STANDPOINT - Citi UK IPB · GLOBAL MARKET ANALYSIS FROM INTERNATIONAL PERSONAL BANKING STANDPOINT...

12

STAND POINT GLOBAL MARKET ANALYSIS FROM INTERNATIONAL PERSONAL BANKING NORTH AMERICA EUROPE JAPAN LATIN AMERICA ASIA PACIFIC Q4 08 GLOBAL INVESTMENT STRATEGY Opinions, forecasts, and weightings expressed by Citigroup Global Consumer Group Investments may not be attained or suitable for all investors. Past performance is no guarantee of future results. There are additional risks associated with international investments, including foreign, political, currency and economic factors to consider. Please contact your financial professional to determine what is suitable for your individual situation. The American Paradox Considering that it was US mortgage-lending that initially triggered the major crisis in the global financial system, the US economy and financial markets have been surprisingly resilient compared to other markets so far this year. In the second quarter, US GDP expanded by 3.3% compared to contractions of -0.8% and -3.0% in the Euro Area and Japan, respectively. In equity markets, the S&P500 index of US stocks has fallen -20.6% year to date, as of September 30, compared to the larger -28.3% drop in the MSCI World Free ex-US index in local currency terms over the same period. Compounding this effect, the US dollar staged a sharp rebound in the late summer against a broad array of currencies. It seems contrary to many commentators’ earlier expectations that the US financial assets have not suffered the most from the credit crunch in 2008. But what does the outlook hold for 2009? Can this American paradox continue? Downside economic risks have intensified The events that unfolded in September, when a major US investment bank was allowed to fail and the US Treasury came to the rescue of two mortgage giants and the world’s largest insurance company, will likely have a meaningful impact on US economic growth over the coming year. As a result, asset values on banks’ balance sheets have likely deteriorated, further constraining the ability of global banks to make new loans to individuals and businesses. Citi analysts are quite clear about the consequences of this. For starters, more restricted mortgage lending may further damage the already-depressed US housing market and consumer spending. Also businesses may struggle to invest or even pay their operating expenses without readily available credit, thereby diminishing labour market prospects (see chart). Let there be little doubt regarding the global nature of these challenges. Many financial institutions worldwide are similarly in a weaker position to offer loans. Citi analysts actually forecast that Euro Area, UK and Japanese GDP growth may continue to be weaker than in the US in 2009. Such a prognosis also has significant negative implications for the Asia-Pacific region and the emerging economies, even if the banking sectors in these regions have managed to avoid most of the sub prime mortgage fallout according to data compiled by Bloomberg. America provides solutions too In the US, the Federal Reserve has orchestrated a coordinated plan with other central banks to inject liquidity into the global banking system. In addition, the US Treasury and US Federal Reserve have put together the most aggressive plan yet to counteract weakness in the global financial system in the form of the Troubled Asset Relief Program (TARP). Although details are sketchy at the time of writing, it is envisaged PAGE 2: GCG Outlook PAGE 3: Regional Analyses PAGE 9: Behind the Numbers PAGE 10: Asset Allocations 1

Transcript of STANDPOINT - Citi UK IPB · GLOBAL MARKET ANALYSIS FROM INTERNATIONAL PERSONAL BANKING STANDPOINT...

GLOBAL MARKET ANALYSIS FROM INTERNATIONAL PERSONAL BANKING

STANDPOINTGLOBAL MARKET ANALYSIS FROM INTERNATIONAL PERSONAL BANKING

NORTH AMERICA

EUROPE

JAPAN

LATIN AMERICA

ASIA PACIFIC

Q4 08

GLOBAL INVESTMENT STRATEGY

Opinions, forecasts, and weightings expressed by Citigroup Global Consumer Group Investments may not be attained or suitable for all investors. Past performance is no guarantee of future results. There are additional risks associated with international investments, including foreign, political, currency and economic factors to consider. Please contact your financial professional to determine what is suitable for your individual situation.

The American ParadoxConsidering that it was US mortgage-lending that initially triggered the major crisis in the global financial system, the US economy and financial markets have been surprisingly resilient compared to other markets so far this year. In the second quarter, US GDP expanded by 3.3% compared to contractions of -0.8% and -3.0% in the Euro Area and Japan, respectively. In equity markets, the S&P500 index of US stocks has fallen -20.6% year to date, as of September 30, compared to the larger -28.3% drop in the MSCI World Free ex-US index in local currency terms over the same period. Compounding this effect, the US dollar staged a sharp rebound in the late summer against a broad array of currencies. It seems contrary to many commentators’ earlier expectations that the US financial assets have not suffered the most from the credit crunch in 2008. But what does the outlook hold for 2009? Can this American paradox continue?

Downside economic risks have intensified

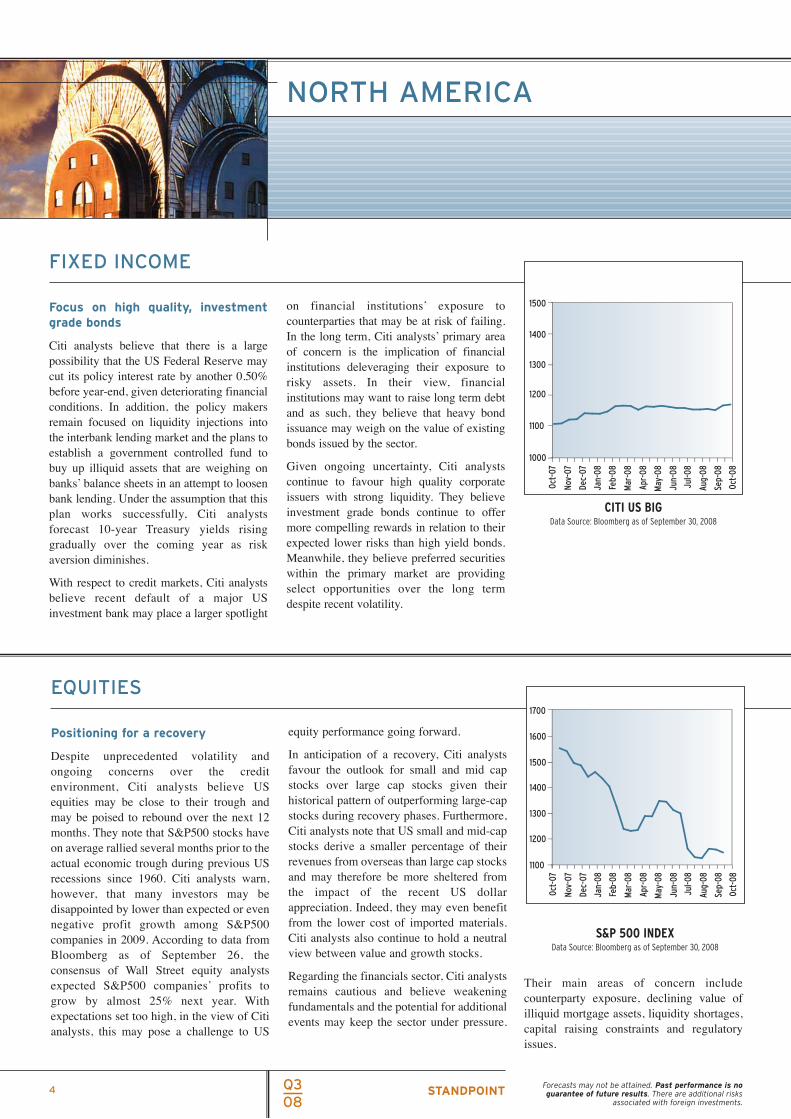

The events that unfolded in September, when a major US investment bank was allowed to fail and the US Treasury came to the rescue of two mortgage giants and the world’s largest insurance company, will likely have a meaningful impact on US economic growth over the coming year. As a result, asset values on banks’ balance sheets have likely deteriorated, further constraining the ability of global banks to make new loans to individuals and businesses. Citi analysts are quite clear

about the consequences of this. For starters, more restricted mortgage lending may further damage the already-depressed US housing market and consumer spending. Also businesses may struggle to invest or even pay their operating expenses without readily available credit, thereby diminishing labour market prospects (see chart).

Let there be little doubt regarding the global nature of these challenges. Many financial institutions worldwide are similarly in a weaker position to offer loans. Citi analysts actually forecast that Euro Area, UK and Japanese GDP growth may continue to be weaker than in the US in 2009. Such a prognosis also has significant negative implications for the Asia-Pacific region and the emerging economies, even if the banking sectors in these regions have managed to avoid most of the sub prime mortgage fallout according to data compiled by Bloomberg.

America provides solutions too

In the US, the Federal Reserve has orchestrated a coordinated plan with other central banks to inject liquidity into the global banking system. In addition, the US Treasury and US Federal Reserve have put together the most aggressive plan yet to counteract weakness in the global financial system in the form of the Troubled Asset Relief Program (TARP). Although details are sketchy at the time of writing, it is envisaged

PAGE 2: GCG Outlook

PAGE 3: Regional Analyses

PAGE 9: Behind the Numbers

PAGE 10: Asset Allocations 1

gcg outlook» A snapshot of the Global Consumer Group’s (GCG) global market views across a select group of asset classes, regions and currencies over the next six to twelve months.

Our Market Outlook reflects our assessment of each asset class independently of other asset classes. Our Portfolio Allocation reflects our relative assessment of each asset class in the context of a portfolio. Overall, we overweight global equities and underweight global bonds. Based largely on our outlook for US dollar appreciation over the coming year, we now favour US and emerging market equities over European and Japanese equities. Further insights on regional prospects can be found within.

GLOBAL EQUITIES

MARKET MARKET PORTFOLIO OUTLOOK ALLOCATION

POSITIVE OVERWEIGHT US Positive Overweight Europe Neutral Neutral Japan Neutral Neutral Latin America Positive Overweight Asia Pacific Positive Overweight Eastern Europe Positive Overweight

GLOBAL FIXED INCOME

MARKET MARKET PORTFOLIO OUTLOOK ALLOCATION

NEGATIVE UNDERWEIGHT US Investment Grade Negative Underweight Euro Investment Grade Neutral Underweight Japan Investment Grade Negative Underweight High Yield Negative Underweight Latin America EM Negative Underweight Asia Pacific EM Negative Underweight

ALTERNATIVE INVESTMENTS

MARKET PORTFOLIO OUTLOOK ALLOCATION

N/A NEUTRAL Hedge Funds Neutral Neutral

GLOBAL CURRENCIES

CURRENCY OUTLOOK OUTLOOK vs USD vs EUR

Euro Negative Yen Negative Positive Sterling Negative Negative US Dollar Positive

Data Source: Citi Global Markets Inc. Weightings provided by Citi Global Wealth Management Investment Strategy Committee and Citi Global Consumer Investments as of September 2008.

GLOBAL INVESTMENT

that a US$700bn government-controlled fund could be established to purchase illiquid bank assets. In doing so, it is intended to unburden bank balance sheets, thus enabling banks to resume lending activities. Citi analysts firmly believe that such action is required in order to help the US economy to avoid a more severe recession.

The measures taken by the US authorities contrast with the more muted policy responses elsewhere. Although the European Central Bank and Bank of England have actively participated in coordinated liquidity provisions along with the US Federal Reserve, they embarked on interest rate easing only recently in conjunction with four other central banks. Before then, their interest rate policies had appeared slanted towards concerns regarding lingering inflation rather than addressing intensifying economic and financial weaknesses. As global inflationary pressures continue to subside, Citi analysts believe that this may provide greater room for them to cut interest rates.

So what does this mean for financial markets?

The establishment of the TARP is likely to increase significantly the US government budget deficit over the coming years. Citi

5000

4000

1000

0

0%

10%

40%

50%

60%

1990 1995

Net Percentage of Senior Loan Officers Reporting Tigher Standards for Large and Medium Sized Businesses (left scale, inverted)

Change in US Non-farm Payrolls from Year Earlier, 000s (right scale)

-30%

3000

2000

-1000

-2000

-3000

-20%

-10%

20%

30%

70%

2005 2000

Source: EM Equities - MSCI EM Index; EM Bonds - Citi GEMS Index; Devel. Equities - MSCI World Index; Devel. Bonds Citi WorldBIG Govt. Index, hedged into USD

STRATEGY

analysts forecast the US government borrowing requirement reaching 6.5% of US GDP in 2009, from 3% this year. With this in mind, some commentators have questioned whether US Treasury paper may continue to be a haven of safety and whether the US dollar may weaken.

As Citi analysts point out, however, the consequences of financial stress are unlikely to fall on US assets alone. Citi analysts actually forecast the US dollar strengthening over the coming 12 months as foreign exchange markets factor in the deteriorating economic outlook outside the US and the potential for lower interest rates, particularly in Europe. The perception of rising financial risks may also continue to feed investors’ appetites for the safety of US Treasury paper, in their view. Indeed, US Treasury yields across all maturities fell in September, suggesting higher demand for this asset class amid higher volatility. Although the risks to the global corporate profit outlook are piled high, Citi analysts are still forecasting a rebound in global stock markets over the next year. Given their 12-month currency markets outlook, Citi analysts believe that US and emerging market equities may deliver higher total returns than European and Japanese equities.

Banking Lending and Jobs, 1990 - 2008 Data Source: Bloomberg as of September 30, 2008

Forecasts may not be attained. Past performance is no Q3 STANDPOINT guarantee of future results. There are additional risks associated with foreign investments. 08

2

‘ ‘ ‘ ‘ ‘ ‘

340

220

160

100

400

Jan-

08

Mar

-08

Apr-

08

Jun-

08

Jul-0

8

by 0.8% annualised rate in the second

strong growth in the first quarter but also the underlying deterioration in economic fundamentals. Citi analysts have reduced

for the second half of the year and 2009 amid poor sentiment and poor manufacturing

membership. So far the German government has been reluctant to opt for a fiscal stimulus package.

appeared to be chiefly concerned about

and wage growth from high commodity prices. Nonetheless, Citi analysts assume that the Bank may revise down its growth outlook further over time and that the

EUROPE

‘‘ ‘ ‘‘ ‘

280

Oct-

07

Nov-

07

Dec-

07

Feb-

08

May

-08

Aug-

08

Sep-

08

Oct-

08

FIXED INCOME

Interest rate cuts expected

The Euro Area economy, as expected by the Bloomberg consensus of analysts, contracted

quarter. This partly reflected a rebound from

their forecast of Euro Area economic activity

Until recently, the European Central Bank

potential second-round effects on inflation

headline inflation rate may drop sharply. order readings. Based on this, they forecast the Bank

incrementally lowering its policy interestWhile some fiscal easing may cushion the CITI EURO BIG (EUR) rate to 2.00% by the end of next year. On this economic slowdown in the Euro Area, Data Source: Bloomberg as of September 30, 2008 basis, Citi analysts expect a slight reductionFrance and Italy may be constrained in this respect since their government deficits are already close to the 3%-of-GDP limit, which is laid down by the rules of Euro Area

in German 10-year government bond yields over the coming year, which would result in coupon-like total returns for investors.

EQUITIES

Jan-

08

Mar

-08

Apr-

08

Jun-

08

Jul-0

8

400

365

330

Oct-

07

Nov-

07

Dec-

07

Feb-

08

May

-08

Aug-

08

Sep-

08

Oct-

08

295

260

Attractive equity market values Stoxx were to fall by a further 20-30%, this

provide some support would raise the price earnings ratio to around 13x, which would still be somewhat cheaper

Slowing European economic growth and than the average of the last 20 years.rising costs have taken their toll on the According to Citi analysts, this suggests thatcorporate sector. Although the consensus of much (if not all) of the bad news is alreadyequity analysts has been downgrading its priced into European equity markets thusexpectations for European profit growth for giving them some support against furthersome months, Citi analysts believe that downward moves. However, given Citi expectations are still set too high and may analysts’ outlook of the depreciating Euro therefore be vulnerable to disappoint going over the coming year, they believe that this forward. may weigh on the performance of European

In favour of the outlook for equity markets, equities in comparison to other international

however, Citi analysts believe that European equity markets. DJ STOXX 600 equity markets offer attractive value for investors. At the end of September the stocks in the DJ Stoxx index traded at values around 10 times higher than their expected profit levels for the coming year (price-earnings ratio), according to data from Bloomberg. Even if the profits of companies in the DJ

Forecasts may not be attained. Past performance is no guarantee of future results. There are additional risks associated with foreign investments.

Given the high global market volatility and slowing economic growth in Europe, Citi analysts remain selective and favour the outlook for defensive sectors such as health care, food & beverage and telecoms over the outlook for banks, autos, construction and retail stocks.

Q3STANDPOINT 08

Data Source: Bloomberg as of September 30, 2008

3

ëëëëëëë

ëëëëëëë

ëëëëëë

ëëëëëë

ëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëë

ëëëëëë

ëë

ëëëëëëë

ëëëëëëë

ëëëëëëë

ëëëëëëë

ëëëëëëë

ëëëëëëë

ëëëëëëë

ëëëëëëë

ëëëëëëë

ëëëëëëë

ëëëëëëë

ëëëëëëë

ëëëëëëë

ëëëëëëë

ëëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëëëëëë

ëë

ëëëëëë

ëë

1500

1400

1100

1000

Jan-

08

Mar

-08

Apr-

08

Jun-

08

Jul-0

8

possibility that the US Federal Reserve may cut its policy interest rate by another 0.50%

conditions. In addition, the policy makers remain focused on liquidity injections into the interbank lending market and the plans to establish a government controlled fund to buy up illiquid assets that are weighing on

bank lending. Under the assumption that this

on financial institutions’ exposure to counterparties that may be at risk of failing.

of concern is the implication of financial institutions deleveraging their exposure to risky assets. In their financial institutions may want to raise long term debt and as such, they believe that heavy bond issuance may weigh on the value of existing

continue to favour high quality corporate They believe

NORTH AMERICA

1300

1200

Oct-

07

Nov-

07

Dec-

07

Feb-

08

May

-08

Aug-

08

Sep-

08

Oct-

08

FIXED INCOME

Focus on high quality, investment grade bonds

Citi analysts believe that there is a large

before year-end, given deteriorating financial

banks’ balance sheets in an attempt to loosen

In the long term, Citi analysts’ primary area

view,

bonds issued by the sector.

Given ongoing uncertainty, Citi analysts

issuers with strong liquidity. plan works successfully, Citi analysts investment grade bonds continue to offer CITI US BIG

forecast 10-year Treasury yields rising gradually over the coming year as risk aversion diminishes.

With respect to credit markets, Citi analysts believe recent default of a major US investment bank may place a larger spotlight

more compelling rewards in relation to their expected lower risks than high yield bonds. Meanwhile, they believe preferred securities within the primary market are providing select opportunities over the long term despite recent volatility.

Data Source: Bloomberg as of September 30, 2008

1600

1500

1400

1100

Jan-

08

Mar

-08

Apr-

08

Jun-

08

Jul-0

8

Despite unprecedented volatility and ongoing concerns over the credit environment, Citi analysts believe US equities may be close to their trough and may be poised to rebound over the next 12

on average rallied several months prior to the actual economic trough during previous US recessions since 1960. Citi analysts warn,

disappointed by lower than expected or even

equity performance going forward.

favour the outlook for small and mid cap

stocks during recovery phases. Furthermore, Citi analysts note that US small and mid-cap stocks derive a smaller percentage of their

and may therefore be more sheltered from the impact of the recent US dollar appreciation. Indeed, they may even benefit

1700

1300

1200

Oct-

07

Nov-

07

Dec-

07

Feb-

08

May

-08

Aug-

08

Sep-

08

Oct-

08

EQUITIES

Positioning for a recovery

months. They note that S&P500 stocks have

however, that many investors may be

In anticipation of a recovery, Citi analysts

stocks over large cap stocks given their historical pattern of outperforming large-cap

revenues from overseas than large cap stocks

negative profit growth among S&P500 companies in 2009. According to data from Bloomberg as of September 26, the consensus of Wall Street equity analysts expected S&P500 companies’ profits to grow by almost 25% next year. With expectations set too high, in the view of Citi analysts, this may pose a challenge to US

from the lower cost of imported materials. Citi analysts also continue to hold a neutral view between value and growth stocks.

Regarding the financials sector, Citi analysts remains cautious and believe weakening fundamentals and the potential for additional events may keep the sector under pressure.

S&P 500 INDEX Data Source: Bloomberg as of September 30, 2008

Their main areas of concern include counterparty exposure, declining value of illiquid mortgage assets, liquidity shortages, capital raising constraints and regulatory issues.

Q3 STANDPOINT 08

Forecasts may not be attained. Past performance is no guarantee of future results. There are additional risks

associated with foreign investments.

4

Î Î Î

JAPAN AND ASIA PACIFIC

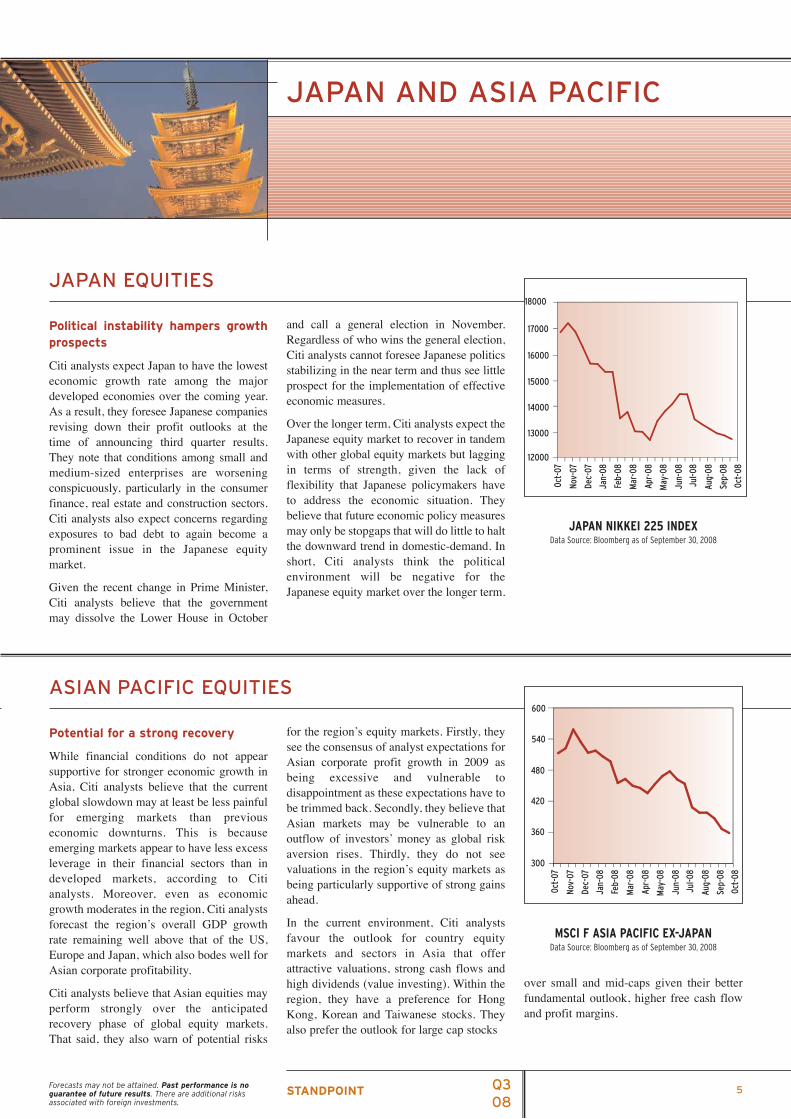

JAPAN EQUITIES

Political instability hampers growth prospects

Citi analysts expect Japan to have the lowest economic growth rate among the major developed economies over the coming year. As a result, they foresee Japanese companies revising down their profit outlooks at the time of announcing third quarter results. They note that conditions among small and medium-sized enterprises are worsening conspicuously, particularly in the consumer

Î ÎÎ ÎÎ Î ÎÎ Î Î ÎÎ ÎÎÎÎ

18000

17000

16000

15000

14000

13000

12000

Oct-

07

Nov-

07

Dec-

07

Jan-

08

Feb-

08

Mar

-08

Apr-

08

May

-08

Jun-

08

Jul-0

8

Aug-

08

Sep-

08

Oct-

08

and call a general election in November. Regardless of who wins the general election, Citi analysts cannot foresee Japanese politics stabilizing in the near term and thus see little prospect for the implementation of effective economic measures.

Over the longer term, Citi analysts expect the Japanese equity market to recover in tandem with other global equity markets but lagging in terms of strength, given the lack of flexibility that Japanese policymakers have to address the economic situation. They believe that future economic policy measures

JAPAN NIKKEI 225 INDEX

finance, real estate and construction sectors. Citi analysts also expect concerns regarding exposures to bad debt to again become a may only be stopgaps that will do little to halt

prominent issue in the Japanese equity market.

Given the recent change in Prime Minister, Citi analysts believe that the government may dissolve the Lower House in October

the downward trend in domestic-demand. In short, Citi analysts think the political environment will be negative for the Japanese equity market over the longer term.

Data Source: Bloomberg as of September 30, 2008

600

540

480

420

360

300

Oct-

07

Nov-

07

Dec-

07

Jan-

08

Feb-

08

Mar

-08

Apr-

08

May

-08

Jun-

08

Jul-0

8

Aug-

08

Sep-

08

Oct-

08

ASIAN PACIFIC EQUITIES

Potential for a strong recovery

While financial conditions do not appear supportive for stronger economic growth in Asia, Citi analysts believe that the current global slowdown may at least be less painful for emerging markets than previous economic downturns. This is because emerging markets appear to have less excess leverage in their financial sectors than in developed markets, according to Citi analysts. Moreover, even as economic growth moderates in the region, Citi analysts

for the region’s equity markets. Firstly, they see the consensus of analyst expectations for Asian corporate profit growth in 2009 as being excessive and vulnerable to disappointment as these expectations have to be trimmed back. Secondly, they believe that Asian markets may be vulnerable to an outflow of investors’ money as global risk aversion rises. Thirdly, they do not see valuations in the region’s equity markets as being particularly supportive of strong gains ahead.

forecast the region’s overall GDP growth rate remaining well above that of the US, Europe and Japan, which also bodes well for Asian corporate profitability.

Citi analysts believe that Asian equities may perform strongly over the anticipated recovery phase of global equity markets. That said, they also warn of potential risks

In the current environment, Citi analysts favour the outlook for country equity markets and sectors in Asia that offer attractive valuations, strong cash flows and high dividends (value investing). Within the region, they have a preference for Hong Kong, Korean and Taiwanese stocks. They also prefer the outlook for large cap stocks

MSCI F ASIA PACIFIC EX-JAPAN Data Source: Bloomberg as of September 30, 2008

over small and mid-caps given their better fundamental outlook, higher free cash flow and profit margins.

Forecasts may not be attained. Past performance is no guarantee of future results. There are additional risks associated with foreign investments.

Q3STANDPOINT 08

5

400

500

Jan-

08

Mar

-08

Apr-

08

Jun-

08

Jul-0

8

Citi analysts believe that the Central and Eastern European economy may soon start

side, Citi analysts note that the global economic slowdown and sharp correction in commodity prices should alleviate inflationary pressures and the need for higher interest rates. In this context, they will

expected profit levels, which is lower than other regional equity markets. Citi analysts

favourably to the more subdued profit growth expected elsewhere around the

attractive combination of good value and potential growth.

Citi analysts have a mixed outlook for equity

CEEMEA AND LATIN AMERICA

250

300

350

450

Oct-

07

Nov-

07

Dec-

07

Feb-

08

May

-08

Aug-

08

Sep-

08

Oct-

08

CEEMEA EQUITIES

Sensitivity to European slowdown

to suffer from the rapidly deteriorating Euro Area economy. They now forecast GDP in the CEEMEA region slowing to 5.1% in 2009, from 5.7% this year. On the positive

The region’s equity markets are currently valued at around 9 times the coming year’s

also expect the region’s corporate profits to grow by over 20% this year, which compares

world. CEEMEA equities therefore offer an

favour the outlook for equity markets in the region with greater policy flexibility, more resilient financial systems and healthier current accounts.

The region’s equity market valuations appear very attractive, in terms of the price-earnings ratio, compared to other regions.

market performances in the region. They have a positive view of Russian, Middle Eastern and Polish equity markets but they remain cautious in their outlook for Turkish stocks, where the large current account deficit may weigh on the currency and on monetary policy. In Russia, although political uncertainties have resurfaced, Citi

MSCI EM EMEA Data Source: Bloomberg as of September 30, 2008

analysts consider that the local equity market has overreacted to the impact of financial instability on the economy. However, substantial risks remain.

Jan-

08

Mar

-08

Apr-

08

Jun-

08

Jul-0

8

Despite recent underperformance, Citi analysts remain optimistic on the long term

attractive valuations as a result of the recent

markets.

back in commodity prices, Citi analysts

potential for this market to sharply rebound with the MSCI Brazil index having underperformed the MSCI EM Latin America index over the third quarter of this

note that second quarter GDP growth exceeded expectations, that inflation appears to have peaked and that the cost of capital

have a favourable outlook for Mexican equities despite the slowdown that they

3500

4300

3900

4700

5100

5500

Oct-

07

Nov-

07

Dec-

07

Feb-

08

May

-08

Aug-

08

Sep-

08

Oct-

08

LATIN AMERICAN EQUITIES

Brazilian equities may lead the region’s markets higher

prospects of Latin American equities given

sell-off and their expectations for higher economic growth rates among the emerging

Whilst the region’s commodity producers may suffer from the recent pull

believe that the region’s equity markets may

year. With regard to Brazil’s economy, they

remains relatively low. Citi analysts also

anticipate in the local economy.

benefit from lower inflation. They warn, however, that these equity markets could continue to be extremely volatile in the coming months.

Within Latin America, Citi analysts favour the outlook for Brazilian equities based on an improved domestic economic situation and strong profit growth momentum and the

Overall, Citi analysts offer several potential catalysts that may lead to a new and MSCI EM LATIN AMERICA sustainable rally within the region’s equity Data Source: Bloomberg as of September 30, 2008

markets including, a steady US dollar exchange rate, a stabilisation in commodity prices, better than expected US economic data, as well as reduced worries over global inflation.

Q3 STANDPOINT 08

Forecasts may not be attained. Past performance is no guarantee of future results. There are additional risks

associated with foreign investments.

6

1800

2050

2300

2550

2800

2000

2600

3200

3800

4400

5000

1800

2050

2300

2550

2800

2000

2600

3200

3800

4400

5000

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

‘‘‘‘‘‘

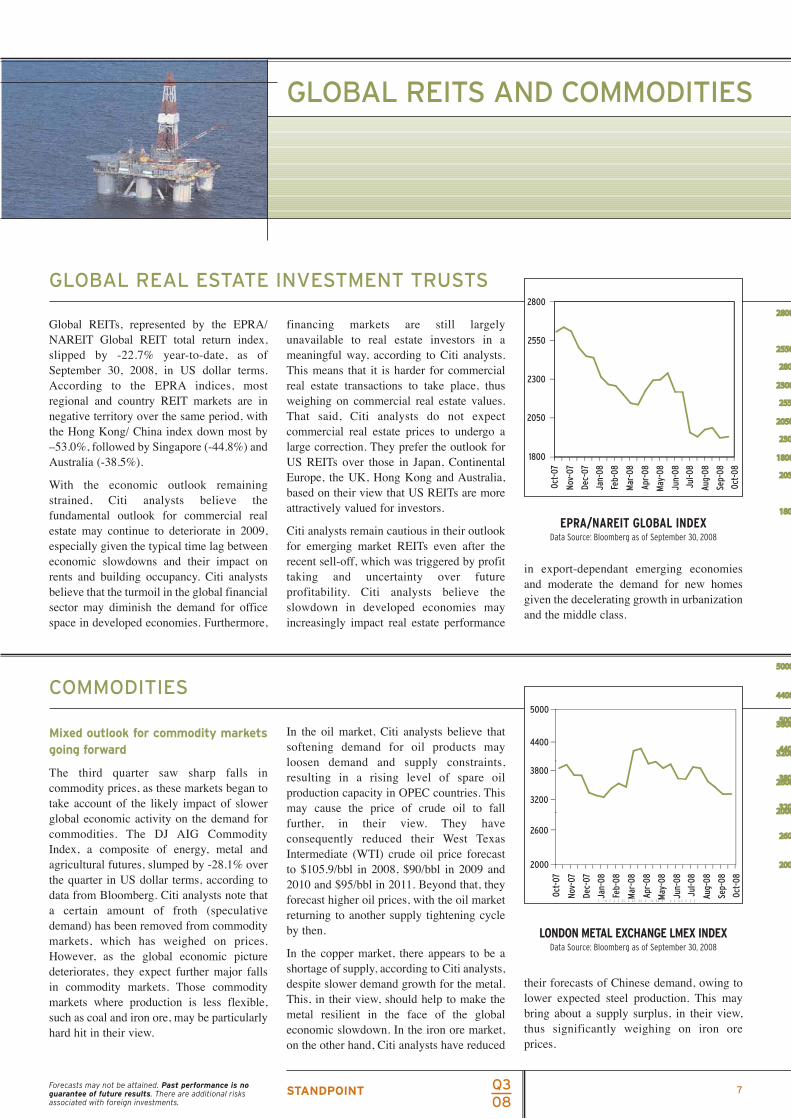

GLOBAL REITS AND COMMODITIES

September 30, 2008, in US dollar terms. According to the EPRA indices, most

negative territory over the same period, with the Hong Kong/ China index down most by –53.0%, followed by Singapore (-44.8%) and Australia (-38.5%).

strained, Citi analysts believe the

financing markets are still unavailable to real estate investors in a

This means that it is harder for commercial real estate transactions to take place, thus weighing on commercial real estate values. That said, Citi analysts do not expect

1800

Jan-

08

Mar

-08

Apr-

08

Jun-

08

Jul-0

8

GLOBAL REAL ESTATE INVESTMENT TRUSTS

Global REITs, represented by the EPRA/ NAREIT Global REIT total return index, slipped by -22.7% year-to-date, as of

regional and country REIT markets are in

With the economic outlook remaining

largely

meaningful way, according to Citi analysts.

commercial real estate prices to undergo a large correction. They prefer the outlook for US REITs over those in Japan, Continental Europe, the UK, Hong Kong and Australia, based on their view that US REITs are more

2800

2550

2300

2050

Oct-

07

Nov-

07

Dec-

07

Feb-

08

May

-08

Aug-

08

Sep-

08

Oct-

08

fundamental outlook for commercial real attractively valued for investors.

EPRA/NAREIT GLOBAL INDEX Data Source: Bloomberg as of September 30, 2008

estate may continue to deteriorate in 2009, Citi analysts remain cautious in their outlook especially given the typical time lag between for emerging market REITs even after the economic slowdowns and their impact on recent sell-off, which was triggered by profit rents and building occupancy. Citi analysts taking and uncertainty over future

in export-dependant emerging economies

believe that the turmoil in the global financial profitability. Citi analysts believe the sector may diminish the demand for office slowdown in developed economies may

and moderate the demand for new homes given the decelerating growth in urbanization and the middle class.

space in developed economies. Furthermore, increasingly impact real estate performance

‘ ‘ ‘

5000

4400

Jan-

08

Mar

-08

Apr-

08

Jun-

08

Jul-0

8

The third quarter saw sharp falls in commodity prices, as these markets began to take account of the likely impact of slower global economic activity on the demand for commodities. The DJ AIG Commodity

agricultural futures, slumped by -28.1% over the quarter in US dollar terms, according to

In the oil market, Citi analysts believe that softening demand for oil products may loosen demand and supply constraints, resulting in a rising level of spare oil

may cause the price of crude oil to fall in their They have

consequently reduced their Intermediate (WTI) crude oil price forecast to $105.9/bbl in 2008, $90/bbl in 2009 and

forecast higher oil prices, with the oil market ‘ ‘ ‘ ‘ ‘ ‘‘ ‘ ‘‘ ‘‘ ‘ ‘ ‘‘ ‘ ‘ ‘ ‘ ‘ ‘ ‘ ‘ ‘

3800

3200

2600

2000

Oct-

07

Nov-

07

Dec-

07

Feb-

08

May

-08

Aug-

08

Sep-

08

Oct-

08

COMMODITIES

Mixed outlook for commodity markets going forward

Index, a composite of energy, metal and

data from Bloomberg. Citi analysts note that

production capacity in OPEC countries. This

further, view. West Texas

2010 and $95/bbl in 2011. Beyond that, they

a certain amount of froth (speculative returning to another supply tightening cycledemand) has been removed from commodity by then. LONDON METAL EXCHANGE LMEX INDEX markets, which has weighed on prices. However, as the global economic picture In the copper market, there appears to be a Data Source: Bloomberg as of September 30, 2008

deteriorates, they expect further major falls in commodity markets. Those commodity markets where production is less flexible, such as coal and iron ore, may be particularly hard hit in their view.

Forecasts may not be attained. Past performance is no guarantee of future results. There are additional risks associated with foreign investments.

shortage of supply, according to Citi analysts, despite slower demand growth for the metal. This, in their view, should help to make the metal resilient in the face of the global economic slowdown. In the iron ore market, on the other hand, Citi analysts have reduced

Q3STANDPOINT 08

their forecasts of Chinese demand, owing to lower expected steel production. This may bring about a supply surplus, in their view, thus significantly weighing on iron ore prices.

7

CURRENCIES

EURO VS US DOLLAR YEN VS US DOLLAR GBP VS US DOLLAR

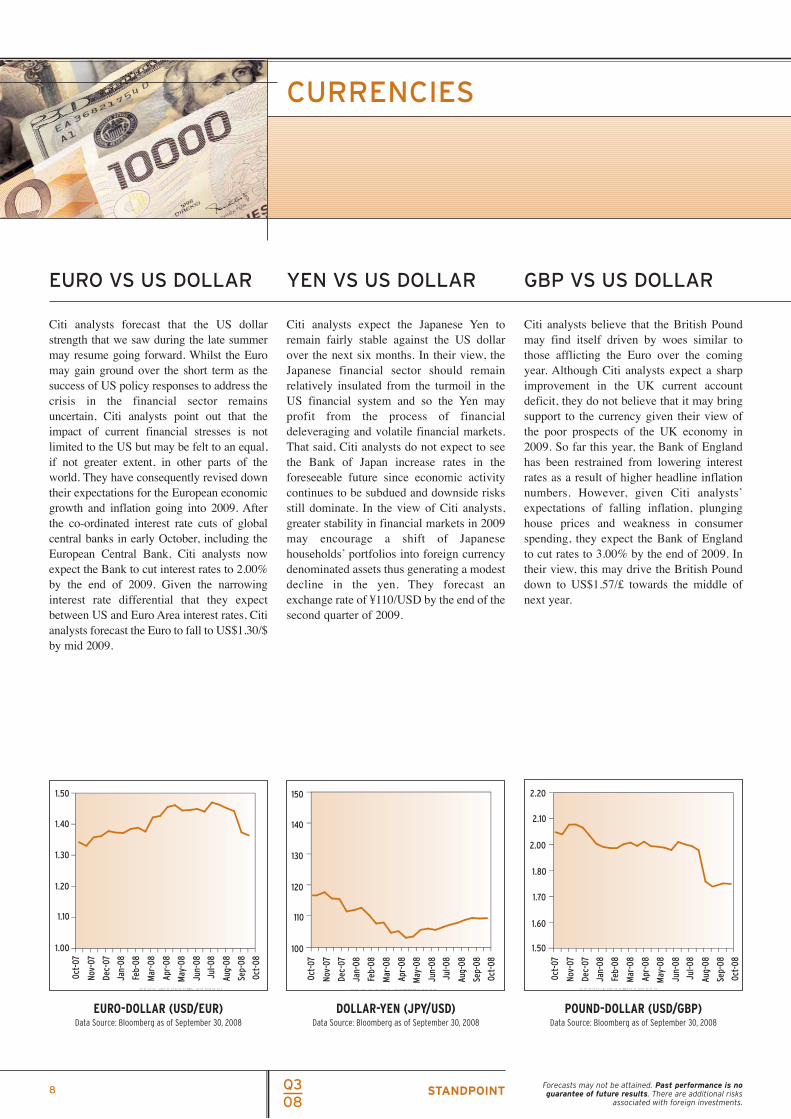

Citi analysts forecast that the US dollar strength that we saw during the late summer may resume going forward. Whilst the Euro may gain ground over the short term as the success of US policy responses to address the crisis in the financial sector remains uncertain, Citi analysts point out that the impact of current financial stresses is not limited to the US but may be felt to an equal, if not greater extent, in other parts of the world. They have consequently revised down their expectations for the European economic growth and inflation going into 2009. After the co-ordinated interest rate cuts of global central banks in early October, including the European Central Bank, Citi analysts now expect the Bank to cut interest rates to 2.00% by the end of 2009. Given the narrowing interest rate differential that they expect between US and Euro Area interest rates, Citi analysts forecast the Euro to fall to US$1.30/$ by mid 2009.

Citi analysts expect the Japanese Yen to remain fairly stable against the US dollar over the next six months. In their view, the Japanese financial sector should remain relatively insulated from the turmoil in the US financial system and so the Yen may profit from the process of financial deleveraging and volatile financial markets. That said, Citi analysts do not expect to see the Bank of Japan increase rates in the foreseeable future since economic activity continues to be subdued and downside risks still dominate. In the view of Citi analysts, greater stability in financial markets in 2009 may encourage a shift of Japanese households’ portfolios into foreign currency denominated assets thus generating a modest decline in the yen. They forecast an exchange rate of ¥110/USD by the end of the second quarter of 2009.

Citi analysts believe that the British Pound may find itself driven by woes similar to those afflicting the Euro over the coming year. Although Citi analysts expect a sharp improvement in the UK current account deficit, they do not believe that it may bring support to the currency given their view of the poor prospects of the UK economy in 2009. So far this year, the Bank of England has been restrained from lowering interest rates as a result of higher headline inflation numbers. However, given Citi analysts’ expectations of falling inflation, plunging house prices and weakness in consumer spending, they expect the Bank of England to cut rates to 3.00% by the end of 2009. In their view, this may drive the British Pound down to US$1.57/£ towards the middle of next year.

1.80

1.60

1.50

Jan-

08

Mar

-08

Apr-

08

Jun-

08

Jul-0

8

150

140

110

100

Jan-

08

Mar

-08

Apr-

08

Jun-

08

Jul-0

8

1.50

Jan-

08

Mar

-08

Apr-

08

Jun-

08

Jul-0

8

ëëëëë ëëëëëëëëëëëëëëë

2.20

2.10

2.00

1.70

Oct-

07

Nov-

07

Dec-

07

Feb-

08

May

-08

Aug-

08

Sep-

08

Oct-

08

ëë ë ë ëëëë ëëë ëëëë ëëëëëëë

130

120

Oct-

07

Nov-

07

Dec-

07

Feb-

08

May

-08

Aug-

08

Sep-

08

Oct-

08

ëëëë ëëëëëëëëëë ëëëëëëë

1.40

1.30

1.20

1.10

1.00

Oct-

07

Nov-

07

Dec-

07

Feb-

08

May

-08

Aug-

08

Sep-

08

Oct-

08

EURO-DOLLAR (USD/EUR) DOLLAR-YEN (JPY/USD) POUND-DOLLAR (USD/GBP) Data Source: Bloomberg as of September 30, 2008 Data Source: Bloomberg as of September 30, 2008 Data Source: Bloomberg as of September 30, 2008

Q3 STANDPOINT 08

Forecasts may not be attained. Past performance is no guarantee of future results. There are additional risks

associated with foreign investments.

8

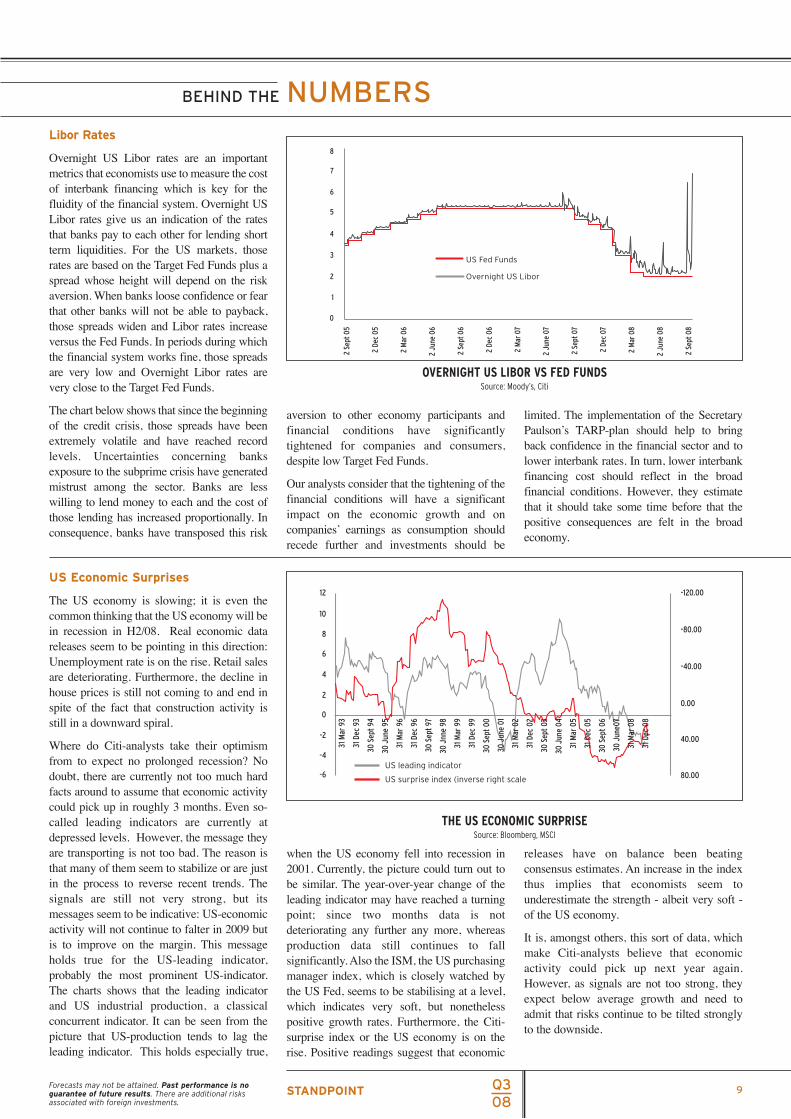

BEHIND THE NUMBERSLibor Rates

Overnight US Libor rates are an important metrics that economists use to measure the cost of interbank financing which is key for the fluidity of the financial system. Overnight US Libor rates give us an indication of the rates that banks pay to each other for lending short term liquidities. For the US markets, those rates are based on the Target Fed Funds plus a spread whose height will depend on the risk aversion. When banks loose confidence or fear that other banks will not be able to payback, those spreads widen and Libor rates increase versus the Fed Funds. In periods during which the financial system works fine, those spreads

2 De

c 05

2 M

ar 0

6

2 Ju

ne 0

6

2 De

c 06

2 M

ar 0

8

2 Ju

ne 0

8

0

1

2

3

4

5

6

7

8

US Fed Funds

Overnight US Libor

2 Se

pt 0

5

2 Se

pt 0

6

2 M

ar 0

7

2 Ju

ne 0

7

2 Se

pt 0

7

2 De

c 07

2 Se

pt 0

8

are very low and Overnight Libor rates are very close to the Target Fed Funds.

The chart below shows that since the beginning of the credit crisis, those spreads have been extremely volatile and have reached record levels. Uncertainties concerning banks exposure to the subprime crisis have generated mistrust among the sector. Banks are less willing to lend money to each and the cost of those lending has increased proportionally. In consequence, banks have transposed this risk

US Economic Surprises

OVERNIGHT US LIBOR VS FED FUNDS Source: Moody’s, Citi

aversion to other economy participants and limited. The implementation of the Secretary financial conditions have significantly Paulson’s TARP-plan should help to bring tightened for companies and consumers, back confidence in the financial sector and to despite low Target Fed Funds. lower interbank rates. In turn, lower interbank

Our analysts consider that the tightening of the financial conditions will have a significant impact on the economic growth and on companies’ earnings as consumption should recede further and investments should be

financing cost should reflect in the broad financial conditions. However, they estimate that it should take some time before that the positive consequences are felt in the broad economy.

The US economy is slowing; it is even the common thinking that the US economy will be in recession in H2/08. Real economic data releases seem to be pointing in this direction: Unemployment rate is on the rise. Retail sales are deteriorating. Furthermore, the decline in house prices is still not coming to and end in spite of the fact that construction activity is still in a downward spiral.

Where do Citi-analysts take their optimism from to expect no prolonged recession? No doubt, there are currently not too much hard facts around to assume that economic activity could pick up in roughly 3 months. Even so

12

10

6

8

2

4

-2

0

-4

-6

-120.00

-80.00

-40.00

0.00

40.00

80.00 US leading indicator

US surprise index (inverse right scale

31 M

ar 9

3

31 D

ec 9

3

30 S

ept 9

4

31 M

ar 9

6

31 D

ec 9

6

30 S

ept 9

7

30 J

nne

98

31 M

ar 9

9

31 D

ec 9

9

30 S

ept 0

0

30 J

une

95

30 J

une

01

31 M

ar 0

2

31 D

ec 0

2

30 S

ept 0

3

30 J

une

04

31 M

ar 0

5

31 D

ec 0

5

30 S

ept 0

6

30 J

une0

7

31 M

ar 0

8

31 D

ec 0

8

called leading indicators are currently at depressed levels. However, the message they are transporting is not too bad. The reason is that many of them seem to stabilize or are just in the process to reverse recent trends. The signals are still not very strong, but its messages seem to be indicative: US-economic activity will not continue to falter in 2009 but is to improve on the margin. This message holds true for the US-leading indicator, probably the most prominent US-indicator. The charts shows that the leading indicator and US industrial production, a classical concurrent indicator. It can be seen from the picture that US-production tends to lag the leading indicator. This holds especially true,

THE US ECONOMIC SURPRISE Source: Bloomberg, MSCI

when the US economy fell into recession in 2001. Currently, the picture could turn out to be similar. The year-over-year change of the leading indicator may have reached a turning point; since two months data is not deteriorating any further any more, whereas production data still continues to fall significantly. Also the ISM, the US purchasing manager index, which is closely watched by the US Fed, seems to be stabilising at a level, which indicates very soft, but nonetheless positive growth rates. Furthermore, the Citisurprise index or the US economy is on the rise. Positive readings suggest that economic

releases have on balance been beating consensus estimates. An increase in the index thus implies that economists seem to underestimate the strength - albeit very soft of the US economy.

It is, amongst others, this sort of data, which make Citi-analysts believe that economic activity could pick up next year again. However, as signals are not too strong, they expect below average growth and need to admit that risks continue to be tilted strongly to the downside.

Forecasts may not be attained. Past performance is no guarantee of future results. There are additional risks associated with foreign investments.

Q3STANDPOINT 08

9

STANDPOINT FINAL WORD

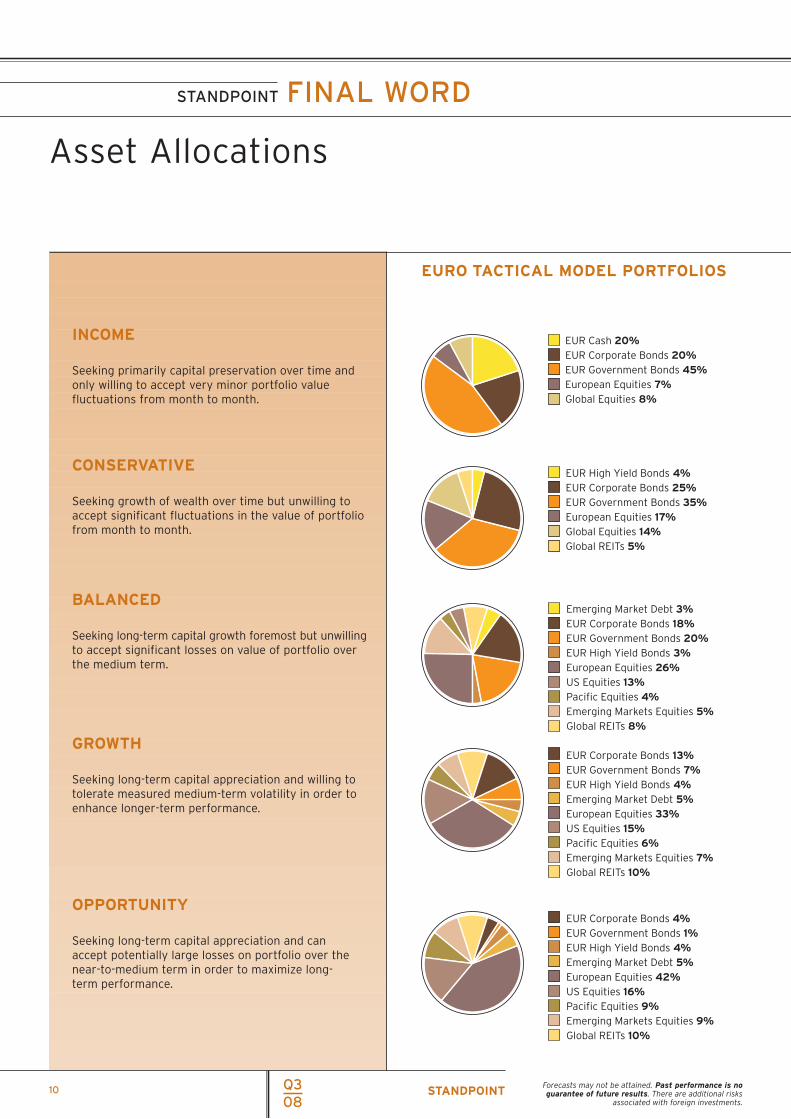

Asset Allocations

INCOME

Seeking primarily capital preservation over time and only willing to accept very minor portfolio value fluctuations from month to month.

CONSERVATIVE

Seeking growth of wealth over time but unwilling to accept significant fluctuations in the value of portfolio from month to month.

BALANCED

Seeking long-term capital growth foremost but unwilling to accept significant losses on value of portfolio over the medium term.

GROWTH

Seeking long-term capital appreciation and willing to tolerate measured medium-term volatility in order to enhance longer-term performance.

OPPORTUNITY

Seeking long-term capital appreciation and can accept potentially large losses on portfolio over the near-to-medium term in order to maximize long-term performance.

Q308

EURO TACTICAL MODEL PORTFOLIOS

EUR Cash 20% EUR Corporate Bonds 20% EUR Government Bonds 45% European Equities 7% Global Equities 8%

EUR High Yield Bonds 4% EUR Corporate Bonds 25% EUR Government Bonds 35% European Equities 17% Global Equities 14% Global REITs 5%

Emerging Market Debt 3% EUR Corporate Bonds 18% EUR Government Bonds 20% EUR High Yield Bonds 3% European Equities 26% US Equities 13% Pacific Equities 4% Emerging Markets Equities 5% Global REITs 8%

EUR Corporate Bonds 13% EUR Government Bonds 7% EUR High Yield Bonds 4% Emerging Market Debt 5% European Equities 33% US Equities 15% Pacific Equities 6% Emerging Markets Equities 7% Global REITs 10%

EUR Corporate Bonds 4%EUR Government Bonds 1%EUR High Yield Bonds 4%Emerging Market Debt 5%European Equities 42%US Equities 16%Pacific Equities 9%Emerging Markets Equities 9% Global REITs 10%

Forecasts may not be attained. Past performance is no STANDPOINT guarantee of future results. There are additional risks

associated with foreign investments.

10

The suggested allocations are intended to be general in nature and are not to be construed as specific investment advice. Investors are encouraged to consult with their Financial Professional to determine their allocation needs based on their risk tolerance, suitability and goals. [Note that there are additional risks associated with hedge funds, as such funds are speculative. Please refer to page 12 for important information about hedge funds.]

Data Source: Citi Global Consumer Group Investments as of September 2008

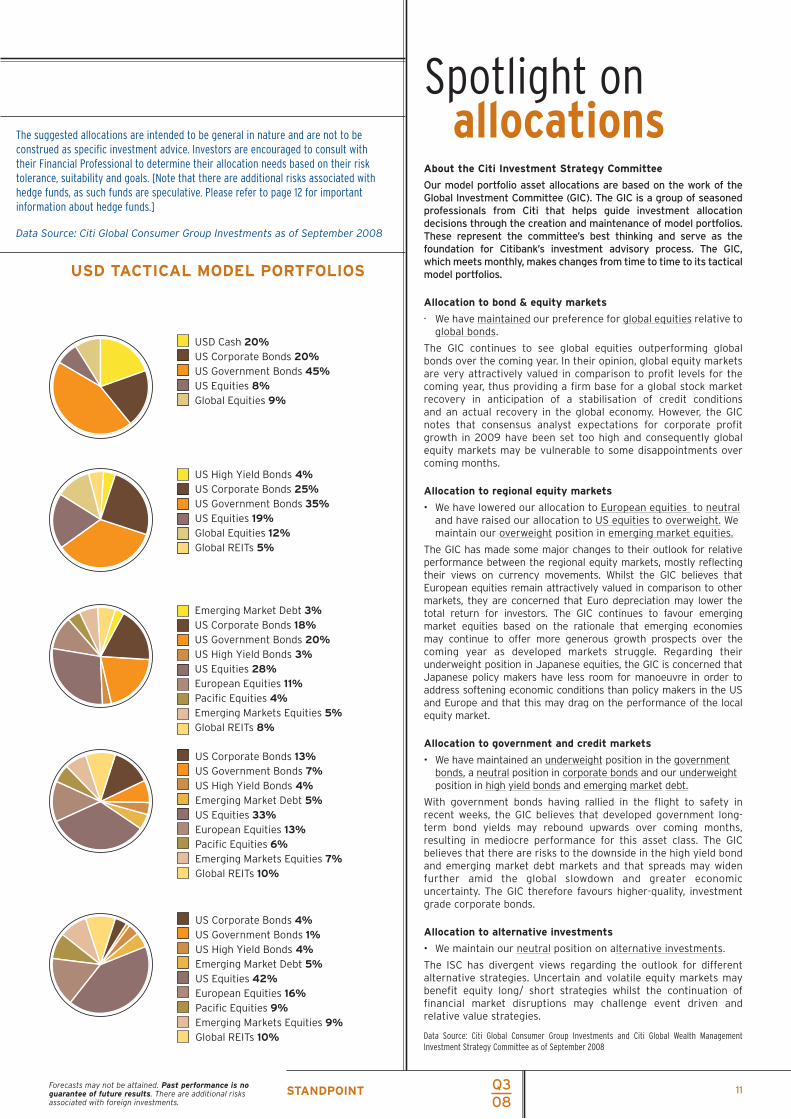

USD TACTICAL MODEL PORTFOLIOS

USD Cash 20%US Corporate Bonds 20%US Government Bonds 45%US Equities 8% Global Equities 9%

US High Yield Bonds 4% US Corporate Bonds 25% US Government Bonds 35% US Equities 19% Global Equities 12% Global REITs 5%

Emerging Market Debt 3% US Corporate Bonds 18% US Government Bonds 20% US High Yield Bonds 3% US Equities 28% European Equities 11% Pacific Equities 4% Emerging Markets Equities 5% Global REITs 8%

US Corporate Bonds 13% US Government Bonds 7% US High Yield Bonds 4%Emerging Market Debt 5%US Equities 33%European Equities 13%Pacific Equities 6%Emerging Markets Equities 7%Global REITs 10%

US Corporate Bonds 4%US Government Bonds 1%US High Yield Bonds 4%Emerging Market Debt 5%US Equities 42%European Equities 16%Pacific Equities 9%Emerging Markets Equities 9%Global REITs 10%

Forecasts may not be attained. Past performance is no guarantee of future results. There are additional risks STANDPOINT associated with foreign investments.

Spotlight onallocations

About the Citi Investment Strategy Committee

Our model portfolio asset allocations are based on the work of the Global Investment Committee (GIC). The GIC is a group of seasoned professionals from Citi that helps guide investment allocation decisions through the creation and maintenance of model portfolios. These represent the committee’s best thinking and serve as the foundation for Citibank’s investment advisory process. The GIC, which meets monthly, makes changes from time to time to its tactical model portfolios.

Allocation to bond & equity markets

· We have maintained our preference for global equities relative to global bonds.

The GIC continues to see global equities outperforming global bonds over the coming year. In their opinion, global equity markets are very attractively valued in comparison to profit levels for the coming year, thus providing a firm base for a global stock market recovery in anticipation of a stabilisation of credit conditions and an actual recovery in the global economy. However, the GIC notes that consensus analyst expectations for corporate profit growth in 2009 have been set too high and consequently global equity markets may be vulnerable to some disappointments over coming months.

Allocation to regional equity markets

• We have lowered our allocation to European equities to neutral and have raised our allocation to US equities to overweight. We maintain our overweight position in emerging market equities.

The GIC has made some major changes to their outlook for relative performance between the regional equity markets, mostly reflecting their views on currency movements. Whilst the GIC believes that European equities remain attractively valued in comparison to other markets, they are concerned that Euro depreciation may lower the total return for investors. The GIC continues to favour emerging market equities based on the rationale that emerging economies may continue to offer more generous growth prospects over the coming year as developed markets struggle. Regarding their underweight position in Japanese equities, the GIC is concerned that Japanese policy makers have less room for manoeuvre in order to address softening economic conditions than policy makers in the US and Europe and that this may drag on the performance of the local equity market.

Allocation to government and credit markets

• We have maintained an underweight position in the government bonds, a neutral position in corporate bonds and our underweight position in high yield bonds and emerging market debt.

With government bonds having rallied in the flight to safety in recent weeks, the GIC believes that developed government long-term bond yields may rebound upwards over coming months, resulting in mediocre performance for this asset class. The GIC believes that there are risks to the downside in the high yield bond and emerging market debt markets and that spreads may widen further amid the global slowdown and greater economic uncertainty. The GIC therefore favours higher-quality, investment grade corporate bonds.

Allocation to alternative investments

• We maintain our neutral position on alternative investments.

The ISC has divergent views regarding the outlook for different alternative strategies. Uncertain and volatile equity markets may benefit equity long/ short strategies whilst the continuation of financial market disruptions may challenge event driven and relative value strategies.

Data Source: Citi Global Consumer Group Investments and Citi Global Wealth Management Investment Strategy Committee as of September 2008

Q308

11

Important Disclosure

“Citi analysts” refers to investment professionals within Citi Investment Research, Citi Global Markets and voting members of the GWM Global Investment Committee and Global Portfolio Committee.

“We” refers to Citi Global Consumer Group Investments.

This document is based on information provided by Citigroup Investment Research, Citigroup Global Markets, Citigroup Global Wealth Management and Citigroup Alternative Investments. It is provided for your information only. It is not intended as an offer or solicitation for the purchase or sale of any security. Information in this document has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Accordingly, investors should, before acting on the information, consider its appropriateness, having regard to their objectives, financial situation and needs. Any decision to purchase securities mentioned herein should be made based on a review of your particular circumstances with your financial adviser. Investments referred to in this document are not recommendations of Citibank or its affiliates.

Although information has been obtained from and is based upon sources that Citibank believes to be reliable, we do not guarantee its accuracy and it may be incomplete and condensed. All opinions, projections and estimates constitute the judgment of the author as of the date of publication and are subject to change without notice. Prices and availability of financial instruments also are subject to change without notice. Past performance is no guarantee of future results.

Subject to the nature and contents of the document, the investments described herein are subject to fluctuations in price and/or value and investors may get back less than originally invested. Certain high-volatility investments can be subject to sudden and large falls in value that could equal the amount invested. Certain investments contained in the document may have tax implications for private customers whereby levels and basis of taxation may be subject to change. Citibank does not provide tax advice and investors should seek advice from a tax adviser.

Turkey: Investment products are not a bank deposit and not an obligation of, nor guaranteed by Citibank A.fi., Citibank N.A., Citigroup or its affiliates. Investment products are not under assurance by the Government. Investment Products are subject to investment risks, including possible loss of principal invested. Investment Products subject to foreign exchange fluctuations, including possible loss of principal when investments are denominated in different currency. Past performance is not indicative of future results, prices can go up or down. Investment Products is not offered to U.S Persons. For all your queries and complaints, you may call Citiphone 444 0 500 or you may contact with us from fax no 0 216 5247314 or www.citibank.com.tr.

Investment products: (i) are not insured by the Federal Deposit Insurance Corporation; (ii) are not deposits or other obligations of any insured depository institution (including Citibank); and (iii) are subject to investment risks, including the possible loss of the principal amount invested.

GR

A19

783

10

/08