On The Path of Global Leadership… - Welspun Corp... · • Top 2 Large Diameter Pipe Company in...

27

April 2011 Page 1 On The Path of Global Leadership… WELSPUN CITY, ANJAR

Transcript of On The Path of Global Leadership… - Welspun Corp... · • Top 2 Large Diameter Pipe Company in...

April 2011 Page 1

On The Path of Global Leadership…

WELSPUN CITY, ANJAR

April 2011 Page 2

Disclaimer

Certain statements made in this presentation may not be based on historical information or facts and may be “forward looking statements,” including

those relating to general business plans and strategy of Welspun Corp. Limited (“WCL"), its future outlook and growth prospects, and future

developments in its businesses and its competitive and regulatory environment. Actual results may differ materially from these forward-looking

statements due to a number of factors, inter alia including future changes or developments in WCL's business, its competitive environment, its ability

to implement its strategies and initiatives and respond to technological changes and political, economic, regulatory and social conditions in India.

This presentation does not constitute a prospectus, offering circular or offering memorandum or an offer invitation, or a solicitation of any offer, to

purchase or sell, any shares of WCL and should not be considered or construed in any manner whatsoever as a recommendation that any person

should subscribe for or purchase any of WCL's shares. Neither this presentation nor any other documentation or information (or any part thereof)

delivered or supplied under or in relation thereto shall be deemed to constitute an offer of or an invitation by or on behalf of WCL to subscribe for or

purchase any of its shares.

WCL, as such, makes no representation or warranty, express or implied, as to, and does not accept any responsibility or liability with respect to, the

fairness, accuracy, completeness or correctness of any information or opinions contained herein. The information contained in this presentation,

unless otherwise specified is only current as of the date of this presentation. WCL assumes no responsibility to publicly amend, modify or revise any

forward looking statements contained herein, on the basis of any subsequent development, information or events, or otherwise. Unless otherwise

stated in this document, the information contained herein is based on management information and estimates. The information contained herein is

subject to change without notice and past performance is not indicative of future results. WCL may alter, modify or otherwise change in any manner

the content of this presentation, without obligation to notify any person of such revision or changes. This presentation may not be copied and

disseminated in any manner.

THE INFORMATION PRESENTED HERE IS NOT AN OFFER INVITATION OR SOLICITATION OF ANY OFFER TO PURCHASE OR SELL ANY

EQUITY SHARES OR ANY OTHER SECURITY OF WCL.

This presentation is not for publication or distribution, directly or indirectly, in or into the United States, Canada or Japan.

These materials are not an offer or solicitation of any offer of securities for purchase or sale in or into the United States, Canada or Japan.

April 2011 Page 3

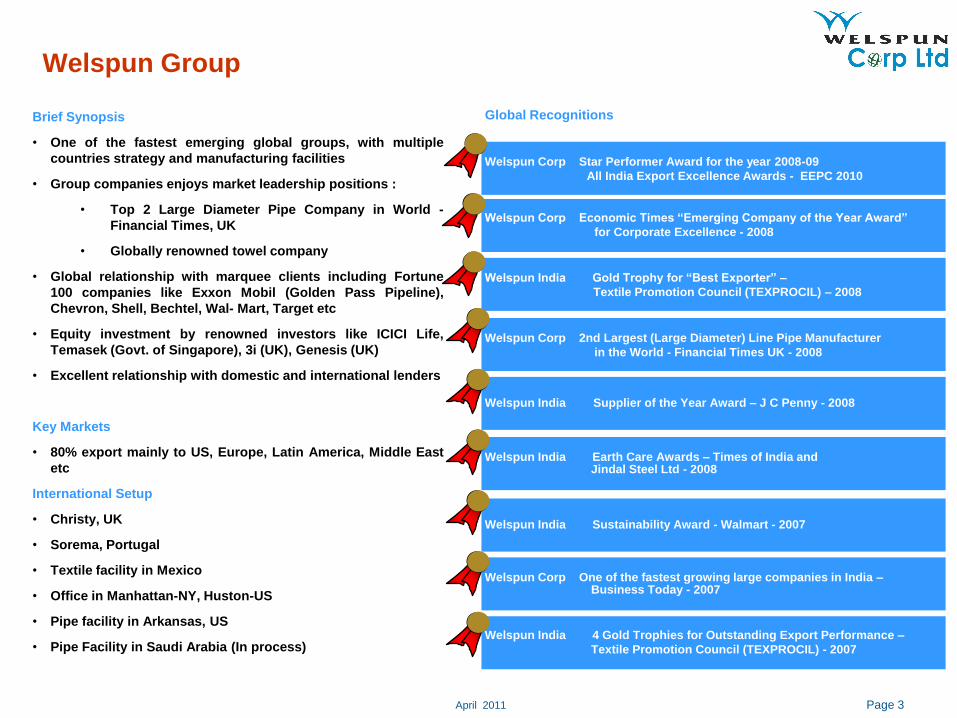

Welspun Group

Brief Synopsis

• One of the fastest emerging global groups, with multiple

countries strategy and manufacturing facilities

• Group companies enjoys market leadership positions :

• Top 2 Large Diameter Pipe Company in World -

Financial Times, UK

• Globally renowned towel company

• Global relationship with marquee clients including Fortune

100 companies like Exxon Mobil (Golden Pass Pipeline),

Chevron, Shell, Bechtel, Wal- Mart, Target etc

• Equity investment by renowned investors like ICICI Life,

Temasek (Govt. of Singapore), 3i (UK), Genesis (UK)

• Excellent relationship with domestic and international lenders

Key Markets

• 80% export mainly to US, Europe, Latin America, Middle East

etc

International Setup

• Christy, UK

• Sorema, Portugal

• Textile facility in Mexico

• Office in Manhattan-NY, Huston-US

• Pipe facility in Arkansas, US

• Pipe Facility in Saudi Arabia (In process)

Welspun Corp Economic Times “Emerging Company of the Year Award”

for Corporate Excellence - 2008

Welspun India Gold Trophy for “Best Exporter” –

Textile Promotion Council (TEXPROCIL) – 2008

Welspun Corp 2nd Largest (Large Diameter) Line Pipe Manufacturer

in the World - Financial Times UK - 2008

Welspun India Supplier of the Year Award – J C Penny - 2008

Welspun India Earth Care Awards – Times of India and Jindal Steel Ltd - 2008

Welspun India Sustainability Award - Walmart - 2007

Welspun Corp One of the fastest growing large companies in India –Business Today - 2007

Welspun India 4 Gold Trophies for Outstanding Export Performance –

Textile Promotion Council (TEXPROCIL) - 2007

Global Recognitions

Welspun Corp Star Performer Award for the year 2008-09

All India Export Excellence Awards - EEPC 2010

April 2011 Page 4

WCL – An Introduction

• WCL, flagship company of Welspun Group, is one of the

largest pipe manufacturing company in the world

• Incorporated in 1995, the Company offers a complete range

of high grade line pipes ranging from ½ inch to 100 inch

used inter alia for transmission of oil & gas

• Partner of Choice for more than 50 Oil & Gas Giants across

the globe with a geographically diverse client base including

Chevron, Exxon Mobil (Golden Pass Pipeline), Saudi Aramco,

British Gas , Kinder Morgan etc

• International footprint

• Accredited with ISO 9001, ISO 14001 and OHSAS 18001

certifications

• Strong order book of U.S. $ 1.4 Bn

26,834 39,945

57,395

73,503

58,604

0

20,000

40,000

60,000

80,000

2006-07 2007-08 2008-09 2009-10 9M 2010-11

(INR MM)CAGR (07-10): 40%

617 991 1,250US $ MM

2,666

5,845 4,768

11,301

9,447

500

3,500

6,500

9,500

12,500

2006-07 2007-08 2008-09 2009-10 9M 2010-11

(INR MM) CAGR (07-10): 62%

61 145 104US $ MM

Gross Profit

Steady Growth in Revenues and ProfitConsolidated Total Revenues

Summary Market Statistics

As of April 4, 2011 INR MM US$ MM(6)

Share Price (INR/ US$) 205.70 4.60

Market Capitalization 42,100 942

Enterprise Value (1) 49,449 1,106

19.78%

41.08%38.94%

0.20%

Promoter

Mutual Funds

FII

Public, Banks and

Financial Institutions

Shareholding Pattern, as on Dec. 31, 2010

Note

1. Net Debt at INR 7,349 MM as on 31 Mar, 2010

2. Average exchange rate of US$1 = Rs 43.51 from 01-Apr-06 till 31-Mar-07

Note

3. Average exchange rate of US$1 = Rs.40.29 from 01-Apr-07 till 31-Mar-08

4. Average exchange rate of US$1 = Rs.45.91 from 01-Apr-08 till 31-Mar-09

5. Average exchange rate of US$1 = Rs.44.90 from 01-Apr-09 till 31-Mar-10

6. Exchange rate of US$1 = Rs. 44.705 on 31tst Dec 2010

1,637

252(5)

(5)(4)(3)(2)

(2) (3) (4)

1311(6)

211(6)

April 2011 Page 5

WCL – An Introduction

Welspun Corp Limited (WCL)Promoters (41.08%) Public and Others (58.92%)

Welspun Plate and Coil Mill

DivisionManufacturer of state-of-art

Plates and Coils

Plates & Coils

Pipes

- Longitudinal (LSAW)

- Helical / Spiral (HSAW)

- Electrical (ERW)

Welspun Pipes Inc, USAWelspun Natural Resources

Pvt. Ltd.

Oil & Gas Exploration Activities

Welspun Tubular LLC

Manufacturer of Pipes,

Coating and Double jointing

Welspun Global Trade LLC

Co

rpo

rate

Str

uctu

reP

rod

ucts

Man

ufa

ctu

rin

g F

acilit

ies

• Premier integrated set-up for manufacturing weldedpipes. Installed state-of-the-art-technology and iscompletely geared to meet the requirements of theglobal industry.

• The Longitudinal Pipes division (LSAW) has acapacity of 350,000 metric ton per annum.

• The Spiral Pipes division (HSAW) has a capacity of550,000 metric ton per annum.

• The ERW Pipes division has a capacity of 200,000metric ton per annum.

• It also has Coating capabilities

Anjar & Dahej Pipe Mills

• With manufacturing facility on a 740-acre site adjacentto the Little Rock Port Authority, the $150 millionfacility commissioned in February 2009.

• This API certified facility currently employs more than300 people and is capable of producing 350,000 tonsof HSAW pipes annually for the use of the oil and gasindustry.

• The facility can produce Pipes from 24 to 60 inches asouter diameter; 6 mm to 25 mm as wall thickness andlength of 40 -80ft.

• It also has Coating and Double Jointing capabilitiesand is a one-stop-solution provider to Welspun'svalued customers

Little Rock , Arkansas, USA

• This backward integration at Anjar, Kutch,Gujarat, India has annual capacity toproduce 1.5 million tones of Plate and Coilwith plates (up to 4.5 meters wide, 140 mmthickness) and Coil (up to 2.8 meters wide,25 mm thickness) with strength of 120,000PSI.

• This mill can cater to high end specializedproduct requirement of Line Pipe Industry(API grades), Shipping, Heavy construction,Bridges, Boiler plates, Wind blades etc.

Plate-cum-Coil Mill

WCL – 100% WCL – 100%

Oil and Gas

100% Beneficial Interest 100% Beneficial Interest

Welspun Infratech Ltd.

Infrastructure

(Welspun Projects ltd)

Welspun Energy Ltd

Solar & Renewable Energy

Renewable Energy &

Infrastructure

Dammam, Saudi Arabia

• Manufacturing facility of 300,000 tons of HSAW pipes annually for the use of the oil and gas industry.

April 2011 Page 6

Growth at Infinity

Merger of coating J.V. with WCL

New Capacity at Anjar, Gujarat for HSAW & Coating

Incorporated

350,000 tons US Spiral Mill commissioned

Approvals from O&G majors for new facility

Anjar Facility , A Key Contributor

Embarked on a Growth Journey

HSAW, Dahej, Gujarat

LSAW, Dahej, Gujarat

Pipe Coating in JV with EUPEC, Germany

Dahej, Gujarat

Growth 8

2006

2005

2004

2001

2000

1998

1995

Rs. 180 mn.

Rs. 585 mn.

Rs. 2,565 mn.

Rs. 8,277 mn.

Rs. 10,385 mn.

Rs. 18,298 mn.

2007Rs. 26,834 mn.

Rs. 39,945 mn. 2008Commissioning of Plate Mill & 43 MW Power Plant

Rs. 57,395 mn. 2009

Rs. 73,503 mn. 2010

- 100,000 tons HSAW Plant in Karnataka

operational

Investment in Middle East with HSAW

capacity of 300,000 MT operational

- 350,000 MT pipe capacity addition under

implementation in India

Foray into infra & pipe laying for O&G and

water through MSK Projects India Ltd.

9M FY 2010-11Rs. 58,604 mn.

Revenue

150,000 MT Spiral Mill commissioned

April 2011 Page 7

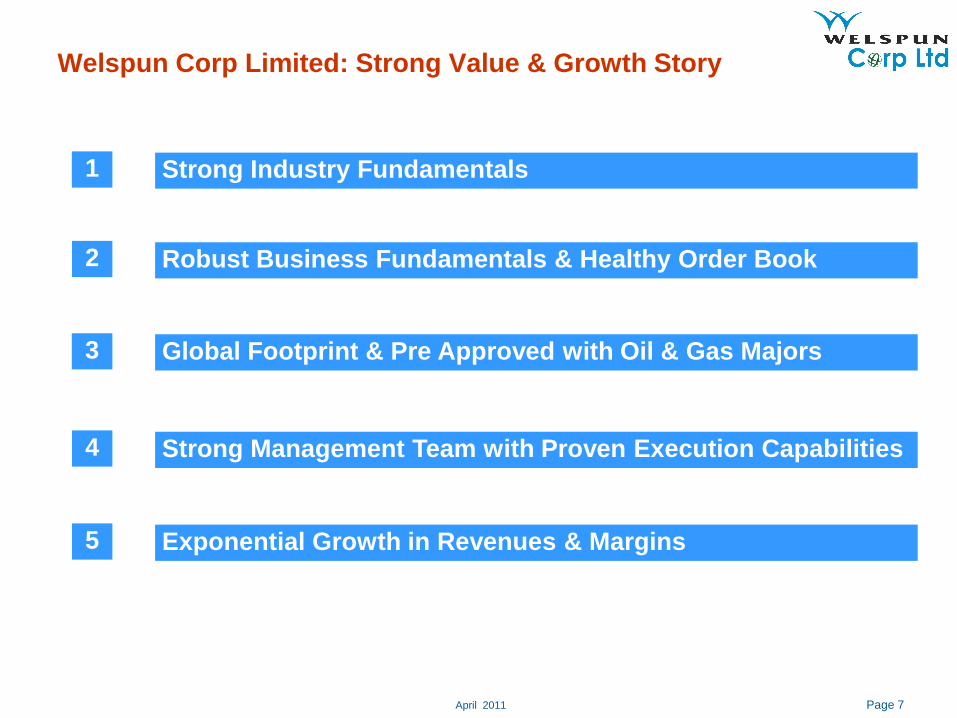

Welspun Corp Limited: Strong Value & Growth Story

Strong Industry Fundamentals1

Global Footprint & Pre Approved with Oil & Gas Majors3

Robust Business Fundamentals & Healthy Order Book2

Strong Management Team with Proven Execution Capabilities4

Exponential Growth in Revenues & Margins5

April 2011 Page 8

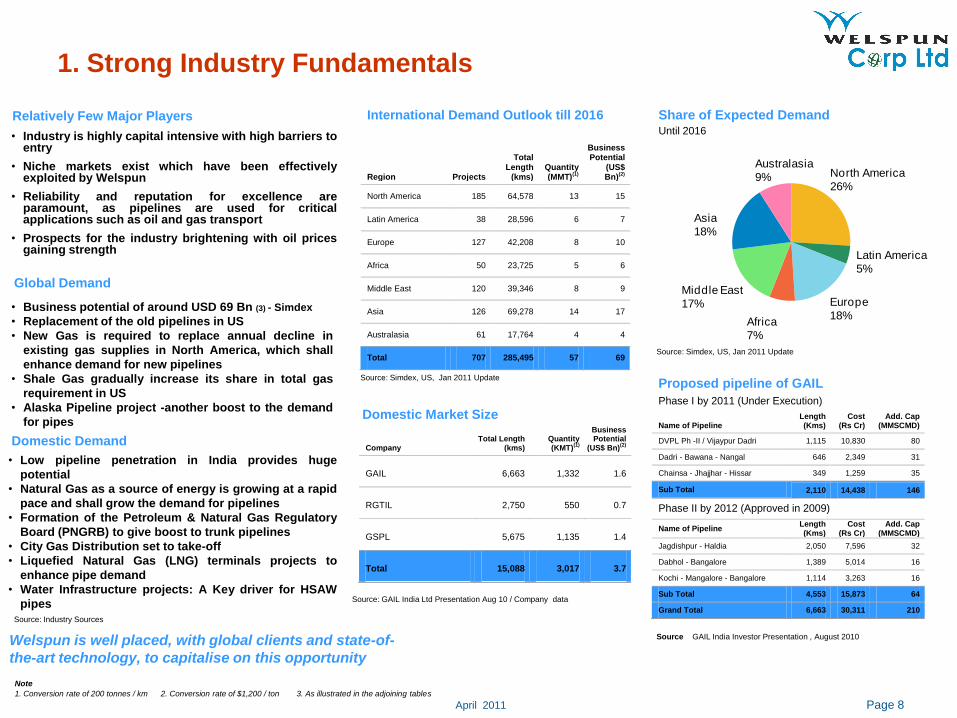

Proposed pipeline of GAIL

Phase I by 2011 (Under Execution)

Name of Pipeline Length (Kms)

Cost (Rs Cr)

Add. Cap (MMSCMD)

DVPL Ph -II / Vijaypur Dadri 1,115 10,830 80

Dadri - Bawana - Nangal 646 2,349 31

Chainsa - Jhajjhar - Hissar 349 1,259 35

Sub Total 2,110 14,438 146

Phase II by 2012 (Approved in 2009)

Name of Pipeline Length (Kms)

Cost (Rs Cr)

Add. Cap (MMSCMD)

Jagdishpur - Haldia 2,050 7,596 32

Dabhol - Bangalore 1,389 5,014 16

Kochi - Mangalore - Bangalore 1,114 3,263 16

Sub Total 4,553 15,873 64

Grand Total 6,663 30,311 210

Company Total Length

(kms) Quantity (KMT)

(1)

Business Potential

(US$ Bn)(2)

GAIL 6,663 1,332 1.6

RGTIL 2,750 550 0.7

GSPL 5,675 1,135 1.4

Total 15,088 3,017 3.7

1. Strong Industry Fundamentals

Relatively Few Major Players

North America

26%

Latin America

5%

Europe

18%Africa

7%

Middle East

17%

Asia

18%

Australasia

9%

Share of Expected DemandUntil 2016

• Industry is highly capital intensive with high barriers toentry

• Niche markets exist which have been effectivelyexploited by Welspun

• Reliability and reputation for excellence areparamount, as pipelines are used for criticalapplications such as oil and gas transport

• Prospects for the industry brightening with oil pricesgaining strength

Welspun is well placed, with global clients and state-of-

the-art technology, to capitalise on this opportunity

Source GAIL India Investor Presentation , August 2010

International Demand Outlook till 2016

Region Projects

Total Length

(kms) Quantity (MMT)(1)

Business Potential

(US$ Bn)(2)

North America 185 64,578 13 15

Latin America 38 28,596 6 7

Europe 127 42,208 8 10

Africa 50 23,725 5 6

Middle East 120 39,346 8 9

Asia 126 69,278 14 17

Australasia 61 17,764 4 4

Total 707 285,495 57 69

Source: Simdex, US, Jan 2011 Update

Source: Simdex, US, Jan 2011 Update

Source: Industry Sources

Note

1. Conversion rate of 200 tonnes / km 2. Conversion rate of $1,200 / ton 3. As illustrated in the adjoining tables

Domestic Market Size

Source: GAIL India Ltd Presentation Aug 10 / Company data

Global Demand

• Business potential of around USD 69 Bn (3) - Simdex

• Replacement of the old pipelines in US

• New Gas is required to replace annual decline in

existing gas supplies in North America, which shall

enhance demand for new pipelines

• Shale Gas gradually increase its share in total gas

requirement in US

• Alaska Pipeline project -another boost to the demand

for pipes

Domestic Demand

• Low pipeline penetration in India provides huge

potential

• Natural Gas as a source of energy is growing at a rapid

pace and shall grow the demand for pipelines

• Formation of the Petroleum & Natural Gas Regulatory

Board (PNGRB) to give boost to trunk pipelines

• City Gas Distribution set to take-off

• Liquefied Natural Gas (LNG) terminals projects to

enhance pipe demand

• Water Infrastructure projects: A Key driver for HSAW

pipes

April 2011 Page 9

377

501

670718

814

720

193

384 373

0

100

200

300

400

500

600

700

800

900

FY06 FY07 FY08 FY09 FY10 9M FY11

Going Strength to Strength

FY07 FY09 FY10

Oil & Gas Co Approval

36 >50 >50

Production ( '000 MT)

501 717 814

Revenue (US$ MM)

571 1,250 1,637

PAT (US$ MM)

36 47 136

No. of countries Glob

al Global Global

Export Market 67% 76% 77%

2. Robust Business Fundamentals & Healthy Order Book

Strongly Positioned

350

1,300

200

1,850 1,500

350

350

(200)

200

600

1,000

1,400

1,800

2,200

LSAW HSAW ERW Total Pipe

Plate Mill

Current Capacities

‘000 MT pa

Export Market Gaining DominanceProduction Growth

‘000 MT

77%76%83%67%

23%24%17%33%

0%

20%

40%

60%

80%

100%

FY07 FY08 FY09 FY10

Export Domestic

• Welspun serves several marquee

customers like Exxon Mobil (Golden

Pass Pipeline), Kinder Morgan, Ruby

(El Paso) and GAIL because of its

specialized offerings

• It has long term contracts with giants

like TransCanada; and framework

agreements with Chevron, Saudi

Aramco, etc

• Successfully expanded into highly

competitive North and Latin America to

take advantage of higher realizations

Pipes Plates

Existing Capacities New Capacities

April 2011 Page 10

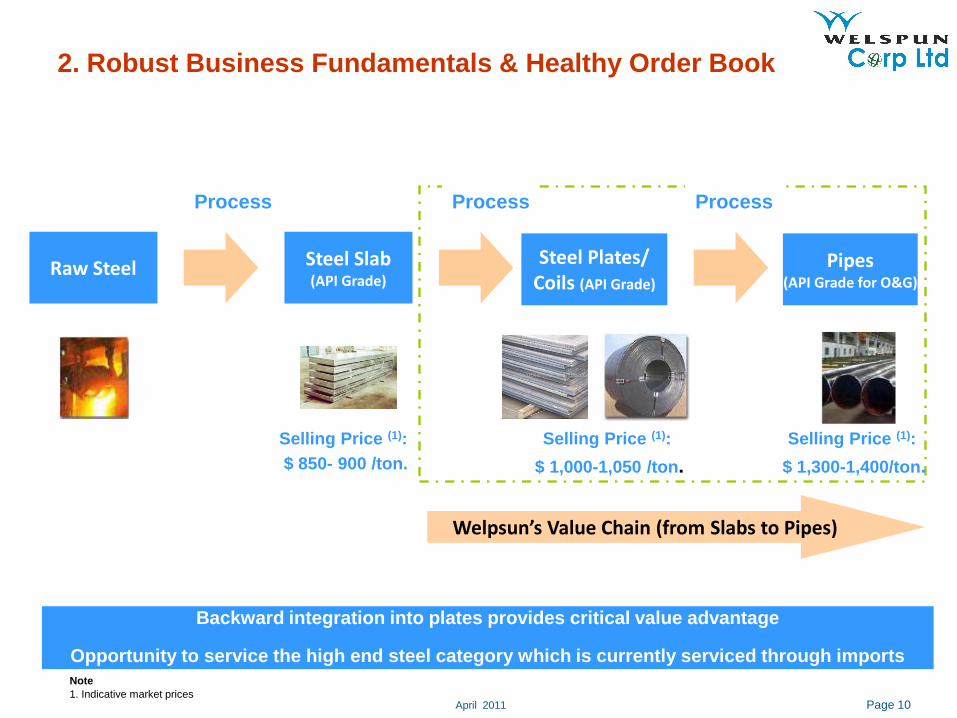

Process Process

Steel Slab(API Grade)

Steel Plates/Coils (API Grade)

Pipes(API Grade for O&G)

Selling Price (1):

$ 850- 900 /ton.

Selling Price (1):

$ 1,000-1,050 /ton.

Selling Price (1):

$ 1,300-1,400/ton.

Raw Steel

Welpsun’s Value Chain (from Slabs to Pipes)

Process

2. Robust Business Fundamentals & Healthy Order Book

Backward integration into plates provides critical value advantage

Opportunity to service the high end steel category which is currently serviced through imports

Note

1. Indicative market prices

April 2011 Page 11

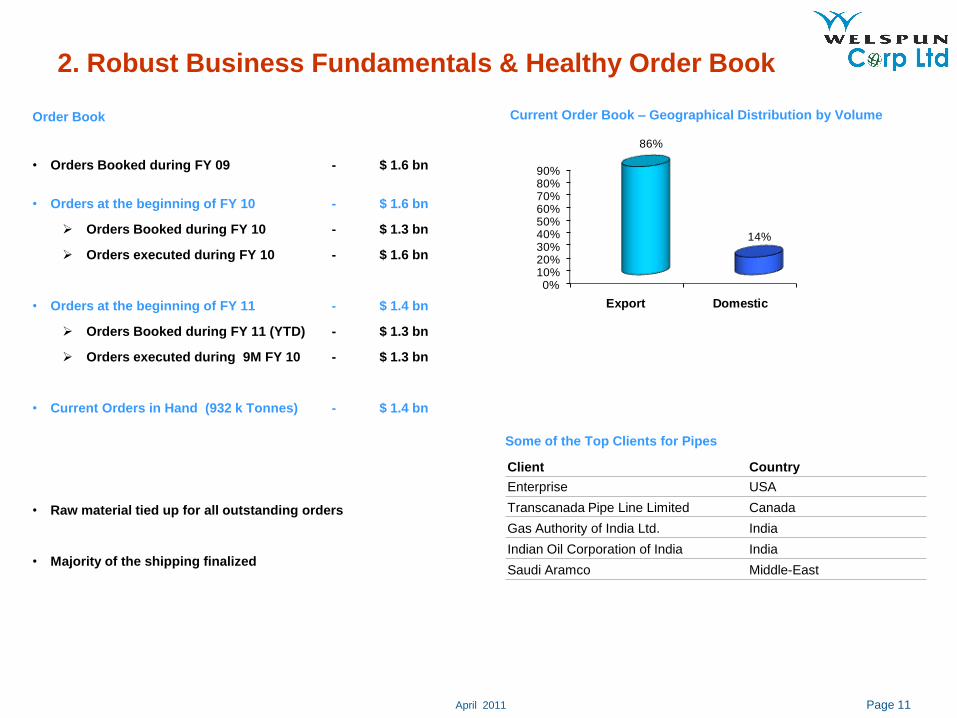

Order Book

• Orders Booked during FY 09 - $ 1.6 bn

• Orders at the beginning of FY 10 - $ 1.6 bn

Orders Booked during FY 10 - $ 1.3 bn

Orders executed during FY 10 - $ 1.6 bn

• Orders at the beginning of FY 11 - $ 1.4 bn

Orders Booked during FY 11 (YTD) - $ 1.3 bn

Orders executed during 9M FY 10 - $ 1.3 bn

• Current Orders in Hand (932 k Tonnes) - $ 1.4 bn

• Raw material tied up for all outstanding orders

• Majority of the shipping finalized

2. Robust Business Fundamentals & Healthy Order Book

Current Order Book – Geographical Distribution by Volume

Some of the Top Clients for Pipes

Client Country

Enterprise USA

Transcanada Pipe Line Limited Canada

Gas Authority of India Ltd. India

Indian Oil Corporation of India India

Saudi Aramco Middle-East

0%10%20%30%40%50%60%70%80%90%

Export Domestic

86%

14%

April 2011 Page 12

3. Global Footprint & Pre Approved with Oil & Gas Majors

What Sets WCL Apart From Competition

• Decade Long Experience

• All Solutions Under One Roof

• High Capacity Equipment to Meet Future Demand

• Backward Integration with In-house Plate-cum-Coil-Mill

World’s largest diameter steel pipe producers(1)

2007 output (million tonnes)

Salzgitter/Europipe* (Germany) 1.3

Welspun (India) 1.0

JFE (Japan) 0.7

Sumitomo (Japan) 0.7

Evraz** (Russia) 0.6

Nippon Steel (Japan) 0.6

Riva (Italy) 0.6

PSL (India) 0.5

JSW (India) 0.3

ArcelorMittal (Luxembourg) 0.2

Stupp (US) 0.1

Tata/Corus (India/UK/Netherlands) 0.1

Others*** 7.3

WCL was rated 2nd largest Pipe Company in 2007 and has since added further capacity of 0.85 MTPA

• Features- Selected few companies considered for supplies that meet stringent process of qualification

- Typically customers with large requirement over a period of time

- Flexibility in pricing terms and continuous business

• Current Framework Agreements

- Chevron, Saudi Aramco (pipe purchase agreement)

Framework Agreements

Global Market Expansion

Year 2000–2001 Year 2001–2002 Year 2002–2003 Year 2003–2004 Year 2004–2005

Year 2005–2006 Year 2006–2007 Year 2007–2008 Year 2008–2009

Canada

US (Trader Mkt.)

US (Projects)

Mexico

Venezuela

Columbia

Spain

Tunisia

Algeria

Libya

Egypt

Sudan

Qatar

Oman

Saudi Arabia

Indonesia

Malaysia

Bangladesh

Iraq

China

Russia

Year 2000–2001Year 2000–2001 Year 2001–2002Year 2001–2002 Year 2002–2003 Year 2003–2004 Year 2004–2005Year 2004–2005

Year 2005–2006 Year 2006–2007Year 2006–2007 Year 2007–2008Year 2007–2008 Year 2008–2009Year 2008–2009

Canada

US (Trader Mkt.)

US (Projects)

Mexico

Venezuela

Peru

Columbia

Spain

Tunisia

Algeria

Libya

Egypt

Sudan

Qatar

Oman

Saudi Arabia

Indonesia

Malaysia

Bangladesh

Iraq

China

Russia

Note

1. As reported by Financial Times on April 13, 2008

–Year 2009 2010

Bolivia

April 2011 Page 13

AGIP NTPC

BECHTEL ONGC

BRITISH GAS PETRO CHINA

BRITISH PETROLEUM PETRONAS, MALAYSIA

CHINA NATIONAL PETROLEUM CORPORATION PDO, OMAN

CPMEC, CHINA PGN, INDONESIA

CHEVRON (Framework Agreement) QATAR PETROLEUM

DOW RELIANCE INDUSTRIES LIMITED

RUBY (ELPASO) SAIPEM, SNAM

EGYPTIAN GENERAL PETROLEUM CORPORATION SAUDI ARAMCO (Framework Agreement)

ENTERPRISE SHELL

EXXON-MOBIL (GOLDEN PASS PIPELINE) STOLT OFFSHORE – Acergy

GAIL SONATRACH

GASCO, ABUDHABI TOTAL

GASCO, EGYPT TECHNIP

GAZPROM (STROYTRANSGAZ) TRANSCANADA (Long Term Contract)

KINDER MORGAN UNOCAL

MOGE, MYANMER PERU LNG (HUNT OIL)

N.A.O.C. - NIGERIA VIETSOPETRO

NPCC, ABU DHABI

3. Global Footprint & Pre Approved with Oil & Gas Majors

3 - 5 years

Setting up plant

2 years

Seeking API

approval

1 year

Approval from major domestic / international

oil and gas companies

2 – 3 years

Accreditation Process

A significant entry barrier

April 2011 Page 14

4. Strong Management Team with Proven Execution

Capabilities

Mr. L. T. Hotwani is Director, Supply Chain Management

of Welspun Corp Limited. With a rich experience of over 36

years, Mr. Hotwani is instrumental in sourcing raw materials

and managing supply chain with global players

Mr. B.K. Goenka is the Chairman, and the chief architect

of the Welspun Group. Today, with his entrepreneurial

ability and professionalism, he has built up one of the most

admired business conglomerates

Mr. R.R. Mandawewala is the Managing Director. He has

been a key contributor in Welspun’s journey. A Chartered

Accountant by profession and with over 20 years of

experience, he has cross-industry expertise varying from

Textiles to SAW pipes.

Mr. M.L. Mittal serves as Executive Director. A Chartered

Accountant by profession, Mr. Mittal has been instrumental

in arranging Long Term Loans and Working Capital

Facilities. During his tenure, the Company has successfully

funded several expansions projects.

Mr. Akhil Jindal serves as Director of Corporate Affairs.

He graduated with an Engineering Degree and thereafter an

MBA from Indian Institute of Management, Bangalore. Mr.

Jindal is responsible for strategic inorganic/organic

initiatives within the Group and has spearheaded large fund

raisings, cross border acquisitions, private equity raisings

and financial closure of projects exceeding over US$ 1 bn.

Mr. Asim Chakraborty is Executive Director and Plant Head

of the Anjar facility. A Civil Engineer from the University of

Kolkata, Mr. Chakraborty has been instrumental in timely

construction of various projects

Mr. Vipul Mathur is the Director of Marketing & Sales

(Pipes & Plates Division). A Science Graduate and Masters in

Business Administration (MBA) in Marketing, he has a rich

experience of over 16 years in the Oil & Gas Pipe Industry

Mr. Prashant Mukherjee serves as Director of Welded

Pipes. A Graduate in Science (Engineering, Mech) with over 24

years experience mostly in the Oil & Gas Pipe Industry, Mr.

Mukherjee has been instrumental in implementing expansion

projects in the Company

Mr. B.R. Jaju serves as Director & CFO. A Chartered

accountant by profession, member of Company Secretary (FCS),

as well as a Law Degree (LL.B). He has a rich experience over

30 years in finance and global M&A activities. Mr. Jaju has been

awarded 3 times as Best Performing CFO in the year 2003, 2005

and 2006, by the most credible nationally renowned jury.

Management Team

Mr. David J. Delie serves as President Welspun Tubular

LLC. A graduate in Science (Electrical Engineering) and a

Masters Degree in Engineering Management from the

University of Pittsburgh, he has an extensive 33-year

background in the steel and pipe industry. Mr Delie has

served on the Board of Directors of Berg Steel Pipe Corp.,

EB Pipe Coating, Inc., the American Iron & Steel Institute

(AISI).

April 2011 Page 15

4. Strong Management Team with Proven Execution

Capabilities

LSAW Pipes ERW Pipes

HSAW Pipes Coating of Pipes

April 2011 Page 16

4. Strong Management Team with Proven Execution

Capabilities

PlatesPlates

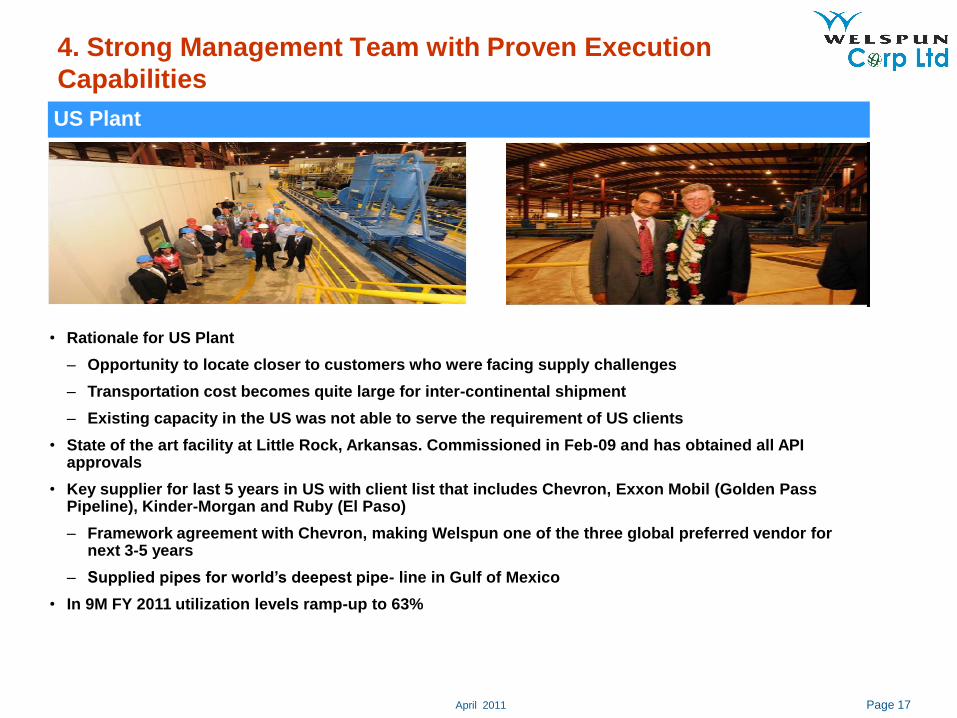

US Plant

April 2011 Page 17

4. Strong Management Team with Proven Execution

Capabilities

US Plant

• Rationale for US Plant

– Opportunity to locate closer to customers who were facing supply challenges

– Transportation cost becomes quite large for inter-continental shipment

– Existing capacity in the US was not able to serve the requirement of US clients

• State of the art facility at Little Rock, Arkansas. Commissioned in Feb-09 and has obtained all API approvals

• Key supplier for last 5 years in US with client list that includes Chevron, Exxon Mobil (Golden Pass Pipeline), Kinder-Morgan and Ruby (El Paso)

– Framework agreement with Chevron, making Welspun one of the three global preferred vendor for next 3-5 years

– Supplied pipes for world‟s deepest pipe- line in Gulf of Mexico

• In 9M FY 2011 utilization levels ramp-up to 63%

April 2011 Page 18

Notes

1. Excluding Other Income

2. Using avg. exchange rate of US$1 = Rs.44.28 from 01-Apr-05 till 31-Mar-06

3. Using avg. exchange rate of US$1 = Rs.43.51 from 01-Apr-06 till 31-Mar-07

4. Using avg. exchange rate of US$1 = Rs.40.29 from 01-Apr-07 till 31-Mar-08

10,493

3,384

1,655

6,555 6,348

13,186

0

4,000

8,000

12,000

2005-06 2006-07 2007-08 2008-09 2009-10 9M-2010-11(3) (4) (7)(5)(2)

37 78

5. Exponential Growth in Revenues & Margins

371

501

641695

814

640

154

356387

50

250

450

650

850

2005-06 2006-07 2007-08 2008-09 2009-10 9M -2010-11

(„000 MT) (INR MM)CAGR (06-10): 22%

(INR MM)

5,150

1,425

614

3,408

2,135

6,104

0

1,500

3,000

4,500

6,000

2005-06 2006-07 2007-08 2008-09 2009-10 9M -2010-11

0.0%

4.0%

8.0%

12.0%

16.0%

PAT Margin (%)(INR MM)CAGR (06-10): 68% CAGR (06-10): 78%

163 138US$ MM

Sales (volume) Consolidated Revenues (1)

EBITDA (1) Profit After Tax

1,250US$ MM 991413(2)

617(3) (4) (5)

Notes

5. Using avg. exchange rate of US$1 = Rs.45.91 from 01-Apr-08 till 31-Mar-09

6. Includes extraordinary items : forex provisioning of INR1,256MM, Inventory write-down of INR 385MM,

ECB provisions of INR 178MM

7. Using avg. exchange rate of US$1 = Rs.44.90 from 01-Apr-09 till 31-Mar-10

8. Includes recovery of past forex provisioning ( in FY09) , which is reflected in better realization and cost of material

9. Exchange rate of US$1 = Rs.44..705 as at 31-Dec-10

(3) (4) (5)(2)14 33 85 47

1,637(7)

294 136(7)

18,29826,834

39,945

57,395

73,503

58,604

0

25,000

50,000

75,000

100,000

2005-06 2006-07 2007-08 2008-09 2009-10 9M-2010-11

CAGR (05-10): 42%

(8)

# Plates

(#)(#)

(#)

(9)1311

235(9)

115(9)

US$ MM

(6)

(6)

April 2011 Page 19

4.2

8.7

18.3

11.5

28.4

23.3

0

7

14

21

28

35

2005-06 2006-07 2007-08 2008-09 2009-10 9M-2010-11

CAGR (06-10): 61%

14.7%

19.5%

11.4%

17.3%19.1%

12.2%

21.8% 21.7%

13.7%

21.0%

0%

5%

10%

15%

20%

25%

2005-06 2006-07 2007-08 2008-09 2009-10

R OC E R OE

5. Exponential Growth in Revenues & Margins

EPS (Rs./Share)(Diluted)

ROCE and ROE (%)

April 2011 Page 20

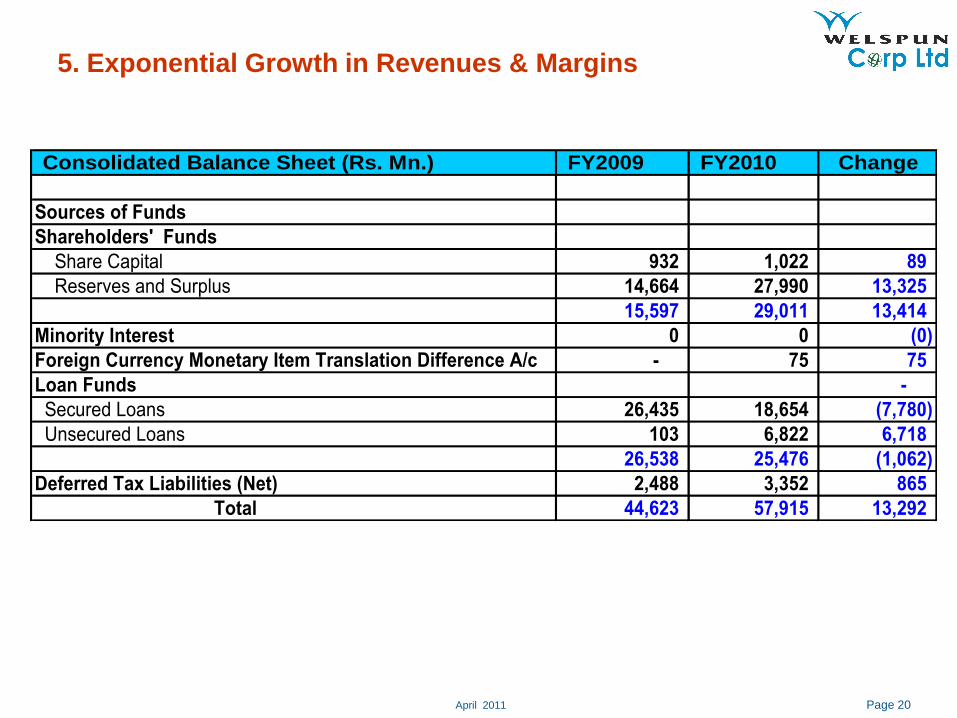

5. Exponential Growth in Revenues & Margins

Consolidated Balance Sheet (Rs. Mn.) FY2009 FY2010 Change

Sources of Funds

Shareholders' Funds

Share Capital 932 1,022 89

Reserves and Surplus 14,664 27,990 13,325

15,597 29,011 13,414

Minority Interest 0 0 (0)

Foreign Currency Monetary Item Translation Difference A/c - 75 75

Loan Funds -

Secured Loans 26,435 18,654 (7,780)

Unsecured Loans 103 6,822 6,718

26,538 25,476 (1,062)

Deferred Tax Liabilities (Net) 2,488 3,352 865

Total 44,623 57,915 13,292

April 2011 Page 21

5. Exponential Growth in Revenues & Margins

Consolidated Balance Sheet (Rs. Mn.) FY2009 FY2010 Change

Application Of Funds

Fixed Assets

Gross Block 34,844 38,810 3,966

Less:Depreciation/Amortisation/Impairment 3,847 5,889 2,042

Net Block 30,996 32,921 1,924

Capital Work-In-Progress 5,808 5,412 (396)

36,804 38,333 1,529

Investments 1,140 1,596 456

Foreign Currency Monetary Item Translation Difference A/c 355 - (355)

Current Assets, Loans and Advances -

Income Accrued on Investments 113 13 (99)

Inventories 26,113 20,322 (5,791)

Sundry Debtors 4,601 8,077 3,476

Cash and Bank Balances 9,470 17,028 7,558

Loans and Advances 5,552 6,031 479

45,848 51,471 5,623

Less : Current Liabilities and Provisions -

Current Liabilities 38,955 32,291 (6,663)

Provisions 601 1,219 618

39,555 33,510 (6,045)

Net Current Assets 6,293 17,961 11,668

Preliminary Expenses 0 0 (0)

Deferred Revenue Expenditure 31 25 (5)

Total 44,623 57,915 13,292

April 2011 Page 22

Consolidated Balance Sheet as on 30th Sept 2010

Particulars

H1 FY 2011

As at 30.09.2010

Unaudited (Rs. Mn)

A Sources of Funds

1 Shareholders Fund

a Share Capital 1,023

b Reserves and Surplus 31,470

c Share Application Money -

d Minority Interest 1,548

2 Loan Funds 38,913

3 Foreign Currency Monetory Item Translation Difference Account 38

4 Deferred Tax Liabilities-Net 3,761

Total 76,753

B Application of Funds

1 Fixed Assets 40,296

2 Build Operate and Transfer Projects Expenditure 4,159

3 Investments 13,065

4 Foreign Currency Monetory Item Translation Difference Account

5 Current Assets, Loans and Advances

a Inventories 19,002

b Sundry Debtors 12,998

c Cash and Bank Balances 13,132

d Loans and Advances 4,964 Less

4 Current Liabilities and Provisions

a Current Liabilities 29,404

b Provisions 1,482 5 Miscellaneous Expenditure 25

Total 76,753

April 2011 Page 23

9M & Q3 FY 2010-11 Highlights

Summary of 9M & Q3 FY11 (Rs. Million)

Breakdown of Production and Sales in MT

Major Highlights in 9M FY11

• Sales strengthened by volume growth and consolidation

of Infra business and is up by 2%

• Interest costs lower by 42%, due to repayment of high

cost debt

• Depreciation is higher by 17%, due to capitalization of

new capacities and consolidation of Infra business

• PAT at Rs. 5,150 million reflects the growth of 16% on a

YoY basis

• Net Debt of Rs 11,120 million and Net Debt Equity Ratio

of 33%

Status of ProjectsCapacity of Pipes is being increased to 2.2 million MTPA:

• LSAW expansion of 350 K MTPA at Anjar in Q1 FY 2012.

• HSAW plant of 100K MTPA at Karnataka is now fully

operational.

• Saudi Plant commences production in Q4 FY11

New Initiatives• The company successfully completed the investment in

the Saudi plant, which has commenced production in Q4

FY11

• Implementation of L-SAW plant at Anjar is on schedule,

and is likely to be commissioned by the end of Q1 FY12

• The Mandya plant in Karnataka has started production

and is ramping up to achieve desired level of production.

• Welspun Middle East is establishing its presence in

Dubai to cater to the bouyant markets of Middle East and

Africa.

Particulars Q3 FY11 Q3 FY10Growth

%

9M

FY11

9M

FY10

Growth

%

Sales 15,862 16,395 -3% 58,604 57,528 2%

Reported EBITDA* 3,154 3,561* -11% 10,493 10,336* 2%

Interest 454 428 6% 1,046 1,790 -42%

Depreciation 653 511 28% 1,808 1,541 17%

PAT 1,465 1,668 -12% 5,150 4,439 16%

Cash PAT 2,297 2,300 7,481 6,191 21%

EPS (Rs./Share) -

Diluted6.65 7.83 -15% 23.26 20.91 11%

Reported EBITDA

Margin (%)19.9% 21.7% 17.9% 18.0%

PAT Margin (%) 9.2% 10.2% 8.8% 7.7%

Production Volume (in

tons) Q3 FY11 Q3 FY10 Change 9M FY11 9M FY10 Change

Total Pipes Consolidated 211,787 156,679 35% 719,613 613,544 17%

Plates & Coils 144,279 93,586 54% 372,635 276,749 35%

Sales Volume (in tons) Q3 FY11 Q3 FY10 Change 9M FY11 9M FY10 Change

Total Pipes Consolidated # 163,611 170,216 -4% 639,862 610,319 5%

Plates & Coils* 124,511 112,329 11% 355,937 288,279 23%

Breakdown of Production and Sales in Metric Tonnes (MT)

*Reported EBITDA and Profits for the quarter and nine months period ended 31st December 2009 includes Foreign Exchange realignment gain of Rs 590 million

and Rs 1,260 million.

# Company recorded higher inventory of pipes in Q3 FY11due to delay in shipment of certain export orders. The above inventory of finished pipes is being

dispatched in Q4 FY11 ensuring that the company achieves its annual sales target and records its highest ever sales in FY11.

* Includes Internal Sales

April 2011 Page 24

Summary

2Robust Business

Fundamentals

& Healthy Order Book

• Strong volume growth

• Order Book in excess of US$

1.4 Bn

• Capacities of global size

• Comprehensive product mix

Strong Management Team

with Proven Execution

Capabilities

• Recognized by the FT as the

second largest steel pipe

producer in the world in 2007

• First Indian company to supply

pipes for offshore projects in US

4 3 Global Footprint & Pre Approved with O&G Majors

• Presence across more than 25 countries

• Pre-approved with more than 50 O&G Majors

1 Strong Industry

Fundamentals

• Capital intensive, high

barriers to entry

• North America expected to

lead demand

5 Exponential Growth in

Revenues & Margins

• Revenues have grown at a

CAGR of 42% over the last

five years

• PAT has grown at a CAGR of

78% in the same period

1 Strong Industry

Fundamentals

• Capital intensive, high

barriers to entry

• North America expected to

lead demand

April 2011 Page 25

Welspun on the Path of Global Leadership

Scale of operations through large economic plants across the globe Scale Leadership

Adopt and innovate cutting-edge technology to satisfy stringent requirements of customers

Technology Leadership

Produce world class products at the least cost and maintain competitive edgeCost Leadership

Consistent focus on quality at all levels; be the best in delighting customersQuality Leadership

Most efficient and effective processes to achieve optimal utilizationsProcess Leadership

Best in class people : Produce extraordinary resultsPeople Leadership

Global Leadership Serve Globally, Act Locally

April 2011 Page 26

Key questions on recent updates

What is Welspun's exposure to current civil proceedings?

During the previous year one of the customer reported defect in the pipes supplied

alleging grade of steel used did not meet the specifications, the company replaced the

defective pipes and also provided for the expected loss on this account. During the year

the said customer initiated legal action against the company in the United States of

America claiming loss / damages of $ 66 million on account of defects in the pipes

supplied, consequently the company also initiated legal action against the steel supplier

claiming corresponding loss / damages it may suffer on account of this claim of the

customer. Hence the company does not expect any liability on account of the claim

against it.

April 2011 Page 27

Thank You

For further details, please contact:

Navin Agarwal

AVP - Corporate Affairs

Email: [email protected]

Akhil Jindal

Director - Corporate Affairs

Email: [email protected]

Company Website: http://www.welspuncorp.com