Parex Resources Corporate Presentation May 2014

22

May 2014 Corporate Presentation PAREXRESOURCES.COM | TSX:PXT Building The Runway

-

Upload

pacecreative -

Category

Investor Relations

-

view

47 -

download

3

Transcript of Parex Resources Corporate Presentation May 2014

May 2014

Corporate Presentation

PAREXRESOURCES.COM | TSX:PXT

Building The Runway

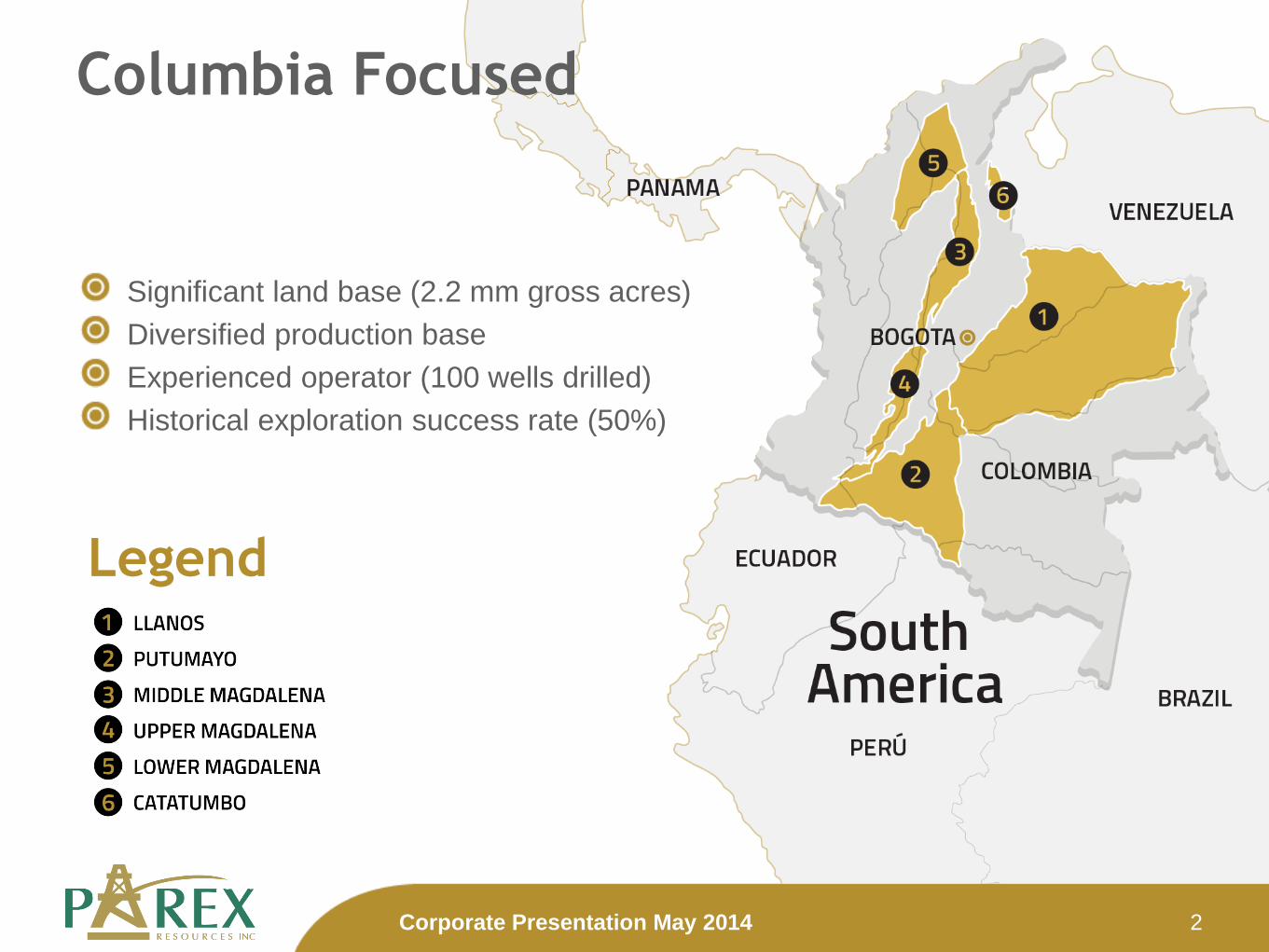

Significant land base (2.2 mm gross acres)

Diversified production base

Experienced operator (100 wells drilled)

Historical exploration success rate (50%)

Legend

Columbia Focused

2 Corporate Presentation May 2014

Objectives

Q1 2014 Operating Netback $61.20/bbl

Q1 2014 Production 18,425 bopd

Q1 Funds Flow $77 MM

Reserves 2P (Dec. 31, 2013) 32 MMboe1

Doubled 2P reserves over 2012 year-end

Capital Structure

Market capitalization at $11.50/share Cdn$1,270 MM

Convertible debenture PXT.DB Cdn$85 MM

(5.25% coupon & $10.15/share conversion with 2016 maturity)

Common shares outstanding (TSX listed)

Basic 110.4 MM

Fully Diluted 127.5 FD2 MM

Snapshot

(1) Parex net working interest, as per the independent reserve report prepared by GLJ Petroleum Consultants Ltd. effective December31, 2013.

(2) Fully diluted shares does not include out of the money options based on a share price of $11.50

3 Corporate Presentation May 2014

Existing Fields: Development & Appraisal Drilling -16,000 bopd

Exploration Drilling 1,500-2,500 bopd

New Play Concepts (types: heavy oil, tight sands, stratigraphic) “upside”

2014 Production* 17,500-18,500 bopd

*Second quarter production to average approximately 19,000 – 19,500 bopd

2014 Guidance

Delivering cash flow funded 15% year-year production growth

Available to support

Exploration Success

#Wells Capex (Net $ million)

Gross Net Wells Facilities Other Total

Development /Appraisal (existing fields) 15 9.6 $54 $34 $2 $90

Exploration (proven plays) 19 11.5 $96 $20 $9 $125

New Play Concepts 3 2.3 $21 $5 $9 $35

Base (Firm) Total 37 23.4 $171 $59 $20 $250

Appraisal (Contingent) 8 4.7 $18 $12 $0 $30

4 Corporate Presentation May 2014

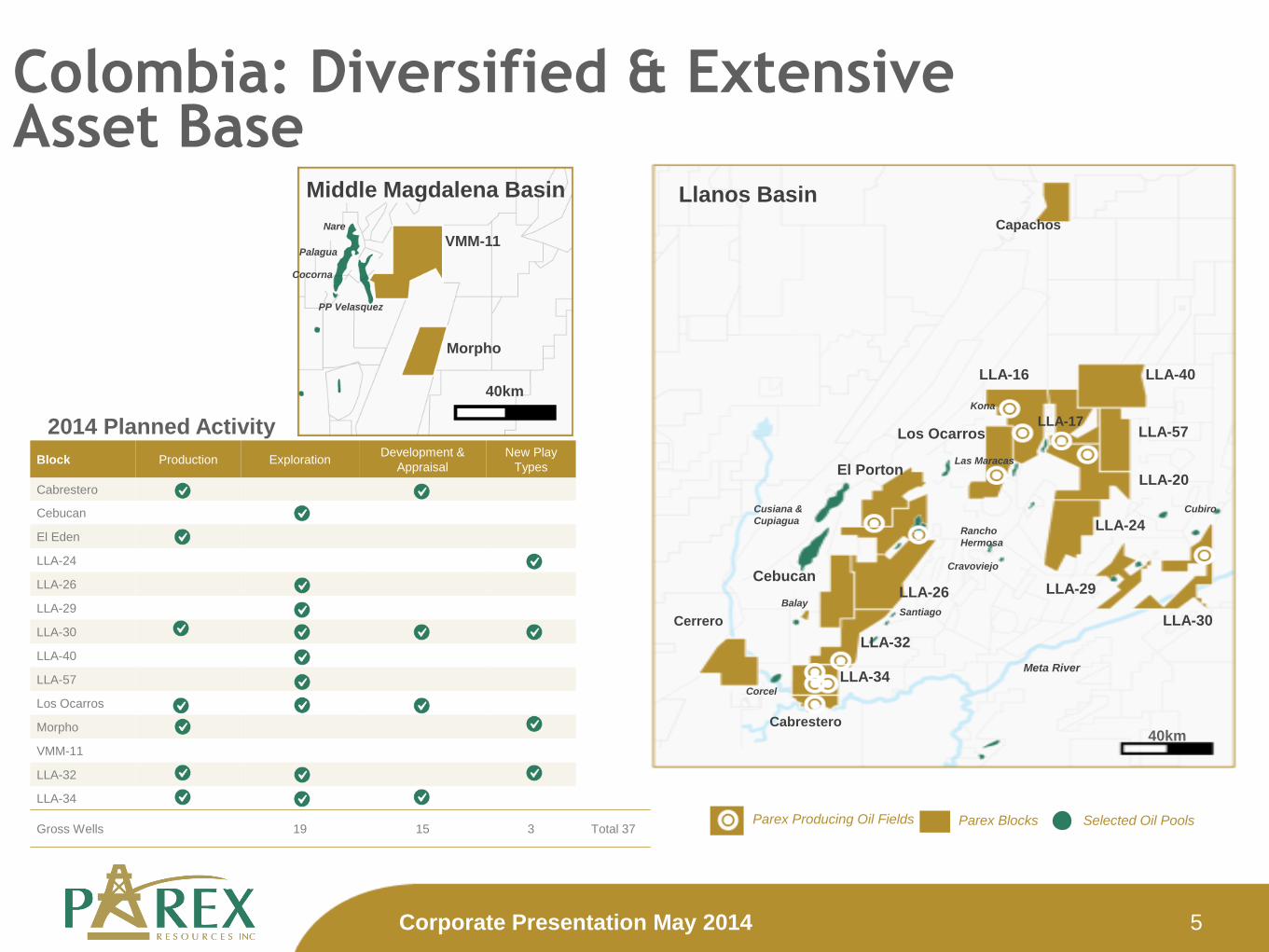

Middle Magdalena Basin

VMM-11

Morpho

PP Velasquez

Palagua

Nare

40km

Cocorna

Parex Producing Oil Fields

2014 Planned Activity

Colombia: Diversified & Extensive Asset Base

Block Production Exploration Development &

Appraisal

New Play

Types

Cabrestero

Cebucan

El Eden

LLA-24

LLA-26

LLA-29

LLA-30

LLA-40

LLA-57

Los Ocarros

Morpho

VMM-11

LLA-32

LLA-34

Gross Wells 19 15 3 Total 37

5 Corporate Presentation May 2014

Parex Blocks Selected Oil Pools

40km

Llanos Basin

LLA-16 LLA-40

LLA-17 LLA-57

LLA-20

LLA-24

LLA-30

Meta River

Cubiro

Corcel

Balay

Cusiana &

Cupiagua Rancho

Hermosa

Cravoviejo

Las Maracas

Los Ocarros

El Porton

Cabrestero

LLA-34

LLA-32

Santiago

LLA-26 Cebucan

Kona

Cerrero

Capachos

LLA-29

Proved + Probable

+ Possible Proved + Probable Proved

2P Reserves Life

Index (1)

After Tax PV10

(USD MM)

Reserves* MMboe

31-Dec 09 - - - - -

31-Dec 10 10.4 5.8 1.1 - $149

31-Dec 11 17.6 10.7 4.6 2.6x $344

31-Dec 12 23.1 16.1 10.1 3.5x $450

31-Dec 12 49.9 32.0 17.4 5.1x $832

Track record of reserve category progression

Increasing reserve life index (RLI) & sustainability

Building A Sustainable Business

June 30, 2013 Company’s reported reserves were 3P-36.4 Mmboe, 2P-23.7 Mmboe and 1P-14.1 Mmboe (1) RLI calculated using 2P year-end reserves divided by Q4 production annualized

*Reserves are independently evaluated by GLJ Petroleum Consultants Ltd.

6 Corporate Presentation May 2014

Median Llanos

100 acres

Kona

300 acres

Low side closures

500 +1000 acres

Oil

Water

Sandstone

Shale

Las Maracas

300 acres

Bottom water drive Edge water drive Edge water drive

Structures: Progressively Larger

Corporate Presentation May 2014 7

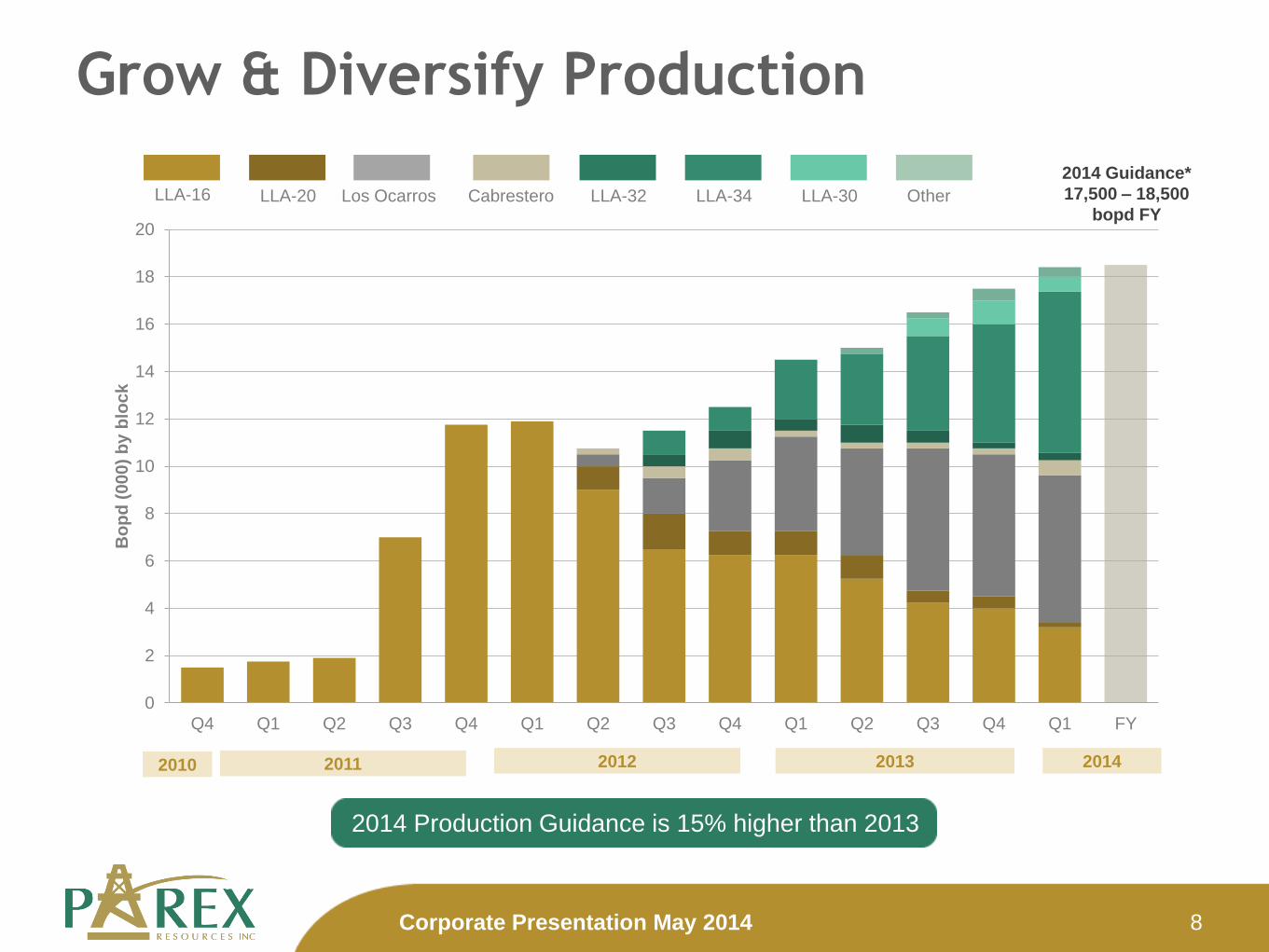

Grow & Diversify Production

2014 Production Guidance is 15% higher than 2013

0

2

4

6

8

10

12

14

16

18

20

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 FY

Bo

pd

(0

00

) b

y b

loc

k

2010 2011 2012 2013 2014

2014 Guidance*

17,500 – 18,500

bopd FY LLA-16 LLA-20 Los Ocarros Cabrestero LLA-32 LLA-34 LLA-30 Other

8 Corporate Presentation May 2014

Parex Exploration Life Cycle

Continue to deliver on our strategy to expand the asset base and added

Meaningful positions for future sustainable growth

Develop

Concept

Acquire

Land

Test

Concept

Initial

Development

Expand

Land Exploitation

Traditional

3-Ways

Low Side

Closures

Stratigraphic

Traps

New Plays

LLA-26, Cebucan

LLA-24, LLA-29 & LLA-30

Cabrestero, LLA-34

VMM-11, Morpho, Llanos Deep Sands, Capachos

9 Corporate Presentation May 2014

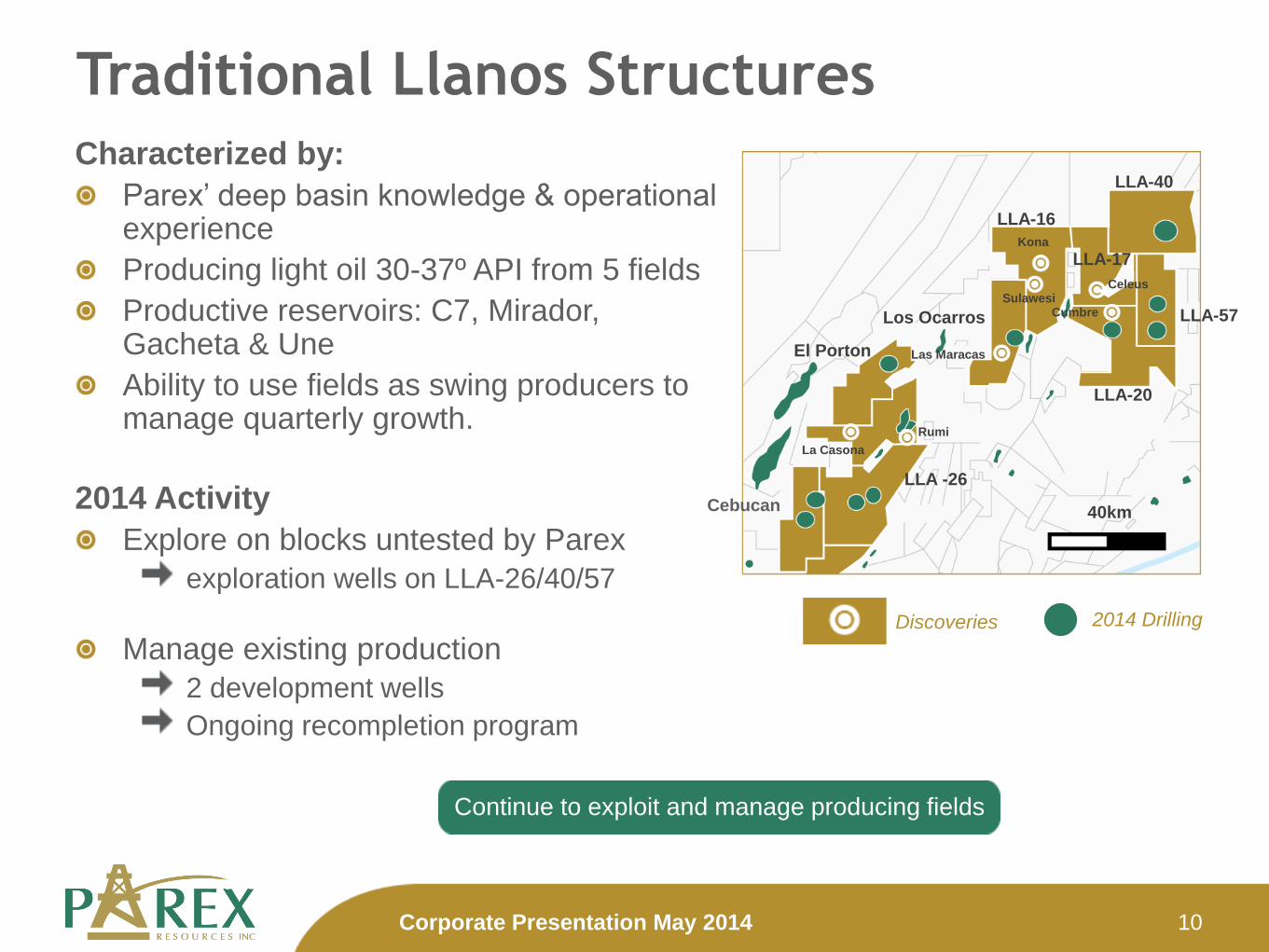

Characterized by:

Parex’ deep basin knowledge & operational experience

Producing light oil 30-37º API from 5 fields

Productive reservoirs: C7, Mirador, Gacheta & Une

Ability to use fields as swing producers to manage quarterly growth.

2014 Activity

Explore on blocks untested by Parex

exploration wells on LLA-26/40/57

Manage existing production

2 development wells

Ongoing recompletion program

Traditional Llanos Structures

Continue to exploit and manage producing fields

10 Corporate Presentation May 2014

Discoveries

40km

LLA-40

La Casona

Rumi

Las Maracas

Sulawesi

Kona

Celeus

Cumbre

LLA-16

LLA-17

LLA-57

LLA-20

Los Ocarros

El Porton

LLA -26

Cebucan

2014 Drilling

Acquired blocks in 2012 to develop concepts

and prove-up in 2013 with discoveries

Cabrestero (100% WI, Operator)

Akira - new play type low side closures

Facility start-up

LLA 34 (45% WI, Non-operated)

Increased new prospect inventory through 3D seismic acquisition on western side

Significant development focus

LLA-32

Kananaskis discovery

2 exploration wells to test

3 appraisal wells

Southern Llanos: Low Side Closures

Explore core position, appraise & develop discoveries, and leverage Parex’ costs and exploration know-how

Corporate Presentation May 2014 11

2013 3D Seismic

Corcel

Cabrestero

LLA-32

Jilguero

Santiago

Max

Tarotaro

LLA-34

Tigana

Tigana Sur

Kananaskis

Tua

Discoveries 2010/11 Seismic

20km

Maniceño -Bandola

Kitaro Akira

Verano Acquisition: Property Summary

Block Parex

WI

Verano

WI

Close PXT

WI

LLA-17 40% 23% 63%

LLA-32 30% 40% 70%

LLA-34 45% 10% 55%

Acquisition subject to Verano shareholder vote. Refer to Parex news release dated May 13, 2014

Corporate Presentation May 2014 12

2013 3D Seismic

Corcel

Cabrestero

LLA-32

Jilguero

Santiago

Max

Tarotaro

LLA-34

Tigana

Tigana Sur

Tua

Discoveries 2010/11 Seismic

20km

Maniceño -Bandola

Kitaro Akira

Kananaskis

Carmentea

Calono

LLA-30 (100% WI, Operator)

New Discoveries 2013:

Adalia-1 38° API at 1,000 bopd

Adalia-2 waiting on completion

Adalia-3 initial test of 38° API at 1,000 bopd

Exploration well in 2014

LLA-24 (100% WI, Operator)

New block for Parex:

Exploration well in 2014 & test concepts

New Play Type: Stratigraphic/Channels

First drilled in 2013 and analyzing stratigraphic concepts. Drilling off structure prospect to prove-up concept.

Corporate Presentation May 2014 13

LLA-20

LLA-24

LLA-29

LLA-30 20km

Discoveries

Adalia

Capachos (50% WI, Operator)

Ecopetrol partnership

ANH royalty contract

Large structure, light oil

Leverages our strengths:

low cost drilling

strong operator

working with communities

Capachos Farm-in

14 Corporate Presentation May 2014

Capachos

LLA-16

LLA-40

LLA-17

LLA-57

VMM-11 (60% WI, Operator)

Farm-in to drill one well

Testing of new play concepts for cold heavy oil

production (CHOPS)

Builds on management’s success with Petro

Andina in Argentina’s Neuquén Basin

Morpho (100% WI, Operator)

Over 2000’ of gross pay in each of the Colorado

(Oligocene) and Eocene

Morpho-1 well completed in 3 of 6 Oligocene

sands, > 100 bopd

Next, new well & optimized frac program

Acquiring new 2D seismic allows us to apply a

resource concept over approximately 10,000 acres

New Play Concepts

New Play Concepts: applying proven technology in Colombia

15 Corporate Presentation May 2014

Middle Magdalena Basin

VMM-11

Morpho

PP Velasquez

Palagua

Cocorna

Nare

40km

Discoveries Ocensa Pipeline

Llanos’ “Deep Basin”

Foothills: large oil & gas structures, +$75MM wells

Plains: small oil structures, $5-$10MM wells

Transition Zone “Deep Basin”: undrilled, +$25MM wells

Parex target $10-15 MM wells

Apply low cost operator advantage to explore the Llanos Transition Zone

Transition

Zone

Corporate Presentation May 2014 16

Expanding Capacity

New take-away capacity exceeds basin production growth

Source: Ecopetrol, 2013

0

500

1000

1500

2000

2500

2010 2011 2012 2013 2014 2015 2016

Colombian demand vs. Capacity* (mbd)

Fuel Oil

Third Parties production

Partners

Pipeline Capacity

*includes trucks

Diluent

Royalties

Ecopetrol’s Production

Total Capacity

Current Production

17 Corporate Presentation May 2014

Growth Opportunity 2012 – 2014:

Crude Oil Pipeline – Key Projects

1. San Fernando - Monterrey System: +390 mbod

2. Bicentenario Phase 1: +120 mbod

3. Magdalena Medio System: +75 mbod

4. Caño Limón - Coveñas: +55 mbod

988

1,133 1,287

1,377 1,446

1,472

2,020

Operating Netback: Colombia Premium

$63 $71 $67 $71

$82 $73 $71 $69 $67

$58 $64 $61 $62

$26

$22 $22

$23

$26

$26 $29 $29 $27

$28

$29 $29 $28

$7

$12

$8 $8

$9

$8 $8 $8 $15

$14

$14 $12 $14

0

20

40

60

80

100

120

140

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

Realized

Pri

ce (

$/b

oe)

Brent Price $/BBL

Price

Fiscal

Costs

Parex’ Take

Q1 2014

5,000 bpd

hedged

> $105/bbl

2011 2012 2013 2014

Brent Price

$/BBL Royalties Opex &

Transportation

Operating

Netback

Corporate Presentation May 2014 18

Proven Management’s track record

Exposure to Brent Oil Pricing LATAM exposure

Self-funded growth

Parex’ Value Proposition

Corporate Presentation May 2014 19

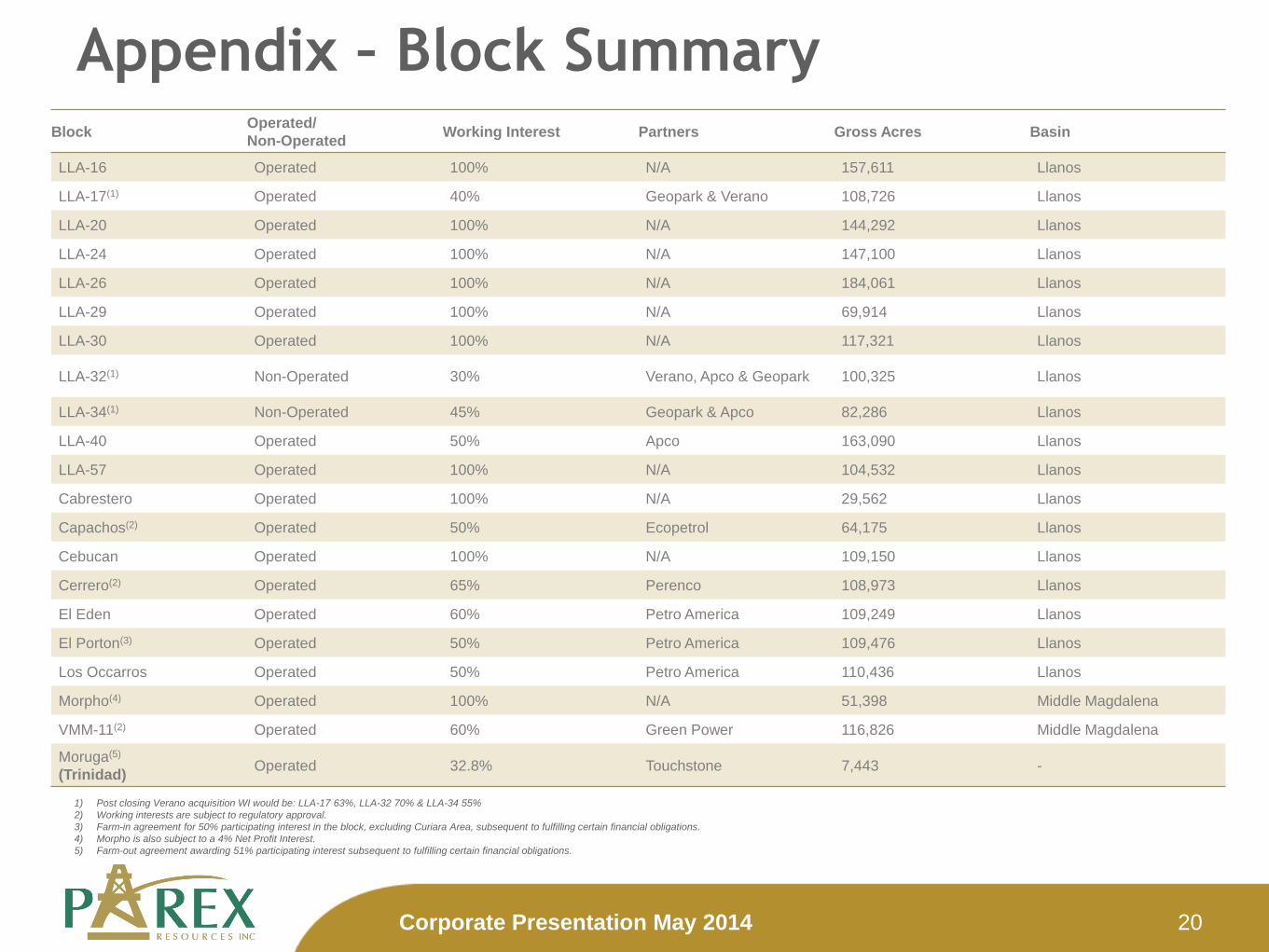

Appendix – Block Summary

1) Post closing Verano acquisition WI would be: LLA-17 63%, LLA-32 70% & LLA-34 55%

2) Working interests are subject to regulatory approval.

3) Farm-in agreement for 50% participating interest in the block, excluding Curiara Area, subsequent to fulfilling certain financial obligations.

4) Morpho is also subject to a 4% Net Profit Interest.

5) Farm-out agreement awarding 51% participating interest subsequent to fulfilling certain financial obligations.

Corporate Presentation May 2014

Block Operated/

Non-Operated Working Interest Partners Gross Acres Basin

LLA-16 Operated 100% N/A 157,611 Llanos

LLA-17(1) Operated 40% Geopark & Verano 108,726 Llanos

LLA-20 Operated 100% N/A 144,292 Llanos

LLA-24 Operated 100% N/A 147,100 Llanos

LLA-26 Operated 100% N/A 184,061 Llanos

LLA-29 Operated 100% N/A 69,914 Llanos

LLA-30 Operated 100% N/A 117,321 Llanos

LLA-32(1) Non-Operated 30% Verano, Apco & Geopark 100,325 Llanos

LLA-34(1) Non-Operated 45% Geopark & Apco 82,286 Llanos

LLA-40 Operated 50% Apco 163,090 Llanos

LLA-57 Operated 100% N/A 104,532 Llanos

Cabrestero Operated 100% N/A 29,562 Llanos

Capachos(2) Operated 50% Ecopetrol 64,175 Llanos

Cebucan Operated 100% N/A 109,150 Llanos

Cerrero(2) Operated 65% Perenco 108,973 Llanos

El Eden Operated 60% Petro America 109,249 Llanos

El Porton(3) Operated 50% Petro America 109,476 Llanos

Los Occarros Operated 50% Petro America 110,436 Llanos

Morpho(4) Operated 100% N/A 51,398 Middle Magdalena

VMM-11(2) Operated 60% Green Power 116,826 Middle Magdalena

Moruga(5)

(Trinidad) Operated 32.8% Touchstone 7,443 -

20

($ millions, except per share amounts) 2014 2013 2012

Q1 FY Q4 Q3 Q2 Q1 FY Q4

Q3 Q2 Q1

OPERATING

Average realized prices, prior to hedging 103 104 102 106 99 110 109 106 108 108 117

Brent Price ($/bbl) 108 109 109 110 103 112 112 110 110 108 119

Vasconia ($/bbl) 101 104 102 106 99 108 106 103 103 104 115

Production (thousands of bopd) 18.4 15.9 17.3 16.2 15.5 14.4 11.4 12.7 10.9 10.4 11.7

FINANCIAL

Sales of crude oil 180 637 167 157 148 165 524 150 131 113 130

Funds flow from operations 77 270 76 68 66 60 242 54 42 61 84

Per share – basic 0.70 2.49 0.70 0.63 0.61 0.56 2.23 0.50 0.39 0.57 0.77

Net income (loss) 10 13 22 (28) 8 11 40 (16) 8 21 27

Per share – basic 0.09 0.20 0.20 (0.26) 0.07 0.10 0.37 (0.15) 0.07 0.19 0.25

Per share – diluted 0.09 0.18 0.18 (0.26) 0.04 0.05 0.31 (0.15) 0.07 0.09 0.25

EBITDA 97 325 92 82 80 72 258 46 62 68 83

Cash and cash equivalents 198 57 57 26 45 27 32 32 27 51 121

Working Capital 37 24 24 19 9 17 (13) (13) (9) (0.6) 116

Net Debt (1) 29 70 70 85 104 88 107 107 94 86 (31)

Capital Expenditures 62 234 59 50 78 47 268 65 51 93 59

Weighed average shares outstanding 109 108 108 108 108 109 108 108 108 108 108

Weighed average shares outstanding, diluted 111 124 124 108 130 129 126 110 109 117 118

TRADING STATISTICS

($, based on intra-day trading)

High 9.50 6.8 6.80 6.30 4.89 6.50 8.67 6.03 5.18 7.15 8.67

Low 6.59 4.05 5.60 4.10 4.05 4.39 4.07 4.27 3.85 4.29 6.49

Close (end of period) 9.50 6.58 6.58 5.83 4.12 4.63 5.80 5.80 4.83 4.72 7.04

Average daily volume (thousands) 360 216 258 193 203 210 236 235 148 335 264

Appendix – Summary of Quarterly Results (Unaudited)

(1) Defined as WC+ Bank Debt + CD Face Value C$85 million.

Bank credit facility currently has a borrowing base of $150 million & Face value of debenture is Cdn $85 million with conversion price of Cdn $10.50/share.

Corporate Presentation May 2014 21

Certain statements in this document are “forward-looking statements”. Forward-looking statements are frequently

characterized by words such as “prospective”, “plan”, “expect”, “project”, “intend”, “believe”, “anticipate”, “estimate”, “forecast”,

or other similar words, or statements that certain events or conditions “may” or “will” occur. Forward-looking statements are not

based on historical facts but rather on the expectations of management of the Company ("Management") regarding the

Company's future growth, results of operations, production, plans for and results of drilling activity, business prospects and

opportunities. Such forward-looking statements reflect Management's current beliefs and assumptions and are based on

information currently available to Management. In particular, this document contains forward-looking statements regarding, but

not limited to, the Company's expected 2013 production rates and Parex' drilling plans. Forward-looking statements involve

significant known and unknown risks and uncertainties. A number of factors could cause actual results to differ materially from

the results discussed in the forward-looking statements including the risks associated with negotiating with foreign

governments as well as country risk associated with conducting international activities, competition, the ability to generate

revenue and exploit operating margins, capital resources, the use of certain technologies and materials, annual impairment

tests, labour relations, insurance, damage from weather and other disasters, operating and maintenance risks and

environmental risks, new information regarding reserves, changes in demand for and volatility of commodity prices of oil and

natural gas, failure to receive all required regulatory approvals for acquisition, the risk that the acquisition may not be

completed as contemplated or at all, legislative, regulatory and political changes, the risks discussed under "Risk Factors" in

Parex' annual information form for the year ended December 31, 2012 and other factors, many of which are beyond the control

of the Company. The risks outlined should not be construed as exhaustive. Although the forward-looking statements contained

in this document are based upon assumptions which Management believes to be reasonable, the Company cannot assure

investors that actual results will be consistent with these forward-looking statements. These forward-looking statements are

made as of the date hereof, and the Company assumes no obligation to update or revise them to reflect new events or

circumstances, except as required by law.

Statements relating to “reserves” are by their nature forward-looking statements, as they involve the implied assessment,

based on certain estimates and assumptions that the reserves described can be profitably produced in the future.

With respect to forward-looking statements contained in this presentation, the Company has made assumptions regarding:

future exchange rates; the price of oil and natural gas; the impact of increasing competition; conditions in general economic

and financial markets; availability of equipment; availability of skilled labour; current technology; cash flow; commodity prices;

production rates; timing and amount of capital expenditures; royalty rates; effects of regulation by governmental agencies;

future operating costs; receipt of all required regulatory approvals for the acquisition; successful completion of the acquisition;

and the Company's ability to obtain financing on acceptable terms. Management has included the above summary of

assumptions and risks related to forward-looking information provided in this presentation in order to provide shareholders

with a more complete perspective on the Company's future operations and such information may not be appropriate for other

purposes.

This is not an offer to sell or a solicitation of an offer to purchase securities by Parex. Before making an investment,

investors should refer to the Offering Documents for more complete information, including investment risks, fees and expenses

and should also thoroughly and carefully review Parex' public disclosure documents available on SEDAR at www.sedar.com

with their financial, legal and tax advisors to determine whether an investment is suitable for them.

Legal Advisory How to Reach Us

Parex Resources Inc. 1900 - 250 Second Street S.W.,

Calgary, Alberta, Canada T2P 0C1

Tel: 403-265-4800

Fax: 403-265-8216

Email: [email protected]

www.parexresources.com

Michael Kruchten Vice President, Investor Relations & Corporate Planning

22 Corporate Presentation May 2014