Simon-Erik Ollus in Finnish Energy Day (Montel), Helsinki, June2015

15

Current challenges for the Finnish energy sector – a producer’s view Montel Finnish Energy Day, 11 June, 2015 Simon-Erik Ollus, Chief Economist, Fortum

-

Upload

fortum -

Category

Presentations & Public Speaking

-

view

762 -

download

1

Transcript of Simon-Erik Ollus in Finnish Energy Day (Montel), Helsinki, June2015

Current challenges for the Finnish energy sector – a producer’s view

Montel Finnish Energy Day, 11 June, 2015 Simon-Erik Ollus, Chief Economist, Fortum

Summary: Current challenges for the Finnish energy sector – a producer’s view

• Oversupply in the Northern European power markets, no urgent need for new investments

• Towards market-driven growth of the renewable energy system

• Finnish governmental program burdens CHP and district heating and misses EVs and cost-effective decarbonisation

• Transition in the energy markets started driven by technological development, environmental policies and digitalization

• Customer participation and consumer centric (retail) model needed

2 11.6.2015 Montel / Simon-Erik Ollus

Power demand has been declining in recent years…

3

Source: Fortum Industrial Intelligence, ENTSO-E. Note, the consumption figures are the actual figures, not adjusted to normal temperature

470

480

490

500

510

520

530

540

550

560

570

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

TWh Annual electricity consumption in Germany

365

370

375

380

385

390

395

400

405

410

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

TWh Annual electricity consumption in the Nordics

~ - 10% ~ - 3% Trendline

Actual demand Trendline

Actual demand

11.6.2015 Montel / Simon-Erik Ollus

…while supply has been growing, driven by subsidised renewables

4

Source: ENTSO-E for 2010, 2014, Marketskraft for 2020

10 % 13 % 21 %

0

50

100

150

200

250

300

350

400

450

2010 2014 Est. 2020

TWh

Total supply and share of subsidized renewable energy in the Nordics

Subsidized RES (Wind and biomass)Other supply

13 % 23 % 29 %

0

100

200

300

400

500

600

700

2010 2014 Est. 2020

TWh

Total supply and share of subsidized renewable energy in Germany

Subsidized RES (Wind, solar and biomass)Other supply

Disclaimer:The presented future development is based on Markedskraft analysis, and does not represent a Fortum view on the development

…and today the market is notably oversupplied and consequently power prices have declined

5

Source: Bloomberg

0

10

20

30

40

50

60

70

80

90

€/MWh German power prices

EEX forward in Nov 2011 EEX forward in May 2015 EEX Actual

~ - 40 %

0

10

20

30

40

50

60

70

80

90

€/MWh Nordic power prices

NPSYS forward in Nov 2011 NPSYS forward in May 2015 NP Actual

~ - 40 %

Power prices have declined by ~40% since 2011 and even ~60% since 2008

11.6.2015 Montel / Simon-Erik Ollus

Consequently, no market signal for new investments in generation…

6

The levelized cost shows the achieved electricity price required for an investment to break even over the lifetime of the project. Disclaimer: The presented figures do not represent Fortum’s own view on the levelized costs of electricity. The figures are based on recent external publications. Key assumptions: real discount rate 5%, corporate tax 20% . Overnight costs, €/kW 4420 for nuclear, 940 for gas, 1920 for coal, 1440 for onshore wind, 2340 offshore wind, 2580 for hydro, 1000 for ground mounted solar. Peak load factor for ground mounted solar 19%; for onshore wind 27%; for offshore wind 34%, for large hydro 40%, for nuclear, gas and coal 91%. Economical lifetime: 30 years for solar, 40 years for nuclear and hydro, 25 years for others. Fuel prices are the market forward prices as of November 2014 extended by applying inflation of 2%. Note, there are large variations in cost of hydro, wind and solar depending on location and conditions.

Sources: Sähkön tuotantokustannusvertailu. Vakkilainen Esa, Kivistö Aija, Tarjanne Risto. Lappeenrannan teknillinen yliopisto. 2012. Projected Costs of Generating Electricity: 2010 Edition. International Energy Agency. 2010. IEA World Energy Investment Outlook 2014. Lazard's Levelized Cost of Energy Analysis - Version 8.0. 2014.

0

10

20

30

40

50

60

70

80

90

100

Nuclear Gas Coal Solar PV inSpain

Onshore wind Offshore wind Large hydro

€/MWh Average levelised costs of new electricity generation (including 20% corporate tax)

LCOE (fuel and CO2prices based on futuresas of May, 2015)

Nordic SYS future pricefor 2020 (as of May 28,2015)

Power prices do not remunerate break even level for new investments, new investments are subsidised

11.6.2015

Meanwhile security of supply is a concern in Finland according to some, but do we seriously even have a problem…

7

*calculated based on (production +import capacity) / (cold year peak load)

Available generation capacity and peak loads during a normal winter day in Finland

Wind generation

Condense generation

DH CHP

Industrial CHP

Hydro

Nuclear

Peak demand, normal year

Peak demand, cold year

Import capacity

Reserve margin of system*:

~13% ~3% ~10% ~13%

Source: Pöyry Consulting, January 2015

Disclaimer: The presented Finnish balance development is based on Pöyry analysis, and does not represent a Fortum view on the development

COPYRIGHT©PÖYRY

…as regional energy markets secure continuity of supply

8

Finland is a part of the broader Nordic and Baltic market and all neighbouring markets are oversupplied

• Generation adequacy needs to be addressed regionally in each market area • Continuity of supply enhanced primary by increased interconnection capacity

05000

10000150002000025000

North-WesternRussia

MW

Peak production

Peak demand

0

10000

20000

30000

40000

50000

60000

70000

Other Nordics

MW

1000MW

0

5000

10000

Baltics

MW

Source: Pöyry, Fortum

11.6.2015 Montel / Simon-Erik Ollus

New internal Nordic grid investments provide for increased available capacity for transmission to the Continent and Baltics

320 MW of transmission capacity available on the 1,300 MW RU-FI link since December 2014

EU’s Connecting Europe Facility co-financing 3rd EE-LV transmission line, due to be ready by 2020

EU’s European Energy Programme for Recovery co-financing 700 MW NordBalt (ready 12/2015)

LitPol link (500+500 MW) to connect the Baltic market to Poland by end -2015/20. Svenska Kraftnät agreed 3/2014

with 50Hertz to study a new Hansa PowerBridge DC link between Sweden and Germany

Jutland – DE capacity planned to grow by 860 MW by 2019, with further 500 MW increase by 2022

EU financial support for a 700 MW DK-NL link, due to be built by 2019

First direct 1,400 MW NO-DE link agreed to be built by 2018

Two 1,400 MW NO-UK links as EU Projects of Common Interest: NSN link to England agreed to be built by 2020, NorthConnect to Scotland still requiring Norwegian permission

Existing connections Future cross-border connections

Future connections

Continuity of supply improved best by enhanced Nordic transmission planning and enforcements

Transmission network operators’ cross-border grid plans by 2020:

9

• Nordic and Continental interconnection capacity will double to over 10,000 MW by 2020

• The 15 price areas in the Nordics is too much

• More effort to decrease price areas and bottlenecks inside the Nordic market area. More focus on joint system planning.

• Additional FI-SE cable a quick win for CoS

Source: ENTSO-E 10-year plan, Fortum

11.6.2015 Montel / Simon-Erik Ollus

Finnish government programme on energy – a producer’s view: No surprises, but several important elements missing

10

Issue Positive (+) / negative (-)

impact

• National RES target > 50% in 2020s (~current RES ~37%) and energy independence to > 55%

+ / - Depends much on the national tool to incentivise development, assumes that specific RES subsidies will be needed in addition to the EU ETS

• RES subsidies towards market based direction

+ + Direction right, concrete proposals missing. Could Finland join the SE-NO elcert-system?

• Phase out coal use in energy production in 2020s

+ / - Depends much on the national tool to incentivise development, could undermine the EU ETS.

• Abandon tax discount on CO2 for CHP

- - Decreases the competitiveness of CHP and district heating

• Increase RES target in transportation – no mention of electrification of transportation

+ / - Target good, but should be technology neutral. No incentive to support EVs

• Decrease wind generation target from 2500MW to 2000MW by 2020

+ Oversupplied markets today, decreased need for RES.

• Industrial compensation for indirect CO2 price effect

+ + Energy intensive industry to get compensation for their CO2 price effect in electricity bill. Industry become more friendly towards CO2 –steering?

11.6.2015 Montel / Simon-Erik Ollus

Several important issues missing in programme: 1. Electrification of transportation, 2. Tools to secure security of supply in case market does not function, 3. Retail market development, and 4. Role of nuclear

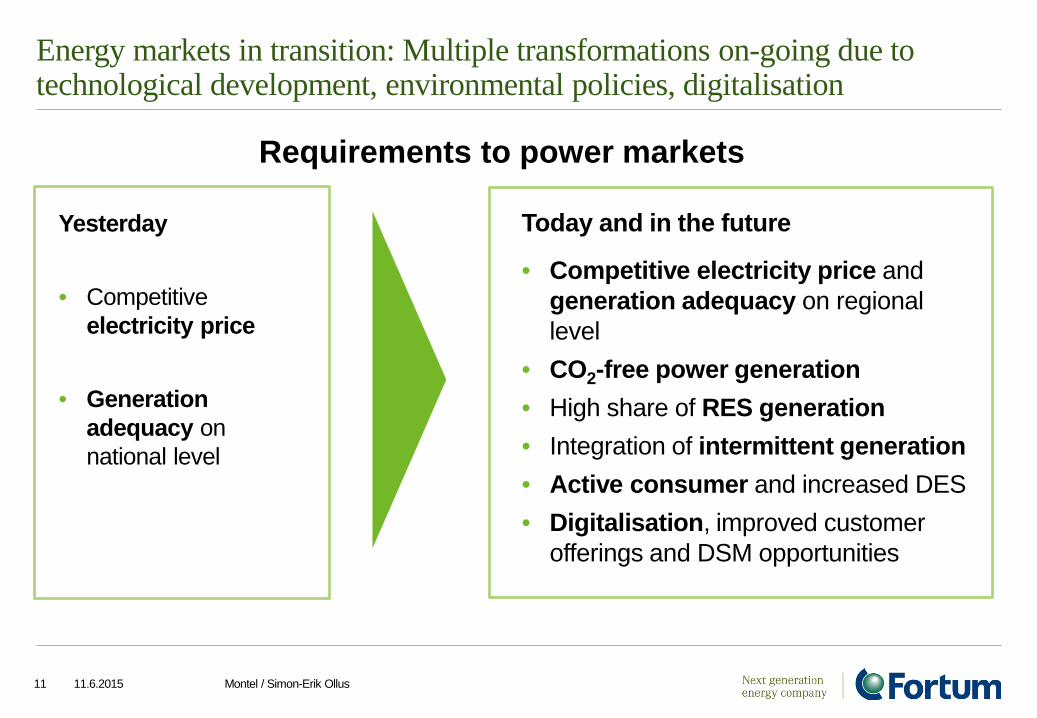

Energy markets in transition: Multiple transformations on-going due to technological development, environmental policies, digitalisation

11

Yesterday

• Competitive electricity price

• Generation adequacy on national level

Today and in the future

• Competitive electricity price and generation adequacy on regional level

• CO2-free power generation • High share of RES generation • Integration of intermittent generation • Active consumer and increased DES • Digitalisation, improved customer

offerings and DSM opportunities

Requirements to power markets

11.6.2015 Montel / Simon-Erik Ollus

How to ensure that energy markets deliver on the future ambitions

• The beauty of simplicity – simple policy steering tools are more efficient than multiple overlapping tools

• Generation adequacy to be assessed regionally in each market area (i.e. Nordics) – National solutions becoming increasingly costly for consumers

• Towards fewer price areas in the Nordic countries. Transmission grid needs to be planned on the Nordic level

• Power markets to better award flexibility and balance intermittency, by e.g. moving gate closure times closer to real-time

• Emissions Trading Scheme as the driver of decarbonisation. And also the driver of growth of renewable energy

• Enable the customer participation. Investments in smart meters and grids to be utilised. Consumer centric (retail) model as the preferred model.

12

No quick fixes – but several principles to work on

11.6.2015 Montel / Simon-Erik Ollus

Wrap-up: Current challenges for the Finnish energy sector – a producer’s view

• Oversupply in the Northern European power markets, no urgent need for new investments

• Towards market-driven growth of the renewable energy system

• Finnish governmental program burdens CHP and district heating and misses EVs and cost-effective decarbonisation

• Transition in the energy markets started driven by technological development, environmental policies and digitalization.

• Customer participation and consumer centric (retail) model needed.

11.6.2015 Montel / Simon-Erik Ollus 13

Next generation energy company

11.6.2015 Montel / Simon-Erik Ollus 14

Back-ups: Electricity wholesale price has dropped in recent years while retail price has climbed

Nordic wholesale and end-consumer prices in 2000-2014, €c/kWh:

Increased taxes, grid charges and subsidies have raised the price consumers pay for electricity

Source: Nord Pool Spot, Eurostat

15 11.6.2015 Montel / Simon-Erik Ollus