Javier Lozano 1 Advanced Applied Macroeconomics 2007 Javier Lozano Universitat de les Illes Balears...

64

1 Javier Lozano Javier Lozano Advanced Applied Macroeconomics Advanced Applied Macroeconomics 2007 2007 Javier Lozano Universitat de les Illes Balears Master and PhD programs in Tourism and Environmental Economics University of the Balearic Islands

-

date post

19-Dec-2015 -

Category

Documents

-

view

215 -

download

0

Transcript of Javier Lozano 1 Advanced Applied Macroeconomics 2007 Javier Lozano Universitat de les Illes Balears...

1Javier LozanoJavier Lozano

Advanced Applied MacroeconomicsAdvanced Applied Macroeconomics

20072007

Javier Lozano

Universitat de les Illes Balears

Master and PhD programs in Tourism and Environmental Economics

University of the Balearic Islands

2Javier LozanoJavier Lozano

Today’s sesion

• Motivation and outline of the course

• Revision of some macro concepts and data

• Start with first part of the course

3Javier LozanoJavier Lozano

Motivation and outline of the course

4Javier LozanoJavier Lozano

What is macroeconomics about?

• Macroeconomics is the study of the determination of the main aggregate economic variables: GDP (national income), unemployment, inflation, exchange rates, balance of payments, etc.

• Intersectoral linkages studied in “Modelling the impact…” are not a topic of macroeconomics. One-sector economy is a typical assumption in macroeconomics

Motivation and outline

5Javier LozanoJavier Lozano

Why to study macroeconomics

• Macroeconomics does not study the specifities of tourism firm’s behaviour and tourist’s behaviour…

…however that behaviour depends on macroeconomic outcomes

• Examples:– Tourism demand depends on cyclical position of the tourists’

country, as well as on exchanges rates and relative CPI– Long-term economic growth and associated improvement of

standards of living have enable mass tourism– Cost pressures on (tourism) firms depend on expected inflation

and the cyclical position of the tourism destination– Macroeconomic stability (price stability, exchange rate stability,

sound public finances) is an important determinant of (tourism) multinationals’ decisions about where to invest.

Motivation and outline

6Javier LozanoJavier Lozano

Outline of the course

• Part I. Basic macro model (Javier Lozano)

• Part II. Topics on open economies (Javier Lozano)

• Part III. Topics on fiscal and monetary policies (Javier Andrés)

Motivation and outline

7Javier LozanoJavier Lozano

Outline of the course

• Part I. Basic macro model (Javier Lozano)– Model IS-PC-MR– Macroeconomic simulator

• Flexible tool that allows for different degrees of understanding, from black-box to full understanding of the underlying model

Evaluated with exercises on simulator (30% of final mark)

Motivation and outline

8Javier LozanoJavier Lozano

Outline of the course

• Part II. Topics on open economies (Javier Lozano)– Exchange rate determination– Exchange rate and balance of payments crisis

Evaluated with two-three problem sets and take-home exam (40% of final mark)

Motivation and outline

9Javier LozanoJavier Lozano

Outline of the course

• Part III. Topics on fiscal and monetary policies (Javier Andrés)

Evaluated with take-home exam (30%)

Motivation and outline

10Javier LozanoJavier Lozano

Revision of some macro concepts and data

11Javier LozanoJavier Lozano

List of some macro concepts

• Interest rates• Money• Inflation• Real and nominal variables• Endogenous and exogenous variables• National income; GDP• Economic growth• Exchange rate• Balance of payments• Exports and imports• Fiscal budget• ...

Revision concepts & data

Brad de Long Macroeconomics

glossary

12Javier LozanoJavier Lozano

Inflation

Revision concepts & data

13Javier LozanoJavier Lozano

Money

Revision concepts & data

14Javier LozanoJavier Lozano

Interest rates

Revision concepts & data

15Javier LozanoJavier Lozano

Nominal GDP vs real GDP

Revision concepts & data

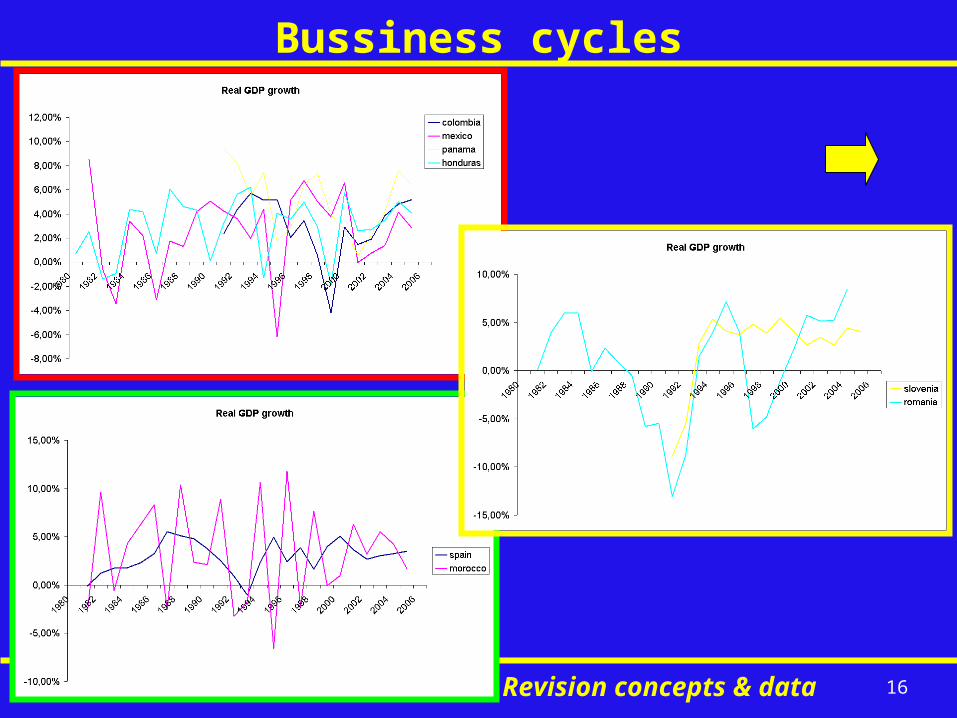

16Javier LozanoJavier Lozano

Bussiness cycles

Revision concepts & data

17Javier LozanoJavier Lozano

Economic growth and development

Revision concepts & data

18Javier LozanoJavier Lozano

Unemployment

Revision concepts & data

19Javier LozanoJavier Lozano

Nominal exchange rates

National currency/$(increase means

depreciation)

Revision concepts & data

20Javier LozanoJavier Lozano

PART I. Basic macroeconomic model

PART 1•Introduction•Phillips curve

What is the PC?

Price setting

Wage setting

Medium term equilibrium

Disequilibrium situations

Graphical representation•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

21Javier LozanoJavier Lozano

Production capacity and utilization

Part I. Basic macro model

PART 1•Introduction•Phillips curve

What is the PC?

Price setting

Wage setting

Medium term equilibrium

Disequilibrium situations

Graphical representation•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

22Javier LozanoJavier Lozano

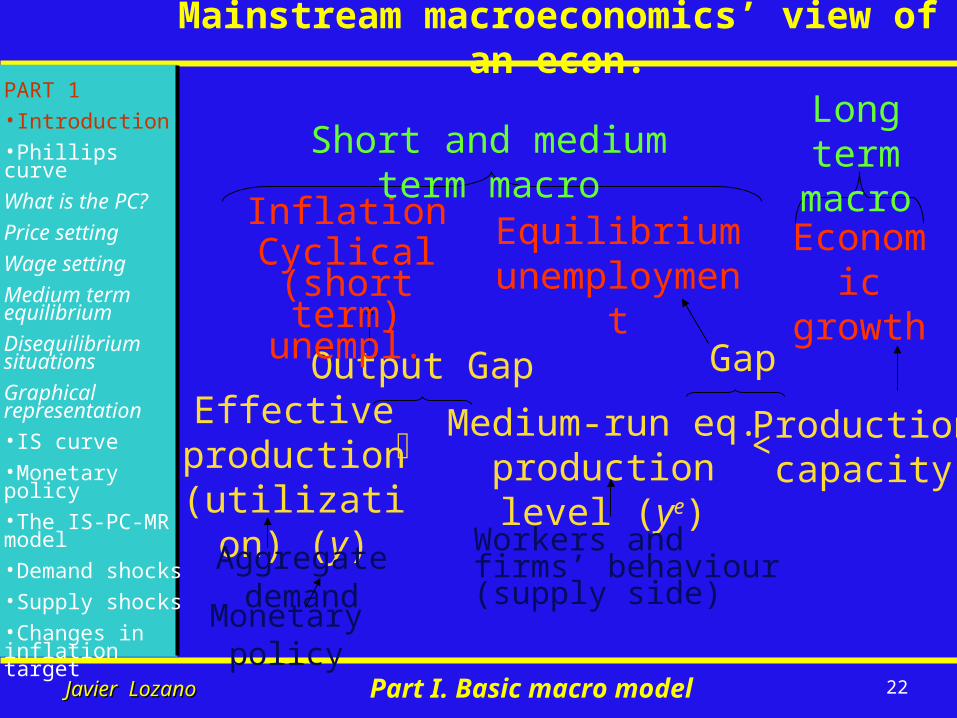

Mainstream macroeconomics’ view of an econ.

Effective production

(utilization) (y)

Production capacity

Output Gap

Medium-run eq. production level (ye)

Gap

<

InflationCyclical (short term) unempl.

Equilibrium unemployment

Economic growth

Short and medium term macroLong term

macro

Workers and firms’ behaviour (supply side)Aggregate demand

Monetary policy

Part I. Basic macro model

PART 1•Introduction•Phillips curve

What is the PC?

Price setting

Wage setting

Medium term equilibrium

Disequilibrium situations

Graphical representation•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

23Javier LozanoJavier Lozano

Model IS-PC-MR• Three equations dynamic model that allows to

understand the medium run equilibrium and fluctuations of inflation and effective production.

• Incorporates the (monetary) policy response to shocks (see The Economist article): monetary policy is endogenous

• We will first understand each of the three equations and then put them to work together.

Reminder: evaluation based on simulator exercises. Partial understanding of the model limits but does not rules out capacity to use simulator and interpret the results.

Part I. Basic macro model

PART 1•Introduction•Phillips curve

What is the PC?

Price setting

Wage setting

Medium term equilibrium

Disequilibrium situations

Graphical representation•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

24Javier LozanoJavier Lozano

Phillips curve (PC)

• Empirical relationship between inflation and the output gap

• Several specifications. Very common:

• Inflation () depends on:– Past inflation (possible more lags)– Output gap– Other factors (z) (exchange rate, price of

commodities such us oil)

• To understand inflation (price growth) we need to understand how prices are set

zyy etttt 1

Part I. Basic macro model

PART 1•Introduction•Phillips curve

What is the PC?

Price setting

Wage setting

Medium term equilibrium

Disequilibrium situations

Graphical representation•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

25Javier LozanoJavier Lozano

Phillips curve (PC)

PC for the Spanish economySource: Europawatch of BBVA. July 2006. pp 17-19

PART 1•Introduction•Phillips curve

What is the PC?

Price setting

Wage setting

Medium term equilibrium

Disequilibrium situations

Graphical representation•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

26Javier LozanoJavier Lozano

Price setting• Let us assume firms set prices according to the rule:

• Let us assume other costs=0

• Let us assume constant. Then:

)cos)(1( tsunitotherW

P

W

W

P

P

)1(

P

WwPS

Firms mark up unit costs by a percentage ( depends

on market power)

Given mark-up, productivity and nominal wage, the price setting implies a given

level of real wage=price-setting real wage

One source of inflation is nominal wage growth. We then need to learn

about wage setting

Part I. Basic macro model

UC

UC

P

P

In order to keep profit margin unchanged firms must raise prices in the same % as UC increase

PART 1•Introduction•Phillips curve

What is the PC?

Price setting

Wage setting

Medium term equilibrium

Disequilibrium situations

Graphical representation•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

27Javier LozanoJavier Lozano

Wage setting

• Let us assume that wages are set by unions. Unions set nominal wages but they care about real wages (purchasing power).

• Let us assume that unions set nominal wages in long term (one/two years) arrangements looking for a desired real wage and ignoring the price level for the arrangement’s period. In this case, wage setting will be as follows:

• We will assume Et= t-1, but, what are the determinants

of wws?

w

ww

W

W

wPWwP

W

WSE

WSEWSE

Unions want to compensate for expected erosion in purchasing

power plus another term to adjust effective w to desired wws

Part I. Basic macro model

PART 1•Introduction•Phillips curve

What is the PC?

Price setting

Wage setting

Medium term equilibrium

Disequilibrium situations

Graphical representation•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

28Javier LozanoJavier Lozano

Summary of 14th March session

• How to explain?price and wage setting

• Price setting:

• Wage setting:

• Example:

• Remaining question: determinants of wage gap (determinants of wws)?

zyy etttt 1

W

W

P

P

w

ww

w

ww

W

W WSWSE

1

%6%1%;51 WW

w

wwWS

29Javier LozanoJavier Lozano

Wage setting

• Some determinants of wws:– Unemployment: higher unemployment increases damage of

losing job (lower probability of finding new job) and then reduces workers aspirations in terms of wws

– Unemployment benefits: high unemployment benefits reduce downward pressure of unemployed on real wage

– Unions’ bargaining power: higher bargaining power will increase target wws

• wws=b(U, ); U=unemployment =other determinants

• wws=b(E, ); E=L-U; E=employment, L=labour force

• wws=b(y, ); y=E

Part I. Basic macro model

PART 1•Introduction•Phillips curve

What is the PC?

Price setting

Wage setting

Medium term equilibrium

Disequilibrium situations

Graphical representation•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

30Javier LozanoJavier Lozano

EL• Medium run equilibrium (Ee,ye): a situation where real

wage is at the level desired by both firms and workers, that is w=wws=wps

• In m-r equilibrium inflation is constant and there are no inflationary nor disinflationary pressures:

• WS:

• PS:

Medium run equilibrium

wps

Ee

wws

0;1

w

ww

w

ww

W

W WSWS

t

1

tt W

W

P

P

Part I. Basic macro model

PART 1•Introduction•Phillips curve

What is the PC?

Price setting

Wage setting

Medium term equilibrium

Disequilibrium situations

Graphical representation•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

31Javier LozanoJavier Lozano

Disequilibrium situations: changes in econ. activity

ELEe

wps

wws

)(0;)(0;1 downturnw

wwupturn

w

ww

w

ww WSWSWS

tt

Et

• An upturn in the economy (increase of E, y) raises wws. To achieve the desired increase in standards of living, unions increase the nominal wage rate of growth. This in turn increases inflation

Part I. Basic macro model

•An economic downturn (fall in E, y) reduces wws. Unions are les “aggressive” in wage setting so that the rate of growth of the nominal wage falls. This in turn reduces inflation

PART 1•Introduction•Phillips curve

What is the PC?

Price setting

Wage setting

Medium term equilibrium

Disequilibrium situations

Graphical representation•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

32Javier LozanoJavier Lozano

Back to the PC

• Notice that depends on the gap between E and Ee (or between y and ye), that is:

w

wwWS

)()( eeWS

yyyyfw

ww

etttt yy 1

Unions want to compensate for expected erosion in purchasing

power

Output gap causes inflationary/disinflationary

pressures since it affects workers’ desired real wage

Part I. Basic macro model

PART 1•Introduction•Phillips curve

What is the PC?

Price setting

Wage setting

Medium term equilibrium

Disequilibrium situations

Graphical representation•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

33Javier LozanoJavier Lozano

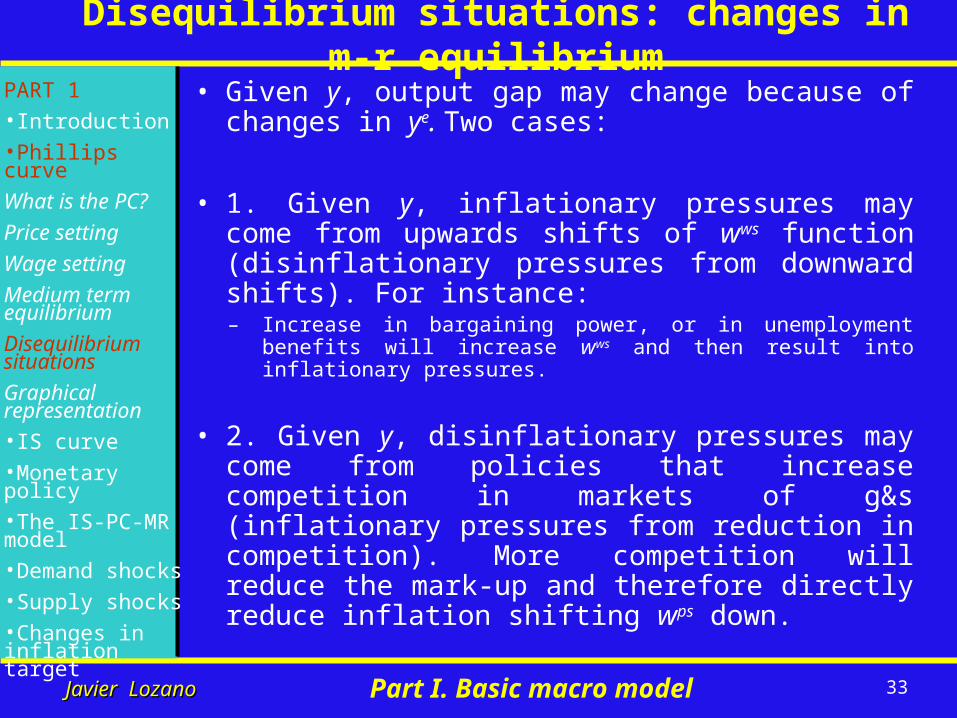

Disequilibrium situations: changes in m-r equilibrium

Part I. Basic macro model

• Given y, output gap may change because of changes in ye. Two cases:

• 1. Given y, inflationary pressures may come from upwards shifts of wws function (disinflationary pressures from downward shifts). For instance:– Increase in bargaining power, or in unemployment benefits will

increase wws and then result into inflationary pressures.

• 2. Given y, disinflationary pressures may come from policies that increase competition in markets of g&s (inflationary pressures from reduction in competition). More competition will reduce the mark-up and therefore directly reduce inflation shifting wps down.

PART 1•Introduction•Phillips curve

What is the PC?

Price setting

Wage setting

Medium term equilibrium

Disequilibrium situations

Graphical representation•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

34Javier LozanoJavier Lozano

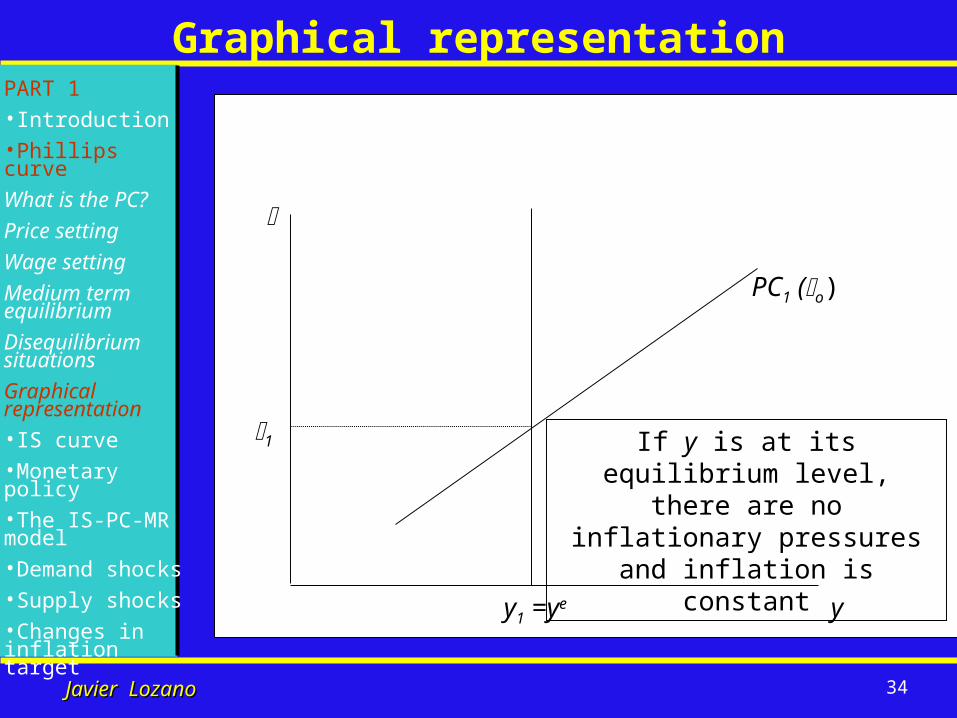

Graphical representation

y

y1 =ye

PC1 (o)

1

PART 1•Introduction•Phillips curve

What is the PC?

Price setting

Wage setting

Medium term equilibrium

Disequilibrium situations

Graphical representation•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

If y is at its equilibrium level, there are no inflationary pressures and

inflation is constant

35Javier LozanoJavier Lozano

Graphical representation

y

y1 =ye

PC2 (1)=PC1(0)

1

PART 1•Introduction•Phillips curve

What is the PC?

Price setting

Wage setting

Medium term equilibrium

Disequilibrium situations

Graphical representation•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

2

y2

Economic upturn creates inflationary pressures and inflation increases

PC3 (2)

This shifts PC upwards: even if inflationary

pressures disappeared (even if y3=ye) inflation

would remain permanently

higher=INFLATION PERSISTENCE

36Javier LozanoJavier Lozano

PC: what have we learnt?

• Current inflation depends on past inflation. This implies inflation persistence: an increase (decrease) in inflation tends to remain in the economy

• Inflation is a cyclical variable: economic upturns (with respect to ye) tend to cause inflationary pressures (economic downturns with respect to ye cause disinflationary pressures)

• Institutional changes in the labour market and changes in competition in the g &s markets have an effect on inflation

• Inflation also depend on changes in costs due to exchange rates fluctuations or changes in the price of imports. For instance, currency depreciation or higher oil prices will increase firms’ costs; firms will react increasing prices to compensate for higher costs

zyy etttt 1

37Javier LozanoJavier Lozano

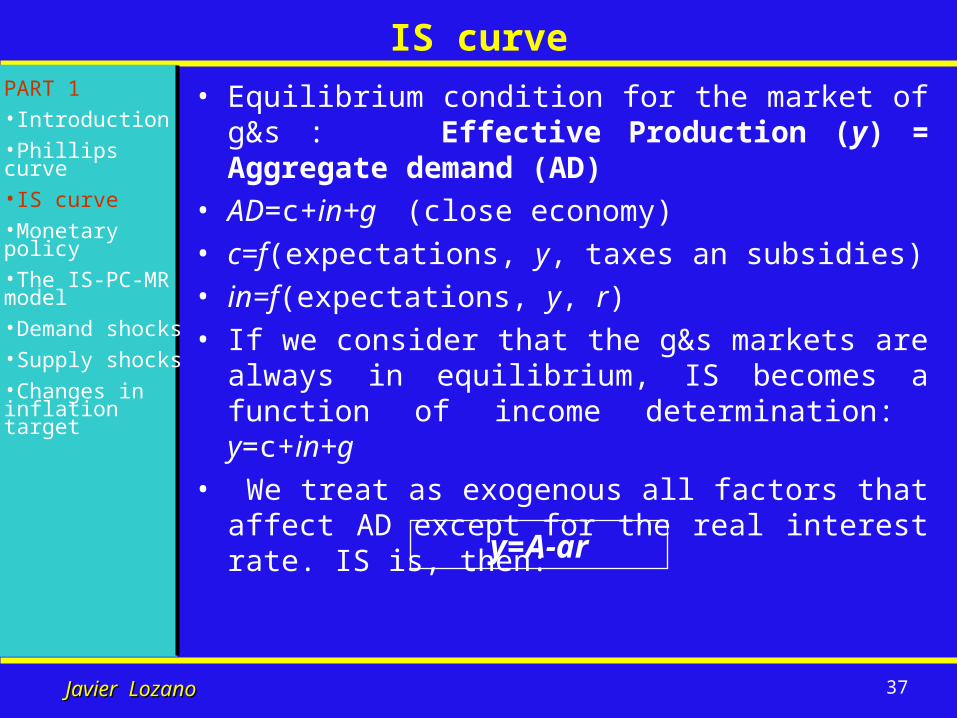

IS curve

• Equilibrium condition for the market of g&s : Effective Production (y) = Aggregate demand (AD)

• AD=c+in+g (close economy)

• c=f(expectations, y, taxes an subsidies)

• in=f(expectations, y, r)

• If we consider that the g&s markets are always in equilibrium, IS becomes a function of income determination: y=c+in+g

• We treat as exogenous all factors that affect AD except for the real interest rate. IS is, then:

PART 1•Introduction•Phillips curve•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

y=A-ar

38Javier LozanoJavier Lozano

We will assume that r is determined by the monetary policy decisions of the Central Bank

IS curvePART 1•Introduction•Phillips curve•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target y

r

IS

A (positive demand shocks;

expansionary fiscal policy)

A (negative demand shocks; contractionary fiscal policy)r0

y0

39Javier LozanoJavier Lozano

Monetary policy

• Monetary policy is a tool by which government can influence the economy by affecting interest rates.

• Central Bank actions to influence interest rates or the money supply

• Macroeconomic policy for aggregate demand management intended to promote macroeconomic goals through the Central Bank capacity to influence the money supply and interest rates.

PART 1•Introduction•Phillips curve•IS curve

Monetary policy

What’s monetary policy?

Transmission mechanism

MP lags

Neutral MP

CB preferences

Monetary rule•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

40Javier LozanoJavier Lozano

Transmission mechanism

• The process through which monetary policy decisions affect the economy in general, and the price level in particular

PART 1•Introduction•Phillips curve•IS curve•Monetary policy

What’s monetary policy?

Transmission mechanism

MP lags

Neutral MP

CB preferences

Monetary rule•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

From “The Monetary

policy of the ECB”, page 45 (see webpage)

41Javier LozanoJavier Lozano

•MP announcements•Current MP decisions•CB reputation (past behaviour)•Institutional design (independence)

Transmission mechanism

Short run nominal interest rate (i) AD y Long run real

interest rate (r) PCIS

expectations

CB

PART 1•Introduction•Phillips curve•IS curve•Monetary policy

What’s monetary policy?

Transmission mechanism

MP lags

Neutral MP

CB preferences

Monetary rule•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

42Javier LozanoJavier Lozano

Lags of monetary policy

MP lags: transmission mechanism is characterised by long, variable and uncertain time lags

To include these lags we consider the following IS:

yt+1 =At+1-art

PART 1•Introduction•Phillips curve•IS curve•Monetary policy

What’s monetary policy?

Transmission mechanism

MP lags

Neutral MP

CB preferences

Monetary rule•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

43Javier LozanoJavier Lozano

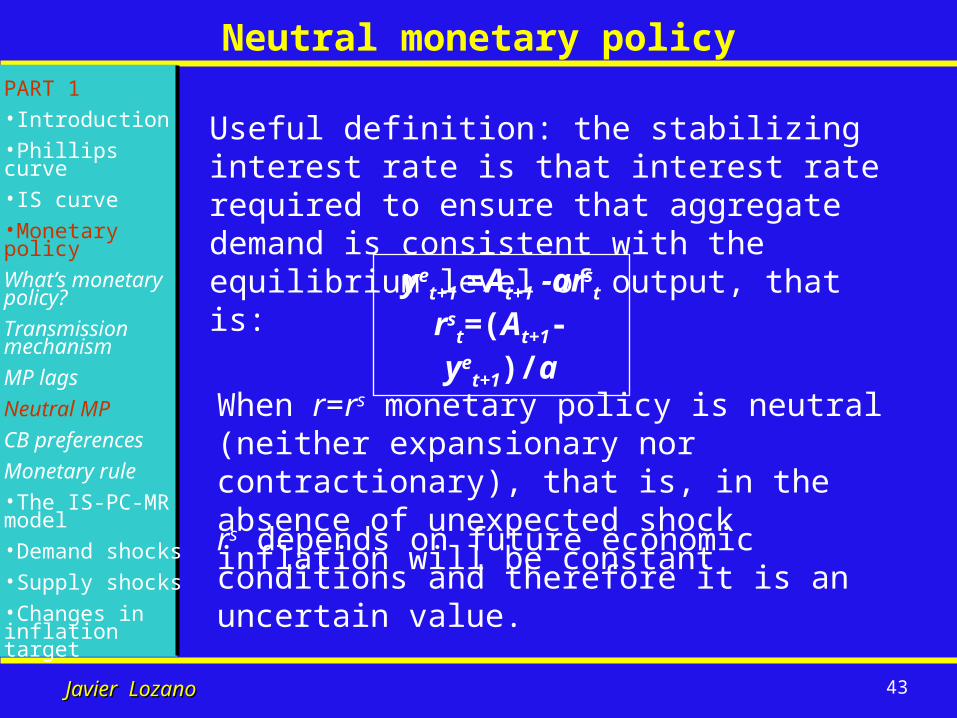

Neutral monetary policy

Useful definition: the stabilizing interest rate is that interest rate required to ensure that aggregate demand is consistent with the equilibrium level of output, that is:

yet+1 =At+1 -ars

t

rst=(At+1-ye

t+1)/a

PART 1•Introduction•Phillips curve•IS curve•Monetary policy

What’s monetary policy?

Transmission mechanism

MP lags

Neutral MP

CB preferences

Monetary rule•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

When r=rs monetary policy is neutral (neither expansionary nor contractionary), that is, in the absence of unexpected shock inflation will be constant

rs depends on future economic conditions and therefore it is an uncertain value.

44Javier LozanoJavier Lozano

Central bank preferences

• CB decision making is a complex process• We now formulate a model of CB decision making.

Despite the simplicity of the model, we will end up with an interest rate rule that describes fairly well current monetary policy.

• So, let us assume that the aim of CB when setting interest rates is to minimize the following loss function:

L=(y-ye)2-(- T)2

where T is an inflation target and measures the relative weight of inflation and y in CB’s preferences. (y-ye) is the output gap, whereas (-T) is the deviation of inflation with respect to target.

PART 1•Introduction•Phillips curve•IS curve•Monetary policy

What’s monetary policy?

Transmission mechanism

MP lags

Neutral MP

CB preferences

Monetary rule•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

45Javier LozanoJavier Lozano

Central bank preferences

• The loss function is based on the following realistic assumptions about modern CB preferences:

– The main CB’s objective is that inflation reaches a given target, T

– CB is also worried about the real effects (that is, on economic growth and employment) of MP. This statement should be qualified by the following:

• CB dislikes the negative effect on output and employment of disinflationary policies.

• Except for cases when inflation is too low, CB would not use MP to boost economic activity above ye because of the resulting increase in inflation

PART 1•Introduction•Phillips curve•IS curve•Monetary policy

What’s monetary policy?

Transmission mechanism

MP lags

Neutral MP

CB preferences

Monetary rule•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

46Javier LozanoJavier Lozano

Monetary rule

y

1. These ellipses are the indifference curves of CB

For each PC, the desired pair (y,) is determined by the

tangency point between the PC and an indifference curve

2. Each PC represent possible pairs (y,)

depending on past inflation

MR4. The MR line show the

preferred y, combinations

PART 1•Introduction•Phillips curve•IS curve•Monetary policy

What’s monetary policy?

Transmission mechanism

MP lags

Neutral MP

CB preferences

Monetary rule•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

T

ye

47Javier LozanoJavier Lozano

• CB cannot “choose” y and but can set an interest rate such that, given the rest of economic conditions, y and reach the desired values expressed by the MR line.

• It can be shown that the best way for the CB to reach the desired levels of y and is to set interest rates according to the following rule:

• Implications:

– If () then i (i); i> such that r (i>r)

– If >T then r>rs, so y<ye (CB creates infl. pressures to )– MP based on current (t) inflation, whereas, given lags, CB can

only influence future (t+1) inflation. Reason: given inflation persistence, current inflation affects future inflation.

– rst depends on future demand (At+1) and supply (ye

t+1) conditions: MP is implemented in an uncertainty context and many shock cannot be predicted beforehand.

Monetary rulePART 1•Introduction•Phillips curve•IS curve•Monetary policy

What’s monetary policy?

Transmission mechanism

MP lags

Neutral MP

CB preferences

Monetary rule•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

)()1( 2

Ttt

st a

ri t

48Javier LozanoJavier Lozano

Monetary rule: the Taylor rule

• In 1993 Taylor proposed the following rule as a good description of CB behaviour:

• It is argued that CBs follow much more complex decision-making procedures than the Taylor rule, and use much more information that the one contained in that rule

• However, it is also true that the Taylor rule fits the data on the CB interest rate fairly well (see slides)

• Our model can give place to a Taylor rule with the following modification of the PC:

where the output gap affects inflation with a lag. In this case, current output gap is relevant information of future inflation. That’s why it appears in the MP rule.

PART 1•Introduction•Phillips curve•IS curve•Monetary policy

What’s monetary policy?

Transmission mechanism

MP lags

Neutral MP

CB preferences

Monetary rule•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

)()( etty

Ttt

st yyri t

etttt yy 1

49Javier LozanoJavier Lozano

Monetary rule: the Taylor rule

50Javier LozanoJavier Lozano

Monetary policy: what have we learnt?

• With the interest rate the CB can trigger changes in economic activity (y) and, in this way, cause inflationary or disinflationary pressures that allow to reach the CB’s inflation target.

• CB’s preferences can be summarised by a set of inflation/output combinations (the MR) that are the most preferred by the CB, given economic conditions.

• CB’s decisions can be summarised by an interest rate rule that determines the interest rate that allows the economy to reach the MR line.

• The interest rate rule implies that to take decisions the CB uses information about current inflation deviations in inflation plus forecasts about future demand and supply conditions

51Javier LozanoJavier Lozano

The IS-PC-MR modelPART 1•Introduction•Phillips curve•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

tetttt zyy 1

)()1( 2

Ttt

st a

ri t

ttt arAy 11IS

PC

MR

(+ definition of rs)

Simulator: fairly easy to give hypothetical values to parameters and initial values to variables and put the three equations in excel

52Javier LozanoJavier Lozano

Demand shock

From “The 3-Equation New

Keynesian Model. AGraphical

Exposition” (see webpage)

PART 1•Introduction•Phillips curve•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

53Javier LozanoJavier Lozano

Supply shock

From “The 3-Equation New

Keynesian Model. AGraphical

Exposition” (see webpage)

PART 1•Introduction•Phillips curve•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

54Javier LozanoJavier Lozano

Changes in inflation target

y

y

r

IS

ye

PC (T)

y

-1 =T

T’MR

MR’

r-1

r0

0

PC (0)

1

r1

01

01

-1

PART 1•Introduction•Phillips curve•IS curve•Monetary policy•The IS-PC-MR model•Demand shocks•Supply shocks•Changes in inflation target

55Javier LozanoJavier Lozano

Shocks and changes in T: what have we learnt?

• Due to lags in the transmission mechanism and imperfect forecasting, the CB cannot avoid temporary deviations of inflation from the target.

• Due to inflation persistence, the CB needs to create disinflationary pressures when inflation increases above the target (this also applies when the CB reduces the target). This implies the implementation of painful fall in output and employment. However, the CB is sensitive with this output loss so it usually applies a gradual disinflationary policy.

• Both demand and supply shocks have temporary effects on inflation. However, whereas the output and employment effect of a demand shock is also temporary, the real effect on output of a (permanent) supply shock is permanent.

56Javier LozanoJavier Lozano

Definition of inflation

• An increase in the overall level of prices in an economy, usually measured as the annual percent change in its consumer price index

57Javier LozanoJavier Lozano

Definition of money

• A word that economists use in a technical sense. To an economist, "money" means only "wealth in the form of readily spendable purchasing power." Cash, plus balances in checking accounts, plus whatever other assets are held primarily as a way to keep purchasing power on hand to spend rather than as long-term investments.

58Javier LozanoJavier Lozano

Definition of interest rate

• The price, measured in percent per year, paid for borrowing money. Conversely, the return earned by saving.

• Nominal interest rate: The relative price at which monetary units can be transferred from the present to the future.

• Real interest rate: the relative price at which purchasing power can be transferred from the present to the future. r=i-

• (Nominal wage (W)=wage in monetary units; real wage=wage in purchasing power=w=W/P)

59Javier LozanoJavier Lozano

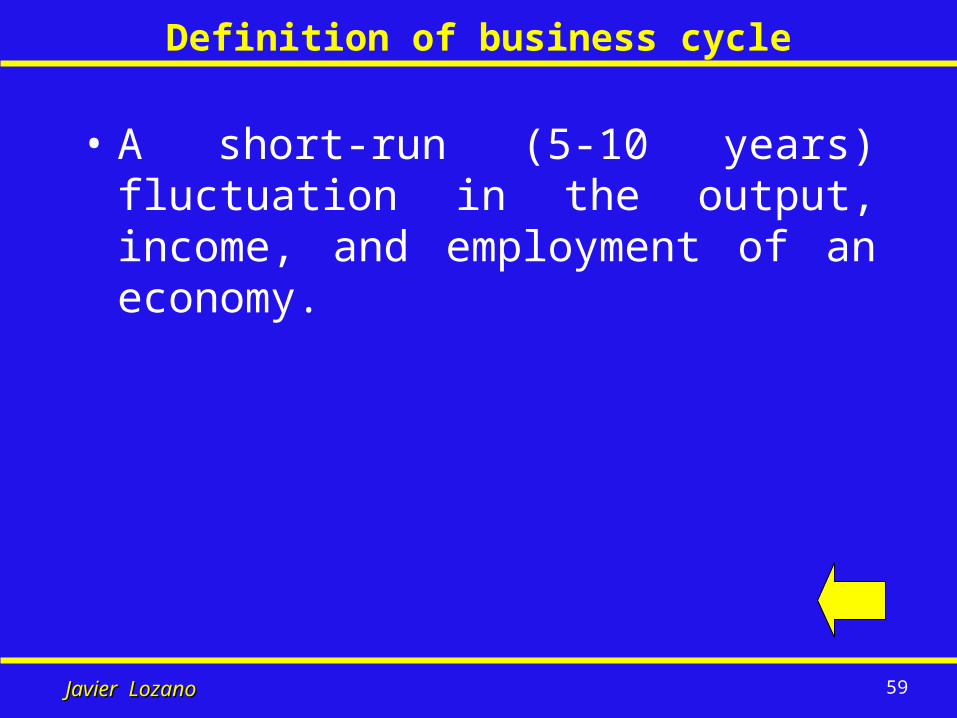

Definition of business cycle

• A short-run (5-10 years) fluctuation in the output, income, and employment of an economy.

60Javier LozanoJavier Lozano

Definition of economic growth

• The process by which productivity, living standards, and output increase (long-term economic growth).

• GDP growth rate

61Javier LozanoJavier Lozano

Definition of unemployment

• The share of the labour force who are looking for but have not found an acceptable job.

• The labour force is that share of working-age population that is willing to work

• Labour force=workers+unemployed

62Javier LozanoJavier Lozano

Definition of exchange rates

• The nominal exchange rate is the rate at which one country's currency can be turned into another's. The real exchange rate is the rate at which goods produced in one country can be bought or sold for another's. The definition of the exchange rate is either the value of home currency, or the price of foreign currency, depending on the country.

63Javier LozanoJavier Lozano

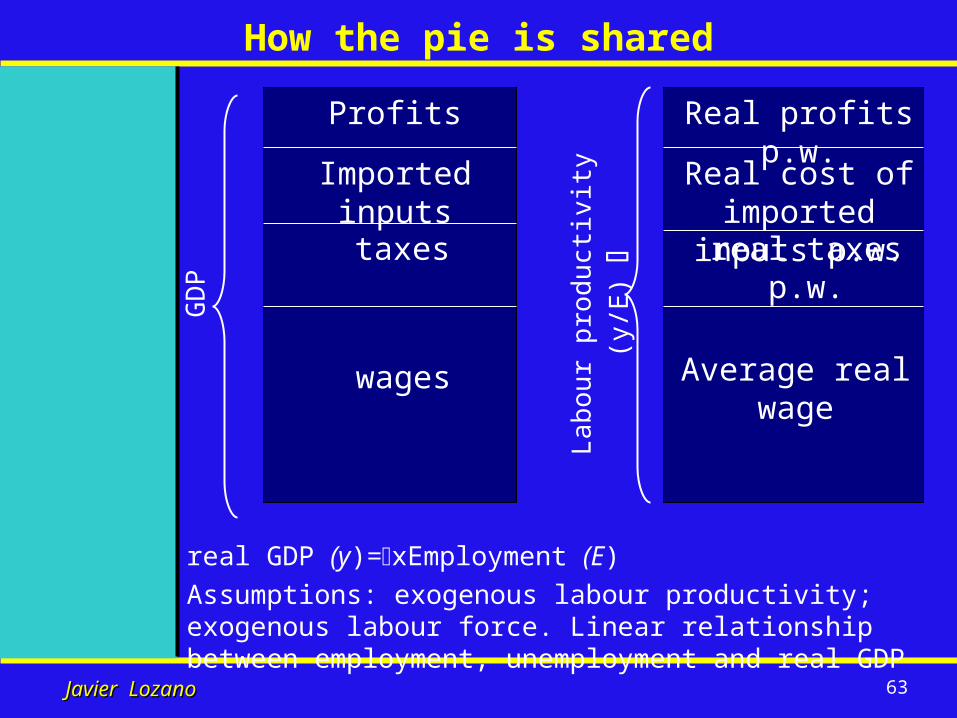

Real cost of imported inputs p.w.

How the pie is shared

GD

P

wages

taxes

Profits

Imported inputs

Lab

our

prod

uctiv

ity (

y/E

)

real GDP (y)=xEmployment (E)

Assumptions: exogenous labour productivity; exogenous labour force. Linear relationship between employment, unemployment and real GDP

real taxes p.w.

Real profits p.w.

Average real wage

64Javier LozanoJavier Lozano

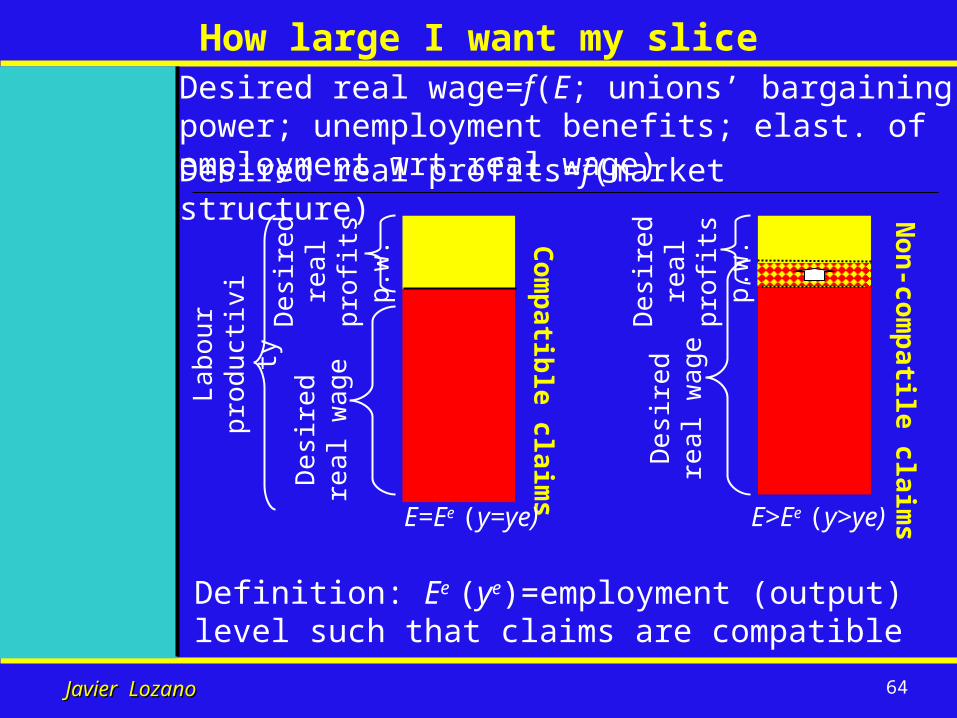

Des

ired

re

al p

rofi

ts

p.w

.

Des

ired

rea

l w

age

How large I want my slice

Lab

our

prod

uctiv

ity

Com

patib

le claims

Non

-comp

atile claims

Desired real wage=f(E; unions’ bargaining power; unemployment benefits; elast. of employment wrt real wage)

Desired real profits=f(market structure)

Des

ired

re

al p

rofi

ts

p.w

.

Des

ired

rea

l w

age

Definition: Ee (ye)=employment (output) level such that claims are compatible

E=Ee (y=ye) E>Ee (y>ye)