.com 60

• Kikani Exports India Pvt. Ltd. – 49 Taxmann.com 601

• Orient Express, 56 taxmann.com 331 (Mad.)

• Faizan Shoes (P.) Ltd., 367 ITR 155 (Mad.)

• SKF Boilers & Driers (P.) Ltd., 343 ITR 385 (AAR)

• Avon Organics Ltd., 28 taxmann.com 170 (Hyd.)

• Priyadarshini Spinning Mills (P.) Ltd., 25 taxmann.com 574 (Hyd.)

• Circular No. 7 of 2009

• Vilas N. Tamhankar – 40 CCH 0770 (Mum Trib.)

• Held Taxable

– Contrary view taken by AAR in case of Wallace Pharma (278 ITR 97) & Rajiv Malhotra 284 ITR 564 (AAR)

– Marketing Survey Services and identifying potential customers—is “consultancy services”—(39 Taxmann.com 50 ) (Cochin Tribunal)

12/9/2015 Sushil Lakhani 35

12/9/2015 Sushil Lakhani 36

REIMBURSEMENT

Reimbursement

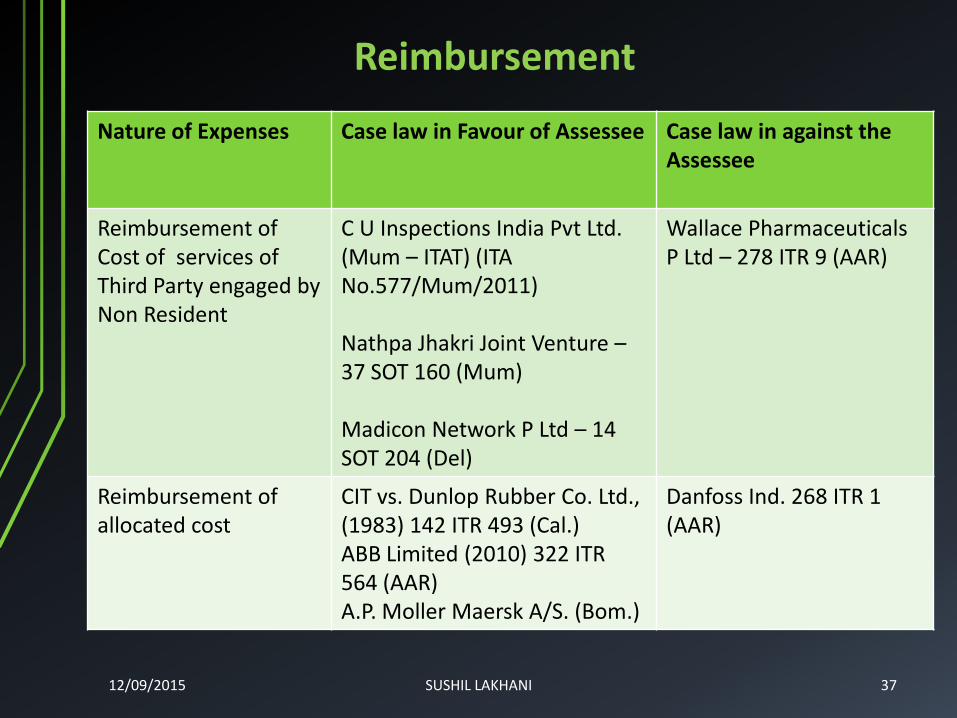

12/09/2015 SUSHIL LAKHANI 37

Nature of Expenses Case law in Favour of Assessee Case law in against the Assessee

Reimbursement of Cost of services of Third Party engaged by Non Resident

C U Inspections India Pvt Ltd. (Mum – ITAT) (ITA No.577/Mum/2011) Nathpa Jhakri Joint Venture – 37 SOT 160 (Mum) Madicon Network P Ltd – 14 SOT 204 (Del)

Wallace Pharmaceuticals P Ltd – 278 ITR 9 (AAR)

Reimbursement of allocated cost

CIT vs. Dunlop Rubber Co. Ltd., (1983) 142 ITR 493 (Cal.) ABB Limited (2010) 322 ITR 564 (AAR) A.P. Moller Maersk A/S. (Bom.)

Danfoss Ind. 268 ITR 1 (AAR)

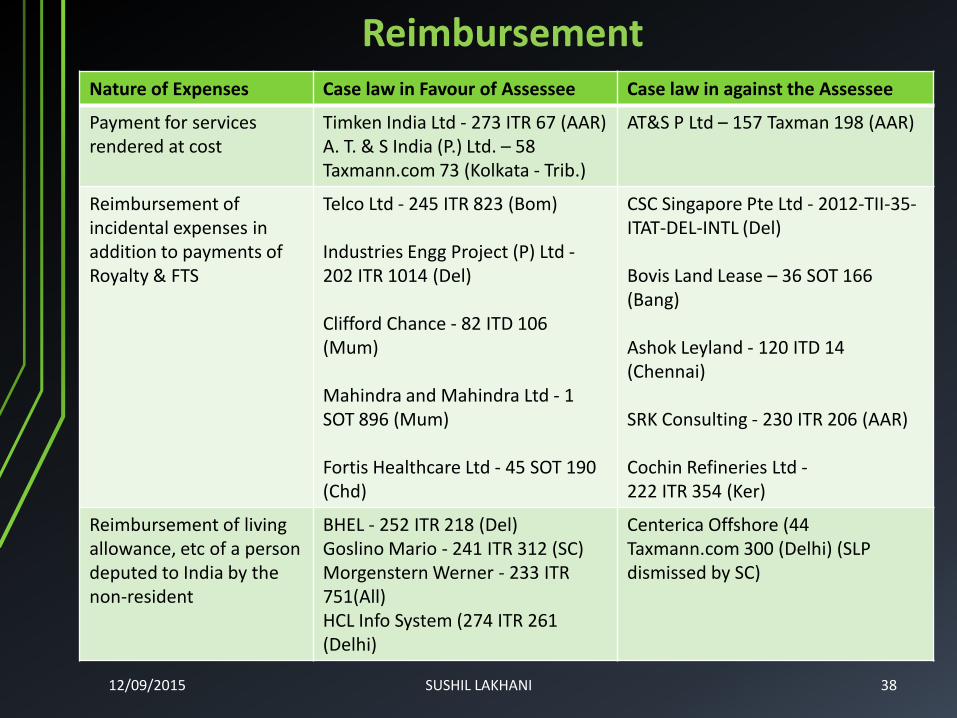

Reimbursement Nature of Expenses Case law in Favour of Assessee Case law in against the Assessee

Payment for services rendered at cost

Timken India Ltd - 273 ITR 67 (AAR) A. T. & S India (P.) Ltd. – 58 Taxmann.com 73 (Kolkata - Trib.)

AT&S P Ltd – 157 Taxman 198 (AAR)

Reimbursement of incidental expenses in addition to payments of Royalty & FTS

Telco Ltd - 245 ITR 823 (Bom) Industries Engg Project (P) Ltd - 202 ITR 1014 (Del) Clifford Chance - 82 ITD 106 (Mum) Mahindra and Mahindra Ltd - 1 SOT 896 (Mum) Fortis Healthcare Ltd - 45 SOT 190 (Chd)

CSC Singapore Pte Ltd - 2012-TII-35- ITAT-DEL-INTL (Del) Bovis Land Lease – 36 SOT 166 (Bang) Ashok Leyland - 120 ITD 14 (Chennai) SRK Consulting - 230 ITR 206 (AAR) Cochin Refineries Ltd - 222 ITR 354 (Ker)

Reimbursement of living allowance, etc of a person deputed to India by the non-resident

BHEL - 252 ITR 218 (Del) Goslino Mario - 241 ITR 312 (SC) Morgenstern Werner - 233 ITR 751(All) HCL Info System (274 ITR 261 (Delhi)

Centerica Offshore (44 Taxmann.com 300 (Delhi) (SLP dismissed by SC)

12/09/2015 SUSHIL LAKHANI 38

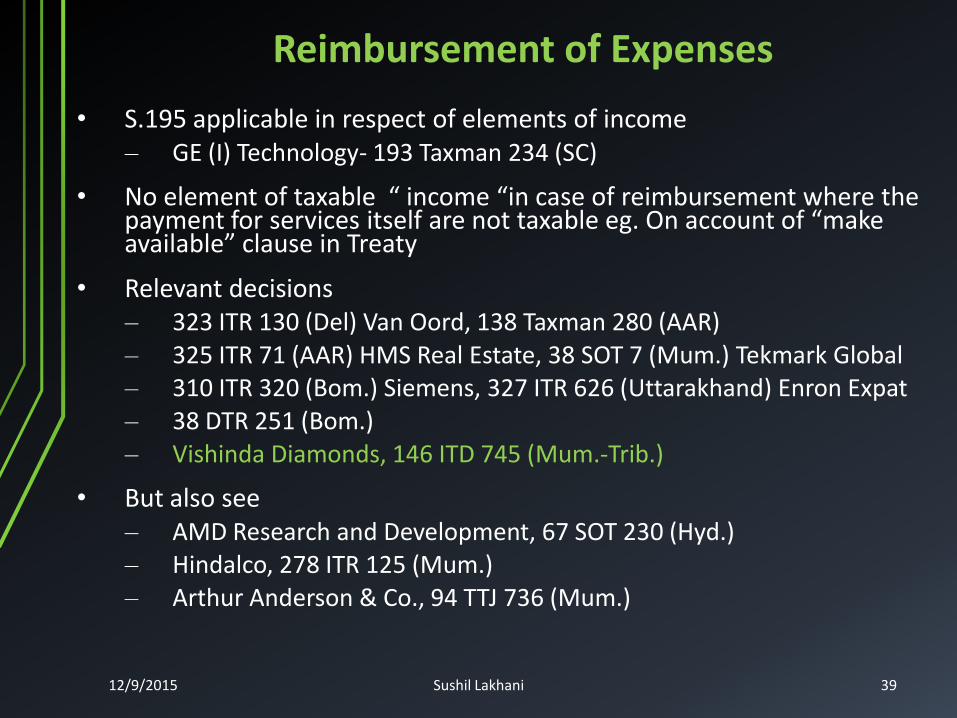

Reimbursement of Expenses

• S.195 applicable in respect of elements of income – GE (I) Technology- 193 Taxman 234 (SC)

• No element of taxable “ income “in case of reimbursement where the payment for services itself are not taxable eg. On account of “make available” clause in Treaty

• Relevant decisions – 323 ITR 130 (Del) Van Oord, 138 Taxman 280 (AAR) – 325 ITR 71 (AAR) HMS Real Estate, 38 SOT 7 (Mum.) Tekmark Global – 310 ITR 320 (Bom.) Siemens, 327 ITR 626 (Uttarakhand) Enron Expat – 38 DTR 251 (Bom.) – Vishinda Diamonds, 146 ITD 745 (Mum.-Trib.)

• But also see – AMD Research and Development, 67 SOT 230 (Hyd.) – Hindalco, 278 ITR 125 (Mum.) – Arthur Anderson & Co., 94 TTJ 736 (Mum.)

12/9/2015 Sushil Lakhani 39

12/9/2015 Sushil Lakhani 40

Software and E-commerce payments

New Explanations 4, 5 and 6 to section 9(1)(vi) Explanation 4: For the removal of doubts it is hereby clarified that the transfer of all or any rights in respect of any such a right, property or information includes and has always included transfer of all or any right for use or right to use a computer software (including granting of a license) irrespective of the medium through which such right is transferred. Explanation 5 : For the removal of doubts it is hereby clarified that royalty includes and has always included consideration in respect of any right, property or information whether or not –

• The possession or control of such a right, property or information is with the payer

• such a right, property or information is used directly by the payer

• The location of such a right, property or information is in India

Explanation 6.—For the removal of doubts, it is hereby clarified that the expression “process” includes and shall be deemed to have always included transmission by satellite (including up-linking, amplification, conversion for down-linking of any signal), cable, optic fibre or by any other similar technology, whether or not such process is secret;’.

41 12/09/2015 SUSHIL LAKHANI

Software and E-Commerce Payments r. w. explanation of 9(1)(vi)

India considers – payments for roaming calls, spectrum license, leasing of transponder as Royalty – India’s position on OECD Commentary.

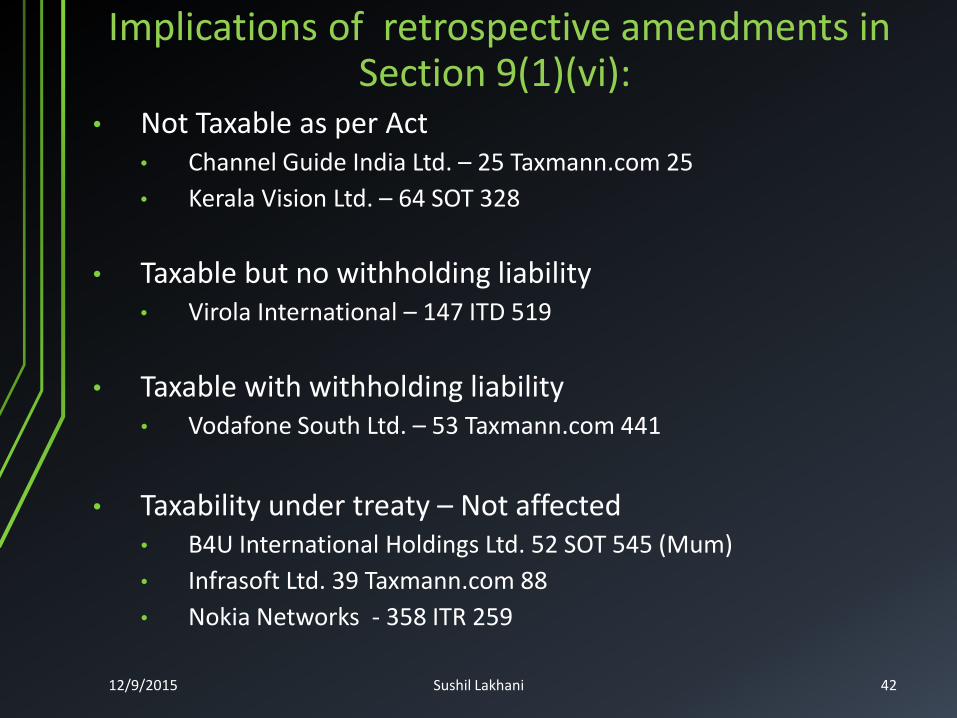

Implications of retrospective amendments in Section 9(1)(vi):

• Not Taxable as per Act • Channel Guide India Ltd. – 25 Taxmann.com 25

• Kerala Vision Ltd. – 64 SOT 328

• Taxable but no withholding liability • Virola International – 147 ITD 519

• Taxable with withholding liability • Vodafone South Ltd. – 53 Taxmann.com 441

• Taxability under treaty – Not affected • B4U International Holdings Ltd. 52 SOT 545 (Mum)

• Infrasoft Ltd. 39 Taxmann.com 88

• Nokia Networks - 358 ITR 259

12/9/2015 Sushil Lakhani 42

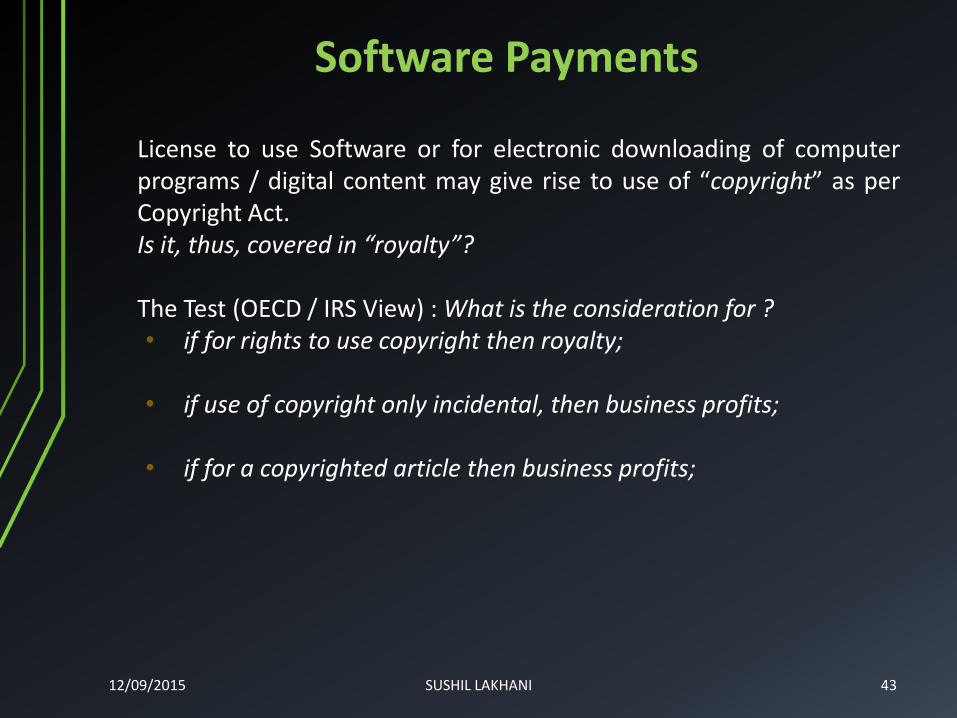

License to use Software or for electronic downloading of computer

programs / digital content may give rise to use of “copyright” as per Copyright Act.

Is it, thus, covered in “royalty”? The Test (OECD / IRS View) : What is the consideration for ?

• if for rights to use copyright then royalty; • if use of copyright only incidental, then business profits;

• if for a copyrighted article then business profits;

43 12/09/2015 SUSHIL LAKHANI

Software Payments

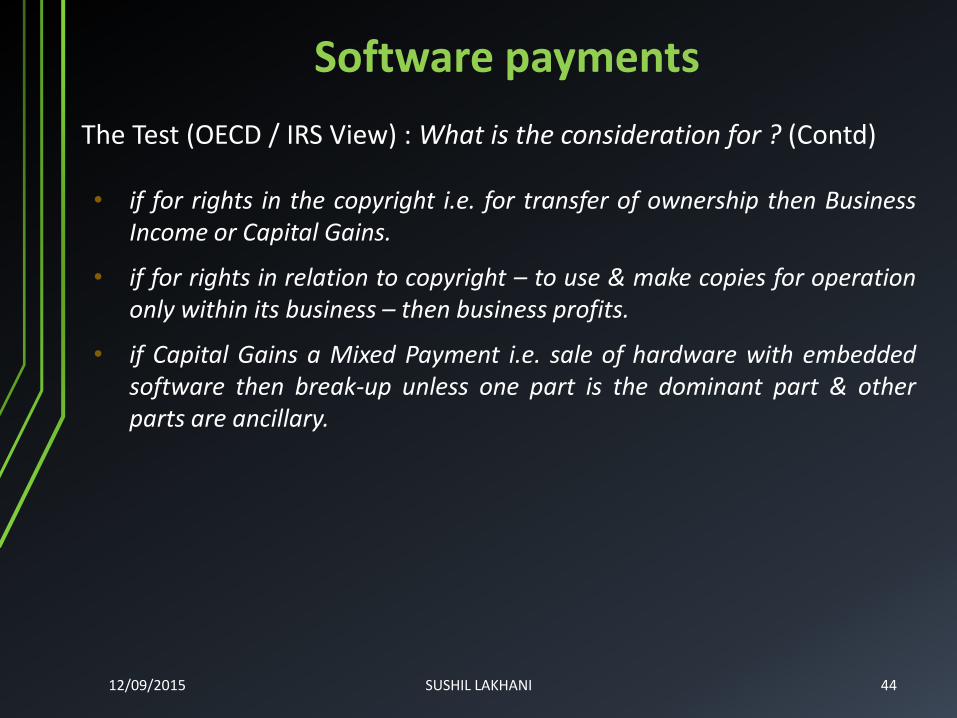

The Test (OECD / IRS View) : What is the consideration for ? (Contd)

• if for rights in the copyright i.e. for transfer of ownership then Business Income or Capital Gains.

• if for rights in relation to copyright – to use & make copies for operation only within its business – then business profits.

• if Capital Gains a Mixed Payment i.e. sale of hardware with embedded software then break-up unless one part is the dominant part & other parts are ancillary.

44 12/09/2015 SUSHIL LAKHANI

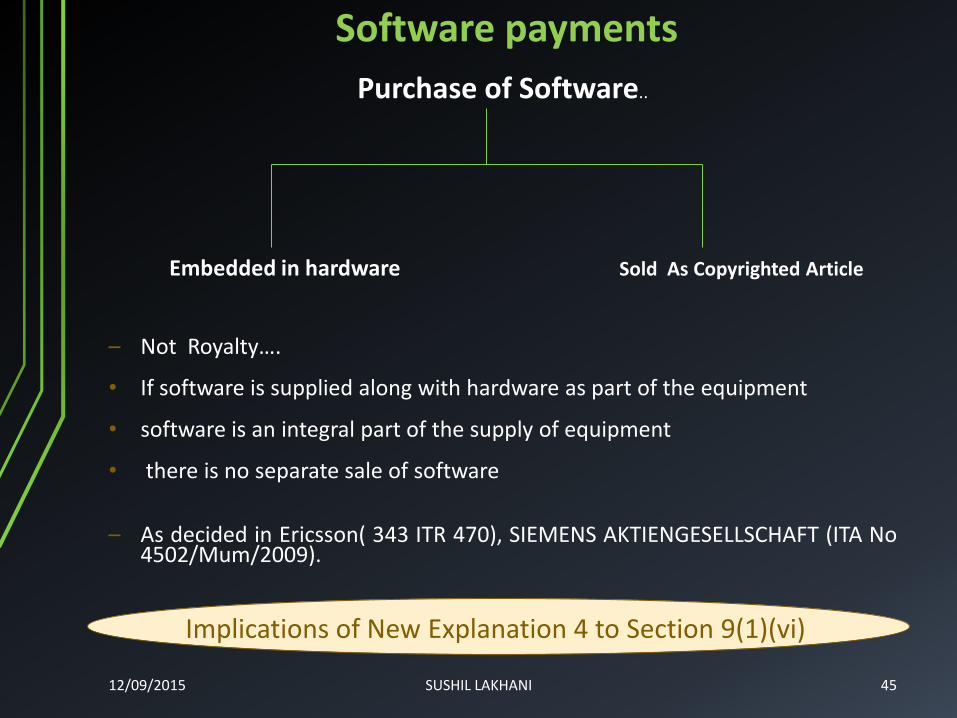

Software payments

Purchase of Software..

Embedded in hardware Sold As Copyrighted Article

– Not Royalty….

• If software is supplied along with hardware as part of the equipment

• software is an integral part of the supply of equipment

• there is no separate sale of software

– As decided in Ericsson( 343 ITR 470), SIEMENS AKTIENGESELLSCHAFT (ITA No 4502/Mum/2009).

45

Implications of New Explanation 4 to Section 9(1)(vi)

12/09/2015 SUSHIL LAKHANI

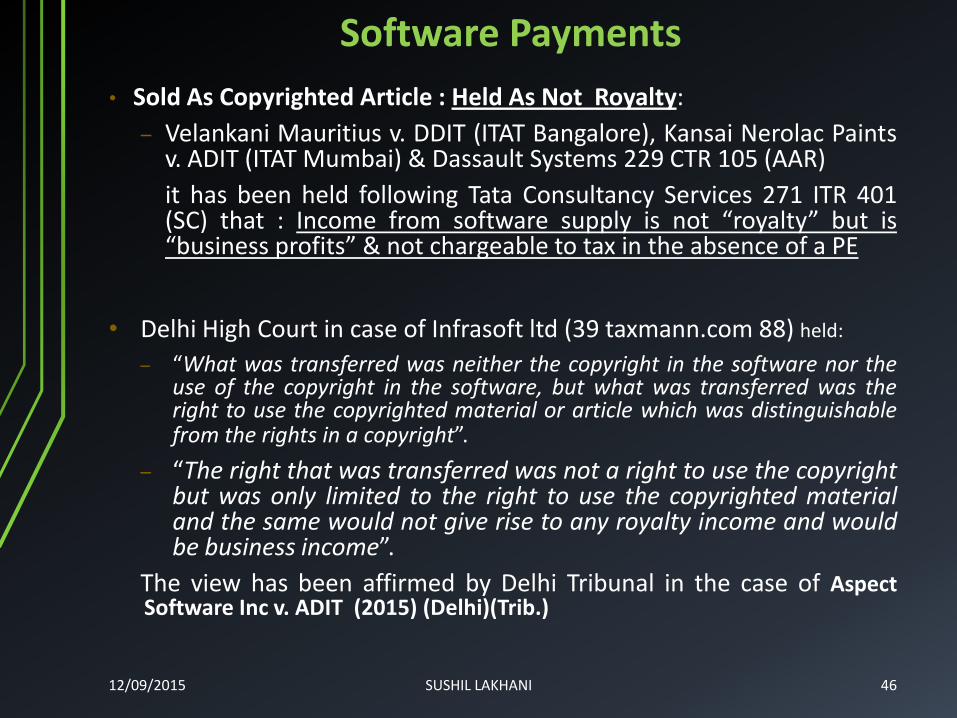

Software payments

• Sold As Copyrighted Article : Held As Not Royalty:

– Velankani Mauritius v. DDIT (ITAT Bangalore), Kansai Nerolac Paints v. ADIT (ITAT Mumbai) & Dassault Systems 229 CTR 105 (AAR)

it has been held following Tata Consultancy Services 271 ITR 401 (SC) that : Income from software supply is not “royalty” but is “business profits” & not chargeable to tax in the absence of a PE

• Delhi High Court in case of Infrasoft ltd (39 taxmann.com 88) held:

– “What was transferred was neither the copyright in the software nor the use of the copyright in the software, but what was transferred was the right to use the copyrighted material or article which was distinguishable from the rights in a copyright”.

– “The right that was transferred was not a right to use the copyright but was only limited to the right to use the copyrighted material and the same would not give rise to any royalty income and would be business income”.

The view has been affirmed by Delhi Tribunal in the case of Aspect Software Inc v. ADIT (2015) (Delhi)(Trib.)

12/09/2015 SUSHIL LAKHANI 46

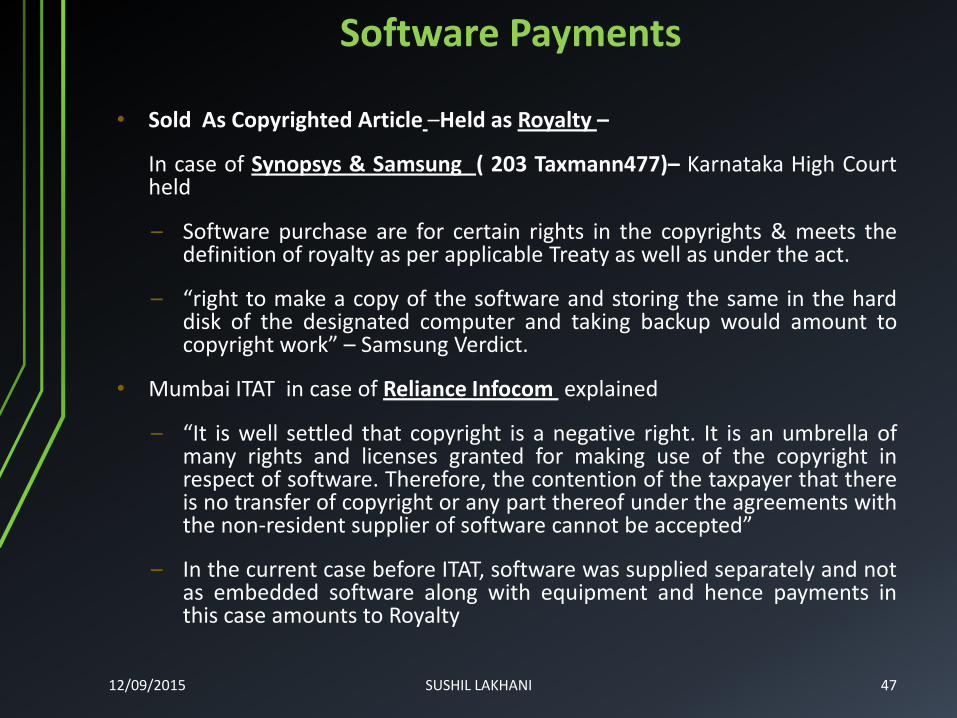

Software Payments

• Sold As Copyrighted Article –Held as Royalty –

In case of Synopsys & Samsung ( 203 Taxmann477)– Karnataka High Court held

– Software purchase are for certain rights in the copyrights & meets the definition of royalty as per applicable Treaty as well as under the act.

– “right to make a copy of the software and storing the same in the hard disk of the designated computer and taking backup would amount to copyright work” – Samsung Verdict.

• Mumbai ITAT in case of Reliance Infocom explained

– “It is well settled that copyright is a negative right. It is an umbrella of many rights and licenses granted for making use of the copyright in respect of software. Therefore, the contention of the taxpayer that there is no transfer of copyright or any part thereof under the agreements with the non-resident supplier of software cannot be accepted”

– In the current case before ITAT, software was supplied separately and not as embedded software along with equipment and hence payments in this case amounts to Royalty

47 12/09/2015 SUSHIL LAKHANI

Software Payments

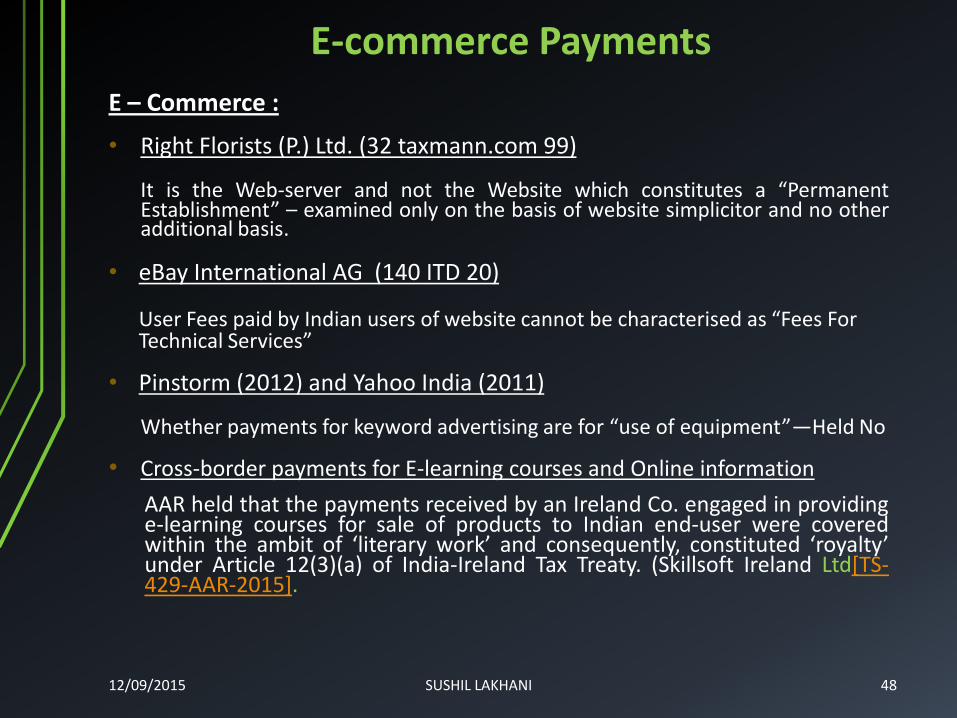

E – Commerce :

• Right Florists (P.) Ltd. (32 taxmann.com 99)

It is the Web-server and not the Website which constitutes a “Permanent Establishment” – examined only on the basis of website simplicitor and no other additional basis.

• eBay International AG (140 ITD 20)

User Fees paid by Indian users of website cannot be characterised as “Fees For Technical Services”

• Pinstorm (2012) and Yahoo India (2011)

Whether payments for keyword advertising are for “use of equipment”—Held No

• Cross-border payments for E-learning courses and Online information

AAR held that the payments received by an Ireland Co. engaged in providing e-learning courses for sale of products to Indian end-user were covered within the ambit of ‘literary work’ and consequently, constituted ‘royalty’ under Article 12(3)(a) of India-Ireland Tax Treaty. (Skillsoft Ireland Ltd[TS-429-AAR-2015].

48 12/09/2015 SUSHIL LAKHANI

E-commerce Payments

12/9/2015 Sushil Lakhani 49

Questions…

SUSHIL LAKHANI Sushil Lakhani & Associates, Chartered Accountants 4th Floor, Bharat House, 104, Mumbai Samachar Marg, Fort, Mumbai-400023 Tel: +91-22-40693900 (M) : 9821111852 E-mail : [email protected]

12/09/2015 SUSHIL LAKHANI 50