LNG PROCUREMENT PROCUREMENT Presented by: ... Fertilizer Co. on board the FSRU on FOB basis which...

16

LNG PROCUREMENT Presented by: Presented by: Sheikh Imran ul Haque Sheikh Imran ul Haque

Transcript of LNG PROCUREMENT PROCUREMENT Presented by: ... Fertilizer Co. on board the FSRU on FOB basis which...

LNG PROCUREMENT

Presented by:Presented by:Sheikh Imran ul HaqueSheikh Imran ul Haque

The Successful Strategy

Under the Fast Track LNG Import Project:

• PSO be assigned the responsibility of LNGimport,

• SSGC manage the receiving of LNG at importterminal and transmission of Regasified LNG(RLNG) to SNGPL through swap arrangements

• SNGPL supply RLNG to end consumers.

Under the Fast Track LNG Import Project:

• PSO be assigned the responsibility of LNGimport,

• SSGC manage the receiving of LNG at importterminal and transmission of Regasified LNG(RLNG) to SNGPL through swap arrangements

• SNGPL supply RLNG to end consumers.

The Mandate• For import of LNG, ECC vide decision dated 2nd July 2013 have authorized this

Ministry to engage in negotiations with Qatargas on Government to Government

basis for importing LNG upto 500 MMCFD on delivered Ex-ship basis.

• Accordingly, Pakistan State Oil Company Limited (PSOCL) and Qatargas

Operating Company Limited (QOCL) have been nominated by respective

governments to negotiate the LNG Sales Purchase Agreement (LNG SPA).

• PSO / GOP and USAID appointed international consultants ( FGE and WFW)

engaged in negotiations with Qatargas, the State of Qatar’s designated entity,

on the terms of a long term LNG Sale and Purchase Agreement (LNG SPA) for

15 years, on Government to Government basis, for supply of LNG up to 3

mmtpa.

• For import of LNG, ECC vide decision dated 2nd July 2013 have authorized this

Ministry to engage in negotiations with Qatargas on Government to Government

basis for importing LNG upto 500 MMCFD on delivered Ex-ship basis.

• Accordingly, Pakistan State Oil Company Limited (PSOCL) and Qatargas

Operating Company Limited (QOCL) have been nominated by respective

governments to negotiate the LNG Sales Purchase Agreement (LNG SPA).

• PSO / GOP and USAID appointed international consultants ( FGE and WFW)

engaged in negotiations with Qatargas, the State of Qatar’s designated entity,

on the terms of a long term LNG Sale and Purchase Agreement (LNG SPA) for

15 years, on Government to Government basis, for supply of LNG up to 3

mmtpa.

FY12 FY13 FY14 FY15No. of Vessels 61 58 49 50Quantity (000 M.Tons) 3,070 2,997 2,573 2,703Import Value (Rs. In Mln) 300,342 319,053 280,226 224,131No. of Vessels 18 16 16 15Quantity (000 M.Tons) 1,016 1,009 1,019 961Import Value (Rs. In Mln) 70,580 67,247 74,499 53,444No. of Vessels 83 71 75 64Quantity (000 M.Tons) 5,177 4,871 4,993 4,334Import Value (Rs. In Mln) 325,306 297,132 326,425 212,980No. of Vessels 9 2 2 1Quantity (000 M.Tons) 210 51 23 10Import Value (Rs. In Mln) 19,652 4,879 2,411 987No. of Vessels 46 43 41 44Quantity (000 M.Tons) 1,127 1,293 1,440 1,945Import Value (Rs. In Mln) 115,808 142,502 174,749 156,525No. of Vessels 217 190 183 174Quantity (000 M.Tons) 10,602 10,246 10,048 9,954

Import Value (Rs. In Mln) 831,688 830,814 858,310 648,067

MOGAS

Total

PSO Imports FY12-15Year

HSD

LSFO

HSFO

Jet Fuel

PSO’s Strength and Ability

Note: Vessel booked at the time of berthing

FY12 FY13 FY14 FY15No. of Vessels 61 58 49 50Quantity (000 M.Tons) 3,070 2,997 2,573 2,703Import Value (Rs. In Mln) 300,342 319,053 280,226 224,131No. of Vessels 18 16 16 15Quantity (000 M.Tons) 1,016 1,009 1,019 961Import Value (Rs. In Mln) 70,580 67,247 74,499 53,444No. of Vessels 83 71 75 64Quantity (000 M.Tons) 5,177 4,871 4,993 4,334Import Value (Rs. In Mln) 325,306 297,132 326,425 212,980No. of Vessels 9 2 2 1Quantity (000 M.Tons) 210 51 23 10Import Value (Rs. In Mln) 19,652 4,879 2,411 987No. of Vessels 46 43 41 44Quantity (000 M.Tons) 1,127 1,293 1,440 1,945Import Value (Rs. In Mln) 115,808 142,502 174,749 156,525No. of Vessels 217 190 183 174Quantity (000 M.Tons) 10,602 10,246 10,048 9,954

Import Value (Rs. In Mln) 831,688 830,814 858,310 648,067

MOGAS

Total

PSO Imports FY12-15Year

HSD

LSFO

HSFO

Jet Fuel

Price NegotiationTo negotiate the LNG price and other important aspects with

Qatargas, ECC vide decision dated 15th August 2014 has

approved constitution of a LNG Price Negotiation Committee

(PNC) comprising of Secretary Petroleum (Chairman),

representatives of Finance Division, Water and Power and BOI

not below the rank of Additional Secretary, MD SNGPL,MD

SSGCL, MD PSO and MD ISGSL ( as Secretary Committee).

To negotiate the LNG price and other important aspects with

Qatargas, ECC vide decision dated 15th August 2014 has

approved constitution of a LNG Price Negotiation Committee

(PNC) comprising of Secretary Petroleum (Chairman),

representatives of Finance Division, Water and Power and BOI

not below the rank of Additional Secretary, MD SNGPL,MD

SSGCL, MD PSO and MD ISGSL ( as Secretary Committee).

Oil and LNG Sector Overview

Feedstock Costs Crude feedstock is main element of thedelivered price

Gas feedstock is a small share of thedelivered price

Annual Value of Trade $2.4 trillion US $193 billion US

Producing Countries 117 (countries with refineries) 18 (exporters)

End-User Countries 196 (all countries) 26 (importers--but growing)

Shipping market Large, competitive and flexible Small with mostly dedicated fleets

Import infrastructure Thousands of ports 93 regas plants in 26 countries

Producing facilities 655 refineries 26 LNG plants (89 trains)

Spot market Large and active with many players Growing, but few major players

Futures markets Large, active drivers of prices & contracts Nonexistent

Typical Contracts 1-2 months up to 1-2 years 4-20 years

Resales/Diversions Common Usually forbidden

OIL LNG

Feedstock Costs Crude feedstock is main element of thedelivered price

Gas feedstock is a small share of thedelivered price

Annual Value of Trade $2.4 trillion US $193 billion US

Producing Countries 117 (countries with refineries) 18 (exporters)

End-User Countries 196 (all countries) 26 (importers--but growing)

Shipping market Large, competitive and flexible Small with mostly dedicated fleets

Import infrastructure Thousands of ports 93 regas plants in 26 countries

Producing facilities 655 refineries 26 LNG plants (89 trains)

Spot market Large and active with many players Growing, but few major players

Futures markets Large, active drivers of prices & contracts Nonexistent

Typical Contracts 1-2 months up to 1-2 years 4-20 years

Resales/Diversions Common Usually forbidden

OIL LNG

Commodity Pricing / Indexation Typical Brent / JCC base price structuresassume following form

LNG Price $/MMBTU = (percentage) xBrent / JCC + XXX; where•Percentage = variable contractto contract – 12% to 16%•Brent (x,y,z) = Brent / JCClinkage; oil prices averaged over past 03,06, 09 or 12 months•XXX = Constant Component / Premium

LNG Price $/MMBTU = (percentage)x Hub Price + Tolling Tariff + FreightCosts + Variables; where

• Hub Price = the final settlementprice (in $/mmbtu) for the New YorkMercantile Exchange's HH natural gasfutures contract for the Month in whichthe relevant cargo's delivery window isscheduled to begin•Percentage = variable contract tocontract – 115% and above•Tolling tariff is a significant costelement. Freight Cost – significantcost element due to distances -$1.5/mmbtu (Europe) to $3/mmbtu(farther distances)•Variables – Premiums etc, adjustedannually based on CPI

LNG Price $/MMBTU = (percentage)x Hub Price + Tolling Tariff + FreightCosts + Variables; where

• Hub Price = the final settlementprice (in $/mmbtu) for the New YorkMercantile Exchange's HH natural gasfutures contract for the Month in whichthe relevant cargo's delivery window isscheduled to begin•Percentage = variable contract tocontract – 115% and above•Tolling tariff is a significant costelement. Freight Cost – significantcost element due to distances -$1.5/mmbtu (Europe) to $3/mmbtu(farther distances)•Variables – Premiums etc, adjustedannually based on CPI

17.80% 16% 18.90% 25.40% 25.10% 33% 29%

Long Term

Long Term v/s Spot & Short termNuclear Shutdown

in Japan

Japan`s long term contractsextended at roughly half of the

volumes

Mild 2013-2014 winter, SouthKorea retreats from Spot Market

2008 2009 2010 2011 2012 2013 2014

A number of key factors have contributed to the rapid growth of non long-term trade in recent years including• The growth in LNG contracts with destination flexibility, mainly from the Atlantic Basin and Qatar, which has

facilitated diversions to higher priced markets.• The increase in the number of exporters and importers. 26 exporters & 28 importers in 2014 as compared to

6 exporters and 8 importers in 2000.• Reliance of Japan, South Korea & Taiwan on spot market for sudden changes in demand (Fukushima) due

to lack of domestic production or pipeline imports.• The large growth in the LNG fleet, which has allowed the industry to sustain the long-haul parts of the spot

market (chiefly the trade from the Atlantic to the Pacific).

Why Qatar?

Europe23%

Asia72%

Americas5% Europe

14%Americas

10%

Middle East1%

2000:101 mmt 2013:

234 mmt

Global LNG imports, 2000 - 2013

Qatar has liquefaction facilities to Produce 77 Mtpa ofLNG with all 14 LNG trains running at full capacity

which confirms Qatar as the world’s main LNGsupplier with a market share of over 30%.

Asia72% Asia

75%

LNG Import InitiatedCommissioning cargo

Given SSGC’s contractual commitment under the LSA, ECC videcase No. ECC-52/7/2015, dated 09-04-2015 approved the followingproposal submitted by MP&NR vide summary dated 02-04-2015;To keep an option of commissioning of LNG terminal throughPSO, PSO may be allowed to import one commissioning cargothrough FSRU on FOB basis or LNG carrier on DES basisunder LNG SPA.’

Accordingly, PSO imported one cargo of LNG from Qatargas for aFertilizer Co. on board the FSRU on FOB basis which arrived on26th March, 2015 and the terminal was commissioned on 27thMarch 2015.

Commissioning cargo

Given SSGC’s contractual commitment under the LSA, ECC videcase No. ECC-52/7/2015, dated 09-04-2015 approved the followingproposal submitted by MP&NR vide summary dated 02-04-2015;To keep an option of commissioning of LNG terminal throughPSO, PSO may be allowed to import one commissioning cargothrough FSRU on FOB basis or LNG carrier on DES basisunder LNG SPA.’

Accordingly, PSO imported one cargo of LNG from Qatargas for aFertilizer Co. on board the FSRU on FOB basis which arrived on26th March, 2015 and the terminal was commissioned on 27thMarch 2015.

Status of LNG cargoes received till Oct 2015

Supplier Month Terms Status Slope PriceDES

AverageQG 26-Mar FOB Arrived $ 8.0500

$7.625

QG 24-Apr FOB Arrived $ 7.5000QG 11-May FOB Arrived $ 7.5000QG 28-May FOB Arrived $ 7.5000QG 15-Jun FOB Arrived $ 7.5000QG 9-Jul FOB Arrived $ 7.7000Tender 17-Jul DES Arrived 12.9500% $ 8.2321Tender 17-Jul DES Arrived 12.9500% $ 8.2321

$7.7151

Tender 28-Jul DES Arrived 13.4900% $ 8.5754

Tender 28-Aug DES Arrived 12.2700% $ 7.6142Tender 7-9 Sept DES Arrived 15.6000% $ 8.7758

Tender 20-22 Sep DES Arrived 11.8669% $ 6.6757Tender 6-8 Oct DES Arrived 14.8899% $ 7.6208Tender 16-18 Oct DES Arrived 15.8800% $8.1275Tender 26-28 Oct DES Arrived 11.9163% $6.0989

PSO – Qatargas2 SPA HighlightsTenure 2015 to December 31,2030

Extendable with mutual consent

Terms Take or PayType Delivered Ex-shipVolumes 2015 (prorate of 1.5mtpa)

2016 (1.5mtpa)2017 onwards (3mtpa)

2015 (prorate of 1.5mtpa)2016 (1.5mtpa)2017 onwards (3mtpa)

BuyerSeller

Pakistan State Oil Company LimitedQatar Liquified Gas Company Limited 2

Price revision After 10 yearsPrice and Terms By Price Negotiating Committee

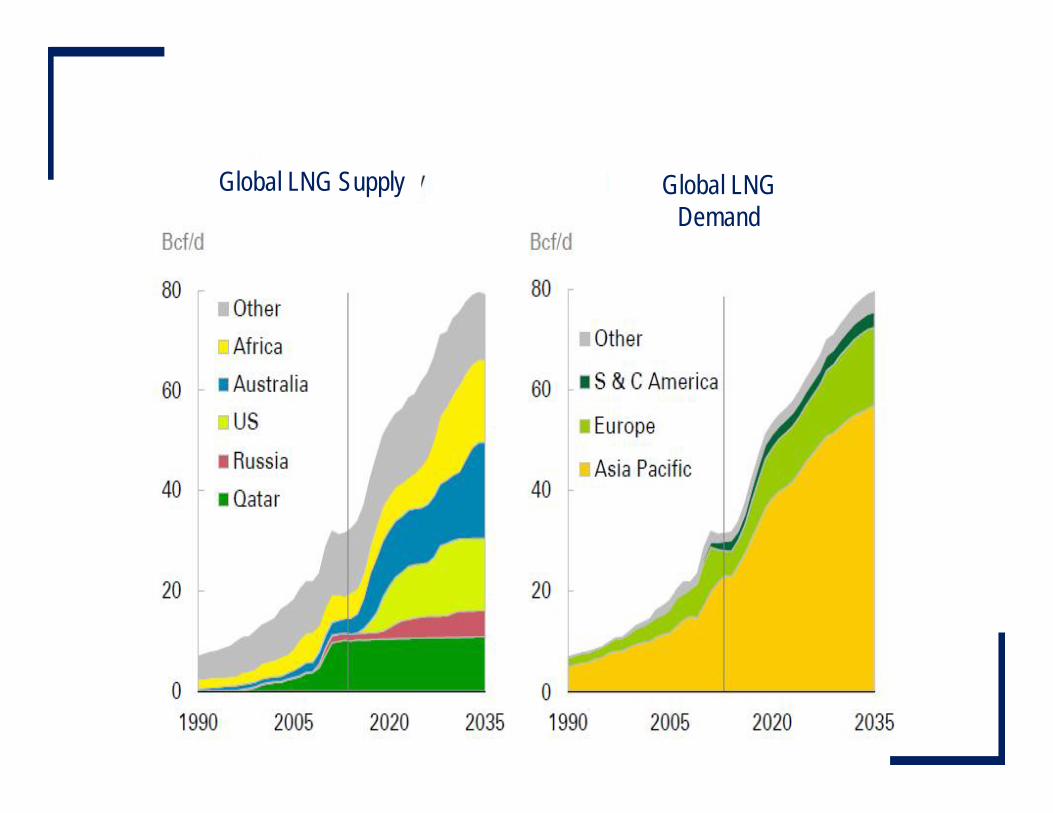

Global LNG Supply Global LNGDemand

Current LNG Import and Way forward

Long Term Deal

Spot/Multi-CargoTender

PSO has experienced Spot / Multicargo tenders since May 2015 andfirst cargo was received in July 2015

Government to Government1. With Qatargas2. Preliminary meetings held with:Petronas, Malaysia’s and with PBTrading Sendirian Berhad, BruneiDarussalam’s designated entity3. Interest shown by: Angola LNG andCNOOC

Spot/Multi-CargoTender

Term Tender for upto5 Years LNG Supplies

PSO has experienced Spot / Multicargo tenders since May 2015 andfirst cargo was received in July 2015

To be floated shortly

Thank You