Market Research Report : Logistics market in china 2014 - Sample

Upload

netscribes-incCategory

view

26download

2

Insert Cover Image using Slide Master View

Do not distort

Foundry Market – India

June 2014

2 FOUNDRY MARKET IN INDIA 2014.PPT

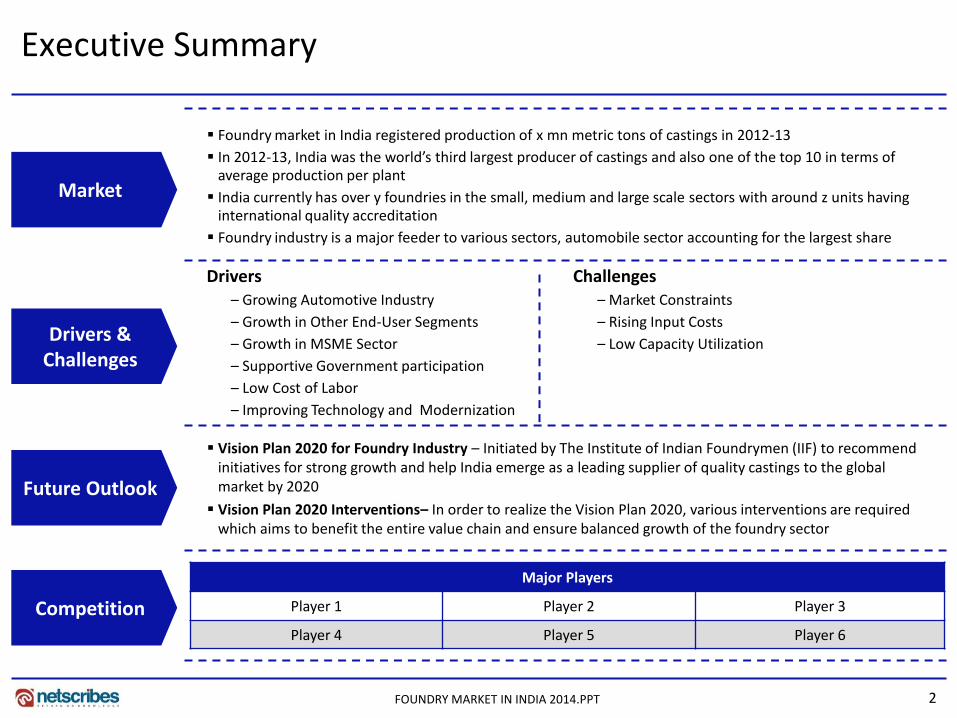

Executive Summary

Market

Drivers & Challenges

Future Outlook

Competition

Foundry market in India registered production of x mn metric tons of castings in 2012-13

In 2012-13, India was the world’s third largest producer of castings and also one of the top 10 in terms of average production per plant

India currently has over y foundries in the small, medium and large scale sectors with around z units having international quality accreditation

Foundry industry is a major feeder to various sectors, automobile sector accounting for the largest share

Vision Plan 2020 for Foundry Industry – Initiated by The Institute of Indian Foundrymen (IIF) to recommend initiatives for strong growth and help India emerge as a leading supplier of quality castings to the global market by 2020

Vision Plan 2020 Interventions– In order to realize the Vision Plan 2020, various interventions are required which aims to benefit the entire value chain and ensure balanced growth of the foundry sector

Drivers – Growing Automotive Industry

– Growth in Other End-User Segments

– Growth in MSME Sector

– Supportive Government participation

– Low Cost of Labor

– Improving Technology and Modernization

Challenges – Market Constraints

– Rising Input Costs

– Low Capacity Utilization

Major Players

Player 1 Player 2 Player 3

Player 4 Player 5 Player 6

3

•Macroeconomic Indicators

•Introduction

•Market Overview

•Foundry Clusters

•Export-Import

•Drivers & Challenges

•Competition

•Future Outlook

•Strategic Recommendations

•Appendix FOUNDRY MARKET IN INDIA 2014.PPT

4

Economic Indicators (1/3)

INR tn

Q4 Q3 Q2 Q1

2013-14 2012-13 2011-12 2010-11

GDP at Factor Cost: Quarterly

Inflation Rate: Monthly

Sep 2013 - Oct 2013 Nov 2013 - Dec 2013 Jul 2013 - Aug 2013 Aug 2013 - Sep 2013 Oct 2013 - Nov 2013

%

FOUNDRY MARKET IN INDIA 2014.PPT

5

•Macroeconomic Indicators

•Introduction

•Market Overview

•Foundry Clusters

•Export-Import

•Drivers & Challenges

•Competition

•Future Outlook

•Strategic Recommendations

•Appendix FOUNDRY MARKET IN INDIA 2014.PPT

6

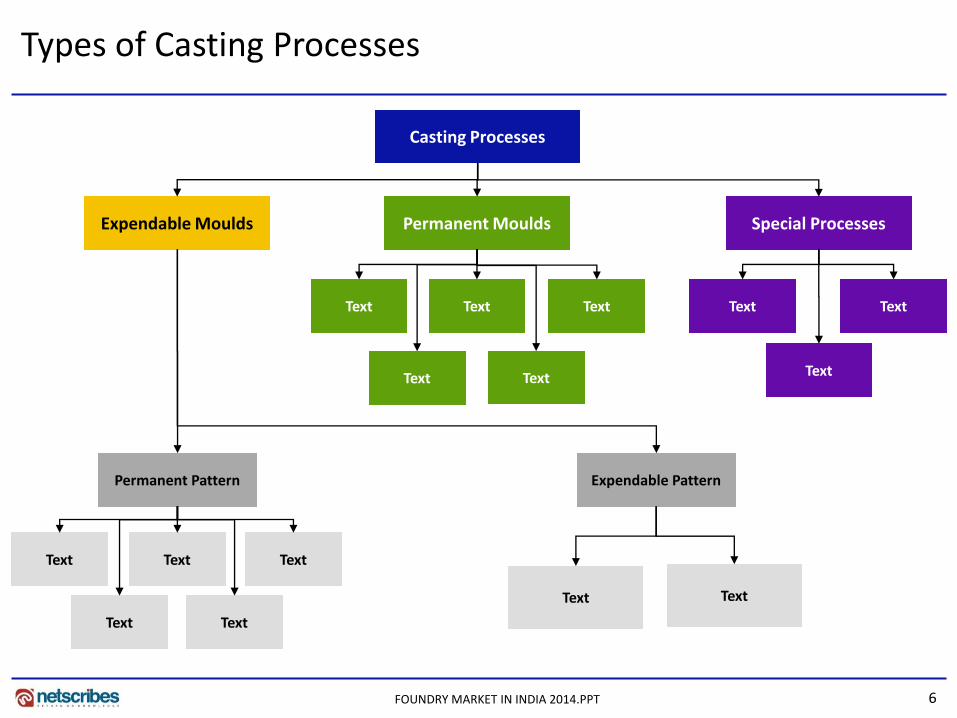

Types of Casting Processes

Casting Processes

Expendable Moulds Permanent Moulds Special Processes

Text Text

Text

Text Text Text

Text Text

Permanent Pattern Expendable Pattern

Text Text Text

Text Text

Text Text

FOUNDRY MARKET IN INDIA 2014.PPT

7

•Macroeconomic Indicators

•Introduction

•Market Overview

•Foundry Clusters

•Export-Import

•Drivers & Challenges

•Competition

•Future Outlook

•Strategic Recommendations

•Appendix FOUNDRY MARKET IN INDIA 2014.PPT

8

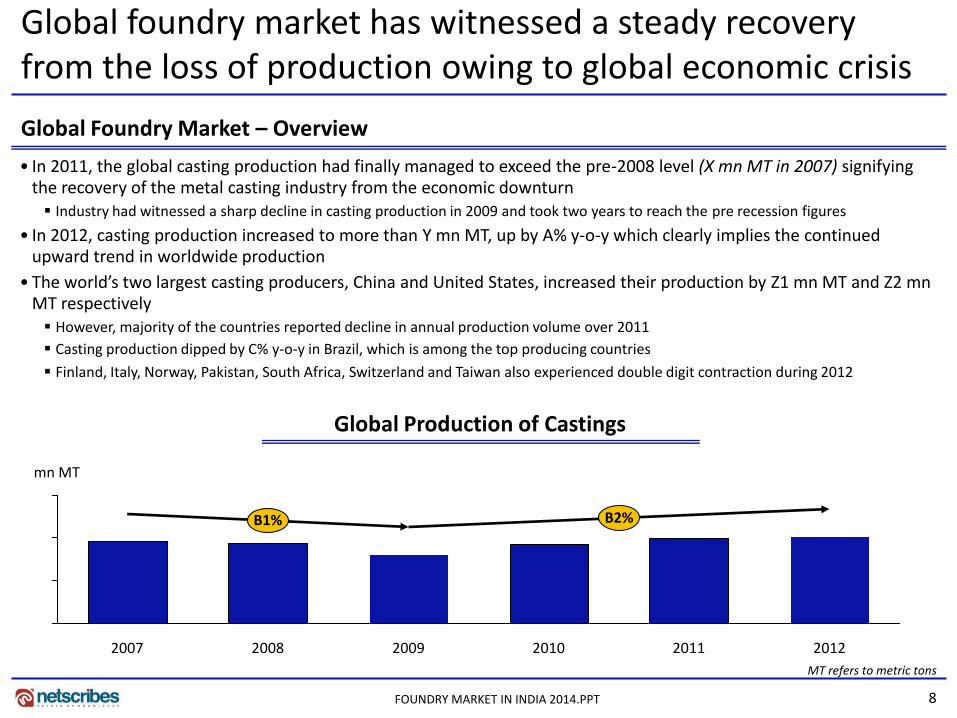

Global foundry market has witnessed a steady recovery from the loss of production owing to global economic crisis

Global Foundry Market – Overview

• In 2011, the global casting production had finally managed to exceed the pre-2008 level (X mn MT in 2007) signifying the recovery of the metal casting industry from the economic downturn Industry had witnessed a sharp decline in casting production in 2009 and took two years to reach the pre recession figures

• In 2012, casting production increased to more than Y mn MT, up by A% y-o-y which clearly implies the continued upward trend in worldwide production

• The world’s two largest casting producers, China and United States, increased their production by Z1 mn MT and Z2 mn MT respectively However, majority of the countries reported decline in annual production volume over 2011

Casting production dipped by C% y-o-y in Brazil, which is among the top producing countries

Finland, Italy, Norway, Pakistan, South Africa, Switzerland and Taiwan also experienced double digit contraction during 2012

2008 2007 2009

B2% B1%

2012 2010 2011

mn MT

Global Production of Castings

MT refers to metric tons

FOUNDRY MARKET IN INDIA 2014.PPT

9

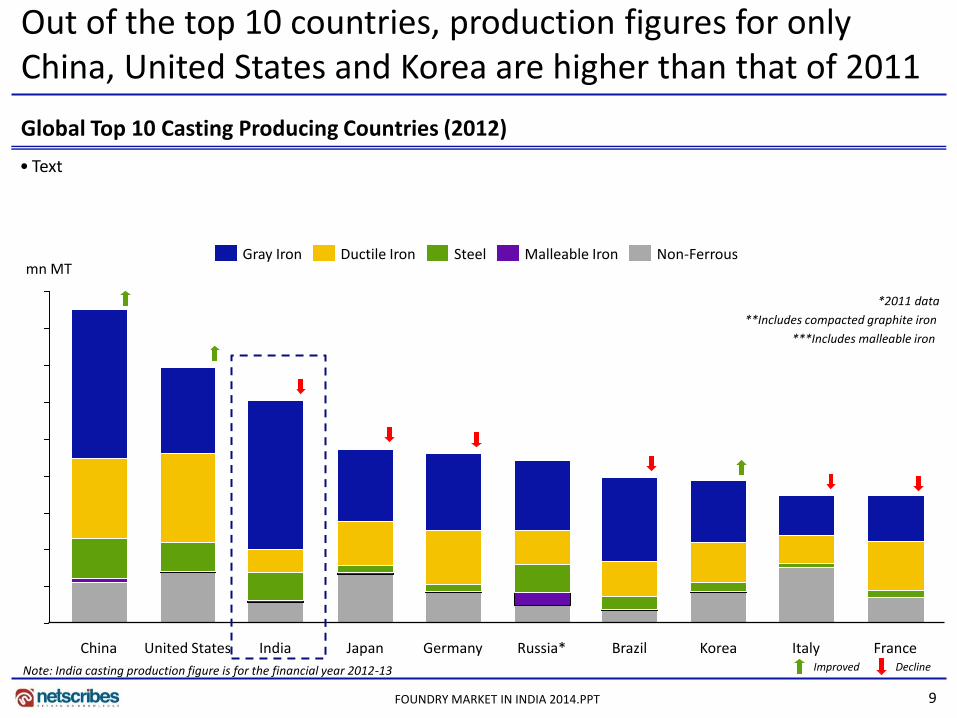

Out of the top 10 countries, production figures for only China, United States and Korea are higher than that of 2011

Global Top 10 Casting Producing Countries (2012)

China

mn MT Ductile Iron Steel Non-Ferrous Malleable Iron Gray Iron

United States India Japan Germany Russia* Brazil Korea Italy France

• Text

Note: India casting production figure is for the financial year 2012-13

*2011 data

**Includes compacted graphite iron

***Includes malleable iron

Improved Decline

FOUNDRY MARKET IN INDIA 2014.PPT

10

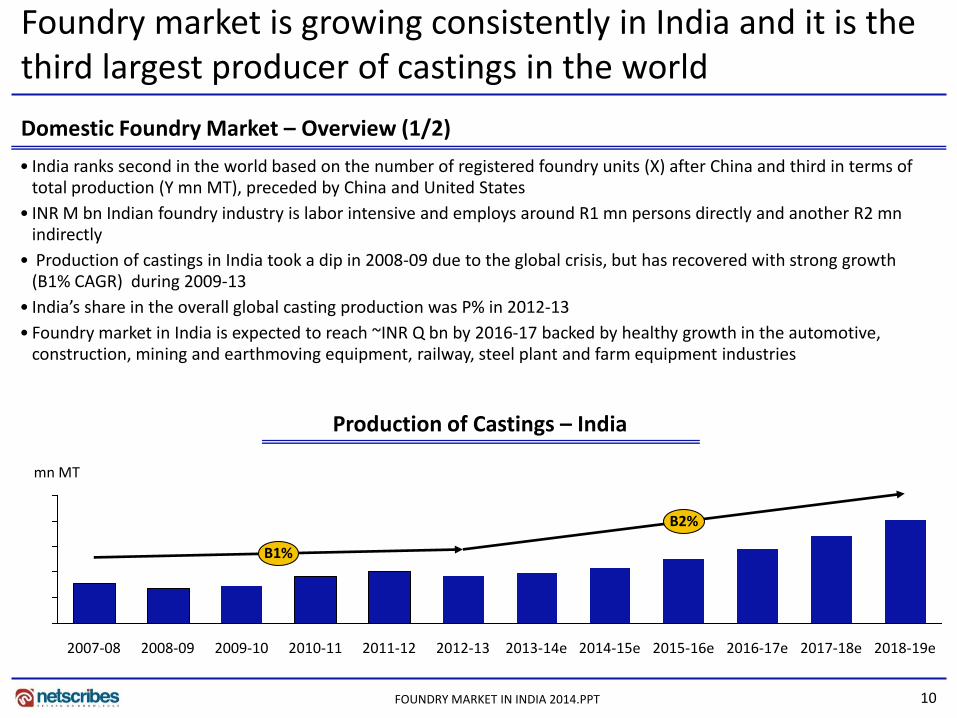

Foundry market is growing consistently in India and it is the third largest producer of castings in the world

Domestic Foundry Market – Overview (1/2) • India ranks second in the world based on the number of registered foundry units (X) after China and third in terms of

total production (Y mn MT), preceded by China and United States

• INR M bn Indian foundry industry is labor intensive and employs around R1 mn persons directly and another R2 mn indirectly

• Production of castings in India took a dip in 2008-09 due to the global crisis, but has recovered with strong growth (B1% CAGR) during 2009-13

• India’s share in the overall global casting production was P% in 2012-13

• Foundry market in India is expected to reach ~INR Q bn by 2016-17 backed by healthy growth in the automotive, construction, mining and earthmoving equipment, railway, steel plant and farm equipment industries

B1%

mn MT

2012-13 2014-15e 2013-14e 2009-10 2007-08 2011-12 2010-11 2008-09

B2%

2015-16e 2017-18e 2016-17e 2018-19e

Production of Castings – India

FOUNDRY MARKET IN INDIA 2014.PPT

11

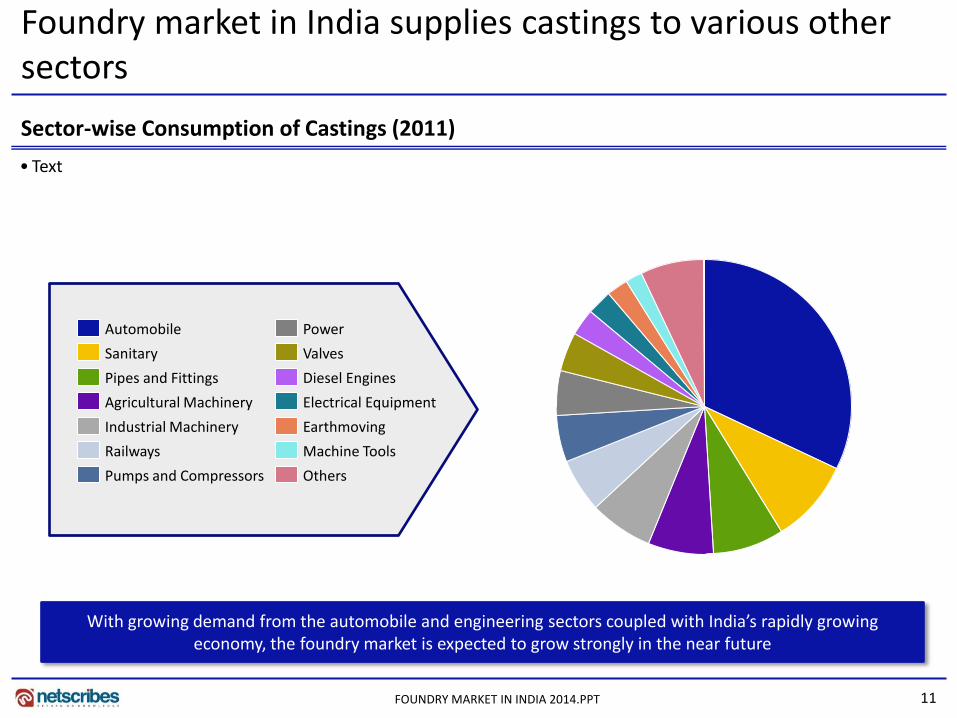

Foundry market in India supplies castings to various other sectors

Sector-wise Consumption of Castings (2011)

• Text

Diesel Engines

Machine Tools

Electrical Equipment

Earthmoving

Railways

Valves

Others Pumps and Compressors

Power

Sanitary

Pipes and Fittings

Industrial Machinery

Automobile

Agricultural Machinery

With growing demand from the automobile and engineering sectors coupled with India’s rapidly growing economy, the foundry market is expected to grow strongly in the near future

FOUNDRY MARKET IN INDIA 2014.PPT

12

•Macroeconomic Indicators

•Introduction

•Market Overview

•Foundry Clusters

•Export-Import

•Drivers & Challenges

•Competition

•Future Outlook

•Strategic Recommendations

•Appendix FOUNDRY MARKET IN INDIA 2014.PPT

13

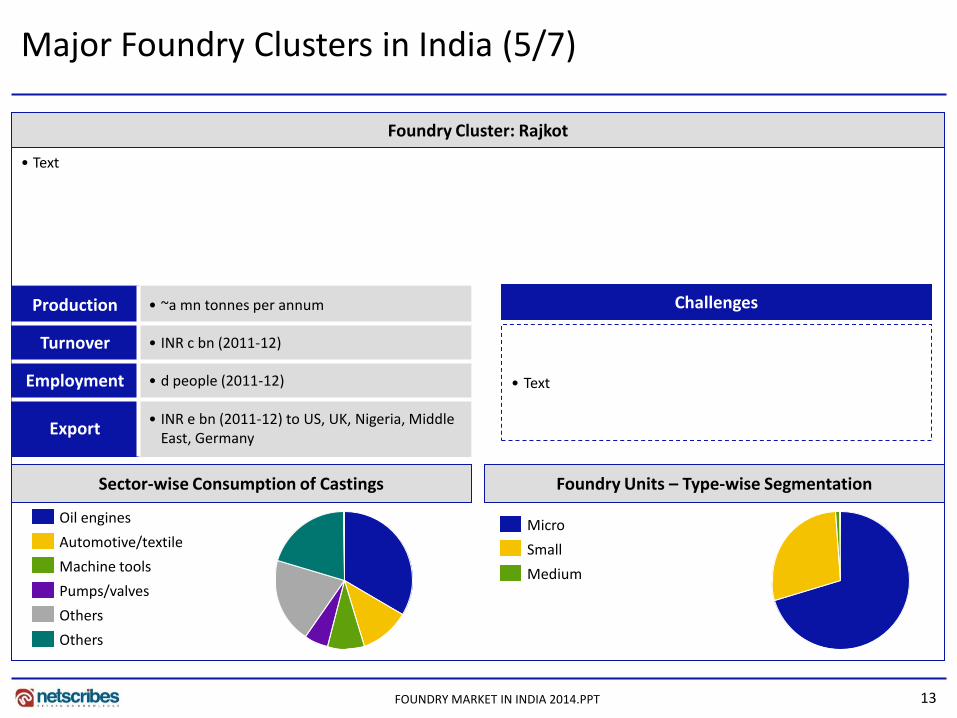

Major Foundry Clusters in India (5/7)

• Text

Foundry Cluster: Rajkot

Sector-wise Consumption of Castings

Pumps/valves

Machine tools

Automotive/textile

Oil engines

Others

Others

Foundry Units – Type-wise Segmentation

Medium

Small

Micro

Production • ~a mn tonnes per annum

Turnover • INR c bn (2011-12)

Employment • d people (2011-12)

Export • INR e bn (2011-12) to US, UK, Nigeria, Middle

East, Germany

• Text

Challenges

FOUNDRY MARKET IN INDIA 2014.PPT

14

•Macroeconomic Indicators

•Introduction

•Market Overview

•Foundry Clusters

•Export-Import

•Drivers & Challenges

•Competition

•Future Outlook

•Strategic Recommendations

•Appendix FOUNDRY MARKET IN INDIA 2014.PPT

15

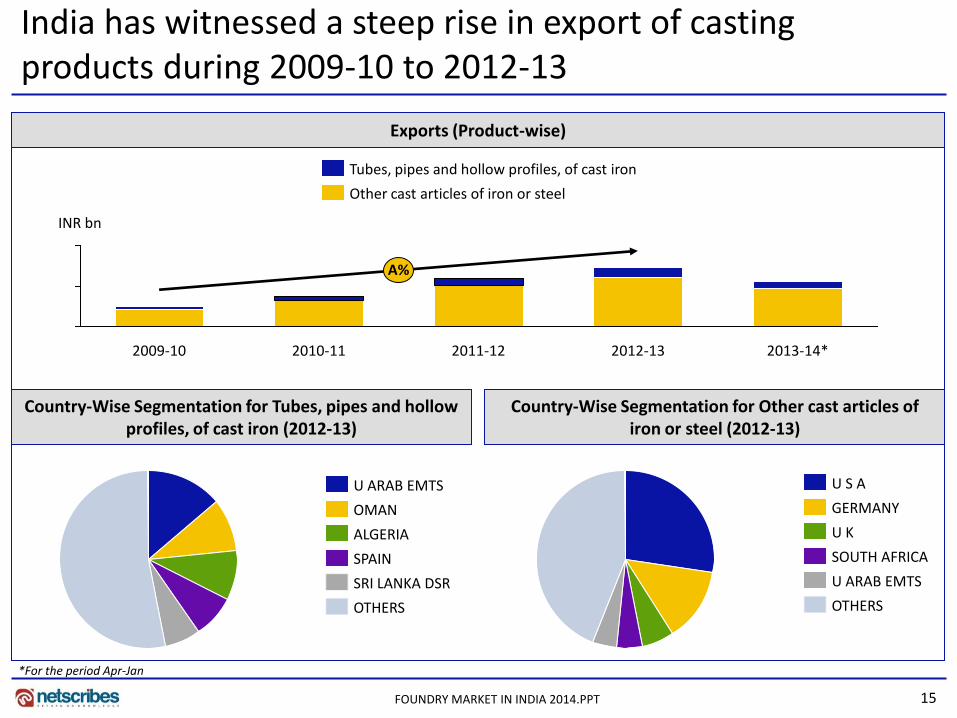

India has witnessed a steep rise in export of casting products during 2009-10 to 2012-13

Exports (Product-wise)

Country-Wise Segmentation for Tubes, pipes and hollow profiles, of cast iron (2012-13)

Country-Wise Segmentation for Other cast articles of iron or steel (2012-13)

SRI LANKA DSR

SPAIN

ALGERIA

OMAN

U ARAB EMTS

OTHERS

U ARAB EMTS

SOUTH AFRICA

U K

OTHERS

GERMANY

U S A

*For the period Apr-Jan

2012-13 2009-10

A%

INR bn

2011-12 2010-11 2013-14*

Tubes, pipes and hollow profiles, of cast iron

Other cast articles of iron or steel

FOUNDRY MARKET IN INDIA 2014.PPT

16

•Macroeconomic Indicators

•Introduction

•Market Overview

•Foundry Clusters

•Export-Import

•Drivers & Challenges

•Competition

•Future Outlook

•Strategic Recommendations

•Appendix FOUNDRY MARKET IN INDIA 2014.PPT

17

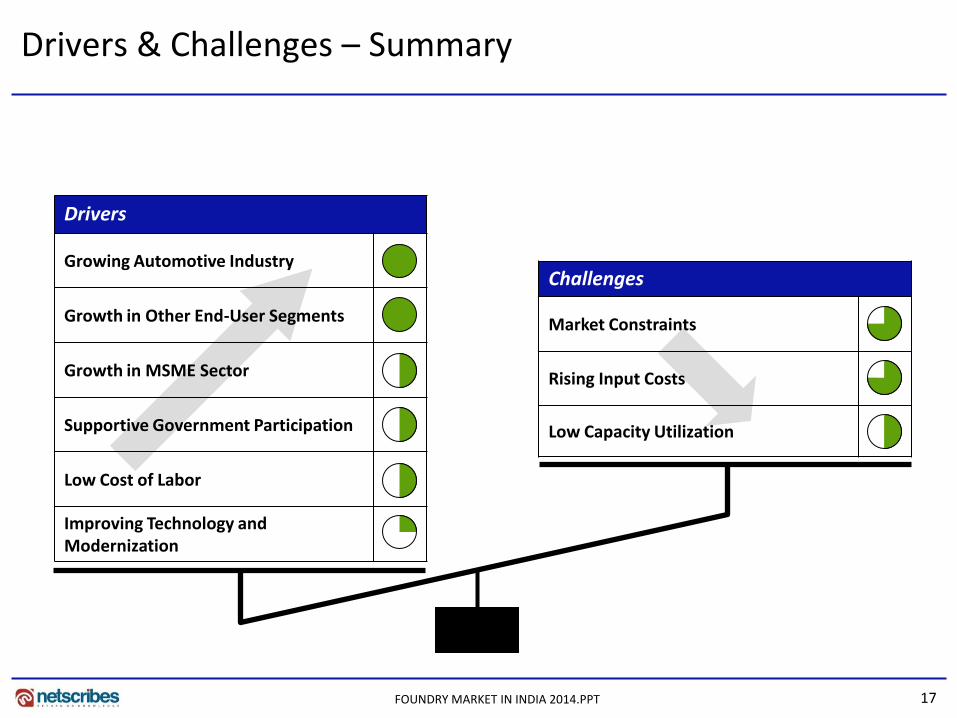

Drivers & Challenges – Summary

Drivers

Growing Automotive Industry

Growth in Other End-User Segments

Growth in MSME Sector

Supportive Government Participation

Low Cost of Labor

Improving Technology and Modernization

Challenges

Market Constraints

Rising Input Costs

Low Capacity Utilization

FOUNDRY MARKET IN INDIA 2014.PPT

18

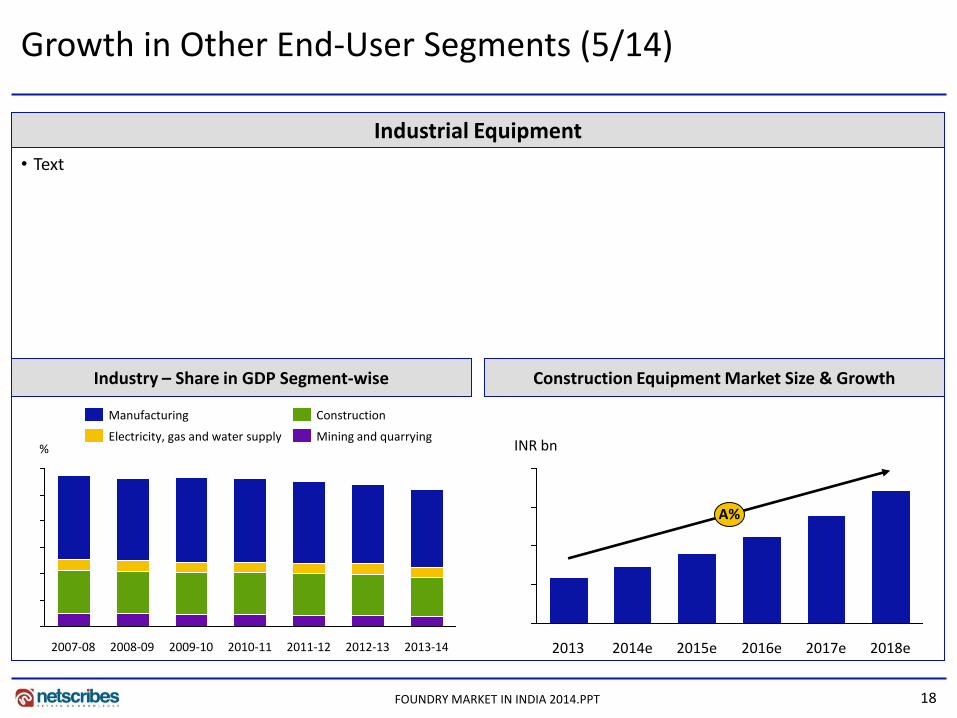

Growth in Other End-User Segments (5/14)

• Text

Industrial Equipment

Industry – Share in GDP Segment-wise Construction Equipment Market Size & Growth

INR bn

A%

2018e 2017e 2016e 2015e 2014e 2013 2007-08

%

2013-14 2012-13 2011-12 2010-11 2009-10 2008-09

Mining and quarrying Electricity, gas and water supply

Construction Manufacturing

FOUNDRY MARKET IN INDIA 2014.PPT

19

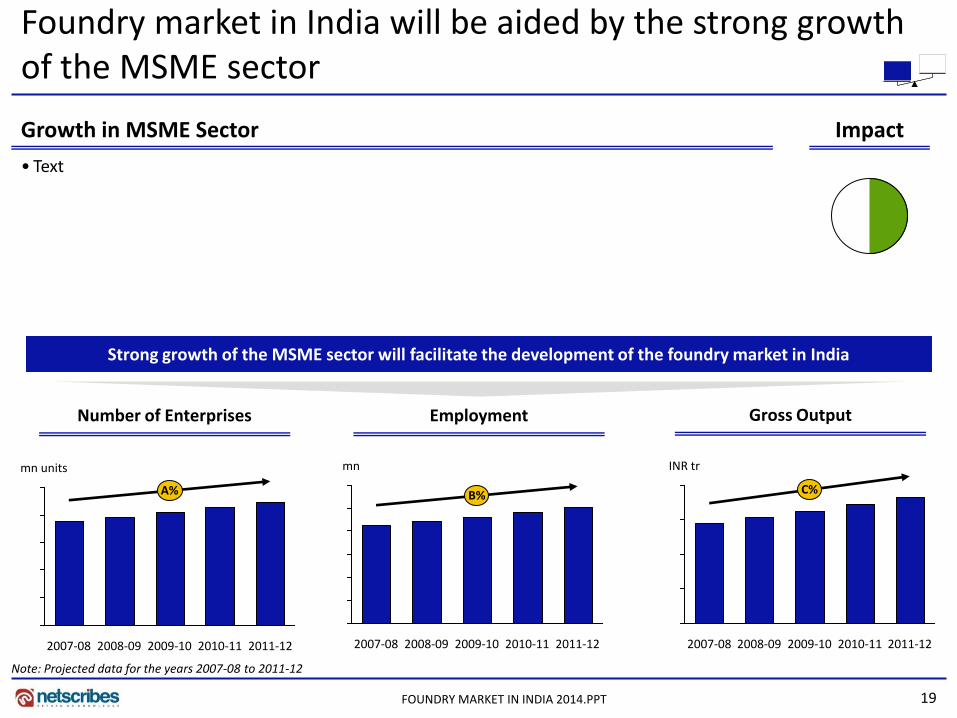

Growth in MSME Sector

Foundry market in India will be aided by the strong growth of the MSME sector

• Text

Impact

Number of Enterprises Employment Gross Output

Strong growth of the MSME sector will facilitate the development of the foundry market in India

2007-08 2008-09 2009-10 2010-11 2011-12

A%

mn units mn

B%

2011-12 2010-11 2009-10 2008-09 2007-08 2010-11 2011-12 2007-08

INR tr

2008-09

C%

2009-10

Note: Projected data for the years 2007-08 to 2011-12

FOUNDRY MARKET IN INDIA 2014.PPT

20

•Macroeconomic Indicators

•Introduction

•Market Overview

•Foundry Clusters

•Export-Import

•Drivers & Challenges

•Competition

•Future Outlook

•Strategic Recommendations

•Appendix FOUNDRY MARKET IN INDIA 2014.PPT

21

Porter’s Five Forces Analysis

Competitive Rivalry

• Text

Bargaining Power of Suppliers

• Text

Bargaining Power of Buyers

• Text

Threat of Substitutes

• Text

Threat of New Entrants

• Text

Impact Text

Impact Text

Impact Text

Impact Text

Impact Text

FOUNDRY MARKET IN INDIA 2014.PPT

22

Competitive Benchmarking (1/5)

Public Trading Comparables (FY 2014)

Player 1 Player 2 Player 3 Player 4

Market Capitalization (INR mn)

Share Price (INR)

EV/EBITDA (INR mn)

EV/Revenue (INR mn)

PE Ratio

Note: Market Capitalization, Share Price and PE ratio is as of 3rdJun 2014

FOUNDRY MARKET IN INDIA 2014.PPT

23

Key Ratios of Major 3 Public Companies – Operational Basis (FY 2013) (1/3)

Competitive Benchmarking (2/5)

Player 3 Player 2 Player 1

% Net Margin Operating Margin

• Text

FOUNDRY MARKET IN INDIA 2014.PPT

24

Public: Domestic Company – Player 1 (1/5)

Key People

Products and Services

Company Information Offices and Centres – India

Corporate Address

Tel No. +

Fax No. +

Website

Year of Incorporation

Ticker Symbol

Stock Exchange

Category Products/Services

Name Designation

Note: The list of products and services is not exhaustive

Head Office

FOUNDRY MARKET IN INDIA 2014.PPT

25

Public: Domestic Company – Player 1 (2/5) Financial Snapshot Key Ratios

Financial Summary

• The company incurred a net loss of INR -- mn in FY 2014, as compared to net loss of INR -- mn in FY 2013

• The company reported total income of INR -- mn in FY 2014, registering an increase of -- per cent over FY 2013

• The company earned an operating margin of -- per cent in FY 2014, an increase of -- percentage points over FY 2013

• The company reported debt to equity ratio of -- in FY 2014, an increase of -- per cent over FY 2013

Key Financial Performance Indicators

Indicators Value (06/06/2014) Market Capitalization (INR mn)

Total Enterprise Value (INR mn)

EPS (INR) .

PE Ratio (Absolute) .

Particulars y-o-y change

(2014-13) 2014 2013 2012 2011

Profitability Ratios Operating Margin

Net Margin

Profit Before Tax Margin

Return on Equity

Return on Capital Employed

Return on Working Capital

Return on Assets

Return on Fixed Assets

Cost Ratios Operating costs (% of Sales)

Administration costs (% of Sales)

Interest costs (% of Sales)

Liquidity Ratios Current Ratio

Cash Ratio

Leverage Ratios Debt to Equity Ratio

Debt to Capital Ratio

Interest Coverage Ratio

Efficiency Ratios Fixed Asset Turnover

Asset Turnover

Current Asset Turnover

Working Capital Turnover

Capital Employed Turnover

Improved Decline

Total Income Net Profit/Loss

2012 2013 2011 2014

INR mn INR mn

FOUNDRY MARKET IN INDIA 2014.PPT

26

Public: Domestic Company – Player 1 (3/5) Key Business Segments Key Geographic Segments

Key Recent Developments (1/2)

Description News

Overview • Text

Clientele • Text

2014

Pipes

2011 2010 2013 2012

Note: Business Segments and Geographic Segments are based on total revenues; Geographic segments were available for latest 2013

Text

Foreign India

FOUNDRY MARKET IN INDIA 2014.PPT

27

Key Recent Developments (2/2)

Description News

Manufacturing Facilities • Text

Research and

Development • Text

Q4 2013-14 • Text

Public: Domestic Company – Player 1 (4/5)

FOUNDRY MARKET IN INDIA 2014.PPT

28

• Text • Text

• Text • Text

T O

W S

Public: Domestic Company – Player 1 (5/5)

FOUNDRY MARKET IN INDIA 2014.PPT

29

Private: Domestic Company – Player 2 (1/5)

Key People

Products and Services

Company Information Offices and Centres – India

Category Products/Services

Name Designation

Note: The list of products and services is not exhaustive

Corporate Address

Tel No. +

Fax No. +

Website

Year of Incorporation Head Office

FOUNDRY MARKET IN INDIA 2014.PPT

30

Shareholders of the Company Ownership Structure

Name No. of Shares held

Total

Note: Shareholding pattern as on AGM dated 29th Sep 2013

Other top 50 shareholders

Corporate Bodies

Directors or relatives of directors

Private: Domestic Company – Player 2 (2/5)

FOUNDRY MARKET IN INDIA 2014.PPT

31

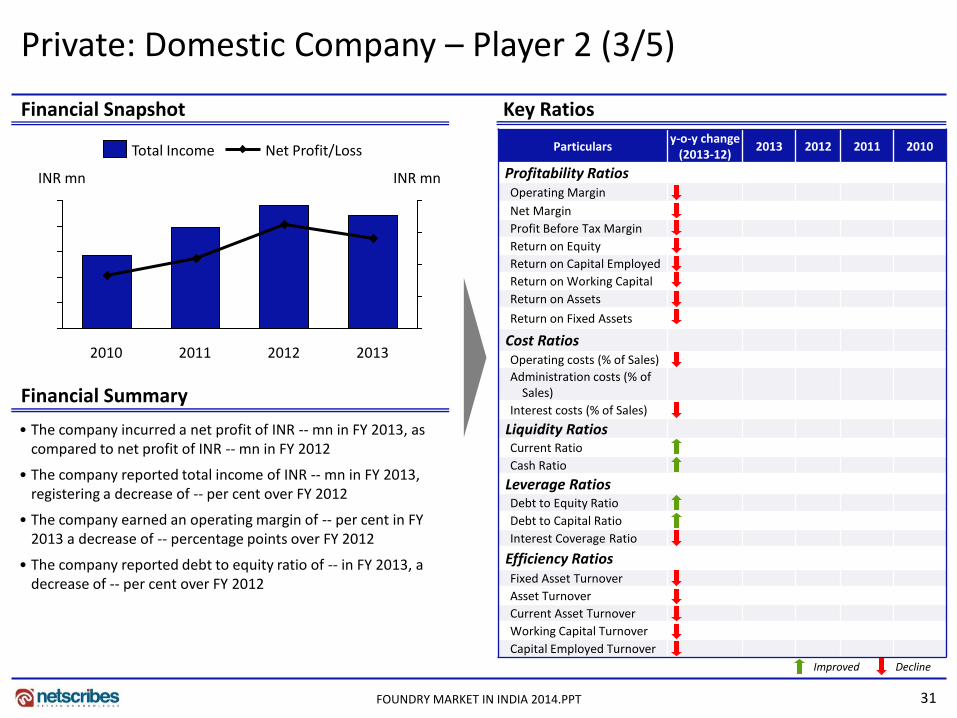

Private: Domestic Company – Player 2 (3/5)

Financial Snapshot Key Ratios

Financial Summary

• The company incurred a net profit of INR -- mn in FY 2013, as compared to net profit of INR -- mn in FY 2012

• The company reported total income of INR -- mn in FY 2013, registering a decrease of -- per cent over FY 2012

• The company earned an operating margin of -- per cent in FY 2013 a decrease of -- percentage points over FY 2012

• The company reported debt to equity ratio of -- in FY 2013, a decrease of -- per cent over FY 2012

Particulars y-o-y change

(2013-12) 2013 2012 2011 2010

Profitability Ratios Operating Margin

Net Margin

Profit Before Tax Margin

Return on Equity

Return on Capital Employed

Return on Working Capital

Return on Assets

Return on Fixed Assets

Cost Ratios Operating costs (% of Sales)

Administration costs (% of Sales)

Interest costs (% of Sales)

Liquidity Ratios Current Ratio

Cash Ratio

Leverage Ratios Debt to Equity Ratio

Debt to Capital Ratio

Interest Coverage Ratio

Efficiency Ratios Fixed Asset Turnover

Asset Turnover

Current Asset Turnover

Working Capital Turnover

Capital Employed Turnover

Improved Decline

Total Income Net Profit/Loss

2010

INR mn INR mn

2013 2012 2011

FOUNDRY MARKET IN INDIA 2014.PPT

32

Private: Domestic Company – Player 2 (4/5)

Key Recent Developments

Description News

Overview • Text

Manufacturing Plants • Text

Certifications • Text

Awards • Text

FOUNDRY MARKET IN INDIA 2014.PPT

33

• Text • Text

• Text • Text

T O

W S

Private: Domestic Company – Player 2 (5/5)

FOUNDRY MARKET IN INDIA 2014.PPT

34

•Macroeconomic Indicators

•Introduction

•Market Overview

•Foundry Clusters

•Export-Import

•Drivers & Challenges

•Competition

•Future Outlook

•Strategic Recommendations

•Appendix FOUNDRY MARKET IN INDIA 2014.PPT

35

In order to realise the Vision Plan 2020, various interventions are required...

Vision Plan 2020 Interventions

Technology Upgradation Fund

• Text

Capacity Consolidation

• Text

New Capacity Creation

• Text

Green Foundry Initiative

• Text

Better facilities • Text

• An Implementing Agency for the India Foundry Mission (IFM) will have full authority to represent, demonstrate the pilots and implement the various recommendations and professionally monitor the growth

• It will have a predetermined lifespan of 5 years and will create and strengthen the vehicles to take on the growth thereafter

India Foundry Mission Vision Plan 2020

FOUNDRY MARKET IN INDIA 2014.PPT

36

Thank you for the attention

About Netscribes, Inc. Netscribes, Inc. is a knowledge-consulting and solutions firm with clientele across the globe. The company’s expertise spans areas of investment & business research, business & corporate intelligence, content-management services, and knowledge-software services. At its core lies a true value proposition that draws upon a vast knowledge base. Netscribes, Inc. is a one-stop shop designed to fulfil clients’ profitability and growth objectives.

Foundry Market – India report is part of Netscribes’ Manufacturing Series. For any queries or customized research requirements, contact us at:

Disclaimer: This report is published for general information only. Although high standards have been used in the preparation, “Netscribes” is not responsible for any loss or damage arising from use of this document. This document is the sole property of Netscribes and prior permission is required for guidelines on reproduction.

Phone: +91 22 4098 7600 E-Mail: [email protected]

FOUNDRY MARKET IN INDIA 2014.PPT