Investor Presentation May 2005 Kingsdale School – 17 th May 2005 Institutional Fund Managers’...

20

Investor Presentation May 2005 Kingsdale School – 17 th May 2005 Institutional Fund Managers’ Presentation

-

Upload

herbert-allison -

Category

Documents

-

view

215 -

download

1

Transcript of Investor Presentation May 2005 Kingsdale School – 17 th May 2005 Institutional Fund Managers’...

Investor Presentation May 2005

Kingsdale School – 17th May 2005

Institutional Fund Managers’ Presentation

Investor Presentation May 2005

Andy Sturgess – Managing Director

Construction

Investor Presentation May 2005

• Strength in sector focus approach

• Aligned to strong investment public & regulated sectors

• Education

• Health

• Affordable Housing

• Water

• Rail

• Well placed to maximise opportunities within changing government procurement initiatives

• Order book approaching £1 billion

Construction

Market Alignment

Investor Presentation May 2005

Construction

• Acknowledged as education specialists

• Award winning PFI expertise

• Northampton Schools – Preferred Bidder

• Norwich - ITN stage

• Building Schools for the Future

Education Capabilities

Investor Presentation May 2005

Construction

Kingsdale School

Investor Presentation May 2005

Construction

• Early contractor involvement

• Aligning logistics and planning with school

• Development of design solutions

• PTFE roof

• Timber geodesic auditorium

• Special finishes

• Safety & Environmental issues - live school

Kingsdale School – Technical Challenges

Investor Presentation May 2005

• Growth in education market - public sector investment

• Building Schools for the Future

• Procurement initiative for secondary education

• Total government spend £2.2 billion per year

• Plans for primary schools investment

• £1.9 billion per year

• Rebuild / refurbish over 8,900 primary schools

• Real opportunity

Construction

Education Outlook

Investor Presentation May 2005

• Sector focused

• Quality of order book across chosen sectors

• Culture aligned to collaboration and partnering

• Significant sustainable opportunities

• Growth in profits set to continue

Construction

Summary

Investor Presentation May 2005

Greg Fitzgerald – Managing Director

Housebuilding

Investor Presentation May 2005

Why Are We Different?

• Develop individually designed schemes

• Expertise in conversion/restoration

• High levels of customer focus

• Strong management teams

• Excellent record on planning

• Knowledge and focus on affordable housing

Housebuilding

Investor Presentation May 2005

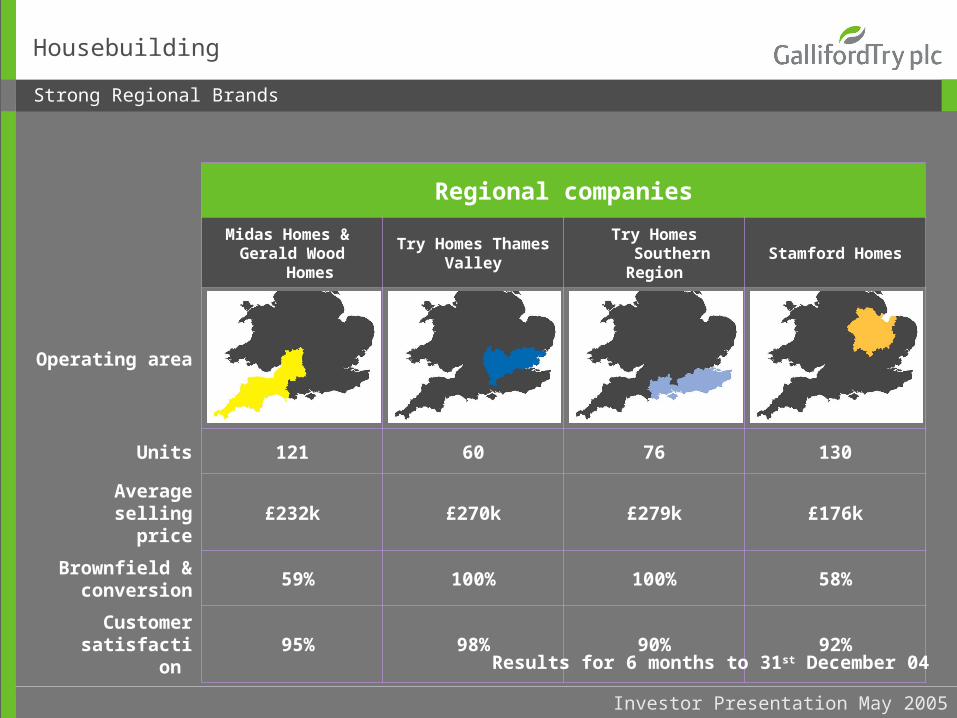

Strong Regional Brands

Regional companies

Midas Homes & Gerald Wood Homes

Try Homes ThamesValley

Try Homes SouthernRegion

Stamford Homes

Operating area

Units 121 60 76 130

Average selling price

£232k £270k £279k £176k

Brownfield & conversion

59% 100% 100% 58%

Customer satisfaction

95% 98% 90% 92%

Housebuilding

Results for 6 months to 31st December 04

Investor Presentation May 2005

2004

Housebuilding

6 months to 31st December 04

2003 Increase %

Units 387 367 5.4

ASP £000 228 228 -

Turnover £m 91.1 87.6 4.0

Margin % 13.3 12.8 3.9

ROCE % 22.5 21.6 4.2

Sales in hand February 05 £m 165.6 171.1 (3.2)

Operating Profit £m 12.1 11.2 8.0

Income per Sq. Ft. £ 220 197 11.7

Landbank February 05 units 2,464 2,342 5.2

Strategic land February 05 acres 666 676 (1.5)

Key Statistics

Investor Presentation May 2005

Current Trading Conditions - Sales

• More challenging market

• Increased use of incentives

• Interest rates close to peak

• New homes the attractive option

• Market fundamentals remain sound

Housebuilding

Investor Presentation May 2005

Current Trading Position - Land

• Hurdle rates for acquisition raised

• High level of competition

• 60% acquired on ‘one-to-one’ basis

• No sales inflation included in appraisals

Housebuilding

Investor Presentation May 2005

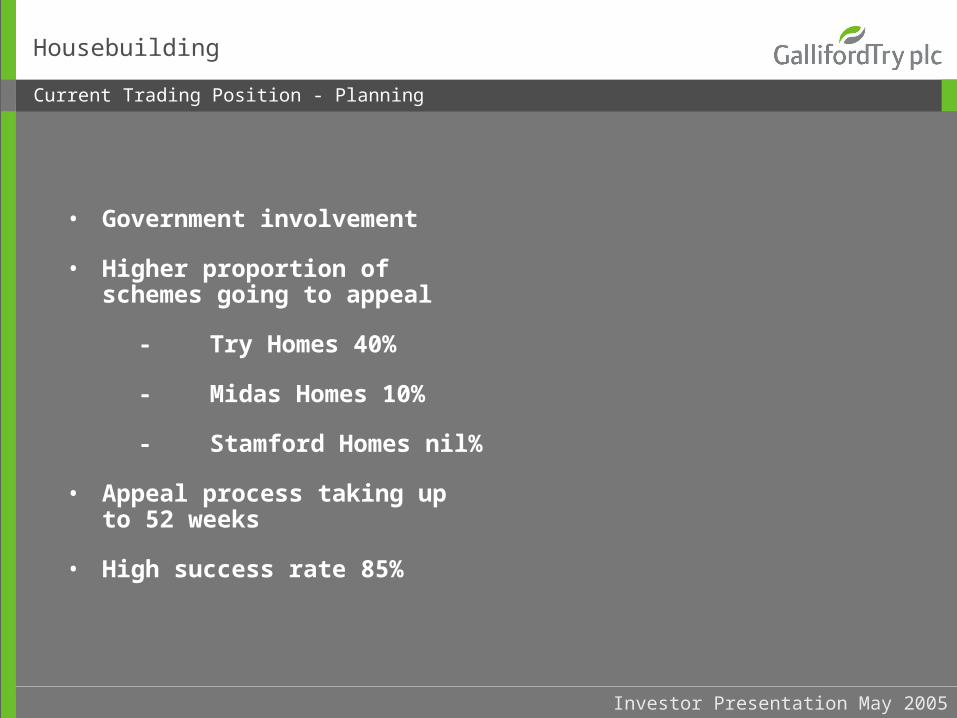

Current Trading Position - Planning

• Government involvement

• Higher proportion of schemes going to appeal

- Try Homes 40%

- Midas Homes 10%

- Stamford Homes nil%

• Appeal process taking up to 52 weeks

• High success rate 85%

Housebuilding

Investor Presentation May 2005

Current Trading Position - Production

• Traditional build 96%

• Timber frame 4%

• Safety record better than industry average

• Sub-contractor buying gains being achieved

Housebuilding

Investor Presentation May 2005

• Track record of success with

mixed tenure development

• Planning changes require different

perspective

• Partnership approach

• Strong regional market presence

Affordable Housing Capability

Housebuilding

Investor Presentation May 2005

• Three main forms:

– Contracting

~ working with 16 affordable

housing providers

– Enabling

~ generally 25% to 50% requirement on

schemes above 14 units

– Collaboration

~ Market leader in Southwest

~ Deferred land payment terms

Affordable Housing Procurement

Housebuilding

Investor Presentation May 2005

Expansion Plan

• 1300 units by 2008

• Management structure in place

• Business plan implemented

- Increased market share

- Geographic expansion

• Bolt-on acquisitions (opportunistic)

Housebuilding

Investor Presentation May 2005

Summary and Outlook

• Expect to achieve full year planned performance

• Well placed to capitalise on growth in affordable housing

• Prepared for tougher market conditions

• Enhance efficiency through additional cost reductions

• Good position for 05/06

• Confident of achieving expansion plan

Housebuilding

![Telecomm presentation [2005]](https://static.fdocuments.net/doc/165x107/55508844b4c9051e5b8b4b8a/telecomm-presentation-2005.jpg)