One Brief Shining Moment(um): Past Momentum … · One Brief Shining Moment(um): Past Momentum...

44

One Brief Shining Moment(um): Past Momentum Performance and Momentum Reversals Usman Ali, Kent Daniel, and David Hirshleifer * Preliminary Draft: May 15, 2017 This Draft: December 27, 2017 Abstract Following periods when momentum strategies have experienced their highest returns, stale momentum portfolios—defined as momentum portfolios formed at least 1 month earlier—experience their worse performance. Specifically, following periods of top-quintile momentum-performance, stale momentum portfolios reverse, earning cumulative returns of -41% from in years 1-5 post-formation. In contrast, following periods of bottom- quintile momentum performance, they earn +19%. A value-weighted trading strat- egy based on this effect generates a monthly Fama and French (1993) three-factor and Carhart (1997) four-factor alphas of 0.24% (t =2.50) and 0.30% (t =2.97), respectively. These patterns are confirmed in international data. These findings can be explained in part by style chasing on the part of momentum investors, but present a puzzle for existing theories of momentum. * MIG Capital, Columbia Business School and NBER, and Merage School of Business, University of Cali- fornia at Irvine and NBER. We thank Sheridan Titman for helpful comments.

Transcript of One Brief Shining Moment(um): Past Momentum … · One Brief Shining Moment(um): Past Momentum...

One Brief Shining Moment(um):

Past Momentum Performance and Momentum Reversals

Usman Ali, Kent Daniel, and David Hirshleifer∗

Preliminary Draft: May 15, 2017

This Draft: December 27, 2017

Abstract

Following periods when momentum strategies have experienced their highest returns,stale momentum portfolios—defined as momentum portfolios formed at least 1 monthearlier—experience their worse performance. Specifically, following periods of top-quintilemomentum-performance, stale momentum portfolios reverse, earning cumulative returnsof -41% from in years 1-5 post-formation. In contrast, following periods of bottom-quintile momentum performance, they earn +19%. A value-weighted trading strat-egy based on this effect generates a monthly Fama and French (1993) three-factor andCarhart (1997) four-factor alphas of 0.24% (t = 2.50) and 0.30% (t = 2.97), respectively.These patterns are confirmed in international data. These findings can be explainedin part by style chasing on the part of momentum investors, but present a puzzle forexisting theories of momentum.

∗MIG Capital, Columbia Business School and NBER, and Merage School of Business, University of Cali-fornia at Irvine and NBER. We thank Sheridan Titman for helpful comments.

Cross sectional equity momentum is the phenomenon that stocks that have earned the

highest (lowest) returns over the preceding 3-12 months continue to outperform (underper-

form) the market over the coming 3-12 months (Jegadeesh and Titman 1993). Zero investment

portfolios which take long positions in past winners and short past losers earn high Sharpe ra-

tios and have low correlations with macroeconomic variables, posing a challenge for standard

rational expectations models.

Behavioral asset pricing models generate momentum, value and reversal effects consistent

with empirical findings.1 In these models, prices show a pattern of initial underreaction and

continuing overreaction and slow correction that results in short-horizon momentum and long-

horizon reversal. Thus these models imply that sufficiently stale momentum portfolios—that

is momentum portfolios formed at least 12 months earlier—will on average earn negative

returns. Jegadeesh and Titman (2001) provide evidence that stale momentum portfolios do

indeed on average experience negative returns.

A recent literature has examined time-series variation in the profitability of momentum

strategies (Cooper, Gutierrez, and Hameed 2004, Daniel and Moskowitz 2016, Barroso and

Santa-Clara 2015, Stivers and Sun 2010). The evidence from these studies suggests that

the momentum premium is strongly dependent upon past-market returns, market volatility,

and the volatility of the momentum portfolio. However, to our knowledge, no study has yet

examined the conditional variation in the performance of stale momentum strategies, i.e., the

performance of momentum portfolios formed between 1-month and 5-years post-formation.

One interesting possibility, motivated by the idea that investors chase past style perfor-

mance, is that strong recent past performance of the momentum style will cause investors to

pile into momentum strategies, eventually resulting in underperformance of the strategy port-

folios. In this paper, we explore this issue by testing whether the long horizon performance

of momentum portfolios is negatively related to realized momentum strategy performance in

the recent past.

In particular, we study the relationship between stale momentum returns and a measure

of the recent performance of the momentum strategy which we call Past Momentum Perfor-

mance, or PMP. PMP is simply the return of a standard (12,2) momentum strategy over the

preceding 2 years (24 months). Our basic finding is that momentum portfolios formed in high

1See, for example, Barberis, Shleifer, and Vishny (1998), Daniel, Hirshleifer, and Subrahmanyam (1998)and Hong and Stein (1999).

1

PMP months (months when PMP is in the top 20% of all months in our sample) generate

strong negative returns and alphas post-formation. Strikingly, momentum portfolios formed in

low PMP months continue to outperform post-formation. Thus, the longer-term momentum

reversal documented by Jegadeesh and Titman (2001) is strongly state dependent.

We explore a set of possible behavioral hypotheses that might explain the dependence

of stale momentum performance on PMP. A baseline hypotheses based upon style chasing

predicts that the performance of the momentum style will tend to continue in the short run,

so that after the momentum strategy has done well it will tend to do well again. (Since our

hypotheses go somewhat beyond the style investing model of Barberis and Shleifer (2003), we

refer to these hypotheses as derived from the ‘style chasing approach’ rather than the style

investing model.) Underlying the style chasing approach is the behavioral hypothesis that,

following high momentum style performance, naive investors switch into this style as a result

of style return extrapolation, meaning that they buy winners and sell losers more heavily.

This trading pressure reinforces the strong performance of the momentum strategy, and will

temporarily cause better-than-usual momentum performance after the conditioning date if

such return chasers arrive gradually.

Following higher PMP, style chasing results in a stronger overpricing of past winners and

underpricing of past losers. As this mispricing is corrected, there is a longer-term reversal

of the momentum effect. So after high PMP, we should on average see negative returns to a

stale momentum strategy of buying past-winners and selling past-losers. In contrast, after low

PMP, investors switch out of the momentum style. Heavy selling of winners and buying of

losers induces underreaction in winner and loser returns. So, after low PMP, this hypothesis

implies longer-term positive returns to a stale momentum strategy. Putting these two cases

together, we expect reversal of momentum portfolios to be stronger when they are formed in

higher PMP months.2

However, similar predictions can apply even in a setting without direct over-extrapolation.If

2A qualification to the reasoning for the case of low PMP is that there are other forces which can ingeneral bring about reversal of momentum (i.e., negative returns to stale momentum portfolios). As modelledin settings that do not condition on PMP (Barberis, Shleifer, and Vishny 1998, Daniel, Hirshleifer, andSubrahmanyam 1998, Hong and Stein 1999), momentum is associated with overreaction to news that eventuallycorrects. In consequence, there is reversal of momentum. If such a setting is viewed as the unconditionalbaseline (i.e., not conditioning on PMP), then the prediction of strong reversal of momentum after highPMP is reinforced, but the prediction that momentum continues (i.e., that even stale momentum strategiesearn positive returns) is weakened. For example, it could be that after low PMP, there is still reversal ofmomentum, but owing to style chasing, the reversal is weaker than usual. Regardless, we expect greaterreversal of momentum returns when PMP is higher.

2

investors naively update their confidence in a momentum investing strategy in response to

historical momentum performance (ie., to PMP), then when realized momentum returns are

strong, their confidence in the strategy increases, amplifying the immediate momentum re-

turns, but leading to eventual poor performance of stale momentum portfolios.3

Motivated by these ideas, we examine the relationship between PMP and stale momentum

portfolio performance. We document several novel effects. We first show that over the full

CRSP sample there is, on average, very little tendency of momentum to reverse after control-

ling for the value effect.4 This finding is in contrast with Jegadeesh and Titman (2001), who

document that, over a shorter sample, equal-weighted momentum portfolios exhibit strong

reversals even after controlling for the value effect.

Turning to our main result, we demonstrate a strong negative relationship between PMP

and stale momentum portfolio returns. Again, our hypothesis is that the long-horizon perfor-

mance of momentum portfolios depends on the performance of momentum leading up to the

portfolio formation date. If the momentum style has recently done well (i.e., if PMP is high),

we expect to see high momentum stocks become more overpriced, leading to longer term re-

versal of the momentum portfolio. To test this, we rank the momentum portfolio formation

months in our sample into quintiles based on PMP and then examine the performance of

momentum portfolios formed in that month for up to five years after the formation date. Our

basic finding is that, the (stale) momentum portfolio returns are strongly negatively related

to PMP as of the formation date.

Specifically, momentum portfolios formed in quintile 1 (i.e, low PMP) months exhibit

weak continuation post-formation, earning a cumulative return of 19% in the five years post-

formation. However, in sharp contrast, momentum portfolios formed in quintile 5 months

lose 42% of their value over the five years post formation. We label this strong reversal of

momentum formed in high PMP months the PMP effect.

Similar results obtain after controlling for exposure to the Fama-French factors; the dif-

ference in cumulative five-year alphas of stale momentum portfolios formed in Quintile 5 and

3As discussed in Section 2, owing to self-attribution bias, we expect this effect to be asymmetric withrespect to high versus low PMP. This asymmetry argument has a parallel to overreaction and correction effectsof attribution bias modelled by Daniel, Hirshleifer, and Subrahmanyam (1998). Here, however, attributionrelates to to beliefs about the momentum investing strategy rather than beliefs about individual stocks.

4Several behavioral theories imply that momentum will tend to reverse in the long run (Daniel, Hirshleifer,and Subrahmanyam 1998, Barberis, Shleifer, and Vishny 1998, Hong and Stein 1999). However, these papersdo not examine whether there will be incremental reversal after controlling for the value effect.

3

Quintile 1 months is 40%.5 In particular, the estimated alpha of momentum portfolios formed

in the highest quintile PMP months is negative in each of the post-formation years 2-5. In

contrast, in each of the post-formation years 2-5, almost all of the alphas of momentum portfo-

lios formed in Quintile 1-4 months are economically modest and statistically insignificant. In

addition, we show that PMP forecasts reversals for both industry and stock-specific momen-

tum portfolios, although the results are stronger for industry momentum. We also find that

PMP predicts extreme industry price run-ups that eventually crash. Greenwood, Shleifer, and

You (2017) examine whether past industry returns predicts industry crashes, but they do not

consider PMP.

The finding that momentum portfolios that are formed at times of high PMP reverse

strongly is consistent with a prediction of the style chasing approach. However, another possi-

ble implication of this approach is that after high PMP, style chasers will pile into momentum

portfolios during the year after stocks are identified as high or low momentum, resulting in

strong short-term performance of momentum portfolios. In contrast, we document that PMP

over the same conditioning period does not positively predict short horizon performance of

momentum portfolios. Indeed, the point estimate suggests that the relation between PMP

and short horizon momentum performance is slightly negative.6 In other words, after high

PMP, a newly formed momentum portfolio portfolio does not earn higher-than-usual abnor-

mal returns over the next 12 months. This suggests that the relationship between PMP and

momentum reversals that we document is not driven by style chasers piling into momentum

portfolios in the 12 months after the portfolios are formed.

This does not rule out the possibility that investors chase momentum style returns at

a higher frequency. If so, the apparent overvaluation of the momentum portfolio that is

identified by high PMP must emerge before the end of the momentum portfolio formation

period (since after high PMP we do not observe high post-formation momentum returns).

This could reflect investors flowing into shorter-term momentum strategies (e.g., 3-month

or 6-month momentum portfolios), so that any continuation of momentum performance is

complete subsequent to the end of our 12-month momentum formation period. Still, our

findings do not fit well with style chasing at an annual frequency as an explanation of the

5Our tests control for the differences in valuation ratios of momentum portfolios across the five PMPquintiles by estimating separate Fama-French loadings for each quintile.

6However, PMP is not useful for timing standard momentum strategies. After controlling for past mar-ket return (which forecasts momentum crashes), we do not find a statistically or economically significantrelationship between PMP and short horizon momentum returns.

4

PMP/momentum reversal effect that we document.

Furthermore, the reversals that we identify extend much too long after the conditioning

date to be explained by simple style chasing. Style chasing implies that these reversals should

be complete within a year, since stocks in a winner (loser) portfolio of the momentum strategy

do not necessarily remain winners (losers) 12 months later. So a style chaser who has recently

been attracted to momentum would tend to exit from any given momentum portfolio within

about 12 months after formation. So style chasing does not provide a full explanation for our

main result.

We perform a number of robustness checks. Our basic tests use full sample information

to rank months based on PMP, potentially introducing a look-ahead bias. Although it is not

obvious why this would induce the effects that we find, we verify that similar results hold in

out-of-sample tests which perform the PMP ranking of months using only information available

at the time. In addition, we replicate our US tests in eight developed markets outside the US

that have reasonably large cross-sections of large, liquid stocks. We find that a strong inverse

relationship between PMP and the performance of stale momentum strategies is present for

almost all of the countries we examine..

We show that cross-sectional portfolio strategies designed to exploit the PMP effect ex-

hibit strong abnormal performance. As with our other tests, the portfolio strategies exploit

the predictability of stale momentum portfolios, that is portfolios formed on the basis from

the 11-month cumulative return of individual firms, lagged between 2 months and 5 years,

rather that just one months. A long-short portfolio designed to exploit the stale-momentum-

reversal effect that we observe following high-PMP months—one that buys stale-loser and

sells stale-winner portfolios formed only in PMP Quintile 5 months—earns monthly 3- and

4-factor alphas of 0.52% (t = 3.90) and 0.25% (t = 1.86). The alphas of such strategies de-

cline monotonically with the past-momentum-performance measured as of the formation date.

Furthermore, a strategy which exploits the continuation of momentum portfolios formed in

low PMP months and reversal of momentum portfolios formed in high PMP months generates

still stronger performance, with a four-factor alpha of 0.30%/month (t = 2.97). In contrast,

an unconditional stale momentum strategy which pools all months generates an insignificant

4-factor alpha of 0.04%/month (t = 0.67).

***We are not the first to perform empirical tests motivated by the style chasing approach.

Using Morningstar classifications along size and value dimensions and the returns of mutual

5

funds in these styles, Teo and Woo (2004) find that stocks in styles with poorly performing

funds do well in the future. Froot and Teo (2008) examine size, value/growth, and sector as

styles. They find that own fund style returns and flows over the past 1-4 weeks positively

forecast weekly stock returns, while opposite fund style returns and flows negatively forecast

returns. We focus on return predictability at longer time horizons. Our paper also differs in

studying time-variation in the performance of stale momentum portfolios. Our focus is on

understanding the relationship between past momentum performance and the future perfor-

mance of momentum portfolios rather than on testing the style investing model (which is just

one possible motivation for such conditional effects). Our approach also differs in focusing on

past strategy performance rather than past fund performance.

This literature focuses on how individual investors respond to the performance of styles

such as value and growth. Our focus is on momentum, and given the importance of insti-

tutional investors for price-setting, we perform tests of whether institutional traders engage

in momentum style-chasing based upon PMP.7 We define momentum traders as institutions

with a history of buying winners and selling losers, and contrarian traders as institutions

with a history of the reverse behavior. We find that following high PMP periods, momentum

traders substantially increase their holdings of recent winners and decrease their holdings of

recent losers. In contrast, there is no association between PMP and the subsequent trading of

contrarian investors (institutions with a history of selling winners and buying losers). These

findings suggest that momentum traders (chasers of past returns of individual stocks) tend to

be chasers of past style, whereas contrarian investors (anti-chasers of past stock returns) are

not heavy style return chasers. This in turn suggests that the behavior of momentum-trading

institutional investors may help explain the PMP effect. However, as discussed earlier, our

return tests indicate that simple style chasing is unlikely to fully explain our findings.

Finally, we conduct a set tests to ensure that the PMP effect is distinct from previously

identified predictors of momentum returns. Previous studies show that negative market re-

turns, high volatility, and high volatility of momentum strategy are followed by momentum

crashes. To control for past market returns, we exclude all months for which the past two-year

market return is negative. We find that the PMP effect actually becomes stronger once down

market months are excluded from the sample. We also find that the component of PMP that

is orthogonal to market and momentum portfolio volatility predicts strong momentum rever-

7Such behavior could reflect the traits of fund managers, or the traits of the clienteles of the funds.

6

sals. Furthermore, we show that using characteristic-adjusted returns to measure abnormal

performance instead of alphas does not affect the main conclusions. Finally, we show that our

results are not driven by differences in momentum characteristic (formation period difference

between returns of winners and losers) across the different PMP quintiles. In other words,

our results are not driven by winners being bigger-than-usual conditioning-period winners, or

losers being bigger-than-usual losers during high PMP periods.

We consider several possible explanations for these findings. As discussed above, style

chasing provides only a partial possible explanation for the findings. We draw the same

conclusion (discussed in the next section) about an explanation based upon bias in investor

self-attribution. We conclude that the PMP effect remains a puzzle. The finding that mo-

mentum portfolios formed in high PMP months eventually reverse strongly suggests that in

high PMP months, momentum formation period returns are at least in part overreaction.

So a full explanation for the puzzle seems to require that in periods of high PMP, a greater

than usual proportion of winner-loser conditioning period returns derives from investor over-

reaction. Our findings on institutional trading suggest that momentum-trading institutions

contribute to such overreaction.

1 Motivation and Hypotheses

As discussed in the introduction, the style chasing approach (building intuitively on the style

investing model of Barberis and Shleifer (2003)) suggests interesting hypotheses about how

past momentum performance should predict returns both fresh and stale momentum strate-

gies. The style investing model is based on the hypothesis that investors overextrapolate past

style returns in forecasting future style returns. For example, if growth stocks have recently

done well, style investors expect growth stocks to do well in the future. As Barberis and

Shleifer show, this can lead to ‘style chasing’ wherein overextrapolating investors buy into a

style when that style has provided high recent historical returns, leading to at least an initial

continuation in style returns.

It is especially interesting to test for style effects on momentum, because momentum is an

inherently active, high turnover strategy. The kind of investors who are potentially attracted

to aggressive styles are likely to be sensation-seeking investors (Grinblatt and Keloharju 2009)

who are not deeply and philosophically attached to a single style. This suggests that style

7

effects may be especially strong for the momentum style.

The style chasing approach discussed above suggests that after high PMP, investors become

enthusiastic about the momentum style, leading to buying of winners and selling of losers,

and therefore to stronger-than usual performance of the momentum style. Similarly, weak

momentum performance should follow low PMP periods. By the same token, after high PMP,

the stronger-than usual price reaction in winner and loser portfolios caused by style chasing

should lead to stronger reversal as these portfolios become stale.8

A more subtle implication of style chasing is that for momentum portfolios formed in

high-PMP months, any style-chasing reversal of momentum performance should occur within

about a year after formation date. This is because past winner (loser) stocks on the long

(short) side of a momentum portfolio do not necessarily remain winners (losers) 12 months

later. So investors who were attracted to a 12-month winner as a result of high PMP will, on

average, no longer have any special reason to be attracted to it 12 months later.9

The style chasing approach is based upon extrapolation of past style returns. An alter-

native approach would be to argue that investors believe that they receive what they regard

as private informative signals about the effectiveness of different styles. For example, a group

of investors might receive a signal suggesting that momentum trading is profitable or unprof-

itable (so that contrarian trading is profitable). This is somewhat analogous to the approach

of Daniel, Hirshleifer, and Subrahmanyam (1998), in which investors are overconfident about

signals they receive about particular securities.

In their model, investors shift their beliefs about the quality of their signals in a self-

enhancing fashion owing to bias in self-attribution. When their style makes money, they

strongly update in favor of believing that their signal was highly accurate, and therefore

become strongly reinforced in their faith in the style. In contrast, when their style loses

8These predictions are not implications of the Barberis and Shleifer model; their paper does not discussthe momentum style. In their model, every stock falls into one of two ‘twin’ styles. For example, one couldapply the model to assign winners to a winner style, and losers to a loser style. This definition of styles doesnot, however, seem closely aligned with how investors view momentum trading in practice. We therefore definethe momentum style to be the strategy of buying winners and selling losers. So in what we call the style-chasing approach, we view style investors as over-extrapolating the returns of the winner-minus-loser portfolioin deciding whether to invest more heavily in the momentum style. We contrast with a ‘twin’ contrarian style,defined as trading in the reverse direction. Since predictions about these styles were not made in Barberis andShleifer (2003), we make no claim to be testing their model.

9The momentum effect suggests that past winners will tend to perform well going forward, which tends tocause such stocks to be part of the momentum winner portfolio in subsequent periods. However, this effect isnecessarily small, since the fraction of realized returns explained by momentum is empirically small (Jegadeeshand Titman 2001).

8

money, they update against their signal only modestly, since they do not like admitting to

themselves that they have a low-quality signal. So they only shift modestly away from their

style.

As applied to the momentum style, this suggests that after high PMP, momentum style in-

vestors should become more confident in their enthusiasm for momentum, resulting in stronger

overvaluation of the winner-minus-loser portfolio. As a consequence, eventual performance of

stale momentum portfolios should be very poor. In contrast, and asymmetrically, after low

PMP, momentum style investors will withdraw only modestly from the momentum style be-

cause they hate to admit to themselves that they were wrong. So there is only modest

undervaluation of the winner-minus-loser portfolio. In consequence, eventual performance of

stale momentum portfolios should be good, but not exceptionally good (compared to the case

of no conditioning on PMP).

The basic reasoning about how high PMP should be associated with future momentum

performance is reinforced by consideration of adherents to the contrarian style. Such adher-

ents gain confidence in contrarianism after low PMP and lose confidence after high PMP.

This reinforces the effect of momentum traders after high versus low PMP. However, the rea-

soning for the asymmetry of the PMP effect is reversed for contrarian style investors. For

such adherents, bias in attribution causes them to gain confidence in contrarianism especially

strongly after low PMP. This asymmetrically causes weakening in any typical overreaction of

the winner-minus-loser portfolio (or even causes underreaction in it). So if contrarian style

investors predominate, we expect that the effect of high versus low PMP on momentum style

returns and on stale momentum returns will be especially strong after low PMP.

Overall, the predicted direction of effect for asymmetry depends on how many investors

are engaged by the momentum style versus the contrarian style.10 Momentum investing (with

a conditioning period of about 12 months) has a very high profile among professional and even

individual investors. For example, many ‘smart beta’ funds state that they trade based upon

10The answer to this question does not automatically follow from market clearing considerations. It istrue that for every investor who follows a momentum strategy there must be other investors trading in theopposite direction. However, such opposite-trading investors are not necessarily adherents of contrarianismas an investment philosophy, and do not necessarily identify themselves as contrarians. For example, supposethere is a set of rational investors who do not over- or under-extrapolate the style returns. Instead, as instandard models of portfolio optimization, their demand for any given security is a decreasing function ofits price (for a given probability distribution of its fundamentals). Then if high PMP drives up style chasingdemand for the winner-minus-loser portfolio, this reduces demand for that portfolio by rational investors. Thisincremental ‘contrarian’ demand is not driven by any change in adherence to the contrarian philosophy, it issimply a rational response to price variation.

9

momentum. So we view the prediction for asymmetry as clear—that the effects of momentum

traders dominate. In other words, the effect of PMP on momentum and stale momentum

performance should be especially strong after high PMP.

The arguments provided here are very different from the argument in Daniel, Hirshleifer,

and Subrahmanyam (1998) for why the momentum anomaly exists. The argument here is

about momentum and reversal in momentum style return performance, not individual stock

return performance. In other words, it involves predictions about the returns on a new winner-

minus-loser portfolio in periods after previous winner-minus-loser portfolios have done well

versus poorly. Similarly, the style-investing approach implies what Barberis and Shleifer call

“style momentum,” in which there is positive autocorrelation in style performance—a different

concept from momentum in individual stock performance. As extended to the momentum

style, this is a prediction about momentum in the momentum style, not a prediction about

the basic existence of return momentum.

2 Data

The main dataset used in this paper is the stock return data from CRSP. Our sample in-

cludes all common stocks (CRSP share codes 10 and 11) traded on NYSE, NYSE MKT

(formerly AMEX), and Nasdaq from 1926:01 to 2014:12. We obtain accounting data from

the CRSP/Compustat merged database, and factor returns from Ken French’s website. The

data for international tests is from S&P Capital IQ and institutional ownership data is from

Thomson Reuters. We discuss these data in more detail later in the paper.

Following Jegadeesh and Titman (2001), we exclude stocks with price below $5 and stocks

with market capitalizations below the 10th percentile size breakpoint (using NYSE size break-

points) at the time of portfolio formation. At the end of each month, we rank stocks into

deciles based on their cumulative return over the past 12 months, skipping the most recent

month. We then construct a long-short Winner-Minus-Loser or WML portfolio that is long

the value-weighted portfolio of top-decile “Winners” and short the value-weighted portfolio

of (bottom decile) “Losers.” Portfolios are held for one month. This procedure results in a

monthly time-series of WML returns.

We calculate past momentum performance in month t, PMPt. as the average monthly

10

return of WML over the past 24 months:

PMPt =1

24

0∑τ=−23

WMLt+τ .

We then rank each month t of the 973 months in our sample11 into quintiles based on PMPt

and examine the performance of WML portfolios formed in different PMP quintile months

over the subsequent five years.

Table 1 reports a set of characteristics of the PMP quintiles. First, note that there is

considerable variation in momentum performance over time; the average PMP across the

bottom quintile (rank 1) months is -0.4%/month, while the average across the rank 5 months

is 3.1%/month. Interestingly, the best momentum performance is associated with lower market

returns, in that the average past 1-year market excess return for PMP-rank-5 months is -4.4%.

Not surprisingly, both high and low PMP quintile months are associated with higher market

volatility in the recent past.

Figure 1 plots the time-series of PMP. While the mean PMP value is high, there is con-

siderable variation in momentum performance over time. The highest level of PMP in our

time series is 6.9%/month, achieved in February 2000, just before the market peak in March

2000. The lowest level of PMP is achieved at the end of June, 1934, almost exactly two years

following the start of a major momentum ‘crash’ (see Daniel and Moskowitz 2016) and is

-6.2%/month.

3 Empirical Analysis

Figure 2 illustrates our key finding: the strong negative relationship between PMP and the

long horizon performance of stale momentum portfolios, defined as portfolios formed at least

one year earlier. Panel A plots the average cumulative excess 5-year returns of the value-

weighted momentum portfolios formed in different PMP quintile months as well as in all

11The PMP time series is from 1928:12 (first month for which PMP can be calculated) to 2009:12. We endin 2009 since we examine returns five years after portfolio formation.

11

months. Specifically, we plot12:

1

Nq

∑t∈Tq

[τ∏s=1

(1 +WMLtt+s + rf,t+s)−τ∏s=1

(1 + rf,t+s)

],

as a function of τ , where:

• WMLtt+s is the return in month t+ s to the momentum portfolio formed in at the start

of month t (i.e., which was formed s months earlier). Note that WMLtt is conventional

“fresh” momentum portfolio.

• rf,t+s is the riskfree rate in month t+ s.

• Tq denotes the set of months that are in PMP quintile q and Nq the number of months.

The yellow line (labeled “ALL”) confirms the finding of Jegadeesh and Titman (2001) that

momentum profits (raw returns) reverse in years 2-5 after portfolio formation—the cumulative

return of the portfolio becomes negative at the end of year five.13Figure 2 also reveals a strong,

monotonically declining relationship between post-formation returns and PMP. Momentum

portfolios formed in PMP Quintile 5 months lose over 42% of their value in five years.14

Panel A of Figure 2 also shows that momentum portfolios formed in Quintile 1 months

do not exhibit any reversals. This is quite surprising since this portfolio loads negatively on

HML, which is known to have a high mean return.

Momentum portfolios load negatively on the value factor and the spread between the

valuation ratios of winners and losers is much wider in Quintile 5 months. Therefore, the

results in Panel A could just reflect the long-run underperformance of growth stocks relative

to value stocks. However, Panel B shows that this is not the case. Panel B plots the cumulative

Fama and French (1993) three-factor alphas (we describe the calculation of alphas below) for

12This is the average cumulative return on an implementable strategy of, at the start of month t+s, puttingVt+s−1 (the value of the portfolio at that time) into the riskfree asset. In addition, Vt+s−1 is invested in thelong-side of the zero-investment portfolio WMLt, which is financed by shorting Vt+s−1 of the short size ofWML. At the end of month t+ s, the sizes of the long- and short-positions are rescaled to a value of Vt+s, sothat the leverage of the portfolio remains at 1. This methodology assumes that there are no margin calls, etc.,except at the end of each month. These calculated returns do not incorporate transaction costs. See Danieland Moskowitz (2016) for more details.

13However, as we show below, the year 2-5 decline is not statistically significant.14Interestingly, momentum portfolios formed in PMP Quintile 5 months do not generate positive returns

even in the first post-formation year. However, this result can be explained by previous findings. Once wecontrol for past market return and exposure to the value factor, these portfolios generate positive alphas inthe first post-formation year (see Table 7).

12

the momentum portfolios for portfolios formed in each PMP quintile. After controlling for

Fama-French factors, momentum portfolios formed in Quintile 5 months continue to exhibit

strong reversals in post-formation years 2-5, while momentum portfolios formed in Quintile

1 months exhibit continuation. Although the spread between top and bottom quintile 5-year

cumulative alpha is smaller than the corresponding spread in raw returns shown in Panel A,

it is still economically very large—almost 40%.

Panels A and B of Figure 3 plot the cumulative alphas of the past-winner and past-loser

portfolios, respectively. For PMP Quintile 5 months, the reversals in post-formation years 2-5

are about twice as strong for the Winner portfolio as for the Loser portfolio. These results

are consistent with the hypothesis that the overvaluation of the Winner portfolios is harder

to arbitrage owing to short-sale constraints.

An interesting question is why the effect of PMP is especially strong in Quintile 5 months

relative to Quintile 1 months. If higher PMP is associated with stronger overreaction, resulting

in long-term reversal for the stale momentum portfolios, why don’t we see the opposite effect

for Quintile 1 PMP, i.e. strong continuation in stale momentum portfolios? One possibility is

that for some reason the PMP effect inherently derives mainly from winners rather than losers

(perhaps for reasons unrelated to short sales constraints). If so, then in high PMP months

the reversal effect will be strong, owing to the fact that the Winner portfolio is predicted to

have low returns, which is hard to arbitrage owing to short sale constraints. In contrast, in

low PMP months, for stale momentum portfolio to earn high return-continuation returns, the

winners would need to earn high returns, which could be arbitraged away without going short.

Figures 4 and 5 provide two alternative depictions of the PMP effect. Figure 4 plots, as a

function of the portfolio formation date, the cumulative return (in excess of the riskfree rate)

of the momentum portfolio from 1-60 months post-formation—this is the line labeled R 1 60—

and in addition the PMP up through that date. Panel A does this for the full sample, and

Panel B for the subsample beginning in 1982. Both panels show that there is a fairly strong

negative correlation between PMP as of the portfolio formation date and the subsequent stale

momentum portfolio return. This correlation is particularly strong in the post-1982 period. As

we discuss in more detail in Section 3.6, the 1982-1997 subsample is interesting, as Jegadeesh

and Titman (2001) find virtually no evidence of reversal of momentum (without conditioning

on PMP) in this period.

One more view of these data is provided in Figure 5, which is a scatterplot with PMP on

13

the x-axis and the cumulative return on the stale momentum portfolio from 1-60 months post-

formation on the y axis. Each dot represents one outcomes (or, alternatively, one monthly

formation date). This scatterplot again suggests a moderately strong negative relationship

between PMP and the long-horizon returns of the stale momentum portfolios. There are also

some extreme observations both in terms of PMP and in terms of the subsequent long-horizon

returns. Figure 4 shows that the large stale momentum returns of greater than 100% occur for

formation dates in the 1995-1996 period, where these stale momentum returns overlap with

the ‘tech-bubble’ period. The strong negative PMP realizations (of < 2%/month) occur for

formation dates just before 1935, following the extreme-negative momentum realizations in

June and July of 1932 (see Daniel and Moskowitz 2016).

Table 2 reports the average monthly returns (in Panel A) and three-factor alphas (in

Panel B) of the stale-momentum portfolios. Each row presents the result for momentum

portfolios formed in a different PMP quintile month, and each column presents the average

return (alpha) for each of five post-formation years. The final column presents the the average

return or alpha for the entire five year period.15 For example, for each momentum portfolio

formed in a PMP-Rank 1 month t, we calculate its average monthly return (alpha) in months

t+1 through t+12 (post-formation year 1), and report this number as the Rank 1/Year 1

return (alpha). The average of all post-formation returns in months t+1 through t+60 is

reported in the All column.

The row labeled All months presents the average monthly returns for the stale momentum

portfolios formed in any month (ie., ranks 1-5), and the row 5-1 gives the difference between

the Rank 1 and Rank returns (alphas). The t-statistics presented are based on Newey and

West (1987) standard errors to account for serial dependence. To calculate alphas, we estimate

a separate set of Fama-French loadings for each event month, t+ 1, t+ 2, . . . , t+ 60, and PMP

quintile pair, and calculate alpha as the intercept plus the average residual. Our results are

stronger if we estimate unconditional loadings by pooling all PMP months together since,

not surprisingly, momentum portfolios formed in Quintile 5 months load more negatively on

the value factor and also since they load more negatively on the market factor compared to

portfolios formed in other months.

Panel A of Table 2 shows that post-formation momentum returns are strongly negatively

15In untabulated results, we examine returns up to 10 years after portfolio formation, and find no evidenceof reversals in years 6 through 10 either unconditionally or conditioning on PMP.

14

related to PMP. In the first post-formation year, momentum portfolios formed in Quintile 1

months generate a highly significant return and the returns decrease monotonically as quintile

ranks increases to 5. In fact, momentum returns are actually negative in the first post-

formation year for Quintile 5 months, though not significantly so. The difference between

top and bottom quintile returns is -1.21% per month and significant at the 5% level. The

same declining pattern shows up in years two through five. For Quintile 1, average returns

are economically and statistically close to zero in all four years. For Quintiles 2-4, almost

all average returns are statistically indistinguishable from zero except for Quintile 3 and 4

returns in year 5, which are negative and significant. In contrast, Quintile 5 returns are all

economically very large, ranging from -0.53% to -1.34% per month, and all are significant—

two at the 1% level and two at the 10% level. The differences between top and bottom quintile

returns are also economically and statistically large in years two through five.

Panel B of Table 2 reports the average monthly alphas. The row labeled “All months”

shows that over the full CRSP sample from 1928-2014, momentum reversals are quite weak

after controlling for Fama-French factors—only the year 5 alpha is negative, -0.17% per month

(t = −2.10). Almost all of this effect is coming from momentum portfolios formed in PMP

Quintile 4 and 5 months. These findings add nuance to the usual understanding that momen-

tum profits reverse in the long run. We find that almost all of their reversals are explained

by their negative loadings on MKT and HML factors and the rest are explained by Quintile

5 months.16

For Quintile 1 months, the alphas are all positive in years two through five, although they

are not statistically significant. For Quintiles 2 to 4, only one other alpha, year 3 alpha for

Quintile 3, is meaningfully negative -0.32% per month (t = −1.92). In sharp contrast, reversals

are strong for Quintile 5—the alpha in each of the four post-formation years 2-5 is negative,

and is statistically significant in years 2 and 5. The differences between Quintile 5 and Quintile

1 alphas are also all negative, and are again significant at the 1% and 10% levels in year 2 and

year 5, respectively. These results strongly support the hypothesis that momentum stocks in

periods of high recent momentum strategy performance become overvalued and on average

gradually exhibit reversals during post-formation years as the mispricing is corrected.

16This does not contradict models which predict overvaluation and therefore reversal of momentum per-formance, since HML is built based on book-to-market, which is, in several behavioral models, a proxy formisvaluation.

15

3.1 Industry versus Residual Momentum

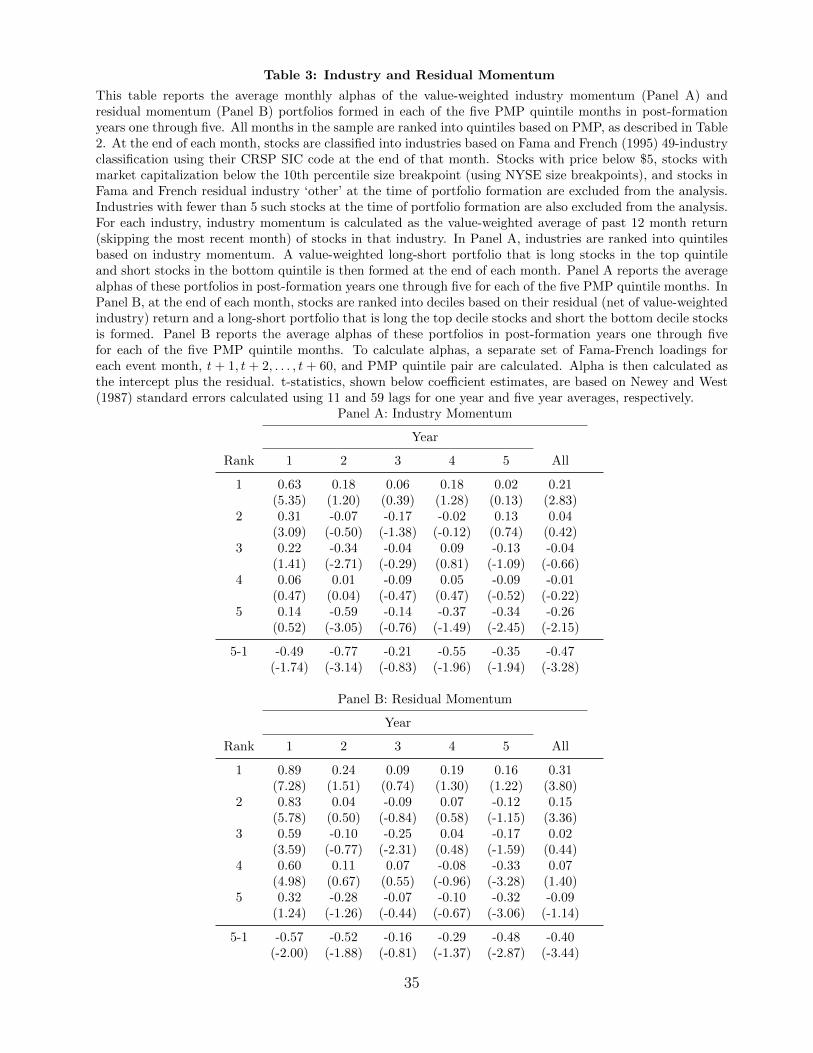

Previous studies document momentum effects for both the industry and firm-specific com-

ponents of stock returns (Moskowitz and Grinblatt 1999, Asness, Porter, and Stevens 2000,

Grundy and Martin 2001). We next test whether the time-variation in stale momentum

portfolio reversals that we observe are driven by industry or stock-specific momentum.

To form residual momentum portfolios, we rank stocks into deciles based on their residual

(net of value-weighted industry) return over the past 12 months, skipping the most recent

month. We then form a value-weighted long-short residual momentum portfolio that is long

the top decile and short the bottom decile.

Table 3 reports the average alphas of industry and residual momentum portfolios during

post-formation years one through five for each of the five PMP quintiles. Although both

industry and residual momentum portfolios exhibit reversals during PMP Quintile 5 months,

reversals are about twice as strong for industry momentum. Industry momentum portfolios

generate statistically significant alphas of -0.59% and -0.34% per month in post-formation

years 2 and 5, respectively. For residual momentum portfolios, the alphas are negative in post-

formation years two through five, but only significantly so in year five. The differences between

extreme quintile alphas are negative in all post-formation years and generally significant for

both residual and industry momentum.

In a recent study, Greenwood, Shleifer, and You (2017) find that sharp industry price

run-ups predict a higher probability of industry crashes, although the run-ups do not (un-

conditionally) predict low future average returns. They also identify various attributes of the

price run-ups, such as volatility, turnover, magnitude of the run-up, and issuance that predict

eventual crashes. We find that PMP has strong power to predict such crashes; 65% of the price

run-ups that eventually crash in their sample are identified in PMP Quintile 5 months and

only 26% of the price run-ups that don’t crash are identified in PMP Quintile 5 months. In

addition, our results on industry momentum indicate that PMP has the ability to forecast low

future returns of high momentum industries in a broader sample (one not limited to extreme

price run-ups).

16

3.2 Out-of-Sample Estimation

The results presented so far use the full sample distribution of PMP to rank months. We

next rank months into PMP quintiles using only the information available at each point in

time and test whether PMP is related to momentum reversals. Specifically, at the end of each

month starting in 1938:12, we use an expanding window from 1928:12 onwards to calculate

a historical distribution of PMP and assign each month to a PMP quintile according to this

distribution.

Table 4 shows a strong inverse relationship between PMP and momentum reversals in

post-formation years two through five. For PMP Quintiles 1-4, only Quintile 4 returns and

alphas in year 5 are significantly negative. All other returns are alphas are not significantly

negative (even at the 10% level) and some are actually positive and significant. For Quintile

5, all of the raw returns are negative in years 2-5 and significant in three of these years and

the alphas are negative and significant in years two and five.

3.3 International Tests

To further evaluate the robustness of our results, we next examine the extent to which the pmp-

related patterns we see in US data also show up in markets outside the US. Our international

sample consists of stocks in the S&P BMI Developed Markets Index starting in 1989:07. We

exclude the smallest 10% of stocks in each country (similar to our US tests) to focus on

large, liquid stocks. We only include those countries in our tests that have at least 75 stocks

per month on average to ensure that the long-short momentum portfolios are reasonably

well diversified. The stock return and market capitalization data are from S&P Capital IQ.

Country-level factor returns are from AQR’s data library.

Based on these data requirements, we end up with eight non-US universes for our inter-

national tests.17 Japan has the largest cross-section of stocks with 1,208 stocks per month on

average; Switzerland has the smallest with 91 stocks per month. At the end of each month

from 1989:07 to 2009:12, we rank stocks in each country excluding Japan and UK into quin-

tiles based on their cumulative return over the past 12 months, skipping the most recent

month, and construct a value-weighted long-short portfolio for each country that is long the

top quintile stocks and short the bottom quintile stocks. Since the cross-section of stocks

17Canada also has at least 75 stocks per month, but the market capitalization data for Canada starts in1998 so we do not include Canada in our tests.

17

is much larger in Japan and UK, we rank stocks into deciles similar to the US tests—the

long-short momentum portfolio is long the top decile and short the bottom decile. We hold

the portfolios for one month. This approach yields a time-series of monthly momentum factor

returns for each country. For each country and each month, we calculate PMP as the average

momentum factor return over the past 24 months. We then rank the 222 months in each

country (from 1991:07 to 2009:12) into quintiles based on PMP and examine the performance

of momentum portfolios in each post-formation years 1-5 and—in the All column—over the

full 5 years post-formation, as was done for the US stock universe in Table 2. To calculate

3-factor alphas, we estimate conditional loadings for each PMP Quintile and event month

pair. Table 5 reports the results of this analysis; for brevity, we only report alphas in Table 5.

Consistent with the US-market findings reported earlier, we see that for most of the non-

US universes, there is a strong inverse relationship between PMP and post-formation alphas.

Specifically, the difference between the five-year post formation alphas (ie., in the All column)

for momentum portfolios formed in rank-5 and rank-1 PMP months is negative for every non-

US universe except for Australia. This difference is statistically significant at at least the 5%

level for 6 of the 8 regions. The only region, other than Australia, where it this difference

is not statistically significant is Switzerland which, as noted earlier, has the smallest cross

section with an average of only 91 stocks.

One difference between the US and non-US results is that after high PMP, reversal of

momentum often seems to start earlier outside the US. Indeed, for six of the eight non-US

universes, the difference between PMP-rank 5 and 1 momentum returns in post-formation

year 1 are significantly negative, while in the US we see relatively little difference in year 1.

3.4 Implications for style chasing and investor self-attribution

Our tests were motivated by the style chasing hypothesis that investors overextrapolate past

momentum performance. This should result in relatively overpriced momentum portfolios

after high PMP, and relatively underpriced momentum portfolios after low PMP. A similar

implication follows from an account based on shifting confidence of momentum investors who

attribute success or failure of their momentum trades to their abilities, and shift in or out of

this strategy accordingly.

Style chasing further implies that after high PMP momentum returns will be higher in the

near term, and after low PMP they will be lower. But as mispricing is corrected, the prediction

18

is that eventually, after high PMP, we expect to see strong reversal of overpriced momentum

portfolios (low returns on stale momentum portfolios), and after low PMP continuation in the

returns of underpriced momentum portfolios (high returns on stale momentum portfolios).

Empirically, we find that PMP does not positively predict short horizon performance of

momentum portfolios. After high PMP, a WML portfolio does not earn higher-than-usual

abnormal returns over the next 12 months. This suggests either that style chasers are not

buying further based on PMP, or that there is little delay in style chasing, so that any price

pressure they place on the WML portfolio has already mostly occurred during the PMP

conditioning period. Also, consistent with the style chasing and self-attribution approaches,

momentum portfolios that are formed at times of high PMP reverse strongly.

However, the timing of the reversals makes clear that the style chasing and investor at-

tribution interpretations are at best incomplete explanations for the PMP effect. Stocks in a

winner (loser) portfolio of the momentum strategy do not necessarily remain winners (losers)

12 months later. So a style chaser or self-attributing investor who has recently been attracted

to momentum would tend to get out of any given momentum portfolio within about 12 months

after formation. It follows that under these hypotheses, reversals should be complete within

a year. This implication is sharply contradicted by the finding that strong reversals continue

over a period of five years.

Our findings also present a challenge to existing behavioral theories that model momentum

as pure underreaction. In such models (Grinblatt and Han 2005) momentum does not reverse.

Our finding of very strong reversals conditional on high PMP suggests that pure underreaction

is not the sole explanation. Overall, the PMP reversal effect that we document presents a new

puzzle for asset pricing and theories of momentum.

3.5 Portfolio strategy

All of the analysis done so far involves overlapping portfolios. Although our statistical tests

appropriately take this into account, it is interesting to verify whether PMP predicts reversal

of momentum using a trading strategy approach. Our first set of strategies consist of portfolios

of stale momentum portfolios formed between 1 and 60 months ago. We consider one trading

strategy for each PMP quintile and, for comparison an unconditional trading strategy that

buys all stale-momentum portfolios in each and every month. For each PMP quintile and each

month t, the trading strategy is “active” if any of the months from t− 60 to t− 1 belong to

19

that particular PMP quintile; the portfolio in month t consists of an equal-weighted average of

the value-weighted stale momentum portfolios formed in months belonging to that particular

PMP quintile from t−60 to t−1. The unconditional trading strategy is just an equal-weighted

portfolio of all stale momentum portfolios formed in months t− 60 to t− 1.

Panel A of Table 6 reports the average returns, the 3- and 4-factor alphas, and the number

of months that each strategy is active. The unconditional trading strategy, labeled All Mths,

generates a return of -0.11% per month (t = −1.23). The 3-factor alpha is statistically signifi-

cant, but the 4-factor alpha is not. These results are consistent with a small momentum effect

in the first year after portfolio formation, but no (unconditional) reversal of the momentum

effect over the 2-5 years post-formation.

However, the Rank 1-5 results in the upper part of Panel A show that there is a strong

monotonic relationship between PMP quintile rank and portfolio returns and alphas. The

monthly portfolio return is 0.38% for quintile 1, and decreases monotonically to -0.47% for

quintile 5. Consistent with our earlier results, both the three- and four-factor alphas suggest

that the stale momentum portfolios do well when the portfolio is formed in a low-PMP month,

and poorly when it is formed in a high-PMP month.

We also consider a combined Quintile 5-minus-Quintile 1 strategy to exploit the reversals

and continuation observed in these quintiles. This strategy is active in any given month if

either Quintile 1 or Quintile 5 strategy is active, or both are active. The portfolio is long

Quintile 5 portfolio during months in which only Quintile 5 strategy is active, short Quintile

1 portfolio during months in which only Quintile 1 strategy is active, and long 50% Quintile

5 portfolio and short 50% Quintile 1 portfolio during months in which both are active. Since

all the portfolios are long-short portfolios, this portfolio is always $1 long and $1 short. This

strategy generates a return of -0.43%/month, and three- and four-factor monthly alphas of

-0.24 and -0.30% per month, and with t-statistics of -2.50 and -2.97, respectively.18.

We also consider similar strategies for each of the five years individually in Panel B of

Table 6. For example, the year 2 strategy for Quintile 5 is active in month t if any of the

months from t− 13 to t− 24 are Quintile 5 months and the portfolio in month t is an equal-

weighted average of the stale momentum portfolios formed in Quintile 5 months from t− 13

to t − 24. These results for year by year strategies are consistent with those presented in

18We note that a strategy that skips the first year, and forms the portfolio based on the PMP from monthst− 13 to t− 60 generates a monthly 3-factor alpha of -0.37% (t = −3.74)

20

Table 2; Quintile 5 returns and alphas are negative in all years and most are significant while

Quintile 1 returns and alphas are generally positive and some significantly so. The Quintile 5

and Quintile 1 combined strategy generates significantly negative alphas in three of the four

years.

3.6 Other robustness checks

We next verify whether these findings are robust to measuring abnormal performance using

characteristic-adjusted returns instead of alphas, and whether these findings are distinct from

previous studies which try to predict momentum returns. While these papers try to forecast

momentum returns in the month after portfolio formation unlike the long-horizon returns that

we examine, it is still possible the variables studied predict long-horizon returns as well and

that the results that we document arise because PMP is correlated with these variables. We

believe that this is unlikely since Table 1 shows that the correlations between PMP and these

variables are fairly low suggesting that our results are unique. Nonetheless, we directly control

for these variables in this section.

Perhaps the most widely studied forecaster of momentum performance is past market

return. Cooper, Gutierrez, and Hameed (2004) and Daniel and Moskowitz (2016), among

others, show that momentum strategies experience crashes after market declines. To address

the possibility that our results are being driven by momentum crashes following down market

months, in Panel A of Table 7, we exclude all portfolio formation months for which the

cumulative market return over the past two years is negative. For brevity, we only report

the alphas in Table 7.19 In post-formation year 1, momentum portfolios formed in Quintile

5 months generate a statistically significant abnormal return of 0.76% per month, and the

difference between top and bottom quintile alphas is not significant. Years 2-5 reversals are

quite strong for Quintile 5, ranging from -0.45% to -0.68% per month, and three of them are

significant at the 5% level. In fact, all of the Quintile 5 alphas in years 2-5 are more negative

than the corresponding numbers in Panel B of Table 2. This analysis clearly indicates that

our results are not being driven by past market performance.

Another possible explanation of our results is that during Quintile 5 months, the formation

period difference between returns of winners and losers (the momentum characteristic spread)

19The ability of PMP to predict momentum reversal is much stronger for raw returns; results available onrequest.

21

is extremely large and, therefore, the subsequent reversals are extremely strong compared to

other months. To address this possibility, we regress PMP on the formation period difference

between mean return of winner and loser portfolios and use the residual from the regression to

rank months into quintiles. Panel B of Table 7 shows that this procedure results in a U-shaped

relationship between PMP and the momentum characteristic spread. Although bottom and

top quintile months have a similar characteristic spread, there is a stark difference in post-

formation momentum returns. For Quintile 1, the alphas in years 2-5 are all positive, though

none are significant, but for Quintile 5, the alphas are all negative and significant in years

2 and 5. The difference in alphas between the two extremes is negative in each year and

significant at the 5% level in years 2 and 5 and at the 10% level in year 4.

In our third test, we orthogonalize PMP with respect to momentum variance—variance of

daily momentum returns over the past 6 months. Barroso and Santa-Clara (2015) show that

momentum variance forecasts low momentum profits. The results in Panel C show that PMP

Quintile 1 and 5 months have almost identical past momentum variance but there is a sharp

difference in post-formation alphas in years 2-5—momentum portfolios formed in Quintile 1

months exhibit weak continuation, while those formed in Quintile 5 months exhibit strong

reversals.

Panel D shows that our results are also robust to controlling for recent market volatility.20

In summary, the results in Table 7 clearly show that PMP’s predictability is distinct from

that of other variables.

Our results are robust to measuring abnormal performance using characteristic-adjusted re-

turns (Daniel, Grinblatt, Titman, and Wermers 1997) instead of Fama-French alphas. Specif-

ically, in June of each year, we rank stocks into size quintiles using NYSE size breakpoints and

within each quintile, we rank stocks into five book-to-market quintiles.21 We then calculate

the size and book-to-market adjusted return of each stock as the raw return minus the value-

weighted return of the same size and book-to-market quintile portfolio. The sample period

for this test starts in 1951:06 due to unavailability of Compustat data in prior years. Panel E

of Table 7 shows that the results are actually somewhat stronger using characteristic-adjusted

returns. Reversals are quite strong for Quintile 5 months. In contrast, momentum portfolios

20We have also run tests in which we regress PMP on all three variables—momentum characteristic spread,momentum variance, and market variance—together and use the residual to rank months. The results arevery similar and reversals are strong in Quintile 5 months.

21Our results are robust to using independent size and book-to-market sorts.

22

formed in Quintile 1 months exhibit return continuation—year 4 return is positive and signif-

icant. The differences between top and bottom quintile returns are all negative, economically

very large, and four are significant at the 5% or lower level, and one at 10% level.

In Panels F and G of Table 7, we sub-divide the sample into two equal periods and show

that our results hold in both periods. In particular, the magnitude of the effect appears similar

in the two subsamples and the overall sample. The statistical significance is lower in the two

subsamples, as would be expected given the smaller sample size.

In Panels H and I, we divide our sample into formation dates pre-1982 and post-1982,

respectively. As noted earlier, Jegadeesh and Titman (2001) divide their sample into pre-and

post-1982 subsamples, and find no evidence of reversal in the post-1982 subsample. Our tests

differ from theirs in that we condition on PMP. It is interesting that this conditioning identifies

reversal even in the post-1982 subsample. Panel I shows that, in the post-1982 subsample,

for momentum portfolios formed in PMP Quintile 5 months, alphas are strongly negative and

statistically significant in years 2 and 5 post-formation.22

3.7 PMP and Institutional Trading

We next test whether institutional investors engage in momentum style chasing based upon

PMP. Our institutional holdings data is from Thomson Reuters. Following previous literature

(Grinblatt, Titman, and Wermers 1995), we calculate the momentum trading measure L0Miq

for fund i in quarter q as the vector product of quarterly portfolio weight changes and past

returns:

L0Miq =3∑

m=1

N(q)∑j=1

(wi,j,q − wi,j,q−1)Rj,q−1,m

where Rj,q−1,m is stock j’s return in the mth month of quarter q − 1, wi,j,q is fund i’s weight

on stock j at the end of quarter-q, and N(q) is the number of stocks in quarter q, and where

(wi,j,q − wi,j,q−1) =SharesHeldi,j,q × pj,q−1∑Nj=1 SharesHeldi,j,q × pj,q−1

− SharesHeldi,j,q−1 × pj,q−1∑Nj=1 SharesHeldi,j,q−1 × pj,q−1

.

22Consistent with Jegadeesh and Titman (2001), we find very weak reversals in the 1982-1998 period (evenfor raw returns) without conditioning on PMP. However, momentum portfolios formed in PMP quintile 5months lose on average 32.8% of their value in post-formation years 2-5 in this 1982-1998 sample period.

23

Here, SharesHeldi,j,q is the number of shares of stock j held by fund i at the end of quarter q,

and pj,q−1 is the price of stock j at the end of quarter q − 1.23

At the end of each quarter from 1985:06 to 2010:03, we rank all institutional investors

with at least five years of historical data available into deciles based on their average past

momentum trading measure. We call the top decile institutions ‘momentum traders’ and

the bottom decile institutions ‘contrarian traders.’ Thus momentum traders have a history

of buying winners and selling losers while contrarian traders have a history of doing the

opposite. We then calculate the time-series of mean quarterly momentum trading measures

for momentum and contrarian traders.

To test how momentum and contrarian traders respond to PMP, we then regress these

trading measures on last quarter’s PMP quintile rank. To control for any mechanical relation-

ship between momentum trading and PMP that might arise because of high cross-sectional

volatility during periods with high PMP, we include past quarter’s cross-sectional standard

deviation of returns as a control in the regressions.

Table 8 presents the results. The highly significant intercept for momentum traders indi-

cates that momentum trading is a highly persistent characteristic—institutions with a history

of trading on momentum continue to do so in the future. Table 8 also shows that there is

a highly significant relationship between PMP and future momentum trading for momentum

traders; increasing PMP quintile rank from one to five increases mean momentum trading of

momentum traders by 0.61, an increase of 62% relative to the unconditional mean of the de-

pendent variable. On the other hand, there is no relationship between momentum trading and

PMP for contrarian traders.24 These results suggest that the behavior of momentum-trading

institutional investors may play a role in the relation between PMP and stale momentum

returns documented in our tests.

23We use prior quarter prices to calculate changes in portfolio weights so that the measure does not pickup changes in weights resulting directly from changes in prices.

24A possible interpretation is that momentum traders pay heavy attention to past momentum performancein deciding how aggressively to follow a momentum strategy—a kind of positive feedback at the strategy ratherthan at the stock level; whereas contrarian investors are less active in adjusting their strategy in response to pastmomentum performance. Of course, equilibrium considerations imply that if the aggressiveness of the tradingof momentum traders changes, there must be a corresponding shift in the trading of some counterparties.However, the trading of contrarians here is not the simple complement of the trading of momentum investorshere, since most investors fall into neither category.

24

4 Conclusion

Motivated by behavioral theories, we examine the relationship between recent past momentum

performance, PMP, and long horizon performance of stale momentum portfolios. Following

period of strong momentum performance, we see that stale momentum portfolios exhibit

strong reversals for five years post-formation. In contrast, follow poor momentum returns,

stale momentum portfolios do not underperform. The difference in cumulative five-year Fama-

French alphas of momentum portfolios formed in top and bottom PMP quintile momentum

portfolios is 40%. We find similar results for both industry and residual momentum and in

several international markets. Our results also obtain after controlling for previously known

predictors of the momentum premium.

We also show that PMP does not forecast short horizon momentum profits and that

the reversals last too long to be fully explained by style chasing and bias in self-attribution

hypotheses. They also conflict with theories of momentum based upon pure underreaction.

Overall, these findings offer a challenge to existing theories of asset pricing and momentum.

25

References

Asness, Clifford S., R. Burt Porter, and Ross L. Stevens, 2000, Predicting stock returns usingindustry-relative firm characteristics, Working paper, AQR Capital Management.

Barberis, Nicholas, and Andrei Shleifer, 2003, Style investing, Journal of Financial Economics68, 161–199.

Barberis, Nicholas, Andrei Shleifer, and Robert Vishny, 1998, A model of investor sentiment,Journal of Financial Economics 49, 307–343.

Barroso, Pedro, and Pedro Santa-Clara, 2015, Momentum has its moments, Journal of Fi-nancial Economics 116, 111–120.

Carhart, Mark M., 1997, On persistence in mutual fund performance, Journal of Finance 52,57–82.

Cooper, Michael J., Roberto C. Gutierrez, and Allaudeen Hameed, 2004, Market states andmomentum, Journal of Finance 59, 1345–1365.

Daniel, Kent, David Hirshleifer, and Avanidhar Subrahmanyam, 1998, Investor psychologyand security market under- and overreactions, Journal of Finance 53, 1839–1885.

Daniel, Kent D., Mark Grinblatt, Sheridan Titman, and Russ Wermers, 1997, Measuringmutual fund performance with characteristic-based benchmarks, Journal of Finance 52,1035–1058.

Daniel, Kent D., and Tobias J. Moskowitz, 2016, Momentum crashes, Journal of FinancialEconomics 122, 221–247.

Fama, Eugene F., and Kenneth R. French, 1993, Common risk factors in the returns on stocksand bonds, Journal of Financial Economics 33, 3–56.

Froot, Kenneth A., and Melvyn Teo, 2008, Style investing and institutional investors, Journalof Financial and Quantitative Analysis 43, 883–906.

Greenwood, Robin, Andrei Shleifer, and Yang You, 2017, Bubbles for Fama, NBER workingpaper No.23191, Harvard Business School.

Grinblatt, Mark, and Bing Han, 2005, Prospect theory, mental accounting, and momentum,Journal of Financial Economics 78, 311–339.

Grinblatt, Mark, and Matti Keloharju, 2009, Sensation seeking, overconfidence, and tradingactivity, Journal of Finance 64, 549–578.

Grinblatt, Mark, Sheridan Titman, and Russ Wermers, 1995, Momentum investment strate-gies, portfolio performance, and herding: A study of mutual fund behavior, AmericanEconomic Review 85, 1088–1105.

26

Grundy, Bruce, and J. Spencer Martin, 2001, Understanding the nature of the risks and thesource of the rewards to momentum investing, Review of Financial Studies 14, 29–78.

Hong, Harrison, and Jeremy C. Stein, 1999, A unified theory of underreaction, momentumtrading and overreaction in asset markets, Journal of Finance 54, 2143–2184.

Jegadeesh, Narasimhan, and Sheridan Titman, 1993, Returns to buying winners and sellinglosers: Implications for stock market efficiency, Journal of Finance 48, 65–91.

Jegadeesh, Narasimhan, and Sheridan Titman, 2001, Profitability of momentum strategies:An evaluation of alternative explanations, Journal of Finance 56, 699–720.

Moskowitz, Tobias J., and Mark Grinblatt, 1999, Do industries explain momentum?, Journalof Finance 54, 1249–1290.

Newey, Whitney K., and Kenneth D. West, 1987, Hypothesis testing with efficient method ofmoments estimation, International Economic Review 28, 777–787.

Stivers, Chris, and Licheng Sun, 2010, Cross-sectional return dispersion and time variationin value and momentum premiums, Journal of Financial and Quantitative Analysis 45,987–1014.

Teo, Melvyn, and Sung-Jun Woo, 2004, Style effects in the cross-section of stock returns,Journal of Financial Economics 74, 367–398.

27

Figures and Tables

19321942

19521962

19721982

19922002

date

0.06

0.04

0.02

0.00

0.02

0.04

0.06

PM

P

PMP Time Series -- 1928:12-2009:12

19321942

19521962

19721982

19922002

date

1

2

3

4

5

PM

P q

uin

tile

PMP Quintile Rank -- 1928:12-2009:12

Figure 1: PMP Time-SeriesPanel A plots the time-series of PMP from 1928:12-2009:12. Panel B plots the corresponding PMPquintile. The calculation of PMP is described in the caption of Table 1.

28

0 10 20 30 40 50 60time after portfolio formation (months)

50

40

30

20

10

0

10

20cu

mula

tive r

etu

rn (

%)

cumulative returns by PMP quintile --- 1928:12-2014:12

PMP Quintile

12345ALL

0 10 20 30 40 50 60time after portfolio formation (months)

15

10

5

0

5

10

15

20

25

30

cum

ula

tive r

etu

rn (

%)

cumulative alphas by PMP quintile --- 1928:12-2014:12

PMP Quintile

12345ALL

Figure 2: Cumulative Returns and Alphas, by PMP QuintileThese figures plot the average cumulative 5-year returns (excess of the cumulative risk-free rate) andFama-French three-factor alphas of the value-weighted momentum portfolios formed in each of thefive PMP Quintile months as well as for the momentum portfolios formed in all months.

29

0 10 20 30 40 50 60time after portfolio formation (months)

10

5

0

5

10cu

mula

tive r

etu

rn (

%)

cumulative alphas by PMP quintile -- past winners --- 1928:12-2014:12

PMP Quintile

12345ALL

0 10 20 30 40 50 60time after portfolio formation (months)

14

12

10

8

6

4

2

0

2

4

cum

ula

tive r

etu

rn (

%)

cumulative alphas by PMP quintile -- past losers --- 1928:12-2014:12

PMP Quintile

12345ALL

Figure 3: Cumulative Alphas, by PMP Quintile, for past-Winner and past-Loser PortfoliosPanels A and B plot the cumulative alphas of the past-winner and past-loser portfolios, respectively.The calculation of the alphas is described in the caption of Table 2.

30

19351945

19551965

19751985

19952005

300

200

100

0

100

200

300

Mom

entu

m R

etur

ns, t

+1

t+60

mon

ths (

%, c

umul

ativ

e)

R_1_60PMP (right)

6

4

2

0

2

4