Specialist Disability Accommodation Presentation

39

1 Footer 4/27/2016 Open consultations January 2016 Specialist Disability Accommodation Pricing and Payments Framework

-

Upload

cpa-australia -

Category

Government & Nonprofit

-

view

221 -

download

1

Transcript of Specialist Disability Accommodation Presentation

1Footer4/27/2016

Open consultations

January 2016

Specialist Disability

Accommodation Pricing and

Payments Framework

Purpose of today

1. Provide an overview of the Specialist Disability Accommodation

Framework

2. Answer questions to clarify the purpose and intent of the

Framework

3. Provide an opportunity for all stakeholders to provide input

4. To discuss ‘top of mind’ concerns and considerations

2

Today’s agenda

1. Background and context

2. Participants

3. Housing providers and choice

4. Financing and mechanics

Morning tea at 11:20- 11:45 (25 minutes)

5. Workshop on the Framework

– Discuss the Framework and provide your feedback

Close at 1 pm

3

1. BACKGROUND AND

CONTEXT

4

Authorising environment

• Convention on the Rights of Persons with Disabilities 2006

• National Disability Strategy 2010 – 2020

• National Disability Insurance Scheme Act (2013)

– National Disability Insurance Scheme Rules (2013)

– Specialist Disability Accommodation Pricing and Payments Framework

– Responsibility for the implementation of the Framework

5

Purpose/ objectives of the SDA Pricing and Payment

Framework

• To set out an initial pricing and payments framework for the funding

of the land and built elements of SDA

• Ensure there’s scope for growth, replacement, change and

innovation in supply

• Not intended to cover:

– broader aspect of policy in respect of SDA

– support arrangements delivered in SDA

6

SDA Pricing and Payment Framework project scope

• The SDA Pricing and Payment Framework project will:

– Consult widely and seek feedback on the Framework

– Establish a pricing model and initial benchmark costs for SDA

– Test the implementability of the model with stakeholders

• Outside the scope of this project:

– Pricing for support services other than housing (acknowledging

impact of integrated service models)

– Accommodation other than SDA (e.g. social or market provision)

– Home modifications to existing properties (covered through other

NDIS funding)

7

Principles informing SDA pricing

• Inclusion: To assist participants to have the same housing opportunities, choices

and responsibilities as the broader community through stimulating market supply

• Rights, choice and control: To allow participants their choice of providers of

housing and of support services, and the way in which they will be provided

• Efficiency in outcomes: Best whole-of-life outcomes with efficient whole-of-package

costs, to support the most people possible

• Continuity: Provide an orderly and managed transition from historic accommodation

options and service models to approaches that support independence and social and

economic participation

• Innovation: To encourage innovation and investment in new Specialist Disability

Accommodation

8

9

Innovation

1. Participants

10

For whom in what circumstances

• Participants currently residing in SDA

• Group homes, large residential centres, cluster or village

accommodation

• Those in innovative accommodation models intended for people with a

need for SDA

• Those not residing in SDA - participants residing in residential aged

care (where primary need is disability related), or in inappropriate

settings (e.g. living with elderly parents who are at risk of not being

able to cope).

11

Priorities for SDA pricing

• Participants currently residing in SDA

– Who wish to stay there

– Who wish to explore other options to change their

accommodation

• Young people residing in aged care

• Over time; participants who are not currently residing in SDA but for

whom SDA would be considered ‘reasonable and necessary’

12

For whom in what circumstances 2

• SDA does not apply to all housing for people with disability, or for all people with disability

• The Agency will determine the participants for whom specialist disability accommodation is reasonable and necessary with reference to two groups;

– Participants requiring a specialist built form.

– Participants whose support needs can only be met cost effectively by SDA.

13

Participants requiring a specialist built form

• Where the impact of their disability, and functional impairment

requires accommodation with:

– Specific design features or;

– Amenity which is not readily supplied through mainstream

housing market

14

Participants whose support needs can only

be met cost effectively by SDA

• High level of complexity or cost in support required

• Need to minimise risk

• Capacity and capability of informal supports

• Capacity and capability of the participant

15

2. Housing providers and choice

16

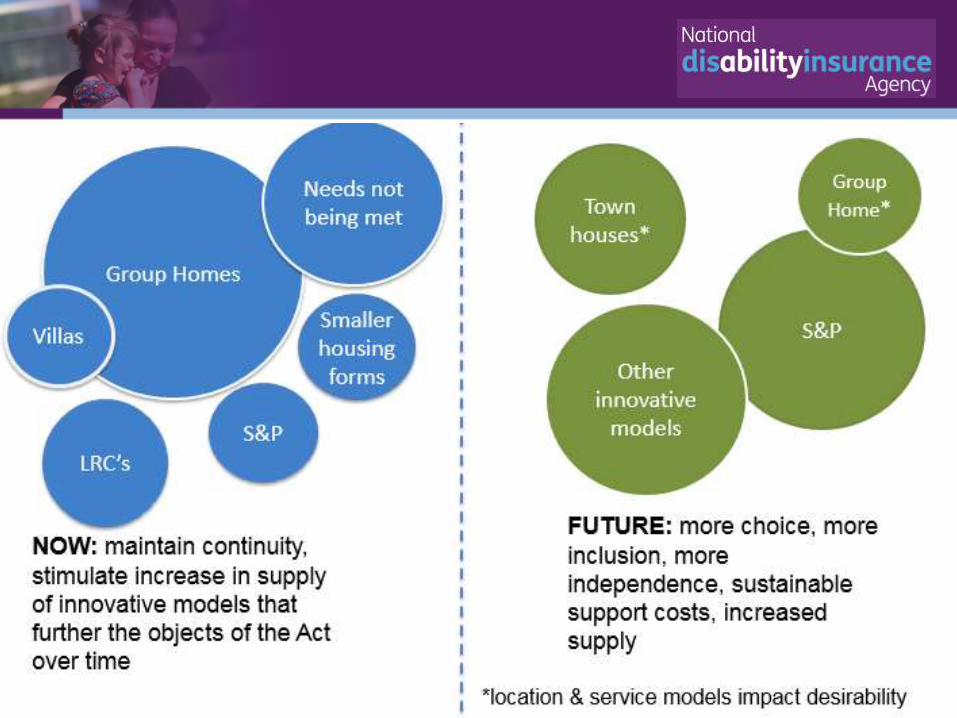

Existing supply of SDA

• Existing stock of SDA is essential to ensuring supply, this includes:

– Group homes

– Large residential facilities (phasing out)

– Smaller innovative models

• Key priority is to transition existing stock into the NDIS to allow

continuity

• Also to ensure scope for replacement, change and innovation over time

17

Housing Forms

• Large residential facility (low choice, low independence, low inclusion)

• Large group homes (6+) (low choice, low independence, onsite support,

meets continuity needs where utilised, higher tenancy management/

vacancy costs )

• Group homes (4-6) (can be associated with - limited choice, limited

independence, lower social inclusion, lower building and shared support

service costs, high continuity/ supply, higher tenancy management/

vacancy costs)

18

Housing Forms continued

• Independent living (high choice, high independence, cost can be prohibitive if high support needs, requires innovation in service models)

• Villa/ cluster/ town house (higher choice, higher independence, low-high social inclusion, shared costs, low current supply)

• ‘Salt and pepper’ accommodation (high independence, shared support costs through on site or mobile support services, high integration, low current supply)

19

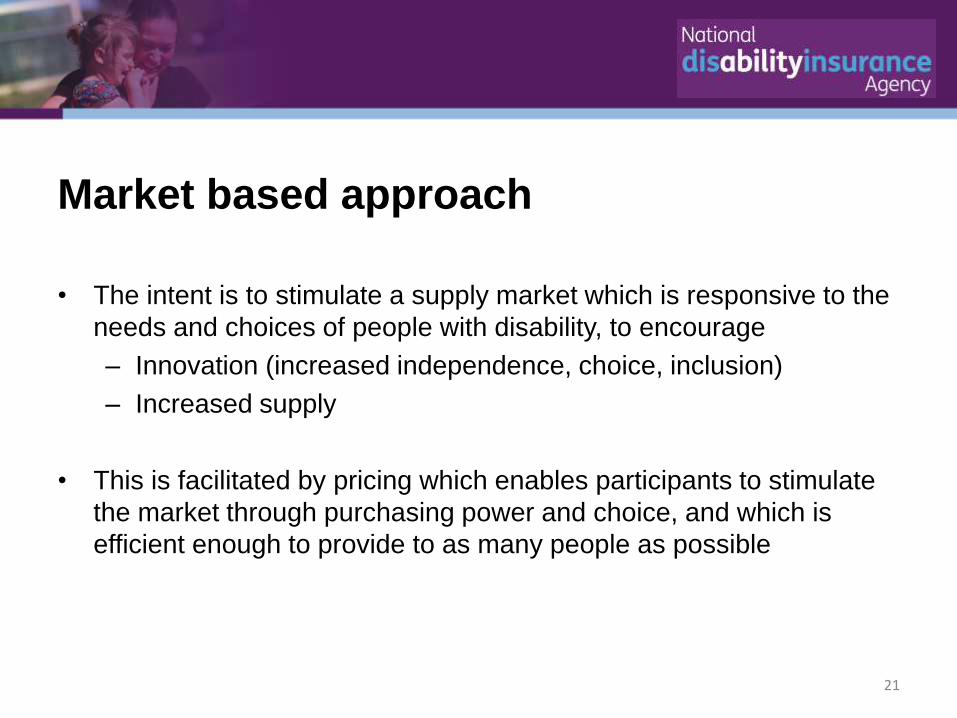

Market based approach

• The intent is to stimulate a supply market which is responsive to the

needs and choices of people with disability, to encourage

– Innovation (increased independence, choice, inclusion)

– Increased supply

• This is facilitated by pricing which enables participants to stimulate

the market through purchasing power and choice, and which is

efficient enough to provide to as many people as possible

21

Challenges

• Substantial capital investments create returns over the long term (not responsive to short-run changes)

• The market may not quickly respond, and may require market incentives

• Benchmark pricing requires simplifying assumptions, cannot be bespoke for all circumstances

• Need to reduce regulatory and administrative burden but ensure adequate quality and safeguards

22

Challenges continued

• In a number of locations there are serious shortages of

affordable accommodation which may impact

disproportionately on NDIS participants

• The NDIS will not replace the existing effort in the social

and community housing sectors which have primary

responsibility for addressing the housing needs of those

on low incomes.

23

24

Estimates (Productivity

Commission and NDIA

Actuary)

3. Financing and pricing

25

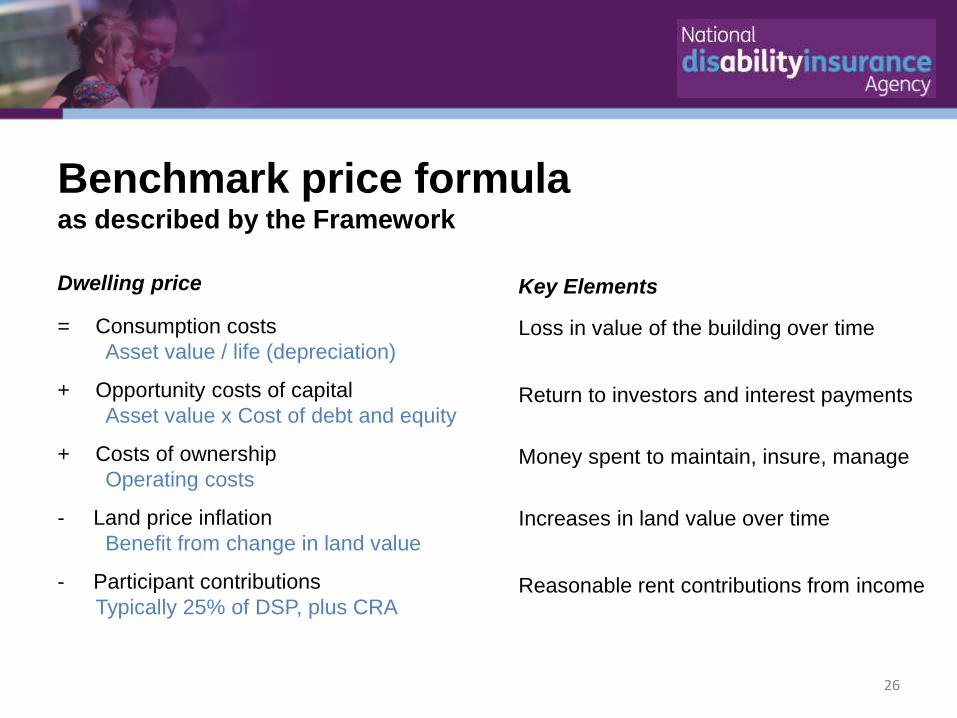

Benchmark price formula as described by the Framework

Dwelling price

= Consumption costs

Asset value / life (depreciation)

+ Opportunity costs of capital

Asset value x Cost of debt and equity

+ Costs of ownership

Operating costs

- Land price inflation

Benefit from change in land value

- Participant contributions

Typically 25% of DSP, plus CRA

Key Elements

Loss in value of the building over time

Return to investors and interest payments

Money spent to maintain, insure, manage

Increases in land value over time

Reasonable rent contributions from income

26

Benchmark price =

Dwelling price / Anticipated number of dwelling residents

Note: Vacancy risk is a critical issue to be addressed in the pricing model. Currently, the Framework specifies only that:

30. The Agency will determine how occupancy rates will be factored into the benchmark prices.

Benchmark price formula as described by the Framework continued

27

Factors

The benchmark prices will have factors or weights including for:

• Geographical location

• Number of bedrooms

• Whether the dwelling is furnished or unfurnished

• Specific building/dwelling features

• Price inflation

• Other factors the Agency determines to be necessary

• Remoteness

28

Frequently asked questions

• “Cashing out”, co-contributions and shared

equity

• Tenancy rights

• How will vacancies be managed

• Frequency and timeframe of payments

• Treatment of land

29

WORKSHOP SESSION

30

Workshop format

To help group people with potentially similar interests and issues, we

ask you to now to please move to one of the three designated tables:

• Participants/families/carers

• Service providers

• Housing Associations/ Financiers/investors/government and others

31

Workshop process

Now, in your groups, please identify which elements of the Pricing and Payment Framework:

1. you support

2. you have concerns about, and any proposed solutions

3. transitional issues

Comments should relate specifically to elements of the Framework.

We suggest that you limit these to no more than 5 key issues each, but more will be accepted.

32

Workshop process continued

• You may either provide a response as a group or as a private individual on the response sheets provided in front of you.

• Submissions can also be provided later. Written feedback can be provided up until the end of February. All comments will be considered.

• Responses underpinned by evidence and demonstrated examples would be preferred.

• Where appropriate, the NDIA will provide a formal response. All responses will be published on our website.

33

Some of our thoughts about issues and

challenges• Legacy issues: How do we address legacy issues while encouraging

innovative new accommodation options?

• Universality of prices: How do we develop benchmark prices, but still differentiate on the basis of condition and features of individual properties?

• Outcomes and efficiency: How do we encourage innovation and better outcomes for participants, taking into account whole-of-life cost efficiency?

• Choice: Can we cater for participants that would prefer to develop non-standard options? Should participants be able to “cash out”?

• Separating service providers: How do we enable the separation of accommodation providers from service providers and ensure the security and rights of tenants?

34

More issues and challenges

• Needs other than specialist built form: Will the pricing framework be able to account for people with acute need but without a clear requirement for specialist built form?

• Financier requirements: What terms and conditions are required to attract financing and ongoing investment?

• Windfall gains: How and when should we protect against windfall gains, and what conditions should be attached to SDA funding?

• Equity arrangements: Should we structure prices to apply equally to rental, ownership or shared equity arrangements?

• Group homes: Should funding continue to support the development of new group homes, or are they a transitionary ‘step down’?

35

What to expect and what’s next

JULY 1 2016

– Reasonable benchmark pricing (focus on pricing to ensure continuity

through transition)

• Not excluding innovative models

– Explicitly expand and apply pricing to new and innovative models

36

Reminder of the key elements of the Framework

• Participants

– Eligibility (existing residents, “reasonable and necessary” requirements for new residents)

– Funding is portable and attached to participants

– Support for individual choice, control and certainty

• Housing providers and choice

– Housing and support to be separated

– Benchmark prices to be based on an efficient, representative provider

– Support for innovative arrangements

• Financing and pricing

– Benchmark pricing formula

– Additive/multiplicative factors (location, bedrooms, furnishing, specific features)

– Treatment of state owned land

• Other considerations

– Registration of approved dwellings

– Quality and safeguards

– Provision for alternative payment arrangements

– Transition of non-NDIA residents to SDA

– Timing of reviews 37

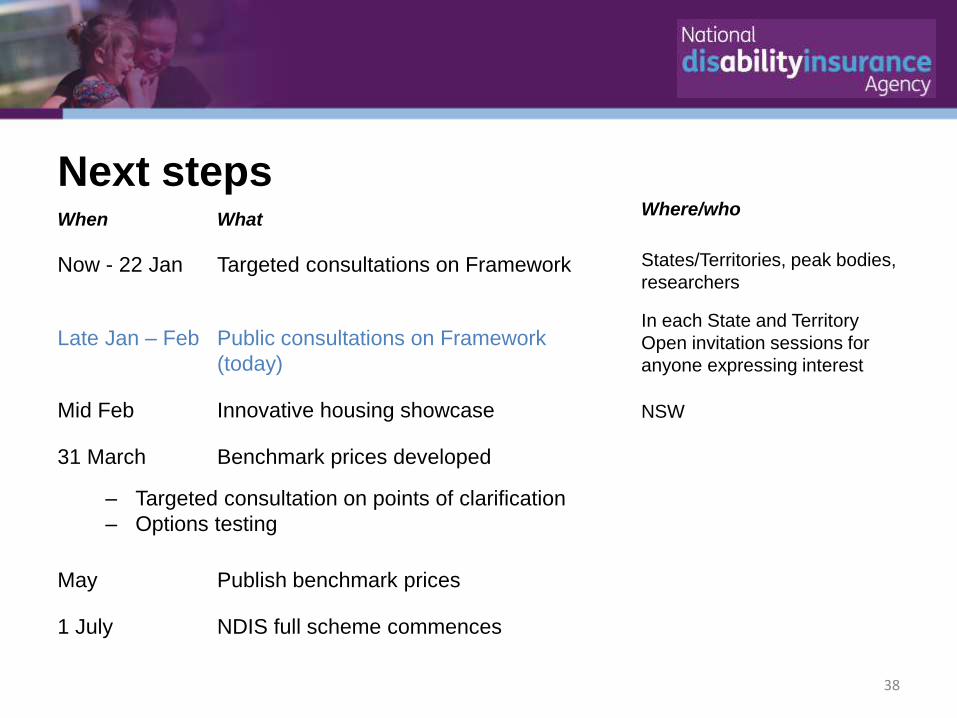

Next stepsWhen What

Now - 22 Jan Targeted consultations on Framework

Late Jan – Feb Public consultations on Framework

(today)

Mid Feb Innovative housing showcase

31 March Benchmark prices developed

– Targeted consultation on points of clarification

– Options testing

May Publish benchmark prices

1 July NDIS full scheme commences

Where/who

States/Territories, peak bodies,

researchers

In each State and Territory

Open invitation sessions for

anyone expressing interest

NSW

38

Thank You

If you would like more information, please see our website:

www.ndis.gov.au

If you would like to provide more information, please email your feedback to us before 29 February 2016 at:

If have any further questions, please contact:

• Minni Saxena, Director Housing, Market and Providers Division, NDIA, [email protected]

• Phil Pickering, Senior Associate, Marsden Jacob Associates, [email protected]

39