Retooling For Growth in a Dynamic Market · Retooling For Growth in a Dynamic Market ......

29

Retooling For Growth in a Dynamic Market CAR MANAGEMENT BRIEFING SEMINARS August 1, 2017 Mike Jackson Executive Director, Strategy and Research Original Equipment Suppliers Association [email protected] +1-248-430-5954

Transcript of Retooling For Growth in a Dynamic Market · Retooling For Growth in a Dynamic Market ......

Retooling For Growthin a Dynamic MarketCAR MANAGEMENT BRIEFING SEMINARS

August 1, 2017

Mike Jackson

Executive Director, Strategy and Research

Original Equipment Suppliers Association

+1-248-430-5954

2Retooling for Growth in a Dynamic Market

Championing the business interests of the automotive

OE supplier community:Founded in 1998, the Original Equipment Suppliers Association (OESA), serves as

the voice of the automotive supplier and a valuable resource for member

organizations. Throughout the supply chain and on legislative and regulatory issues,

OESA represents the collective voice of suppliers.

Exclusively for automotive suppliers: Supplier membership is exclusive to original equipment automotive suppliers that

directly provide components, tools, materials and services to the OE light vehicle

industry.

Strength in numbers: Membership is comprised of approximately 375 Tier 1,2, and 3 automotive suppliers

with North American OE sales that range from $10 million to $5+ billion. Affiliate

members support the supplier community with thought leadership, industry analysis

and other key information.

LED By supplier industry executives: OESA’s interests are guided by a board of directors consisting of CEOs from

member companies of all sizes.

Staff that works for members: Members enjoy direct access to a staff of dedicated association employees in

Detroit and Washington, D.C.

Retooling for Growth in a Dynamic Market

4

• Vehicle Sales Dynamics

• Production Outlook

• Supplier Implications

• Summary

AGENDA

Retooling for Growth in a Dynamic Market

4

6

8

10

12

14

16

18

20

22

199

6

199

8

200

0

200

2

200

4

200

6

200

8

201

0

201

2

201

4

201

6

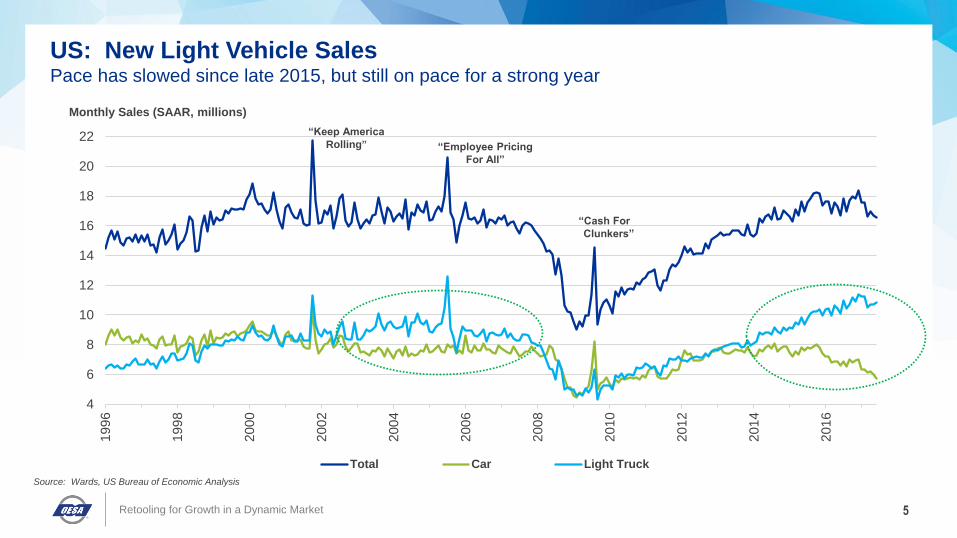

Total Car Light Truck

5

“Keep America

Rolling” “Employee Pricing

For All”

“Cash For

Clunkers”

Monthly Sales (SAAR, millions)

Source: Wards, US Bureau of Economic Analysis

US: New Light Vehicle SalesPace has slowed since late 2015, but still on pace for a strong year

Retooling for Growth in a Dynamic Market

US Light Vehicle Incentives and Inventory

6

2.0

2.5

3.0

3.5

4.0

4.5

-50%

-25%

0%

25%

50%

Mill

ions

Y/Y (%) US InventorySource: Automotive News Data Center, Autodata

Vehicle Inventory (millions)

$2.0

$3.0

$4.0

-25%

-15%

-5%

5%

15%

25%

Thou

sa

nd

s

Y/Y (%) US Incentive/Unit

Vehicle Incentive Spending (thousands)

Retooling for Growth in a Dynamic Market

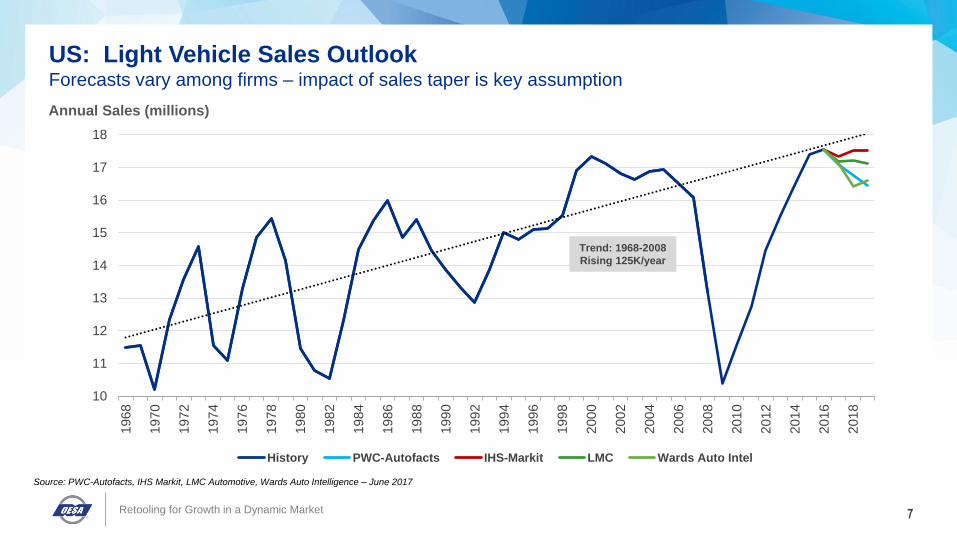

US: Light Vehicle Sales OutlookForecasts vary among firms – impact of sales taper is key assumption

Annual Sales (millions)

10

11

12

13

14

15

16

17

181

96

8

197

0

197

2

197

4

197

6

197

8

198

0

198

2

198

4

198

6

198

8

199

0

199

2

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

201

0

201

2

201

4

201

6

201

8

History PWC-Autofacts IHS-Markit LMC Wards Auto Intel

Trend: 1968-2008

Rising 125K/year

7

Source: PWC-Autofacts, IHS Markit, LMC Automotive, Wards Auto Intelligence – June 2017

Retooling for Growth in a Dynamic Market

8

14%

16%

18%

20%

22%

24%

26%

2010 2011 2012 2013 2014 2015 2016 2017

Lease Share Fleet Share

Lease and Fleet Share of New LV Registrations

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1996 2000 2004 2008 2012 2016

Lease Originations (millions)

Source: Cox Automotive, IHS Markit, Manheim Consulting

Lease and Fleet ShareRetail Slowing, Industry Reverting to Bad Habits? Current Strength Borrows from Tomorrow

Retooling for Growth in a Dynamic Market

9

90

95

100

105

110

115

120

125

130

199

5

199

7

199

9

200

1

200

3

200

5

200

7

200

9

201

1

201

3

201

5

201

7

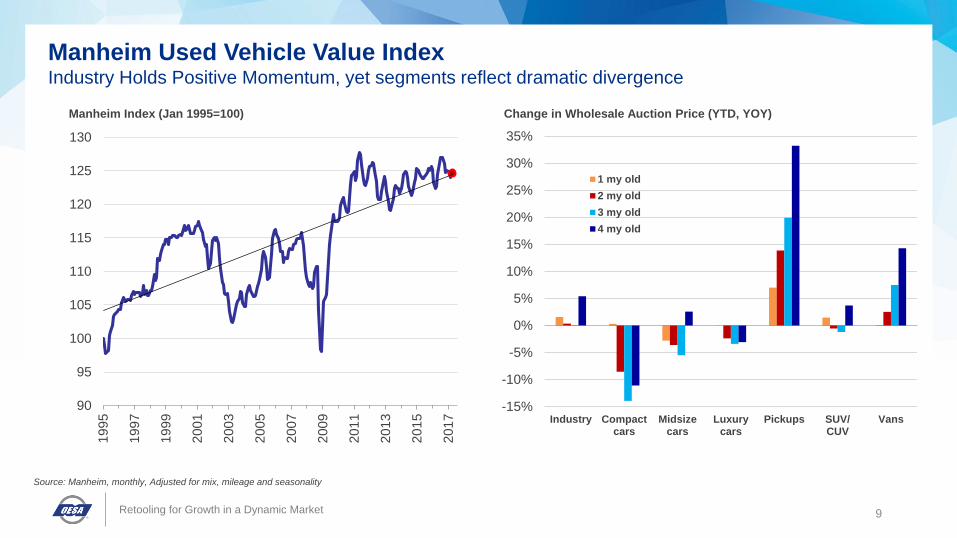

Manheim Index (Jan 1995=100)

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Industry Compactcars

Midsizecars

Luxurycars

Pickups SUV/CUV

Vans

1 my old

2 my old

3 my old

4 my old

Change in Wholesale Auction Price (YTD, YOY)

Manheim Used Vehicle Value IndexIndustry Holds Positive Momentum, yet segments reflect dramatic divergence

Source: Manheim, monthly, Adjusted for mix, mileage and seasonality

Retooling for Growth in a Dynamic Market

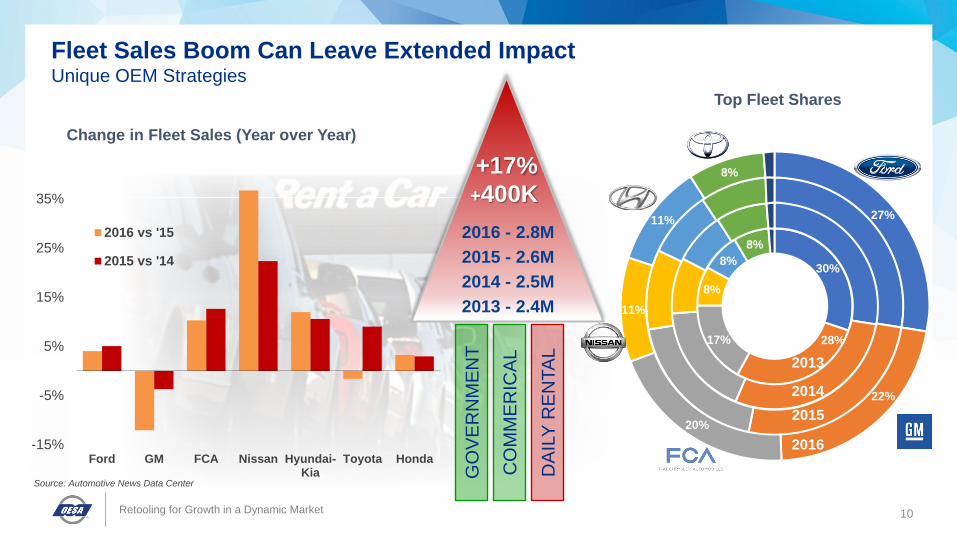

10

Source: Automotive News Data Center

Fleet Sales Boom Can Leave Extended ImpactUnique OEM Strategies

Change in Fleet Sales (Year over Year)

30%

28%17%

8%

8%

8%

27%

22%

20%

11%

11%

8%

Top Fleet Shares

2013

2014

2015

2016

2016 - 2.8M

2015 - 2.6M

2014 - 2.5M

2013 - 2.4M

+400K

+17%

GO

VE

RN

ME

NT

CO

MM

ER

ICA

L

DA

ILY

RE

NTA

L

-15%

-5%

5%

15%

25%

35%

Ford GM FCA Nissan Hyundai-Kia

Toyota Honda

2016 vs '15

2015 vs '14

Retooling for Growth in a Dynamic Market

US Light Vehicle Sales Outlook By Type

11

0

2

4

6

8

10

12

14

16

18

20

2005 2010 2015 2020

Mill

ions

Car

Utility

Truck

-5%(865K)

No Change

(6K)

+16%1,180K

-30%(2,039K)

2016 - ∆ 2024

Source: Wards Auto Intelligence

17.516.6

Retooling for Growth in a Dynamic Market

12

• Vehicle Sales Dynamics

• Production Outlook

• Supplier Implications

• Summary

AGENDA

Retooling for Growth in a Dynamic Market

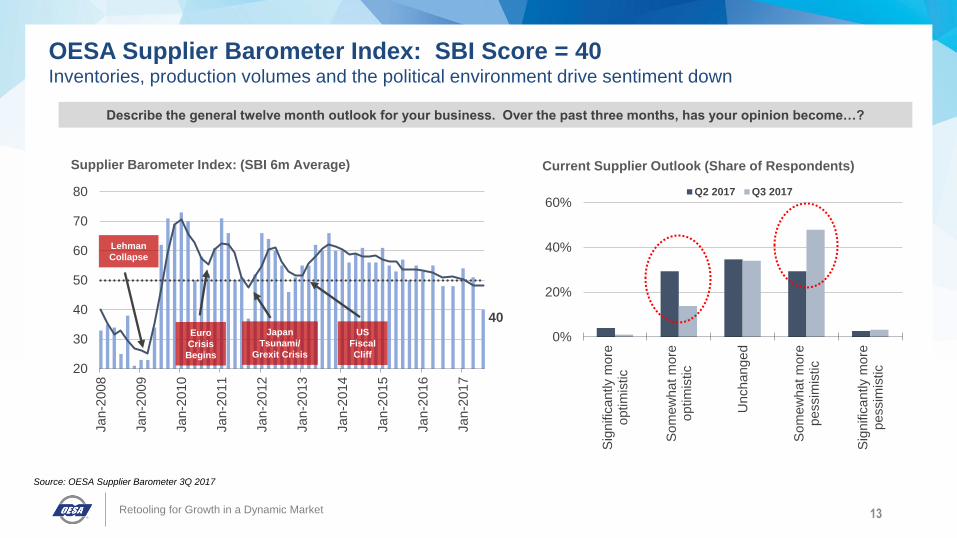

OESA Automotive Supplier Barometer- July 2017

20

30

40

50

60

70

80

Ja

n-2

008

Ja

n-2

009

Ja

n-2

010

Ja

n-2

011

Ja

n-2

012

Ja

n-2

013

Ja

n-2

014

Ja

n-2

015

Ja

n-2

016

Ja

n-2

017

13

Supplier Barometer Index: (SBI 6m Average)

Describe the general twelve month outlook for your business. Over the past three months, has your opinion become…?

OESA Supplier Barometer Index: SBI Score = 40Inventories, production volumes and the political environment drive sentiment down

Euro

Crisis

Begins

Japan

Tsunami/

Grexit Crisis

US

Fiscal

Cliff

Lehman

Collapse

40

0%

20%

40%

60%

Sig

nific

an

tly m

ore

optim

istic

So

mew

ha

t m

ore

op

tim

istic

Un

ch

ang

ed

So

mew

ha

t m

ore

pessim

istic

Sig

nific

an

tly m

ore

pessim

istic

Q2 2017 Q3 2017

Current Supplier Outlook (Share of Respondents)

Source: OESA Supplier Barometer 3Q 2017

Retooling for Growth in a Dynamic Market

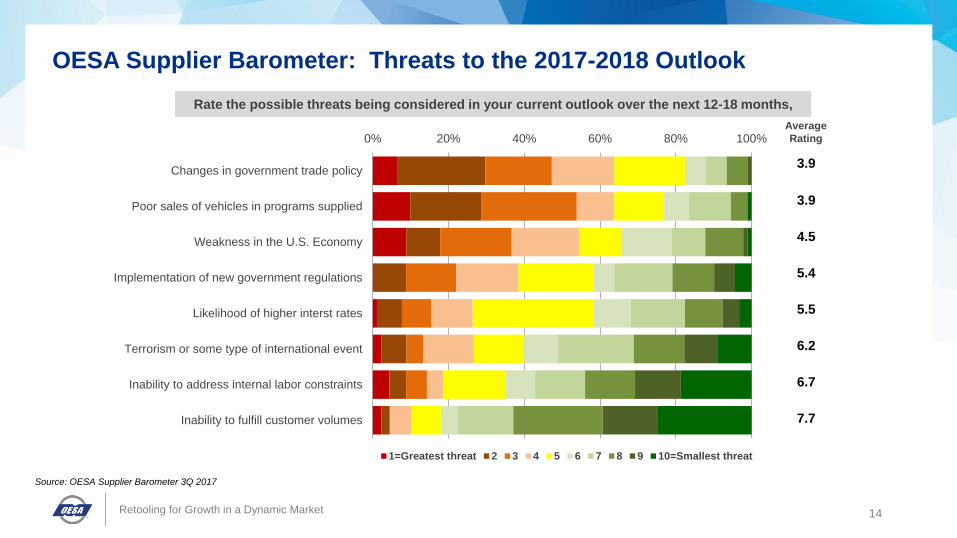

OESA Automotive Supplier Barometer- July 2017

0% 20% 40% 60% 80% 100%

Changes in government trade policy

Poor sales of vehicles in programs supplied

Weakness in the U.S. Economy

Implementation of new government regulations

Likelihood of higher interst rates

Terrorism or some type of international event

Inability to address internal labor constraints

Inability to fulfill customer volumes

1=Greatest threat 2 3 4 5 6 7 8 9 10=Smallest threat

14

Rate the possible threats being considered in your current outlook over the next 12-18 months,

Average

Rating

3.9

3.9

4.5

5.4

5.5

6.2

6.7

7.7

OESA Supplier Barometer: Threats to the 2017-2018 Outlook

Source: OESA Supplier Barometer 3Q 2017

Retooling for Growth in a Dynamic Market

15

(in millions)

20172018

Forecast

2019

Forecast1Q

Actual

2Q

Forecast

3Q

Forecast

4Q

Forecast

2017

Forecast

4.474.49

↓0.06

4.21

↓0.06

4.30

↓0.12

17.47

↓0.29

17.97

↓0.22

18.65

↓0.27

4.534.53

↓0.08

4.20

↑0.02

4.29

↑0.06

17.56

Δ0

17.72

↓0.19

17.90

↓0.27

4.564.54

↓0.18

4.24

↓0.04

4.44

↓0.01

17.78

↓0.21

17.88

↓0.46

18.02

↓0.42

Forecast Average 4.52 4.52 4.22 4.34 17.60 17.86 18.19

Forecast Spread 0.05 0.04 0.15 0.31 0.25 0.75

2016 Average 4.47 4.61 4.39 4.34 17.81

Source: OESA Forecast Snapshot – June 2017

Retooling for Growth in a Dynamic Market

NORTH AMERICA2017-2019 Production Forecast Comparison(VOLUMES REPRESENT NA CAR, LT TRUCK CLASS 1-5)

North America – Industry Production Cycles

16

0

2

4

6

8

10

12

14

16

18

20

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Mill

ions

NA Production

Recession

Linear (NA Production)

-26%-3.8M

-42%-6.4M

-19%-2.6M

-10%-1.7M

-48%-7.8M

Source: Wards Auto Intelligence

Stress

testing

-10%?

-20%?

-30%?

?-2.2%-385K

Retooling for Growth in a Dynamic Market

North American ProductionDemand Drives Divergent Growth

17

6.54.0

6.9 6.0

5.1

2.7

7.2 8.5

4.1

1.8

3.8 3.5

0

3

6

9

12

15

18

21

2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

Milli

on

s

Car Utilities Truck

-271K

-7%

+1.3M

+19%

-878K

-13%

Source: IHS Markit

Retooling for Growth in a Dynamic Market

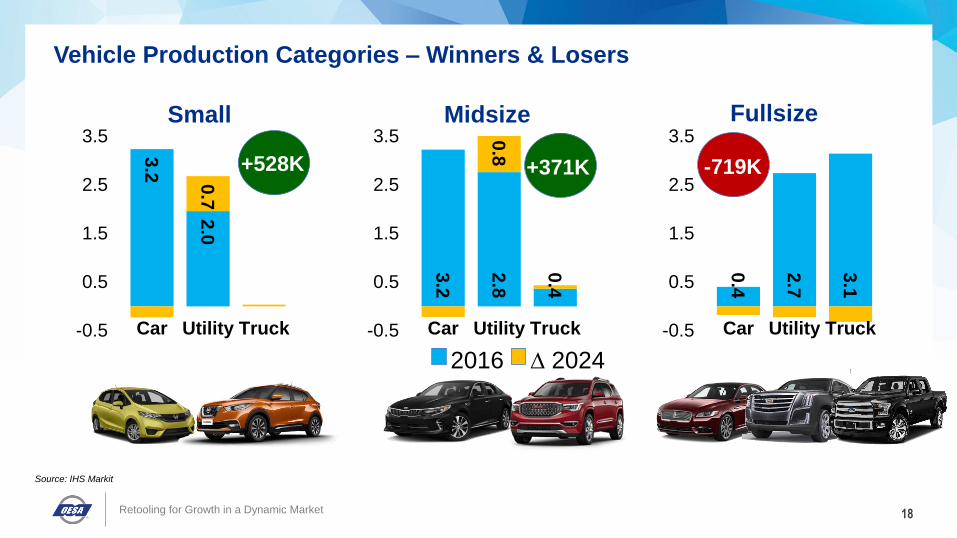

3.2

2.8

0.4

0.8

-0.5

0.5

1.5

2.5

3.5

Car Utility Truck

Vehicle Production Categories – Winners & Losers

18

3.2

2.0

0.7

-0.5

0.5

1.5

2.5

3.5

Car Utility Truck

0.4

2.7

3.1

-0.5

0.5

1.5

2.5

3.5

Car Utility Truck

Small Midsize Fullsize

+528K +371K -719K

Source: IHS Markit

2016 ∆ 2024

Retooling for Growth in a Dynamic Market

19

• Vehicle Sales Dynamics

• Production Outlook

• Supplier Implications

• Summary

AGENDA

Retooling for Growth in a Dynamic Market

Future Launch Activity

20

19 1925

16

34

19 20 24

1017

12 148 9

25

33

29

13

1620

0

10

20

30

40

50VehiclesCarsTrucks

Source: IHS Markit, Kelly Blue Book

Average Transaction Price

By Segment ($) – June 2017

0 10 20 30 40

B-Segment

C-Segment

D-Segment

Thousands

Utility

Car

+46%

+39%

+51%

Retooling for Growth in a Dynamic Market

Priorities & Positioning for Profitability

21

$17,250 profit/unit

.24 Million units sold - 2016

$4.1 Billion

~$10,000 profit/unit

2.28 Million units sold - 2016

$22.8 Billion

Retooling for Growth in a Dynamic Market

MARGIN MARKET

COMPETENCY SCALE

Production Portfolio Comparison - 2016

22

OEM Units Car SUV Truck

General Motors 3,647 32% 34% 34%

Ford 3,068 25% 36% 39%

FCA 2,516 13% 61% 27%

Toyota 2,125 47% 36% 17%

Honda 1,957 47% 51% 2%

Renault-Nissan 1,846 56% 28% 16%

Hyundai 859 66% 34% 0%

BMW 411 0% 100% 0%

Daimler 354 20% 69% 11%

Volkswagen 517 98% 2% 0%

Other 524 95% 5% 0%

Unit volume - 6,866 7,130 3,829

NA average 17,825 39% 40% 21%

$

Source: IHS Markit

Retooling for Growth in a Dynamic Market

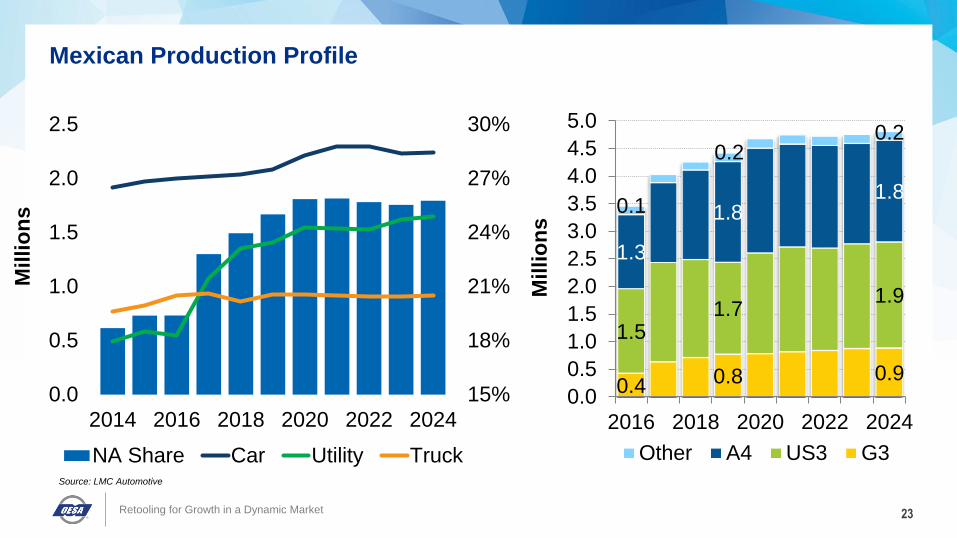

Mexican Production Profile

23

15%

18%

21%

24%

27%

30%

0.0

0.5

1.0

1.5

2.0

2.5

2014 2016 2018 2020 2022 2024

Milli

on

s

NA Share Car Utility Truck

0.4 0.8 0.9

1.51.7

1.9

1.3

1.81.8

0.1

0.20.2

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2016 2018 2020 2022 2024

Milli

on

s

Other A4 US3 G3Source: LMC Automotive

Retooling for Growth in a Dynamic Market

Passenger Cars: Under PressureSteady March To Reduce US3 Car Portfolios and Utilize Global Sourcing

24

Fiesta

Dart Focus

200

Sonic

Taurus

Verano

LaCrosse? Impala? CT6?

Volt? Cruze?

Segment

A/B

C

D

E

Retooling for Growth in a Dynamic Market

Top Automotive States

25

0 50 100

VirginiaIowa

MissouriWisconsinNew York

GeorgiaPennsylvania

CaliforniaTexas

South CarolinaNorth Carolina

IllinoisAlabama

KentuckyTennessee

IndianaOhio

Michigan

Top 20 - Supplier Employment (000s) US Vehicle Output - 2016 (Millions)

5%6%

49%8%

32%

Regional Share %

Source: 2017 MEMA Economic Study – 2015CY ; Share of total direct employment Source: LMC Automotive, OESA Analysis

0 1 2

California

Kansas

Georgia

South Carolina

Mississippi

Texas

Illinois

Missouri

Tennessee

Alabama

Kentucky

Indiana

Ohio

Michigan

5%1%

Midwest, 56%

S-East, 38%

Regional Share %

Retooling for Growth in a Dynamic Market

CAR TRUCK

• ENGINEERS

• TECHNICIANS

• HOURLY SKILLED26

OESA Supplier Barometer Survey: HR & Talent Focus

SKILLS +

CULTURE

GAP

63%MODERATE

TO WIDE

NEW

VALUES:

TIME

FLEXIBILITY

TALENT

SCARCITY

CHANGE ROLESTO FIT SKILLS

Retooling for Growth in a Dynamic Market

CROSS

FUNCTIONAL

TRAINING

APPRENTICESHIPS

NEW HIRING

PRACTICES

∆ SKILL SETS

•SPECIALIZED

•AUTONOMOUS

•COLLABORATIVE

ACTION PLANS:

27

• Vehicle Sales Dynamics

• Production Outlook

• Supplier Implications

• Summary

AGENDA

Retooling for Growth in a Dynamic Market

Summary

28

• Market: US demand slowing, divergent performance

• Strategy: Cycle requires dramatic reboot, ‘engaged’ planning

• Offense: SUV growth/Truck peak—bring opportunities and risks

• Defense: Growing scope of passenger car dislocation, turbulence

• Flexibility: Liquidity is key; vital to balance ‘Core’ vs Emerging

• Stretch: Build on strong foundation, adapt to grow – reach higher

Retooling for Growth in a Dynamic Market

Thank You...CAR MANAGEMENT BRIEFING SEMINARS

August 1, 2017

FOR QUESTIONS OR ASSISTANCE,

PLEASE FEEL FREE CONTACT ME:

Mike Jackson

Executive Director, Strategy and Research

Original Equipment Suppliers Association

+1-248-430-5954