Q3 2012 Stockholm road show - 4 Dec 2012 - Cargotec · Could result in a reduction of around 245...

38

Transcript of Q3 2012 Stockholm road show - 4 Dec 2012 - Cargotec · Could result in a reduction of around 245...

Q3 2012 Stockholm road show - 4 Dec 2012

CFO Eeva Sipilä

Strategy and structure

Nov 2012 3

Nov 2012

Cargotec’s businesses

Share of total sales in 1-9/12

Services share of sales in 1-9/12

4

Geographical split of sales in 1-9/12

Order to delivery lead time

Solutions for maritime transportation and offshore industries.

Ship-to-shore and container handling solutions for ports and terminals

Solutions for industrial and on-road load handling

33%

42%

25%

16%

25%

28%

12-24 months

6-9 months

2-4 months

EMEA 23% APAC 73% AMER 4%

EMEA 42% APAC 22% AMER 36%

EMEA 55% APAC 13% AMER 32%

Cargotec´s evolution

Nov 2012 5

MacGregor

Kalmar

Hiab

Preparing listing of MacGregor

More independent

businesses

Services integrated into

businesses

New role for group functions

Building shared

legal structure and regional footprint

Building shared

support functions

Development of supply footprint

MacGregor

Hiab

Kalmar

Industrial & Terminal

Marine

Centralised supply and sourcing organisation

Centralised

services development

Common frontline

organisation

Building one ERP

Marine

Terminals

Centralised support functions

Shared MAU’s

Common frontline

Common ERP

Common processes

Load Handling

2008 2013-

Separate listing of Marine in Asia

A separate listing of Marine business area provides an opportunity to accelerate growth and value creation of the business

The Board of Directors has decided to proceed with the preparations for a separate listing of Marine in Asia latest by second half of 2013 subject to market conditions

Cargotec will retain a majority stake in the listed subsidiary

Nov 2012 6

Service

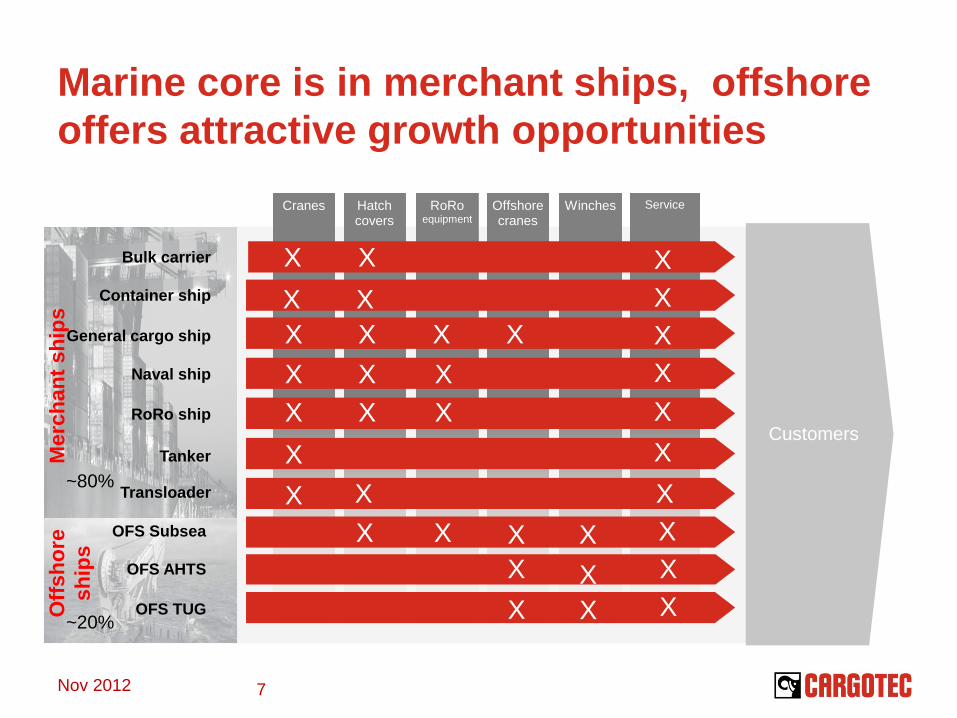

Marine core is in merchant ships, offshore offers attractive growth opportunities

Bulk carrier

Naval ship

RoRo ship

Tanker

Transloader

Offshore cranes

Hatch covers

Cranes

RoRo equipment

Customers

Container ship

General cargo ship

Winches

OFS Subsea

OFS AHTS

OFS TUG

Mer

chan

t shi

ps

Offs

hore

sh

ips

X X X X X X X X X X X X X X X X X

X X X

X X X

X X

X X X X X X X X X X

Nov 2012 7

~80%

~20%

Nov 2012

Manufacturing Installation After Sales Service

Outsourced MacGregor

Sales & Marketing

MacGregor

Design & Engineering

MacGregor

Outsourced

MacGregor

Outsourced

Concept focused on design, engineering and service

Reasonable margins Focus on core competencies

Cash positive Low fixed cost

High flexibility

Marine’s business model – built-in flexibility

8

Outsourced

Product fit

Fleet performance

Customer performance

Terminals’ strategy 2011–2015

To make our customers businesses run more effectively and efficiently

Objective is to be the leading and most efficient box moving company

Focus on integrated automation solutions

Navis

Extensive R&D investment

Improve competitiveness of product offering

Grow services business

Nov 2012 9

Services Global service network

Rebuilding and refurbishing Service contracting

Terminal development

The most comprehensive offering for Terminals

Nov 2012

Systems & Automation Terminal operating systems

Automated equipment Automated terminals

Equipment Complete set of equipment for container and cargo handling

tasks

Systems & Automation

Terminal operating systems Automated equipment Process automation

Packaging, Integration & Operationalisation

10

Terminals’ short term strategic actions

Improve operational efficiency Organisation with clear P&L responsibilities

Reduction of fixed cost

Improve volume product competitiveness Transfer of production from Lidhult to

Poland EMEA network integration

Improve profitability of big projects Increased project management competence Rainbow-Cargotec joint venture in China for

production Development of way of working and tools Tighter integration of sales and delivery

Nov 2012 11

Load Handling’s strategy 2011–2015

Focus on customer needs

Target is to be the leading on-road load handling supplier

Profitability over sales growth

Product differentiation

Route to market

Presence in mature markets with focused approach in China, Brazil and Russia

Nov 2012 12

Load Handling’s short term strategic actions

Cost efficiency Outsourcing Sourcing footprint Product cost improvement Supply efficiency Investment in Poland

Frontline execution development

Offering development

Nov 2012 13

January-September financials

Nov 2012 14

Highlights of Q3

Order intake decreased 11% y-o-y to EUR 719 (811) million

Sales grew 5% y-o-y to EUR 794 (753) million

Operating profit margin was 4.9% Focus on improving profitability,

restructuring measures launched

Cash flow from operations positive totalling EUR 34.2 (6.4) million

New outlook guides for approximately 5% operating profit margin excluding non-recurring cost for 2012

Nov 2012 15

January–September key figures

Q3 12 Q3 11 Change Q1-Q3/12 Q1-Q3/11 Change 2011 Orders received, MEUR 719 811 -11% 2,348 2,391 -2% 3,233

Order book, MEUR 2,312 2,349 -2% 2,312 2,349 -2% 2,426

Sales, MEUR 794 753 5% 2,437 2,310 5% 3,139

Operating profit, MEUR* 39.0 54.4 -28% 117.7 159.1 -26% 207.0

Operating profit margin, %* 4.9 7.2 4.8 6.9 6.6

Cash flow from operations, MEUR 34.2 6.4 6.4 78.0 166.3

Interest-bearing net debt, MEUR 485 362 485 362 299

Earnings per share, EUR 0.41 0.58 1.31 1.86 2.42

Nov 2012 16

*excluding restructuring

Performance development

Nov 2012 17

811

719 753 794

7.2

4.9

0

1

2

3

4

5

6

7

8

Q1/09 Q2/09 Q3/09 Q4/09 Q1/10 Q2/10 Q3/10 Q4/10 Q1/11 Q2/11 Q3/11 Q4/11 Q1/12 Q2/12 Q3/12

Orders Sales EBIT%

1,000

800

600

400

200

0

MEUR %

EBIT% excluding restructuring

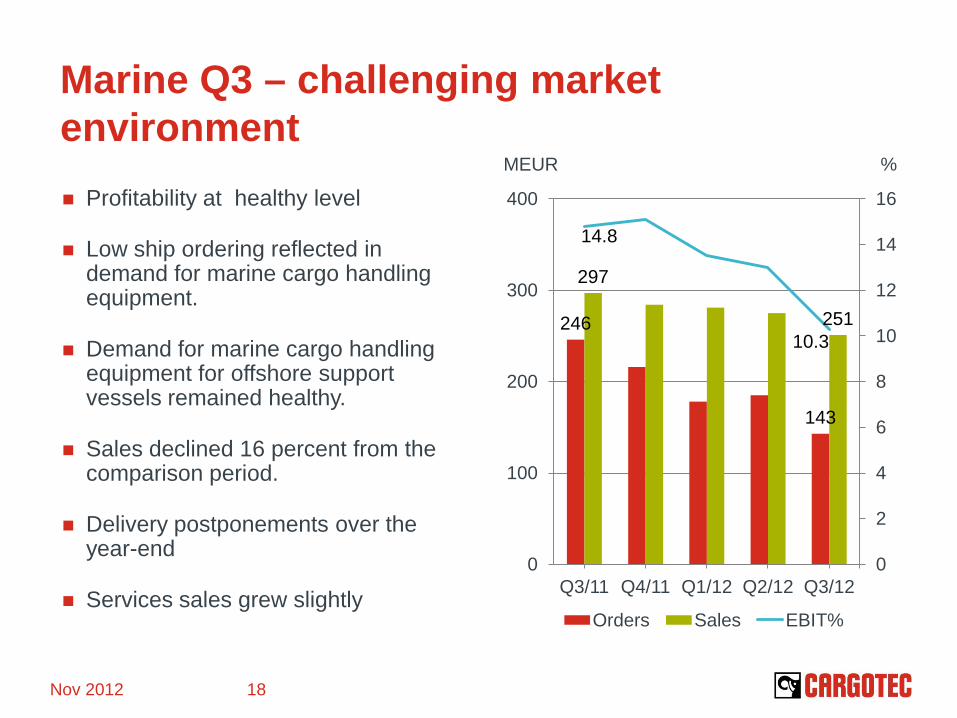

Marine Q3 – challenging market environment Profitability at healthy level

Low ship ordering reflected in demand for marine cargo handling equipment.

Demand for marine cargo handling equipment for offshore support vessels remained healthy.

Sales declined 16 percent from the comparison period.

Delivery postponements over the year-end

Services sales grew slightly

Nov 2012 18

246

143

297

251

14.8

10.3

0

2

4

6

8

10

12

14

16

0

100

200

300

400

Q3/11 Q4/11 Q1/12 Q2/12 Q3/12

Orders Sales EBIT%

MEUR %

Terminals Q3 – two major port equipment orders from Australia Demand for large projects and

automation solutions remained brisk.

Orders at the level of the comparison period

Sales grew 27% y-o-y.

Profitability was 3.6% Cost overruns on large deliveries Low relative share of services Investment in port automation

technology

Focus on profitability and project execution

Nov 2012 19

389 383

278

352

6.2

3.6

0

2

4

6

8

0

100

200

300

400

500

600

Q3/11 Q4/11 Q1/12 Q2/12 Q3/12

Orders Sales EBIT%

MEUR %

EBIT% excluding restructuring

Load Handling Q3 – profitability rebounded from Q2 Demand for load handling

equipment in Europe weakened following the general economic uncertainty, and remained strong in the US.

Orders grew 8% y-o-y.

Sales grew 7% y-o-y.

Profitability was 3.1% rebounding from Q2 as expected.

Focus on profitability

Nov 2012 20

177 192

178 191

1.9

3.1

0

1

2

3

4

0

50

100

150

200

250

300

Q3/11 Q4/11 Q1/12 Q2/12 Q3/12

Orders Sales EBIT%

MEUR %

EBIT% excluding restructuring

Cash flow from operations positive

Nov 2012 21

6 34

-50

0

50

100

150

200

250

300

350

2008 2009 2010 2011 Q1/11 Q2/11 Q3/11 Q4/11 Q1/12 Q2/12 Q3/12

MEUR

Services sales grew 3% y-o-y

Nov 2012 22

183 188

2008 2009 2010 2011 Q1/11 Q2/11 Q3/11 Q4/11 Q1/12 Q2/12 Q3/12

800

1,000

600

400

200

0

MEUR

Balanced geographical split in sales

Nov 2012 23

25 %

42 %

33 % 39%

36%

24%

Marine Terminals Load Handling Americas APAC EMEA

Equipment 84% (86) Services 16% (14)

Equipment 72% (72) Services 28% (28)

Equipment 75% (69) Services 25% (31)

Sales by reporting segment 1-9/2012, % Sales by geographical segment 1-9/2012, %

(41)

(40)

(20) (24)

(36)

(40)

Cargotec’s ongoing actions

Interim President and CEO

New more business-focused structure

Employee cooperation negotiations Could result in a reduction of around 245 man-years

globally

Centralisation of reachstacker and empty container handler production from Lidhult, Sweden, to Stargard Szczecinski, Poland Could result in a reduction of around 130 employees

Adjusting capacity to demand and restructuring operations in Hudiksvall, Sweden Could result in a reduction of around 150 employees

Business areas will be named after their industry leading brand names MacGregor, Kalmar and Hiab

Nov 2012 24

Outlook

Cargotec’s operating profit margin for 2012 is expected to be approximately 5 percent excluding non-recurring costs.

Sales are expected to grow from 2011.

Nov 2012 25

Appendices

Nov 2012 26

Source: IHS Global Insight Q3/2012

Truck sales GVW over 15 ton - regions Sales growth GVW over 15 ton - regions

Macro indicator trends

Nov 2012 27

0

200 000

400 000

600 000

800 000

1 000 000

1 200 000

1 400 000

EMEA APAC AMER

2008 2009 2010 2011 2012 2013 2014 2015 2016

-60,0 %

-40,0 %

-20,0 %

0,0 %

20,0 %

40,0 %

60,0 %

80,0 %

EMEA APAC AMER

2008 2009 2010 2011 2012 2013 2014 2015 2016

Macro indicator trends

Nov 2012 28 Source: Oxford Economics Q3/2012

0 100 200 300 400 500 600 700 800 900

EMEA AMER APAC

Total Construction Output 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Billion EUR

90

95

100

105

110

115

-8

-6

-4

-2

0

2

4

6

EMEA: Construction output

INDEX CHANGE (%)

Annual change (%)

Index 2005 = 100

0

50

100

150

200

0

2

4

6

8

APAC: Construction Output

INDEX CHANGE (%)

Annual change (%)

Index 2005 = 100

0

20

40

60

80

100

120

140

-12 -10

-8 -6 -4 -2 0 2 4 6 8

10

AMER: Construction Output

INDEX CHANGE (%)

Annual change (%)

Index 2005 = 100

Macro indicator trends

Nov 2012 29

0

100 000

200 000

300 000

400 000

500 000

600 000

AMER EMEA APAC

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

-15,0 %

-10,0 %

-5,0 %

0,0 %

5,0 %

10,0 %

15,0 %

20,0 %

AMER EMEA APAC

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Drewry (Throughput TEU % change) Drewry (Throughput ’000 TEU units)

Source: Drewry Global Container Terminal Operators, Annual Report 2012

Ship contracting forecast

Nov 2012 30

Source: Clarkson Shipbuilding forecast 9/2012

Low gearing and strong liquidity 30 Sep 2012 Gearing 38.8%

Net debt MEUR 485

Liquidity MEUR 426 Cash and cash equivalents

MEUR 126 Unused and committed long-

term revolving credit facility of MEUR 300

Cargotec is well prepared financially for the coming years

Nov 2012 31

MEUR Repayment schedule of interest-bearing

liabilities

137

47 93

5 3

91

239

0

40

80

120

160

200

240

280

2012 2013 2014 2015 2016 2017 2018-

Services

Truck-mounted forklifts Demountables Loader cranes

Forestry cranes Tail lifts Stiff boom cranes

Hiab offering

Nov 2012 32

Key competition with Hiab offering

Nov 2012 33

Knuckle-boom Cranes Demountables Truck-mounted

Forklifts Forestry Cranes Tail Lifts Stiff boom

Cranes

X X X X X X

X

X X X

X X X X

X X X

X X X X X X X

X X

X

X X

X X

X X X X

X X

X X X

• Hiab • Palfinger • Hyva • Fassi • Effer • HMF • Unic • Tadano • National • Meiller • VDL • Stellar • Shimaywa • D’Hollandia • Bär • Dautel • Anteo • Maxon • Tommy Gate • Manitou • Terberg Kinglifter • Chrisman • Donkey • Kesla • Prentice

Terminal tractors Forklift trucks Reachstackers Straddle carriers

Ship-to-Shore cranes RTGs, RMGs Services Spreaders

Kalmar offering

Nov 2012 34

Key competition with Kalmar offering

Nov 2012 35

Ship-to- shore cranes

Mobile harbour cranes

RTG/RMG cranes

Straddle/ Shuttle carriers

Reach stackers

Fork lift trucks

Terminal tractors. AGVs

Services Spreaders

X X X X X X X X

X

X

X

X X

X X X X

X

X X X X

X X

X X

X

X X X X

X X X X X X X

X

X X X

X

X X X X X

X X

X

X

X X X X

• Kalmar • ZPMC • Konecranes • Terex/Gottwald • Sany • Liebherr • Mitsubishi • Mitsui • Kunz • TCM • CVS • Hyster Heavy • Taylor • Linde Heavy • Zoomlion • Tomac • Toyota • Sinotruk • Capacity • Terberg • Mafi • Stinis • RAM

X X

X

X

X

X X

ASC carriers

X X X X X X X X X X

Link spans

Ship cranes Securing Hatch covers

RoRo Services Bulk loaders

Offshore deck equipment

MacGregor offering

Nov 2012 36

Key competition with MacGregor offering

Nov 2012 37

• MacGregor • TTS • SMS (ex Seohae) • Iknow (ex Tsuji) • Kyoritsu • Nakata • IHI • Coops & Nieborg • Macor • Navalimpianti • Liebherr • Oriental Precision • Huisman • MHI • German Lashing • SEC • Taiyo • National Oilwell Varco • Rolls Royce • Aker Solutions (Pusnes) • Hatlapa • EMS-Tech • Seabulk • Oshima

Hatch covers

Deck cranes

Offshore winches

Lashing equipment Services

X X X X X X

X X

(X)

X

X X

X

X

X X X X

X

X X X

X X

X

X X X X X

X X

(X) (X)

(X)

X

X X

X X

(X)

RoRo equipment

X X

X (X) X X X

X X

Offshore ALH

X X X X X X

X X

Self unloaders

X

X X X