Refining An Overview - Pakistan Credit Rating … · 2014-12-31 · Refining –An Overview October...

37

Refining – An Overview October 2014 Petroleum Industry: Technical Jargons Crude Oil Shale Oil International Refining Trends Lube Base Oil (LBO) Domestic Oil Dynamics Domestic Refineries Outlook

Transcript of Refining An Overview - Pakistan Credit Rating … · 2014-12-31 · Refining –An Overview October...

Refining – An Overview

October 2014

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Petroleum Industry – Technical Jargons

Upstream - It involves the exploration for and extraction of petroleum crude

oil and natural gas. The upstream oil sector is also known as the exploration and production

(E&P) sector.

Midstream - The midstream involves storing, marketing and transporting petroleum

crude oil, natural gas. Midstream operations are sometimes included in the downstream category.

Downstream - The downstream sector includes petroleum refineries, petroleum

product distribution, retail outlets and natural gas distribution companies.

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Crude Oil

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Largest Consumer

USA - 801 mln tonnes

China - 507 mln tonnes

Largest Producer

Saudi Arabia - 542 mln tonnes

Russia - 531 mln tonnes

Largest Reserves

Venezuela - 46,576 mln tonnes

Saudi Arabia - 36,518 mln tonnes

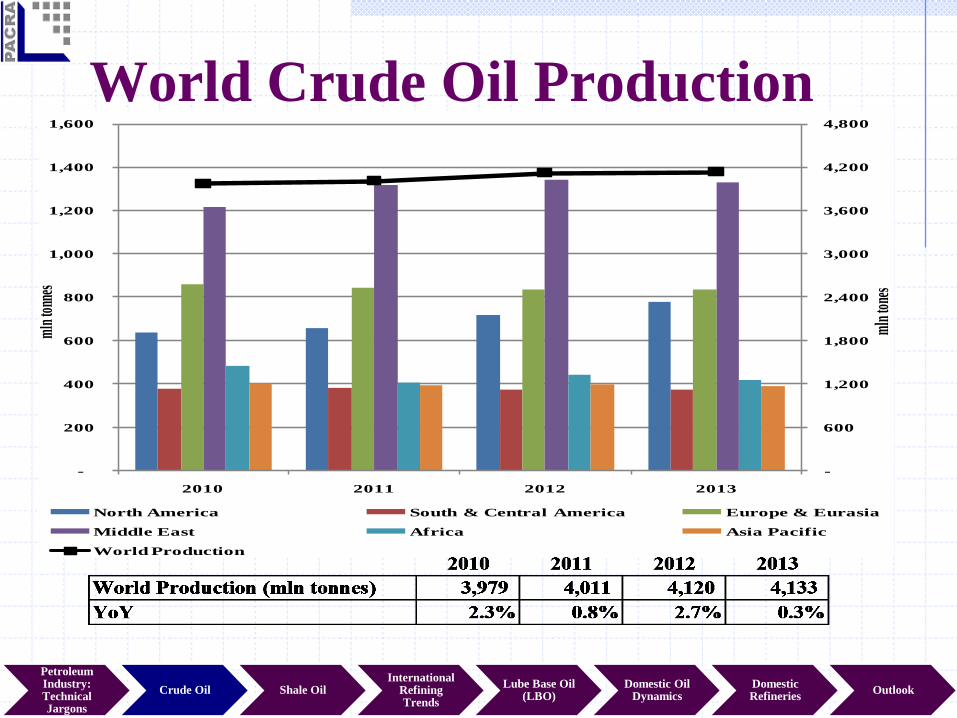

mln tonnes 1990 2000 2010 2013

World Oil Reserves 145,007 177,550 228,851 238,204

World Consumption (annual) 3,162 3,584 4,040 4,185

World Production (annual) 3,175 3,620 3,979 4,133

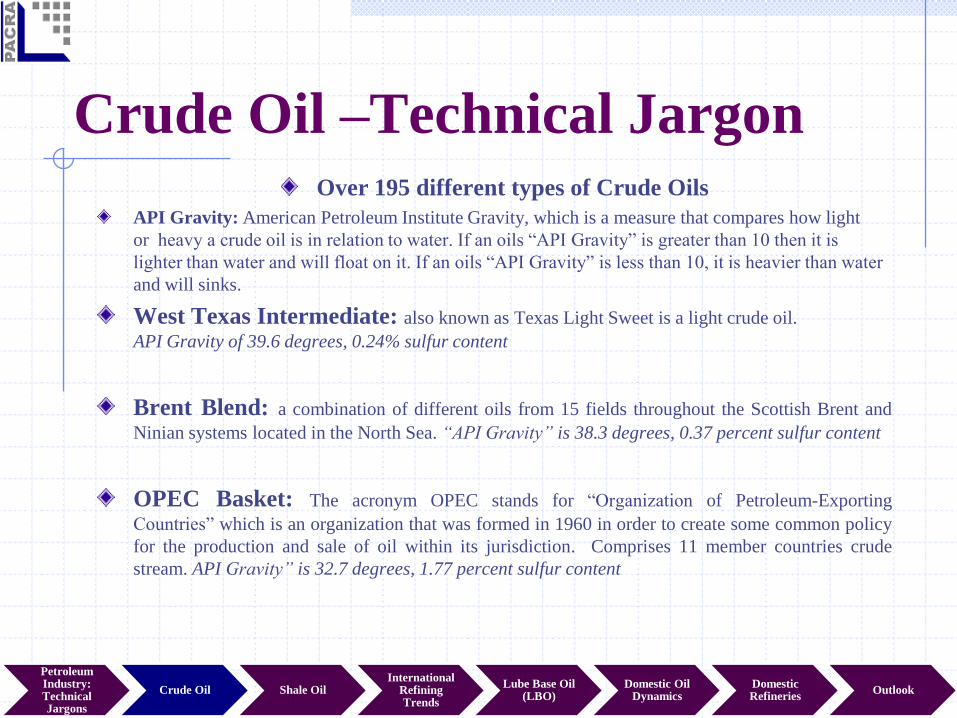

Crude Oil –Technical JargonOver 195 different types of Crude Oils

API Gravity: American Petroleum Institute Gravity, which is a measure that compares how light

or heavy a crude oil is in relation to water. If an oils “API Gravity” is greater than 10 then it is

lighter than water and will float on it. If an oils “API Gravity” is less than 10, it is heavier than water

and will sinks.

West Texas Intermediate: also known as Texas Light Sweet is a light crude oil.

API Gravity of 39.6 degrees, 0.24% sulfur content

Brent Blend: a combination of different oils from 15 fields throughout the Scottish Brent and

Ninian systems located in the North Sea. “API Gravity” is 38.3 degrees, 0.37 percent sulfur content

OPEC Basket: The acronym OPEC stands for “Organization of Petroleum-Exporting

Countries” which is an organization that was formed in 1960 in order to create some common policy

for the production and sale of oil within its jurisdiction. Comprises 11 member countries crude

stream. API Gravity” is 32.7 degrees, 1.77 percent sulfur content

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

World Crude Oil Reserves

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

-

50

100

150

200

250

2011 2012 2013

000'

mln

tonn

es

North America South & Central America Europe & Eurasia

Middle East Africa Asia Pacific

Total

-

600

1,200

1,800

2,400

3,000

3,600

4,200

4,800

-

200

400

600

800

1,000

1,200

1,400

1,600

2010 2011 2012 2013

mln

tone

s

mln

tonn

es

North America South & Central America Europe & Eurasia

Middle East Africa Asia Pacific

World Production

World Crude Oil Production

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

World Crude Oil Consumption

-

600

1,200

1,800

2,400

3,000

3,600

4,200

4,800

-

200

400

600

800

1,000

1,200

1,400

1,600

2010 2011 2012 2013

mln

tone

s

mln

tonn

es

North America South & Central America Europe & Eurasia

Middle East Africa Asia Pacific

World Consumption

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

-

20

40

60

80

100

120

140

160

US

D / b

bl

Price Comparison | WTI and Brent

Brent Crude WTI

Global Crude Oil TradeIn mln tons

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Shale Oil

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Shale Oil & Shale Gas –Technically Recoverable Reserves

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Shale Oil

Shale Gas

International Refining Trends

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

1990 2000 2010 2013

Global Refining Capacities (mln tonnes) 3,706 4,094 4,572 4,727

YoY 10.5% 11.7% 3.4%

Refining Process

}

}}

Light

Distillates

Medium

Distillates

Heavy

Distillates

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Types of RefineriesTopping - The topping refinery just separates the crude into its constituent petroleum products by distillation,

known as Atmospheric Distillation. Topping Refinery produces naphtha but no gasoline.

Hydroskimming - The hydroskimming refinery is equipped with Atmospheric Distillation, naphtha

reforming and necessary treating processes. Hydroskimming refinery is more complex than a topping refinery

and it produces gasoline.

Cracking - The cracking refinery, in addition to the above, is equipped with vacuum distillation and catalytic

cracking. The cracking refinery reduces fuel oil by conversion to light distillates and middle distillates.

Coking - The coking refinery is equipped to process the vacuum residue into high value products using the

Delayed Coking Process. The coking refinery adds further complexity to the cracking refinery by high

conversion of fuel oil into distillates and petroleum coke.

Nelson Complexity Index - The Nelson Complexity Index typically varies from about 2 for

Hydroskimming refineries, to about 5 for the Cracking refineries and over 9 for the Coking refineries.

Refineries, with high Nelson Complexity Index have the necessary flexibility in processing a wide variety of

crudes and are capable of achieving higher value addition.

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

-

600

1,200

1,800

2,400

3,000

3,600

4,200

4,800

-

200

400

600

800

1,000

1,200

1,400

1,600

2010 2011 2012 2013

mln

tone

s

mln

tonn

es

North America South & Central America Europe & Eurasia

Middle East Africa Asia Pacific

Global Refining Capacities

Global Refining Capacities

2010 2011 2012 2013

Global Refining Capacities (mln tonnes) 4,572 4,591 4,658 4,727

YoY 1.1% 0.4% 1.5% 1.5%

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Regional Capacity Utilization

50%

60%

70%

80%

90%

50%

60%

70%

80%

90%

2010 2011 2012 2013

%a

ge

%age

North America South & Central America Europe & Eurasia

Middle East Africa Asia Pacific

Global Capacity Utilization

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

In mln tons

Global Refined Products Trade

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Lube Base Oils (LBO)

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Lube Oil –Technical JargonViscosity Index?

Used to measure the “thickness” of liquid.

High for “thin” liquids and “low” for thick, which means,

The higher the VI, the less an oil will thicken as it gets cold and the less it will thin out at higher temperatures –

providing better lubricant performance at both temperature extremes.

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

50%

30%

11%9%

Group I Group II

Group III Group IV & V

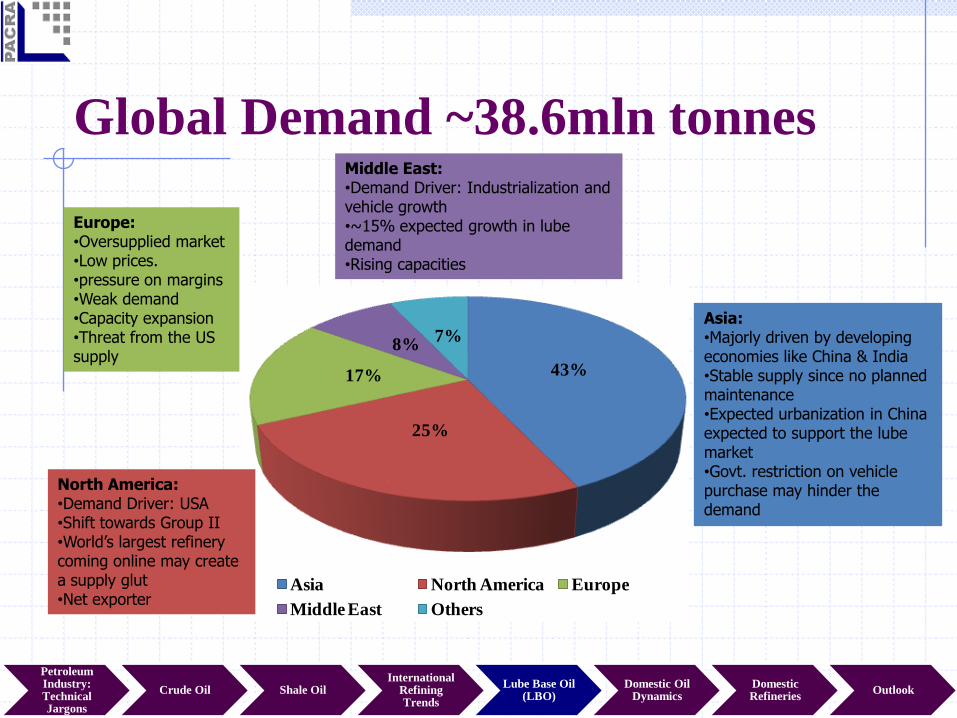

Global Demand ~38.6mln tonnes

43%

25%

17%

8%7%

Asia North America Europe

Middle East Others

Europe:•Oversupplied market•Low prices.•pressure on margins•Weak demand•Capacity expansion •Threat from the US supply

Asia:•Majorly driven by developing economies like China & India•Stable supply since no planned maintenance•Expected urbanization in China expected to support the lube market•Govt. restriction on vehicle purchase may hinder the demand

North America:•Demand Driver: USA•Shift towards Group II•World’s largest refinery coming online may create a supply glut•Net exporter

Middle East:•Demand Driver: Industrialization and vehicle growth•~15% expected growth in lube demand•Rising capacities

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

•Margins still under pressure post Baltic Sea glut problems.

•Going forward, the margins are expected to remain under pressure owing to the extensive

capacity expansion, which is expected to rise by ~3.5mln tonnes per annum by 2014.

Refining Margins

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Capacity Expansion

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Domestic Oil Dynamics

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Recoverable Reserves

51%

60% 58%

20%

15%14%

11%8% 10%

9% 8% 8%

7% 9%9%2% 1%

-

80

160

240

320

400

0%

20%

40%

60%

80%

100%

2011 2012 2013

mln

ba

rrel

s

%

ag

e

OGDCL MOL PPL POL UEPL Others Total

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Crude Production

56% 57% 54%

11% 12%14%

10%10%

9%

5%4%

3%

13% 10% 15%

5% 6% 5%

-

6

12

18

24

30

0%

20%

40%

60%

80%

100%

2011 2012 2013

mln

bar

rels

% a

ge

OGDCL MOL PPL POL UEPL Others Total

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Domestic Refineries

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Refining Capacity & Utilization

Capactity Utilization Capactity Utilization Capactity Utilization

Byco Petroleum 1.7 26.9% 1.8 7.3% 7.2 10.8% -

Pak Arab Refinery 4.5 74.6% 4.5 70.4% 4.5 91.6% -

National Refinery 2.7 89.3% 2.7 83.9% 2.7 78.8% -

Pakistan Refinery 2.1 76.2% 2.1 78.7% 2.1 74.1% -

Attock Refinery 1.9 95.8% 1.9 97.5% 2.0 100.0% 0.5

ENAR Petrotech 0.1 86.3% 0.1 98.2% 0.3 56.0% -

Dhodak Refinery 0.1 4.4% - - - - -

Total 13.15 74% 13.09 70% 18.79 57% 0.5

11.6 86%

Refinery 2011 2012 2013

Expansion

Without Byco

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Crude Oil Processed

12.4 11.5 10.5

6.7 6.1

7.4

3.1

3.1 3.3

-

5.0

10.0

15.0

20.0

25.0

2011 2012 2013

mln

to

nn

es

POL Imports Imported Crude Local Crude

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

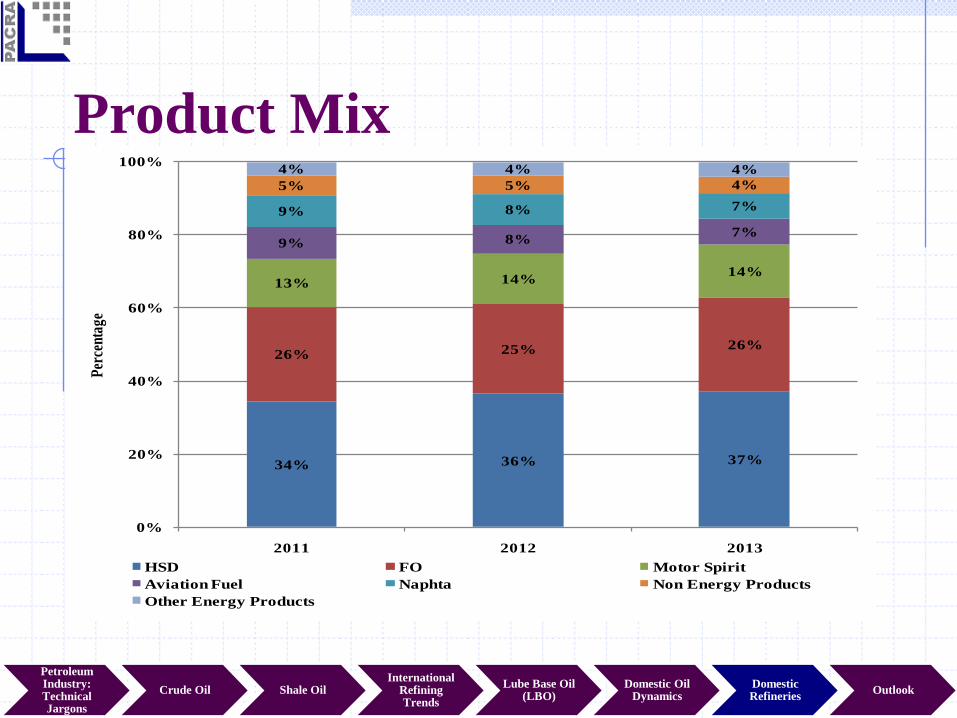

Product Mix

34% 36% 37%

26% 25% 26%

13% 14%14%

9% 8%7%

9% 8% 7%

5% 5% 4%

4% 4% 4%

0%

20%

40%

60%

80%

100%

2011 2012 2013

Per

cent

age

HSD FO Motor Spirit

Aviation Fuel Naphta Non Energy Products

Other Energy Products

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Supply Demand Mix – Fuels

56%

48%43%

50%56% 54%

75% 77%

67%

44%

52%57%

50%44% 46%

25% 23%

33%

-

2

4

6

8

10

0%

20%

40%

60%

80%

100%

2011 2012 2013 2011 2012 2013 2011 2012 2013

HSD Motor Spirit Furnace Oil

mln

to

nn

es

% a

ge

Imports Local Consumption

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

88

92

96

100

104

108

112

Jun-13 Sep-13 Dec-13 Mar-14 Jun-14

Exchange Rate

Exchange Rate

(1,500)

(1,000)

(500)

-

500

1,000

1QFY14 2QFY14 3QFY14 4QFY14

Exchange Gain / Loss

PARCO NRL ARL PRL

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Impact of Regulatory Duty

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Sale of HSD (Thousand Tonnes) 6,820 2,954 3,866 554 725 1,655 607 290

Conversion to Liters (Mln Liters) 8,149 3,530 4,620 661 866 1,978 725 346

Average Ex-Refinery Price (PKR/Liter) 74.39 74.39 74.39 74.39 74.39 74.39 74.39 74.39

Total Revenue (PKR Mln) 507,318 219,726 287,592 41,177 53,920 123,128 45,159 21,538

Deemed Duty on HSD - 7.5% (PKR Mln) 38,049 16,479 21,569 3,088 4,044 9,235 3,387 1,615

Profitability (PKR Mln) 27,580 2,627 3,520 19,950 1,482

Profitability excluding deemed duty (PKR Mln) 6,010 (461) (524) 10,716 (1,905)

Deemed Duty increase from FY16 - 9% (PKR Mln) 7,610 3,296 4,314 618 809 1,847 677 323

Pakistan

Refinery

(PRL)

Byco

Petroleum

Pakistan

(Byco)

Refining

Sector

Government of

Pakistan

(Imports)

Country's

CollectionFY13

Attock

Refinery

(ARL)

National

Refinery

(NRL)

Pak

Arab

Refinery

(PARCO

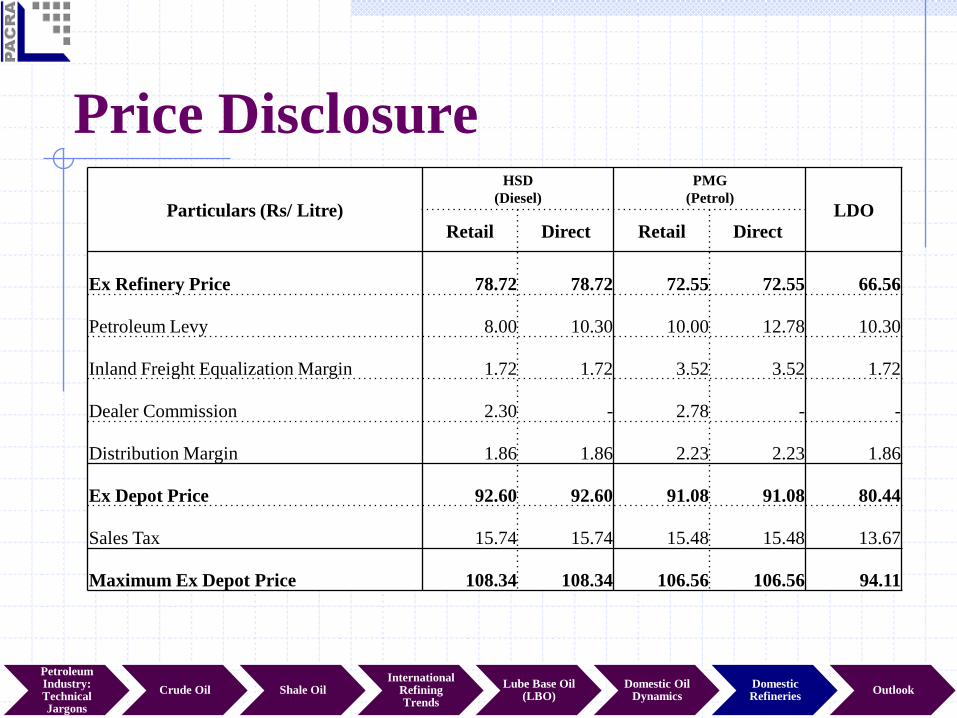

Price Disclosure

Particulars (Rs/ Litre)

HSD

(Diesel)

PMG

(Petrol)LDO

Retail Direct Retail Direct

Ex Refinery Price 78.72 78.72 72.55 72.55 66.56

Petroleum Levy 8.00 10.30 10.00 12.78 10.30

Inland Freight Equalization Margin 1.72 1.72 3.52 3.52 1.72

Dealer Commission 2.30 - 2.78 - -

Distribution Margin 1.86 1.86 2.23 2.23 1.86

Ex Depot Price 92.60 92.60 91.08 91.08 80.44

Sales Tax 15.74 15.74 15.48 15.48 13.67

Maximum Ex Depot Price 108.34 108.34 106.56 106.56 94.11

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Key Risks

Volatility in margins an outcome of fluctuating crude oil

prices and simpler technology

Unfavorable changes in pricing regime – removal of deemed

duty

Prevailing Inter-Corporate Debt – impacting throughput

levels

Exchange rate depreciation

What’s the outlook | Stable

Petroleum Industry: Technical Jargons

Crude Oil Shale OilInternational

Refining Trends

Lube Base Oil (LBO)

Domestic Oil Dynamics

Domestic Refineries

Outlook

Bibliography

1. Pakistan Energy Year Book : 2012-2013

2. Attock Petroleum Limited: www.apl.com.pk | Petroleum Product Prices

3. Attock Refinery Limited –Annual & Quarterly Financial Statements –Sep13, Dec13, Mar14, Jun14

4. BP Statistical Review of World Energy 2013: bp.com

5. US Energy Information Administration

6. Bain & Company: www.bain.com | Global Refining

7. zedatawatch: A Brief History of Oil Prices and Middle East Tensions: Fear of a Black Gold Shortage

8. Oil Price History and Analysis: http://www.wtrg.com/prices.htm

9. The Economist: http://www.economist.com/node/18285768

10. ICIS Base Oil Review 2013

11. Argus Base Oil Report -2014

12. Kline & Company

13. Fuels & Lube International: http://fuelsandlubes.com

14. Lube Report: www.lubengreases.com

15. Ernst & Young - The international dynamics of shale

16. Ernst & Young -Shale gas in Europe: Revolution or evolution?

17. KPMG -Shale Development: Global Update

18. PricewaterhouseCoopers Shale Oil, the next energy resolution

19. Deloitte University Press- US shale: A game of choices

20. Oxford Business Group

21. http://instituteforenergyresearch.org/analysis/colorado-an-energy-and-economic-analysis/

DISCLAIMERPACRA has used due care in preparation of this document. Our information has been obtained

from sources we consider to be reliable but its accuracy or completeness is not guaranteed.

The information in this document may be copied or otherwise reproduced, in whole or in part,

provided the source is duly acknowledged. The presentation should not be relied upon as

professional advice.

Analysts Rai Umar Zafar

Manager Ratings

+92 42 3586 9504

Muhammad Siddiq

Senior Financial Analyst

+92 42 3586 9504

Suffiyan Saleem

Financial Analyst

+92 42 3586 9504