Optimal Taxation and Food Policy: Impacts of Food Taxes on Nutrient Intakes New Directions in...

28

Optimal Taxation and Food Policy: Impacts of Food Taxes on Nutrient Intakes New Directions in Welfare – OECD, Paris – July 2011 Thomas Allen (University of Perpignan, CIHEAM/IAMM-MOISA and INRA- ALISS) Olivier Allais (INRA-ALISS) Véronique Nichèle (INRA-ALISS) Martine Padilla (CIHEAM/IAMM-MOISA)

-

Upload

giles-mcdaniel -

Category

Documents

-

view

217 -

download

4

Transcript of Optimal Taxation and Food Policy: Impacts of Food Taxes on Nutrient Intakes New Directions in...

Optimal Taxation and Food Policy: Impacts of Food Taxes

on Nutrient Intakes

New Directions in Welfare – OECD, Paris – July 2011

Thomas Allen (University of Perpignan, CIHEAM/IAMM-MOISA and INRA-ALISS)

Olivier Allais (INRA-ALISS)

Véronique Nichèle (INRA-ALISS)

Martine Padilla (CIHEAM/IAMM-MOISA)

Outline of the presentation

• Background

• Research objectives

• Methodology

• Results

• Discussion

Background

• Increase in the prevalence of obesity and overweight in France since 1990 (Obépi, 2009);

• Higher risk of illnesses for which nutrition is an essential determinant, among the low-income groups (InVS, 2006)

• Nutrient-rich food are associated with higher diet costs and energy-dense food with lower costs (Darmon et al., 2007);

• Public Health authorities’ questioning and academic discussion on the prospect of potential « fat taxes ».

Research Question

How best to design a fiscal policy improving households’ allocation of goods in terms of nutrient adequacy

to recommendations?

Objective

Identify the optimal price conditions improving

households’ diet quality.

Review of the Litterature

• Food consumption economics : Estimation of a food demand system to capture price elasticities (Deaton et al.)

• Health studies : Definition of the public health question and tools of analysis (Drewnowski et al.)

• Public economics: Modelisation of the optimal taxation conditions (Ramsey, Murty et al.)

Optimal taxation modelRamsey's model (1927)

IpVVMax ,. s.c.

i

ii xtR

Taxes' objective: Raise funds.

Planner's ojective: Maximise social welfare under the constraint that tax revenue covers a given level of public expenditure.

Optimal taxation modelInverse elasticity rule

• Ramsey rule: The reduction in demand for each good, caused by the tax system, should be proportional for each good.

• Inverse elasticity rule: Optimal tax rates on each good should be inversely proportional to the good’s own–price elasticity of demand.

kkk

k

ep

t 1

Optimal taxation modelApplication to a nutritional policy objective• Taxes' objective: Transforming consumption behaviours.

• Planner's objectif: Maximise social welfare under the constraint that the overall diet quality of consumers' food basket reach a minimum level in terms of nutrient adequacy to recommendations.

IpVVMax ,.

s.c.

i

iiobj xqualiquali

i

ii xtR

Optimal taxation modelA nutritional quality/price ratio

• Optimal financing criteria : The optimal tax rates, for each good, are decreasing functions of their own-price elasticity of demand.

• Optimal adequation criteria: The optimal tax rates, for each good, are decreasing functions of their « nutritional quality/ price » ratio.

k

k

kkk

k

p

quali

ep

t

2

11

2

2

Optimal taxation modelSystem of simultaneous equations

,,,,, ** txpequaliftk

• The maximization program results in a system of equations where each optimal price variation, tk, :

• Solving this sytem requires to estimate a complete food demand system.

Where quali, p and x are vectors of the diet quality indicators, initial prices and quantities associated with each good and e the own and cross price elasticities.

Methodology – Demand model A conditionally linear system

• Selection of the Almost Ideal Demand System model (Deaton and Muellbauer, 1980):

• Iterated Least Square Estimator (Blundell and Robin, 1999).

iij

n

jijii PMpw

)ln(lnln1

Methodology – Pseudo-Panel Data• A panel of scanner data:

- 156 periods: 1996-2007

- 8 cohorts: Date of birth/Social status

- 27 food groups

• Group agregation:

Homogenous categories in terms of nutritional content (fruits/vegetables fresh/processed, snacks/already prepared meals, vegetable/animal fat, salty/sugary fat).

• Price construction:

24 clusters of price according to Localisation/Social status.

Methodology - Nutrient adequacy indicators

• MAR:

• LIM:

• SAIN:

1001

1

n

j jRNI

nutri

nMAR ij

i

100

1001

1

i

n

j

ENER

RNI

nutri

nSAIN

j

ij

i

10050

_

22

_

31533

1

ii

i

sugarAddfatSatNaLIM i

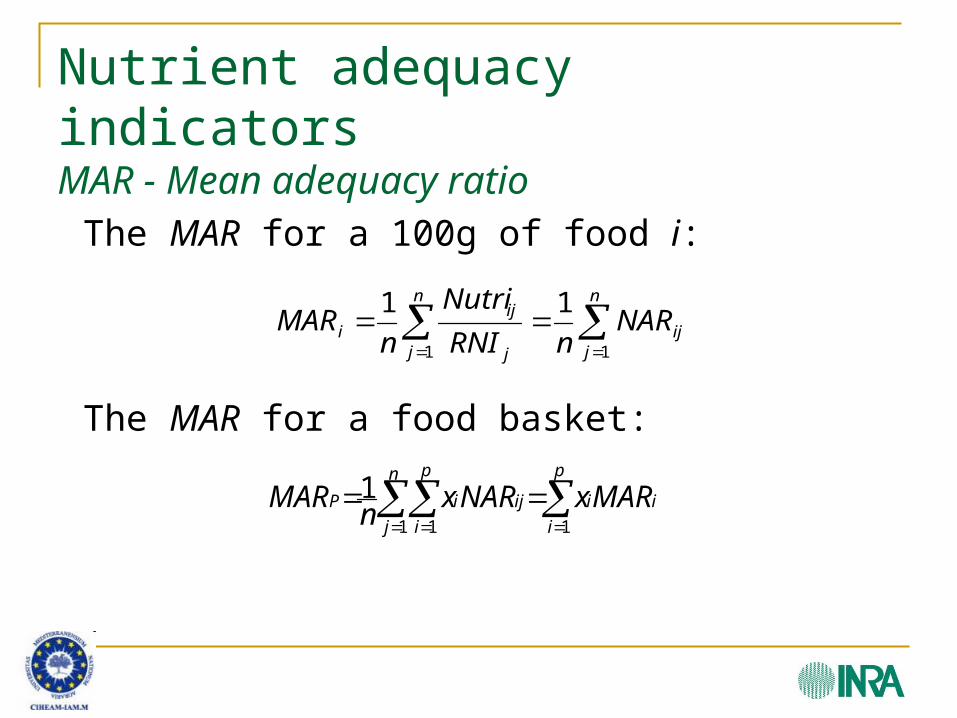

Nutrient adequacy indicatorsMAR - Mean adequacy ratio

The MAR for a 100g of food i:

The MAR for a food basket:

n

jij

n

j j

iji NAR

nRNI

Nutri

nMAR

11

11

p

i

ii

n

j

ij

p

i

iP MARxNARxn

MAR11 1

1

Nutrient adequacy indicatorsLIM – Score des composés à limiter

The LIM for a 100g o food i:

The LIM for a food basket:

n

jij

ijijiji LAR

n

sugarAddedfatSatNaLIM

1

1

50

_

22

_

31533

1

p

i

ii

n

j

ij

p

i

iP LIMxLARxn

LIM11 1

1

Nutrient adequacy indicatorsSAIN – Score d’adéquation individuel aux recommandations nutritionnelles

The SAIN for a 100g of food i:

The SAIN for a food basket:

n

j i

iji

ENERNAR

nSAIN

1

1

p

i

iiP

in

j P

ijp

i

iP SAINxENERENER

ENERNARx

nSAIN

11 1

1

Results – Price elasticty of demand

Uncompensated own-price elasticities

• Statistically significant.

• Negatives.

• Low and inelastic.

• Within usual range.

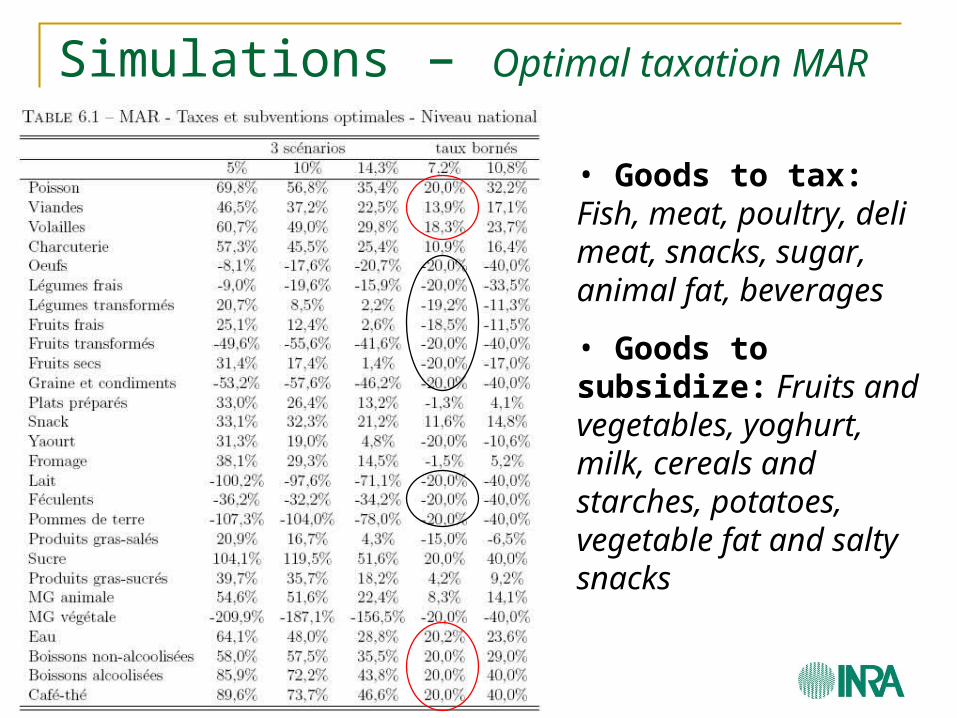

Simulations – Optimal taxation MAR

• Goods to tax: Fish, meat, poultry, deli meat, snacks, sugar, animal fat, beverages

• Goods to subsidize: Fruits and vegetables, yoghurt, milk, cereals and starches, potatoes, vegetable fat and salty snacks

Simulations – Optimal taxation LIM

• Goods to tax: Fruits and soft drinks, deli meat, snacks, mixed dishes, dairy products, cereals and starches, vegetable and animal fat, sweets and salty snacks.

• Goods to subsidize: Fish, meat, poultry, vegetables, potatoes, water coffee and tea and alcoholic beverages.

Simulations – Optimal taxation SAIN

• Improvements once calorie intakes are taken into consideration:

• Mixed dishes are to be taxed; water to be subsidized.

• Meat are more heavily taxed; fruits and vegetables more heavily subsidized.

Fiscal incidence

Welfare losses homogeneously spread over all income groups.

ConclusionResults and policy implications

• Theoretical result: A « diet quality/price » ratio and an augmented inverse elasticity rule;

• Empirical results: Mixed evidence supporting food taxation:

- Low price elasticities and high tax rates;

- Weak convergence on food groups to tax/ subsidize accross nutrient adequacy indicators.

Appendices

Use of the Lagragian Method to obtain a system of n+2 linear and non-linear equations and n+2 unknowns.

j i i

jijij

jjj R

p

xettxt

)0(

)0(

,)0( ...

0..2

2.

2

1, )0(

)0(

)0(

,)0(

)0(

,)0(

)0(

,

ki i

kiki

i k

ikii

i k

ikii x

p

xet

p

xet

p

xequalik

I

IpV c

,

j jjj

i i

jijij xqualiobj

p

xetquali 0...%.. )0(

)0(

)0(

,

with

Methodology – Optimal taxation (2)

Methodology – Optimal taxation (3)

i k

ikii

i k

ikiik pxet

pxeMARxk )0(

)0(

,)0(

)0(

,* .2

2.2

1,

• Using the Lagrangian method:

I

IpV c

,with

• And assuming a differentiable demand function:

i

i i

kikkk tpxexxk ., )0(

)0(

,)0(*

Methodology – Optimal taxation (4)

i

cii IpxMARMARMax ,.

s.c. i

cii CostIpxt ),(

• Increasing the MAR objective until the other constraints collapse is equivalent to:

• Maximisation Program:

Methodology – Optimal taxation (5)

IpVVMax c ,.

s.c.

• Maximisation Program:

i

cii ObjectIpxMAR .),(

i

cii CostIpxt ),(

)0(%.40, kk ptk