South Indian Bank (SOUIN0) - ICICI...

20

March 24, 2010 ICICIdirect.com | Equity Research Initiating Coverage Good thing in small package… South Indian Bank (SIB) is shedding its regional tag and growing its pan-India reach. The total business of the bank grew at 22% CAGR over FY05-09 to Rs 30237 crore. We expect 22% CAGR over FY09-12E to Rs 54,845 crore. The deposits and advances grew at 22% CAGR over FY07- 09. We expect a growth of 21% and 24% CAGR, respectively, over FY09- 12E. The C/D ratio of the bank improved from 51% in FY04 to 72% for Q3FY10. We expect it to stabilise around 70% by FY12E. Low cost deposits, improving C/D ratio to help maintain NIM Above 35% of the total bank’s deposit consists of low cost deposits, (~24% CASA and 11% NRI deposits). The interest rates on these deposits are comparatively on the lower side at around 3-3.5%. This helps in controlling the cost of deposits. We expect NIMs at 3% until FY12E. Substantial improvement in asset quality: A boon SIB has now brought down its net NPA to 0.4% from a high of 6.7% and GNPA to 1.5% from over 10% in FY02. The total stressed assets (GNPA and restructured) at about 2.6% of total loans, with provision coverage of 73% looks in good shape for SIB. We expect GNPA at 1.6% and NNPA at 0.8% by FY12E after factoring in slippages from restructured loans. Higher HTM proportion to cushion investment book from MTM SIB’s bond portfolio is well cushioned in a rising interest rate scenario since 77% of the total investment is in the HTM category, on the one hand, while the remaining AFS portfolio of 23% carries a short duration of 0.6 years. The total investment book duration stands at 4.5 years. We do not expect a major MTM hit on the AFS book. Hence, there will be no material effect on its profitability. Valuations At the CMP of Rs 156, the bank is trading at 0.9x FY12E ABV, which looks attractive. The bank, with a healthy low cost deposit base of around 35%, NIM of 3%, strong asset quality (2.5% of stressed assets) and CAR of 17% is poised for above industry growth in the coming period. However, it continues to be regional with 55% of the total business contributed by the southern region. This is a point of concern to us. Assuming sustainable RoE of 18%, terminal growth of 3% and CoE of 14.5%, we value the bank at 1.2x FY12E ABV of Rs 167 and assign it a fair value of Rs 200. Exhibit 1: Key Financials FY09 FY10E FY11E FY12E Net Profit (Rs crore) 194.7 247.6 322.6 409.8 EPS (Rs) 17.2 21.9 28.5 36.3 Growth (%) 2.8 27.2 30.3 27.0 P/E (x) 9.0 7.1 5.4 4.3 Price / Book (x) 1.4 1.2 1.0 0.8 Price / Adj Book (x) 1.5 1.3 1.1 0.9 GNPA (%) 2.2 1.7 1.7 1.6 NNPA (%) 1.1 0.9 0.8 0.8 RoNA (%) 1.0 1.1 1.2 1.3 RoE (%) 16.0 18.0 20.2 21.6 Source: Company, ICICIdirect.com Research South Indian Bank (SOUIN0) Rs 156 Rating Matrix Rating : Strong Buy Target : Rs 200 Target Period : 12-15 months Potential Upside : 28 % YoY Growth (%) FY09 FY10E FY11E FY12E NII 39.0 24.5 22.3 21.6 PBT 30.1 31.5 19.8 27.0 PAT 28.5 27.2 30.3 27.0 Stock Data \ Bloomberg Code SIB.IN Reuters Code SIBK.BO Face value (Rs) 10 Market Cap (Rs Crore) 1763 52 week H/L 171 / 48 Sensex 17451 Average volumes 69000 Comparative return matrix (%) Company 1m 3m 6m 12m SIB 10 8 32 220 City Union bk -9 13 16 178 Karnataka bank 3 -5 -16 86 Indus ind bank 13 26 61 474 Price movement (Stock vs. Nifty) 0 50 100 150 200 Apr-09 May-09 Jun-09 Jul-09 Aug-09 Sep-09 Oct-09 Nov-09 Dec-09 Jan-10 Feb-10 Mar-10 1000 2000 3000 4000 5000 6000 South Indian bank Nifty (RHS) Analyst’s name Kajal Gandhi [email protected] Chirag Shah [email protected] Viraj Gandhi [email protected]

Transcript of South Indian Bank (SOUIN0) - ICICI...

March 24, 2010

ICICIdirect.com | Equity Research

Initiating Coverage

Good thing in small package… South Indian Bank (SIB) is shedding its regional tag and growing its pan-India reach. The total business of the bank grew at 22% CAGR over FY05-09 to Rs 30237 crore. We expect 22% CAGR over FY09-12E to Rs 54,845 crore. The deposits and advances grew at 22% CAGR over FY07-09. We expect a growth of 21% and 24% CAGR, respectively, over FY09-12E. The C/D ratio of the bank improved from 51% in FY04 to 72% for Q3FY10. We expect it to stabilise around 70% by FY12E.

Low cost deposits, improving C/D ratio to help maintain NIM Above 35% of the total bank’s deposit consists of low cost deposits, (~24% CASA and 11% NRI deposits). The interest rates on these deposits are comparatively on the lower side at around 3-3.5%. This helps in controlling the cost of deposits. We expect NIMs at 3% until FY12E.

Substantial improvement in asset quality: A boon

SIB has now brought down its net NPA to 0.4% from a high of 6.7% and GNPA to 1.5% from over 10% in FY02. The total stressed assets (GNPA and restructured) at about 2.6% of total loans, with provision coverage of 73% looks in good shape for SIB. We expect GNPA at 1.6% and NNPA at 0.8% by FY12E after factoring in slippages from restructured loans.

Higher HTM proportion to cushion investment book from MTM SIB’s bond portfolio is well cushioned in a rising interest rate scenario since 77% of the total investment is in the HTM category, on the one hand, while the remaining AFS portfolio of 23% carries a short duration of 0.6 years. The total investment book duration stands at 4.5 years. We do not expect a major MTM hit on the AFS book. Hence, there will be no material effect on its profitability.

Valuations At the CMP of Rs 156, the bank is trading at 0.9x FY12E ABV, which looks attractive. The bank, with a healthy low cost deposit base of around 35%, NIM of 3%, strong asset quality (2.5% of stressed assets) and CAR of 17% is poised for above industry growth in the coming period. However, it continues to be regional with 55% of the total business contributed by the southern region. This is a point of concern to us. Assuming sustainable RoE of 18%, terminal growth of 3% and CoE of 14.5%, we value the bank at 1.2x FY12E ABV of Rs 167 and assign it a fair value of Rs 200.

Exhibit 1: Key Financials FY09 FY10E FY11E FY12E

Net Profit (Rs crore) 194.7 247.6 322.6 409.8EPS (Rs) 17.2 21.9 28.5 36.3Growth (%) 2.8 27.2 30.3 27.0P/E (x) 9.0 7.1 5.4 4.3Price / Book (x) 1.4 1.2 1.0 0.8Price / Adj Book (x) 1.5 1.3 1.1 0.9GNPA (%) 2.2 1.7 1.7 1.6NNPA (%) 1.1 0.9 0.8 0.8RoNA (%) 1.0 1.1 1.2 1.3RoE (%) 16.0 18.0 20.2 21.6

Source: Company, ICICIdirect.com Research

South Indian Bank (SOUIN0) Rs 156

Rating Matrix Rating : Strong Buy

Target : Rs 200

Target Period : 12-15 months

Potential Upside : 28 %

YoY Growth (%) FY09 FY10E FY11E FY12E

NII 39.0 24.5 22.3 21.6

PBT 30.1 31.5 19.8 27.0

PAT 28.5 27.2 30.3 27.0

Stock Data

\

Bloomberg Code SIB.INReuters Code SIBK.BOFace value (Rs) 10Market Cap (Rs Crore) 176352 week H/L 171 / 48Sensex 17451Average volumes 69000

Comparative return matrix (%) Company 1m 3m 6m 12mSIB 10 8 32 220City Union bk -9 13 16 178Karnataka bank 3 -5 -16 86Indus ind bank 13 26 61 474

Price movement (Stock vs. Nifty)

0

50

100

150

200

Apr-0

9

May

-09

Jun-

09

Jul-0

9

Aug-

09

Sep-

09

Oct-0

9

Nov

-09

Dec-

09

Jan-

10

Feb-

10

Mar

-10

1000

2000

3000

4000

5000

6000

South Indian bank Nifty (RHS)

Analyst’s name

Kajal Gandhi [email protected]

Chirag Shah [email protected]

Viraj Gandhi [email protected]

South Indian Bank (SOUIN0)

ICICIdirect.com | Equity Research Page 2

Company Background

South Indian Bank (SIB) is one of the oldest banks in south India, based out of Thrissur, Kerala. The bank has a business mix of Rs 35,511 crore. SIB has a dominant presence in Kerala and Tamil Nadu, with ~74% of total branches and 55% of the business from there. The bank has a pan-India presence with a network of over 573 branches and over 230 ATMs across 23 states and two union territories.

Exhibit 2: Branch distribution (region wise)

Rural18%

Semi Urban43%

Urban23%

Metro16%

Source: Company, ICICIdirect.com Research

Exhibit 3: Shareholding pattern

Public35%

FII38%

Mutual fund8%

Others19%

Source: Company, ICICIdirect.com Research

Exhibit 4: Branch concentration

Source: Company, ICICIdirect.com Research

Key management profile VA Joseph, who took charge of SIB as MD and CEO from June 5, 2005, was instrumental in bringing development and revolution at SIB. He has overall 38 years of experience in the banking industry. The business and quality parameters of SIB like C/D ratio, asset quality, NIM, RoA, RoE all improved considerably. We can attribute this to the new management in place.

Shareholding pattern (Q3FY10)

Shareholder Holding (%)Promoters -Institutional investors 51.3General public 48.7

FII & DII holding trend (%)

38 4037 36

14 14 13 12

10

20

30

40

50

Q3FY10 Q2FY10 Q1FY10 Q4FY09

(%)

FII DII

High concentration

South Indian Bank (SOUIN0)

ICICIdirect.com | Equity Research Page 3

Investment Rationale

SIB is shifting its focus from a regional bank to a bank with a pan-India presence. The branch concentration in the south zone provided the bank ~35% of low cost deposits. This helped to control the interest cost and maintain NIM of 3%. The total business of the bank grew at 22% CAGR over FY05-09 to Rs 30,237 crore. We expect it to grow at 22% CAGR over FY09-12E to Rs 54,845 crore. The C/D ratio of the bank improved from 51% in FY04 to 72% for Q3FY10. We expect it to stabilise around 70% by FY12E. The GNPA improved from 6.6% in FY05 to 1.5% in Q3FY10. We expect a GNPA of 1.6% and NNPA of 0.8% in FY12E.

Total business to grow at 18% CAGR over FY09-12E SIB’s total business grew at 22% CAGR over FY05-09 to Rs 30,237 crore. Going forward, we expect 24% and 21% CAGR in advances and deposits over FY09-12E to Rs 22578 crore and Rs 32267 crore, respectively. This will result in a 22% CAGR in business mix over the same period.

The credit growth in the industry was dismal at around 9.9% during October 2009. It has started to pick up from early January. However, the pace of deposit growth was steady at around 20%. According to latest RBI data, bank credit grew at 15.8% showing early signs of a strong pick-up in industry credit. We expect industry loan growth of 21% and 20%, for FY11E and FY12E, respectively, while we expect deposit growth of 20% and 18%, respectively. We feel that SIB should grow ahead of the industry because of the small base and strategic expansion plans laid by the bank along with comfortable capital adequacy ratio (CAR) of 17.4% (Tier I CAR- 14%) for Q3FY10.

Exhibit 5: Industry loan growth

0

10000

20000

30000

40000

50000

FY 0

7

FY 0

8

FY 0

9

YTDF

Y10

FY10

E

FY11

E

FY12

E

0

10

20

30

40

Amount (Rs. billion) YOY (%) (RHS)

Source: RBI, ICICIdirect.com Research

Exhibit 6: Industry deposit growth

010000200003000040000500006000070000

FY 0

7

FY 0

8

FY 0

9

YTDF

Y10

FY10

E

FY11

E

FY12

E

0

10

20

30

40

Amount (Rs. billion) YOY (%) (RHS)

Source: RBI, ICICIdirect.com Research

Exhibit 7: Total business growth for SIB

1385

7

1632

4

2054

2

2591

0

3023

7

3551

1

3710

3 4502

1 5484

5

0

10000

20000

30000

40000

50000

60000

FY05 FY06 FY07 FY08 FY09 9MFY10 FY10E FY11E FY12E

(Rs

Cror

e)

Source: Company, ICICIdirect.com Research

SIB is aiming for a pan-India presence

Total business growth of 18% CAGR will support 21% growth in the balance sheet size

We expect above industry business growth for SIB

South Indian Bank (SOUIN0)

ICICIdirect.com | Equity Research Page 4

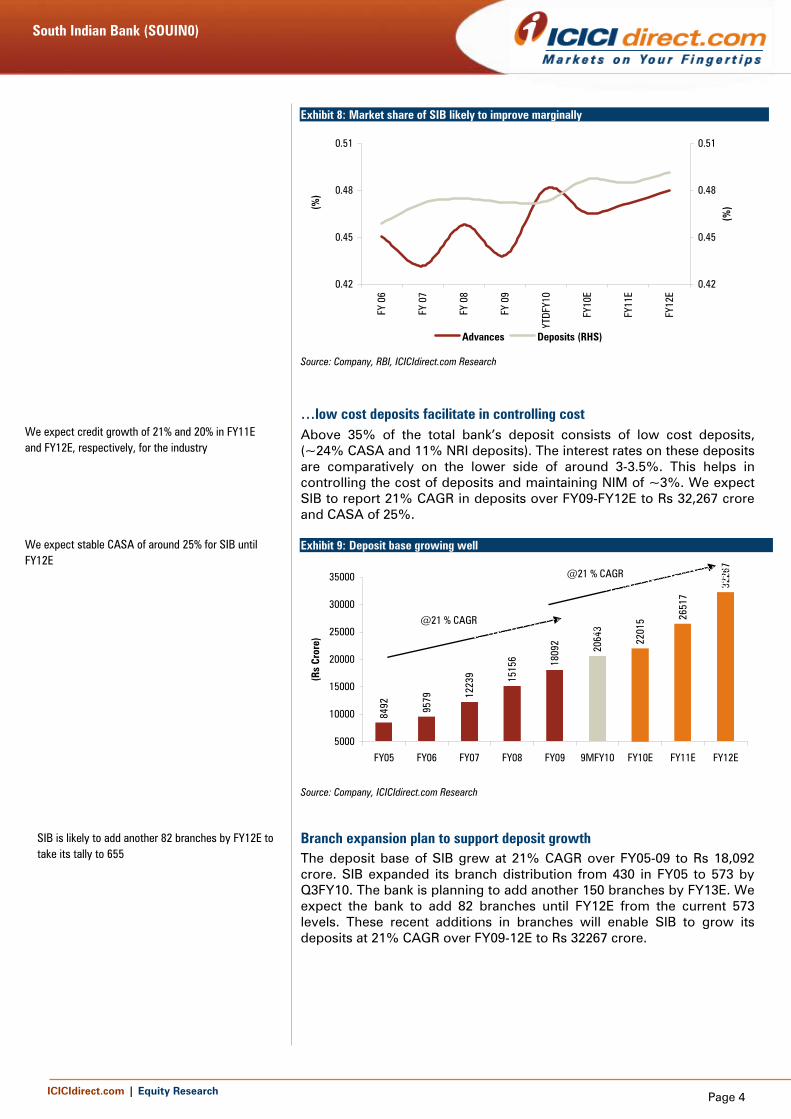

Exhibit 8: Market share of SIB likely to improve marginally

0.42

0.45

0.48

0.51

FY 0

6

FY 0

7

FY 0

8

FY 0

9

YTDF

Y10

FY10

E

FY11

E

FY12

E

(%)

0.42

0.45

0.48

0.51

(%)

Advances Deposits (RHS)

Source: Company, RBI, ICICIdirect.com Research

…low cost deposits facilitate in controlling cost Above 35% of the total bank’s deposit consists of low cost deposits, (~24% CASA and 11% NRI deposits). The interest rates on these deposits are comparatively on the lower side of around 3-3.5%. This helps in controlling the cost of deposits and maintaining NIM of ~3%. We expect SIB to report 21% CAGR in deposits over FY09-FY12E to Rs 32,267 crore and CASA of 25%. Exhibit 9: Deposit base growing well

8492 95

79 1223

9 1515

6 1809

2 2064

3

2201

5 2651

7

3226

7

5000

10000

15000

20000

25000

30000

35000

FY05 FY06 FY07 FY08 FY09 9MFY10 FY10E FY11E FY12E

(Rs

Cror

e)

@21 % CAGR

@21 % CAGR

Source: Company, ICICIdirect.com Research

Branch expansion plan to support deposit growth

The deposit base of SIB grew at 21% CAGR over FY05-09 to Rs 18,092 crore. SIB expanded its branch distribution from 430 in FY05 to 573 by Q3FY10. The bank is planning to add another 150 branches by FY13E. We expect the bank to add 82 branches until FY12E from the current 573 levels. These recent additions in branches will enable SIB to grow its deposits at 21% CAGR over FY09-12E to Rs 32267 crore.

We expect credit growth of 21% and 20% in FY11E and FY12E, respectively, for the industry

We expect stable CASA of around 25% for SIB until FY12E

SIB is likely to add another 82 branches by FY12E to take its tally to 655

South Indian Bank (SOUIN0)

ICICIdirect.com | Equity Research Page 5

Exhibit 10: Branch expansion plan

430 450 475 500 530573 575

615655

20 21 26 30 34 36 38 4349

200

400

600

800

FY05

FY06

FY07

FY08

FY09

9MFY

10

FY10

E

FY11

E

FY12

E

0

20

40

60

80

100

(Rs

Cror

e)

Branches Deposit/branch (RHS)

Source: Company, ICICIdirect.com Research

The bank is predominantly a south-based player, with major concentration in Kerala and Tamil Nadu. Of the total branches currently, 55% is concentrated in Kerala and 19% in Tamil Nadu. We have seen that CASA accumulation for south-based banks is lower compared to other banks where it ranges between 32% and 33%. Exhibit 11: CASA proportion for south based banks (Q3FY10)

24 2520 19

22

33

0

5

10

15

20

25

30

35

SIB Federal bank Karnatak bank City Unionbank

Dhanlaxmibank

Industry*

(%)

Source: Company, RBI, ICICIdirect.com Research *Industry CASA is for FY09

Exhibit 12: Region wise distribution of CASA in India (Industry)

West28%

North21%

South21%

Central14%

East14%

North-East2%

Source: RBI, ICICIdirect.com Research

Higher concentration in the southern zone poses concentration risk to SIB

South zone’s contribution is equal to the northern zone in total CASA accumulation in the industry

South Indian Bank (SOUIN0)

ICICIdirect.com | Equity Research Page 6

Exhibit 13: CASA per branch lowest in Kerala

29

20

12 12 13 1310

0

5

10

15

20

25

30

35

West North South Central East North-East Kerala(R

s Cr

ore)

Focus area of operation

Source: RBI, ICICIdirect.com Research

Exhibit 14: Contribution from Kerala and Tamil Nadu in total business of SIB

54

33

53

33

51

32

11

33

12

33

12

32

0

10

20

30

40

50

60

Deposits Advance Deposits Advance Deposits Advance

Mar-08 Mar-09 Dec-09

(%)

Kerala Tamil Nadu

Source: Company, ICICIdirect.com Research

The share of Kerala in the total business of the bank is declining from 45% in FY08 to 42% by 9MFY10. The management is aiming to curtail it to 35% by FY13E. With branch expansion outside southern states, we expect the share of these states to moderate from current levels. NRE deposits: Hidden CASA

SIB has benefited by operating in Kerala in the form of access to low cost NRE deposits, in addition to CASA deposits, enabling to contain its cost of deposits and, thus, supporting NIM. The cost of these deposits ranges around 3-3.5%. The proportion of NRE deposits in total deposits for SIB has reduced in the past two years from over 20% in FY08 to 17% by Q3FY10 on account of higher growth in bulk deposits to support loan growth. We expect the share of low cost deposits (CASA + NRE deposits) to remain stable around 35% until FY12E. The recent addition of new branches is likely to contribute significantly to CASA accumulation after FY12E.

South zone is a highly banked region of India resulting in lower CASA per branch especially for Kerala

The share of Kerala and Tamil Nadu combined in total business is likely to drift from current levels of 45% owing to branch expansion plans of SIB outside the south zone

South Indian Bank (SOUIN0)

ICICIdirect.com | Equity Research Page 7

Exhibit 15: Low cost deposits boosting NIM

6951

7048

7196 77

27 8047

8306

8555

0

2000

4000

6000

8000

10000

Jun-

08

Sep-

08

Dec-

08

Mar

-09

Jun-

09

Sep-

09

Dec-

09

(Rs

Cror

e)

10

20

30

40

50

(%)

CASA + NRI deposits % of Total deposits(RHS)

Source: Company, ICICIdirect.com Research

Of the total deposit of Rs 20,643 crore in 9MFY10, CASA constitutes ~24% and 11% of NRE deposits as low interest bearing deposits. The NRE deposit base stands at Rs 3,556 crore. Of this, the FCNR account constitutes Rs 1,600 crore where RBI pegs interest rates. Lately, the growth in NRE deposits has moderated because of slowdown in Middle East countries. However, we expect the CASA growth to stem sliding NRE deposit growth. We, thus, expect low cost deposits to stay at current levels of 35% until FY12E. Trend in remittance inflow into India Remittances form a major share of the current account in the balance of payments owing to a large number of Indians who are working abroad and repatriating income mainly for family maintenance. India today is the highest receiver of remittances according to the World Bank's Migration and Development Brief. Remittances to India increased from US$28 billion in 2006 to US$52 billion in 2008. However, it declined to US$47 billion in 2009 owing to the economic recession. With the global economic scenario improving, remittances would rise continuing the trend. South Indian Bank would benefit from such an increase due to its stronghold in southern India. It is the largest recipient of remittance income in India. Exhibit 16: SIB to benefit from growing remittances in India

14

22

28

37

5247

0

10

20

30

40

50

60

2001 2005 2006 2007 2008 2009(est.)

USD

(bn)

Source: RBI, ICICIdirect.com Research

We do not expect a sharp drop in NRE deposits for SIB from current levels

SIB to benefit from remittance income owing to high southern concentration

South Indian Bank (SOUIN0)

ICICIdirect.com | Equity Research Page 8

Loan book growth strong, retail portfolio constitutes ~50% The loan book of SIB grew at 23% CAGR over FY05-09 from Rs 5,365 crore to Rs 12,145 crore. We believe the industry is set for an uptrend in credit growth. The credit growth was dismal @9.9% in Q3FY10. This accelerated to 15.8% in the fortnight ended February 26. We expect credit growth in the industry at 21% and 20% in FY11E and FY12E, respectively. With comfortable CAR of 17.4% and a relatively small loan base, SIB should grow ahead of the industry during our investment horizon. Therefore, we expect 24% CAGR over FY09-FY12E to Rs 22578 crore. Exhibit 17: Loan book grows at 23% CAGR

5365 67

45 8303 10

754

1214

5 1508

8 1850

5 2257

8

1486

8

0

5000

10000

15000

20000

25000

FY05

FY06

FY07

FY08

FY09

9MFY

10

FY10

E

FY11

E

FY12

E

(Rs

Cror

e)

0

10

20

30

40

(%)

Advance YoY Growth (RHS)

Source: Company, ICICIdirect.com Research

The loan book of SIB is tilted towards retail loans, which constitutes nearly 50% of total loans by 9MFY10. Despite such higher retail portfolio, the bank managed to improve its asset quality over the years, reflecting better credit assessment of the bank. We expect the share of retail portfolio to stay at 49-50% until FY12E. Of the retail portfolio, nearly 32% comes from gold loans (~16% of total loan book) where yields are comparatively higher allowing SIB to maintain higher yield on advances of ~11%. Exhibit 18: Components of loan book

13 14 14 14 15 16 169 10 10 10 9 10 1115 14 15 16 14 15 1512 12 14 10 11 10 10

52 50 48 50 51 51 50

Q1FY09 Q2FY09 Q3FY09 Q4FY09 Q1FY10 Q2FY10 Q3FY10

(%)

Agri SME Corporate Housing Others including retail

Source: Company, ICICIdirect.com Research

SIB is adequately capitalised for near term growth

Gold loan forms 32% of total retail loans i.e. 16% of total loan book as of Q3FY10

South Indian Bank (SOUIN0)

ICICIdirect.com | Equity Research Page 9

C/D ratio shifting gears and improving NIM

The C/D ratio of the bank was around 51% during FY04 and started to gain momentum from FY05. In the past five years, the C/D ratio stabilised around 65-66% and improved to 72% in 9MFY10. We expect credit growth to pick up with growth in loan demand in the industry. However, recent branch additions will result in a growth in the deposit base. Thus, the C/D ratio is likely to stabilise around 70%. Exhibit 19: C/D ratio to stabilise around 68%

5553

51

6367

65

6966

7269 70 70

40

45

50

55

60

65

70

75

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

9MFY

10

FY10

E

FY11

E

FY12

E

(%)

Source: Company, ICICIdirect.com Research

Exhibit 20: Industry C/D ratio likely to stay stable

72

7474

72

71

72 72 72

68

69

70

71

72

73

74

75

FY 0

6

FY 0

7

FY 0

8

FY 0

9

YTDF

Y10

FY10

E

FY11

E

FY12

E

(%)

Source: RBI, ICICIdirect.com Research

The new management in place from FY05 started to focus on growing the core business operations. On account of this, the C/D ratio of the bank improved. The reliance on treasury gains reduced drastically and NII growth started to pick up. The net interest income accelerated at 21% CAGR during 2004-2009. We expect 23% CAGR over FY09-12E to Rs 968 crore. SIB was heavily dependent on treasury gains, which contributed over 40% to the net total income in FY04. The C/D ratio in FY04 was dismal at 51%. It gathered momentum and stabilised around 68% after that. We expect the quality of earnings to improve further and estimate the share of interest on advances in total interest income to rise to 80% by FY12E from 71% in FY07.

The C/D ratio of SIB was dismal at 51% in FY04. It improved to 72% in 9MFY10 and we expect it to stabilise at 70% until FY12E

We expect industry C/D ratio of 72% in the next couple of years

South Indian Bank (SOUIN0)

ICICIdirect.com | Equity Research Page 10

Exhibit 21: Income from advances to improve

7174 75 77

79 80

60

70

80

90

FY07

FY08

FY09

FY10

E

FY11

E

FY12

E

(%)

Interest on advances to total int income

Source: Company, ICICIdirect.com Research

Exhibit 22: Treasury gains to net total income

(%)

-10

0

10

20

30

40

50

FY02

FY03

FY04

FY07

FY08

FY09

FY10

E

FY11

E

FY12

E

Source: Company, ICICIdirect.com Research

Interest rates are likely to move northwards again. This will result in higher yield on advances. However, rising deposit cost will result in NIM being maintained at current levels. We, therefore, expect the NIM to stay stable at 3% levels until FY12E.

Exhibit 23: Stable NIM

2.8

3.2 3.1

2.5

2.93.1 3.0 3.0 3.0

0.0

4.0

8.0

12.0

16.0

FY05

FY06

FY07

FY08

FY09

9MFY

10

FY10

E

FY11

E

FY12

E

(%)

1.0

1.5

2.0

2.5

3.0

3.5

(%)

YoA CoD NIM

Source: Company, ICICIdirect.com Research

Lately we have seen steady growth in industrial production. The latest reported figure shows 16.7% YoY growth for January. This suggests that demand for credit (both working capital and term loans) will pick up coupled with a revival in industrial capex. Improving credit demand and rising interest rates should help SIB to protect its NIM at 3% until FY12E.

Exhibit 24: IIP trend positive

8.37.2

119.6 10.3

11.7

17.6 16.7

0

5

10

15

20

Jun-

09

Jul-0

9

Aug-

09

Sep-

09

Oct-0

9

Nov

-09

Dec-

09

Jan-

10

(%)

Source: Industry, ICICIdirect.com Research

Exhibit 25: Credit growth picking up

0

10000

20000

30000

40000

50000

FY 0

7

FY 0

8

FY 0

9

YTDF

Y10

FY10

E

FY11

E

FY12

E

0

10

20

30

40

(%)

Amount (Rs. billion) YOY (%)

Source: RBI, ICICIdirect.com Research

Core interest income contribution to total interest income is gradually rising. This looks quite healthy for SIB

Strong IIP number and economic recovery expected to push credit growth in the coming fiscal

South Indian Bank (SOUIN0)

ICICIdirect.com | Equity Research Page 11

Improving asset quality: A boon SIB has been able to improve its asset quality over the past few years through cautious loan book growth, better recoveries and lower delinquencies. SIB brought down its net NPA to 0.4% from a high of 6.7% and GNPA to 1.5% from over 10% in FY02.

The total stressed assets (GNPA and restructured) at about 2.6% of total loans, with provision coverage of over 73% looks in good shape for SIB. We estimate GNPA at 1.6% and NNPA at 0.8% by FY12E. Exhibit 26: NPAs to rise marginally from current level

366328 321

188

261214

261307

363

204

11878

34

134

57

137 153 175

0

100

200

300

400

FY05 FY06 FY07 FY08 FY09 9MFY10 FY10E FY11E FY12E

(Rs

Cror

e)

GNPA NNPA

Source: Company, ICICIdirect.com Research

Exhibit 27: Improvement in asset quality

5.03.9

1.8 2.2 1.5 1.7 1.7

1.9

1.0

0.31.1

0.40.9 0.8

1.6

6.6

0.8

3.8

0

2

4

6

8

10

12

FY05 FY06 FY07 FY08 FY09 9MFY10 FY10E FY11E FY12E

(%)

GNPA NNPA

Source: Company, ICICIdirect.com Research

Exhibit 28: Stressed asset: Comparative matrix (Q3FY10)

1.53.0

1.3 0.9

2.71.8

1.11.7

4.45.2

4.55.5

2.6

4.75.7 6.1

7.2 7.3

0

2

4

6

8

SIB Federal bank Corporationbank

Andhra bank Central bank Allhabad bank

(%)

GNPA Restructured assets Total stressed

Source: Company, ICICIdirect.com Research

Strong asset quality and low stressed assets to bode well for SIB

SIB has lowest stressed assets among comparatives

South Indian Bank (SOUIN0)

ICICIdirect.com | Equity Research Page 12

Higher HTM proportion to cushion investment book from MTM hit G-sec yields are expected to harden in a rising interest rate scenario. SIB is well placed in such an environment since 77% of the total investment portfolio of Rs 5,838 crore is held in the HTM category, 23% in the AFS category (Rs 1335 crore), with a duration of 0.58 years, and very little in the HFT category. The total investment book duration stands at 4.5 years. Exhibit 29: Distribution of investment book

(Rs Crore)

HTM, 4478, 77%

AFS, 1335, 23%HFT, 25, 0%

Source: Company, ICICIdirect.com Research HTM- Held till maturity, AFS- Available for sale, HFT- Held for trading

Because of a rise in G sec yields from current levels to 8.5%, we estimate SIB will have to provide Rs 7.8 crore of MTM hit on its AFS portfolio. This will affect the bottom-line to that effect. Exhibit 30: Sensitivity analysis of rising G sec yields

Rs Crore HTM AFS AFS duration (yrs) 50 bps 75 bps 100 bps9MFY10 4495 1343 0.6 3.9 5.8 7.8

FY10E 248 1.6% 2.4% 3.1%PAT FY11E 323 1.2% 1.8% 2.4%

FY12E 410 1.0% 1.4% 1.9%

Estimated MTM hit for rise in G sec yields by

Pre tax impact on PAT

Source: Company, ICICIdirect.com Research

Driven by rising food prices India's annual rate of inflation, based on the WPI, rose 9.89% in February YoY against 8.56% in the previous month. We saw inflation rising, resulting in a spike in yields mostly in the long duration (10 years) bond portfolio. The average duration of the SIB investment portfolio is 4.5 years. The movement in five-year yields is not expected to move so drastically as the 10-year bond. Exhibit 31: Movement in G sec yields

5.15.2

7.37.0

8.07.3

4

5

6

7

8

9

1-De

c

7-De

c

13-D

ec

19-D

ec

25-D

ec

31-D

ec

6-Ja

n

12-J

an

18-J

an

24-J

an

30-J

an

5-Fe

b

11-F

eb

17-F

eb

23-F

eb

1-M

ar

7-M

ar

13-M

ar

(%)

1 Year 5 Year 10 Year

Source: Reuters, ICICIdirect.com Research

Bond portfolio is well placed in a rising interest rate scenario

South Indian Bank (SOUIN0)

ICICIdirect.com | Equity Research Page 13

Financials

Net interest income to grow at 24% CAGR The new management, which took charge of SIB in FY06, focused on higher business growth and aimed to reduce dependency on treasury gains. The higher business growth led to strong NII growth of 19% CAGR over FY07-09 to Rs 523 crore. We expect above industry business growth for SIB. This will result in 23% CAGR over FY09-12E to Rs 968 crore. Exhibit 32: Higher than industry business growth to support NII growth

368 376

523 489

651

796

968

200

400

600

800

1000

1200

FY07

FY08

FY09

9MFY

10

FY10

E

FY11

E

FY12

E

(Rs

Cror

e)

Source: Company, ICICIdirect.com Research

Core fee-based income to drive non-interest income We expect the growth in non-interest income to moderate from 26% CAGR over FY07-09 at Rs 164 crore to 17% CAGR over FY09-12E to Rs 266 crore owing to lower treasury gains and comparatively higher growth in fee based income. Exhibit 33: Non-interest income growth to be in line with business growth

103

143164 165

194224

266

0

50

100

150

200

250

300

FY07

FY08

FY09

9MFY

10

FY10

E

FY11

E

FY12

E

(Rs

Cror

e)

Source: Company, ICICIdirect.com Research

Healthy NII growth to support NIM at 3%

South Indian Bank (SOUIN0)

ICICIdirect.com | Equity Research Page 14

Exhibit 34: Break-up of non interest income

7 8 9 4 8 6 85 2

1315

2637

104 7

7 6

6

5

517 22

1818

17

18

21

0

20

40

60

80

Q1FY09 Q2FY09 Q3FY09 Q4FY09 Q1FY10 Q2FY10 Q3FY10

(Rs

Cror

e)

CEB Treasury Forex Others

Source: Company, ICICIdirect.com Research

Employee cost and efficiency The cost ratio of SIB improved from 57% in FY06 to 45% in 9MFY10. However, it is still higher than peers are currently. We do not expect it to fall drastically from current levels owing to the recent branch expansion put into operation by the bank. We expect the cost to income ratio to stabilise around 44% by FY12E. Exhibit 35: Cost to income ratio likely to stabilise around 44% by FY12E

4223 45

23 4893

4900 51

97 5502

48 4845 46 44 44

10001500200025003000350040004500500055006000

FY08 FY09 9MFY10 FY10E FY11E FY12E

Nos

.

10

20

30

40

50

(%)

Employee Cost to income ratio (RHS)

Source: Company, ICICIdirect.com Research

The investment made by the bank in human capital and technology (CBS implementation) is yielding dividends. The business per employee and branch is on the rise. We expect a further improvement on both fronts.

We expect SIB to add over 600 employees by FY12E

South Indian Bank (SOUIN0)

ICICIdirect.com | Equity Research Page 15

Exhibit 36: Efficiency parameters to improve further in tandem with growth in business activity

0

2

4

6

8

10

12

FY05

FY06

FY07

FY08

FY09

9MFY

10

FY10

E

FY11

E

FY12

E

(Rs

cror

e)

0

30

60

90

120

(Rs

cror

e)

Business/Employee Business/ branch (RHS)

Source: Company, ICICIdirect.com Research

PAT estimated at 28% CAGR over FY09-12E The pick-up in business activity coupled with stable NIM and cost ratio will boost PAT growth in the coming period. The PAT, which grew at 37% CAGR over FY07-09, is estimated at 28% CAGR over FY09-12E to Rs 410 crore. The pick-up in PAT will drive return ratios. RoE, which improved from 1.9% in FY05 to 17.4% by Q3FY10, is expected to be around 22% by FY12E. Similarly, RoA is expected at ~1.3% for FY12E. Exhibit 37: Return ratios to improve further

0.9

0.1

0.5

0.80.9 1.0

1.11.2 1.3

1.2

21.4

1.9

8

14 1315

17 1820

22

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

FY04

FY05

FY06

FY07

FY08

FY09

9MFY

10

FY10

E

FY11

E

FY12

E

(%)

0

5

10

15

20

25

(%)

RoA RoE (RHS)

Source: Company, ICICIdirect.com Research

CAGR of 28% in PAT over FY09-12E to improve the return ratio for SIB

South Indian Bank (SOUIN0)

ICICIdirect.com | Equity Research Page 16

Risks & concerns

Concentration risk The share of Kerala in the total business of the bank was 42% by 9MFY10. The management is aiming to curtail it to 35% by FY13E. Hence, it is vulnerable to region specific risk. Delay in expansion plan The management is confident of growing its pan-India reach. We have assigned a valuation multiple on its growing pan India reach. Any delay in plan will affect our future growth projections and bottomline to that effect. Sluggish loan growth in industry We have estimated a revival in growth of credit demand in the industry from FY11E. Any disappointment in credit growth for the industry will affect SIB to that extent. Deterioration of asset quality SIB currently has one of the lowest stressed assets among peers with 2.6% (GNPA 1.5% and 1.1% of restructured assets). The bank has high contribution of the retail portfolio that could lead to higher slippage and rise in NPA in case of prolonged slowdown in economy.

South Indian Bank (SOUIN0)

ICICIdirect.com | Equity Research Page 17

Valuations

At the CMP of Rs 156, the bank is trading at 0.9x FY12E ABV, which looks attractive. The bank, with a healthy low cost deposit base of around 35%, NIM of 3%, strong asset quality (2.5% of stressed assets) and CAR of 17% is poised for above industry growth in the coming period.

South Indian Bank has always traded at a discount to most of its peers historically because of regional concentration, poor asset quality and higher dependency on treasury gains. The new management has concentrated on higher business growth. This has improved the C/D ratio of SIB from a dismal 50% in FY04 to 72% by 9MFY10. A stable C/D ratio and rich low cost deposit enabled it to maintain its NIM of 3%.

Going forward, we expect the bank to grow its balance sheet at 21% CAGR over FY09-12E to Rs 35,832 crore. We have modelled in 24% and 21% CAGR in advances and deposits to Rs 22578 crore and Rs 32267 crore, respectively. We anticipate [email protected]%and [email protected]% for FY12E. With an RoE of above 20% and RoA>1% the stock is trading at a compelling valuation.

Whereas the bank has already improved on most parameters like NPA, NIM and management, it continues to be regional with 55-60% of the total business contributed by the southern region. This is a point of concern for us. Assuming sustainable RoE of 18%, terminal growth of 3% and CoE of 14.5%, we value the bank at 1.2x FY12E ABV of Rs 167 and assign it a fair value of Rs 200.

Exhibit 38: P/ABV band

0

50

100

150

200

Mar

-06

Jun-

06

Sep-

06

Dec-

06

Mar

-07

Jun-

07

Sep-

07

Dec-

07

Mar

-08

Jun-

08

Sep-

08

Dec-

08

Mar

-09

Jun-

09

Sep-

09

Dec-

09

Mar

-10

Price 1.5x 1.3x 1.1x 0.9x 0.7x

Bouncing from trough valuation

Source: Company, ICICIdirect.com Research

Exhibit 39: Peer P/ABV : A comparative matrix

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jan-

05

May

-05

Sep-

05

Jan-

06

May

-06

Sep-

06

Jan-

07

May

-07

Sep-

07

Jan-

08

May

-08

Sep-

08

Jan-

09

May

-09

Sep-

09

Jan-

10

(x)

Federal bank City union bank Karur Vyasa bank SIB

Source: Company, ICICIdirect.com Research

The parameters that traditionally warranted discount in valuation multiple for SIB have improved drastically and warrant higher P/ABV multiple, whichwe are assigning

SIB has always traded at a discount to most peers

South Indian Bank (SOUIN0)

ICICIdirect.com | Equity Research Page 18

Exhibit 40: Ratios FY09 FY10E FY11E FY12E

ValuationNo. of Equity Shares 11.3 11.3 11.3 11.3EPS (Rs.) 17.2 21.9 28.5 36.3BV (Rs.) 113.8 129.8 152.5 182.9BV-ADJ (Rs.) 101.9 117.7 139.0 167.5P/E 9.1 7.1 5.5 4.3P/BV 1.4 1.2 1.0 0.9P/ABV 1.5 1.3 1.1 0.9DPS (Rs.) 3.0 5.0 5.0 5.0

Yields & Margins (%)Yield on avg int earning assets 9.2 8.8 9.1 9.3Avg. cost on funds 6.9 6.2 6.4 6.7Net Interest Margins 2.9 3.0 3.0 3.0Avg. Cost of Deposits 6.3 6.1 6.4 6.6Yield on average advances 10.7 11.0 11.3 11.5

Profitabilty (%)Interest income/ total avg. assets 9.0 8.5 8.8 9.1Net interest income/ total income 28.2 30.9 30.6 30.0Non-interest income/ total income 8.9 9.2 8.6 8.2Non-interest income/ avg. assets 0.9 0.9 0.8 0.8Trading gains/ total income 5.2 4.5 3.9 4.7Non-interest income/ total net income 23.9 23.0 21.9 21.5

Quality and Efficiency (%)Credit/Deposit ratio 65.5 68.5 69.8 70.0GNPA 2.2 1.7 1.7 1.6NNPA 1.1 0.9 0.8 0.8RONW 16.0 18.0 20.2 21.6ROA 1.0 1.1 1.2 1.3

Source: Company, ICICIdirect.com Research

Exhibit 41: RoE decomposition

FY09 FY10E FY11E FY12ENet interest income/ avg. total assets 2.8 2.9 2.9 3.0Non-interest income/ avg. total assets 0.9 0.9 0.8 0.8Non-operating profit/ avg. total assets 3.7 3.8 3.8 3.8Operating expenses/ avg. total assets 1.8 1.7 1.7 1.7Operating profit/ avg. total assets 1.9 2.0 2.1 2.1Provisions/ Avg. total assets 0.3 0.3 0.3 0.3Return on Avg. assets 1.0 1.1 1.2 1.3Leverage (Avg assets/ Avg equity) (x) 15.4 16.4 17.0 17.2Return on equity 16.0 18.0 20.2 21.6

Source: Company, ICICIdirect.com Research

South Indian Bank (SOUIN0)

ICICIdirect.com | Equity Research Page 19

Exhibit 42: Profit and loss account Rs Crore FY09 FY10E FY11E FY12EInterest Earned 1686.9 1911.5 2381.0 2963.5Interest Expended 1164.0 1260.8 1585.3 1995.8Net Interest Income 522.9 650.7 795.7 967.7growth (%) 39.0 24.5 22.3 21.6Non Interest Income 164.3 194.3 223.6 265.6Net Income 687.2 845.0 1019.2 1233.2Operating expense 328.5 387.3 451.4 547.0Gross profit 358.6 457.7 567.8 686.2Provisions 57.3 61.5 93.4 83.5Taxes 106.6 148.6 151.8 192.9Net Profit 194.7 247.6 322.6 409.8growth (%) 28.5 27.2 30.3 27.0

Source: Company, ICICIdirect.com Research

Exhibit 43: Balance sheet Rs Crore FY09 FY10E FY11E FY12ELiabilitiesCapital 113 113 113 113Reserves and Surplus 1191 1373 1629 1973Networth 1304 1486 1742 2086Deposits 18092 22015 26517 32267Borrowings 257 291 338 455Other Liabilities & Provisions 730 851 951 1024Total 20384 24643 29548 35832

AssetsFixed Assets 136 166 197 230Investments 6075 6393 7924 9819Advances 11852 15088 18505 22578Other Assets 284 805 515 507Cash with RBI & call money 1038 1049 1098 1199Total 20384 24643 29548 35832

Source: Company, ICICIdirect.com Research

South Indian Bank (SOUIN0)

ICICIdirect.com | Equity Research Page 20

RATING RATIONALE ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns ratings to its stocks according to their notional target price vs. current market price and then categorises them as Strong Buy, Buy, Add, Reduce, and Sell. The performance horizon is two years unless specified and the notional target price is defined as the analysts' valuation for a stock. Strong Buy: 20% or more; Buy: Between 10% and 20%; Add: Up to 10%; Reduce: Up to -10% Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk, ICICI Securities Limited, 7th Floor, Akruti Centre Point, MIDC Main Road, Marol Naka, Andheri (East) Mumbai – 400 093

[email protected] ANALYST CERTIFICATION We /I, Kajal Gandhi CA Chirag Shah PGDBM Viraj Gandhi MBA-CM research analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our personal views about any and all of the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. Analysts aren't registered as research analysts by FINRA and might not be an associated person of the ICICI Securities Inc.

Disclosures: ICICI Securities Limited (ICICI Securities) and its affiliates are a full-service, integrated investment banking, investment management and brokerage and financing group. We along with affiliates are leading underwriter of securities and participate in virtually all securities trading markets in India. We and our affiliates have investment banking and other business relationship with a significant percentage of companies covered by our Investment Research Department. Our research professionals provide important input into our investment banking and other business selection processes. ICICI Securities generally prohibits its analysts, persons reporting to analysts and their dependent family members from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would endeavour to update the information herein on reasonable basis, ICICI Securities, its subsidiaries and associated companies, their directors and employees (“ICICI Securities and affiliates”) are under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities is acting in an advisory capacity to this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein is solely for informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks. The value and return of investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities and affiliates accept no liabilities for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice.

ICICI Securities and its affiliates might have managed or co-managed a public offering for the subject company in the preceding twelve months. ICICI Securities and affiliates might have received compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of public offerings, corporate finance, investment banking or other advisory services in a merger or specific transaction. ICICI Securities and affiliates expect to receive compensation from the companies mentioned in the report within a period of three months following the date of publication of the research report for services in respect of public offerings, corporate finance, investment banking or other advisory services in a merger or specific transaction. It is confirmed that Kajal Gandhi CA Chirag Shah PGDBM Viraj Gandhi MBA-CM research analysts and the authors of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months. Our research professionals are paid in part based on the profitability of ICICI Securities, which include earnings from Investment Banking and other business.

ICICI Securities or its subsidiaries collectively do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the publication of the research report.

It is confirmed that Kajal Gandhi CA Chirag Shah PGDBM Viraj Gandhi MBA-CM research analysts and the authors of this report or any of their family members does not serve as an officer, director or advisory board member of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. ICICI Securities and affiliates may act upon or make use of information contained in the report prior to the publication thereof.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.