Scintillations principle, working, merits & demerits & applications

Upload

truonglienCategory

view

215download

0

MANAGEMENT ACCOUNTING

Course Code UM15MB605

Chief Course Instructor

Course Instructor

Dr. Anitha S Yadav

Course Credits 4

No. of Hours 52

Credit pattern

Lecture Tutorial Practical/

Seminar

Self

study Credits

3 1 4

ISA 40% (30% for two tests + 5% for activities +5% for

attendance)

ESA 60%

Course Objectives

This course provides the students an understanding of

relevance of cost in managerial decision making. The

course provides a comprehensive knowledge of

classification of cost, apportionment of overheads,

process costing, activity based costing, segmental

reporting, preparation of budgets and cost –volume profit

analysis for decision making and cost control

Course Outcome

At the end of the course, students are able to

1. Explain the concepts of unit costing activity based

costing, apportionment of overheads, process

costing, segmental reporting and budgeting.

2. Exhibit skills in Identifying, Measuring and

Analysing costing data.

3. Provide alternative solutionsfor cost control and

related cost management applications in practice.

Pedagogy/Andragogy/Didactics

Each unit will have 60% of time in Lecture, 20% in

case and 20% learning through GD, Flip classes,

Audio-visuals and other activities.

COURSE PLAN (52 Hours)

No. Session Topics Coverage Didactics

% age Cum%

UNIT-1

1 Introduction: Basic Concepts of costs 2

2

2 Cost Classification, 2 4

3 Centres, Profit centres and Investment Centres, Cost

unit.

2 6

4 Cost analysis for Management Decision Making. 2 8

5 Cost Sheet and Unit Costing. 2 10

6 Cost Sheet and Unit Costing. 2 12

7 Preparation of tenders and quotations. 2 14

8 Preparation of tenders and quotations. 2 16

9 Job Costing. 2 18

10 Differences between Job Costing and Unit Costing. 2 20

ASSIGNMENT 1

1 Briefly explain costs relevant for decision making.

2. Explain the various elements of cost with suitable eg.

3The following data is extracted from the books of a manufacturer who manufactures a standard

produced during a 4 week period ending 31-3-2010:-

Particulars Amount

Raw Materials consumed 4,000

Wages 6,000

Machine hours worked 1000 hours -------

Machine hour Rate 0.50

Office overhead @ 20% on works cost

Selling overhead per unit 0.06

Units produced in the period 20,000 units

Units sold in the period( @ Re 1/- per unit) 18,000units

You are required to prepare a cost sheet showing the cost per unit and the profit for the period.

Unit 2 11 Apportionment of Overheads and Budgetary

Control: Accounting for Factory Overheads,

Differences between Allocation and Absorption

2

22

12 Apportionment of Overheads- Primary Distribution

of Overheads.

2 24

13 Secondary Distribution of Overheads- Repeated

Distribution Method.

2 26 Case study

14 Simultaneous Equation Method. 2 28

15 Overhead Absorption rates- Treatment of Over-

absorption and Under absorption of Overheads.

2 30

16 Reasons for Over and Under absorption. 2 32

17 Meaning of Budgetary Control and budgeting. 2 34

18 Preparation of Production Budgets. 2 36

19 Preparation of Flexible Budgets. 2 38

20 Preparation of Flexible Budgets. 2 40

ASSIGNMENT 2 1. Distinguish between Allocation and Absorption.

3. What do you understand by primary and secondary distribution of overheads?

3 Prepare a flexible budget for overheads on the basis of the following data. Ascertain the overhead rates

at 50%, 60% and 70% capacity.

At 60% capacity

Variable overheads: Rs.

Indirect material 6,000

Indirect labour 18,000

Semi-variable overheads:

Electricity (40% fixed, 60% variable) 30,000

Repairs (80% fixed, 20% variable) 3,000

Fixed overheads:

Depreciation 16,500

Insurance 4,500

Salaries 15,000

Total Overheads 93,000

Estimated direct labour hours 1,86,000

4.For the manufacture of 10,000 locks, the following are the budgeted expenses:

Per unit

Rs

Direct material 60

Direct labour 30

Variable overhead 25

Fixed overhead (Rs.1,50,000) 15

Variable expenses (direct) 5

Selling expenses (10% fixed) 15

Administrative expenses (Rs.50,000 fixed for all levels

of production) 5

Distribution expenses (20% fixed) 5

Total cost of sale per unit 160

Prepare a budget for the production of 6,000, 7,000 and 8,000 locks, showing distinctly the marginal cost

and total cost.

Unit 3

21 Cost Volume Profit Analysis

Cost Volume Profit (CVP) relationship,

2 42

22 Profit Planning and behaviour of expenses. 2 44

23 Assumptions of CVP Model. 1 45

24 Sensitivity Analysis. 1 46

25 Marginal Costing. 2 48

26 Differential Costing. 2 50

27 Decisions involving Make or Buy. 2 52

28 Decisions involving Acceptance or Rejection of

Special Orders.

2 54 Case study

29 Product Mix. 2 56

30 Sell or Process further. 2 58

31 Shut Down or Continue. 2 60

32 Product and Pricing Decisions. 2 62

ASSIGNMENT 3 1.The Sales Turnover and Profit during the two years were as follows :-

Year Sales Profit

Rs Rs

2012 1,50,000 20,000

2013 1,70,000 25,000

You are required to calculate:-

P/ V ratio. BEP.

The sales required to earn a Profit of Rs. 40,000

Margin of safety at a profit of Rs. 50,000

The Profit made when sales are Rs. 2,50,000.

Variable costs of the two periods.

2.From the following calculate the Break Even Point.

Variable Cost per unit Rs 10

Selling Price per unit Rs 15

Fixed expenses Rs 50,000.

What should be the selling price per unit if the BEP is to be brought down to 5,000 units.

3.“Cost-Volume Profit analysis is a very useful technique to management for cost control, profit planning

and decision making”. Explain

Unit 4 33 Process Costing

Meaning, Features of Process

2 64

34 Significance of Process Costing. 2 66

35 Treatment of Normal and Abnormal Losses

in Process Accounts.

2 68

36 Treatment of Normal and Abnormal Losses

in Process Accounts.

2 70

37 Treatment of Normal and Abnormal Gain in Process

Accounts.

2 72

38 Preparation of profit and loss accounts 2 74

39 Preparation of Process Accounts. 2 76

40 Preparation of Process Accounts. 2 78

41 Preparation of Process Accounts with profit and loss

A/c.

2 80 Case Study

42 Meaning Joint and By-Products. Preparation of

Process Accounts.

2 82

Unit 5 43 Activity Based Costing Introduction and

applications

2

84

44 Cost Drivers for Activity Based Costing. 2 86

45 Cost Analysis at unit level. 1 87

46 Cost Analysis at Batch level and product. 2 89

47 Merits and Demerits of ABC. 1 90

48 Problems on ABC Costing. 2 92 Case study

49 Cost Reduction and Cost Control. 2 94

50 Management Reporting purpose of Reporting. 2 96

51 Segment Reporting, Objectives and users of Segment

Reporting.

2 98

52 Applicability of Accounting Standard 17. 2 100

Recommended Book:

1. Managerial Accounting Jiambalvo,James, , Wiley India publications

2. Management Accounting, Khan & Jain, , Tata McGraw Hills.

Reference Book

1 . Management Accounting Arora.M.N. Cost and Vikas Publication

2. Cost Accounting, S.P.Jain, K.L.Narang, Kalyani Publishers.

Note: Each session is one hour duration

QUESTION BANK

Unit 1

3 MARK QUESTION

1. What is Cost?

2. What is a Cost centre?

3. What is Costing?

4. What is Cost accounting?

5. What is prime cost?

6. What do you understand by Management Accounting?

7. What is a Cost sheet?

8. What is works cost

9. What do understand by a cost unit?

10. Name any three tools of Cost Management.

11. What do you understand by classification of cost?

12. Differentiate between Job costing and Process costing.

13. What do you understand by Opportunity costs?

14. What are overheads?

15. What is an investment centre?

5/7/10 MARK QUESTIONS

16. Briefly explain costs relevant for decision making.

17. Briefly explain the various elements of cost.

18. Distinguish between job costing and process costing

19. The following figures for the month of April 2010 were extracted from the books of a manufacturing

concern.

Opening stock of finished goods (5,000 units) Rs 45,000

Purchase of Raw Materials Rs 2,57,100

Direct wages Rs 1,05,000

Factory overheads: 100 % of Direct wages.

Administrative overhead: Re 1 per unit

Selling and Distribution overhead: 10% of sales.

Closing stock of finished goods (10,000 units) ?

Sales (45,000 units) Rs 6,60,000

Prepare a cost sheet for the month of April 2010 assuming that sales are made on the basis of First in First

out principle.

20. A firm is manufacturing motors and the following information was extracted from its costing records

for the year ended 31-3-2010.

Work in Progress on 1- 4- 2009:-

At Prime Cost Rs. 51,000

Manufacturing expenses Rs. 15,000 Rs.66,000

Work in Progress on 31-3-2010:-

At Prime Cost Rs. 45,000

Manufacturing expenses Rs. 9,000 Rs.54,000

Opening stock of raw Materials as on 1-4-2009 Rs.2,25,000

Purchase of Raw Materials Rs.4,77,000

Direct Labour Rs.1,71,000

Manufacturing expenses Rs.84,000

Stock of Raw materials as on 31-3-2010 Rs.2,04,000

Prepare a Cost Sheet showing the Cost of Production.

Unit II

3 MARK QUESTION

1. What are overheads?

2. Distinguish between Allocation and Absorption.

3. What do you understand by primary and secondary distribution of overheads?

4. What is the impact of over absorption of overheads in books of account.

5. What are the reasons for under absorption of overhead?

6. State the reasons for over -absorption of overhead?

7. What is budgetary control?

8. What are the uses of flexible budgets?

9. Why do we prepare a production Budget?

10. What are the step involved in repeated distribution method of absorption service department

expenses?

11. What are absorption rates?

12. Distinguish between allocation, apportionment and absorption of overheads.

13. XYZ Ltd. is a manufacturing company having three Production Departments A, B and C and two

Service Departments Stores and Workshop. The following is the budget for March 2012.

Particulars Total A B C Stores Workshop

Direct materials 1,000 2,000 4,000 2,000 1,000

Direct wages 5,000 2,000 6,000 1,000 2,000

Factory rent 4,000

Power 2,500

Depreciation 1,000

Other overheads 9,000

Additional Information:-

Particulars A B C Stores Workshop

Area (Sq.ft) 500 250 500 250 500

Capital value of assets( Rs.lakhs) 20 40 20 10 10

Machine hours 1,000 2,000 4,000 1,000 1,000

Horsepower of machines 50 40 20 15 25

The apportionment of expenses of service departments is as under:

Particulars A B C Stores Workshop

Service Dept. X (%) 45 15 30 __ 10

Service Dept. Y (%) 60 35 __ 5 __

Required:

1. A statement showing distribution of overheads to various departments

2. A statement showing re-distribution of services department expenses to production departments.

14. Prepare a flexible budget for overheads on the basis of the following data. Ascertain the overhead

rates at 50%, 60% and 70% capacity.

At 60% capacity

Variable overheads: Rs.

Indirect material 6,000

Indirect labour 18,000

Semi-variable overheads:

Electricity (40% fixed, 60% variable) 30,000

Repairs (80% fixed, 20% variable) 3,000

Fixed overheads:

Depreciation 16,500

Insurance 4,500

Salaries 15,000

Total Overheads 93,000

Estimated direct labour hours 1,86,000

15. ABC Co. Ltd. Manufactures two different products, M and N. Forecasts of the number of units to be

sold in the first seven months of the year are given below:

Months Product M Product N

Jan 1,000 2,800

Feb 1,200 2,800

Mar 1,600 2,400

Apr 2,000 2,000

May 2,400 1,600

June 2,400 1,600

July 2,000 1,800

It is expected that (i) there will be no work-in-process at the end of every month (ii) finished units equal

to half the sales for the next month will be in stock at the end of each month (including previous

December).

Budgeted production and production costs for the whole year are as follows:

Production in Units Product M Product N

22,000 24,000

Per unit cost (Rs.) Direct Material 10.00 15.00

Direct Labour 5.00 10.00

Total factory overhead apportioned (Rs.) 88,000 72,000

Prepare a month-wise production budget for the six months ending 30th June and a summarized

production cost budget.

16. Manju Agro Industries Ltd. manufactures pickles and juices. The sales department has prepared the

following forecasts for the quarter ending March 31, 2013:

Product No. of Bottles

Pickles:

Lemon 1,00,000

Mixed 75,000

Juices:

Orange 25,000

Mango 15,000

Pear 35,000

The inventory levels have been determined as under:

Products Work-in-Progress Finished Goods

Units % Completed

Opening Closing Opening Closing Opening Closing

Pickles:

Lemon 25,000 40,000 80 60 7,500 6,000

Mixed 15,000 25,000 60 80 3,000 2,000

Juices:

Orange 5,000 4,000 80 75 1,500 2,000

Mango 3,000 3,000 70 80 800 500

Pear 4,000 5,000 75 80 2,000 2,000

The production in each month is expected to be uniform. Prepare production budget for the quarter.

17. For the manufacture of 10,000 locks, the following are the budgeted expenses:

Per unit

Rs

Direct material 60

Direct labour 30

Variable overhead 25

Fixed overhead (Rs.1,50,000) 15

Variable expenses (direct) 5

Selling expenses (10% fixed) 15

Administrative expenses (Rs.50,000 fixed for all levels

of production) 5

Distribution expenses (20% fixed) 5

Total cost of sale per unit 160

Prepare a budget for the production of 6,000, 7,000 and 8,000 locks, showing distinctly the marginal cost

and total cost.

18. Elixir Electronics Co. Ltd. has prepared its budget at capacity level of 6,000 units of their only

product as under:

Particulars Amount (Rs)

Raw material

Direct wages

Direct expenses

Admn. Overheads

Advt. & Distribution overheads

Repairs & maintenance

Insurance

Depreciation

Power

30,000 (100 % varying)

18,000 (100 % varying)

12,000 (100 %varying)

6,000 (70 % varying)

3,000 (40 % varying)

5,000 (75 % varying)

3,000 (25 % varying)

6,000 (75 % varying)

1,200 (75 % varying)

Compute the unit cost of the production levels of 3,000 units and 9,000 units.

19. The expenses budgeted for productions of 10,000 units in a factory are furnished below:

Particulars Per Unit

Rs.

Materials 70

Labour 25

Variable Overheads 20

Fixed Overheads (Rs.1,00,000) 10

Variable Expenses (Direct) 5

Selling Expenses (10% fixed) 13

Administrative Expenses (Rs.50,000) 5

Distribution Expenses (20% fixed) 7

Total 155

Prepare a budget for the production of (a) 8,000 units and (b) 6,000 units. Assume that

administrative expenses are rigid for all levels of production.

20. A company is working at 50% capacity manufactures 10,000 units of a product. At 50% capacity the

product cost is Rs.180 and sale price is Rs.200. The breakup of the cost is as below:

Cost per unit

Material Rs.100

Wages 30

Factory 30 (40% fixed)

Administration overheads 20 (50% fixed)

At 60% working, raw material cost goes up by 2% and sales price falls by 2%. At 80% working, the raw

material cost increases by 5% and sale price decreases by same percentage, i.e., 5%.

Prepare a statement to show profitability at 60% and 80% capacity.

Unit III

3 MARK QUESTION

1. What is marginal cost?

2. What do you understand by Marginal Costing?

3. Why do we use P/V ratio?

4. Briefly discuss Break even analysis?

5. What do you understand by Cost Volume Profit analysis?

6. Mention any 3 advantages of Marginal Costing.

7. What are the demerits of using Marginal Costing?

8. How does marginal costing help a Manufacturing concern in decision making?

9. What is Margin of safety?

10. The size of margin of safety is an extremely valuable guide to the strength of a business. Discuss.

11. What is sensitivity analysis?

12. What are the uses of budget?

13. What are the assumptions of CVP analysis?

14. What is Key Factor?

15. What is variable cost?

5/7/10 MARK QUESTION

16. The following figures relate to a company manufacturing a varied range of products:-

Particulars Total Sales Rs. Total Cost Rs.

Year ended 31-12-2011 22, 23,000 19, 83,600

Year ended 31-12-2012 24, 51,000 21, 43,200

Assuming stability in prices with Variable Costs carefully controlled to reflect predetermined

relationships and an unvarying figure for fixed costs calculate :-

The P/V ratio to reflect the rates of growth for profit and sales.

Fixed cost.

Fixed cost % to Sales.

Break even point.

Margin of safety for both the years.

17. The Sales Turnover and Profit during the two years were as follows :-

Year Sales Profit

Rs Rs

2012 1,50,000 20,000

2013 1,70,000 25,000

You are required to calculate:-

P/ V ratio. BEP.

The sales required to earn a Profit of Rs. 40,000

Margin of safety at a profit of Rs. 50,000

The Profit made when sales are Rs. 2,50,000.

Variable costs of the two periods.

18. From the following calculate the Break Even Point.

Variable Cost per unit Rs 10

Selling Price per unit Rs 15

Fixed expenses Rs 50,000.

What should be the selling price per unit if the BEP is to be brought down to 5,000 units.

19. A company engaged in plantation activities has 200 hectares of virgin land which can be used for

growing jointly or individually Tea, Coffee or Cardamom. The yield per hectare of the different crops and

their selling prices are as follows:-

Products Yield in kgs Selling price per kg in Rs

Tea 2000 20

Coffee 500 40

Cardamom 100 250

The relevant cost data are as follows :-

Variable cost per kg

Tea Coffee Cardamom

Labour Charges Rs 8 Rs 10 Rs 120

Packing Materials Rs 2 Rs 2 Rs 10

Other Costs Rs 4 Rs 1 Rs 20

Total costs Rs 14 Rs 13 Rs 150

Fixed cost per annum:-

Cultivation and growing Cost Rs. 10,00,000

Administrative cost Rs. 2,00,000

Land revenue Rs. 50,000

Repairs and Maintenance Rs. 2,50,000

Other costs Rs. 3,00,000

Total Cost Rs. 18,00,000

The policy of the company is to produce and sell all the three kinds of products and the maximum and

minimum area to be cultivated per product is as given below:

Hectares

Maximum Minimum

Tea 160 120

Coffee 50 30

Cardamom 30 10

Calculate the most profitable product mix and the maximum profit which can be achieved.

20. The following particulars are extracted from the records of a company,

Particulars Product A Product B

Rs. Per Unit Rs. Per Unit

Sales Price 100 110

Consumption of Materials (Kgs) 5 4

Material cost 24 14

Direct Wages 2 3

Machine hours used 2 3

Variable overheads 4 6

Comment on the profitability of each product (both use the same raw material) when:

A. Total sales potential in units is limited

B. Total sales potential in value is limited

C. Raw materials is in short supply

Production capacity in terms of machine hour is the limiting factor

21. “Cost-Volume Profit analysis is a very useful technique to management for cost control, profit

planning and decision making”. Explain

UNIT IV

3 MARK QUESTION

1. What is process costing?

2.How do you treat normal and abnormal loss in process costing?

3.What is abnormal effectiveness?

4. What do you understand by joint and by-products?

5. Discuss the features of process costing.?

6. What are Joint costs?

7. A product passes through three distinct processes to completion. These processes are numbered

respectively I, II, and III. During the week ended 15th January 2015, 500 units are produced. Following

information is obtained:

Particulars Process I Process II Process III

Rs. Rs. Rs.

Direct Materials 3,500 1,600 1,500

Direct Labour 2,500 2,000 2,500

The overhead expenses for the period were Rs.1,400 apportioned to the processes on the basis of wages.

No work- in- progress or process stocks existed at the beginning or at the end of the week. Prepare

process accounts.

8. Eureka Chemicals Ltd. Produced three chemicals during the month of July 2014 by three consecutive

processes. In each process 2% of the total weight put in is lost and 10% is scrap which from processes (1)

and (2) realises Rs.100 a ton and from process (3) Rs.20 a ton.

The product of the three processes are dealt with as follows:

Particulars Process I Process II Process III

Passed on to the next process 75% 50% ___

Sent to warehouse for sale 25% 50% 100%

Expenses incurred:

Particulars Process I Process II Process III

Rs. Tons Rs. Tons Rs. Tons

Raw materials 1,20,000 1,000 28,000 140 1,07,840 1,348

Manufacturing wages 20,500 ____ 18,520 ____ 15,000 _____

General Expenses 10,300 ____ 7,240 _____ 3,100 ______

Prepare process cost accounts showing the cost per ton of each product.

9 Following data are available pertaining to a product after passing through two processes A & B.

Output transferred to process C from process B 9,120 units for Rs. 49,263.

Expenses incurred in process C:

Sundry materials – Rs. 1,480

Direct labour - Rs. 6,500

Direct expenses - Rs. 1,605

The wastage of process C is sold at Rs. 1.00 per unit. The overhead charges were 168% of direct labour.

The final product was sold at Rs. 10.00 per unit fetching a profit of 20% on sales. Find the percentage of

wastage in process C and prepare process C account.

10. The product of the company passes through three distinct processes to completion. They are known as

A, B, and C. From past experience it is ascertained that loss is incurred in each process as : Process A –

2%, Process B-5%, Process C- 10%. In each case the percentage of loss is computed on the number of

units entering the process concerned. The loss of each process has a scrap value. The loss of processes A

& B is sold at Rs. 5 per 100 units and that of process C at Rs. 20 per 100 units.

The output of each process passes immediately to the next process and the finished units are passed from

process C into stock.

Particulars Process A Process B Process C

Rs. Rs. Rs.

Materials Consumed 6,000 4,000 2,000

Direct labour 8,000 6,000 3,000

Manufacturing

expenses

1,000 1,000 1,500

20,000 units have been issued to process A at a cost of Rs. 10,000. The output of each process has been as

under:

Process A 19,500; Process B 18,800; Process C 16,000. There is no work-in-progress in any process.

Prepare process accounts. Calculations should be made to the nearest rupee.

11. A certain product passes through two processes desired before it is transferred to finished stock.

Following information is obtained for the month of March 2015.

Particulars Process I Process II Finished stock

Rs. Rs. Rs.

Opening stock 7,500 9,000 22,500

Direct material 15,000 15,750

Direct wages 11,200 11,250

Production Overheads 10,500 4,500

Closing stock 3,700 4,500 11,250

Profit % on transfer price

to the next process

25% 20%

Inter-process _______ 1,500 8,250

Stocks in processes are valued at prime cost and finished stock has been valued at the price at which it

was received from Process II. Sales during the period were Rs. 1,40,000.

Prepare and compute:

a. Process cost accounts showing profit element at each stage

b. Actual realised profit

12. A product passes through three distinct processes A,B and C. The normal loss of units in each process

is 5%, 10% and 15% and the same is sold at Rs.2,4 and 5 Rs per unit respectively. Expenses for the

month were as follows:

Particulars Process A Process B Process C

Materials(Rs) 5,200 3,960 5,924

Wages (Rs.) 4,000 6,000 8,000

Actual Output in units 1,900 1,680 1,500

2,000 units @ Rs. 3 per unit were put into Process A. The total overheads are Rs. 18,000 which are to be

recovered at 100% of wages. Prepare necessary process accounts.

13. The following particulars relate to two process X and Y for the month of Jan.2015:

Particulars Process X Process Y

Total input(in units) 50,000 1,000

@ Rs.1.50 p.u

Normal loss( % of input) 10% 5%

Additional costs incurred:

Materials ---- 3,600

Direct Labour 35,000 45,000

Overheads 27,500 39,500

Realisable values of scrap p.u. Re.0.50 Rs. 2

Output in units 43,000 43,000

The entire output of process X was transferred to process Y. The entire output of process Y was sold at

Rs.6 per unit. Assume, there was no opening or closing stock . You re required to prepare necessary

accounts for the period.

14. Distinguish between normal and abnormal wastage of materials with specific reference to the

accounting treatment and control.

15. The finished product of a factory has to pass through three processes A,B and C. The normal wastage

of each process if 2% in A,5% in B and 10% in C. The percentage of waste is computed on the number of

units entering each process.

The scrap value of wastage of Process A,B and C are Rs.10,Rs.40, Rs 20 per 100 units respectively. The

following further information is obtained.

Particulars Process A Process B Process C

Materials consumed 12,000 4,000 4,000

Direct Labour 8,000 6,000 6,000

Mfg. expenses 2,000 4,000 2,000

2,000 units were out to process A at a cost of Rs. 16,000.The output of each process has been A 19,600

units, B-18,400 and C – 16,700 units.

Prepare process accounts.

16) A product passes through two Processes. The output of Process 1 becomes the input of Process 2

and the output of process 2 is transferred to warehouse. The quantity of raw materials introduced into

Process 1 is 20,000 kgs at Rs.10 per kg. The cost and output data for the month under review are as

under:

Process 1 Process 2

Direct Materials Rs. 60,000.00 Rs. 40,000.00

Direct Labour Rs. 40,000.00 Rs. 30,000.00

Production Overheads Rs. 39,000.00 Rs.40,250.00

Normal Loss 8% 5%

Output 18,000 17400

Loss realization Rs./unit 2.00 3.00

The company’s policy is to fix the selling price of the end product in such a way as to yield

a profit of 20% on selling price.

UNIT V

MARK QUESTIONS

1. What do you mean by Management Reporting? Discuss its importance in modern business.

2. Explain the principles of good reporting system.

3. Explain the various informational needs of different levels of management.

4. Discuss various managerial reports prepared by business firms.

5. What do you understand by internal reports? How are they different from external reports?

6. Explain in detail the various kinds of internal reports.

7. How do you classify the Reports according to Contents?

8. Define a special report. Discuss its importance in a trading concern.

9. What are the objectives of Segmental Reporting?

10. Examine the applicability of AS-17.

11. What is Activity based costing?

12. Explain cost drivers and cost pool?

13. Analyse the merits and demerits of ABC costing?

14. Who are the users of Segment reporting?

15. Distinguish between Cost control and cost reduction

16. What is target costing?

17. What do mean by peanut butter costing

18. What is a cost driver? Explain the types of cost driver.

19. A company manufacturing two products furnishes the following data for a year: Product

Annual Output Total Machine Total No.of Total No. Of

(Units) Hours purchase orders set-ups

A 5,000 20,000 160 20

B 60,000 1,20,000 384 44

The annual overheads are as under:

Volume related activity costs: 5,50,000

Set-up related costs 8,20,000

Purchase related costs 6,18,000

You are required to calculate the cost per unit of each product A and B based on:

a) Traditional method of charging overheads.

b) Activity based costing method.

20. Cello company produces Delux pen and Regular pens. Data relating to the two products is presented

below:-

Particulars Delux Pen Regular Pen

Annual production in units 30,000 70,000

Direct Material costs 1,00,000 2,00,000

Direct Manufacturing labour costs 30,000 60,000

Direct Manufacturing labour hours 2,500 5,000

Machine hours 15,000 30,000

Number of production runs 50 50

Inspection hours 500 250

Both the products pass through department I and Department II. The department combined manufacturing

overhead costs are:

Machining costs 4,00,000

Setup costs 1,50,000

Inspection costs 1,20,000

Compute manufacturing overhead cost per unit for each product and cost per unit for each product.

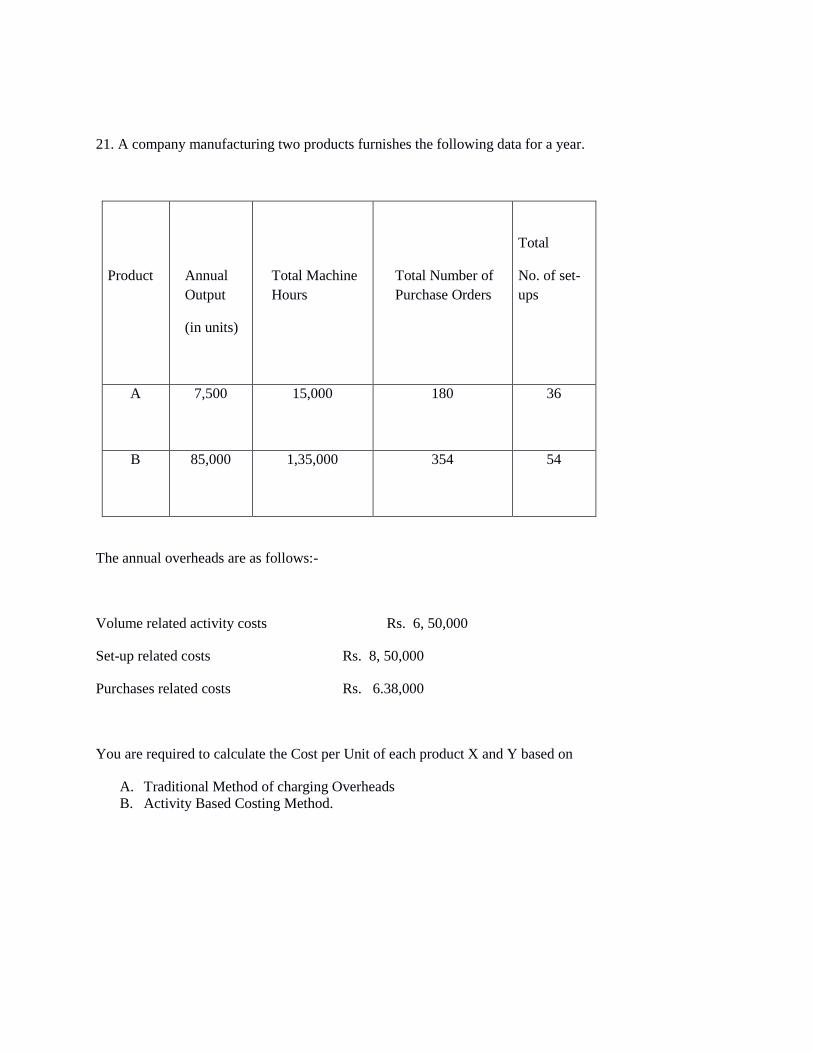

21. A company manufacturing two products furnishes the following data for a year.

Product

Annual

Output

(in units)

Total Machine

Hours

Total Number of

Purchase Orders

Total

No. of set-

ups

A 7,500 15,000 180 36

B 85,000 1,35,000 354 54

The annual overheads are as follows:-

Volume related activity costs Rs. 6, 50,000

Set-up related costs Rs. 8, 50,000

Purchases related costs Rs. 6.38,000

You are required to calculate the Cost per Unit of each product X and Y based on

A. Traditional Method of charging Overheads

B. Activity Based Costing Method.