Marketing Metrics 2004 The Changing Role of Metrics...

41

Marketing Metrics 2004 The Changing Role of Metrics Across the Product Lifecycle Leon Ramselaar Head Strategy, Intelligence and Business Planning Philips Consumer Electronics Lisa Phelan Director Consumer and Market Intelligence, Philips Consumer Electronics 28 May 2004 All rights are reserved. Members of MSI and academic researchers may make limited copies of this presentation, electronically or in print, solely for their internal, non- commercial use. Any other use of this presentation—including reproduction for purposes other than those noted above, modification, distribution, or republication—without prior written permission of the Author is strictly prohibited.

Transcript of Marketing Metrics 2004 The Changing Role of Metrics...

Marketing Metrics 2004The Changing Role of Metrics Across the Product LifecycleLeon RamselaarHead Strategy, Intelligence and Business Planning Philips Consumer ElectronicsLisa PhelanDirector Consumer and Market Intelligence, Philips Consumer Electronics

28 May 2004

All rights are reserved. Members of MSI and academic researchers may make limited copies of this presentation, electronically or in print, solely for their internal, non-commercial use. Any other use of this presentation—including reproduction for purposes other than those noted above, modification, distribution, or republication—without prior written permission of the Author is strictly prohibited.

2

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

OVERVIEW

• Trends, Threats & Opportunities in the CE Business

• Managing our Business Portfolio Across the PLC

• Measurement Tools to Understand Consumers Across the PLC

3

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

Change is inherent to our business

Today’s industry dynamics• Trends

– Transformation Era– Reconnecting– Convergence

• Threats and Opportunities

4

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

We are moving out of an ‘experience’ era and into a ‘transformation’ era

We shifted our focuses from ‘making boxes’ to addressing the softer side of the equation and are

now faced with the need for another shift in thinking to

delivering more personalized and content driven solutions.

5

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

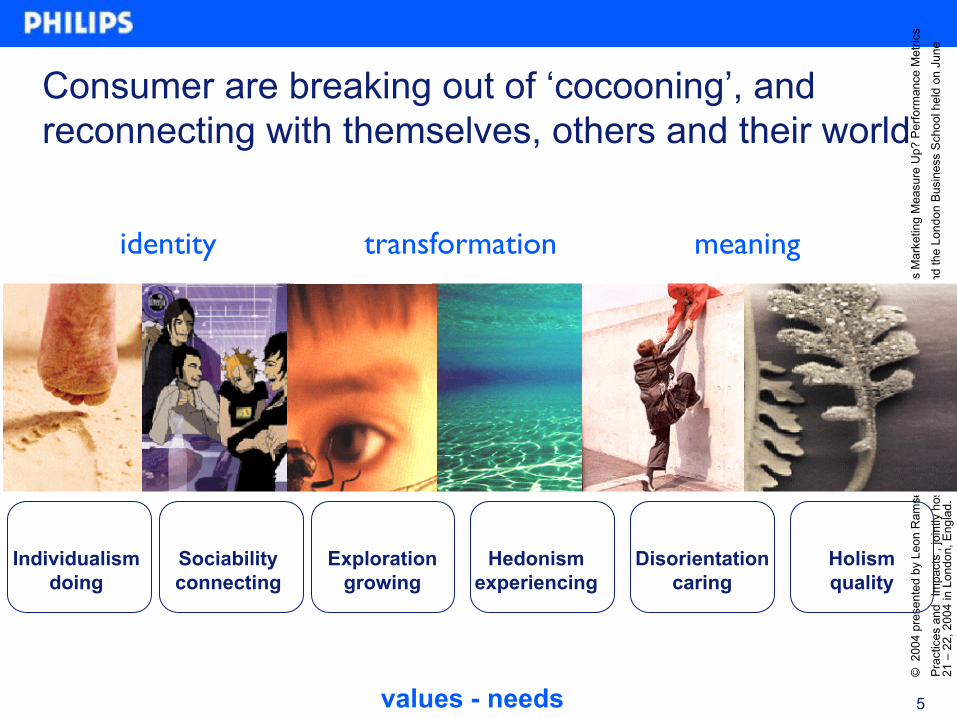

Individualismdoing

Sociabilityconnecting

Explorationgrowing

Hedonismexperiencing

Disorientationcaring

Holismquality

values - needs

identity transformation meaning

Consumer are breaking out of ‘cocooning’, and reconnecting with themselves, others and their world

6

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

Telecom PC/IT

Gaming CE

Telecom PC/IT

Gaming CE

Simultaneously, the world transits from analogue to digital, starting the convergence of industries.

This new space is all about breaking down boundaries between these historically remained separate. The

compartmentalism of experiences will become a

thing of the past.

7

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

Changing industry dynamics

• Trends• Threats and Opportunities

– Retail relationship & power

– Changing competitive landscape

– Short product lifecycles and commoditisation

8

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

Winning with retailers requires improved skills

0 1 2 3 4 5

Harmonised Consumer Pricing PoliciesTrade Terms Aligned Across Borders

Shares Systems With RetailersHarmonised Global Trade Terms System

Significant Presence In All Key MarketsTailored Responses For Selected Partners

Highly Qualified Multinational ManagersFull Internal Transparency Of Cost To Serve

Category Management SkillsStrong KAM Skills

Strong European / Global Brands

Retailer’s view ofoverall importance

Retailer’s perception of manufacturer’s performance

Retailer’s view of importance and perception of manufacturer’s performance

Source: McKinsey survey on leading retailers

9

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

The Mass Merchandisers Are Playing a Much Bigger Role in both the US and Europe

They want ‘self-explainable’ products that move quickly. Their focus is volume not service.

Source: GFK, July 2003 Source: NPD Intelect, July 2003, excluding Wal Mart

50

100

150

200

2000 2001 200250

100

150

200

2000 2001 2002

Independents Buying groupsMass MerchantChains

Inde

x

Electronic superstore A/V specialtyMass Merchant

Inde

x

CE growth per retail contact Europe 2000 = 100, cumulative

CE growth per retail contact USA 2000 = 100, cumulative

10

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

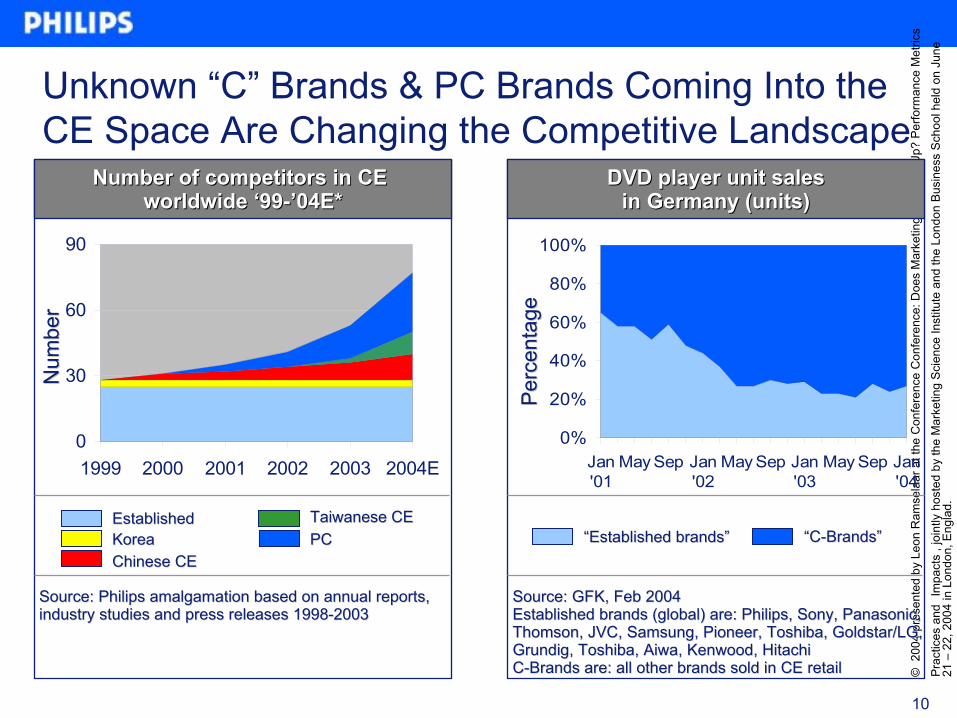

Unknown “C” Brands & PC Brands Coming Into the CE Space Are Changing the Competitive Landscape

0%

20%

40%

60%

80%

100%

Jan'01

May Sep Jan'02

May Sep Jan'03

May Sep Jan'04

Source: GFK, Feb 2004Source: GFK, Feb 2004Established brands (global) are: Philips, Sony, Panasonic, Established brands (global) are: Philips, Sony, Panasonic, Thomson, JVC, Samsung, Pioneer, Toshiba, Thomson, JVC, Samsung, Pioneer, Toshiba, GoldstarGoldstar/LG, /LG, GrundigGrundig, Toshiba, Aiwa, Kenwood, Hitachi, Toshiba, Aiwa, Kenwood, HitachiCC--Brands are: all other brands sold in CE retailBrands are: all other brands sold in CE retail

““Established brands”Established brands” ““CC--Brands”Brands”P

erce

ntag

eP

erce

ntag

e

DVD player unit salesDVD player unit salesin Germany (units)in Germany (units)

Source: Philips amalgamation based on annual reports, Source: Philips amalgamation based on annual reports, industry studies and press releases 1998industry studies and press releases 1998--20032003

0

30

60

90

1999 2000 2001 2002 2003 2004E

EstablishedEstablishedKoreaKorea

Taiwanese CETaiwanese CEPCPC

Chinese CEChinese CE

Num

ber

Num

ber

Number of competitors in CE Number of competitors in CE worldwide ‘99worldwide ‘99--’04E*’04E*

11

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

Consumers are also adopting new products at a much quicker pace, while lifecycles are shortening.

Source: Philips CE World Market Forecast 2003

DVD Recorder (PH SC) DVD Player (1997) VCR (1971)

0

10

20

30

40

50

60

1 2 3 4 5 6 7 8 9 10

Years after introduction

Mar

ket

in m

illio

n qu

antit

ies

Faster adoption of new products

0

20

40

60

80

100

120

1975 1985 1995 2005

Mar

ket

in m

illio

n qu

antit

ies

DVD PlayerVCR

Shorter life cycles –world quantities

For CE Manufacturers, this means…

• We have a shorter period to make to make our money

And

• It is more painful to make mistakes than in the past.

12

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

In the CE business, profit is basically only realized once the products reach the mature stage …

EmbryonicEmbryonic GrowthGrowth

Invest Harvest or Divest

MaturityMaturity DecliningDeclining

IFO = -10% IFO = 0% IFO = 4% IFO = 2%

Indicative figures

13

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

OVERVIEW

• Trends, Threats & Opportunities in the CE Business

• Managing our Business Portfolio Across the PLC

• Measurement Tools to Understand Consumers Across the PLC

14

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

…thus we must manage our developed categories carefully to have funding for our innovations

The Juggling Act…– Being on the Forefront of

Innovation

– Maximizing Future Potential during the Growth Phase

– Reaping the Rewards of the Established Markets

– Getting Out at the Right Time

15

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

In CE, we must balance our efforts across the span of the product lifecycle.

VCRDVD Recorder

DVD Players

EmbryonicEmbryonic GrowthGrowth

Invest Harvest or Divest

Home Theaters

MaturityMaturity DecliningDeclining

Mini Systems

Micro Systems

CRT TVs

Portable HDD

Flat TVs

Flat Monitors

CD Portables

Media Centers3G Mobile

16

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

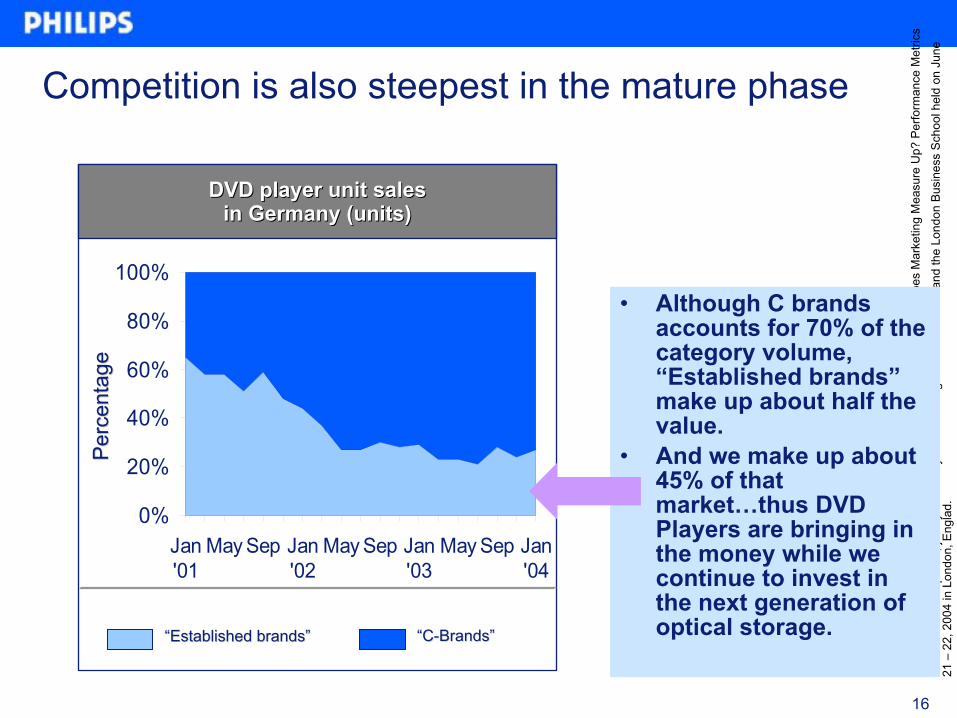

Competition is also steepest in the mature phase

• Although C brands accounts for 70% of the category volume, “Established brands” make up about half the value.

• And we make up about 45% of that market…thus DVD Players are bringing in the money while we continue to invest in the next generation of optical storage.

0%

20%

40%

60%

80%

100%

Jan'01

May Sep Jan'02

May Sep Jan'03

May Sep Jan'04

““Established brands”Established brands” ““CC--Brands”Brands”

Per

cent

age

Per

cent

age

DVD player unit salesDVD player unit salesin Germany (units)in Germany (units)

17

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

OVERVIEW

• Trends, Threats & Opportunities in the CE Business

• Managing our Business Portfolio Across the PLC

• Measurement Tools to Understand Consumers Across the PLC

18

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

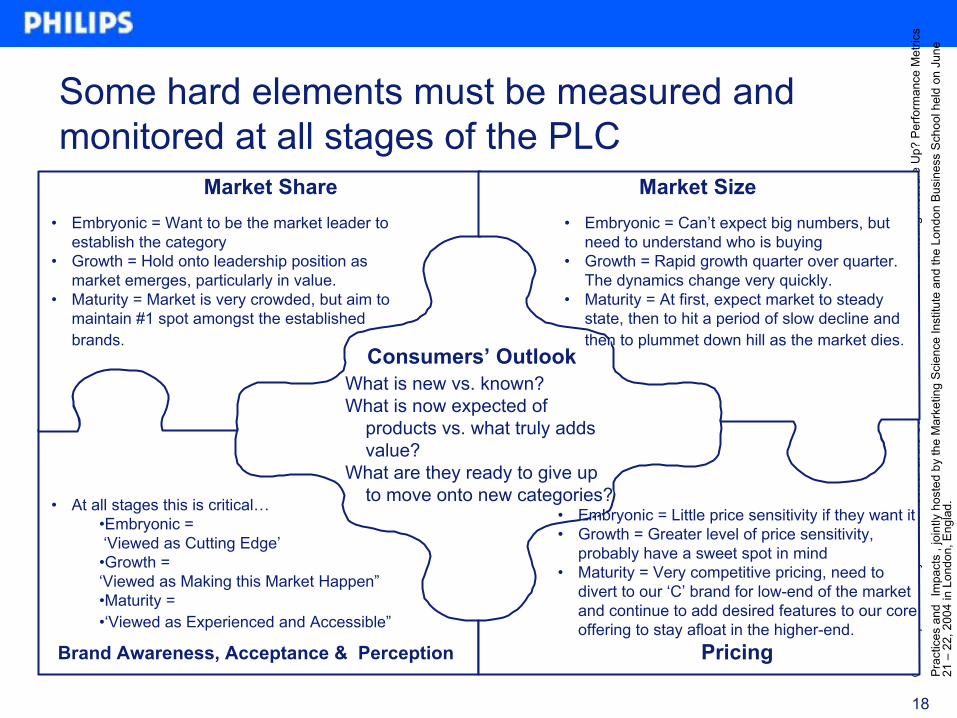

Some hard elements must be measured and monitored at all stages of the PLC

Market ShareMarket Share• Embryonic = Want to be the market leader to

establish the category• Growth = Hold onto leadership position as

market emerges, particularly in value. • Maturity = Market is very crowded, but aim to

maintain #1 spot amongst the established brands.

• Embryonic = Want to be the market leader to establish the category

• Growth = Hold onto leadership position as market emerges, particularly in value.

• Maturity = Market is very crowded, but aim to maintain #1 spot amongst the established brands.

• Embryonic = Can’t expect big numbers, but need to understand who is buying

• Growth = Rapid growth quarter over quarter. The dynamics change very quickly.

• Maturity = At first, expect market to steady state, then to hit a period of slow decline and then to plummet down hill as the market dies.

• Embryonic = Can’t expect big numbers, but need to understand who is buying

• Growth = Rapid growth quarter over quarter. The dynamics change very quickly.

• Maturity = At first, expect market to steady state, then to hit a period of slow decline and then to plummet down hill as the market dies.

PricingPricingBrand Awareness, Acceptance & PerceptionBrand Awareness, Acceptance & Perception

Market SizeMarket Size

Consumers’ OutlookConsumers’ OutlookWhat is new vs. known?What is now expected of

products vs. what truly adds value?

What are they ready to give up to move onto new categories?

What is new vs. known?What is now expected of

products vs. what truly adds value?

What are they ready to give up to move onto new categories?

• Embryonic = Little price sensitivity if they want it• Growth = Greater level of price sensitivity,

probably have a sweet spot in mind• Maturity = Very competitive pricing, need to

divert to our ‘C’ brand for low-end of the market and continue to add desired features to our core offering to stay afloat in the higher-end.

• Embryonic = Little price sensitivity if they want it• Growth = Greater level of price sensitivity,

probably have a sweet spot in mind• Maturity = Very competitive pricing, need to

divert to our ‘C’ brand for low-end of the market and continue to add desired features to our core offering to stay afloat in the higher-end.

• At all stages this is critical…•Embryonic = ‘Viewed as Cutting Edge’

•Growth = ‘Viewed as Making this Market Happen”•Maturity = •‘Viewed as Experienced and Accessible”

• At all stages this is critical…•Embryonic = ‘Viewed as Cutting Edge’

•Growth = ‘Viewed as Making this Market Happen”•Maturity = •‘Viewed as Experienced and Accessible”

19

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

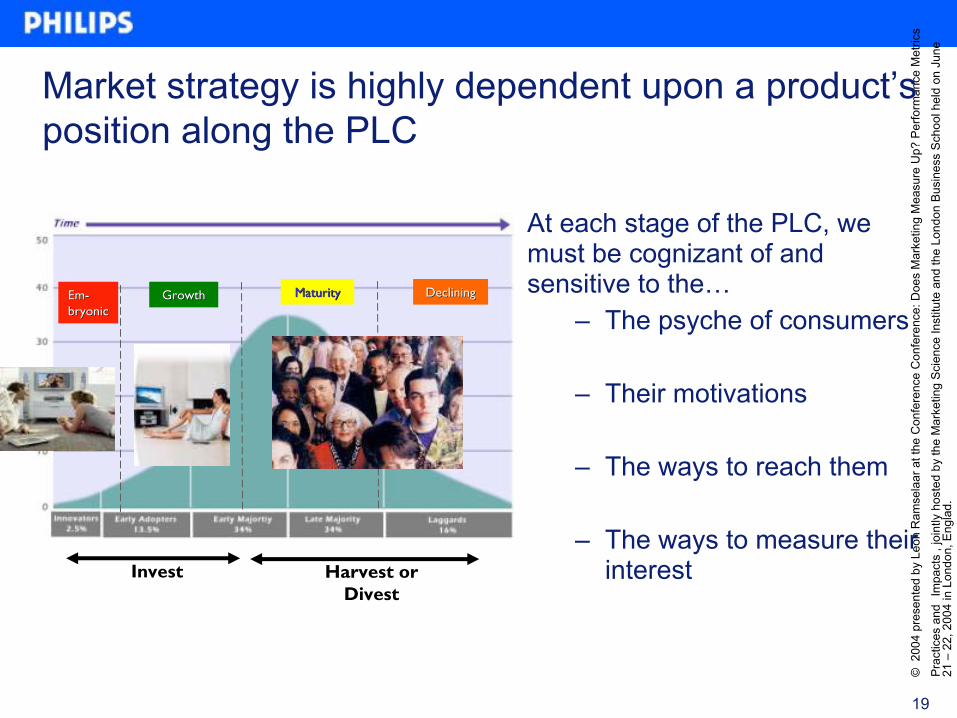

Market strategy is highly dependent upon a product’s position along the PLC

At each stage of the PLC, we must be cognizant of and sensitive to the…

– The psyche of consumers

– Their motivations

– The ways to reach them

– The ways to measure their interest

EmEm--bryonicbryonic

GrowthGrowth MaturityMaturity DecliningDeclining

Invest Harvest or Divest

20

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

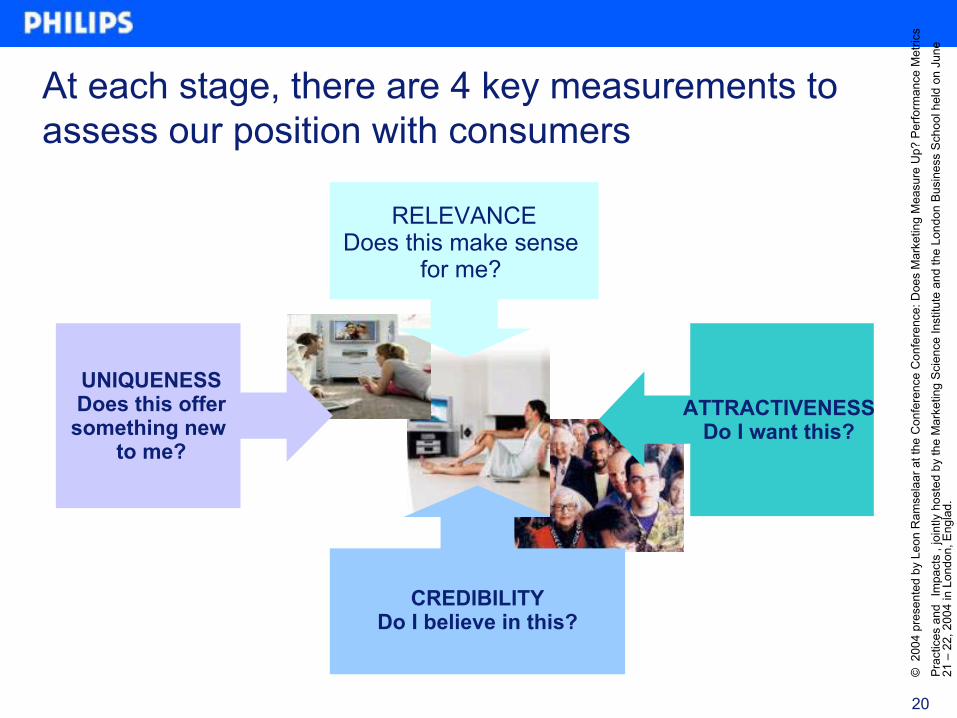

At each stage, there are 4 key measurements to assess our position with consumers

ATTRACTIVENESSDo I want this?

CREDIBILITYDo I believe in this?

UNIQUENESSDoes this offer

something new to me?

RELEVANCEDoes this make sense

for me?

21

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

Maturity stage: The psyche of mainstream buyers

• The products that have reached maturity are now known, accepted, and the luster has worn off.– Only when a market is fully proven and they know someone who

has had the ‘experience’.

– However, they are excited about buying this product…finally theyfeel like they…

• are ready• can afford and/or justify the purchase• and don’t want to be completely left behind.

22

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

Maturity Stage: Small innovations to continue to differentiate

• Minor changes to the product help us differentiate in this crowded market.– Aim to offer ‘value for money’. We can hold prices if we can offer

greater value through our unique feature/function/look.

– The modifications must remain true to the core essence of the product and should not ‘complicate’ the proposition.

– These adaptations focus upon…• Design/Style• Ease of Use• Combination of ‘known’ features (aka VCR/DVD combis)• Credible ways of doing the primary function better (aka Pixel

Plus on CRT TVs)

23

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

We cannot ignore the mature products, but they can now ‘sell themselves’.

Company implications in the mature phase:

This is where we make our money, thus our future innovations are dependent upon getting it right here. We want to prolong the maturity phase as long as possible, through small, evolutionary innovations. The

goal is to maintain price points via these attractive premium features.

Consumer implications in the mature phase:

They typically know what they want at this stage and don’t need to be educated further. Many have waited in the wings for price to come down and/or for others to embrace and experiment with the

products first. However, many will still be looking for something that offers a little extra, an obvious benefit that doesn’t complicate the product.

Retailer implications in the mature phase:

Retailers are pressuring companies at this point to justify their worth in these soon declining categories via typically FMCG measurements, such as shelf turnover and revenue per sq. meter. They have lots of choices and we must demonstrate that we can drive their business in this established market to stay

visible to consumers.

24

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

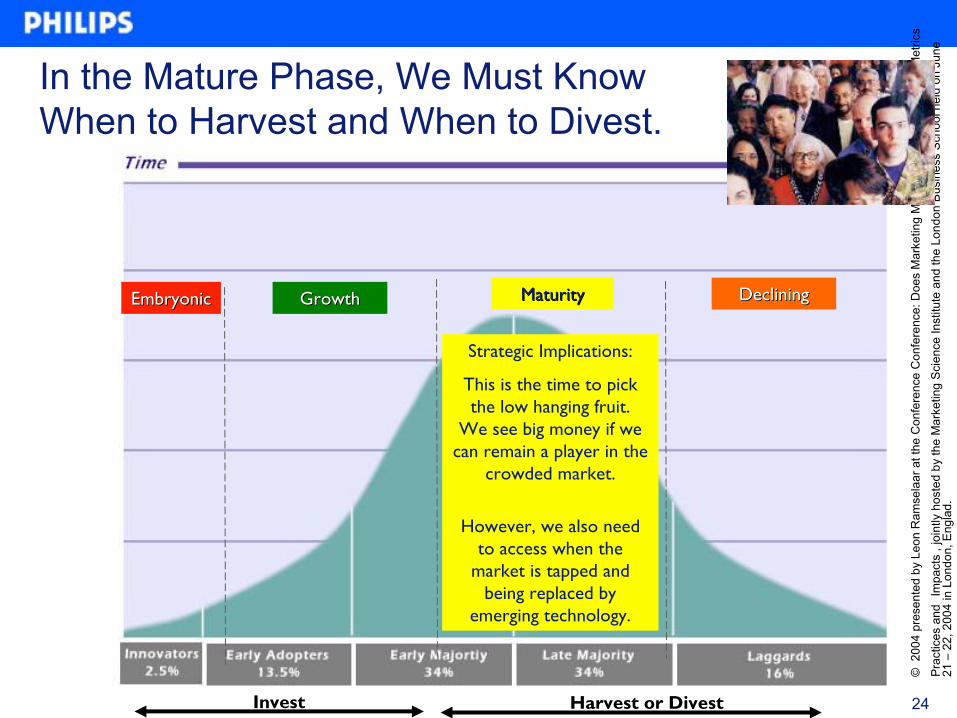

In the Mature Phase, We Must Know When to Harvest and When to Divest.

EmbryonicEmbryonic GrowthGrowth

Invest Harvest or Divest

MaturityMaturity DecliningDeclining

Strategic Implications:

This is the time to pick the low hanging fruit.

We see big money if we can remain a player in the

crowded market.

However, we also need to access when the

market is tapped and being replaced by

emerging technology.

25

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

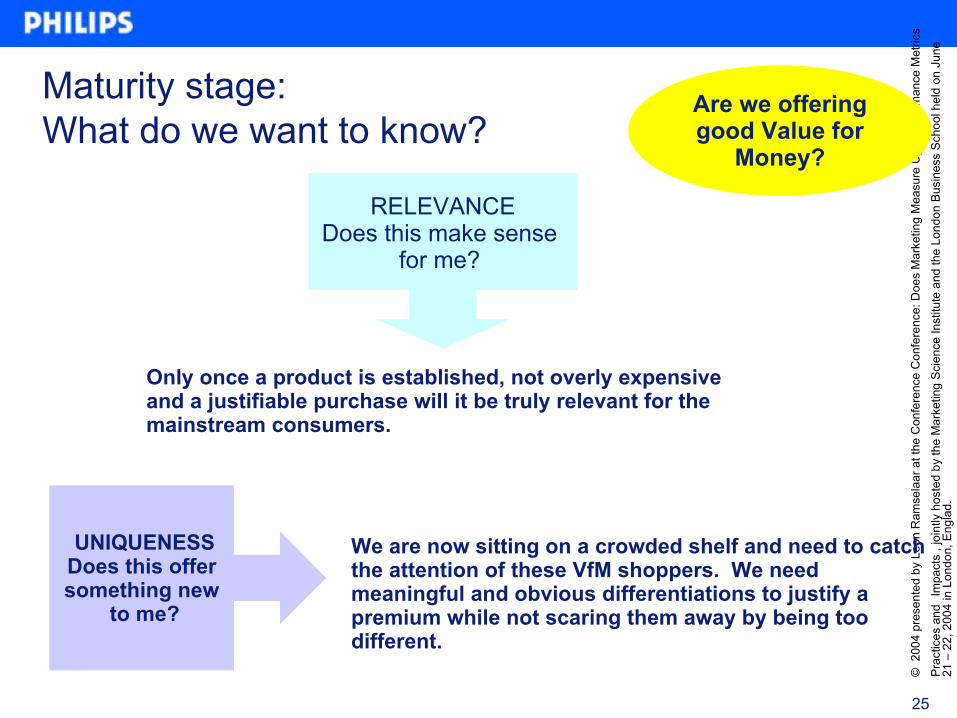

Maturity stage: What do we want to know?

Are we offering good Value for

Money?

UNIQUENESSDoes this offer something new

to me?

RELEVANCEDoes this make sense

for me?

Only once a product is established, not overly expensive and a justifiable purchase will it be truly relevant for the mainstream consumers.

We are now sitting on a crowded shelf and need to catch the attention of these VfM shoppers. We need meaningful and obvious differentiations to justify a premium while not scaring them away by being too different.

26

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

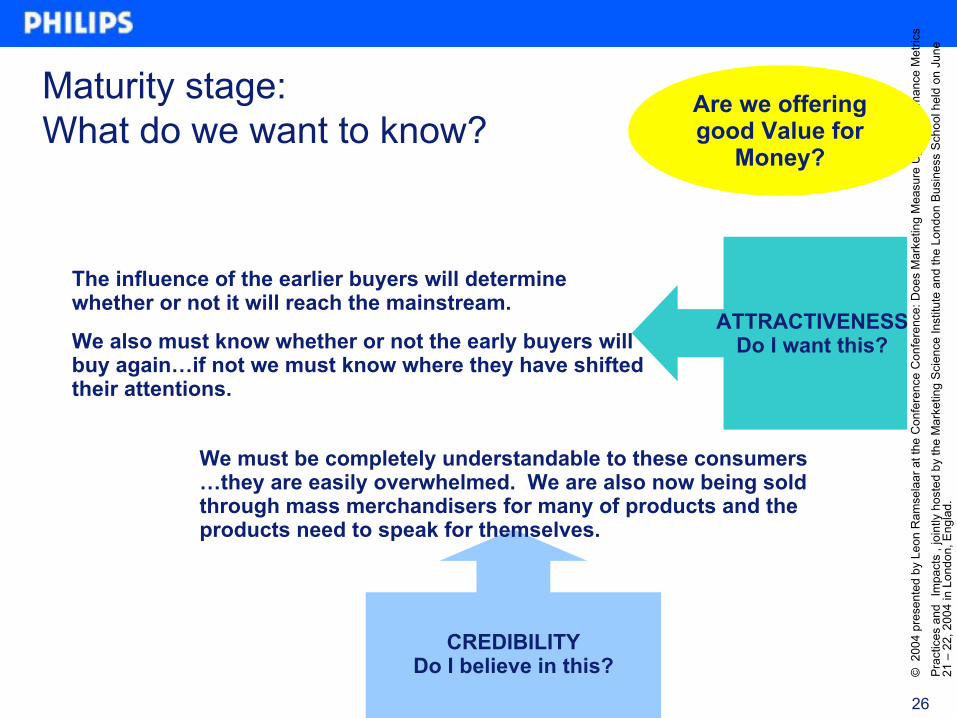

Are we offering good Value for

Money?

ATTRACTIVENESSDo I want this?

CREDIBILITYDo I believe in this?

The influence of the earlier buyers will determine whether or not it will reach the mainstream.

We also must know whether or not the early buyers will buy again…if not we must know where they have shifted their attentions.

We must be completely understandable to these consumers …they are easily overwhelmed. We are also now being sold through mass merchandisers for many of products and the products need to speak for themselves.

Maturity stage: What do we want to know?

27

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

Growth stage: The psyche of early adopters

• These consumers have likely been excited from the onset, but do not want to be the true guinea pigs.– This is where we cannot make mistakes. The market is now very

visible.

– They are still quite proud to be ‘on the cutting edge’ of a market growth, and have great influence over the next wave of buyers. They caught the buzz from the first buyers and now may be advocates themselves.

– They also typically waited for a magic price point to be hit. They are still willing to spend for innovations, but have likely had a price set in their mind before they could justify the purchase.

28

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

Growth stage: Focus on functionality ~ “meaningful innovations”

• This wave of buyers is intrigued by technology but will not buy technology for technology sake.

• Right now, the Growth stage is characterized by products that…– Bring together a number of known, and loved functionalities (DVDR).– Provide new ways to enjoy Digital content (Portable HDDs, Home

Networking)– Have been long desired, with many consumers holding out until the

pricing reaches their thresholds (Flat TVs) – Address a dormant need and become an essential item in consumers

lives (Mobile Phones a few years ago)– Delivers a better, more immersive, more enjoyable experience (HTiB)

29

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

Small, incremental innovations keep these products exciting and draw consumers into the market.

Company implications in the growth phase:The product is now in the limelight and we can share some of this glory if we have gotten it right in the

early stages (DVDR). We need to continue to innovate but not radically, and continue to build a buzz via incremental steps. The risk has subsided and there is internal optimism…”We knew this would work.”

Consumer implications in the growth phase:Consumers have recognized the benefits of the product and have been waiting for ‘word of mouth’ to support their desire or for a magic price point to be achieved. They still may have lots of questions, but

as long as they feel they can understand the product and envision it in their lives…they are ready to jump into the market.

Retailer implications in the growth phase:

Retailers are now giving these products substantial store space. They are now confident about the product possibilities and will ‘know’ how to sell them. We also see mass merchandisers wanting to get a

hold of a product once it has proven itself; however also typically then speeding up the price erosion.

30

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

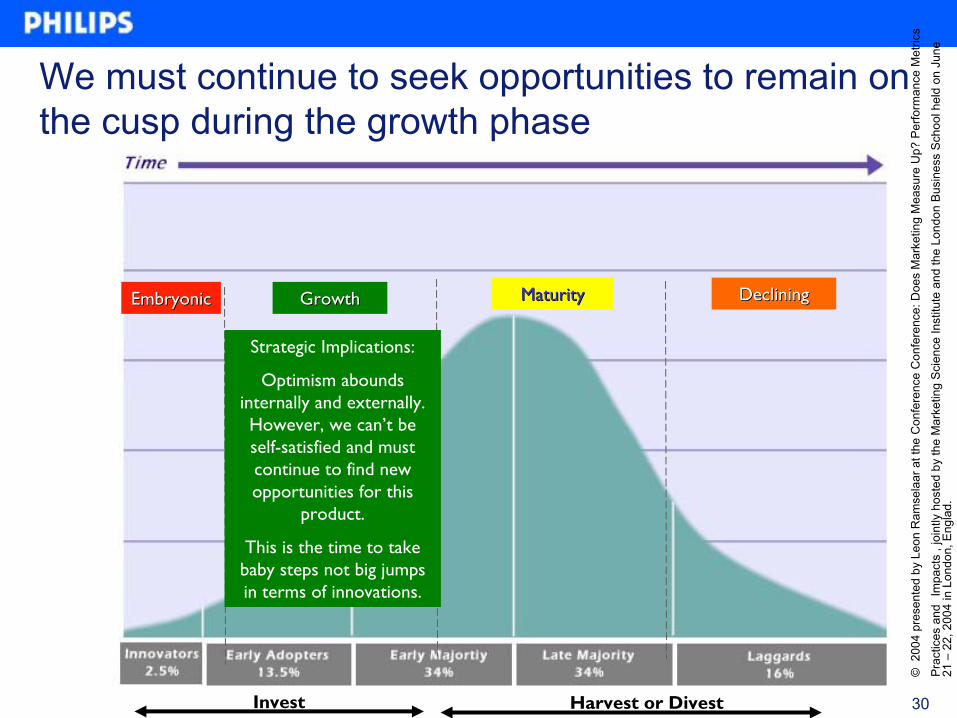

We must continue to seek opportunities to remain on the cusp during the growth phase

EmbryonicEmbryonic GrowthGrowth

Invest Harvest or Divest

MaturityMaturity DecliningDeclining

Strategic Implications:

Optimism abounds internally and externally. However, we can’t be self-satisfied and must continue to find new opportunities for this

product.

This is the time to take baby steps not big jumps in terms of innovations.

31

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

Growth stage: What do we want to know?

UNIQUENESSDoes this offer something new

to me?

RELEVANCEDoes this make sense

for me?

Consumers must be able to envision this product in the lives and in their homes. Once interested, they will be seeking lots of information from all sources…on their own, through friends who are in the know and in the stores to confirm that this is something for them.

We need to be innovative, but now in a more controlled way. Too much uniqueness can have a polarizing effect…and force consumers to wait a little longer if they find it to be too much of a stretch. Minor innovations to the core proposition along this part of the curve are the way to make it move.

Are we ready for the take-off?

32

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

ATTRACTIVENESSDo I want this?

CREDIBILITYDo I believe in this?

If the buzz from the first buyers is revving high, this will be an attractive proposition to the second wave of consumers. We then must ensure that they can find the information they need to convert the feeling of ‘I would like to have it’ to ‘ I must have it’.

They believe that this is something that will make their lives better, more enjoyable, easier, more connected, etc… and this belief must be confirmed during their info search. They also must feel comfortable that they know what they are getting themselves into with this purchase.

Are we ready for the take-off?

Growth stage: What do we want to know?

33

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

Embryonic stage: The psyche of first buyers

• The Embryonic products will only appeal to those who revel in technology, take immense amount of pleasure in being truly the first, and find great satisfaction and pride in being able to make work.

– We want and need to be selling technology at this point in time.This is a stage of experimentation for us and the consumers.

– They are willing to absorb lots of risk, and take pride in the amount that they spend to own something right as it hits the shelf. Price is not the barrier if they are intrigued.

– These products are their toys, and they are willing to abandon something quickly if it’s not working; or boast to their friends when it does push their buttons. (Blackberry, etc.)

34

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

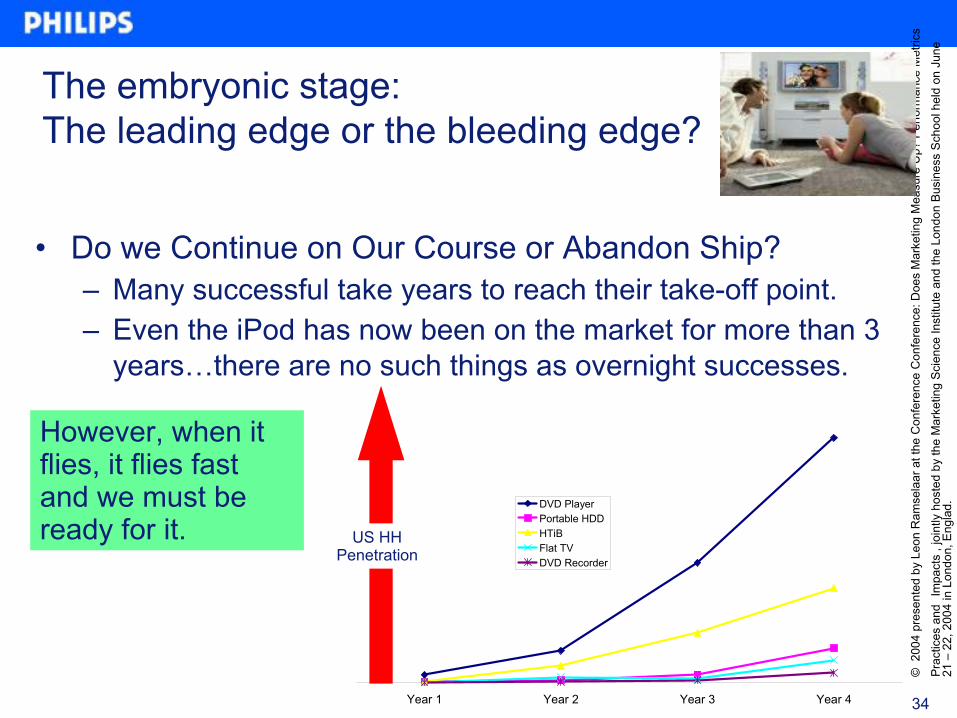

The embryonic stage:The leading edge or the bleeding edge?

• Do we Continue on Our Course or Abandon Ship?– Many successful take years to reach their take-off point. – Even the iPod has now been on the market for more than 3

years…there are no such things as overnight successes.

Year 1 Year 2 Year 3 Year 4

DVD PlayerPortable HDDHTiBFlat TVDVD Recorder

US HHPenetration

However, when it flies, it flies fast and we must be ready for it.

35

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

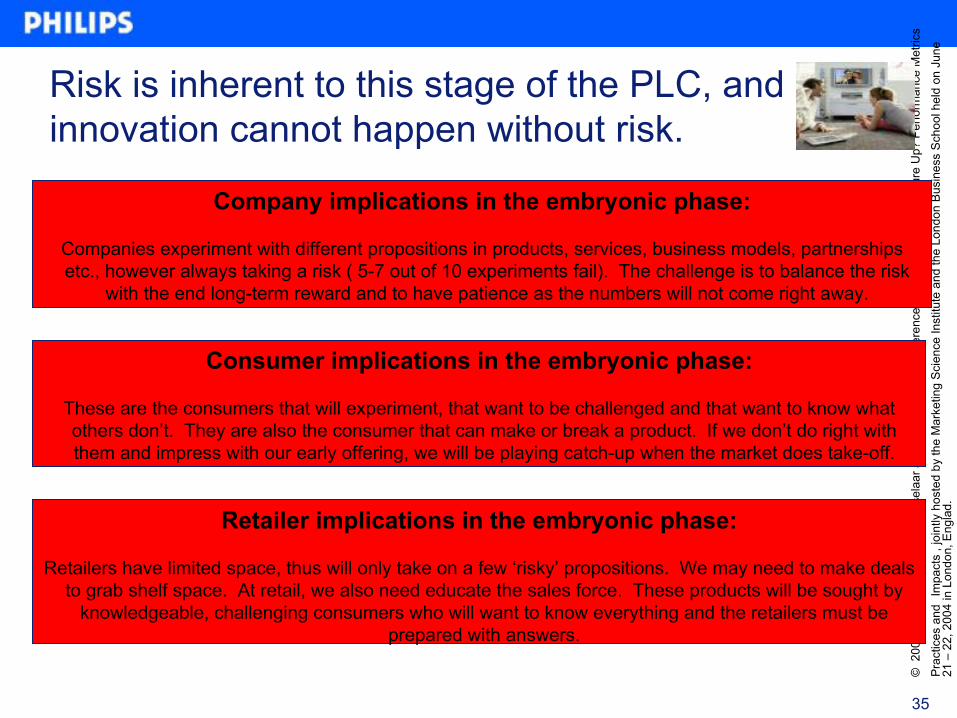

Risk is inherent to this stage of the PLC, and innovation cannot happen without risk.

Company implications in the embryonic phase:

Companies experiment with different propositions in products, services, business models, partnerships etc., however always taking a risk ( 5-7 out of 10 experiments fail). The challenge is to balance the risk

with the end long-term reward and to have patience as the numbers will not come right away.

Consumer implications in the embryonic phase:

These are the consumers that will experiment, that want to be challenged and that want to know what others don’t. They are also the consumer that can make or break a product. If we don’t do right with them and impress with our early offering, we will be playing catch-up when the market does take-off.

Retailer implications in the embryonic phase:

Retailers have limited space, thus will only take on a few ‘risky’ propositions. We may need to make deals to grab shelf space. At retail, we also need educate the sales force. These products will be sought by

knowledgeable, challenging consumers who will want to know everything and the retailers must be prepared with answers.

36

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

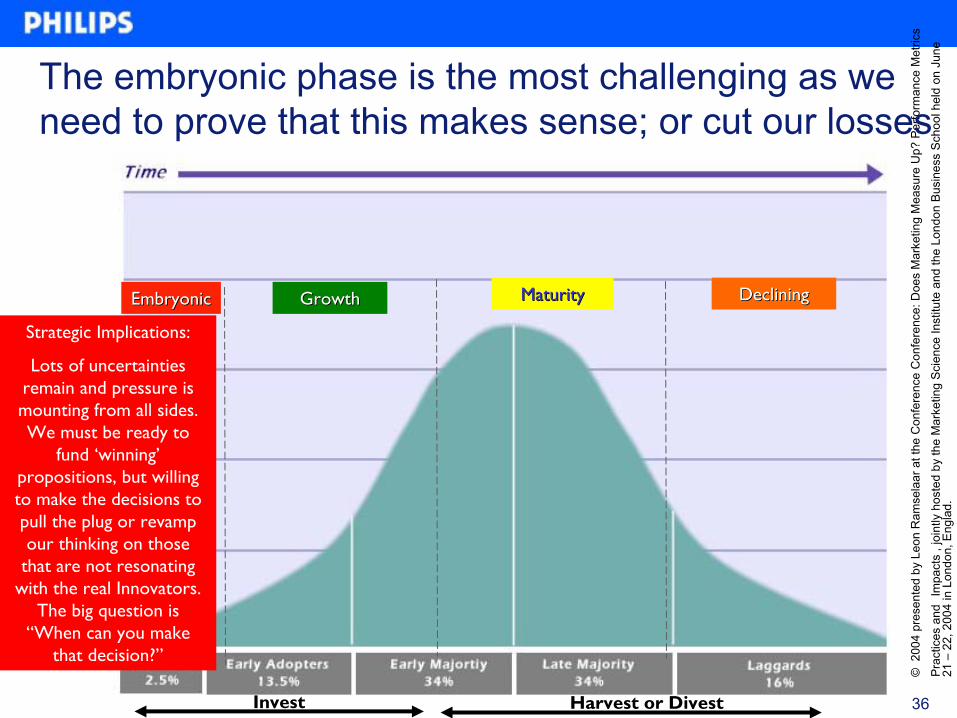

The embryonic phase is the most challenging as we need to prove that this makes sense; or cut our losses

EmbryonicEmbryonic GrowthGrowth

Invest Harvest or Divest

MaturityMaturity DecliningDeclining

Strategic Implications:

Lots of uncertainties remain and pressure is mounting from all sides. We must be ready to

fund ‘winning’ propositions, but willing to make the decisions to pull the plug or revamp our thinking on those

that are not resonating with the real Innovators.

The big question is “When can you make

that decision?”

37

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

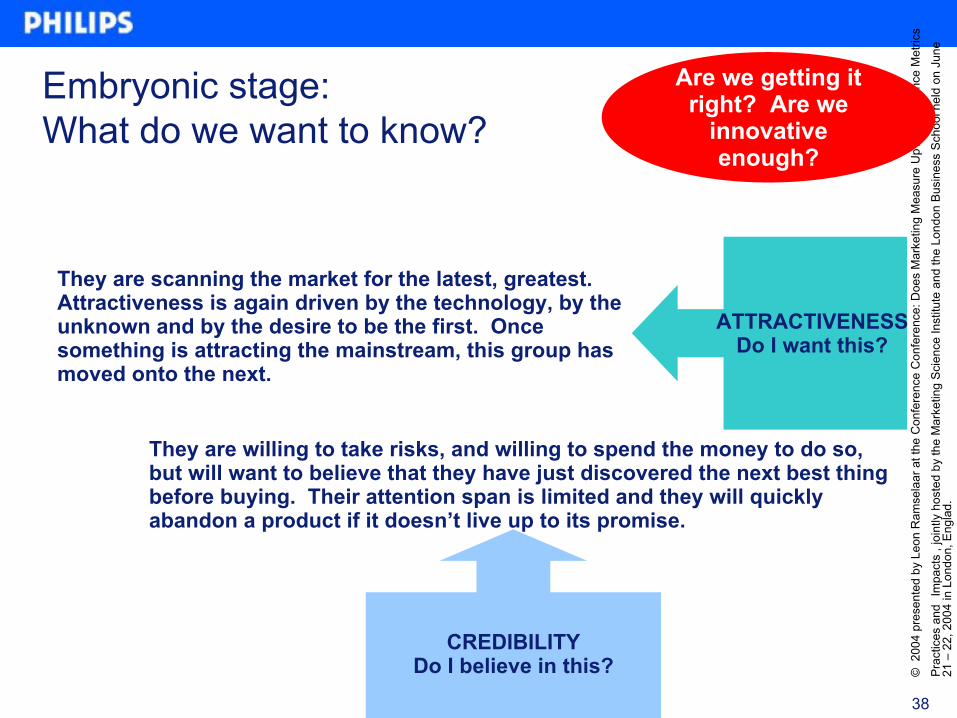

Embryonic stage: What do we want to know?

UNIQUENESSDoes this offer something new

to me?

RELEVANCEDoes this make sense

for me?

This only makes sense for them if it is an recognizable advancement of technology. They want the revolutions and they want to be at the forefront of the movement.

New products must have a ‘Wow’ factor to grab the attention of the true Innovators. They are seeking surprises and are energized rather than frustrated by technology.

Are we getting it right? Are we

innovative enough?

38

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

ATTRACTIVENESSDo I want this?

CREDIBILITYDo I believe in this?

They are scanning the market for the latest, greatest. Attractiveness is again driven by the technology, by the unknown and by the desire to be the first. Once something is attracting the mainstream, this group has moved onto the next.

They are willing to take risks, and willing to spend the money to do so, but will want to believe that they have just discovered the next best thing before buying. Their attention span is limited and they will quickly abandon a product if it doesn’t live up to its promise.

Are we getting it right? Are we

innovative enough?

Embryonic stage: What do we want to know?

39

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

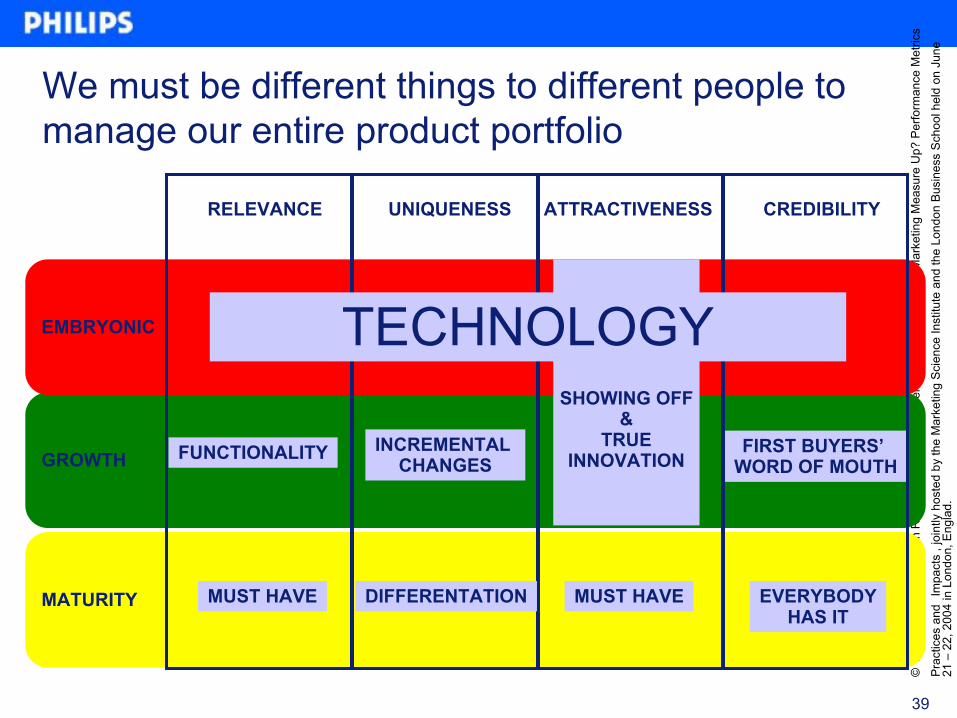

GROWTHFIRST BUYERS’

WORD OF MOUTH

EMBRYONIC

SHOWING OFF&

TRUEINNOVATION

We must be different things to different people to manage our entire product portfolio

MATURITY

RELEVANCE UNIQUENESS ATTRACTIVENESS CREDIBILITY

TECHNOLOGY

FUNCTIONALITY INCREMENTAL CHANGES

MUST HAVE DIFFERENTATION MUST HAVE EVERYBODYHAS IT

40

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

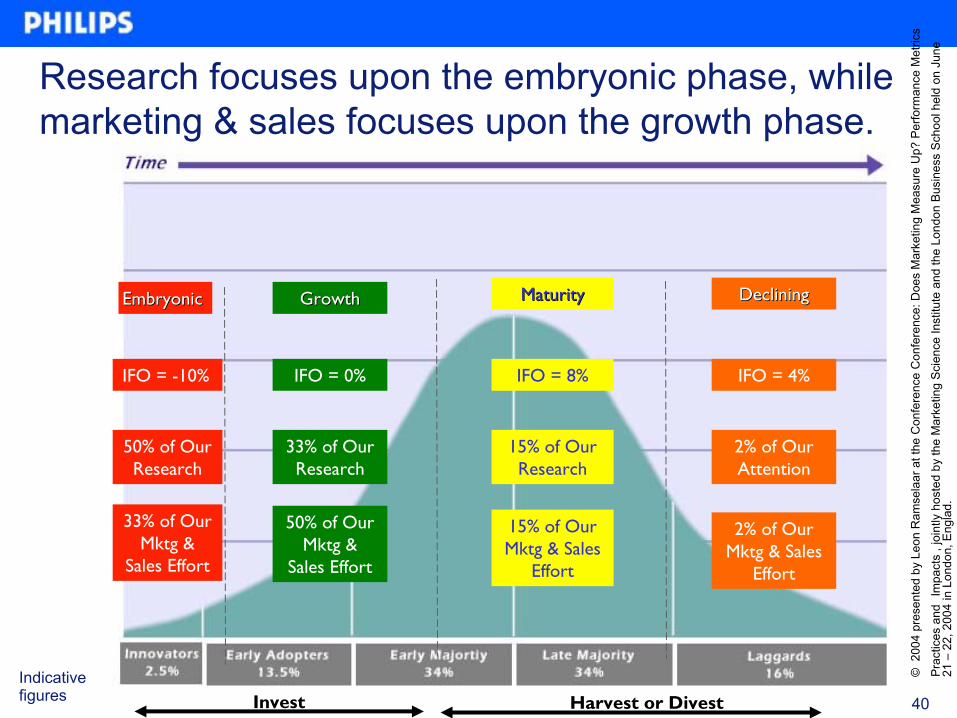

Research focuses upon the embryonic phase, while marketing & sales focuses upon the growth phase.

EmbryonicEmbryonic GrowthGrowth

Invest Harvest or Divest

MaturityMaturity DecliningDeclining

IFO = -10% IFO = 0% IFO = 8% IFO = 4%

50% of Our Research

33% of Our Research

15% of Our Research

2% of Our Attention

33% of Our Mktg &

Sales Effort

50% of Our Mktg &

Sales Effort

15% of Our Mktg & Sales

Effort

2% of Our Mktg & Sales

Effort

Indicative figures

41

©20

04 p

rese

nted

by

Leon

Ram

sela

arat

the

Con

fere

nce

Con

fere

nce:

Doe

s M

arke

ting

Mea

sure

Up?

Per

form

ance

Met

rics

Pra

ctic

es a

ndIm

pact

s , j

oint

ly h

oste

d by

the

Mar

ketin

g S

cien

ce In

stitu

te a

nd th

e Lo

ndon

Bus

ines

s Sc

hool

hel

d on

Jun

e 21

–22

, 200

4 in

Lon

don,

Eng

lad.

In summary…

• In the Consumer Electronics business, we need to fuel innovation with profits from mature products.

• Different metrics for different PLC phases, however there is a framework that works across the entire lifecycle.

• Relevance• Attractiveness• Uniqueness• Credibility

• In each phase the critical success factors are known

• Research and Marketing efforts must focus on the early phases to be able to reap the benefits of maturity.