International Marketing Plan

158

International Marketing Plan For the Export of "Shirohana Flowers" to Germany Planning Year: 2011 A Group Assignment by Lecturer: Mr. G.D. Samarasinghe Name MC CPM P.J.B.R. Nirmali 55595 4442 U.G.A. Gunawardene 55414 4262 M.S.M. Perera 55645 4492 K.K.P.S.K Kohombakanda 57580 5454 M.L.C.A. Vincent 55829 4675

-

Upload

anuradhasaliyaamarathunga -

Category

Documents

-

view

267 -

download

2

Transcript of International Marketing Plan

International Marketing Plan

For the Export of

"Shirohana Flowers" to GermanyPlanning Year: 2011

A Group Assignment

by

Lecturer: Mr. G.D. Samarasinghe

The Department of Marketing Management

The University of Sri Jayewardenepura

Name MC CPMP.J.B.R. Nirmali 55595 4442U.G.A. Gunawardene 55414 4262M.S.M. Perera 55645 4492K.K.P.S.K Kohombakanda 57580 5454M.L.C.A. Vincent 55829 4675

1

Sri Lanka.

Table of Contents

Executive Summary.............................................................................................................3

1. Introduction......................................................................................................................5

1.1 Introduction to the Company.....................................................................................5

1.2 Global Cut Flower Industry.....................................................................................12

1.3 Floriculture industry in Sri Lanka............................................................................16

2. Country Introduction....................................................................................................19

2.1 Geographical Setting................................................................................................19

2.2 Relevant History......................................................................................................21

2.3 Social Institutions.....................................................................................................25

2.4 Cultural Aspects.......................................................................................................28

2.5 Living conditions.....................................................................................................36

2.6 Languages and Religions.........................................................................................37

2.7 General facts............................................................................................................38

3. Economic Analysis........................................................................................................39

3.1 Population................................................................................................................39

3.2 Economic Statistics & Activity................................................................................40

3.3 Development in Science & Technology..................................................................47

3.4 Channels of Distribution..........................................................................................50

3.5 Media.......................................................................................................................54

4. Market Audit and Competitive Market Analysis...........................................................61

4.1 The Product..............................................................................................................61

4.1.1 Evaluation of the product's USP........................................................................61

4.1.2 Major problems of product acceptance.............................................................64

4.2 The Market...............................................................................................................65

4.2.1 Market size & evolution....................................................................................65

4.2.2 Consumer buying habits....................................................................................66

2

4.2.3 Existent competitors’ products..........................................................................70

4.2.4 Marketing mix typically used............................................................................75

4.3 Government Intervention in the Market place.........................................................84

5. Preliminary Marketing Plan...........................................................................................88

5.1 Marketing Plan.........................................................................................................88

5.1.1 Marketing Objectives........................................................................................88

5.1.2 Product Adaptations / Modifications.................................................................89

5.1.3 Promotion Mix..................................................................................................93

5.1.4 International Distribution..................................................................................96

5.1.5 Local Channel of Distribution...........................................................................98

5.1.6 Price Determination.........................................................................................100

5.1.7 Terms of Sale...................................................................................................100

5.1.8 Method of Payment.........................................................................................102

5.2 Pro-Forma Financial Statements & Budget...........................................................102

5.2.1 Marketing Budget............................................................................................102

5.2.2 Pro Forma Annual Profit & Loss Statement...................................................103

5.3 Resource Requirements..........................................................................................104

5.3.1 Financial Resources.........................................................................................104

5.3.2 Human Resources............................................................................................105

5.3.3 Production Capacity........................................................................................105

5.4 Implementation and Control..................................................................................106

6.0 Sources of information..............................................................................................107

3

Executive Summary

Shirohana is the leader in the cut flower industry in Sri Lanka. The management team at

Shirohana is contemplating moving into lucrative export markets. An analysis was

carried out to identify potential export destinations, of which Germany was chosen as the

proposed export destination out of a list of 20 potential countries.

A thorough analysis was carried out on the political and economic situation prevailing in

Germany. It was identified that the German economy was recovering from the global

economic and financial turmoil in 2009.

A review of the cut flower market in Germany revealed that there was a significant trend

in giving flowers as gifts for males. Despite this majority of the cut flower purchases are

made by females (74%). Mono-bunches account for nearly 50% of the entire cut flower

market, with Rosa accounting for 50% of all mono-bunches. It was also found that

elderly people generally spend relatively more money on flowers than young people. The

most important attributes governing the purchase of cut flowers in order of importance

were flower/bloom quality, colour, price, design/arrangement, longevity, availability and

fragrance. Florists are the most important retail channels in Germany, holding a market

share of more than 50%.

Shirohana flowers initially hopes to grab a 0.5% share of German cut flowers imports of

Carnations (Dianthus) and Orchids. A contract is to be entered with Omniflora, an

importing wholesaler in Germany, for the sale of cut flowers. In addition, a business

partnership is expected to be developed with Real, a hypermarket and several florists via

Omniflora. The domestic distribution would be handled by E.B. Creasy (freight

forwarder) and the international distribution by the logistics arm of Omniflora, Jet

Flowers. The FOB price was determined to € 0.16 and € 0.09 for orchids and carnations

respectively.

4

A range of advertising and promotional activities are planned and the marketing budget

for the first year of operation comes to around € 6,300. The operation is expected to yield

the following results during its first year of operation:

Sales revenue: € 146,016

Gross profit: € 43,805

Net profit: € 1,591

The net profit in domestic currency is expected to be Rs. 250,000 and the net profit

margin is 1.1%.

The current spare production capacity at Shirohana is 500,000 stems which is 819,375

stems below the total export requirement for 2011. Hence, it is necessary to invest in a

new greenhouse to cater for both domestic and international expansion.

It was also determined that the initial financial requirement amounts to Rs. 2,500,000 on

account of the need to construct a new greenhouse (Rs. 1,500,000), and the material cost

to be incurred for the production of the first batch of cut flower exports (Rs. 1,000,000).

The additional human resource cost amounts to Rs. Rs. 5,160,000, which also includes

the recruitment of an International Operations Manager who would overlook the entire

operation and would be responsible for the implementation of the plan.

5

1. Introduction

1.1 Introduction to the Company

The Shirohana website unfolds the story of

Shirohana as follows. Shirohana was

established in Sri Lanka in 1986 in an era

when good quality greenhouse grown flowers

and stylish flower shops were not in existence.

Over the next few years, the Shirohana concept

of sensational flower shops situated at

exclusive locations in Colombo, using antique

and reclaimed objects together with stylish

flower arrangements, began to set new trends

and changed opinions about flowers in Sri

Lanka. The Shirohana concept had begun and

instantaneously, presenting flowers as gifts

became immensely popular and accepted.

The first Shirohana shop was opened over 20 years ago in Galle Face, the heart of

Colombo. Today, its flower shops are located in the most exclusive locations in the City,

including Colombo 02, 03, 04, 07, 08 and Negombo, Kandy, and very soon in the historic

Fort of Galle.

The market for flowers has grown at a tremendous pace and Shirohana has helped to

develop this trend by making beautiful bouquets of flowers easily available, thus

developing an awakening interest in flowers amongst a generation of retail customers.

Constantly challenging boundaries and concepts, Shirohana remains the Leader in the Sri

Lanka flower scene. Their highly acclaimed chain of flower shops recognizes the power

of flowers to awake a range of emotions. The designs inspire without been fussy,

reflecting the natural world while oozing sophistication.

6

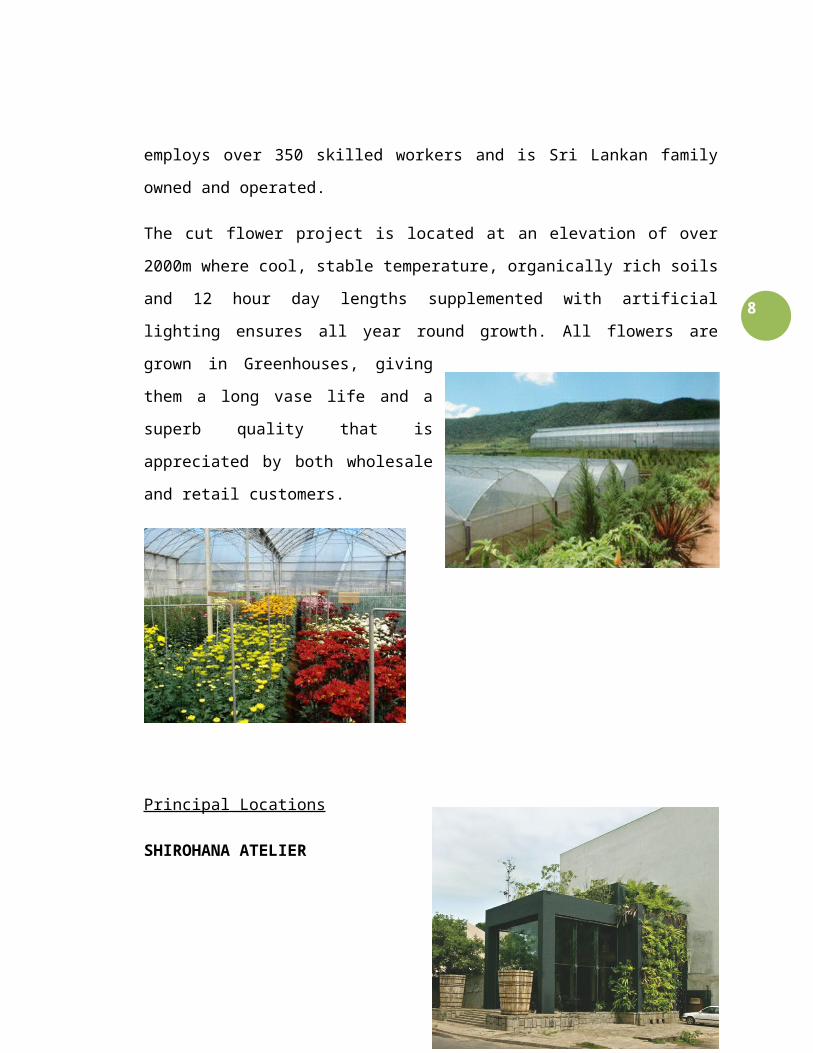

Flower production

Shirohana is the pioneer in cut flower production in Sri Lanka with over 35 years

experience in the growing of cut flowers. It has its own farm located in Nuwara Eliya

which employs over 350 skilled workers and is Sri Lankan family owned and operated.

The cut flower project is located at an elevation of over 2000m where cool, stable

temperature, organically rich soils and 12 hour day lengths supplemented with artificial

lighting ensures all year round growth. All flowers are grown in Greenhouses, giving

them a long vase life and a superb quality that is appreciated by both wholesale and retail

customers.

Principal Locations

SHIROHANA ATELIER

No. 21/3, Alfred House Gardens, Colombo

03, Sri Lanka

SHIROHANA FLOWER ROAD

No. 47, Flower Road, Colombo 07, Sri

Lanka

7

SHIROHANA PETAL GURU

No. 61, Dudley Senanayake Mawatha, Colombo 08, Sri Lanka

SHIROHANA GALLE FACE

No. 32B, Sir Mohamed Marcan Markar Mawatha, Colombo 03, Sri Lanka

SHIROHANA KANDY

Kandy City Centre, LI - 12, Daladha Veediya, Kandy, Sri Lanka

SHIROHANA NEGOMBO

No. 206 B, Colombo Road, Negombo, Sri Lanka

Proposed new showrooms locations include;

SHIROHANA PALAWATTE

474, Palawatte, Battaramulla, Sri Lanka

SHIROHANA ROMANTICO

32/01 B, Dickmons Road, Colombo - 04, Sri Lanka

SHIROHANA FORT GALLE

No.9, Church Cross Street, Fort Galle, Sri Lanka

Product and Service Offerings

Shirohana is a full service wedding and party design establishment focused on designing

and availing the freshest flowers for any event. Whatever the occasion, whether it be a

new product or business launch, fashion show, academic or corporate event, birthdays,

8

graduation, anniversary, holiday celebration or private parties, Shirohana offers its expert

floral services.

The Shirohana client base is made up of discerning brides, elite socialites, and prominent

businesses all over the country and overseas.

As part of its wedding services Shirohana offers;

Wedding flowers – include bouquets, corsages,

boutonnieres, and ceremony décor

Bridal flowers – bride’s bouquet, going away, maids

bouquet, groom and bestmen and flower girls

Reception – adorning the reception tables

Car décor

Church décor

Floral designing and planning services

Shirohana offers flowers for a variety of other occasions under the following themes.

Anniversary

Birthday

Get well

Love you

I’m sorry

New baby

Party

Thank you

Garlands

Sympathy

9

Varieties

The flower varieties offered by Shirohana include the following;

Standard Carnations Spray Carnations

Alstomeria Chrysanthemum (standard)

Chrysanthemum (spray) Lilies

10

Gerberas Gypsophila

Iris Tulips

Heliconias Roses

11

Orchids Lotus

Jasmine

Competitive advantage of Shirohana in Sri Lanka

The competitive advantage of Shirohana in Sri Lanka is as follows.

Direct dealing with the end consumer – fresher flowers that are reasonably priced

Follow international trends and constantly upgrade their flower designs

Cater to all budgets, from a single stem to a large and dazzling arrangement

Possession of one of the leading floricultural farms in South East Asia

Broad product range – from bouquets to interior décor

Personalization – arrangements can follow emotions and be as variable as moods or

fashions. Each bouquet is delivered with personalized cards with the customer’s own

individual messages.

12

Decision to go global

Shirohana is the market leader in the Sri Lankan flower industry, and as part of its

expansion strategy the management has decided to tap potential export markets.

Where to go?

An initial screening was done on 20 identified potential export destinations:

Germany, UK, France, Netherlands, Italy, Belgium, Denmark, Spain, Ireland,

Finland, Austria, Sweden, Greece, US, Japan, Switzerland, Canada, Norway, Poland

and Czech Republic. Countries were screened based on cost of air freight to

destination and share of world imports. Three key potential markets were identified

for entry: Germany, UK and Netherlands.

A detailed analysis of the selected 03 economies based on political stability,

economic situation, market situation and potential revealed Germany to be the best

export destination.

1.2 Global Cut Flower Industry

Wernett (1998) explain the evolution of the global cut flower industry. Forty years ago,

demand for cut flowers by consumers around the world was satisfied by local cut flower

production. In Europe, per capita consumption was significant, and consumer culture

required a large supply of cut flowers for gifts, occasions, and everyday use. As a result,

cut flower production in Europe was sizeable. Gradually as transportation systems

developed throughout this region, it became possible to distribute cut flowers grown in

southern areas of Europe to northern areas of Europe. Consequently, the European flower

industry began to extend its boundaries for cut flower production and along with this

expansion grew the influence of the European flower industry. This background history

could be considered the beginning of commercial floriculture as we know it today.

13

When the world energy crisis occurred in 1973, the marketing plan for distributing cut

flowers grown in different European countries to Holland for sale through the Dutch

flower auction and back to markets throughout Europe became a significant production

opportunity for southern European cut flower growers. Increasingly larger quantities of

cut flowers were grown in southern Europe to meet the demand for cut flower sales

through Holland. Flower growers in the southern regions had a price advantage over

growers located in northern regions because cut flower production was more expensive

for northern growers during the winter season due to increased energy costs required to

obtain quality flowers in controlled temperature greenhouses.

Then, competition for southern European cut flower growers intensified when Israeli cut

flower growers, who were located further south entered the market with product to be

sold through the Dutch flower auction. Israeli growers had the production advantage of

being further south where they could produce cut flowers in open fields or plastic tunnels

year round, eliminating most of the overhead expenses for greenhouses and heating

systems. But in order to develop a potentially lucrative export cut flower industry for

themselves, the Israelis needed to address limiting factors to their success. The two main

limiting factors were transportation costs to Europe and a water shortage if production

were to expand.

Solutions to these limiting factors were found for Israeli growers. In the case of

transportation costs which offset growers cost advantage in terms of energy compared to

growers in southern Europe, the government provided transportation subsidies which

have reduced the costs to the growers to ship their cut flower product to Europe, thereby

maintaining a competitive cost advantage over European growers. As for the water

shortage, research on irrigation systems that would conserve water usage was applied to

production systems for cut flowers.

Through the 1970’s, the activities of the European flower industry had begun to influence

cut flower production and sales beyond the borders of Europe. Cut flower sales through

the Dutch flower auctions had gained a share of the United States market. This was

14

achieved by promotion activities in the USA supported by the Holland Flower Council

which encouraged Americans to purchase more cut flowers for gifts, occasions and

everyday use, similar to consumer habits in Europe. Most of the flowers sold to the USA

through the Dutch flower auctions are shipped to the USA by air through New York.

Simultaneously, Miami, USA, was being developed as a key import distribution base for

cut flowers being grown in Columbia, South America and shipped north. This caused

considerable competition for local cut flower growers in the USA. Manufacturers and

suppliers from the European flower industry were quick to find opportunity in this

situation. Not only were South American cut flower growers purchasing varieties from

Europe but flower growers from the USA were persuaded to invest in production systems

and equipment from Europe in hopes of becoming more efficient producers like the

Dutch growers who had once faced competition from southern European growers. As a

result, the United States flower industry owes a significant share of its growth in terms of

promotion and sales and improved production systems to the influence of the European

flower industry.

It is worthwhile to mention that the Israeli flower industry has become a formidable

competitor of the European flower industry. Israeli cut flower producers ship significant

quantities of product into the USA market via both New York and Miami. This

compensates Israeli producers for the reduction in cut flower sales to the European

market which is increasingly being supplied by flower growers from regions in Africa,

especially Kenya. Also, Israelis have been successful in selling their production

equipment and varieties to flower growers in other countries.

Continuing to advance in the 1980’s, the European flower industry began seeking further

opportunity and expansion in Asia by 1985. Japan’s bubble economy was starting to

inflate and discretionary income spending by the Japanese was rising. European flower

imports made headway into the lucrative market in Japan. Within a few years, as

economies in Korea, Taiwan, and Hong Kong strengthened, the European flower industry

moved into these markets with their cut flower exports as well.

15

Since the early 1990’s, the European flower industry, as a worldwide leader in

commercial floriculture, has been impacting the rest of Asia with cut flower imports from

Holland and sales of flower varieties, production equipment, and technology for new

production operations in Asia. Israeli cut flower producers, manufacturers, and suppliers

have followed but, one step behind. The main difference between the European flower

industry and the Israeli flower industry is that the European flower industry enters their

new markets by launching aggressive marketing campaigns which call attention to the

quality and image of Dutch flowers. These campaigns stimulate demand by new

consumers for their cut flower products. So far, the Israelis have not particularly created

an image for end consumers of Israeli flowers. This difference is one of the factors which

contribute to the European flower industry being the worldwide leader in commercial

floriculture.

Initially, commercial floriculture production in Southeast Asia was developed because of

increasing need for low cost flowers by the European cut flower market place. European

flower traders identified commercial floriculture production in Southeast Asian countries

as a source of supply. Ironically, Dutch auctions often served to re-distribute this product

to the Japanese market. By the mid to late 1980’s, Dutch importers/exporters had begun

selling floriculture product in Japan. With economies expanding, the “little tigers”, i.e.

Taiwan, Korea and Hong Kong were the next Asian targets with market needs for

floriculture products from Europe and potentially from other Asian countries which could

produce floriculture products less expensively.

The development of the commercial cut flower industry in Asia has been unlike that of

Israel, African countries, south and Central American countries. In the latter regions, cut

flowers have been a product produced mainly for export with no thought of a potential

domestic market. On the other hand, in Asia, whereas cut flowers were initially produced

for export, the market potential has rapidly changed to include opportunities for

supplying the local market as well. This unique development is on account of the rapid

strengthening of economies in the region, high population densities, and the consumer

16

perception which has been promoted heavily by the European flower industry that the use

of fresh flowers in one’s everyday life represents an improved, quality lifestyle.

1.3 Floriculture industry in Sri Lanka

The Sri Lanka Export Development Board provides the following information regarding

the floriculture industry in Sri Lanka. The export-oriented floriculture Industry was

established during year 1980/81 period. Since then it has shown a remarkable growth.

Today the industry is comprised of about 40 major export companies, including a few

foreign investors. Floriculture sector employees over 5,000 people and more than 10,000

families in the semi urban and rural areas are indirectly involved in exports as out

growers to the existing companies. This is one of the few agriculture based industries that

employees people throughout the year at the rate of 5-7 workers per acre. The net foreign

exchange earning capacity of the sector is around 85%-90%. In year 2008 Sri Lanka has

earned Rs 1,562 Mn (US $ 14.52) worth of foreign exchange by exporting floriculture

products and in year 2010 there was a drop in exports to US$ 11.5 due to the global

recession. The exports have slightly recovered during year 2010.

Strengths

Climatic variations and diverse topography enabling to cultivate a range of products

from tropical to temperate

Availability of cultivation technology to finish products according to international

standards

Skilled labor

Availability of coco peat as a growing media

Reputation built up as a supplier of quality products

Encouragement received from the Government

17

Application of Good Agricultural Practices to protect the environment, safeguard

workers and sustainable use of natural resources.

Opportunities

Expanding new markets

Opportunities to export value added products

New developments in sea transportation

Product Assortment

Ornamental Foliage Plants

Cut decorative leaves

Cut Flowers

Aquarium plants

Landscaping plants

Tissue cultured plants

Major Production Regions

Western province-Gampaha, Kaluthara and Colombo Districts

North Western Province- Kurunegala, Puttalam Districts

Central Province – Kandy, Kegalle, Matale, N’ Eliya, Bandarawela

Possible Areas for Expansion

Southern Province

Sabaragamuwa Province

18

Share in the world market

Sri Lankan Exports 2010 – US$ Mn. 11.7

Growth in Sri Lankan exports (2006-2010) – 3 %

Sri Lankan Share in the World Market (2010) – 0.1%

World Ranking (2010) – 52

Sri Lanka Floriculture Exports

Product 2006 2007 2008 2009 2010Live Plants 4,989,546 4,873,013 6,798,738 5,894,094 5,923,955Cut Flowers 5,597,486 6,323,128 6,568,802 5,117,526 4,701,978Fresh Decorative Leaves

661,931 832,232 816,442 435,240 1,116,914

Total 11,248,963 12,028,373 14,183,982 11,446,860 11,742,847Source: Sri Lanka Export Development Board

The export market

Europe is the major market for Sri Lankan floricultural products and accounted for 62%

(Rs. 820 Mn) of our total floriculture exports in year 2009. The Netherlands is the leading

importer in Europe and continues to be the number one market for Sri Lankan floriculture

products absorbing 36% of our total exports (Rs. 477 Mn) in year 2009. Japan, South

Korea and the Middle East are the other major import markets.

Major Competitors

Central America – Costa Rica, Guatemala

Africa – Kenya, Israel, Ethiopia

Asia – India, Malaysia, Thailand, China

19

2. Country Introduction

Germany is the largest economy in the in the European Union (EU), and is the world's

fourth largest economy by nominal GDP and the fifth largest by purchasing power parity

(World Bank, 2011). It is also the third largest exporter and importer of goods and

services in the world. As per the Centre for the Promotion of Imports (2008) Germany is

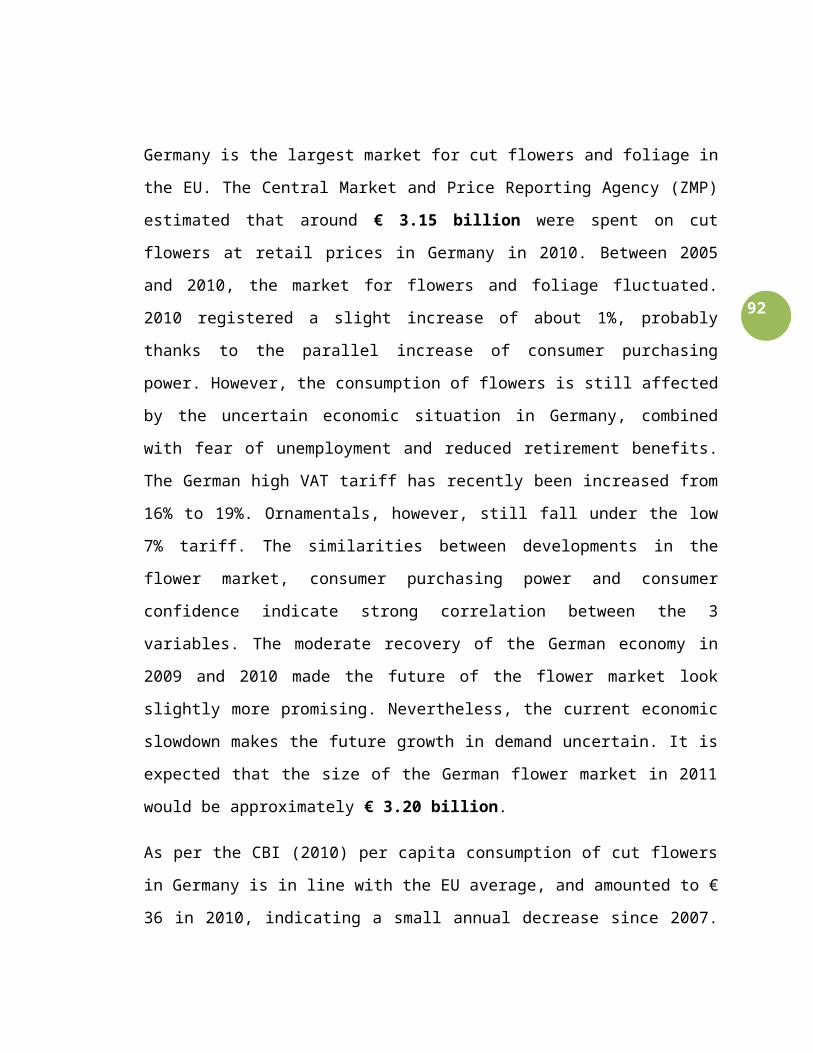

the largest market for cut flowers and foliage in the EU.

2.1 Geographical Setting

Germany is in Western and

Central Europe, bordering

Denmark in the north, Poland

and the Czech Republic in the

east, Austria and Switzerland in

the south, France and

Luxembourg in the south-west,

and Belgium and the

Netherlands in the north-west.

It lies mostly between latitudes

47° and 55° N (the tip of Sylt is

just north of 55°), and

longitudes 5° and 16° E. The

territory covers 357,021 km2

(137,847 sq mi), consisting of

349,223 km2 (134,836 sq mi) of

land and 7,798 km2 (3,011 sq

mi) of water. It is the seventh largest country by area in Europe and the 62 nd largest in the

world. (Source: CIA Factbook)

20

Elevation ranges from the mountains of the Alps in the south to the shores of the North

Sea in the north-west and the Baltic Sea in the north-east. Major rivers such as the Rhine,

Danube and Elbe cut across the German landscape.

Natural resources

Source: CIA Factbook

Climate

Most of Germany has a temperate seasonal climate in which humid westerly winds

predominate. Rainfall occurs year-round, especially in the summer. Winters are mild and

summers tend to be cool, though temperatures can exceed 30 °C. The east has a more

continental climate; winters can be very cold and summers very warm with frequent long

21

dry periods. Central and Southern Germany are transition regions which vary from

moderately oceanic to continental. (Source: German Culture)

2.2 Relevant History

The website “Facts About Germany” provides the following historic milestones of

Germany.

800: Charlemagne

The ruler of the Frankish Empire is crowned Roman emperor by Pope Leo III. Later the

Carolingian, who dies 814 in Aachen, is declared the “Father of Europe”.

962: Otto I or Otto the Great

His crowning as emperor marks the start of the “Holy Roman Empire”.

1024–1125/1138–1268: Salier and Staufer

The dynasties of the Salier (builders of Speyer Cathedral, photo) and Staufer families

shape the destiny of Europe.

1179: Hildegard von Bingen

The abbess and healer, one of the most influential women in medieval Germany, dies

aged 81 in Bingen on Rhine.

1452–1454: Invention of printing

Johannes Gutenberg (c. 1400–1468), inventor of printing with movable type, produces

the first printed Bible in Mainz – roughly 180 copies.

22

1493: Rise of the House of Habsburg

The regency of Maximilian I marks the rise of the House of Habsburg. For centuries it

was one of the dominant aristocratic dynasties in Central Europe, supplied the majority of

emperors and kings of the Holy Roman Empire of the German Nation, and from 1504–

1700 the kings of Spain

1517: Religious schism

The Age of the Reformation begins when Martin Luther (1483–1546) publicly declares

his 95 Theses against the system of indulgences in the Catholic Church in Wittenberg.

1618–1648: Thirty Years’ War

Both a religious war and political conflict, the Thirty Years’ War ends with the Peace of

Westphalia: The Catholic, Lutheran and Reformist faiths are recognized as equal.

1740–1786: Frederick the Great

During the reign of Frederick II, literary scholar and general, Prussia emerges as a

European superpower. His rule is seen as exemplary for the age of “enlightened

absolutism”.

1803: Secularization

The secularization of ecclesiastical rule and the dissolution of Imperial free cities by the

Final Recess herald the end of the “Holy Roman Empire of the German Nation”.

1848/49: March Revolution

The “German Revolution” begins in the Grand Duchy of Baden. Before long it spreads to

the other states of the German Federation and leads to the first German National

Assembly, which convened in the Paulskirche, Frankfurt/Main.

23

1871: Foundation of the Reich

On January 18 during the Franco-Prussian War Wilhelm I is proclaimed German

Emperor in Versailles. The (second) German Reich is a constitutional monarchy. Shortly

before the foundation of the empire the nation experienced an economic upswing known

as the “Gründerjahre”.

1914–1918: World War I

Emperor Wilhelm II isolates Germany from its neighbors and leads the country into the

catastrophe of the First World War, which costs the lives of almost 15 Mn people. In June

1919 the Treaty of Versailles is signed, ending the war.

1918/19: Weimar Republic

On November 9, 1918 Social Democrat Philipp Scheidemann proclaims the Republic;

Emperor Wilhelm II abdicates. On January 19, 1919 elections are held for the National

Assembly.

1933: National Socialism

The NSDAP gains the most votes in the Reichstag elections in 1932; on January 30 1933

Adolf Hitler becomes Chancellor of the Reich. The National Socialist dictatorship begins

with the “Enabling Act”.

1939: Start of the Second World War

Through his invasion of Poland on September 1, 1939 Hitler unleashes the Second World

War, which cost 60 Mn people their lives and devastated large parts of Europe and East

Asia. The Nazi extermination policy results in the murder of six Mn Jews.

24

1945: The Second World War ends

The capitulation of the German Wehrmacht between May 7th and 9th, 1945 ends the

Second World War in Europe. The four Allies divide the country into four occupation

zones and Berlin into four sectors.

1948: Blockade of Berlin

The introduction of the deutschmark in the Western occupation zones prompts the Soviet

Union on June 14, 1948 to cut off access to West-Berlin. The Allies respond with an

airlift dropping supplies to the population in West Berlin until September 1949.

1949: Birth of the Federal Republic of Germany

On May 23, 1949 the Basic Law of the Federal Republic of Germany is proclaimed in

Bonn. The first parliamentary elections are held on August 14. Konrad Adenauer (CDU)

is elected Chancellor. On October 7, 1949 the division between East and West is

completed when the Constitution of the German Democratic Republic comes into force.

1957: Treaties of Rome

The Federal Republic of Germany is one of the six nations to sign the founding treaties of

the European Economic Community.

1961: Building of the Berlin Wall

East Germany cuts itself off on August 13, 1961 by erecting a wall through the middle of

Berlin and the “Death Strip” along the border between the two Germanies.

1963: Elysée Treaty

The Treaty of Friendship between France and Germany is signed by West German

Chancellor Konrad Adenauer and the French President Charles de Gaulle.

25

1970: Brandt kneels in Warsaw

The gesture by West German Chancellor Willy Brandt (SPD) before the memorial for the

victims of the uprising in the Jewish ghetto in Warsaw became a symbol of the German

plea for reconciliation.

1989: The Fall of the Wall

The peaceful revolution in East Germany leads in November 9 to the Berlin Wall coming

down and with it the border between East and West Germany.

1990: German reunification

On October 3, East Germany formally ceases to exist. Germany’s political unity is

restored. The first general elections of the united Germany are held on December 2, 1990.

Helmut Kohl (CDU) becomes the unified nation’s first Chancellor.

2004/2007: EU Expansion

Following the disintegration of the Soviet Union and the fall of Communism, in 2004

eight Central and East European nations plus Cyprus and Malta joined the EU, followed

in 2007 by Bulgaria and Romania.

2005: First Female Chancellor

Angela Merkel became the first female Chancellor of Germany as the leader of a grand

coalition.

2.3 Social Institutions

The CIA Factbook on Germany provides the following information regarding the social

institutions in Germany.

26

Government

Government type: Federal republic

Constitution

23 May 1949, known as Basic Law; became constitution of the united Germany 3

October 1990

Legal system

Civil law system and accepts compulsory ICJ (International Court of Justice) jurisdiction

with reservations; accepts ICCt (International Criminal Court) jurisdiction.

Executive branch

Chief of state: President Christian Wulff (since 30 June 2010)

Head of government: Chancellor Angela Merkel (since 22 November 2005)

Cabinet: Cabinet or Bundesminister (Federal Ministers) appointed by the president on the

recommendation of the chancellor

Legislative branch

Bicameral legislature comprise of 02 groups.

Federal Council or Bundesrat – 69 votes; state governments sit in the Council; each

has three to six votes in proportion to population and is required to vote as a block.

Federal Diet or Bundestag – 622 seats; members elected by popular vote for a four-

year term under a system of personalized proportional representation.

Judicial branch

Federal Constitutional Court or Bundesverfassungsgericht (half the judges are elected

by the Bundestag and half by the Bundesrat)

27

Federal Court of Justice

Federal Administrative Court

Political parties and leaders

Alliance '90/Greens [Claudia Roth and Cem Ozdemir]

Christian Democratic Union or CDU [Angela Merkel]

Christian Social Union or CSU [Horst Seehofer]

Free Democratic Party or FDP [Guido Westerwelle]

Left Party or Die Linke [Klaus Ernst And Gesine Loetzsch]

Social Democratic Party or SPD [Sigmar Gabriel]

Political pressure groups and leaders

Business associations and employers' organizations; trade unions; religious, immigrant,

expellee, and veterans groups

International organization participation

ADB (nonregional member), AfDB (nonregional member), Arctic Council (observer),

Australia Group, BIS, BSEC (observer), CBSS, CDB, CE, CERN, EAPC, EBRD, EIB,

EMU, ESA, EU, FAO, FATF, G-20, G-5, G-7, G-8, G-10, IADB, IAEA, IBRD, ICAO,

ICC, ICRM, IDA, IEA, IFAD, IFC, IFRCS, IHO, ILO, IMF, IMO, IMSO, Interpol, IOC,

IOM, IPU, ISO, ITSO, ITU, ITUC, MIGA, NATO, NEA, NSG, OAS (observer), OECD,

OPCW, OSCE, Paris Club, PCA, Schengen Convention, SECI (observer), SICA

(observer), UN, UN Security Council (temporary), UNAMID, UNCTAD, UNESCO,

UNHCR, UNIDO, UNIFIL, UNMIL, UNMIS, UNRWA, UNWTO, UPU, WCO, WHO,

WIPO, WMO, WTO, ZC

28

Religious organizations

Protestant Evangelical Church (EKD)

Roman Catholic Church

2.4 Cultural Aspects

German Etiquette and Customs

As cited in kwintessential.com some common etiquette and customs include;

Meeting Etiquette

Greetings are formal.

A quick, firm handshake is the traditional greeting.

Titles are very important and denote respect.

In general, wait for your host or hostess to introduce you to a group.

When entering a room, shake hands with everyone individually, including children.

Gift Giving Etiquette

If you are invited to a German's house, bring a gift such as chocolates or flowers.

Yellow roses or tea roses are always well received.

Do not give red roses as they symbolize romantic intentions.

Do not give carnations as they symbolize mourning.

Do not give lilies or chrysanthemums as they are used at funerals.

If you bring wine, it should be imported, French or Italian. Giving German wines is

viewed as meaning you do not think the host will serve a good quality wine.

Gifts are usually opened when received.

29

Good manners

www.ediplomat.com provides useful information on mannerisms considered as

appropriate by Germans.

A man or younger person should always walk to the left side of a lady.

Traditional good manners call for the man to walk in front of a woman when walking

into a public place.

A man should open the door for a woman and allow her to walk into the building.

Don't be offended if someone corrects your behavior (i.e., taking jacket off in

restaurant, parking in wrong spot, etc.). Policing each other is seen as a social duty.

Compliment carefully and sparingly -- it may embarrass rather than please.

Don’t lose your temper publicly. This is viewed as uncouth and a sign of weakness.

Stand when an elder or higher ranked person enters the room.

Values

German people value honesty, hard work, and order.

They connect more easily with people who they consider to be skilled, prompt, and

intelligent.

At the same time, they tend shy away from strange or foreign ideas.

Germans are more formal and punctual than most of the world. They have prescribed

roles and seldom step out of line.

Time

Punctuality is highly valued. Being on time for meetings, appointments, and services

is expected.

Buses and trains are almost always on time, being even two minutes late is rare.

If invited to a big informal party, being fashionably late is fine provided it is not more

than 15 minutes late.

30

Festivals in the Germany

Germany is a country full of traditions and festivals throughout the year.

Month Festival

January Three Hallowed Kings

February Carnival

March Berlin’s Spandau Spring Festival, Strong Beer weeks

April FilmFest, International Dance week and Easter

May Munich Spring festival, the Bodensee Festival, the Dresden Music

Festival and the Asparagus Festival

June Rock am Ring and Rock am Park and the festival of classical music,

Sailing

July Rheinkultur Bonn, Schlagermove pop music festival, Zeltfestival and Das

fest

August August is popular for beer festivals like Berlin Beer Festival, wine

festivals and theatre festivals

Septembe

r

Beethoven Festival, Alstadt Autumn Festival, Berlin Musicfest, Potsdam

Jazz Festival, Oktoberfest

October Oktoberfest

November Christmas

December Christmas and New Year

Don'ts in Germany

It is impolite to cross your arm over people who are shaking hands, as well as chew

gum in public.

Talking while your hands are in your pockets is also impolite.

Don’t shout or be loud and avoid putting your feet on furniture.

31

When talking to someone, do not chew gum as it is considered as bad manners in

Germany.

When eating, do not put your elbows on the table. Only your hands should be on the

table.

If you are visiting a bar, then make sure you do not get drunk.

Business Customs and Etiquette in Germany

As cited in kwintessential.com some common business etiquettes to be followed include;

Relationships & Communications

Germans do not need a personal relationship in order to do business.

They will be interested in your academic credentials and the amount of time your

company has been in business.

Germans display great deference to people in authority, so it is imperative that they

understand your level relative to their own.

Germans do not have an open-door policy. People often work with their office door

closed. Knock and wait to be invited in before entering.

German communication is formal.

Following the established protocol is critical to building and maintaining business

relationships.

As a group, Germans are suspicious of hyperbole, promises that sound too good to be

true, or displays of emotion.

Germans will be direct to the point of bluntness.

Expect a great deal of written communication, both to back up decisions and to

maintain a record of decisions and discussions.

32

Business Meeting Etiquette

Appointments are mandatory and should be made 1 to 2 weeks in advance.

Letters should be addressed to the top person in the functional area, including the

person's name as well as their proper business title.

If you write to schedule an appointment, the letter should be written in German.

Punctuality is taken extremely seriously. If you expect to be delayed, telephone

immediately and offer an explanation. It is extremely rude to cancel a meeting at the

last minute and it could jeopardize your business relationship.

Meetings are generally formal.

Initial meetings are used to get to know each other. They allow your German

colleagues to determine if you are trustworthy.

Meetings adhere to strict agendas, including starting and ending times.

Maintain direct eye contact while speaking.

Although English may be spoken, it is a good idea to hire an interpreter so as to avoid

any misunderstandings.

At the end of a meeting, some Germans signal their approval by rapping their

knuckles on the tabletop.

There is a strict protocol to follow when entering a room:

o The eldest or highest ranking person enters the room first.

o Men enter before women, if their age and status are roughly equivalent.

Business Negotiation

Do not sit until invited and told where to sit. There is a rigid protocol to be followed.

Meetings adhere to strict agendas, including starting and ending times.

Treat the process with the formality that it deserves.

Germany is heavily regulated and extremely bureaucratic.

33

Germans prefer to get down to business and only engage in the briefest of small talk.

They will be interested in your credentials.

Make sure your printed material is available in both English and German.

Contracts are strictly followed.

You must be patient and not appear ruffled by the strict adherence to protocol.

Germans are detail-oriented and want to understand every innuendo before coming to

an agreement.

Business is hierarchical. Decision-making is held at the top of the company.

Final decisions are translated into rigorous, comprehensive action steps that you can

expect will be carried out to the letter.

Avoid confrontational behaviour or high-pressure tactics. It can be counterproductive.

Once a decision is made, it will not be changed.

Dress Etiquette

Business dress is understated, formal and conservative.

Men should wear dark coloured, conservative business suits.

Women should wear either business suits or conservative dresses.

Do not wear ostentatious jewellery or accessories.

Behavior

Germans are strongly individualistic.

Germans do not like surprises. Sudden changes in business transactions, even if they

may improve the outcome, are unwelcome.

German citizens do not need or expect to be complimented. In Germany, it is

assumed that everything is satisfactory unless the person hears otherwise.

When being introduced to a woman, wait to see if she extends her hand.

34

Business is viewed as being very serious, and Germans do not appreciate humor in a

business context.

People that have worked together for years still shake hands each morning as if it

were the first time they met.

Titles are very important to Germans. German men frequently great each other with

Herr 'last name', even when they know each other very well.

Germans love to talk on the telephone. While important business decisions are not

made over the phone, expect many follow up calls or faxes.

Germans guard their private life, so do not phone a German executive at home

without permission.

In business situations, shake hands at both the beginning and the end of a meeting.

Gestures

When gesturing or beckoning for someone to come, you should face your palm

downwards and make a scratching motion with the fingers.

Waving the hand back and forth with the palm up usually signifies “no”.

The OK sign and thumbs up are understood, but do not tend to be used that often.

At the end of a presentation or performance, Germans often signal their approval or

thanks by gently rapping their knuckles on the tabletop instead of applauding.

Taboos

Making a circular motion using the index finger while pointing to the side of one’s

head is a rude gesture indicating that someone is crazy or deranged.

Forming a circle with the thumb and index finger (meaning "OK" in North America)

is usually considered an obscene gesture.

An erect middle finger is a very offensive gesture with the meaning of "go screw

yourself".

35

Whistling at a performance is usually an expression of contempt or displeasure.

Putting your thumb between your middle and index finger while making a fist is

usually considered an obscene gesture.

“Facts About Germany” provides the following information about literature and culture.

Literature

German writers, composers and philosophers such as Goethe, Schiller, Bach, Beethoven,

Kant and Hegel have strongly influenced cultural epochs and are acclaimed figures the

world over.

Cultural institutions

Berlin, as the capital city, is a spectacular case in point, with three opera houses, 120

museums, more than 50 theaters and a lively art community that also attracts many young

foreign artists.

Cultural facilities

6,200 museums (630 of them art museums), 820 theaters (including musical theaters and

opera houses), 130 professional orchestras, 8,800 libraries.

UNESCO World Heritage

Germany features 33 natural and cultural heritage sites protected under the UNESCO

World Heritage program.

36

2.5 Living conditions

HIV

Indicator As at 2009 World ranking

Adult prevalence rate 0.1% 132

People living with HIV/AIDS 67,000 51

Deaths fewer than 1,000 73

Drinking water source:

100% of urban and rural population

Infant mortality rateMale: 3.84 deaths/1,000 live birthsFemale: 3.21 deaths/1,000 live births (2011 est.)Total: 3.54 deaths/1,000 live birthsWorld ranking: 209

Life expectancy at birthMale: 77.82 yearsFemale: 82.44 years Total: 80.07 yearsWorld ranking: 27

Total fertility rate 1.41 children born/woman World ranking: 198

37

Sanitation facility access:

100% of urban and rural population

2.6 Languages and Religions

The CIA Factbook reveals the following facts.

Religions:

Protestant 34%, Roman Catholic 34%, Muslim 3.7%, unaffiliated or other 28.3%

Languages:

German

LiteracyMale: 99%Female: 99%Total population: 99%

School life expectancy Male: 16 yearsFemale: 16 yearsTotal: 16 years

Education expenditures4.5% of GDP World ranking: 82

38

2.7 General facts

Capital: Berlin

Administrative divisions: 16 states

Independence:

Federal Republic of Germany (FRG or West Germany) proclaimed on 23 May 1949

German Democratic Republic (GDR or East Germany) proclaimed on 7 October 1949

West Germany and East Germany unified on 3 October 1990

National holiday: Unity Day, 3 October (1990)

National anthem: "Lied der Deutschen" (Song of the Germans)

Flag description:

three equal horizontal bands of black (top), red, and gold; these colors have played an

important role in German history and can be traced back to the medieval banner of the

Holy Roman Emperor - a black eagle with red claws and beak on a gold field

National holidays:

39

3. Economic Analysis

3.1 Population

The population facts based on the CIA Factbook are as follows.

Indicator As at July 2011 (est.) World Ranking

Population 81,471,834 16

Population growth rate -0.208% 212

Birth rate 8.3 births/1,000 population 219

Death rate 10.92 deaths/1,000 population 39

Net migration rate 0.54 migrant(s)/1,000 population 62

Age structure:

0-14 years: 13.3% (male 5,569,390/female 5,282,245)

15-64 years: 66.1% (male 27,227,487/female 26,617,915)

65 years and over: 20.6% (male 7,217,163/female 9,557,634) (2011 est.)

Median age:

total: 44.9 years

male: 43.7 years

female: 46 years (2011 est.)

Urbanization:

Urban population: 74% of total population (2010)

Rate of urbanization: 0% annual rate of change (2010-15 est.)

Major cities (in terms of population):

Berlin (capital) 3.438 Mn; Hamburg 1.786 Mn; Munich 1.349 Mn; Cologne 1.001 Mn

(2009)

40

Population (ranking in Europe):

Second most populous country in Europe after Russia

Sex ratio:

At birth: 1.055 male(s)/female

Under 15 years: 1.05 male(s)/female

15-64 years: 1.04 male(s)/female

65 years and over: 0.72 male(s)/female

Total population: 0.97 male(s)/female (2011 est.)

Ethnic groups:

German 91.5%, Turkish 2.4%, other 6.1% (made up largely of Greek, Italian, Polish,

Russian, Serbo-Croatian, Spanish)

3.2 Economic Statistics & Activity

The CIA Factbook provides the following overview of the German economy. It is the

fifth largest economy in the world in PPP terms and Europe's largest and is a leading

exporter of machinery, vehicles, chemicals, and household equipment and benefits from a

highly skilled labor force. Like its western European neighbors, Germany faces

significant demographic challenges to sustained long-term growth. Low fertility rates and

declining net immigration are increasing pressure on the country's social welfare system

and necessitate structural reforms. The modernization and integration of the eastern

German economy - where unemployment can exceed 20% in some municipalities -

continues to be a costly long-term process, with annual transfers from west to east

amounting in 2008 alone to roughly $12 Bn. Reforms launched by the government of

Chancellor Gerhard Schroeder (1998-2005), deemed necessary to address chronically

high unemployment and low average growth, contributed to strong growth in 2006 and

2007 and falling unemployment. These advances, as well as a government subsidized,

41

reduced working hour scheme, help explain the relatively modest increase in

unemployment during the 2008-09 recession - the deepest since World War II - and its

decrease to 7.4% in 2010. GDP contracted 4.7% in 2009 but grew by 3.6% in 2010. In its

annual projection for 2011, the Federal Government expects the upswing to continue,

with GDP forecast to grow this year at a real rate of 2.3%. The recovery was attributable

primarily to rebounding manufacturing orders and exports - increasingly outside the Euro

Zone. Domestic demand, however, is becoming more significant driver of Germany's

economic expansion. Stimulus and stabilization efforts initiated in 2008 and 2009 and tax

cuts introduced in Chancellor Angela Merkel's second term increased Germany's budget

deficit to 3.5% in 2010. The Bundesbank expects the deficit to drop to about 2.5% in

2011, below the EU's 3% limit. A constitutional amendment approved in 2009 likewise

limits the federal government to structural deficits of no more than 0.35% of GDP per

annum as of 2016.

Some key economic indicators are shown below (CIA Factbook).

GDP 2010 2009 2008World

Ranking

GDP (purchasing

power parity)$2.94 trillion

$2.841

trillion$2.98 trillion 6

GDP (official

exchange rate)$3.316 trillion

GDP - real

growth rate3.5% -4.7% 0.7% 111

GDP - per capita

(PPP)$35,700 $34,500 $36,200 33

GDP - composition by sector:

Agriculture: 0.8%, Industry: 27.9% and Services: 71.3% (2010 est.)

42

Employment 2010 2009 World Ranking

Labour force 43.35 Mn 14

Unemployment rate 7.4% 7.5% 78

Labor force - by occupation:

Agriculture: 2.4%, Industry: 29.7% and Services: 67.8% (2005)

Income

Population below poverty line:

15.5% (2010 est.)

Household income or consumption by percentage share:

Lowest 10%: 3.6%

Highest 10%: 24% (2000)

Distribution of family income - Gini index:

27 (2006)

30 (1994)

World ranking: 124

Investment (gross fixed):

18% of GDP (2010 est.)

World ranking: 112

43

Banking

Indicators2010 2009 2008 2007

World

Ranking

Central bank

discount rate1.75% 1.75% 129

Commercial

bank prime

lending rate

4.96% 5.97% 133

Stock of narrow

money

$1.627

trillion

$1.681

trillion6

Stock of broad

money

$4.288

trillion

$4.202

trillion6

Stock of

domestic credit

$5.2

trillion

$5.019

trillion5

Market value of

publicly traded

shares

$1.298

trillion

$1.108

trillion

$2.106

trillion9

Budget:

Revenues: $1.396 trillion

Expenditures: $1.516 trillion (2010 est.)

44

Public debt:

78.8% of GDP (2010 est.)

72.5% of GDP (2009 est.)

World ranking: 20

Inflation rate (consumer prices):

1.1% (2010 est.)

0.4% (2009 est.)

World ranking: 24

Agriculture products:

Potatoes, Wheat, Barley, Sugar beets, Fruit, Cabbages; Cattle, Pigs, Poultry

Industries:

Among the world's largest and most technologically advanced producers of iron, steel,

coal, cement, chemicals, machinery, vehicles, machine tools, electronics, food and

beverages, shipbuilding, textiles

Industrial production growth rate:

9% (2010 est.)

World ranking: 24

45

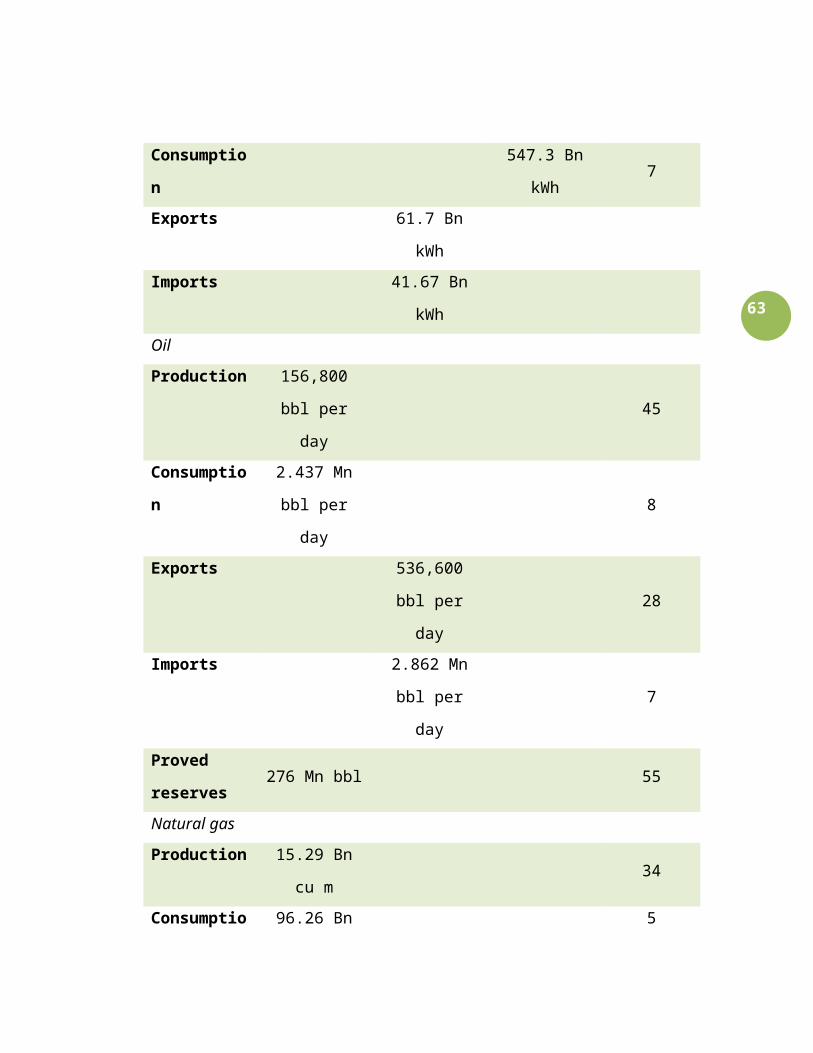

Energy Facts 2009 2008 2007World

Ranking

Electricity

Production 593.4 Bn kWh 8

Consumption 547.3 Bn kWh 7

Exports 61.7 Bn kWh

Imports 41.67 Bn kWh

Oil

Production 156,800 bbl per

day45

Consumption 2.437 Mn bbl

per day8

Exports 536,600 bbl per

day28

Imports 2.862 Mn bbl

per day7

Proved

reserves276 Mn bbl 55

Natural gas

Production 15.29 Bn cu m 34

Consumption 96.26 Bn cu m 5

Exports 12.64 Bn cu m 16

Imports 94.57 Bn cu m 2

Proved

reserves175.6 Bn cu m 47

Reserves of foreign exchange and gold:

$180.8 Bn (31 December 2009 est.)

46

External balance 2010 2009 World Ranking

Current account balance $162.3 Bn $168.1 Bn 3

Exports $1.337 trillion $1.145 trillion 3

Imports $1.12 trillion $956.7 Bn 4

External debt $4.713 trillion $5.158 trillion 4

Exports commodities:

Machinery, Vehicles, Chemicals, Metals And Manufactures, Foodstuffs, Textiles

Exports partners:

France 10.1%, US 6.7%, UK 6.6%, Netherlands 6.6%, Italy 6.3%, Austria 5.7%, Belgium

5.2%, China 4.7%, Switzerland 4.5% (2009)

Imports commodities:

Machinery, Vehicles, Chemicals, Foodstuffs, Textiles, Metals

Imports partners:

Netherlands 13%, France 8.2%, Belgium 7.2%, China 6.8%, Italy 5.6%, UK 4.7%,

Austria 4.4%, US 4.2%, Switzerland 4.1% (2009)

FDI 2010 2009 World Ranking

At home $1.057 trillion $1.054 trillion 4

Abroad $1.484 trillion $1.46 trillion 4

Exchange rates:

47

2006 2007 2008 2009 20100.62

0.64

0.66

0.68

0.7

0.72

0.74

0.76

0.78

0.8

0.82

Exchange rateEu

ros (

EUR)

per

US

dolla

r

3.3 Development in Science & Technology

Germany is not only the largest economy in Europe and the third largest in the world, but

it is also one of the world's most active and diversified markets for science and

technology research and development. Over half of Germany's industrial production is

accounted for by R&D-intensive industries.

Germany has also been the home of some of the most prominent researchers in various

scientific disciplines, notably physics, mathematics, chemistry and engineering. Scientific

research in the country is supported by industry, by the network of German universities

and by scientific state-institutions such as the Max Planck Society and the Deutsche

Forschungsgemeinschaft.

Germany's technological performance is essential for German companies' success in

international technological competition. It is the basis for economic growth and viable

jobs in Germany. Technological performance is documented by new, innovative products

and processes which can compete on international markets. They depend on the creativity

of German entrepreneurs and on the commercialization of the results of efficient public

48

research. But above all, Germany's technological performance will in future depend on

the availability of highly qualified workers. Education and research are therefore a top

priority for the Federal Government. (Source: BMBF, i.e. the Federal Ministry of

Education and Research in Germany).

The key findings by the BMBF on Germany's technological performance are as follows.

Germany ranks high in comparison to other countries when it comes to research and

knowledge intensities in industry. It produces 277 patents with global market

potential per million employed persons whereas the EU and OECD average is 182

and 152 respectively.

The share of companies that launched new products or new processes stand at 59

percent.

Sectors with technological strength are reporting increasingly higher levels of export

trade. German enterprises account for 15.6 percent of global trade in research-

intensive goods, ranking second only to the USA. For years now, German exports of

research-intensive goods have grown an average of more than eight percent a year.

The ability of German companies to compete in international markets has improved

noticeably since the mid-1990s.

Production and employment in those industries that invest strongly in R&D has

grown vigorously. Gross output in these industries grew an average of 4.4 percent a

year (other industries: 1.5 percent) between 1995 and 2003. Germany's specialization

profile has shifted slightly in favor of cutting-edge technologies.

Combined public and private expenditure on R&D as a percentage of Germany's

gross domestic product grew from 2.31 percent to 2.55 percent between 1998 and

2003. Research intensity is high in Germany. Research budgets of universities and

non-university research facilities grew 3.1 percent a year in real terms in the first

years of this decade.

49

Challenges

Emerging threshold countries are expanding their investment in research and

development at an extraordinarily fast pace. This group increased its nominal

expenditure on R&D by 180 percent during the period from 1995-2003. China alone

quadrupled its R&D spending since the mid-1990s. Spending US$ 72 billion on R&D

during this period, it catapulted itself to third place on the list of the world's most

R&D-rich countries. By comparison, spending on R&D rose by 80 percent in the

Nordic countries, by 50 percent in the USA and on average for OECD countries and

by 35 percent in Germany.

Germany's technological strengths revolve increasingly around the automotive sector.

The "knowledge society" needs much more skilled workers with engineering or

scientific education than ever before. It is estimated that the German workforce needs

approximately 50.000 additional academically trained workers annually.

The Federal Government has taken numerous measures to sustain and to strengthen

Germany's technological performance.

Investments in education, research, and innovation remain a high funding priority.

The German government demands excellent research in Germany. It has proposed a

competition for the development of elite universities. The Excellence Initiative is to

be used to expand cutting-edge research at universities and scientific institutions and

make it internationally visible.

The German government is boosting the ability of small and medium-sized

enterprises to produce innovations.

50

The government is responding to the growing need for skilled workers and the

international competition for highly qualified workers with a number of measures

aimed at strengthening Germany's education system and universities such as the

reform of the Federal Training Assistance Act giving financial aid to students.

The government has launched the Partners for Innovation initiative to boost

momentum at all levels of the German innovation system. This initiative is jointly

sponsored by leading representatives from industry, trade unions and the science

community.

3.4 Channels of Distribution

With more than 82 million people, the German market is the largest and most important

in Europe. It is both very competitive and segmented, with supply-side saturation in

many sectors and for many products. Quality and service are of the utmost importance in

this market. The main trading areas of the country North Rhine-Westphalia, Baden

Wurtenberg, Bavaria, Hamburg, Berlin and Hanover, as well as Leipzig in the former

East Germany.

A brief overview of the distribution network in Germany as cited in www.alibaba.com is

as follows.

The Business to Consumer (B to C) market

The structure of German distribution is characterized by:

large number of small independent shops

low level of concentration in each sector, compared to the main European markets

(France, United Kingdom, Belgium)

predominance of distribution in city centers and urban areas

low number of hypermarkets

51

predominance of discount stores and the importance of distance selling (mail order, e-

commerce, teleshopping)

German distribution is divided up according to the following distribution channels:

Distribution channel (%)

Traditional retail trade 24.8

Specialized superstores 22

Non-food shop chains 13

DIY superstores 11.7

Discounters 11

Supermarkets 7.9

Mail Order 5.8

Department stores 3.8

The top three German distribution groups are Metro, Rewe and Edeka/Ava. Discount

stores are the leading format for food distribution, registering a growth of approximately

10% and generating 40% of total food sales. The growth in the number of discounters,

such as Lidl and Aldihas forced distributors to wage a price war. Thus, insufficient

margins risk slowing down the modernization of sales outlets and the development of

new distribution concepts. The relationships between the distributors and their suppliers,

reputed to be very difficult, have become even more strained. A trend toward

52

consolidation has developed, and groups such as Karstadt-Quelle, Edeka-Tengelmann

and discounters such as Wal-Mart have engaged in severe competition, resulting in a

lowering of suppliers' margins.

Classification of the top ten German distributors in 2003

CompaniesTurnover (Million €,

2003)

1. Metro Gruppe 32,232

2. Rewe Gruppe 30,373

3. Edeka/AVA-Gruppe 29,090

4. Aldi-Gruppe 24,000

5. Schwarz-Gruppe 21,500

6. Karstadt Quelle 15,500

7. Tengelmann-Gruppe 13,108

8. Spar AG 9,000

9. Lekkerland-Tobaccoland 8,230

10. Schlecker 5,600

The Business to Business (B to B) market

53

To sell in Germany, it is vital to be represented on a regional level, either by independent

regional agents, or by a national organization with regional support. Regional division

usually corresponds with the Länder (states of Germany).

Germany is the world's leading country for the organization of trade exhibitions and fairs.

These events are vital for a company to make a name for itself, find out who its

competition is, find new customers, and develop loyalty among longer-standing ones.

One benchmark exhibition is EUROSHOP, the premier worldwide retail distribution

exhibition, with almost 1,500 exhibitors. The cities which stage international trade fairs

are Cologne, Düsseldorf, Frankfurt, Hanover, Munich, Nuremberg, Berlin, Leipzig,

Stuttgart, Hamburg and Essen.

In addition, regional exhibitions are held all over Germany, generally smaller and which

are organized by either distributors or agents.

Transportation of goods

By road

The German road network covers more than 238,000 km of roads of which more than

11,000 km are toll free highways.

By rail

The railroad network extends over 44.500 km of lines and is capable of transporting over

290 million tons of goods.

By sea

The main German ports are Hamburg, Rostock, Bremen and Duisburg.

By air

54

The airport of Frankfurt ensures 70% of the air freight and is ranked 9 th in the world. The

other main international airports are Munich, Stuttgart and Dusseldorf.

3.5 Media

The media landscape in Germany was outlined by the European Journalism Centre

(2010) as follows.

Germany looks back at a long history of mass media. Some of the first newspapers

started roughly 400 years ago. Today, the major media production centers are located in

the “old” West. Newspapers of the former East Germany are usually controlled by

Western companies and broadcasting is integrated into the Western dual system.

Traditional Media

Germany has a "dual system" of both public and commercial broadcasting. The

traditional public service broadcaster is set up as an independent and non-commercial

organization, financed primarily by license fees. Because of the de-centralized character,

there are many media centers in the country, e.g. Hamburg (NDR), Cologne (WDR),

Munich (BR), Berlin-Potsdam (rbb).

Print Media

Independent editorial units 135

Number of newspapers 354

Penetration (1990-2008) 79.1% to 72.4%

Types of newspaper subscription press and tabloid press

Total circulation 20.2 Mn

55

- National 1.65 Mn

BILD, Süddeutsche Zeitung (SZ), Frankfurter Allgemeine Zeitung (FAZ), Welt,

Frankfurter Rundschau (FR), Tageszeitung (Taz)

- Sold on the street 4.47 Mn

- Regional 14.1 Mn

Subscription press 14.3 Mn

Tabloid Press 5.9 Mn (BILD Zeitung – 3.3 Mn – also best in Europe)

Weekly newspapers Die Zeit (ca. 525,000)

Newspaper Publishers

- Axel Springer Group 22.1%

- Verlagsgruppe Stuttgarter Zeitung 8.5%

- WAZ Group 6%

- DuMont Schauberg 4.2%

- Ippen Gruppe 4%

The 10 largest publishers of dailies together control 44.8% of the market.

Number of magazines

- General 906 (total circulation = 117.9 Mn)

- Specialized 1,218 (total circulation = 13.6 Mn)

Weekly news magazines Der Spiegel (ca. 1.07 Mn)

56

Magazine publishers Bauer, Springer, Burda, Gruner + Jahr (60% share)

Radio

Daily consumption 176 minutes

Regional programmes 06

National programmes 02

Slightly more than a half comes from public service broadcasters. Commercial radio is

licensed in all Länder-states; therefore it follows mostly a regional pattern. In North

Rhine-Westphalia, the largest state, 46 local stations work commercially but with local,

non-commercial windows. Non-commercial radio exists but is regulated differently in

each state. Some states allow community stations; others prefer public access (also for

television), educational stations, campus stations etc.

Television

Daily viewing time 219 minutes

Television receivers 46.5 Mn

Televisions 51.4 Mn

National channels Das Erste (ARD) and ZDF

Commercial television

Broadcasters ProSiebenSAT.1Media AG (21.6%)

RTL Group S.A. (24.1%)

Transmission

57

- Cable 18.66 Mn

- Satellite 14.93 Mn

- Terrestrial 1.4 Mn

Public service (43.6%)

Broadcasters ARD (13.4%)

ZDF (13.1%)

Third channels (13.2%)

RTL (11.7%)

SAT1 (10.3%)

ProSieben (6.6%)

Pay TV Sky (2.4 Mn viewers)

Cinema

Film with German origin 20%-27%

No of film theaters 1,793

No of screens 4,810

No of visits per year 1.58

Telecommunications

Private

58

Largest company Deutsche Telekom

Internet TV T-Home (IPTV subscribers = 700,000)

Advertising Medium

New Media

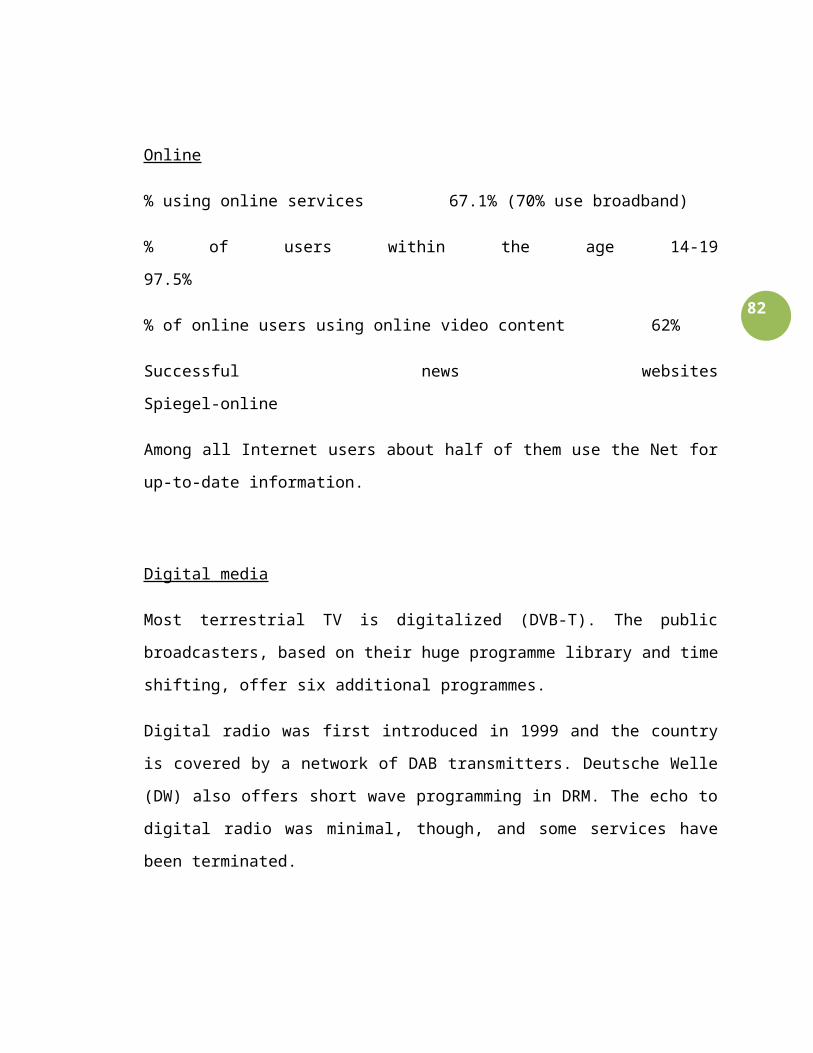

Online

% using online services 67.1% (70% use broadband)

% of users within the age 14-19 97.5%

% of online users using online video content 62%

Successful news websites Spiegel-online

Among all Internet users about half of them use the Net for up-to-date information.

59

Digital media

Most terrestrial TV is digitalized (DVB-T). The public broadcasters, based on their huge

programme library and time shifting, offer six additional programmes.

Digital radio was first introduced in 1999 and the country is covered by a network of

DAB transmitters. Deutsche Welle (DW) also offers short wave programming in DRM.

The echo to digital radio was minimal, though, and some services have been terminated.

Media organizations

News agencies

There are eight agencies with Deutsche Presseagentur (DPA), Associated Press (AP),

German Reuters and Agence France Presse (AFP) in the top 04.

Film production

- Bavaria Atelierbetriebsgesellschaft (Munich)

- Studio Hamburg (Hamburg)

- Studio Babelsberg (Berlin/Potsdam)

- Magic Media Company (Cologne)

Nearly 80 percent of production outlets, which are involved in new feature films,

produced only one film in total (Clevé, 1995).

Media research

60

Media research is hosted by a vast variety of institutions

University-based institutes

Media research divisions of both public and commercial broadcasters

Independent research institutes (GfK and Nielsen Media Research)

Some other media stats as cited in Nationmaster are as follows.

Average cost of local call ($ per 3

min)

0.09

Book production 3,718

Cable TV subscribers 247

Cinema attendance 148,996,000

Fax machines 45.55 per 1,000

people

Films produced 121

Households with television > % 95 %

Mobile phones 71.67 per 100 people

Number of PCs 40,000

Phone subscribers 1,316.52

61

4. Market Audit and Competitive Market Analysis

4.1 The Product

Cut flowers can be defined as flowers or flower buds (often with some stem and leaf)

that have been cut from the plant bearing it (The Flower Expert). It is usually removed

from the plant for indoor decorative use. Typical uses are in vase displays, wreaths and

garlands. Many gardeners harvest their own cut flowers from domestic gardens, but there

is a significant commercial market and supply industry for cut flowers in most countries.

The plants cropped vary by climate, culture and the level of wealth locally. Often the

plants are raised specifically for the purpose, in field or glasshouse growing conditions.

Cut flowers can also be harvested from the wild.

4.1.1 Evaluation of the product's USP

Table 1 overleaf shows a vis-à-vis comparison of the main cut-flower producing nations.

Competitors from Africa choose to focus on cost reduction to win from the competition,

whilst the growers in the Netherlands, Colombia and Ecuador focus on quality and

services. Due to the low volumes of Sri Lankan cut flower producers it is difficult to

achieve cost advantages, and since cut flowers are still an amateur market in Sri Lanka

we cannot compete with South American countries. As such it is necessary to look

beyond traditional criteria to develop the product’s USP.

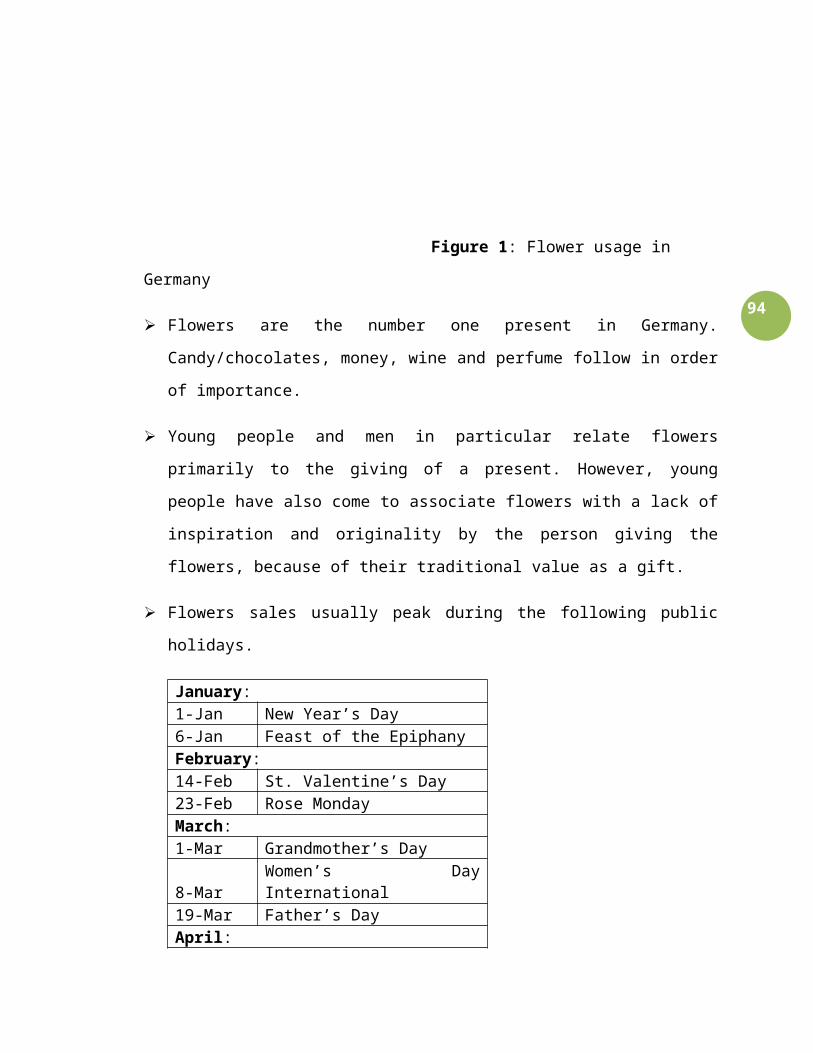

The USP of Shirohana flowers will be as follows.

Masculinity

Symbol of peace

Energy saving

62

Table 1: Main cut-flower producing nations

63

Reasons behind the choice of USP

Masculinity

A study on the German market (2008) found that there is considerable potential for

marketing flowers to men. The eHow website further states that surveys have shown

that men like to receive flowers nearly as much as women do. A survey conducted by

the Society of American Florists found that nearly 60% of men would enjoy receiving

flowers on Valentine's Day. However, not all of these men are willing to admit this

fact in public. Another study by Rutgers University researchers found that men who

received flowers were more open socially. Male flower recipients smiled more often,

stood closer to subjects, and maintained direct-eye contact more than men who did

not receive flowers. The study found that ethnicity, age or background did not matter.

There are many types of flowers that come in masculine flowers, such as orchids,