International Marketing Plan of Skoda

46

Volkswagen Skoda International Marketing Plan Henrie&a An&onen Kristyna Feldova Patricia Garber Mar8na Porubcova Nathalie Weber BAA 2-204-08 HIV2016 – Interna8onal Marke8ng – Group #1 Volkswagen 1

-

Upload

patricia-kimberley-garber -

Category

Business

-

view

157 -

download

5

Transcript of International Marketing Plan of Skoda

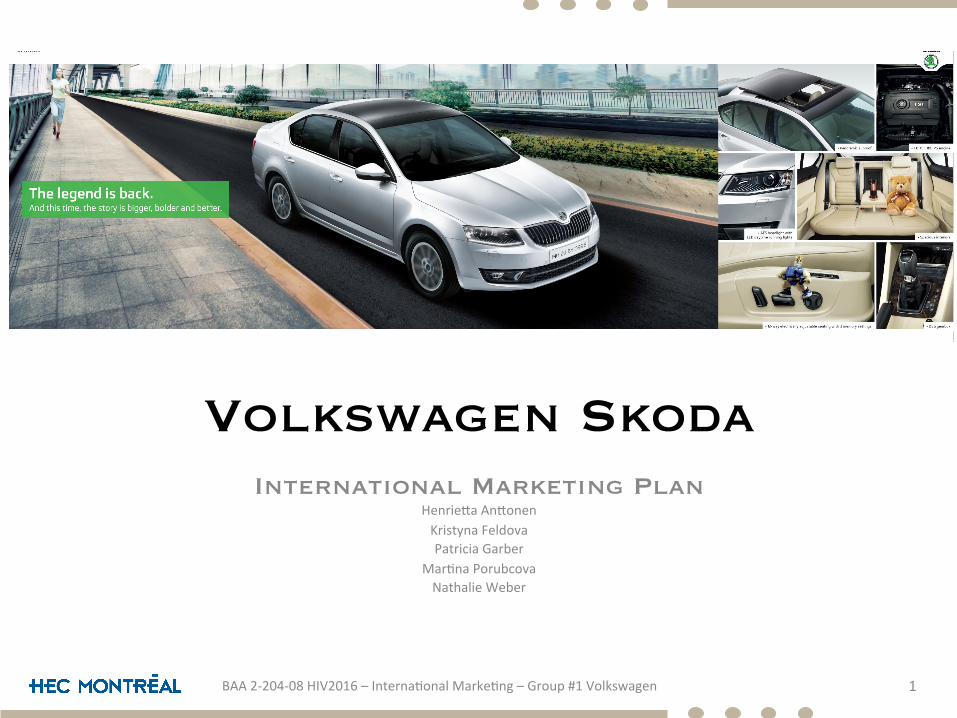

Volkswagen SkodaInternational Marketing Plan

Henrie&aAn&onenKristynaFeldovaPatriciaGarber

Mar8naPorubcovaNathalieWeber

BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen 1

1. PROFILEOFTHECOMPANY

2. SITUATIONANALYSIS3. OPTIONS4. IMPLEMENTATION

5. CONCLUSION6. REFERENCES7. APPENDICES

1. Introduction

Situation

3BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

1. Introduction

Existing Markets

4BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Skoda’smainmarkets:▷ WesternEurope▷ CentralEurope▷ China

Context

keysuccessfactorsexcellentpricevaluera8o

uniqueknowledge&skillpoolforemployees

valueformoney

8ming&speed

customiza8onofcars

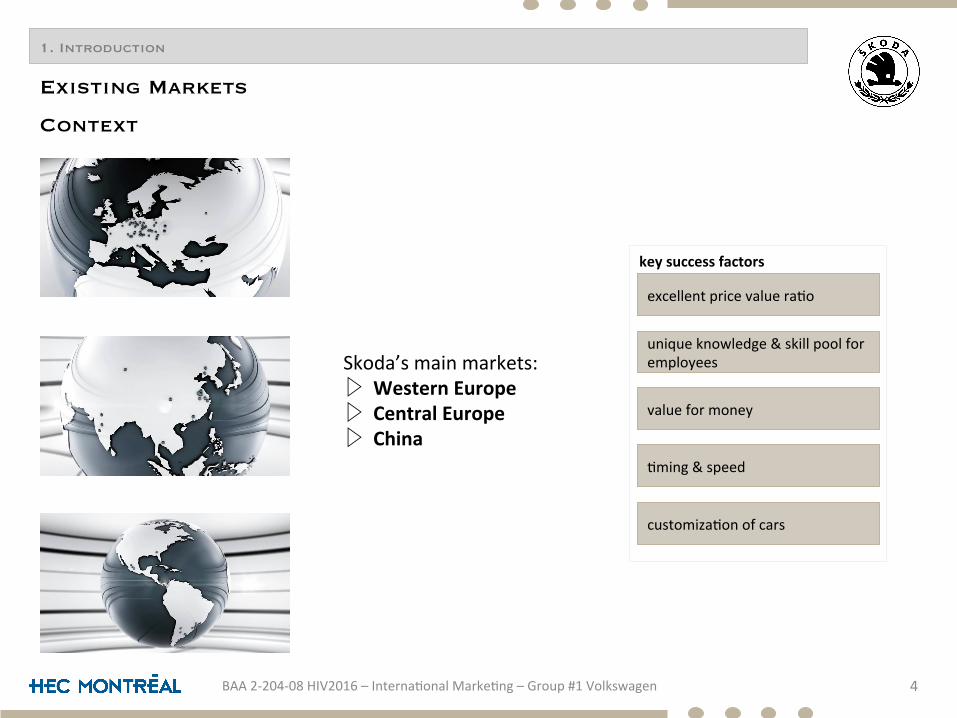

1. Introduction

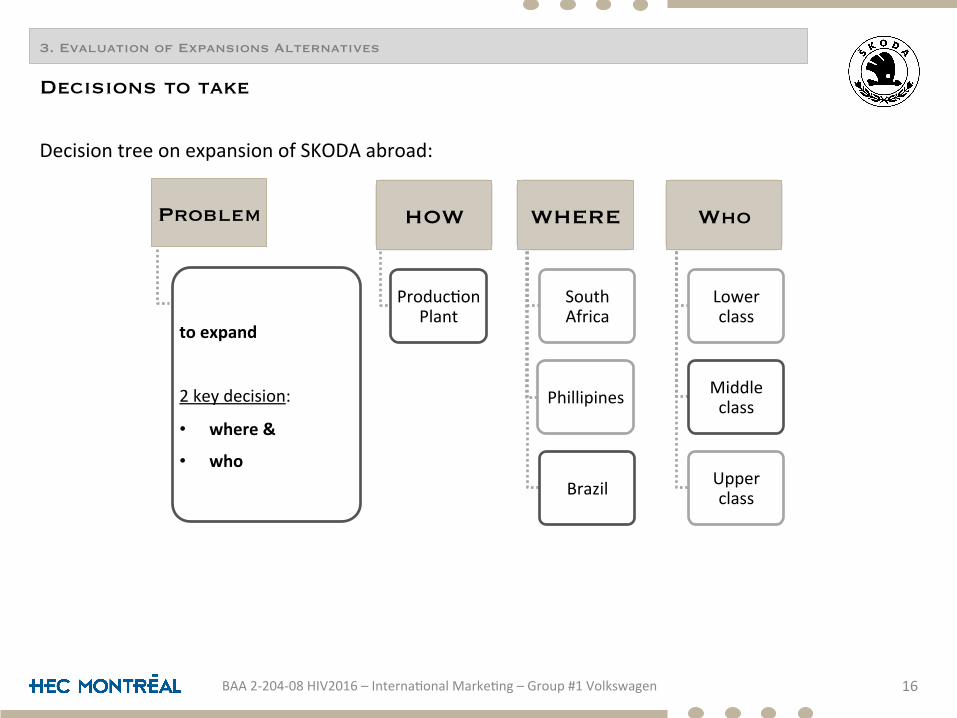

DecisiontreeonexpansionofSKODAabroad:

Decisions to take

5BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

HOW

Produc8onPlant

Philippines

WHERE

SouthAfrica

Brazil

Who

Lowerincome

Middleincome

Upperincome

Problem

toexpand

2keydecision:

• whatentrymode&

• where

1. PROFILEOFTHECOMPANY

2. SITUATIONANALYSIS3. OPTIONS4. IMPLEMENTATION

5. CONCLUSION6. REFERENCES7. APPENDICES

2. Situation Analysis

Target Markets

7BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

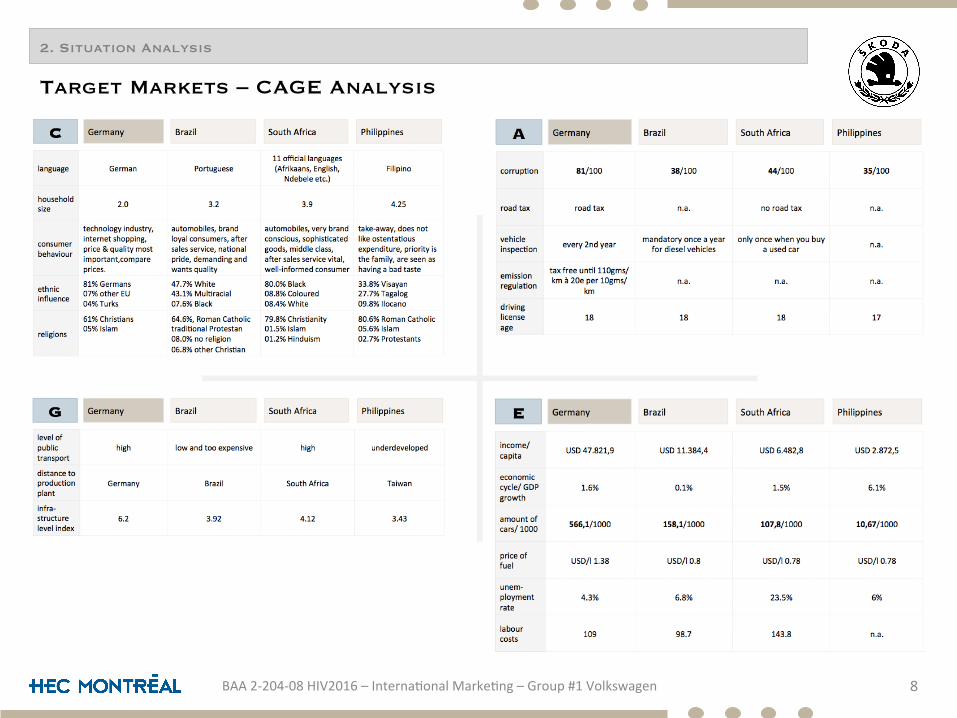

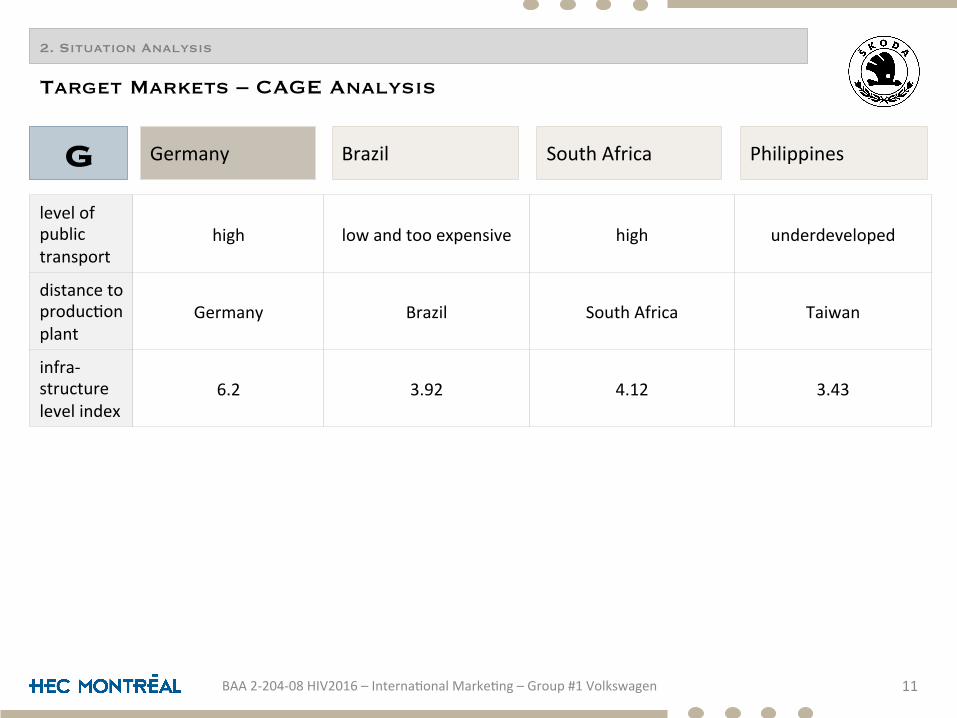

2. Situation Analysis

Target Markets – CAGE Analysis

8BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

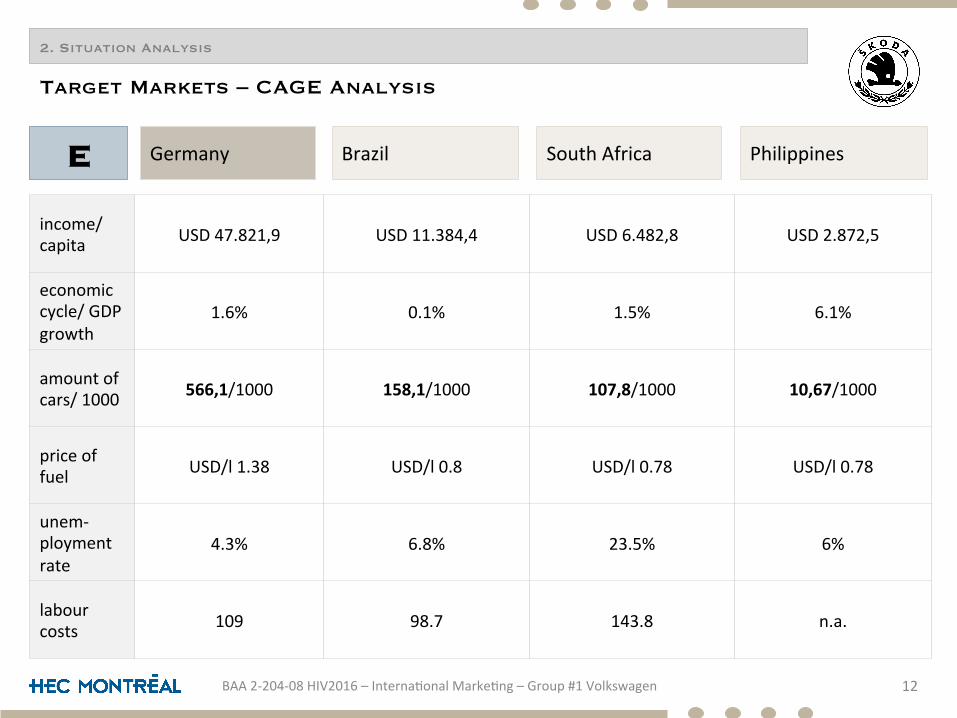

2. Situation Analysis

Target Markets – CAGE Analysis

9BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Brazil SouthAfrica Philippines

language German Portuguese11officiallanguages(Afrikaans,English,

Ndebeleetc.)Filipino

householdsize 2.0 3.2 3.9 4.25

consumerbehaviour

technologyindustry,internetshopping,price&qualitymostimportant,compareprices.

automobiles,brandloyalconsumers,ahersalesservice,na8onalpride,demandingandwantsquality

automobiles,verybrandconscious,sophis8catedgoods,middleclass,ahersalesservicevital,well-informedconsumer

take-away,doesnotlikeostenta8ousexpenditure,priorityisthefamily,areseenashavingabadtaste

ethnicinfluence

81%Germans07%otherEU04%Turks

47.7%White43.1%Mul8racial07.6%Black

80.0%Black08.8%Coloured08.4%White

33.8%Visayan27.7%Tagalog09.8%Ilocano

religions

61%Chris8ans05%Islam

64.6%,RomanCatholictradi8onalProtestan08.0%noreligion06.8%otherChris8an

79.8%Chris8anity01.5%Islam01.2%Hinduism

80.6%RomanCatholic05.6%Islam02.7%Protestants

GermanyC

2. Situation Analysis

Target Markets – CAGE Analysis

10BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Brazil SouthAfrica Philippines

corrup8on 81/100 38/100 44/100 35/100

roadtax roadtax n.a. noroadtax n.a.

vehicleinspec8on every2ndyear mandatoryonceayear

fordieselvehiclesonlyoncewhenyoubuy

ausedcar n.a.

emissionregula8on

taxfreeun8l110gms/kmà20eper10gms/

kmn.a. n.a. n.a.

drivinglicenseage

18 18 18 17

GermanyA

2. Situation Analysis

Target Markets – CAGE Analysis

11BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Brazil SouthAfrica Philippines

levelofpublictransport

high lowandtooexpensive high underdeveloped

distancetoproduc8onplant

Germany Brazil SouthAfrica Taiwan

infra-structurelevelindex

6.2 3.92 4.12 3.43

GermanyG

2. Situation Analysis

Target Markets – CAGE Analysis

12BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Brazil SouthAfrica Philippines

income/capita USD47.821,9 USD11.384,4 USD6.482,8 USD2.872,5

economiccycle/GDPgrowth

1.6% 0.1% 1.5% 6.1%

amountofcars/1000 566,1/1000 158,1/1000 107,8/1000 10,67/1000

priceoffuel USD/l1.38 USD/l0.8 USD/l0.78 USD/l0.78

unem-ploymentrate

4.3% 6.8% 23.5% 6%

labourcosts 109 98.7 143.8 n.a.

GermanyE

1. PROFILEOFTHECOMPANY

2. SITUATIONANALYSIS3. OPTIONS4. IMPLEMENTATION

5. CONCLUSION6. REFERENCES7. APPENDICES

3. Evaluation of Expansions Alternatives

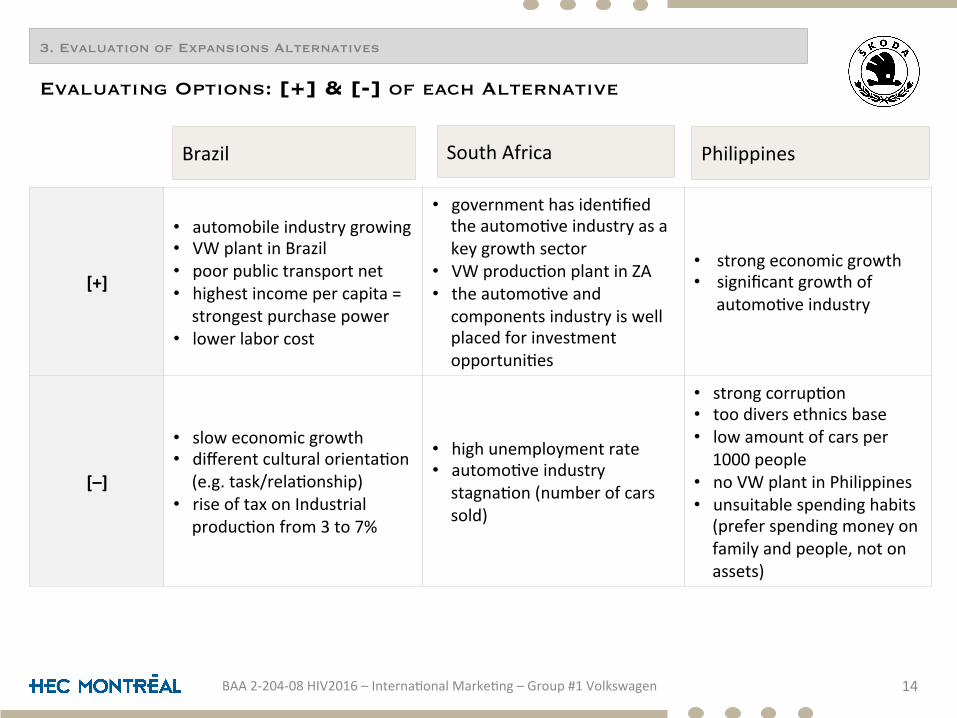

Evaluating Options: [+] & [-] of each Alternative

14BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Brazil SouthAfrica Philippines

[+]

• automobileindustrygrowing• VWplantinBrazil• poorpublictransportnet• highestincomepercapita=strongestpurchasepower

• lowerlaborcost

• governmenthasiden8fiedtheautomo8veindustryasakeygrowthsector

• VWproduc8onplantinZA• theautomo8veandcomponentsindustryiswellplacedforinvestmentopportuni8es

• strongeconomicgrowth• significantgrowthof

automo8veindustry

[–]

• sloweconomicgrowth• differentculturalorienta8on(e.g.task/rela8onship)

• riseoftaxonIndustrialproduc8onfrom3to7%

• highunemploymentrate• automo8veindustrystagna8on(numberofcarssold)

• strongcorrup8on• toodiversethnicsbase• lowamountofcarsper1000people

• noVWplantinPhilippines• unsuitablespendinghabits(preferspendingmoneyonfamilyandpeople,notonassets)

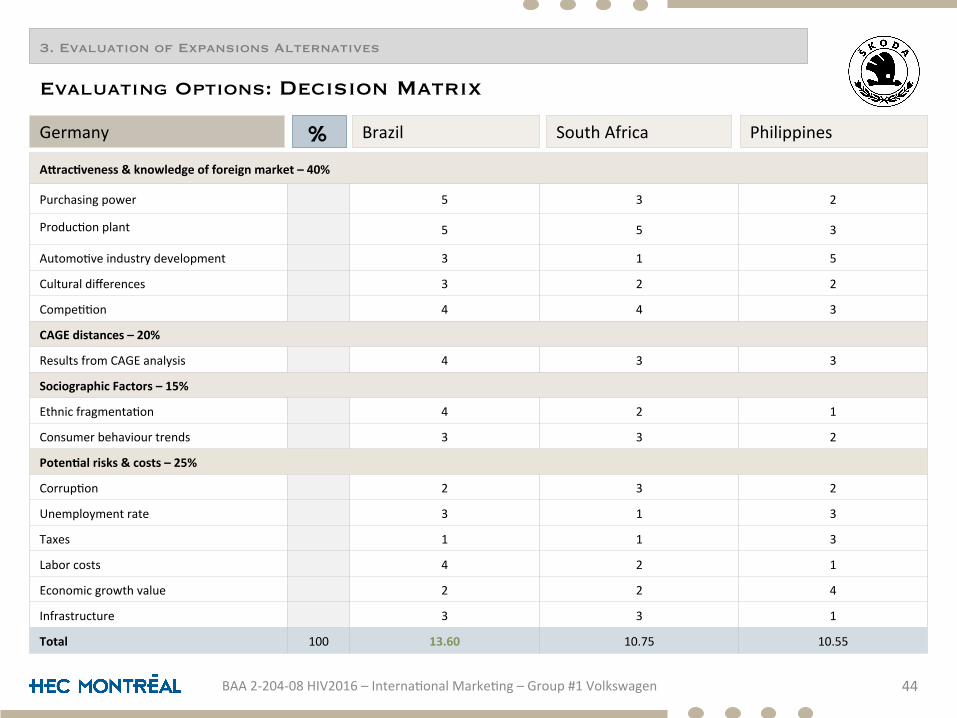

3. Evaluation of Expansions Alternatives

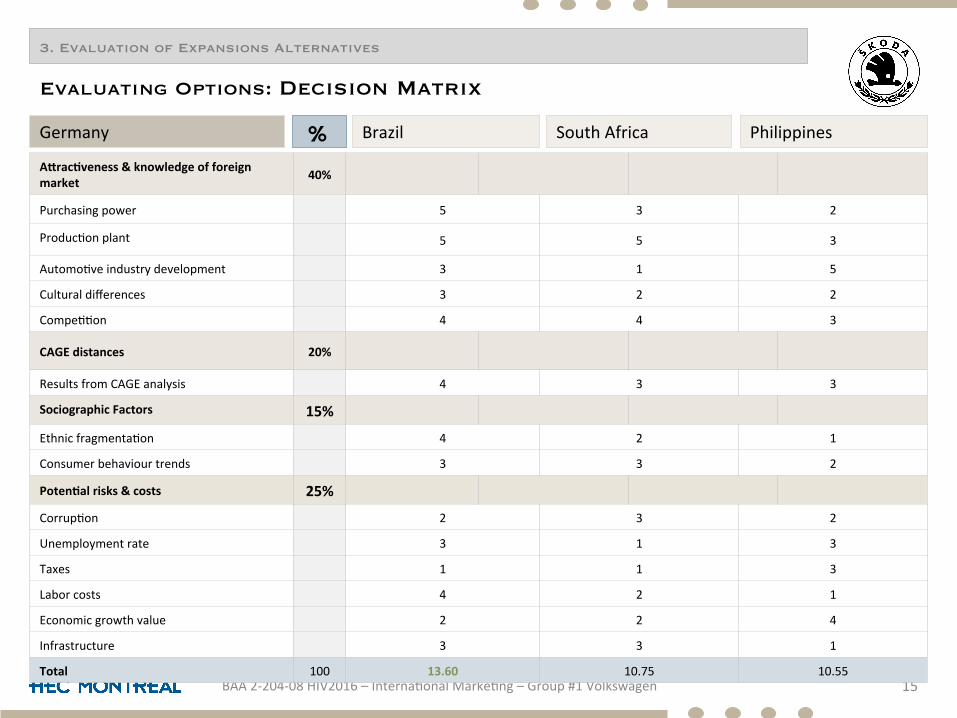

Evaluating Options: Decision Matrix

15BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Brazil SouthAfrica Philippines

AUracVveness&knowledgeofforeignmarket 40%

Purchasingpower 5 3 2

Produc8onplant 5 5 3

Automo8veindustrydevelopment 3 1 5

Culturaldifferences 3 2 2

Compe88on 4 4 3

CAGEdistances 20%

ResultsfromCAGEanalysis 4 3 3

SociographicFactors 15%

Ethnicfragmenta8on 4 2 1

Consumerbehaviourtrends 3 3 2

PotenValrisks&costs 25%

Corrup8on 2 3 2

Unemploymentrate 3 1 3

Taxes 1 1 3

Laborcosts 4 2 1

Economicgrowthvalue 2 2 4

Infrastructure 3 3 1

Total 100 13.60 10.75 10.55

Germany %

3. Evaluation of Expansions Alternatives

DecisiontreeonexpansionofSKODAabroad:

Decisions to take

16BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

HOW

Produc8onPlant

Phillipines

WHERE

SouthAfrica

Brazil

Who

Lowerclass

Middleclass

Upperclass

Problem

toexpand

2keydecision:

• where&

• who

3. Evaluation of Expansions Alternatives

Evaluating Options: SWOT Analysis of Brazil

17BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Strengths Weakness

Opportunities Threats

• marketsize• poli8cally&economicallystable• investment-gradedebt• op8mis8cgrowthprojec8onsinnumerous

industries• increasingglobalinfluence

• largebureaucracy• complexregula8onsandtaxcode• restric8velabourlaws• importtaxesandprotec8onism• shortageofqualifiedpersonnelforsome

industries

• growingeconomic8estoChina,US,Europe&La8nAmerica

• largeinvestmentsbeingmadeininfrastructure• majoroildiscoveries• growingmiddleclasswithincreasingpurchasing

power

• prolongeddownturnintheglobaleconomy• fallincommodityprices• weakeningofthecurrencyaffec8ngcorporate

profits• governmentinac8onintacklingna8onal

economicimbalances

3. Evaluation of Expansions Alternatives

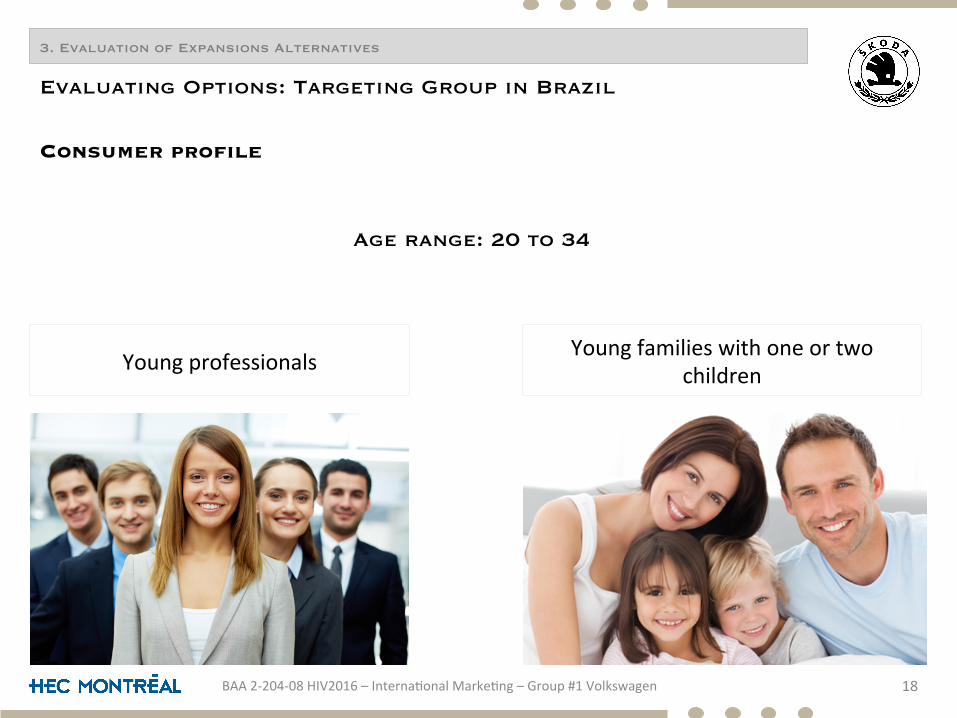

Consumer profile

18BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Evaluating Options: Targeting Group in Brazil

Youngprofessionals Youngfamilieswithoneortwochildren

Age range: 20 to 34

1. PROFILEOFTHECOMPANY

2. SITUATIONANALYSIS3. OPTIONS4. IMPLEMENTATION

5. CONCLUSION6. REFERENCES7. APPENDICES

4. Recommendations for Implementations

Place: Brazil

20BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Degree of Adaption – Standardization of the Marketing Mix

4. Recommendations for Implementations

Place: Brazil, Taubate

21BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Degree of Adaption – Standardization of the Marketing Mix

4. Recommendations for Implementations

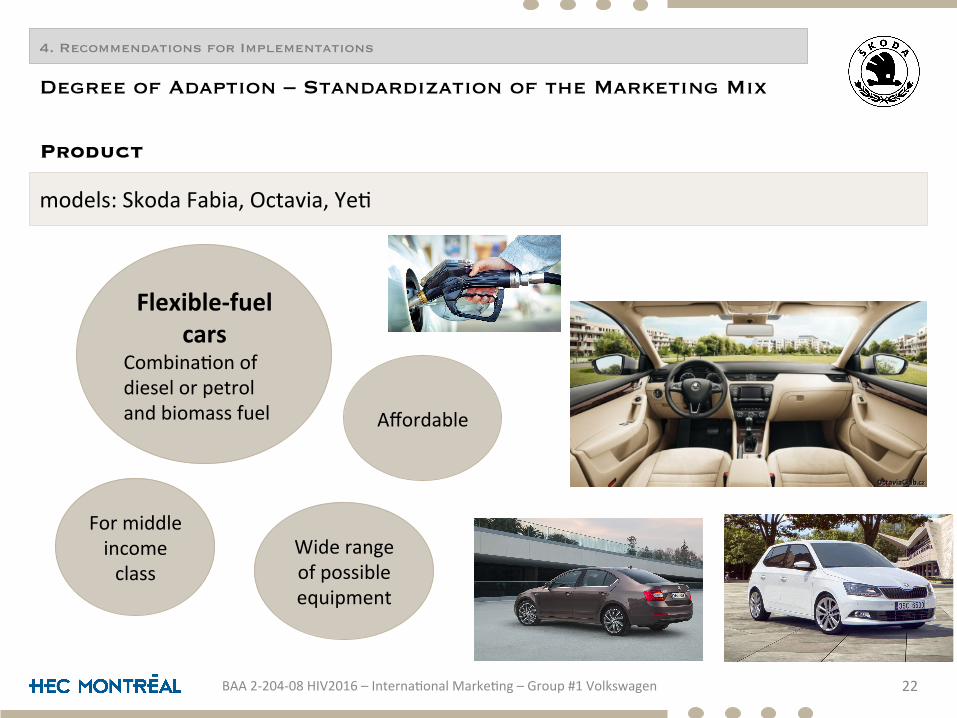

Product

22BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Degree of Adaption – Standardization of the Marketing Mix

models:SkodaFabia,Octavia,Ye8

Flexible-fuelcars

Combina8onofdieselorpetrolandbiomassfuel Affordable

Formiddleincomeclass

Widerangeofpossibleequipment

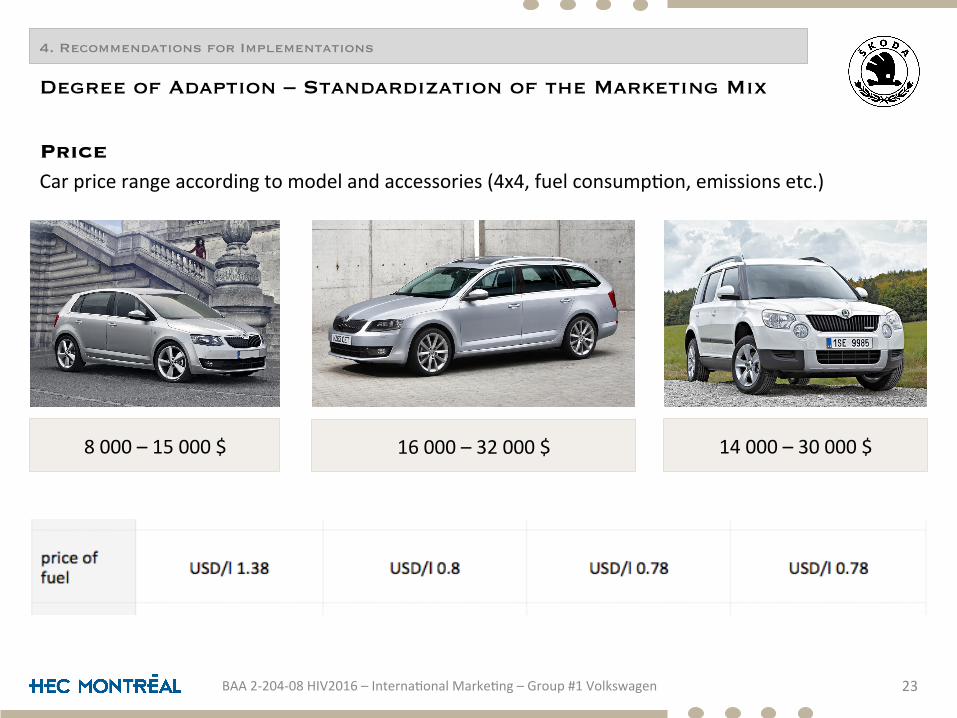

4. Recommendations for Implementations

PriceCarpricerangeaccordingtomodelandaccessories(4x4,fuelconsump8on,emissionsetc.)

23BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Degree of Adaption – Standardization of the Marketing Mix

8000–15000$ 16000–32000$ 14000–30000$

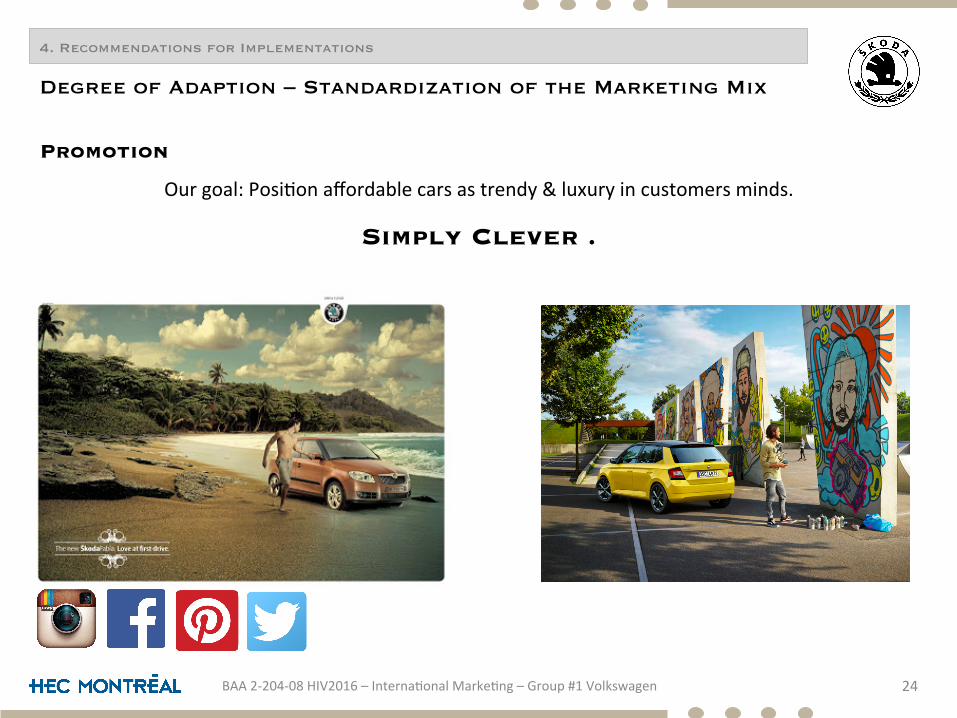

4. Recommendations for Implementations

Promotion

Ourgoal:Posi8onaffordablecarsastrendy&luxuryincustomersminds.

Simply Clever .

24BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Degree of Adaption – Standardization of the Marketing Mix

4. Recommendations for Implementations

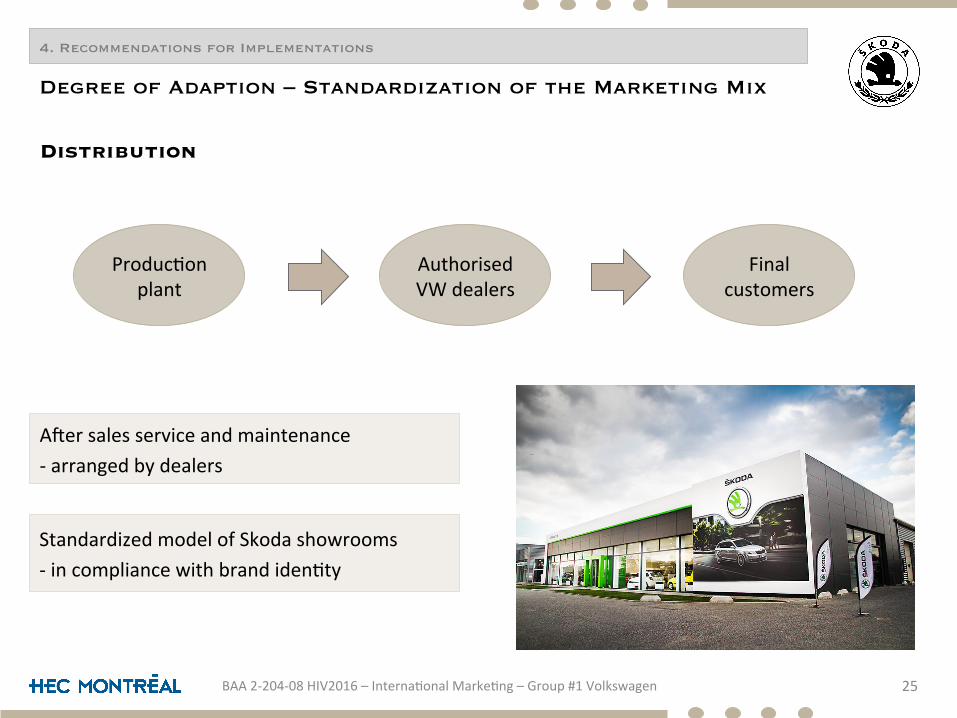

Distribution

25BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Degree of Adaption – Standardization of the Marketing Mix

Produc8onplant

AuthorisedVWdealers

Finalcustomers

Ahersalesserviceandmaintenance-arrangedbydealers

StandardizedmodelofSkodashowrooms-incompliancewithbrandiden8ty

4. Recommendations for Implementations

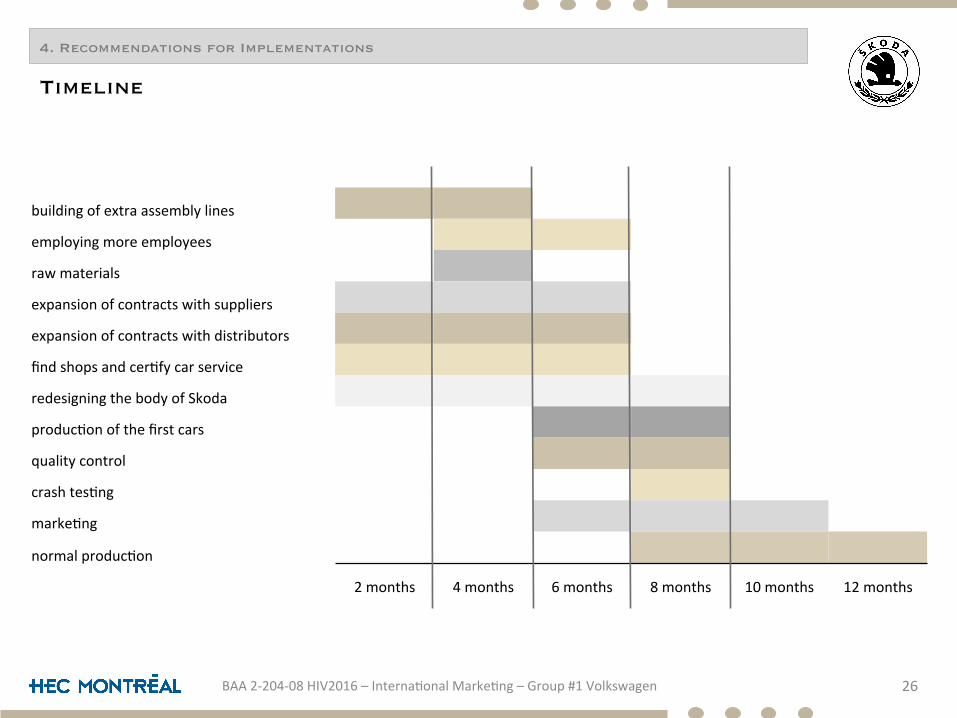

26BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Timeline

buildingofextraassemblylines

employingmoreemployees

rawmaterials

expansionofcontractswithsuppliers

expansionofcontractswithdistributors

findshopsandcer8fycarservice

redesigningthebodyofSkoda

produc8onofthefirstcars

qualitycontrol

crashtes8ng

marke8ng

normalproduc8on

2months 4months 6months 8months 10months 12months

4. Recommendations for Implementations

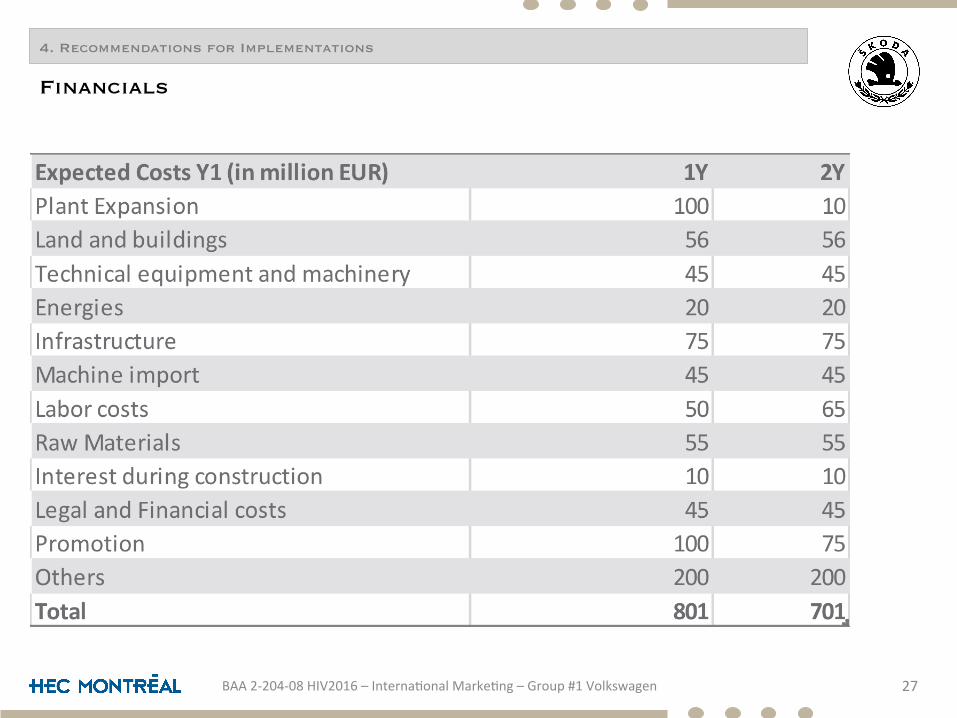

27BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Financials

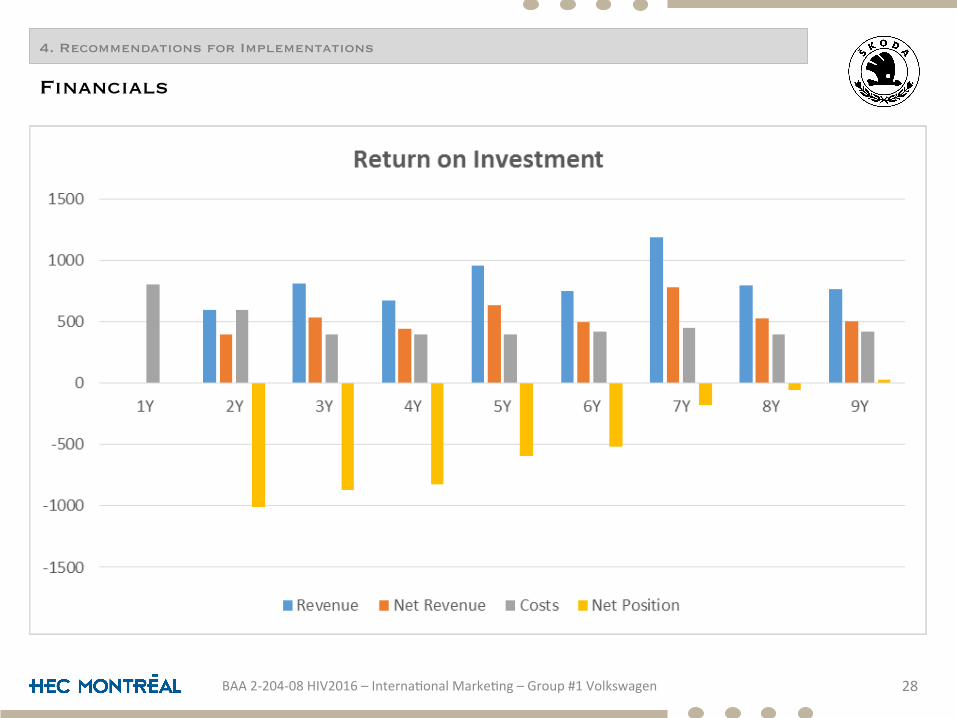

4. Recommendations for Implementations

28BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Financials

1. PROFILEOFTHECOMPANY

2. SITUATIONANALYSIS3. OPTIONS4. IMPLEMENTATION

5. CONCLUSION6. REFERENCES7. APPENDICES

29BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

5. Conclusion

30BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

CHOICE : BRAZIL

• growingmarket

• growingmiddleclass

• increasingglobalinfluence

• highconsumingculture

• welldevelopedinfrastructurecomparedtoSouthAfricaandPhilippines

Entry Mode & Implementation :

• exis8ngproduc8onplant

• 3models(Fabia,Octavia,Ye8)

• biomassfuel(sugarcane)

• affordableprice

• celebri8es&socialmediapromo8on

• plantàdealersàcustomers

FINANCIALS

• ROI:5to10y

1. PROFILEOFTHECOMPANY

2. SITUATIONANALYSIS3. OPTIONS4. IMPLEMENTATION

5. CONCLUSION5. REFERENCES6. APPENDICES

6. References

32BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

• h&p://www.volkswagenag.com/content/vwcorp/content/en/the_group/strategy.html• h&p://www.strategy-business.com/ar8cle/05306?gko=e07fe• h&p://www.skoda-auto.com/SiteCollec8onDocuments/experience/120-years/120-years-skoda-mobil.pdf• h&p://skoda-auto.cm/en/company• h&p://www.strategy-business.com/ar8cle/05306?gko=e07fe• h&p://www.skoda.com.au/about-skoda/skoda-history• h&ps://www.imd.org/research/challenges/upload/from_industry_joke_to_serious_compe8tor.pdf

h&p://automo8velogis8cs.media/intelligence/skoda-simply-clever-logis8cs• h&p://www.strategyand.pwc.com/perspec8ves/2015-auto-trends• h&p://www.skoda-auto.com/en/company/investors/sales-results/• h&ps://www.rolandberger.com/media/pdf/Roland_Berger_Automo8ve_market_perspec8ves_Brazil_2014_2018_20141027.pdf• h&p://www.havasmedia.com/documents_library/insights/hd_automo8vebrazil_genericsept11.pdf• h&p://www.sustainableci8escollec8ve.com/global-site-plans-grid/259241/use-public-transporta8on-brazil-dropped-25-past-15-

years• h&p://www.bloomberg.com/news/ar8cles/2015-12-14/how-bad-is-brazil-car-market-drop-equals-all-of-mexico-s-sales• h&p://www.lightstoneauto.co.za/news/Vehicle_and_home_buying_pa&erns_changing.pdf• h&p://www.cars.co.za/motoring_news/new-vehicle-sales-south-africa-december-2014/28054/#.VsFRt86dJlJ• h&p://www.sta8sta.com/sta8s8cs/388260/adver8sing-expenditures-share-by-medium-south-africa/• h&p://www.campiauto.org• h&ps://www.sta8sta.com/outlook/220/123/social-media-adver8sing/philippines#market-revenue• h&p://www.reportlinker.com/p0487890/Consumer-Lifestyles-in-the-Philippines.html• h&p://www.philippines.hvu.nl/transport1.htm• h&p://www.topgear.com.ph/news/industry-news/if-you-re-interested-volkswagen-ph-now-has-a-leasing-program• h&p://www.apexbrasil.com.br/strategic-priority-sectors

Sitographie

6. References

33BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

• h&ps://www.volkswagen-media-services.com/documents/10541/2074387/Uitenhage_March+2015_en.pdf• h&p://www.forbes.com/sites/kenrapoza/2015/01/03/brazils-automarket-faces-headwinds-ford-expects-sales-to-flatline/

#169fa35f20e4• h&p://bernersconsul8ng.com/de/assets/files/Berners-Consul8ng_Brochure_BR-EU-implementa8on.pdf• h&p://la8nlink.usmediaconsul8ng.com/2012/08/the-top-10-trends-in-brazilian-marke8ng-and-media/

Sitographie

1. PROFILEOFTHECOMPANY

2. SITUATIONANALYSIS3. OPTIONS4. IMPLEMENTATION

5. CONCLUSION5. REFERENCES6. APPENDICES

2. Situation Analysis

Company

Existing Markets

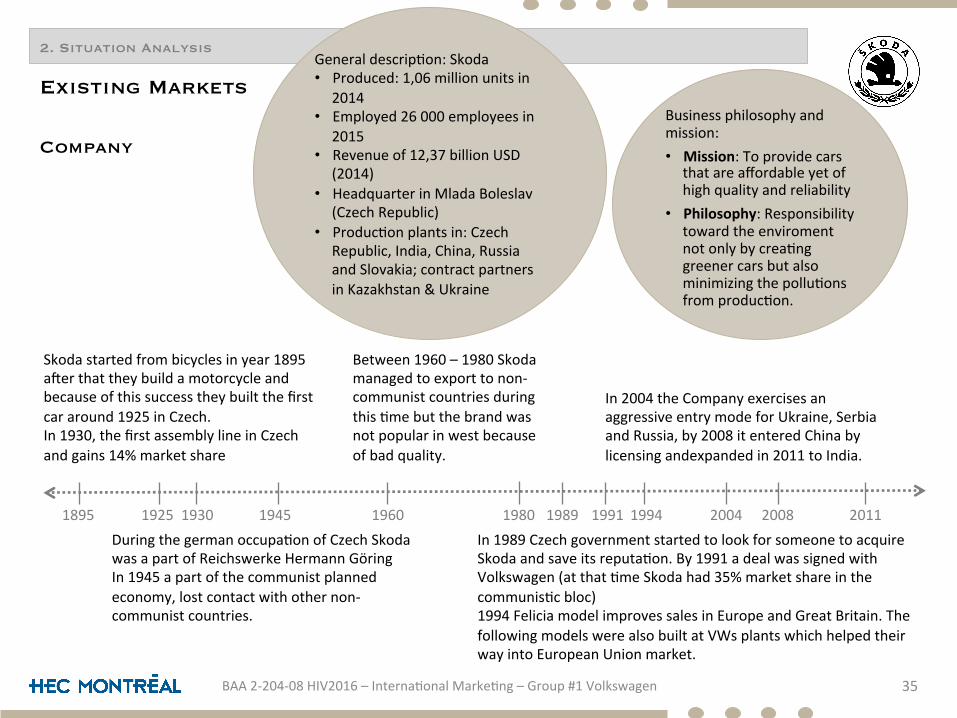

35BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Generaldescrip8on:Skoda• Produced:1,06millionunitsin

2014• Employed26000employeesin

2015• Revenueof12,37billionUSD

(2014)• HeadquarterinMladaBoleslav

(CzechRepublic)• Produc8onplantsin:Czech

Republic,India,China,RussiaandSlovakia;contractpartnersinKazakhstan&Ukraine

Businessphilosophyandmission:• Mission:Toprovidecars

thatareaffordableyetofhighqualityandreliability

• Philosophy:Responsibilitytowardtheenviromentnotonlybycrea8nggreenercarsbutalsominimizingthepollu8onsfromproduc8on.

1895 1925 1930 1945 1960 19891980 1991 1994 2004 2008 2011

Skodastartedfrombicyclesinyear1895aherthattheybuildamotorcycleandbecauseofthissuccesstheybuiltthefirstcararound1925inCzech.In1930,thefirstassemblylineinCzechandgains14%marketshare

Duringthegermanoccupa8onofCzechSkodawasapartofReichswerkeHermannGöringIn1945apartofthecommunistplannedeconomy,lostcontactwithothernon-communistcountries.

Between1960–1980Skodamanagedtoexporttonon-communistcountriesduringthis8mebutthebrandwasnotpopularinwestbecauseofbadquality.

In1989CzechgovernmentstartedtolookforsomeonetoacquireSkodaandsaveitsreputa8on.By1991adealwassignedwithVolkswagen(atthat8meSkodahad35%marketshareinthecommunis8cbloc)1994FeliciamodelimprovessalesinEuropeandGreatBritain.ThefollowingmodelswerealsobuiltatVWsplantswhichhelpedtheirwayintoEuropeanUnionmarket.

In2004theCompanyexercisesanaggressiveentrymodeforUkraine,SerbiaandRussia,by2008itenteredChinabylicensingandexpandedin2011toIndia.

2. Situation Analysis

Target Markets

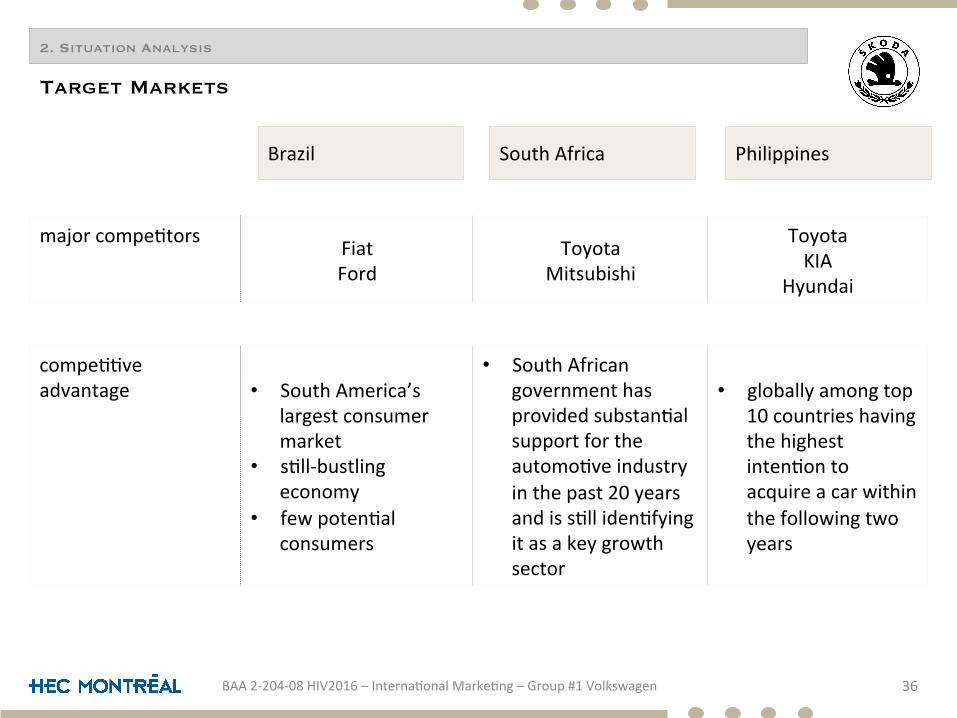

36BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Brazil SouthAfrica Philippines

majorcompe8tors FiatFord

ToyotaMitsubishi

ToyotaKIA

Hyundai

compe88veadvantage • SouthAmerica’s

largestconsumermarket

• s8ll-bustlingeconomy

• fewpoten8alconsumers

• SouthAfricangovernmenthasprovidedsubstan8alsupportfortheautomo8veindustryinthepast20yearsandiss8lliden8fyingitasakeygrowthsector

• globallyamongtop10countrieshavingthehighestinten8ontoacquireacarwithinthefollowingtwoyears

2. Situation Analysis

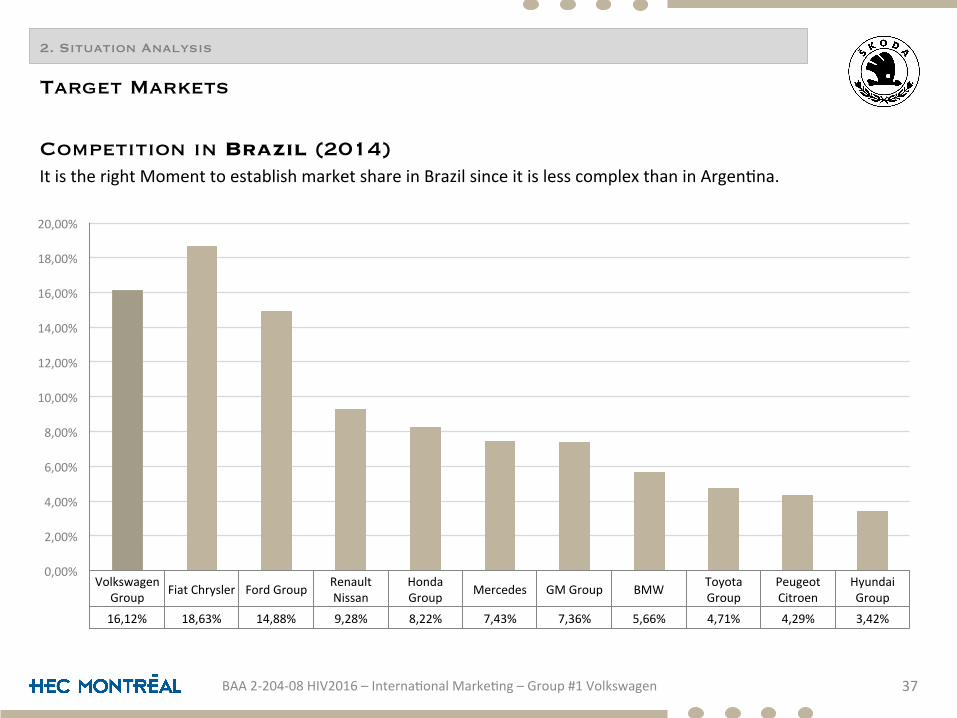

Competition in Brazil (2014)ItistherightMomenttoestablishmarketshareinBrazilsinceitislesscomplexthaninArgen8na.

Target Markets

37BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

VolkswagenGroup FiatChrysler FordGroup Renault

NissanHondaGroup Mercedes GMGroup BMW Toyota

GroupPeugeotCitroen

HyundaiGroup

Datenreihe1 16,12% 18,63% 14,88% 9,28% 8,22% 7,43% 7,36% 5,66% 4,71% 4,29% 3,42%

0,00%

2,00%

4,00%

6,00%

8,00%

10,00%

12,00%

14,00%

16,00%

18,00%

20,00%

2. Situation Analysis

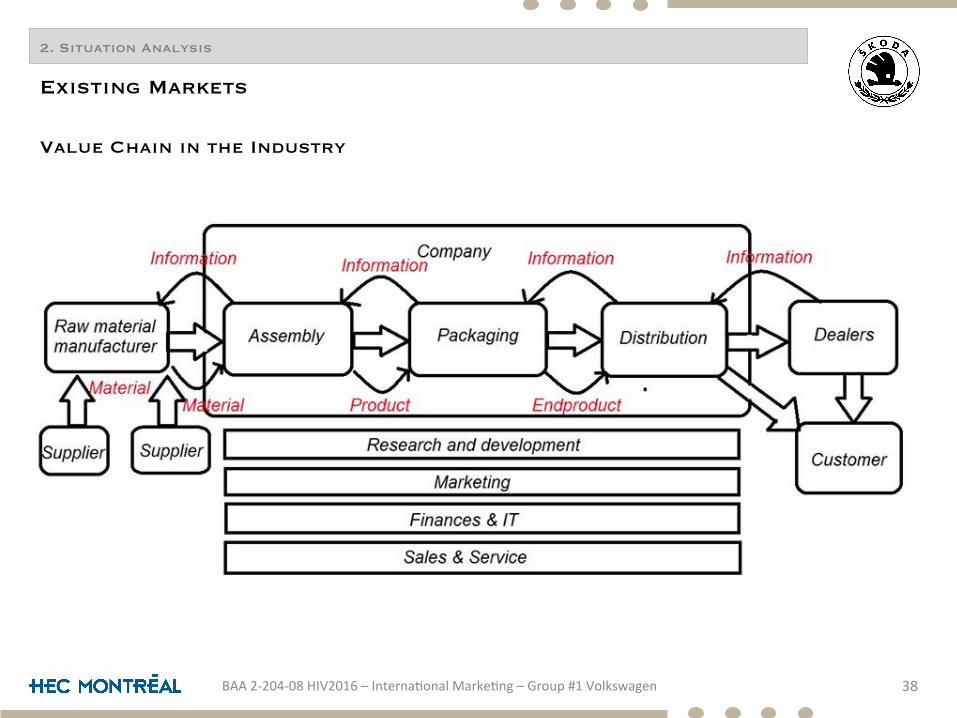

Value Chain in the Industry

Existing Markets

38BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

2. Situation Analysis

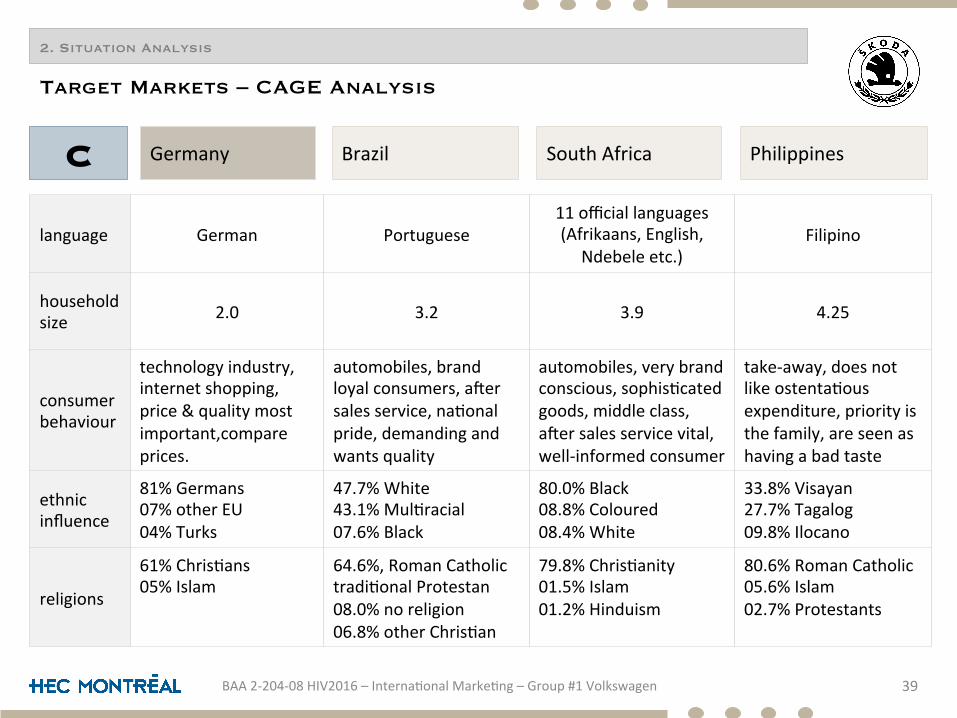

Target Markets – CAGE Analysis

39BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Brazil SouthAfrica Philippines

language German Portuguese11officiallanguages(Afrikaans,English,

Ndebeleetc.)Filipino

householdsize 2.0 3.2 3.9 4.25

consumerbehaviour

technologyindustry,internetshopping,price&qualitymostimportant,compareprices.

automobiles,brandloyalconsumers,ahersalesservice,na8onalpride,demandingandwantsquality

automobiles,verybrandconscious,sophis8catedgoods,middleclass,ahersalesservicevital,well-informedconsumer

take-away,doesnotlikeostenta8ousexpenditure,priorityisthefamily,areseenashavingabadtaste

ethnicinfluence

81%Germans07%otherEU04%Turks

47.7%White43.1%Mul8racial07.6%Black

80.0%Black08.8%Coloured08.4%White

33.8%Visayan27.7%Tagalog09.8%Ilocano

religions

61%Chris8ans05%Islam

64.6%,RomanCatholictradi8onalProtestan08.0%noreligion06.8%otherChris8an

79.8%Chris8anity01.5%Islam01.2%Hinduism

80.6%RomanCatholic05.6%Islam02.7%Protestants

GermanyC

2. Situation Analysis

Target Markets – CAGE Analysis

40BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Brazil SouthAfrica Philippines

corrup8on 81/100 38/100 44/100 35/100

roadtax roadtax n.a. noroadtax n.a.

vehicleinspec8on every2ndyear mandatoryonceayear

fordieselvehiclesonlyoncewhenyoubuy

ausedcar n.a.

emissionregula8on

taxfreeun8l110gms/kmà20eper10gms/

kmn.a. n.a. n.a.

drivinglicenseage

18 18 18 17

GermanyA

2. Situation Analysis

Target Markets – CAGE Analysis

41BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Brazil SouthAfrica Philippines

levelofpublictransport

high lowandtooexpensive high underdeveloped

distancetoproduc8onplant

Germany Brazil SouthAfrica Taiwan

infra-structurelevelindex

6.2 3.92 4.12 3.43

GermanyG

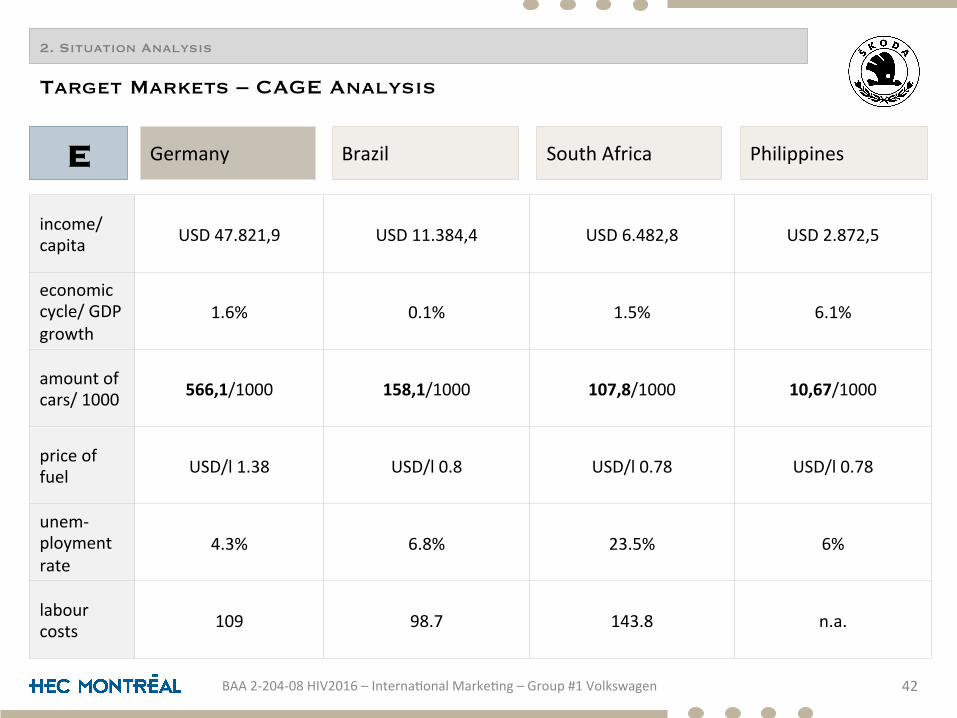

2. Situation Analysis

Target Markets – CAGE Analysis

42BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Brazil SouthAfrica Philippines

income/capita USD47.821,9 USD11.384,4 USD6.482,8 USD2.872,5

economiccycle/GDPgrowth

1.6% 0.1% 1.5% 6.1%

amountofcars/1000 566,1/1000 158,1/1000 107,8/1000 10,67/1000

priceoffuel USD/l1.38 USD/l0.8 USD/l0.78 USD/l0.78

unem-ploymentrate

4.3% 6.8% 23.5% 6%

labourcosts 109 98.7 143.8 n.a.

GermanyE

3. Evaluation of Expansions Alternatives

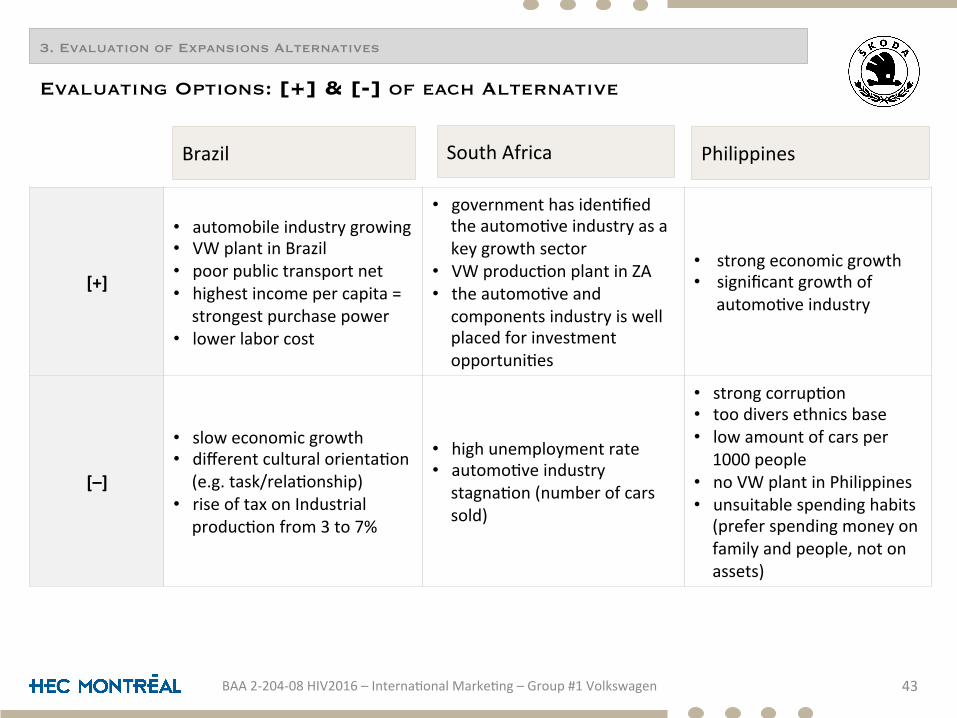

Evaluating Options: [+] & [-] of each Alternative

43BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Brazil SouthAfrica Philippines

[+]

• automobileindustrygrowing• VWplantinBrazil• poorpublictransportnet• highestincomepercapita=strongestpurchasepower

• lowerlaborcost

• governmenthasiden8fiedtheautomo8veindustryasakeygrowthsector

• VWproduc8onplantinZA• theautomo8veandcomponentsindustryiswellplacedforinvestmentopportuni8es

• strongeconomicgrowth• significantgrowthof

automo8veindustry

[–]

• sloweconomicgrowth• differentculturalorienta8on(e.g.task/rela8onship)

• riseoftaxonIndustrialproduc8onfrom3to7%

• highunemploymentrate• automo8veindustrystagna8on(numberofcarssold)

• strongcorrup8on• toodiversethnicsbase• lowamountofcarsper1000people

• noVWplantinPhilippines• unsuitablespendinghabits(preferspendingmoneyonfamilyandpeople,notonassets)

3. Evaluation of Expansions Alternatives

Evaluating Options: Decision Matrix

44BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Brazil SouthAfrica Philippines

AUracVveness&knowledgeofforeignmarket–40%

Purchasingpower 5 3 2

Produc8onplant 5 5 3

Automo8veindustrydevelopment 3 1 5

Culturaldifferences 3 2 2

Compe88on 4 4 3

CAGEdistances–20%

ResultsfromCAGEanalysis 4 3 3

SociographicFactors–15%

Ethnicfragmenta8on 4 2 1

Consumerbehaviourtrends 3 3 2

PotenValrisks&costs–25%

Corrup8on 2 3 2

Unemploymentrate 3 1 3

Taxes 1 1 3

Laborcosts 4 2 1

Economicgrowthvalue 2 2 4

Infrastructure 3 3 1

Total 100 13.60 10.75 10.55

Germany %

3. Evaluation of Expansions Alternatives

Evaluating Options: SWOT Analysis of Brazil

45BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Strengths Weakness

Opportunities Threats

• marketsize• poli8cally&economicallystable• investment-gradedebt• op8mis8cgrowthprojec8onsinnumerous

industries• Increasingglobalinfluence

• largebureaucracy• complexregula8onsandtaxcode• restric8velabourlaws• importtaxesandprotec8onism• shortageofqualifiedpersonnelforsome

industries

• growingeconomic8estoChina,US,Europe&La8nAmerica

• largeinvestmentsbeingmadeininfrastructure• majoroildiscoveries• growingmiddleclasswithincreasingpurchasing

power

• prolongeddownturnintheglobaleconomy• fallincommodityprices• weakeningofthecurrencyaffec8ngcorporate

profits• governmentinac8onintacklingna8onal

economicimbalances

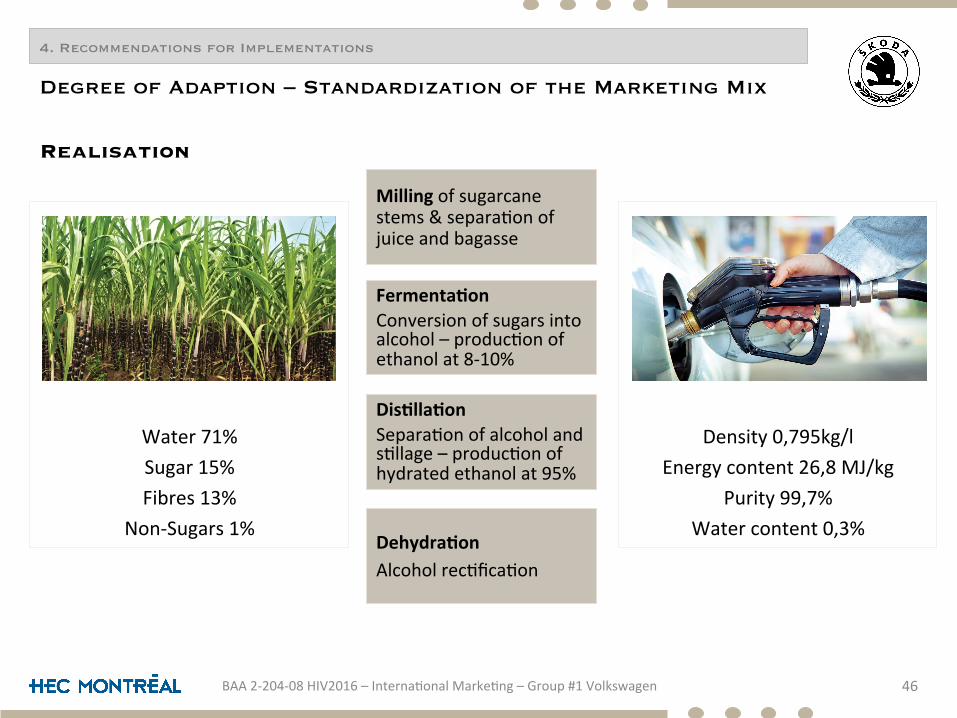

4. Recommendations for Implementations

Realisation

Degree of Adaption – Standardization of the Marketing Mix

46BAA2-204-08HIV2016–Interna8onalMarke8ng–Group#1Volkswagen

Water71%Sugar15%Fibres13%

Non-Sugars1%

Density0,795kg/l

Energycontent26,8MJ/kgPurity99,7%

Watercontent0,3%

Millingofsugarcanestems&separa8onofjuiceandbagasse

FermentaVonConversionofsugarsintoalcohol–produc8onofethanolat8-10%

DisVllaVonSepara8onofalcoholands8llage–produc8onofhydratedethanolat95%

DehydraVonAlcoholrec8fica8on