Review of the Business Innovation Facility portfolio

85

Review of the Business Innovation Facility portfolio Assessing results and trajectories of inclusive businesses at the end of a three year pilot BIF M&E team, Caroline Ashley, Carolin Schramm, Adriano Scarampi December 2013 Full version

Transcript of Review of the Business Innovation Facility portfolio

Review of the Business Innovation

Facility portfolio Assessing results and trajectories of inclusive businesses at the end of a three year pilot

BIF M&E team, Caroline Ashley, Carolin Schramm, Adriano Scarampi

December 2013

Full version

Content

Section name Page #

Introduction 3

Section 1 – Portfolio overview 9

Section 2 – Lead organisations 14

Section 3 – Inclusive business models 20

Section 4 – Inclusive business implementation process 26

Section 5 – Commercial results 35

Section 6 – Development impacts 55

Section 7 – Additionality of BIF support 68

Section 8 – Short projects feedback 79

Key acronyms

BoP: Bottom of the

pyramid

IB: Inclusive Business

MNC: Multi-national

Corporation

TA: Technical assistance

Introduction

3

The purpose of this document is to share the full M&E findings from the BIF

portfolio. It covers facts and figures in detail and includes reflections and

summarised findings. More information can be found in other BIF

publications (http://bit.ly/BIFPublications)

• This review summarises and explores emerging results and findings from the almost 300 inclusive businesses across

five countries (Bangladesh, India, Malawi, Nigeria and Zambia), that have been supported by the Business Innovation

Facility (BIF) over the past 3.5 years. Support from BIF is not cash, but technical input – some weeks or months of

advisory support to help the business overcome challenges, seize momentum, and make progress in its inclusive

business journey (see page 5 for further information on the logic of BIF support).

• BIF offers two types of support.

• Long term technical support has been offered to 40 companies on a cost-sharing basis. In general, this support

can last between three and six months. The providers of technical assistance are often deeply involved with the

company for the period of time. The impact of the support is carefully monitored and evaluated. We call these

‘Long Projects’

• Short term technical support. This is provided to a company, or a cluster of companies on one aspect of their

business venture. This short term support (up to 20 days) focuses on helping them to overcome an immediate

bottleneck or to seize an opportunity. We call these ‘Short Projects’. Around 60 companies have been the

direct beneficiaries of this support, as well as almost 200 companies that have taken part to workshops and

focus groups.

• We draw on various data sources (company data, consultant feedback and BIF team knowledge and insights) both

quantitative and qualitative. This review focuses mainly on long projects for which – given the fact support is longer and

more substantial – we also have obtained more monitoring & evaluation data (see pages 7 and 8 for further

information).

• This review builds on previous analysis done over the lifetime of the BIF pilot and compares data over time where

possible. To access previous reviews please visit http://businessinnovationfacility.org/group/inclusive-business-impacts-

network

BIF Context & Background

4

The logic of BIF

5

For a more detailed overview of BIF's logic chain see our Spotlight, the logic of Business Innovation Facility

support ( http://bit.ly/BIFlogic ), that builds up a diagram of our logic chain in six steps. It shows the journey that

companies are on developing inclusive business, where BIF intervenes, and how this is intended to lead to

impacts at the Base of the Pyramid, changes in systems and uptake of inclusive business by others.

BIF support The pilot BIF has provided support to 40 long and 68 short projects across five countries. The total value of the technical

assistance for long projects is $1,883,475 and $759,817 for short projects, i.e. a total of approximately $2.6million. This

review focuses mainly on long projects.

Lead organisations Medium and large companies predominate regardless of location. Only a few are start-ups or led by NGOs. In our

analysis of lead organisations for long projects we differentiate between two categories:

• Established medium/large companies that are diversifying into inclusive business (63%); we refer to these as

‘diversifying-into-IB’ in short

• Where the inclusive business is the core business model of the company (35%); we refer to these as ‘core-IB’ in short

Inclusive Business

Models

The portfolio is split almost evenly between inclusive business projects that primarily benefit consumers at the BoP and

those that benefit producers. Projects are spread across many sectors, but with a heavy concentration in food and

agriculture. A handful of projects have a particular focus on women and/or the environment.

Inclusive Business

implementation

progress

It was always expected that the BIF portfolio would include businesses that flourish, many that progress, and a few that

falter, though firm predictions of percentages were never made. As of September 2013, a snapshot of the portfolio

shows that 80% of the large projects are progressing and one in five has stalled or been cancelled. Of those making

progress, two so far count as flourishing, and just over half count as progressing well.

Commercial

Results

Current turnover of the inclusive businesses varies widely from zero to several millions. Business growth has been

variable in the first year or two since a baseline was completed with BIF. Focusing exclusively on the 18 businesses that

have actual outturns for Years 0 and 1, we can see that turnover grew by 62 per cent from around $95,000 to $155,000.

Based on latest actual figures available four projects are reporting positive profits. A further seven estimate positive

profits in year 1.

Development

impacts

Impacts at the BoP are moderate so far, potentially high, certainly variable and difficult to estimate.

At the time of BIF baselines, the total portfolio was reaching around 75,000 people at the BoP, while latest data for Year

1 is to reach around 235,000. Companies have reported that the reach is expected to grow to a total of 5.7m households

in year 5. Adjusting these estimates by an optimism factor and scaling them down by the current progress of the projects

has allowed us to estimate these figures to a more realistic 3.7m. Of these, we believe that 1.5m households can be

plausibly linked to BIF’s input.

BIF BIF support has focused mainly on business planning support. About 50% of projects perceive strong additionality.

Around 40% identify medium additionality.

Headline messages

7

Data sources for this review

The methodology of BIF’s Monitoring and Evaluation (M&E) system is centred around three milestones

1. An initial Baseline, just before or at the start of service delivery

2. A Progress Report, at completion of service delivery from the Facility

3. An Update Report, completed 12 months after the Progress Report

The data used during this portfolio review has been collected during the three milestones, as well as during the initial

application process through ongoing project management. It is made of both quantitative and qualitative data, which

we have aggregated to provide an overview of the composition of the portfolio, the progress to date and the

expectations going forward.

In addition, we have conducted regular team assessments of various indicators around project progress which are

also part of this review

The diagram below summarizes the various stages of the process, including the type of forms that have been

collected along the way.

BIF

technical

Support

Selection

M&E

milestone #1

Baseline

assessment

After 1

year

M&E

milestone #2

Completion of

support

M&E

milestone #3

Update on

progress

Baseline

Country Manager Wrap

Up report

Service Provider

Feedback report

Project Update

report

Application

form

Application

Progress

Report

8

Project sample sizes subject of this review

40 Application forms

Baseline forms 40*

Progress Reports A (qualitative) 32

Progress Reports B (quantitative) 25

Project Update reports 14

Service Provider Feedback

Country Manager Wrap Up

Team knowledge and research

Sample subject of this portfolio review

Data sources

40**

46

37

32

Long projects approved by BIF selection committee

Long projects contracted, for which baseline was

carried out and BIF support started

Long projects for which BIF support is completed or

expected to be completed

Projects for which updated quantitative & qualitative

data is available (Progress Report or Project Update)

Data availability

* In some instances the sample will be lower than 32 because of the impossibility to capture certain data or poor data provided by the

organisations

** Although all projects completed the baseline reports, one was not able to provide any financial data

Various

39

In total 46 long projects have been approved by the BIF selection committee over the past 3.5 years. BIF support,

however, only began for 40 of these. For 32 projects we obtained updates to information collected at baseline.

Hence, for basic analysis our sample size is 40 and for comparison over time our sample size, in most cases, is 32*.

Section 1

Portfolio overview

9

Overview of BIF input

• The BIF portfolio includes 40 long projects for which

support has been completed (or completion is expected

in due course)

• The average contractual length of the long projects is of

5.5 months. The longest project lasted for 17 months

and the shortest for 2

• The total contracted value of TA support provided is

$1,883,475

• Average BIF spend per project: $47,087

• Highest BIF project input: $115,930

• Lowest BIF project input: $13,200

Match funding

• Total amount match funded by the businesses

themselves is: $2,223,509, which corresponds to 117%

of the amount spent by BIF on TA

• Of this funding, $791,380 was in actual cash

contribution, equal to 42% of BIF’s spend on TA (this

was spent for marketing costs, paying for the hire of

external resources etc…)

• The highest match funding has been for a total of

$175,000, that went to cover product R&D and

marketing costs

Portfolio of the 40 long projects

10

9

6

9

6

10 Zambia

India

Bangladesh

Malawi

Nigeria

Long projects by country of operation (N=40)

$41,947

$56,167 $54,960 $49,538

$43,205

-

10,000

20,000

30,000

40,000

50,000

60,000

Zambia India Bangladesh Malawi Nigeria$

Average long project BIF spend per country, $ (N=40)

46%

35%

19%

BIF TA spend

In kind from recipientorganisations

Cash injection from recipientorganisations

Breakdown of spend (N=40)

Our portfolio of long projects: 40 companies, 5

countries

11

Bangladesh – 9

JITA, Agora, Pabna Meat, ERAS,

ACI, Shiblee, PRAN Agro, large

international NGO*, food producer*

India - 6

Azure, HUL, MCX

GSK, Saraplast,

mKRISHI®,

Waterlife/Bosch

Nigeria - 10

AACE, Furniture Village,

Guinness, Stanbic, Dala

Food, Teragro, L&Z, d.light,

Best Foods, O-Gas

Zambia - 9

Ischool, Barrick,

Healthstore, Sylva Foods,

Tata Tannery, CEC,

Cropserve, Sun Hotels,

Lafarge Malawi - 6

Malawi Mangoes,

Microloan, MEGA, Afrinut,

Universal, tea company*

* confidential

* confidential

Logos are illustrative

Overview of BIF input

• The BIF portfolio includes 68 short projects

• Of these, 46 were one-to-one TA interventions, and 22

were one-to-many workshops and research projects

• The total value of TA support provided is $759,817

• Average BIF spend per project: $11,174

• Highest BIF project input: $24,543

• Lowest BIF project input: $2,550

Portfolio of the 68 short projects

12

$10,998

$13,646

$10,626 $9,999

$12,307

Zambia India Bangladesh Malawi Nigeria

Average short project spend per country (N=68)

10

6

14 21

17 Zambia

India

Bangladesh

Malawi

Nigeria

Short projects by country of operation

(N=68)

46

22 one-to-one

one-to-many

Short projects: one-to-one vs one-to-many (N=68)

Our portfolio of short projects

13

Bangladesh – 15

ACI, BSOA (Bangladesh

Supermarket Owners

Association, FSB, M&S,

Mitsubishi, Pabna Meat, Gain +

workshop participants

India - 6

Airtel, Milk Mantra,

Azure Power, Better

Cotton Initiative,

Sankalp + workshop

participants

Nigeria - 18

Abira, Beekeeping

Extension Society, Folawiyo

Farms Ltd, Guinness,

League of Contractors,

Onward Papermill,

Sabeanat Nigeria Ltd +

workshop participants

Zambia – 10

ARK, BioCarbon Partners

Zambia Limited, CHC

Commodities, Sun Hotels,

Sunline, Taj Pamodzi Hotel

+ workshop participants

Malawi – 22

Afrisphere Worldwide, Charles Stewart, CISP,

Ecobricks, Global Tea and Commodities,

Independent, Malawi Mangoes, Moringa

Miracles, Nali, Rab Processors, Tree Crops

Ltd + workshop participants

Logos are illustrative

Section 2

Lead organisations

In our analysis we distinguish between host companies (“lead organisations”) and their inclusive business models.

In some cases the two are identical, e.g. a small start-up company for which the main and only activity is the

‘inclusive business’. For others, this is not the case, e.g. for medium or large companies that only focus a part of

their business on becoming more inclusive. This gives us two important categories:

• Established medium/large company that is diversifying into inclusive business (62.5%), we refer to these as

‘diversifying-into-IB’ in short

• Inclusive business is the core business model of the company ( 35%), we refer to these as ‘core-IB’ in short.

2.5% of businesses cannot be clearly associated with one category because they are led by an NGO or

International organisation.

14

5

10

3

5

13

10

- 5 10 15

4

10

1

5

6

14

- 5 10 15

NGO international

Internationalmedium/large

NGO domestic

Domestic & startup

Domestic and small

Domestic andmed/large

• We differentiate between lead organisations and

the inclusive business venture

• Lead organisations are defined as the organisations

that BIF has a contractual relationship with

• The size of the lead organisation is determined by

its number of employees:

• Start up or Micro: 10 employees or less

• Small: less than 50 employees

• Medium: between 50 and 250

• Large: more than 250

• The portfolio is diverse: two thirds of lead

organisations are domestic, and one third

international

• Over half of the companies of the 40 long projects

are medium or large (size based on employee

numbers)

• Short projects have a larger proportion of small

domestic lead organisations

A diverse portfolio of lead organisations

15

Long projects (N=40) Short projects (N=46)*

Number of projects per type of lead organisation

* Only 46 lead organisations for the short projects are included as these are the one-on-

one projects. BIF does not have contractual relationships with any organisations on most

one-to-many short projects

# projects

• In terms of number of employees, 43% of the organisations BIF has contracted with have over 250 employees

• Medium and large companies predominate also when looking at the lead firm turnover

• Amongst the 35 contracting organisations for which turnover data is available, 29 (81% of the total) have turnovers

over $1 million

• Seven of these are MNCs: Hindustan Unilever, Tata Group, Waterlife, Guinness, Stanbic, Tata Tannery, and a large

food producer

Medium and large companies predominate in our

portfolio of long projects

16

4

9 10

17

0

2

4

6

8

10

12

14

16

18

Start-up ormicro (10

employees orless)

Small (less than50)

Medium(between 50

and 250)

Large (250plus)

Categorisation of lead firm by number of employees

(N=40)

For four lead firms, turnover data is not available

2 1

4

12

17

-

2

4

6

8

10

12

14

16

18

>=0,<=10,000

>10,000,<=100,000

>100,000,<=1,000,000

>1,000,000,<=10000000

>10,000,000,

$

Categorisation of lead firm turnover (N=36)

17

Medium and large companies predominate regardless

of location. Only a few are start-ups or led by NGOs

1

2

2

1

4

1

2

3

1

2

4

4

3

5

2

3

- 2 4 6 8 10

Zambia

India

Bangladesh

Malawi

Nigeria

# projects

Start-up or micro (10 employees or less)

Small (less than 50)

Medium (between 50 and 250)

Large (250 plus)

Lead organisations categorised by number of

employees and country (N=40)

• In all countries medium and large companies make up a

large proportion of all long projects

• India does not have any small, micro or startup projects

in its portfolio

• Three lead organisations can be classified as startups:

MEGA and Malawi Mangoes in Malawi, AACE in Nigeria

• Six projects are led by NGOs

Lead NGO Country Project name /

company name

Twin Trading Malawi Afrinut

Microloan Foundation Malawi Microventures

Large international NGO* Bangladesh

CARE Bangladesh JITA

Waterlife India Partnership with Bosch

Healthstore Foundation Zambia One Family Health

Projects where the leading organisation is an NGO

* Confidential

Project relationship to lead organisation

18

• We categorise how the inclusive businesses fits into the lead

organisation in the following way:

– Diversifying into IB (62.5% of all long projects): these

are organisations for which the Inclusive Business is a

small part of their overall operations (see diagram with

ACI’s example below)

– Core-IB (35% of all long projects): organisations for

which the Inclusive Business is the lead organisation

itself (see MEGA’s example below)

– Other (2.5% of all long projects): These are projects for

which the other two categorisations do not apply. Only

one cannot be categorised as it is a large NGO-led

programme

• Our portfolio of large projects is well split between the two

different business models

MEGA’s Inclusive Business boundaries ACI’s inclusive business boundaries

25

14

1

Diversifying into IB

Core-IB

Other

Portfolio Breakdown of type of project (N=40)

19

Driving departments in lead organisations

* Using latest available data, 14 projects reported at Progress Update / Project Report, 18 at Baseline

“Other” also includes “General Management”

3

5

4

1

3

2

6

4

4

- 4 8 12

Social responsibility / Public affairs / Communities relations

Operations / Procurement / Supply / Sales

Central innovation / Strategy / R&D

General Management

Other

# projects

Diversifying-into-IB Core-IB

Driving departments in lead organisations, by IB model (N=32)

Section 3

Inclusive business models

This section looks at a range of different characteristics that we use to define and categorise the inclusive business

ventures that BIF has supported. For example, the type of project is defined by sector, product and beneficiary

group (consumers / producers / distributors) . Or in other words the area in the value chain where the greatest

benefits for low income people occur. We also illustrate which projects have a particular focus on women and/or the

environment.

20

• The portfolio is split almost evenly between inclusive

business projects that primarily benefit consumers at

the BoP and those that benefit producers. JITA in

Bangladesh, is the only long project that targets BoP

distributors.

• Around one quarter of projects* also have a

secondary group of beneficiaries. In the case of JITA,

it is projected that up to 2million rural women

consumers will also benefit

• It is important to note that a project is considered

‘consumer focused’ if it sells goods and services to

the BoP – even if they are farmers and their

livelihood is production, E.g. mKrishi® or MCX

• Short projects are predominantly producer focused.

This is driven by the predominance of Malawian and

Nigerian projects in the portfolio, which have a

greater focus on BoP producers.

• Six short projects cannot be classified in terms of

BoP focus. These are networking workshops aimed

at bringing together various players within an industry

sector, not focusing on a specific BoP target

Base of the Pyramid (BoP) focus

21

49

11

2 6 Producer

Consumer

Distributor

N/A

Short projects by primary BOP beneficiary type

(N=68)

21 18

1

Producer

Consumer

Distributor

Long projects by primary beneficiary type (N=40)

JITA

* JITA (Consumer), Malawi Mangoes (Distributor), d.light (Distributors), L&Z (Distributors), Dala Food (Producers), Healthstore

(Distributors), Sylva Foods (Consumers),

BoP focus by country

22

5

5

5

6

4

6

3

1

4

1

- 2 4 6 8 10

Zambia

India

Bangladesh

Malawi

Nigeria

# projects

Project BoP Focus by Country (N=40)

Producer Consumer Distributor

• When looking at BoP focus by country, we see

divergence.

• The largest of our markets, India, focuses

exclusively on projects targeting consumers at

the BoP. These are mainly inclusive businesses

bringing products to the BoP that aim at

improving their lifestyle and living conditions (e.g.

Waterlife, mKrishi®, HUL)

• The smaller Malawian economy, with a large

rural population heavily reliant on the agricultural

sector, has a majority of projects targeting

producers. The principle aim of these projects is

to develop inclusive value chains linking

smallholder farmers to markets, such as

Universal, Malawi Mangoes and Afri-nut

• The Zambian, Nigerian and Bangladeshi

portfolios are more balanced.

32

7

8

10

1

3

3

4

20

7

6

3

2

1

1

- 10 20 30 40

Agriculture and Food

Energy and Infrastructure

Retail, manufacturing andconsumer goods

Other (includes education andICT)

Water, sanitation and wastemanagement

Health

Finance

Cross-sector

# projects

Number of projects by sector of operation

Long projects (N=40) Short projects (N=68)

• Projects are spread across many sectors, but

with a heavy concentration in food and

agriculture.

• This sector includes projects that sell to

farmers (e.g. soil testing kits), purchase farm

products for processing (e.g. mangoes for

juice, hides for tanning), or are sourcing for

food manufacture (e.g. soups) or retail sale

(e.g. urban supermarkets).

• Long projects that benefit farmers as

consumers include mKrishi®, MCX GSK,

ERAS, Cropserve

• Four short projects are not aligned to any

specific industry sector and have been

categorised as “cross-sector”. These are

workshops bringing actors from various

industries together to discuss and network

around the issue of ‘doing’ Inclusive Business

Projects by sector of operation

23

Farmers as consumers: 4

Farmers as consumers: 6

24

Focus on women

Project Country Focus on women

JITA Bangladesh Rural distribution

Pabna Meat Bangladesh Value chain / cattle

PRAN Bangladesh Value chain / cassava

Food

producer **

Bangladesh Nutrition

Shiblee Bangladesh Fish farming

Afri-nut Malawi Value chain / groundnut

Universal Malawi Value chain / cassava

Microloan Malawi Micro-credit for farming

O-Gas Nigeria Cookstoves

Projects with a focus on women (more than 50% of BOP

beneficiaries)

* Categorisation based on BIF team assessment

** Company name confidential

• Nine projects (22.5% of total) are categorised as having a

particular focus on women. Among these, there are producer

focused projects targeting value chains in which women play

an important role (Afri-nut / peanuts, Pabna Meat / Beef,

Universal / cassava), projects linking women to agricultural

markets (Microloan and ERAS) and projects aimed at

empowering distributor women (JITA)

• The thirteen projects classified as targeting less than 50% of

women beneficiaries are mostly projects engaging with male

farmers 13

18

9

-

2

4

6

8

10

12

14

16

18

20

Less than 50% Around 50% More than 50%

Projects by % of women beneficiaries (N=40) *

25

Focus on the environment, ‘climate smart’

projects

7

33

Climate smart projects

Non-climate smart projects

Projects that are be classified as ‘climate smart’ (N=40)

Project Country

ERAS Bangladesh

Waterlife / Bosch India

Azure Power India

MEGA Malawi

Malawi Mangoes Malawi

O-Gas Nigeria

CEC Zambia

List of ‘climate smart’ projects

Example projects

Waterlife/Bosch - India

In partnership with Bosch, Waterlife is seeking to

develop an inclusive business project based on

sound water management. The objective of this

project is to develop an end-to-end system for

water management. As affordable clean drinking

water in India is scarce due to the high cost of

filtration, by 2050, water availability is expected to

drop by about 44%. Waterlife have therefore

identified a significant opportunity to develop a

new technology solution to supply affordable

drinking water to low-income communities.

ERAS - Bangladesh

ERAS aims to create viable private sector supply

chains that give smallholders access to affordable

and effective soil testing services. The

Environmental Research and Analytical Service

(ERAS) aims to provide low-cost materials (start-

up laboratory kits and chemical reagents),

knowledge and support (training and long-term

advisory) for local entrepreneurs to develop soil

testing businesses in rural areas.

Section 4

Inclusive business implementation process

What common constraints and challenges are being faced? What phase of development are projects in – early

design or reaching significant scale? Have phases changed over the lifetime of BIF? This section looks at

• Project progress

• Project maturity

• Partnerships

• Common challenges and constraints

26

27

Assessment of project progress

Category Example project

Flourishing JITA already reaches some thousands of low – income people, turnover is in the hundreds of thousands,

and it is reaching break even ahead of schedule.

Progressing

well

After initial delay in the first season, Malawi Mangoes has now secured first round investment, the

processing plant is being completed, first mangoes will be harvested this year, and further expansion is

underway.

Progressing

slowly

One Family Health is planning to roll out Child and Family Wellness Clinics in Zambia. A great many

obstacles have had to be tackled along the way to get ready for implementation.

Stalled After exploring options for Tata Tannery’s sustainable leather sourcing initiative, it is not clear that the

feasibility and benefits of intervention are strong enough.

On ice Microventures plan to develop market linkages was cancelled after initial problems in the concept

coincided with a gap in staffing.

4 4

13

17

2

-

6

12

18

On ice Stalled / on hold Progressing slowly Progressing well Flourishing / securelyestablished

Project progress by BIF team assessment (N=40)

75% of

projects

The BIF team assessment is an assessment of the progress of the individual projects carried out in September 2013. It is a collaborative effort

between the Country Managers and the BIF core M&E team

25%

68%

7%

Project progress optimism level (N=27)

More optimisticorganisations

Organisationsassessment equal toBIF team's

More pessimisticorganisations

28

Data is only available for 27 projects out of 32 that have completed a progress report or project update

The ‘optimism level’ is the difference between the project

progress reported by the organisations themselves and the

progress that has been assessed by the BIF team

• For 68% of all organisations, the perception of the

progress of their project is in line with the assessment

made by the BIF team

• There is, however, a larger number or organisations that

are optimistic (25%) rather than pessimistic (7%) about

the progress of their project

• There is no visible pattern around the optimism level.

Optimism and pessimism is not driven by the business

model (core-IB vs diversifying-into-IB), nor by the project

progress or maturity (blueprint and design,

implementation etc…)

Assessment of project progress

Assessment of Project Maturity

29

Building on work done by Acumen and Monitor* we differentiate four different phases of development or maturity:

1. Blueprint and design

2. Early operation

3. Implementation

4. Moving to scale

It is important to bear in mind that in some cases the company itself may be well established, but the categorisation

applies to the specific inclusive business project that is supported.

We have assessed project maturity levels** at three milestones during the BIF pilot. At the first milestone in June 2012,

assessment was mainly driven by self categorisation of companies at baseline which explains the high share of projects

‘moving to scale’ in June 2012. When looking at the last two assessments (February and September 2013) we can see

an overall tendency of increasing maturity, and as of September 2013, the majority of projects (66%) are in the

operational phases.

5

22

11 Negative change

No change

Positive change

Project maturity change from February 2013

to September 2013 (N=38)

* Concept note entitled: “Building markets for impact at scale” a research proposal being part funded by DFID, April 2013.

** The assessment of the project’s maturity has been made by BIF’s central M&E team at the milestones: June 2012, February 2013

and September 2013

25%

41%

33%

37%

33%

20%

10%

2%

0% 20% 40% 60% 80% 100%

September 2013(N=40)

February 2013(N=41)

BIF project maturity index (N = various)

Blueprint and design Early operation and Validation

Implementation Moving to scale

Challenge / constraint to the

success of the Inclusive Business

Number of organisations

that identified this as a

challenge at Baseline

(N=40)

How this challenge

ranks in terms of

importance, out of

17 categories

Proportions of

organisations that

believe that BIF has

made an impact on this

challenge / constraint **

Need partnerships with government 12 3/17 44%

Need new or better partnerships

with others 10 7/17 60%

How important are partnerships to the inclusive

business? How has BIF helped?

• Partnerships can also be viewed as a significant obstacle to the success of the inclusive business. This is especially

true for partnerships with the government (this can be either the local or central government)

• Two of the companies that have indicated that BIF has improved their partnerships with the government are:

Universal (Malawi) and ERAS (Bangladesh)

45%

41%

14% High

Medium

Low

Impact that the collaboration with BIF has had

on new partnerships (N=22)*

* We were able to collect data from 22 organisations on this specific

benefit

• When carrying out the baseline assessment, businesses

were asked to rate their expectations on various benefits

that the collaboration with BIF could bring. The same

information was then collected at Progress Report to

understand the impact that BIF had in practice

• Out of 11 benefit categories, ‘New partnerships’ ranks 4th

in terms of BIF contribution, with 45% of businesses

saying that BIF had an impact higher than expected

** out of the organisations that were able to report on this indicator, this refers to the percentage of those that reported that BIF has made a

significant impact on the challenge

31

During our baseline assessment, companies were asked to indicate their top challenges from a drop down list (but could

also add other constraints not listed)

• A wide variety of challenges were identified

• In general, challenges do not seem to be dependent on the BOP focus of the projects but we can see some divergence:

• The policy and regulatory environment is a challenge almost exclusively identified by consumer focused projects

• Lack of infrastructure on the other hand has only been identified as a key challenge by producer focused projects

Common challenges and constraints identified at

baseline

2

2

1

7

5

4

6

6

5

5

4

4

2

4

8

8

1

2

3

2

4

5

5

6

6

8

8

5

6

- 5 10 15

Lack of development impacts

Insufficient internal company support or consensus

Not sure how to move from pilot to scale

Lack of demand/ lack of expertise and/or resources for marketing

Lack of infrastructure

Project development is taking too long/ long timeframe for payback

Too much effort to develop new ways of working

Lack of information about similar work elsewhere

Need new or better partnerships with others

Low return on investment

High risk project

Need to access finance that is appropriate to the nature of the project

Lack of skills within company (knowledge, awareness, expertise)

Policy and regulatory environment are restrictive

Need partnerships with government

Insufficient internal resources and finance

Lack of market information

Challenges of the Inclusive Business identified at Baseline, by BOP focus (N=40)

Producer Consumer

The producer project, JITA, has been merged with the rest of the producer projects in this diagram

32

Has BIF made

a difference?

28 companies have responded to the question “how do you now rate in terms of importance the top 10 challenges that were identified at

Baseline?”

In addition, these 28 companies were asked if BIF had had an impact on addressing this challenge since Baseline. “Has BIF made a

difference” refers to the percentage of respondents that have said “yes” to this question, out of the ones that had identified this challenge as

important at Baseline

At Progress Report, companies were

asked to update the importance of their

top challenges, and report if BIF had

made a difference to addressing it

The bars on the left show the

percentage of projects that have rated

the challenge as ‘high” (high indicates

challenge is still very relevant)

Challenges have been ordered by most

popular at baseline (the highest being

at the top)

• The policy and the regulatory

environment, and the risk of the

project are the two challenges that

are still the most relevant at Progress

Report

• BIF has had the strongest impact at

addressing the risk of the projects,

the lack of skills within the

company, the lack of market

information

• The low return on investment is the

challenge for which BIF’s support has

made the least difference

Evolution of top challenges over the lifetime of

BIF

14%

40%

33%

50%

43%

33%

57%

33%

30%

27%

0% 25% 50% 75%

Lack of information about similarwork elsewhere

Need new or better partnershipswith others

Low return on investment

High risk project

Need to access finance that isappropriate to the specific nature…

Lack of skills within company(knowledge, awareness, expertise)

Policy and regulatory environmentare restrictive

Need partnerships withgovernment

Insufficient internal resources andfinance

Lack of market information

Percentage of projects identifying the challenge as “high”

Top 10 challenges identified at baseline and % of

projects rating them ‘high’ at Progress Report (N=28)

73%

60%

44%

43%

83%

57%

67%

33%

60%

43%

Need to access finance that is

appropriate to the nature of the project

33

21 18

1

Producer

Consumer

Distributor

Portfolio breakdown by primary beneficiary type (N=40)

Summarising some key characteristics of the

portfolio of long projects

4

4

13

17

2 On ice

Stalled / on hold

Progressing slowly

Progressing well

Flourishing / securelyestablished

Portfolio breakdown by status of IB project in September

2013 (N=40)

25

14

1 Diversifying into IB

Core-IB

Other

Portfolio Breakdown of type of project (N=40)

34

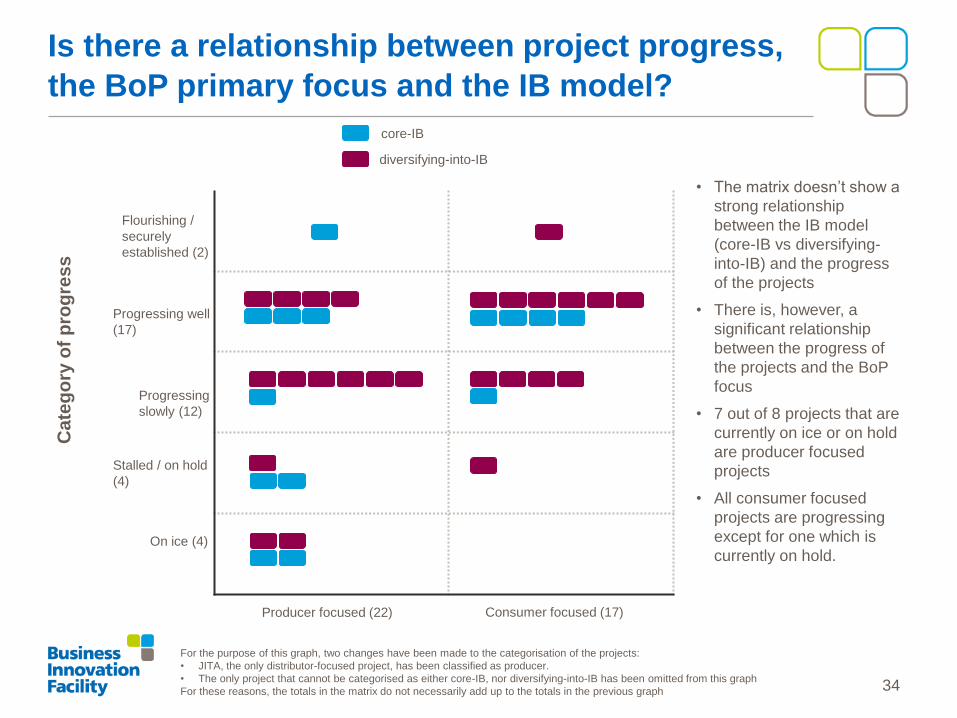

Is there a relationship between project progress,

the BoP primary focus and the IB model?

• The matrix doesn’t show a

strong relationship

between the IB model

(core-IB vs diversifying-

into-IB) and the progress

of the projects

• There is, however, a

significant relationship

between the progress of

the projects and the BoP

focus

• 7 out of 8 projects that are

currently on ice or on hold

are producer focused

projects

• All consumer focused

projects are progressing

except for one which is

currently on hold.

Producer focused (22) Consumer focused (17)

On ice (4)

Stalled / on hold

(4)

Progressing

slowly (12)

Progressing well

(17)

Flourishing /

securely

established (2)

core-IB

diversifying-into-IB

Ca

teg

ory

of

pro

gre

ss

For the purpose of this graph, two changes have been made to the categorisation of the projects:

• JITA, the only distributor-focused project, has been classified as producer.

• The only project that cannot be categorised as either core-IB, nor diversifying-into-IB has been omitted from this graph

For these reasons, the totals in the matrix do not necessarily add up to the totals in the previous graph

Section 5

35

Commercial results

In this section we look at

1. Commercial drivers of projects and to what extent companies feel they are on track to achieve them

2. Financial data: turnover figures collected from long projects

3. Types and levels of investment

4. Assessments of a project’s perceived likelihood to reach commercial viability

Commercial drivers

36

9

8

9

8

4

6

3

10

4

3

6

6

3

3

8

10

8

3

6

6

4

- 10 20 30

Increase profitability of your product/business, increase productivity, reduce costs

Get first mover advantage in an inclusivebusiness model

Access new markets (geographic markets,product markets, base of pyramid markets

etc)

Increase market share of your product/business

Increase/ guarantee security andsustainability of the supply chain

Develop competitive advantage anddifferentiation from competitors

Enhance brand identity/ value, customerappeal

Identified at baseline, but no update available

Identified at baseline, no signs of delivering

Identified at baseline, showing signs of delivering at progress report

Main commercial drivers for long projects identified at baseline, and

progress made (N=40)**

37

• 67.5% of long projects have

identified “Increasing

profitability” as one of their

main commercial drivers at

baseline

• So far, 44% of projects (8 out

of 18) are showing signs of

delivery for this driver *

• The drivers delivered most

successfully so far are

’accessing new markets’

and ‘Getting first mover

advantage’. For these, 70%

of projects are reporting signs

of delivery at progress report

* ‘showing signs of delivering at progress report’ are all projects that have reported that the driver has either been successfully delivered or

that is showing “signs of delivering”

** Only 28 projects have returned Progress Report forms with the progress of the commercial drivers, hence the large amount of drivers with

no update available

What are the most common commercial drivers?

Are projects on track to achieve them?

38

11

11

9

7

- 5 10 15 20

Get first mover advantage in aninclusive business model

Access new markets (geographicmarkets, product markets, base of

pyramid markets etc)

Increase profitability of your product/business, increase productivity, reduce

costs

Develop competitive advantage anddifferentiation from competitors

Four most popular commercial drivers for consumer

focused projects identified at Baseline (N=18)

Projects that identified the challenge at baseline

18

13

11

11

- 5 10 15 20

Increase profitability of your product/business, increase productivity,…

Increase/ guarantee security andsustainability of the supply chain

Get first mover advantage in aninclusive business model

Increase market share of your product/business

Four most popular commercial drivers for producer &

supplier focused projects identified at Baseline (N=21)

Projects that identified the challenge at baseline

• Increase of profitability / productivity of

the product and inclusive business has

been identified as important at Baseline by

85% (18 projects out of 21) of all producer

focused projects

• Consumer focused projects have identified

a wider range of drivers.

• Access to new markets and getting first

mover advantage are the two most

popular ones, with 61% of consumer

focused projects identifying them as

important at Baseline

Do commercial drivers differ between producer

and consumer focused projects?

Increase profitability of your product /

business, increase productivity,

reduce costs

39

88%

71%

50%

67%

69%

62%

0% 20% 40% 60% 80% 100%

Get first mover advantage in an inclusivebusiness model

Access new markets (geographic markets,product markets, base of pyramid markets etc)

Increase profitability of your product/ business,increase productivity, reduce costs

Develop competitive advantage anddifferentiation from competitors

Average for top 4 drivers

Average across all drivers

Consumer focused projects showing signs of delivering the top 4

drivers

40%

50%

50%

40%

45%

53%

0% 20% 40% 60% 80% 100%

Increase profitability of your product/ business,increase productivity, reduce costs

Increase/ guarantee security and sustainabilityof the supply chain

Get first mover advantage in an inclusivebusiness model

Increase market share of your product/business

Average for top 4 drivers

Average across all drivers

Producer & supplier focused projects showing signs of delivering the

top 4 drivers

Which commercial drivers are showing signs of

delivery at progress report?

• 45% of producer focused projects

and 69% of consumer focused

projects are showing signs of

delivering their four most important

drivers at progress report

• Producer focused projects are

therefore showing slower signs of

delivering their key drivers at

progress report

• For consumer projects, signs of

delivery are particularly strong for

‘getting first mover advantage in

an inclusive business model’, for

which 88% of projects are already

showing some signs of delivery at

progress report.

• ‘Increase profitability’ is the driver

of consumer focused projects

showing the slowest progress (50%)

Signs of delivering is the percentage of the projects that have reported to be either seeing initial signs of delivering the driver, or that have

already successfully delivered the driver

Financial data

40

41

The key questions that we are aiming to answer in this section are the following:

What was the financial performance of the projects at Year 0?

How is this performance expected to evolve during the first year?

Were estimates for year 1 in line with actuals?

What are the projections for the next 5 years?

Throughout our M&E data collection, organisations were asked at each M&E milestone to provide estimates and / or

actuals, where available, on their financial performance, and to project these up to 5 years into the future from the

moment that BIF’s intervention began (which we refer to as Year 0). This has allowed us to compare how the financial

performance that organisations have realised differs from what was previously estimated.

It has only been possible to carry out this type of analysis for a small sample of our long projects that have completed a

Progress Report or Project Update form and have also completed their first year of operations.

Most of our analysis in this section is focused on turnover, the indicator for which we have the most data available

Financial analysis

42

Turnover – what was the situation at year 0?

19

10

5 5

-

2

4

6

8

10

12

14

16

18

20

No turnover Smaller than $50k Between $50k and $1m Larger than $1m

Nu

mb

er

of

pro

jects

Turnover of large projects at Year 0 , including outliers (N=39)

The total turnover for the whole portfolio in year 0 is around $806,500,000

The data presented in this slide is the turnover of the inclusive business in year 0, and is a mix of estimated figures and actuals. It includes

all organisations, including outliers.

These figures are a mix of actuals and estimates. Estimated turnover figures are likely to be higher than reality because of the natural

optimism of some of the organisations

Some of the organisations included in this chart have not been able to differentiate the operations of their core business from the inclusive

business. These have been removed from later analysis (see following slide)

It is important to note that data on turnover is heavily skewed by three consumer focused projects (see graph below comparing these three projects with the remaining portfolio combined). In the subsequent analysis we have removed these outliers.

Normally we try to base financial analysis on the inclusive business venture only, however in some cases (particular for large companies) this is tricky:

• In one example, it was impossible to isolate the returns originating from sorghum based products (i.e. brewed products like beer) from the rest of the organisation. Given that the project aims to change the company’s overall sourcing strategy, this was the closest proxy that seemed appropriate at the time of baseline.

• Similarly, a large retailer was unable differentiate the inclusive business financial data from the whole organisation’s, and has reported financials that are not representative of the Inclusive Business.

• In addition, another organisation has also been removed from the aggregation analysis because of its large size – its turnover at year 0 of $6m is as large as the other 36 projects combined

Turnover – what are the data outliers?

43 * No data for one project, 39 projects have reported financial data at year 0

$6 million

$763 million

$32 million

$6 million

- 100 200 300 400 500 600 700 800

Remaining 36 projects(with available year 0 data)

Guinness

Agora

Cropserve

Turnover, $ million

Comparison of Turnover at baseline ($) of outliers vs the rest of the portfolio of large projects

Business #1

Business #2

Business #3

44

Turnover – turnover growth from year 0 to year 1,

actuals against estimates

Year 0

turnover

Year 1

estimated

turnover

Estimated

increase

Y0-Y1

Year 1

actual

turnover

Actual

increase

Y0-Y1

Total TO

($) 1,722,000 4,990,000 3,267,000 2,790,000 1,070,000

Average

TO ($) 96,000 277,000 180,500 155,000 59,500

• Actual turnover growth from year 0 to year 1 has been of 62%

• The estimated turnover growth from Year 0 to Year 1 was of

190%

• Turnover in year 1 has therefore grown 44% less than what

expected

Slower progress has been driven by two factors:

• A natural optimism – even where the business in progressing

well, passionate entrepreneurs were expecting faster

expansion than was possible in reality

• A slower project progress caused by unexpected obstacles /

constraints

Turnover estimates and actuals in year 0 and year 1 (N=18) 96,000

$155,000

$277,000

-

50,000

100,000

150,000

200,000

250,000

300,000

Year 0 Year 1

Growth in turnover per business, Year 0 to Year

1, estimated and actual, $ pa (N=18)

+190%

+62%

Year 1 actual turnover

Year 1 estimated turnover

- 44%

• The analysis excludes outliers and only includes those projects that have reported year 0 turnover figures, and both estimates AND actuals

for year 1.

• The sample used for this analysis is made of projects of different types and sizes and is fairly small (18 out of 40 projects). Although the

figures are not a fair representation of the full portfolio, the trend is likely to be applicable to the majority of the businesses in the portfolio.

• Data has been rounded to the closest thousand or 500

$70,500

$144,500

$256,000

Year 0 Year 1

$126,500

$168,000

$303,000

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Year 0 Year 1

Average turnover per project (N=18)

45

+140%

+33%

+261%

+104%

Turnover – how does estimated and actual growth

compare between different IB models?

-45%

Year 1 actual turnover

Year 1 estimated turnover

-44%

Core-IB [N=8] Diversifying-into-IB [N=10]

• The analysis excludes outliers and only includes those projects that have reported year 0 turnover figures, and both estimates AND actuals

for year 1.

• The sample used for this analysis is made of projects of different types and sizes and is fairly small (18 out of 40 projects). Although the

figures are not a fair representation of the full portfolio, the trend is likely to be applicable to the majority of the businesses in the portfolio.

• Data has been rounded to the closest thousand or 500

• Out of $260m of projected turnover in year 5, $200m is

expected to come from 5 particularly large projects

• Half of the inclusive businesses (13 out of 26) are

reporting projections for year 5 of less than $2m

46

Turnover – What are the future projections?

Year 0 Year 1 Year 2-3 Year 4-5

Number of projects

in sample 31 30 31 26

Total TO ($) 7,545,000 16,415,000 96,645,000 260,000,000

Average TO($) 243,000 547,000 3,118,000 10,020,000

Projects with TO>0 15 17 31 26

Average TO ($) 503,000 965,000 3,118,000 10,020,000

• Data on year 2 was used when estimates for year 3 were not available

• Data on year 4 was used when estimates for year 5 were not available

• Data has been rounded to the closest thousand or 500

$243,000 $547,000

$3,118,000

$10,020,000

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

Year 0(N=31)

Year 1(N=30)

Year 3(N=31)

Year 5(N=26)

$

Turnover projections, average per project, $ (N =

various)*

• The data in this slide is made of estimated turnover projections up to 5 years from the beginning of BIF support.

• As shown in the previous slide, estimated data is likely to be inflated by optimism. The sample used is also fairly small compared to the

overall portfolio. All figures should, as a consequence, be used as an indication. The overall trend of high growth is, however,

representative of most inclusive businesses

47

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Year 0 Year 1 Year 2/3Year 4/5

$

Range: up to $140,000

-

1

2

3

4

5

6

Year 0 Year 1 Year 2/3 Year 4/5

Millio

n $

Range: up to $6,000,000

-

10

20

30

40

50

60

70

80

90

Year 0 Year 1 Year 2/3 Year 4/5

Millio

n $

Range: up to $90,000,000

Turnover projections per project

The data in this slide is made of estimated turnover projections up to 5 years from the beginning of BIF support.

As shown in the previous slide, estimated data is likely to be inflated by optimism. The sample used is also fairly small compared to the

overall portfolio. All figures should, as a consequence, be used as an indication. The overall trend of high growth is, however,

representative of most inclusive businesses

48

What are the current and planned levels of

investment?

Total

Average per

project

Total investment to

date ($) 104,323,292 3,597,355

Total investment

planned ($) 70,798,500 2,441,328

Organisations were also asked about their preferred

way to obtain financing, and which financial vehicles

they were intending to use in the future

• Commercial debt is the preferred financial

vehicle out of the BIF projects

• A growing number of projects are looking to use

concessional debt and/or equity

7

5

12

5

-

2

4

6

8

10

12

14

No investment Between 0 and$500k

Between $500kand $5m

More than $5m

Total investment to date (mid 2013), (N=28)

10

5

9

5

-

2

4

6

8

10

12

No investment Between 0 and$500k

Between $500kand $5m

More than $5m

Planned investment over the next few years (as of mid

2013) (N=28)

Concessional debt is defined as: “lending extended by creditors at terms that are below market terms with the aim of achieving a certain

goal”, IMF, 2004

Levels of investment (N=28)

How likely is commercial

growth?

Some further commercial analysis

To assess the project’s likelihood of reaching commercial viability

49

50

0% 20% 40% 60% 80% 100%

Zambia

India

Bangladesh

Malawi

Nigeria

BIF Country Manager’s

assessment

Service Providers’

assessment

Organisations self-

assessment

Perception of likelihood to reach commercial

viability across different stakeholders

• Likelihood is generally high,

most scores are above 50%

• Businesses tend to be more

optimistic about the likelihood

of their own project to reach

commercial viability than

external parties, such as the

BIF Country Manager and the

technical assistance service

providers

• At present, Nigerian projects

have the highest reported

likelihood of reaching

commercial viability

• Zambian and Indian projects

on the other hand seem to be

the least likely to reach

commercial viability

As part of our M&E system we asked the key stakeholders involved in the long projects to rate their likelihood to reach

commercial viability within 2-3 years, on a scale from 0 to 100%

All assessments are based on latest available data, however, most of the feedback was received in June-September

2013. The graph below shows the average that the projects have scored in each country.

In addition to people’s assessments of commercial viability

likelihoods (see page 51), we have created our own index

to measure the commercial viability of the Inclusive

Business

We refer to it as the BIF Commercial Viability Index,

which is an index based on a range of six different

indicators:

1. Does the business have a business plan?

2. Has the project reached breakeven?

3. What is our assessment of the likelihood to reach

commercial viability?

4. Is there evidence of strong leadership?

5. Is it on track against identified targets?

6. Do they have access to external leverage?

As of Sept 2013, over half of the projects score medium.

The following pages explore how scores have changed over

the lifetime of BIF.

BIF Commercial Viability Index

51

12

22

6

0 5 10 15 20 25

High

Medium

Low

Project scoring BIF commercial viability index Sep 2013 (N=40)

# projects

Evolution of the commercial viability index over

the lifetime of BIF

52

* N = 39 , an additional project in Nigeria was added to the

portfolio in June 2013

The assessment over time does not show any significant changes. When comparing scores between February 2013 and

September 2013, we can see that the majority of projects has remained in the same overall category, roughly a quarter has

gone down and a fifth of projects score higher than before

Change in scores

(Feb 2013 to Sept

2013)

# projects %

Higher 8 21

Same 21 53

Lower 10 26

6

8

6

22

17

21

12

16

6

0% 20% 40% 60% 80% 100%

September (2013)

February (2013)

June (2012)

Low Medium High

Commercial viability index June 2012 (N=30), February

2013 (N=41) and September 2013 (N=40) Change in Commercial Viability Index (N = 39) *

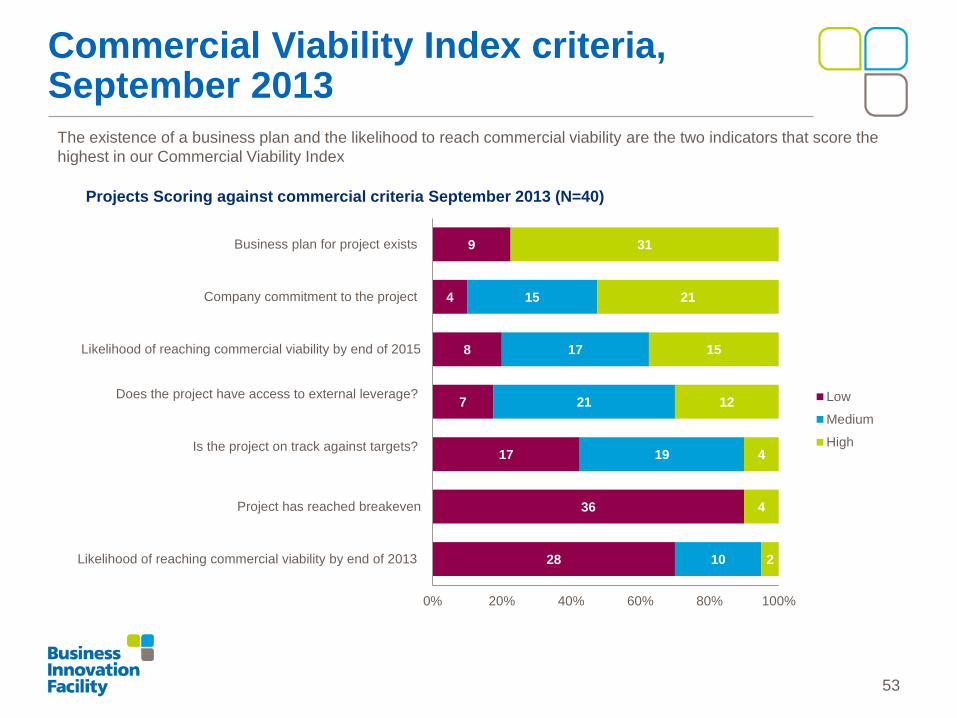

Commercial Viability Index criteria, September 2013

53

The existence of a business plan and the likelihood to reach commercial viability are the two indicators that score the

highest in our Commercial Viability Index

28

36

17

7

8

4

9

10

19

21

17

15

2

4

4

12

15

21

31

0% 20% 40% 60% 80% 100%

Likelihood of reaching commercial viability by end of 2013

Project has reached breakeven

Is the project on track against targets?

Does the project have access to external leverage?

Likelihood of reaching commercial viability by end of 2015

Company commitment to the project

Business plan for project exists

Projects Scoring against commercial criteria September 2013 (N=40)

Low

Medium

High

Commercial criteria comparison over time

54

% of high scoring projects

2

6

7

4

4

5

4

13

11

12

15

15

15

11

12

21

27

23

31

22

16

0 5 10 15 20 25 30 35

Sep-13

Feb-13

Jun-12

Sep-13

Feb-13

Jun-12

Sep-13

Feb-13

Jun-12

Sep-13

Feb-13

Jun-12

Sep-13

Feb-13

Jun-12

Sep-13

Feb-13

Jun-12

Sep-13

Feb-13

Jun-12

Lik

elih

oo

d o

fre

ach

ing

com

me

rcia

lvia

bili

tyb

y e

nd

of 2

013

Pro

ject

has

reach

ed

bre

ake

ve

n

Is t

he

pro

ject

on t

rack

aga

inst

targ

ets

?

Do

es

the

pro

ject

have

acce

ss

toe

xte

rna

lle

ve

rag

e?

Lik

elih

oo

d o

fre

ach

ing

com

me

rcia

lvia

bili

tyb

y e

nd

of 2

015

Co

mpa

ny

com

mit

me

nt

toth

ep

roje

ct

Bu

sin

es

s p

lan

for

pro

ject

exis

ts

Projects scoring against commercial criteria June 2012 (N=30), February 2013 (N=41) and September 2013 (N=40)

Likelihood of reaching

commercial viability by

end of 2013

Project has reached

breakeven

Is the project on track

against targets?

Does the project have

access to external

leverage?

Likelihood of reaching

commercial viability by

end of 2015

Company commitment to

the project

Business plan for project

exists

• At the latest available assessment

(September 2013), there is a growing

proportion of projects that score high

on having a business plan in place

• All other indicators have not

experienced a substantial change in

the proportion of projects scoring

‘high’

Section 6

Development impacts

In this section we look at

1. Households reached at the BoP: figures collected from long projects

2. Assessments of a project’s perceived likelihood to going to scale, reaching thousands of households at the

BoP

55

The key questions that we are analysing in this section are the following:

• What was the BoP reach of the projects at Year 0?

• Were estimates for year 1 in line with actuals?

• What are the projections for the next 5 years?

• How can we calculate realistic projections, given that estimates tend to be inflated by optimism?

Our analysis

Similar to the way the financial data was collected, organisations were asked to provide either estimates or actuals on their

BoP reach, and to project these up to 5 years into the future from the moment that BIF’s intervention began (which we

refer to as Year 0). This has then allowed us to compare how the BoP reach that has been realised differs from the initial

estimates.

Our approach to measuring BoP reach

The inclusive business projects do not have one single type of development impact. As part of our results measurement

approach in BIF we look at:

• Reach to Base of Pyramid (BOP) – the number of low income people reached. In this regard, it is important to

distinguish between low-income producers and entrepreneurs (who gain livelihoods and income) and low-income

consumers (who gain access to goods and services). Inclusive businesses tend to reach many more consumers than

producers, so these totals cannot just be summed together.

• The significance of the project to a low-income person, not just total numbers matters, though is subjective.

• Estimating growth in BOP reach is important. But difficult, as projects are at different stages, a few have large

numbers, and not all have estimates. Figures are unreliable and comparisons worse.

• Other development results are also considered, particularly likelihood of replication, of systemic impact,

Understanding development results

56

57

What was the expected BoP reach in year 0?

9

6

2 1

2

9

1

3

1

3

1

-

2

4

6

8

10

12

14

16

18

0 >0, <=500 >500, <=2,000 >2,000, <=10,000 >10,000

# p

roje

cts

Households reached

Distributor Consumer Producer

BoP households reach for year 0 reported during baseline assessment, by primary BoP focus (N=38)

• At Baseline, 18 out of 38 projects* estimated that no BoP households would be reached in year 0

• Five projects expected to reach more than 10,000 households in year 0. Of these, two had a producer focus

• In our analysis we are only looking at primary BoP reach

*It has not been possible to collect any BoP data for two projects

This slide looks at the BOP reach of the projects in year 0. Some projects have reported actual figures for year 0, while some others have

estimated their BOP reach. Results should therefore be taken as an indication of the overall reach as estimates are likely to be driven by optimism

and are too high as a consequence

178

546

1,189

-

200

400

600

800

1,000

1,200

1,400

Year 0 Year 1

Ho

useh

old

s

620 1,092

6,080

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Year 0 Year 1

Ho

useh

old

s

Year 1 actual turnover

Year 1 estimated turnover

+570%

+207%

+881%

+76%

Producer focused projects (N=7) Consumer focused projects (N=5)

58

Growth of BoP reach from year 0 to year 1, actuals

vs estimates

-54% -82%

The analysis excludes outliers and only includes those projects that have reported year 0 BoP reach figures, and both estimates AND

actuals for year 1.

The sample used for this analysis is made of projects of different types and sizes and is fairly small (18 out of 40 projects). Although the

figures are not a fair representation of the full portfolio, the trend is likely to be applicable to the majority of the businesses in the portfolio.

• Producer-focused businesses tend to have a faster rate of growth and are less divergent from their estimates

than the consumer-focused ones

• Consumer-focused projects, however, have a higher overall BoP reach. When looking at projections up to 5

years in the future, we expect consumer-focused businesses to reach roughly 100 times as many households

per business as producer-focused businesses (see page 60)

59

BOP reach projections – average per project

2,310 3,346

216,911

466,440

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

Year 0 Year 1 Year 2/3Year 4/5

Ho

useh

old

s

Average BOP reach per project,

consumer focused projects (N=10)

193

496

1,395

2,059

-

500

1,000

1,500

2,000

2,500

Year 0 Year 1 Year 2/3 Year 4/5

Ho

useh

old

s

Average BOP reach per project,

producer focused projects (N=8)

The data in this slide is made of estimated BoP reach projections up to 5 years from the beginning of BIF support.

As seen in the previous slide, data is likely to be inflated by optimism, and the sample used is fairly small compared to the overall portfolio.

All figures should, as a consequence, be used as an indication. The overall trend of high growth is, however, representative of most

inclusive businesses

Estimates for future BoP reach, revised for

realism

60

As seen previously (see page 59), organisations tend to overestimate their BOP reach projections. In order to

estimate total reach to the BoP across the portfolio, we have aggregated estimates from companies and scaled them

down by two different weights based on:

1. Actual project progress so far (see page 27)

Year 3 and 5 calculations:

Because some projects have provided actual figures for year 1 and projected estimates for year 3 and 5, we have

unpacked year 3 and year 5 BoP projections in an actual and an estimated component, weighing down only the

estimated component (a more detailed explanation can be seen in an example in the next page)

Optimism Weight

Optimism factor 70%

Project progress Weight

5. Flourishing/securely established 100%

4. Progressing well 75%

3. Progressing slowly 50%

2. Stalled/on hold 10%

1. On ice 0%

2. Our assessment of general over-optimism

within the portfolio

Example – BoP reach revised for realism

61

Optimism weight 70%

Project Progress: Progressing well weight 75%

Year 0 -

latest

Actual /

estimate Year 1

Actual /

estimate Year 2

Actual /

estimate Year 3 Year 4 Year 5

2,100 Actual 2,900 Actual 21,403 Actual 2 120,708 157,548 223,286

Revised for realism BoP reach

Year 1 Year 3 Year 5

Actual component

Year 1 actual 2,900 2,900 2,900

Estimated component

Estimated increase from year 1 (year x - year 1) 0 117,808 220,386

Adjusted for optimism (70%) 0 82,466 154,270

Adjusted for Progress (75%) 0 61,849 115,703

TOTAL reach 2,900 64,749 118,603

62

BoP reach across the whole portfolio,

revised for realism

Notes

• All figures have been rounded to the closest thousand

• 8 projects (20% of total) are either on ice or stalled – these have been excluded from our aggregation as it is assumed that they will not

progress and not realise any of their BOP reach

• Year 3 and 4 / 5 data is not available for 12 businesses. For these 12 businesses our assessment of current progress is on average slower

than for the 20 for which data is available. To estimate the BoP reach for all 32, the total for the 20 has been multiplied by a factor of 40% (to

reflect the slower increase that we are expecting).

Our ‘revised for realism’ projections for year 4 / 5 are about one third of what the companies estimated: from 5,706,000

households reported by the businesses to 2,631,000 once revised for realism (for twenty projects)

The portfolio is reaching at least 80,000 households at the BOP at the end of Year 1, post BIF support.

The portfolio is likely to be reaching around 1.2 million households by Year 3 and perhaps 3.7 million by Year 5.

Realistic BOP reach (totals and

averages across the portfolio)

Year 1 (actuals)

N = 16

Year 1 (estimates

and actuals)

N = 29

Year 3

N = 20

Year 4 / 5

N = 20

Total Average Total Average Total Average Total Average

Figures provided by organisations

(households) 21,000 1,200 228,500 7,900 2,088,000 104,000 5,706,000 285,000

Adjusted for progress and

optimism (households) 21,000 1,200 119,000 4,000 839,000 42,000 2,631,000 131,500

Estimated BOP household reach for all 32 projects progressing** 1,175,000 37,000 3,680,000 115,000

Estimated BOP individuals reached across the 32 projects

progressing*** 5,880,000 184,000 18,400,000 575,000

Moving beyond the numbers…

Some further analysis of development impacts

63

64

0% 20% 40% 60% 80% 100%

Zambia

India

Bangladesh

Malawi

Nigeria

BIF Country Managers’

assessment Service Providers’

Assessment

Recipient Organisations self-

assessment

Perception of likelihood of going to scale, reaching

thousands of BoP households across different stakeholders

• Likelihood is generally high,

most scores are above 50%

• Recipient organisations are

substantially more optimistic

than service providers and

country managers

• BIF Country Managers have

only rated projects an average

of 54% across the BIF portfolio

• Discrepancy between the

perceived likelihood of the

recipient organisations and the

BIF in-country team is

particularly strong in India and

Zambia

• Nigerian projects seem to be the

most likely to be reaching

thousands of low income people

As part of our M&E system we asked the key stakeholders involved in the long projects to rate, on a scale from 0 to

100% , the likelihood to go to scale reaching thousands of BoP households within 2-3 years

All assessments are based on latest available data, however, most of the feedback was received in June-September

2013. The graph below shows the average that the projects have scored in each country.

I addition, to people’s assessments of scale likelihoods,

we have created our own index to measure the

development impacts. We refer to it as BIF Development

Index, a weighted aggregation of the following indicators:

1. Primary beneficiaries reached

2. Likelihood of reaching significant scale by end of 2015

3. Does the project have potential for game changing

scale by year 3

4. Significance per person BOP

5. Systemic Impacts (significance and likelihood of the

projects' influence)

As of Sept 2013, over half of the projects score medium.

The following pages explore how scores have changed

over the lifetime of BIF.

Development Index Sept 2013

65

# projects

7

22

11

0 5 10 15 20 25

High

Medium

Low

Project scoring BIF development index Sep 2013 (N=40)

Evolution of the Development Index over the lifetime of BIF

66

Change in

scores (Feb

2013 to Sept

2013)

# projects %

Higher 4 10

Same 25 64

Lower 10 26

More projects have been rated low in terms of

development index in September 2013 than in

February 2013.

10 projects have a decreased development index

compared to 7 months earlier, while 4 have improved

their rating

11

5

5

22

29

24

7

7

4

0% 20% 40% 60% 80% 100%

September (2013)

February (2013)

June (2012)

Low Medium High

Project scoring BIF development index June 2012

(N=33) , February 2013 (N=41) and September 2013

(N=40)

* N = 39 , Best Foods (Nigeria) was added to the portfolio in

June 2013