FUTURE DIRECTIONS FOR FIBER DEEP HFC DEPLOYMENTS … · future directions for fiber deep hfc...

35

FUTURE DIRECTIONS FOR FIBER DEEP HFC DEPLOYMENTS JOHN ULM ZORAN MARICEVIC A CASE STUDY ON HFC TO FTTX MIGRATION STRATEGIES

Transcript of FUTURE DIRECTIONS FOR FIBER DEEP HFC DEPLOYMENTS … · future directions for fiber deep hfc...

FUTUREDIRECTIONSFORFIBERDEEPHFCDEPLOYMENTS

JOHNULMZORANMARICEVIC

ACASESTUDYONHFCTOFTTXMIGRATIONSTRATEGIES

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 2

TABLEOFCONTENTSINTRODUCTION.............................................................................................3NETWORKCAPACITY–PLANNINGFORTHENEXTDECADE..........................3Nielsen’sLawandCloonan’sCurves...............................................................................3

SelectiveSubscriberMigrationStrategy.........................................................................5

ACCESSNETWORKCASESTUDY....................................................................9ACCESSNETWORKUPGRADEOPTIONS:COSTIMPACTS.............................16HFCBAUvFTTH–PreviousFindings............................................................................16

CostComparisonofVariousHFCUpgradeOptions......................................................19

DOCSISPay-as-You-GrowStrategy...............................................................................23

CONCLUSION...............................................................................................27ACKNOWLEDGEMENTS...............................................................................28ABBREVIATIONS...........................................................................................29RELATEDREADINGS.....................................................................................32REFERENCES................................................................................................34

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 3

INTRODUCTIONTodayingreenfieldscenarios,ithasbecomemorecommonforoperatorstoinstallfiberallthewaytothehomeorMDU(FibertothePremise-FTTP),asitisviewedastheultimateendgamefromaplantperspective.Withtheconstanttideofbroadbandspeedgrowth,operatorsarenowstartingtoconsidertheirHFCtransitiontoFTTPforbrownfieldscenariosaswell.ShouldtheystopinvestinginHFCandjustgorighttoFTTP?Thisisadauntingtaskgiventhecostsinvolved.

Thispaperdetailsacasestudyofseveralactualnodedesignsandexploresthecostimpactsofvariousplantupgrades;fromsimplysplittingnodestotacklebusinessasusualdemands,allthewaytoFTTP.ItalsohighlightssomeemerginginnovativeconceptsforadistributednodearchitecturethatcosteffectivelyenablesFiberDeep(FD)designssuchasFibertotheLastActive(FTTLA)orFibertotheCurb(FTTC).

Thepaperstartswithacomprehensivenetworkcapacityanalysisthatshowswhatcapacitiesmightbeneeded,andatwhattimeoverthecomingdecades.ThisallowsustolayoutanHFCmigrationstrategytoFTTxovera10+yearwindow.ANetPresentValueanalysisshowsthatthismulti-stepapproachismorecosteffectivethandivingheadfirstintoFTTP.Itwillalsoshowthatformanyormostsubscribersontoday’sHFC,FTTPmaynotnecessarilybetheendgame,ratherFTTLAorFTTCmaysuffice.

ThefindingsfromthispaperareimportantinallowingoperatorstoplantheirHFCtofiberjourneyinapayasyougomanner.Acompanionpapertothis[ULM_2016]discussestheenergyimpactstoboththeaccessnetworkandheadendfacilities.

NETWORKCAPACITY–PLANNINGFORTHENEXTDECADETheInternethasbeengrowingatabreakneckspeedsinceitsinception.Andwithit,wehaveseenacorrespondinggrowthindedicatednetworkcapacity.WhileMoore’sLawisinfamousinsiliconrealms,Nielsen’sLawofInternetBandwidthhasbecomerenowninthenetworkingworld.Itbasicallystatesthatnetworkconnectionspeedsforhigh-endhomeuserswouldincrease50%peryear.Thislawhasdrivenmuchofthetrafficengineeringandnetworkcapacityplanningintheserviceproviderworld.Ithasalsoledtomuchresearchonthosetopics.

Nielsen’sLawandCloonan’sCurvesIn[CLOONAN_2014,EMM_2014],thisresearchwasexpandedtoalsoincludetrafficutilizationinadditiontothenetworkconnectionspeed.Inhischartbelow,knownas

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 4

Cloonan’sCurves,Nielsen’sLawisrepresentedbythebluelineinthemiddle.Sinceitisalogscale,the50%CompoundedAnnualGrowthRate(CAGR)appearsasastraightline.Aninterestingfactisthatthegraphstartsin1982witha300-baudphonemodem.Wearenowinthefourthdecadeofcloselyfollowingthistrend.

Figure1–Cloonan’sCurves

Cloonannotedthattheprimetimeaveragesubscriberconsumption(a.k.a.Tavg)hasalsobeenfollowingthissamebasictrendasshownintheFigure1.Forserviceproviders,animportantmetricisthetrafficutilizationinaServiceGroup(SG).TheSGtrafficutilizationisafunctionofthenumberofsubscribers(Nsub)timestheaveragebandwidthpersub(Tavg)andisshowninaseriesoflinesaboveNielsen’sline.

IntheearlyDOCSISdays,manynodeswerecombinedtogetherandaSGmightconsistofthousandsofsubscribers.Atthistime,theSGtrafficwasanorderofmagnitudehigherthanthemaximumnetworkconnectionspeed(a.k.a.TmaxaftertheDOCSISparameterthatdictatesmaxnetworkrates).Overtime,theSGsizehasbeenshrinkingandwithittheratiobetweenNsub*TavgtoTmax.Asshowninthechartabove,theSGtrafficeventuallyapproachesthatofTmax.AsSGsizesdipbelow100subs,thenTmaxstartstodominatethetrafficengineering.

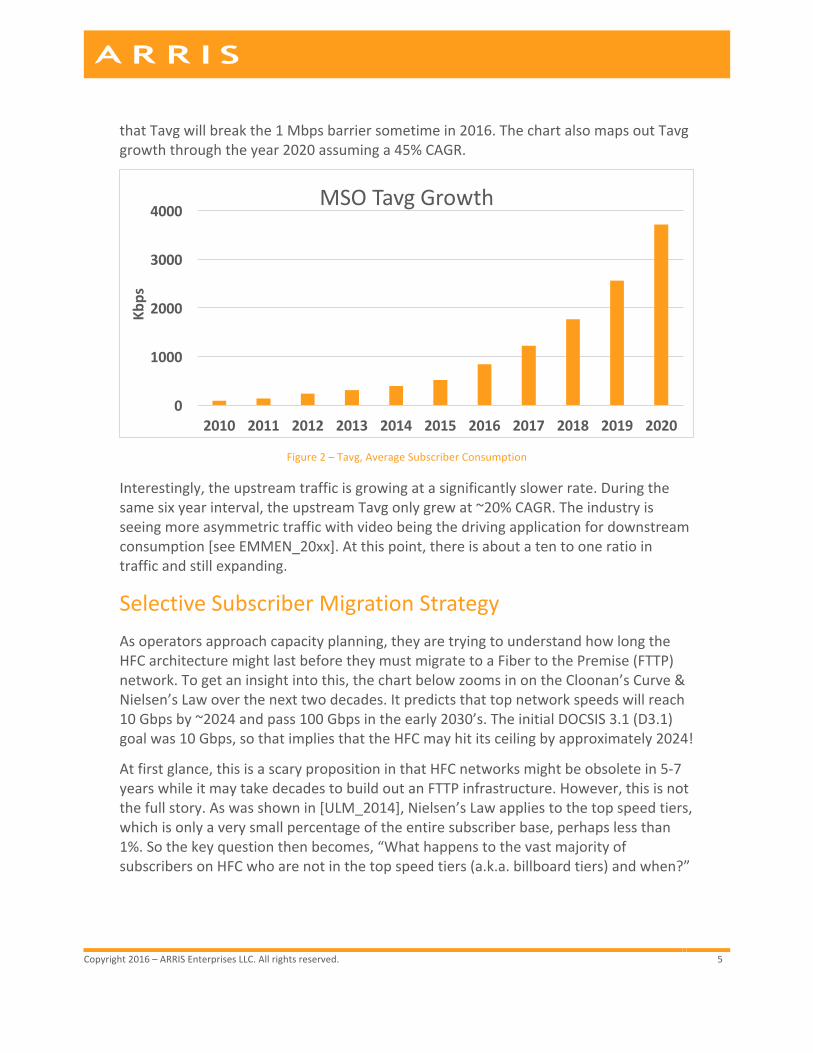

Wehavebeenmonitoringsubscriberusageformanyyearsnow.ThechartbelowshowsTavg,theaveragesubscriberdownstreamconsumptionduringpeakbusyhours,foranumberofMSOsoverthelastsixyears.Atthestartof2016,Tavgwasapproximately850Kbps.Overthissixyearperiod,Tavghasgrownat~45%CAGR.Weareexpecting

8000 Subs/SG (Many Nodes)

2000 Subs/SG (Many Nodes)

512 Subs/SG

128 Subs/SG (256 HHP Nodes)

32 Subs/SG (64 HHP Nodes)64 Subs/SG (128 HHP Nodes)

16 Subs/SG (32 HHP Nodes)116 DOCSIS 3.0 Chans.32 DOCSIS 3.0 Chans.

256 Subs/SG (512 HHP Nodes)512 Subs/SG (2x 512 HHP Nodes)

64 DOCSIS 3.0 Chans.

1.2 GHz of DOCSIS 3.1 Chans.

DS BW as a function of time(w/ ~50% Annual Growth Rate)

DS

BW

for M

odem

s (b

ps)

1982 1986 1990 1994 19981

10

100

1k

2002 2006

10k

100k

1M

10M

100M

1G

2010 2014

10G

100G

2018

The Era of

CableModems

The Era of

Dial-Up Modems

2022

D3.0 DS Limit = 4.9 Gbps (750 MHz)

2026 2030

D3.1 DS Limit = 10.8 Gbps (1200 MHz)

1 DOCSIS 3.0 Chan.

4 DOCSIS 3.0 Chans.

16 DOCSIS 3.0 Chans.

~100 kbpsin 2010

Nielsen’s Law’sTmax

Avg BW/SG

300 bpsin 1982

~500 bpsin 1997

~332 Mbpsin 2030

8 DOCSIS 3.0 Chans.

The Eraof3.0

Modems

~150 kbpsin 1997

Avg BW/sub

The Eraof

3.1Modems

Consumption-Oriented Period(Tmax < 1 Ch &Tmax < Avg SGConsumption)

Consumption+ Tmax-

Oriented Period(Tmax =~ Avg SG

Consumption)

Tmax-OrientedPeriod

(Tmax >> Avg SGConsumption)

Avg BW/SG

Max BW/sub

2 DOCSIS 3.0 Chans.

Year

1000 Subs/SG

16000 Subs/SG (Many Nodes)

4000 Subs/SG (Many Nodes)

Avg BW/SG

~100Gbpsin 2030

Proposed Human Factors Formula:

Required SG Capacity =K* Max BW/sub + Num_subs * Avg BW/sub

(K=1 may yield acceptable QoE)

~30Mbpsin 2010

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 5

thatTavgwillbreakthe1Mbpsbarriersometimein2016.ThechartalsomapsoutTavggrowththroughtheyear2020assuminga45%CAGR.

Figure2–Tavg,AverageSubscriberConsumption

Interestingly,theupstreamtrafficisgrowingatasignificantlyslowerrate.Duringthesamesixyearinterval,theupstreamTavgonlygrewat~20%CAGR.Theindustryisseeingmoreasymmetrictrafficwithvideobeingthedrivingapplicationfordownstreamconsumption[seeEMMEN_20xx].Atthispoint,thereisaboutatentooneratiointrafficandstillexpanding.

SelectiveSubscriberMigrationStrategyAsoperatorsapproachcapacityplanning,theyaretryingtounderstandhowlongtheHFCarchitecturemightlastbeforetheymustmigratetoaFibertothePremise(FTTP)network.Togetaninsightintothis,thechartbelowzoomsinontheCloonan’sCurve&Nielsen’sLawoverthenexttwodecades.Itpredictsthattopnetworkspeedswillreach10Gbpsby~2024andpass100Gbpsintheearly2030’s.TheinitialDOCSIS3.1(D3.1)goalwas10Gbps,sothatimpliesthattheHFCmayhititsceilingbyapproximately2024!

Atfirstglance,thisisascarypropositioninthatHFCnetworksmightbeobsoletein5-7yearswhileitmaytakedecadestobuildoutanFTTPinfrastructure.However,thisisnotthefullstory.Aswasshownin[ULM_2014],Nielsen’sLawappliestothetopspeedtiers,whichisonlyaverysmallpercentageoftheentiresubscriberbase,perhapslessthan1%.Sothekeyquestionthenbecomes,“WhathappenstothevastmajorityofsubscribersonHFCwhoarenotinthetopspeedtiers(a.k.a.billboardtiers)andwhen?”

0

1000

2000

3000

4000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Kbps

MSOTavgGrowth

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 6

Figure3–DownstreamGrowthoverNextTwoDecades

The[ULM_2014]casestudytookalookatservicetierevolutionatafewMSOs.Table1laysoutresultsfromthatstudy.Perhapsthekeyfindingfromthisstudyisthatthedifferentservicetiersaregrowingatdifferentrates.WhilethetopbillboardtiercontinuestofollowNielsen’sLaw50%,eachsubsequentlowerspeedtierisgrowingataslowerrate.Hence,thelowertheservicetierrate,theloweritsCAGR.

Table1–MSOCaseStudyonMultipleServiceTierLevels

2014 Service Tier Levels on HFC % of Subs Tmax (Mbps)

Tmax CAGR

Top Tier – Billboard Rate 1% 300 50%

Performance Tier 14% 75 32%

Basic Tier 65% 25 26%

Economy Tier 20% 5 15%

Figure4mapsoutthevariousservicetiergrowthoverthenexttwodecades.Whilethe1%ofsubsinthetopbillboardtierhit10Gbpsin~2024,the14%ofsubsintheperformancetierdon’thitthatmarkuntil~2032.Noticethat85%ofsubscribersintheflagshipbasictierandeconomytierstaybelowthismarkforseveraldecades.

100

1000

10000

100000

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

Mbp

s

DownstreamGrowth

Tmax

Tavg

Tmax+Tavg

Hits10GCeilingby2024

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 7

Figure4–DownstreamGrowthwithMultipleServiceTiers

DatawasinputintotheARRISNetworkCapacitymodeltotakeacloserlookatthenetworktrafficgrowth.Table2showstheTmaxmigrationusedforeachtierleveloverthenextdecade.Notethatby2021,thetopbillboardtierstartstoexceedthecapacityoftheinitialD3.1modemsthatarebeingusedtoday.Andby2026,thistierisforecasttohit40Gbps.Thiswillrequirenewtechnology,whichmightbeanewergenerationofDOCSIS(e.g.ExtendedSpectrum)orpossiblyanextgenerationofPONtechnology(e.g.100GEPON).

Table2–ServiceTierMigrationforNetworkCapacityModel

MSO Case Study DS Service Tiers

% of Subs

Tmax CAGR 2014 2016 2021 2026

Top Billboard Tier <1% 50% 300 675 5G 40G

Performance Tier 14% 32% 75 125 500 2G

Basic Tier 65% 26% 25 40 150 400

Economy Tier 20% 15% 5 10 20 50

Itisimportanttonotethat99%ofthesubscribersarestillcomfortablyusingtoday’sDOCSIStechnologyonHFCadecadefromnow.

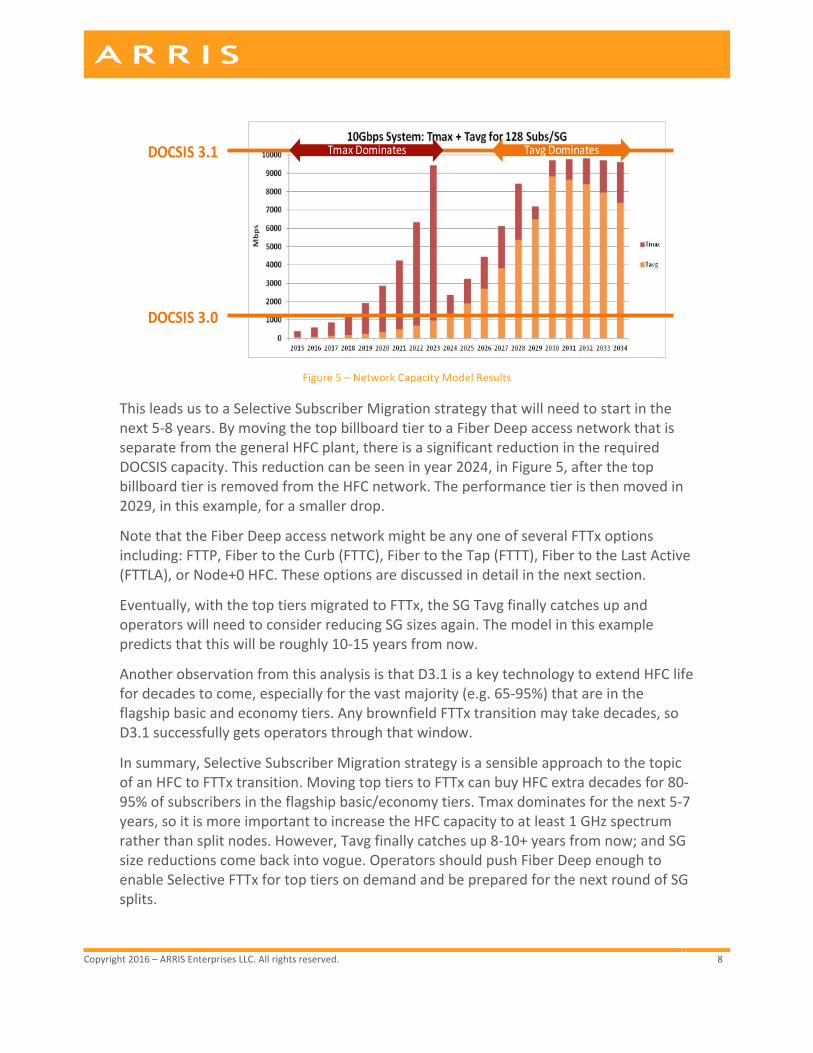

SomeresultsfromtheARRISNetworkCapacitymodelareshowninFigure5.ItprovidesaninsightintobothTmaxandSGTavgbehavior.Duringthenext5-7years,theTmaxcomponentdominatestrafficengineeringasitisdrivenbyNielsen’sLaw.ThebandwidthneededbythetopbillboardtierdominatescomparedtotheSGTavg.

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 8

Figure5–NetworkCapacityModelResults

ThisleadsustoaSelectiveSubscriberMigrationstrategythatwillneedtostartinthenext5-8years.BymovingthetopbillboardtiertoaFiberDeepaccessnetworkthatisseparatefromthegeneralHFCplant,thereisasignificantreductionintherequiredDOCSIScapacity.Thisreductioncanbeseeninyear2024,inFigure5,afterthetopbillboardtierisremovedfromtheHFCnetwork.Theperformancetieristhenmovedin2029,inthisexample,forasmallerdrop.

NotethattheFiberDeepaccessnetworkmightbeanyoneofseveralFTTxoptionsincluding:FTTP,FibertotheCurb(FTTC),FibertotheTap(FTTT),FibertotheLastActive(FTTLA),orNode+0HFC.Theseoptionsarediscussedindetailinthenextsection.

Eventually,withthetoptiersmigratedtoFTTx,theSGTavgfinallycatchesupandoperatorswillneedtoconsiderreducingSGsizesagain.Themodelinthisexamplepredictsthatthiswillberoughly10-15yearsfromnow.

AnotherobservationfromthisanalysisisthatD3.1isakeytechnologytoextendHFClifefordecadestocome,especiallyforthevastmajority(e.g.65-95%)thatareintheflagshipbasicandeconomytiers.AnybrownfieldFTTxtransitionmaytakedecades,soD3.1successfullygetsoperatorsthroughthatwindow.

Insummary,SelectiveSubscriberMigrationstrategyisasensibleapproachtothetopicofanHFCtoFTTxtransition.MovingtoptierstoFTTxcanbuyHFCextradecadesfor80-95%ofsubscribersintheflagshipbasic/economytiers.Tmaxdominatesforthenext5-7years,soitismoreimportanttoincreasetheHFCcapacitytoatleast1GHzspectrumratherthansplitnodes.However,Tavgfinallycatchesup8-10+yearsfromnow;andSGsizereductionscomebackintovogue.OperatorsshouldpushFiberDeepenoughtoenableSelectiveFTTxfortoptiersondemandandbepreparedforthenextroundofSGsplits.

DOCSIS3.0

DOCSIS3.1 TmaxDominates TavgDominates

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 9

AndwhichFTTxisthebestoptionisanotherinterestingdebate.DOCSIScontinuestoevolvewithworkonFullDuplex(FDX)andExtendedSpectrumDOCSIS.Someofthisresearchwashighlightedin[CLOONAN_2016].ThesenewtechnologiespromisetodoforDOCSIS&cablewhatG.fastisattemptingtodoforDSLandtwistedpair.Figure6showssomeresultsfromthatpaperforbothFTTCandFTTLAsystems.Ascanbeseen,thesystemcapacitycanincreasesignificantlyasfiberispushedclosertothepremise.

Figure6–NetworkCapacityModelResults

ACCESSNETWORKCASESTUDYThenetworkcapacityplanningshowsthatoperatorswillneedtoevolvetheirexistingHybridFiberCoax(HFC)networkstoremaincompetitivewithFTTPserviceproviderssuchasGoogleFiberandVerizonFiOS[VENK_2016,VENK_2015andULM_2015].Forcableoperators,theycanutilizetheirexistingfiberinvestmentsasastartingpointtogetajumpstartcomparedtonewentrantsthatmuststarttheirfiberinstallationfromscratch.Butthecriticalquestionforcableoperatorsishowdeepshouldtheypullthefiber?Theyarepresentedwithatoolboxofarchitecturalchoicestoconsider:

• “Businessasusual”(BAU)–anodesplitwhereneeded,andarefreshoftheHFCfieldactives,withperhapsanupgradeto5-85MHzinthereturnand104-1002MHzintheforward

• FiberDeep(FD)Node+0(N+0)pushesfibermuchdeeperintotheHFCandeliminatesalloftheactiveRFelements.Thereisanarrayofpotentialoptionsincluding:

o TraditionalFiberDeepNode+0“FDN+0”whichredesignsexistingHFC(e.g.N+3toN+6with3-6activesafterthefibernode)into“nodeasthelastactive”.Thetypicalwaytodothisistorewirethecoaxplantinawaytominimizehowmanyofthesestandard-sizenewnodesneedtobeadded.Eachnewnodemayultimatelybecomeitsownservicegroup,andinadditiontotheRFandopticalmodules,itmayhouseRemotePHYDevices(RPDs)andPONOLTs

0

5

10

15

20

25

30

35

0 2 4 6 8

Capa

city[G

bps]

SpectrumSize[GHz]

CapacityinanFTTLAsystem

100ft

150ft

200ft

250ft

400ft

500ft

Dropcablelength

0

50

100

150

200

250

300

0 5 10 15 20 25 30

Throughp

ut(G

bps)

SpectrumSize[GHz]

CapacityinanFTTCSystem

100ft

150ft

200ft

250ft

400ft

500ft

DropcableLength

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 10

o Fibertothelastactive(FTTLA)isavariantoftheFiberDeepN+0architecture.However,inthiscasethenodesarelocatedpreciselyatlegacyRFamplocations.Thesenodesthengetaggregatedintoaproperly-sizedservicegroup.Thisaggregationcanbedonebyusingan“activesplitter/combiner”,housedinavirtualhub,whichislocatedpreciselyatthelegacynodelocationtosaveonopticscosts&spaceinthefacility

o Fibertothecurb(FTTC)orFibertothetap(FTTT)wherefiberisrundownthestreetbuttheexistingcabledropcablesarereused

• FibertothePremise(FTTP)–thisiswhatisbeingdeployedtodaywithtraditionalPONsystemsaswellasRFoGsystems

Collectively,thesefiberdeeperoptionsarereferredtoasFTTxorFibertothe“x”,where“x”mightbePremise,Curb,Tap,LastActive,orFiberDeepnode.Forcableoperatorstobuildoutanyoftheabovearchitecturesintoday’sbrownfields,thenewfiberconstructionbeginsfromanexistingfibernode;unlikethenewentrantswhomustbuildthefiberconstructionfromthecentraloffice/headend.

EachMSOwillmakechangestotheirownHFCplanttooptimizefortheattributesthattheydeemtobethemostimportant.DifferentMSOswilllikelyprioritizethemanyattributesindifferentways.Forexample,someMSOsmaychoosetooptimizetheirnetworkevolutionbymovingasrapidlyaspossibletoend-statetechnologiesofthefuture.TheseMSOswilllikelymoverapidlytowards(passiveopticalnetwork)PONorPoint-to-PointEthernetsolutions.OtherMSOswillchoosetooptimizetheirnetworkevolutiontoreduceheadendpowerandrack-spacerequirementsbymovingtowardsFiberDeeparchitectureswithDistributedAccessArchitecturesub-systemsthatremovefunctionalityfromtheheadend.TheseMSOswilllikelydeploy(RemotePHY)RPHYor(RemoteMACPHY)RMACPHYsub-systemswithintheirnodes.OtherMSOswillwanttopreservemuchoftheircurrentarchitectureswhilecapitalizingonimprovedtechnologies.

Inordertocalibrateourconceptualthinkingagainstreality,asetoffivereal-lifeHFCnodeswasidentifiedforevaluation,representingadiversityofimplementations.Thesearerepresentativeoflow,medium,andhighdensities,asmeasuredbyhowmanyhomesarepassedpermileineacharea.Thefivenodeareas,labeledA,B,C,D,&Epossessotherattributesofinterest:milesofhardlinecoaxplant,percentageofaerialplant,numberofRFactives,numberofhomespassedpernode,andHP/mile,asshowninTable3.

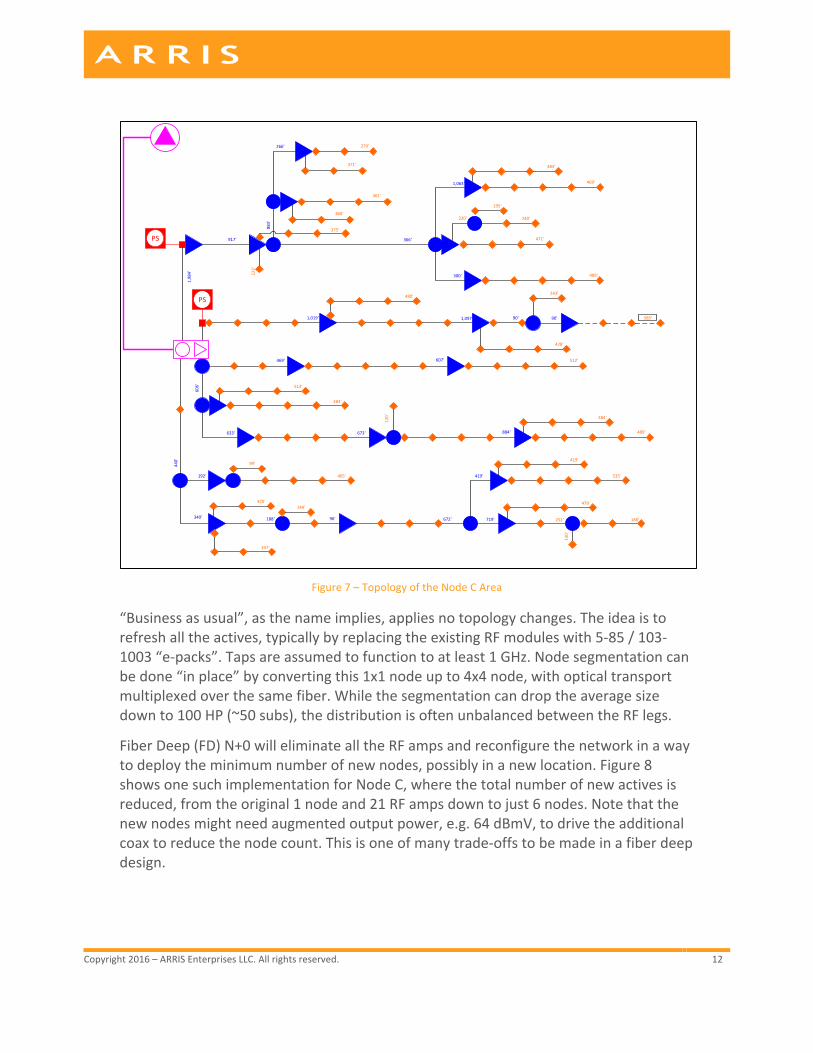

Figure7showsthetopologyofoneofthenodes:NodeC.Theheadend(upperleft)isfiber-linkedtothenode(center-leftinpink),whichRF-feedsintoRFamps(bluetriangles)RFsplitters(bluecircles),andtaps(orangediamonds).Two15Afieldpowersuppliesprovideenoughpowerforthewholenodearea.NodeCcontains3.5milesof

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 11

coaxplant(excludingdropcables)with21activesand398HomesPassed(HP).Sothismightrepresent~200subscribers@50%penetration.

NodeCwillbeusedasabaselineexampletoshowhowtheotherarchitecturesmightbeimplemented.

Table3–Propertiesof5NodeAreasUnderStudy

Node A B C D E Overall Average

Plant Coax Mileage 4.2 6.2 3.5 2.5 1.9 18.3 3.7

% Aerial 20% 77% 97% 87% 91% 70% 70%

Total Active 21 30 21 19 14 105 21

Actives/Mile 5.0 4.9 5.9 7.6 7.4 5.7 5.7

Cascade Depth N+3 N+3 N+3 N+3 N+2 N+3

Total Homes Passed 153 352 398 469 520 1892 378

HP/Mile 37 57 112 187 274 104 104

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 12

Figure7–TopologyoftheNodeCArea

“Businessasusual”,asthenameimplies,appliesnotopologychanges.Theideaistorefreshalltheactives,typicallybyreplacingtheexistingRFmoduleswith5-85/103-1003“e-packs”.Tapsareassumedtofunctiontoatleast1GHz.Nodesegmentationcanbedone“inplace”byconvertingthis1x1nodeupto4x4node,withopticaltransportmultiplexedoverthesamefiber.Whilethesegmentationcandroptheaveragesizedownto100HP(~50subs),thedistributionisoftenunbalancedbetweentheRFlegs.

FiberDeep(FD)N+0willeliminatealltheRFampsandreconfigurethenetworkinawaytodeploytheminimumnumberofnewnodes,possiblyinanewlocation.Figure8showsonesuchimplementationforNodeC,wherethetotalnumberofnewactivesisreduced,fromtheoriginal1nodeand21RFampsdowntojust6nodes.Notethatthenewnodesmightneedaugmentedoutputpower,e.g.64dBmV,todrivetheadditionalcoaxtoreducethenodecount.Thisisoneofmanytrade-offstobemadeinafiberdeepdesign.

512'607'469'

483'

513'

606'

633' 673'

120'

884' 489'

484'

192' 465'

99'

340'

440'

188' 96' 672' 719' 188'252'

130'

479'

419'

419'

535'

144'470'

337'

1,019' 1,097' 90' 90'

243'

585'

428'

480'

1,984'

917' 366'

1,063' 469'

483'

300' 489'

471'

220'

195'

240'

883'

361'

360'

266' 279'

371'

PS

PS

375'

123'

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 13

Figure8–NodeCAreaReconfiguredasFiberDeepN+0

Inadditiontothenewfiberrequiredtofeedthosenodes,thereisaneedtoaddsomecoaxplant,too.Thenewcoaxsegmentsareshowningreen.Asignificantredesignofthetapvaluesandorientationsisrequired,too.However,ifanoperatoralreadyplanstoupgradethetapsto1.2GHzperformance,thentheargumentisthetapreworkmaynotbesoonerousofanextrastep.Theadditionalnewfibertoconnectthenewnodesisthereasonthisapproachiscalled“FiberDeep”.ForFDN+0inNodeC,thissteptakesfibertoascloseas195feettothelasttap,whilethefurthesttapisat1,448feet.Onaverage,tapsare1,007feetawayfromthefiberplant.ThenewnodesarealsocapableofhousingRemotePHYDevices(RPDs)andPONOLTs,ifandwhenneeded.

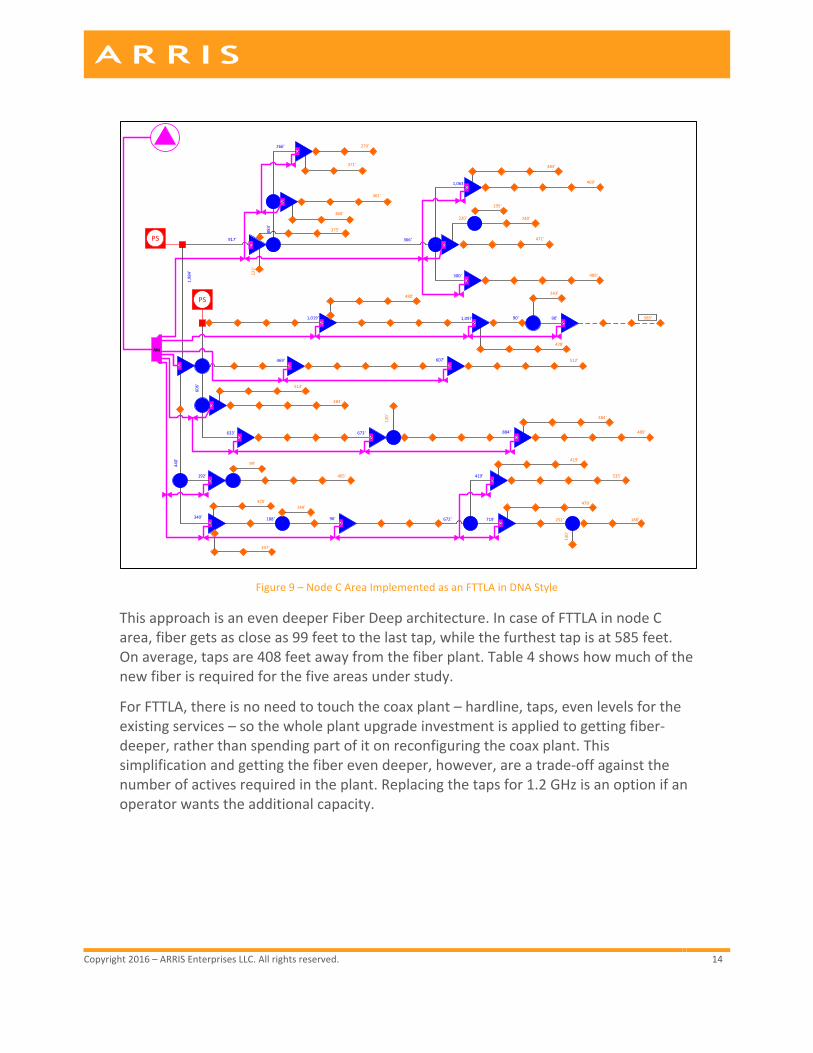

Fibertothelastactive(FTTLA)isalsoanN+0implementation.However,thenumberofactivesisnotminimized.Rather,thelocations(andeventhehousings,ifwarranted)oftheexistingRFactivesarepreserved–andreservedforthelast-activenodes.Figure9showstopologyofsuchanetwork,ifimplementedforNodeC.Thisresultsin21nodesforthisdesignreplacingtheoriginalactives.

131'NewCoax

633' 489'

484'

465'

99'

719' 188'

130'

419'

419'

535'

470'

337'

585'

480'

401'NewCoax

946'NewCoax

PowerOnly

PSPS

123'NewCoaxSS

300'

NewCoax

360'NewCoax

S

S

S816'NewCoax

120'NewCoax

872'NewCoax

240'NewCoax

S

Note:PSLocationdidnotchange

426'NewCoax

S

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 14

Figure9–NodeCAreaImplementedasanFTTLAinDNAStyle

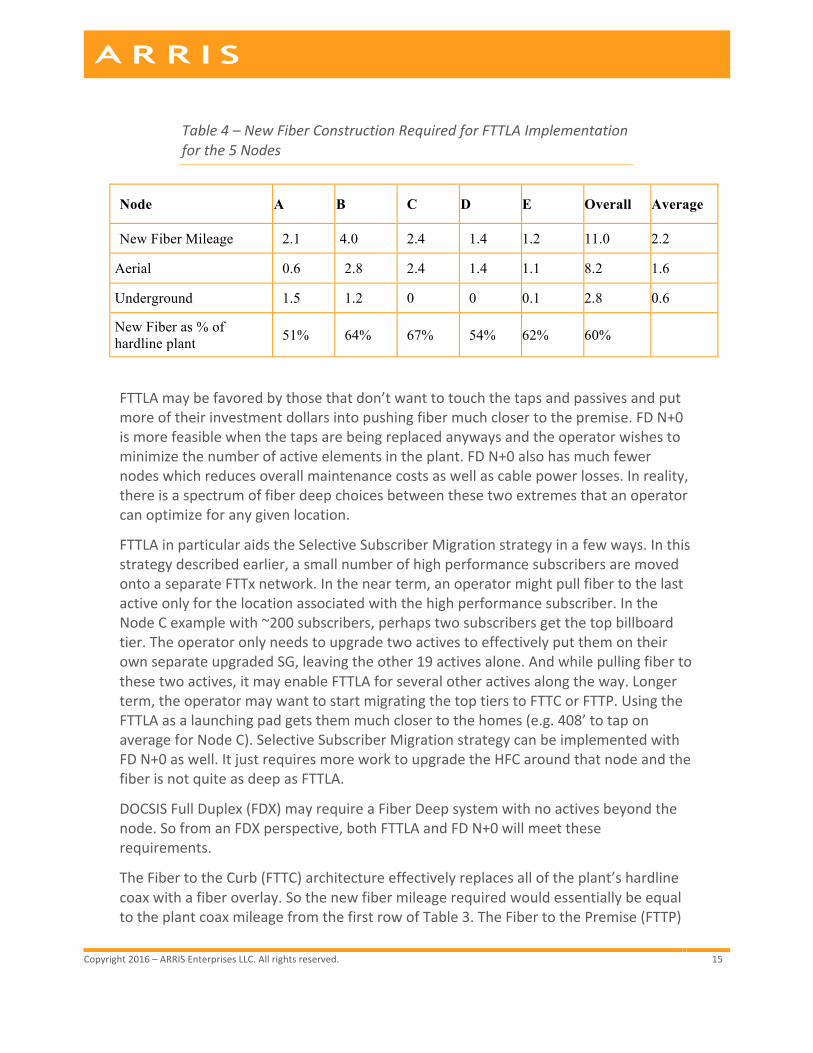

ThisapproachisanevendeeperFiberDeeparchitecture.IncaseofFTTLAinnodeCarea,fibergetsascloseas99feettothelasttap,whilethefurthesttapisat585feet.Onaverage,tapsare408feetawayfromthefiberplant.Table4showshowmuchofthenewfiberisrequiredforthefiveareasunderstudy.

ForFTTLA,thereisnoneedtotouchthecoaxplant–hardline,taps,evenlevelsfortheexistingservices–sothewholeplantupgradeinvestmentisappliedtogettingfiber-deeper,ratherthanspendingpartofitonreconfiguringthecoaxplant.Thissimplificationandgettingthefiberevendeeper,however,areatrade-offagainstthenumberofactivesrequiredintheplant.Replacingthetapsfor1.2GHzisanoptionifanoperatorwantstheadditionalcapacity.

512'607'469'

483'

513'

606'

633' 673'

120'

884' 489'

484'

192' 465'

99'

340'

440'

188' 96' 672' 719' 188'252'

130'

479'

419'

419'

535'

144'470'

337'

1,019' 1,097' 90' 90'

243'

585'

428'

480'

1,984'

917' 366'

1,063' 469'

483'

300' 489'

471'

220'

195'

240'

883'

361'

360'

266' 279'

371'

AM

PS

PS

375'

123'

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 15

Table4–NewFiberConstructionRequiredforFTTLAImplementationforthe5Nodes

Node A B C D E Overall Average

New Fiber Mileage 2.1 4.0 2.4 1.4 1.2 11.0 2.2

Aerial 0.6 2.8 2.4 1.4 1.1 8.2 1.6

Underground 1.5 1.2 0 0 0.1 2.8 0.6

New Fiber as % of hardline plant 51% 64% 67% 54% 62% 60%

FTTLAmaybefavoredbythosethatdon’twanttotouchthetapsandpassivesandputmoreoftheirinvestmentdollarsintopushingfibermuchclosertothepremise.FDN+0ismorefeasiblewhenthetapsarebeingreplacedanywaysandtheoperatorwishestominimizethenumberofactiveelementsintheplant.FDN+0alsohasmuchfewernodeswhichreducesoverallmaintenancecostsaswellascablepowerlosses.Inreality,thereisaspectrumoffiberdeepchoicesbetweenthesetwoextremesthatanoperatorcanoptimizeforanygivenlocation.

FTTLAinparticularaidstheSelectiveSubscriberMigrationstrategyinafewways.Inthisstrategydescribedearlier,asmallnumberofhighperformancesubscribersaremovedontoaseparateFTTxnetwork.Inthenearterm,anoperatormightpullfibertothelastactiveonlyforthelocationassociatedwiththehighperformancesubscriber.IntheNodeCexamplewith~200subscribers,perhapstwosubscribersgetthetopbillboardtier.TheoperatoronlyneedstoupgradetwoactivestoeffectivelyputthemontheirownseparateupgradedSG,leavingtheother19activesalone.Andwhilepullingfibertothesetwoactives,itmayenableFTTLAforseveralotheractivesalongtheway.Longerterm,theoperatormaywanttostartmigratingthetoptierstoFTTCorFTTP.UsingtheFTTLAasalaunchingpadgetsthemmuchclosertothehomes(e.g.408’totaponaverageforNodeC).SelectiveSubscriberMigrationstrategycanbeimplementedwithFDN+0aswell.ItjustrequiresmoreworktoupgradetheHFCaroundthatnodeandthefiberisnotquiteasdeepasFTTLA.

DOCSISFullDuplex(FDX)mayrequireaFiberDeepsystemwithnoactivesbeyondthenode.SofromanFDXperspective,bothFTTLAandFDN+0willmeettheserequirements.

TheFibertotheCurb(FTTC)architectureeffectivelyreplacesalloftheplant’shardlinecoaxwithafiberoverlay.SothenewfibermileagerequiredwouldessentiallybeequaltotheplantcoaxmileagefromthefirstrowofTable3.TheFibertothePremise(FTTP)

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 16

architecturewouldrequirealloftheFTTCfiberplusthedropcableforeachsubscriber.NopictureisneededasthesesimplyoverlaytheexistingHFCcoaxwithfiber.

ACCESSNETWORKUPGRADEOPTIONS:COSTIMPACTSAswasnotedin[VENK_2015],gettingfiberdeepisajourney,notasingleevent.Venkshowsthatatcurrentplantinvestmentrates,itwilltakeatleastseveraldecadestoachieveFTTPeverywhere.Soitisaslowandsteadyevolution,asopposedtoarevolution.ThisnextsectiontakesalookatthecostimplicationsforthevariousHFCupgradeoptions.ItfirstreviewssomepreviousfindingsoncomparingFTTHdeploymentsvs.“Businessasusual”(BAU),HFCupgrades.Thepaperthenlooksatthecostimpactsforeachupgradeoptionforthefivenodeareasunderstudy.

HFCBAUvFTTH–PreviousFindingsTherehasbeenextensiveanalysisdonepreviouslyin[EMM_2016,EMM_2015]oncomparinginvestmentsintoHFCwithacompleteswitchtoafullFibertotheHome(FTTH)overlayinexistingbrownfieldareas.Thesereportstakealookattheentiresystemcostfromheadendfacilitycosts,toplantinvestments,andincludesthehome/CPEinvestmentsaswell.

Twoseparatebusinessmodelsarediscussedtooffer1Gservicesacrosstheoperator’sfootprint.Thefirstapproachisknownassystemwideandthesecondisknownassuccessbasedbuilds.Thesystemwideapproachisusedforgreenfieldbuildsandmayalsobeusedforbrownfieldoverbuilds.Itskeyadvantageisthatitofferstheservicesacrossanoperator’sentirefootprint.Ifanycustomercallstogettheservice,itcanbeturnedonrapidly.Thisrequiresthattheoperatorbuildoutenoughoftheplanttoenablethisservice.Thisisknownastheenablementcosts.Oncethecustomercallstoobtaintheservice,thereareadditionalcostssuchasthetruckroll,CPEcosts,andthefiberdropinstallationforFTTH.Thesearereferredtoassuccess-basedcosts.

Forthesuccessbasedapproach,noenablementcostsareincurredinadvance.Itisonlyoncethecustomerorderstheservicethattheplantisbuiltoutandtheothersuccess-basedcostsareshouldered.Thekeybenefithereisthatitsavestheoperatortremendousupfrontinvestment,butitnowrequiresapotentiallylengthyperiodtoinstallandactivateservices.Thisismoreeffectivewhenthepenetrationrateontheseservicesareverylow.

DescribedlaterinthispaperisamiddlegroundapproachthatcanbereachedonthesetwobusinessmodelsusingfiberdeeptechnologysuchasFDN+0orFTTLA.FiberdeepHFCisasystemwideapproachforofferingsymmetricgigabitserviceswithoutthetotal

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 17

costofFTTP.Butitalsoenablesasuccess-basedFTTPapproachsincethefiberispulledmuchclosertoeveryhomes(e.g.lessthan1000’).Sointhissense,itbecomesablendofthetwoapproachesdescribedbyEmmendorfer.

Figure10showsthreedifferentusecasesfrom[EMM2016].Usecases1and2areasimpleupgradetoDOCSIS3.1intheCMTS/CCAPplatform.Thisonlyimpactstheheadendfacilitytoenable1GservicesacrosstheentireHFCfootprint.TheD3.1upgradeistheenablementcosts.ThesuccesscapitalincludesthecostoftheD3.1modemalongwithatruckrolltoinstallit.

UseCase3inFigure10upgradestheHFCinadditiontotheD3.1CMTS/CCAPupgrade.TheHFCisupgradedto1002/85MHz.Thenodeisalsosplitandasmallamountoffiberisalsoinstalled.Theenablementcostsriseaccordinglywhilethesuccessbasedcapitalremainsunchanged.

UseCase4looksata10GEPONFTTHsolution.TheenablementcostsincludetheOLTinthefacilityalongwiththecostofbuildingoutfibertoeveryneighborhood.Thefibercostsdominate.Thefiberisnowcloseenoughtothehometoallowatimelyinstallationonceacustomerorderstheservice.Thesuccess-basedcapitalismoreexpensiveforthisapproachasitalsoincludestheinstallationofthefiberdropcabletothehome.

UseCase1and2:HFC2GDOCSIS

UseCase3:HFCMid-split2Gx500MDOCSIS

$40EnablementCapitalPerHouseholdsPassed $235SuccessCapital

fiber coax

HybridFiberCoax(HFC)Node

HFCAmplifiersandPassives

CoaxDrop

Telephone

fiber

Headend

coax

DOCSISCMTS

OpKcalTransport

coax

OutsidePlantFacility Subscriber

BrownfieldassumesexisKngvideodeliverynetworkused

EMTAGW

EmbeddedMulKmediaTerminalAdapter(EMTA)&Gateway(GW)BrownfieldAssumesLeveragingExisKngDigitalCableSTB

DOCSIS3.032x8

$145EnablementCapitalPerHouseholdsPassed $235SuccessCapital

fiber coax

HybridFiberCoax(HFC)Node

HFCAmplifiersandPassives

fiber

Headend

DOCSISCMTS

OpKcalTransport

coax

OutsidePlantFacility Subscriber

BrownfieldassumesexisKngvideodeliverynetworkused

CoaxDrop

EmbeddedMulKmediaTerminalAdapter(EMTA)&Gateway(GW)BrownfieldAssumesLeveragingExisKngDigitalCableSTB

DOCSIS3.032x8andDOCSIS3.1DS2x192MHzandUS2x96MHz

Telephone

coaxEMTAGW

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 18

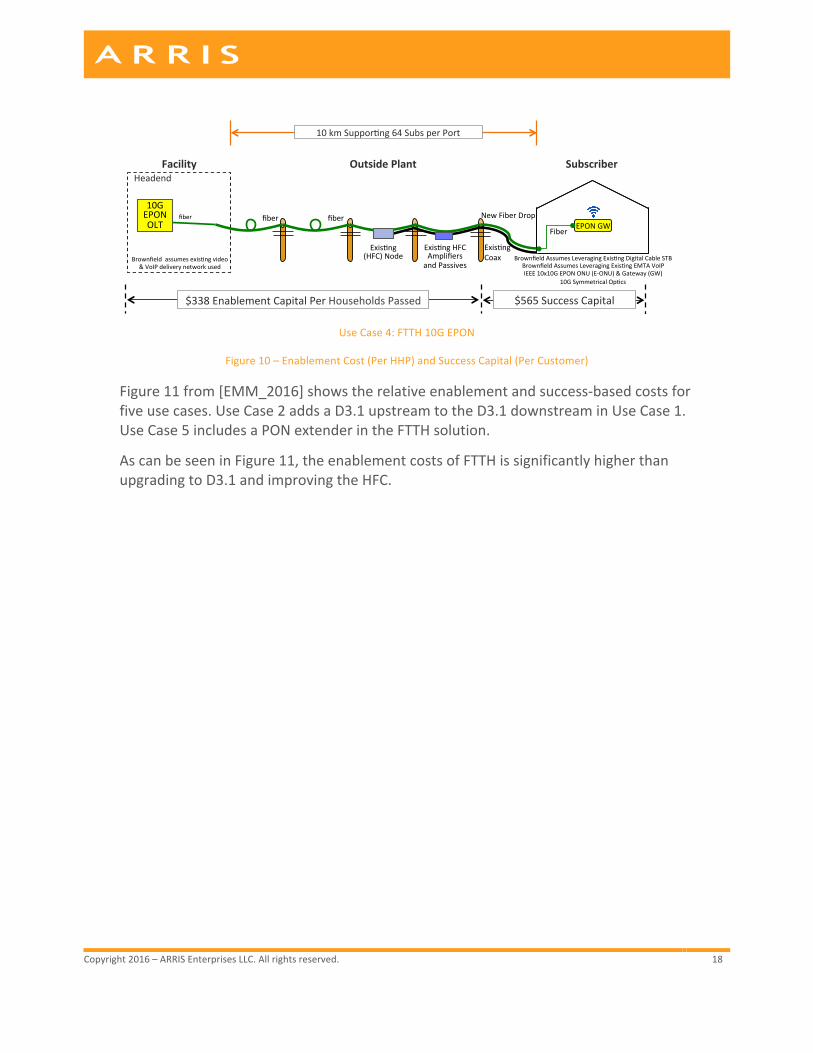

UseCase4:FTTH10GEPON

Figure10–EnablementCost(PerHHP)andSuccessCapital(PerCustomer)

Figure11from[EMM_2016]showstherelativeenablementandsuccess-basedcostsforfiveusecases.UseCase2addsaD3.1upstreamtotheD3.1downstreaminUseCase1.UseCase5includesaPONextenderintheFTTHsolution.

AscanbeseeninFigure11,theenablementcostsofFTTHissignificantlyhigherthanupgradingtoD3.1andimprovingtheHFC.

$338EnablementCapitalPerHouseholdsPassed $565SuccessCapital

fiber NewFiberDropfiber

Headend

10GEPONOLT

OutsidePlantFacility Subscriber

fiber

ExisHng(HFC)Node

ExisHngHFCAmplifiersandPassives

ExisHngCoaxBrownfieldassumesexisHngvideo

&VoIPdeliverynetworkused

EPONGWFiber

10GSymmetricalOpHcs

BrownfieldAssumesLeveragingExisHngEMTAVoIPBrownfieldAssumesLeveragingExisHngDigitalCableSTB

IEEE10x10GEPONONU(E-ONU)&Gateway(GW)

10kmSupporHng64SubsperPort

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 19

EnablementCapitalComposition(PerHHP)

SuccessCapitalComposition(PerCustomer)

Figure11–CostComparison:EnablementandSuccessBased

CostComparisonofVariousHFCUpgradeOptionsHFCplantsvarysignificantly.Notonlydotheyvaryoperatortooperator,buttheircharacteristicscanvarydramaticallyfromnodetonodewithinthesamecommunity.Thecostanalysisin[EMM_2016]wasdoneononeparticularsamplenodewhosecharacteristicsaredescribedinthatpaper,andforonetypeofHFCupgrade.

OneofthekeyconsiderationsforthispaperwastoinvestigatetheimpactofthesevariousHFCarchitectureupgradesacrossaverywidespectrumofnodes.AswasshowninTable3,thefivenodesunderstudyvariedfromaveryrural37HP/miletoaverydenseurbansettingof274HP/mile.Thiscandramaticallyimpactthecostofupgrades.

$-

$100.00

$200.00

$300.00

$400.00

$500.00

$600.00

UseCase1:HFC2GDOCSIS

UseCase2:HFC2Gx200MDOCSIS

UseCase3:HFCMid-split2Gx500M

DOCSIS

UseCase4:FTTH10GEPON

UseCase5:FTTH10GEPON+PON

Extender

OSPLabor

OSPMaterials

OSPEquipment

FacilityLabor

FacilityEquipment

$-

$100.00

$200.00

$300.00

$400.00

$500.00

$600.00

UseCase1:HFC2GDOCSIS

UseCase2:HFC2Gx200MDOCSIS

UseCase3:HFCMid-split2Gx500M

DOCSIS

UseCase4:FTTH10GEPON

UseCase5:FTTH10GEPON+PON

Extender

DropLabor

DropMaterials

In-homeLabor

In-homeEquipment

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 20

Inthissection,thefocusisonanalyzingvariousHFCupgradeoptionsforthefivenodesunderstudy.Ittakesalookatthefollowingupgradescenarios:

1. UpgradingHFCactivesto1002/85MHzwithouttouchingthetapsandpassives2. UpgradingHFCactives,tapsandpassivesto1218/85MHz3. UpgradingHFCactivesto1002/85MHz;add2nd&3rdnode;don’ttouch

taps/passives4. UpgradingHFCactives,tapsandpassivesto1218/85MHz;add2nd&3rdnode5. UpgradingHFCtoFTTLAwithouttouchingthetapsandpassives6. UpgradingHFCtoFTTLAwithnewtaps/passives

Figure12showstherelativecostsforthesesixscenarios.Foreachscenario,itshowstherangeofcostsacrossthefivenodesunderstudyalongwiththeaveragecostsacrossthefivenodes.

Figure12–RelativeCostperMileforVariousHFCUpgradeOptions

Relativecostsareusedsincelaborisasignificantcostvariableandvariestremendouslyfromlocationtolocation.Theaveragecostforscenario1wasarbitrarilychosentoequal100.Tonosurprise,theaveragecostsincreaseasfiberispusheddeeperintothenetwork.Andascanbeseenfromscenarios2,4,and6,touchingthetapsnotonlyaddsadditionalexpense,butthevariabilityincreasessignificantlyaswell.

ForFTTLAinFigure12,thefiberinstallationcostsaresignificantandpulledoutseparately.The“FTTLA,noTaps/Fiber”andthe“FTTLA+Taps,noFiber”includeseverythingexceptanycostsassociatedwiththefiberinstallation.TheFTTLAfiber

0

100

200

300

400

500

600

1GHzonly 1.2GHz+Taps

1GHz+3*N 1.2GHz+3*N

FTTLA,noTaps/Fiber

FTTLA+Taps,noFiber

FTTLAFiberOnly

Relativ

eCo

st/Mile

HFCUpgradeOptions

Min Max Avg

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 21

installationcostsareshownseparatelyontherightinFigure12.Thefiberinstallationcostsvarydramaticallyonwhethertheplantisaerialorunderground.Inthisstudy,theundergroundfiberinstallationcostswerealmost8Xthatofaerial.Separatingthefiberinstallationcomponentwilllettheoperatormoreeasilyapplytheseresultstotheirownscenarios.

Theupgradecostsarenottheonlystoryhere.Asfiberispulleddeeperandmorenodesareinstalled,theoverallsystemcapacityisincreasing.Thetotalsystemcapacityisafunctionofboththenumberofnodes(i.e.potentialDOCSISSG)andthecapacityofeachlink.Figure13showsboththeaverageplantupgradecostsandthetotalsystemcapacityforeachscenario.Inthisfigure,theFTTLAscenariosincludetheassociatedfiberinstallationcosts.

Figure13–RelativeCostandCapacityforVariousHFCUpgradeOptions

Figure13alsoincludesaFTTPscenariowith10GEPON.Thisrepresentstheexpectedaveragecostofinstallingthefiber.ThisdoesnotincludeOLTorONUcostsandtheirinstallation.NotethatthetotalsystemcapacityforFTTLAwithupdatedtapsisidenticalto10GEPON.Bothofferidenticallinkcapacityof~8.6Gbpsandprovideforabout30to60homespassedperservinggroup.

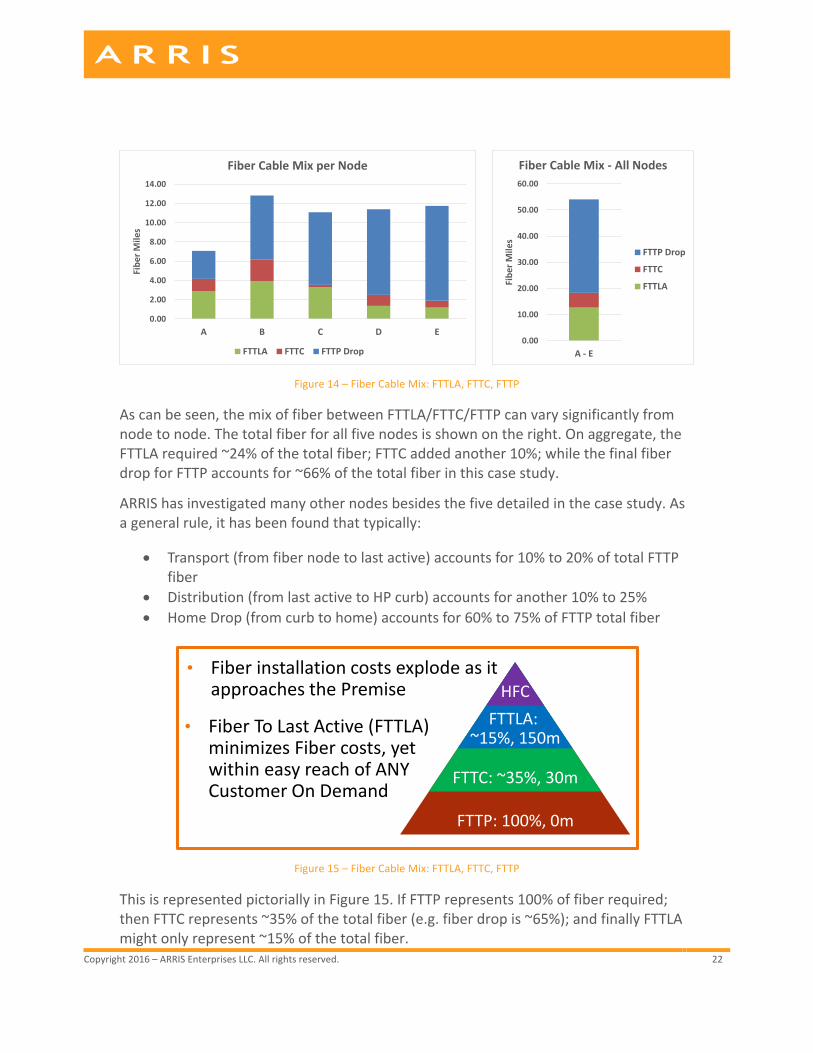

FiberinstallationisalargevariableincomparingthesevariousFiberDeepapproaches.Foreachnodeinthecasestudy,howmuchfiberneedstobeinstalledforFTTLA,FTTC,andFTTHsystemswasanalyzed.ThisisshowninFigure14.TheFTTCandFTTPshowtheincrementaladditionalfiberrequired.

0

2

4

6

8

10

12

1GHzonly 1.2GHz+Taps

1GHz+3*N 1.2GHz+3*N FTTLA,noTaps

FTTLA+Taps FTTP-10GEPON

Relativ

eto

1GH

zUpgrade

HFCUpgradeOptions-CostandDownstreamCapacity

AvgPlantCosts TotalSystemCapacity

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 22

Figure14–FiberCableMix:FTTLA,FTTC,FTTP

Ascanbeseen,themixoffiberbetweenFTTLA/FTTC/FTTPcanvarysignificantlyfromnodetonode.Thetotalfiberforallfivenodesisshownontheright.Onaggregate,theFTTLArequired~24%ofthetotalfiber;FTTCaddedanother10%;whilethefinalfiberdropforFTTPaccountsfor~66%ofthetotalfiberinthiscasestudy.

ARRIShasinvestigatedmanyothernodesbesidesthefivedetailedinthecasestudy.Asageneralrule,ithasbeenfoundthattypically:

• Transport(fromfibernodetolastactive)accountsfor10%to20%oftotalFTTPfiber

• Distribution(fromlastactivetoHPcurb)accountsforanother10%to25%• HomeDrop(fromcurbtohome)accountsfor60%to75%ofFTTPtotalfiber

Figure15–FiberCableMix:FTTLA,FTTC,FTTP

ThisisrepresentedpictoriallyinFigure15.IfFTTPrepresents100%offiberrequired;thenFTTCrepresents~35%ofthetotalfiber(e.g.fiberdropis~65%);andfinallyFTTLAmightonlyrepresent~15%ofthetotalfiber.

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

A B C D E

Fibe

rMiles

FiberCableMixperNode

FTTLA FTTC FTTPDrop0.00

10.00

20.00

30.00

40.00

50.00

60.00

A-E

Fibe

rMiles

FiberCableMix- AllNodes

FTTPDrop

FTTC

FTTLA

• FiberinstallationcostsexplodeasitapproachesthePremise

FTTP:100%,0m

FTTC:~35%,30m

FTTLA:~15%,150m

HFC

• FiberToLastActive(FTTLA)minimizesFibercosts,yetwithineasyreachofANYCustomerOnDemand

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 23

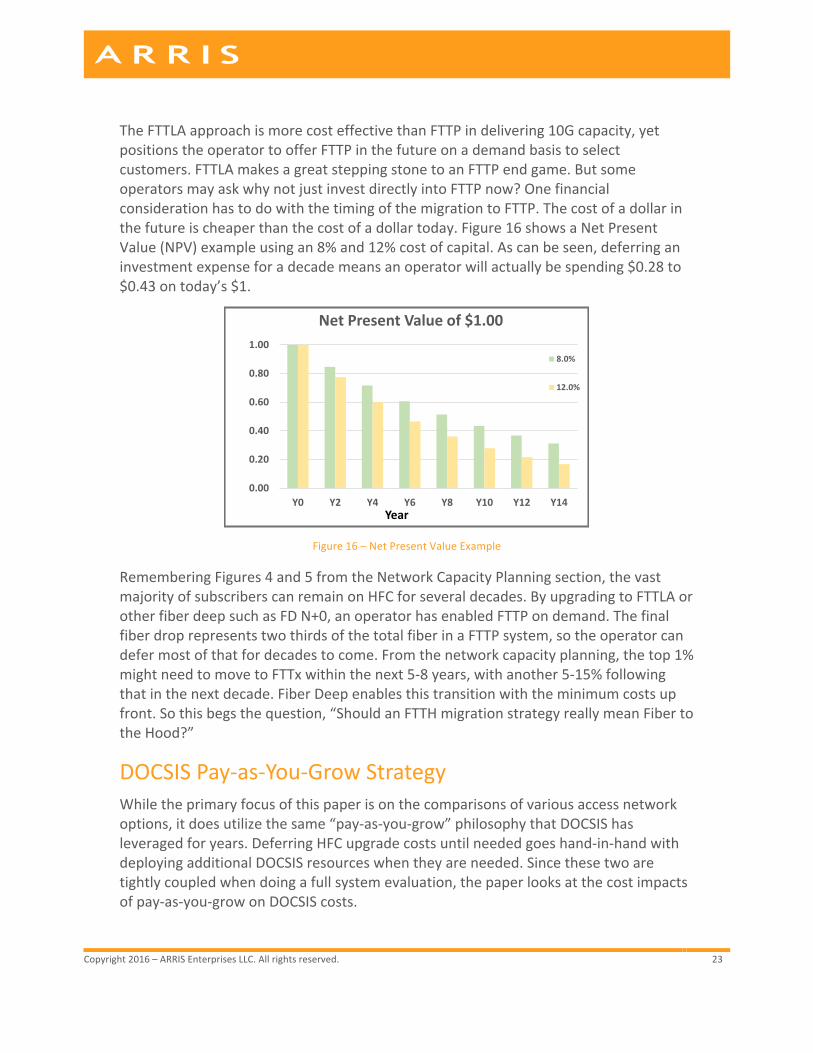

TheFTTLAapproachismorecosteffectivethanFTTPindelivering10Gcapacity,yetpositionstheoperatortoofferFTTPinthefutureonademandbasistoselectcustomers.FTTLAmakesagreatsteppingstonetoanFTTPendgame.ButsomeoperatorsmayaskwhynotjustinvestdirectlyintoFTTPnow?OnefinancialconsiderationhastodowiththetimingofthemigrationtoFTTP.Thecostofadollarinthefutureischeaperthanthecostofadollartoday.Figure16showsaNetPresentValue(NPV)exampleusingan8%and12%costofcapital.Ascanbeseen,deferringaninvestmentexpenseforadecademeansanoperatorwillactuallybespending$0.28to$0.43ontoday’s$1.

Figure16–NetPresentValueExample

RememberingFigures4and5fromtheNetworkCapacityPlanningsection,thevastmajorityofsubscriberscanremainonHFCforseveraldecades.ByupgradingtoFTTLAorotherfiberdeepsuchasFDN+0,anoperatorhasenabledFTTPondemand.ThefinalfiberdroprepresentstwothirdsofthetotalfiberinaFTTPsystem,sotheoperatorcandefermostofthatfordecadestocome.Fromthenetworkcapacityplanning,thetop1%mightneedtomovetoFTTxwithinthenext5-8years,withanother5-15%followingthatinthenextdecade.FiberDeepenablesthistransitionwiththeminimumcostsupfront.Sothisbegsthequestion,“ShouldanFTTHmigrationstrategyreallymeanFibertotheHood?”

DOCSISPay-as-You-GrowStrategyWhiletheprimaryfocusofthispaperisonthecomparisonsofvariousaccessnetworkoptions,itdoesutilizethesame“pay-as-you-grow”philosophythatDOCSIShasleveragedforyears.DeferringHFCupgradecostsuntilneededgoeshand-in-handwithdeployingadditionalDOCSISresourceswhentheyareneeded.Sincethesetwoaretightlycoupledwhendoingafullsystemevaluation,thepaperlooksatthecostimpactsofpay-as-you-growonDOCSIScosts.

0.00

0.20

0.40

0.60

0.80

1.00

Y0 Y2 Y4 Y6 Y8 Y10 Y12 Y14Year

NetPresentValueof$1.00

8.0%

12.0%

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 24

ThisphilosophyreallytookholdwiththeadventofDOCSIS3.0andchannelbonding.DOCSIShasembracedapay-as-you-growmentalitysincethen.Itbasicallysaystoinstallenoughcapacitynowtosatisfycustomerrequirements;thengrowcapacitylaterleveragingnewertechnologyandinnovations.Somefactorsthatallowthisworkinclude:

• Minimizeinitialup-frontinvestments• Addadditionalcapacityonlywhenandasmuchasyouneed• Takeadvantageofreducingcostsovertime

Figure17providesahistoricalperspectiveonCMTS/CCAPcostsoverthelastdecade.ThisisfromdatathathasbeencollectedovertheyearsbyInfonetics[IHS_2010-16].ThechartontheleftshowsCMTSrevenueperdownstreamchanneloverthelastdecade.Itisshownonalogscalebecauseofthemagnitudeandalsotoshowtheconsistentdecreaseinprices.

Figure17–CMTS/CCAPCosts–HistoricalPerspective

ThechartontherightinFigure17zoomsinonthelast5yearsandshowsseveralproductsincluding:CMTS,CCAP,EQAM,andCMC.TherevenueperdownstreamDOCSISchannelhasdropped~25%peryearoverlast5years.Thisisdownfrom~32%peryearforprevious5years.EventherelativelymatureEQAMmarkethasdropped~13%peryearoverlast5years.

WillDOCSISrevenueperdownstreamchannelcontinuetodecline?Asanystockbrokerwilltellyou,itisimpossibletopredictfuturepricesbasedonpastperformances.Togetahandleonthisitisimportanttoconsider:IsDOCSIStechnologymaturingorisitinnovating?Ifitismaturing,thentherateofdeclinemayslow.Ifitisinnovating,thennewtechnologiescanfuelfurtherdecreases.LookingatrecentDOCSIStechnologies,DOCSIS3.1isnowenteringitsproductionphaseandwilldramaticallyincreaseDOCSIScapacityfrom1Gbpsto10Gbps.

Additionally,therearealotofotherinnovationsgoingonintheDOCSISworld.NewdistributedarchitecturessuchasRemotePHY,RemoteMACPHY,andRemoteCCAParebringingnewsolutionsandnewcompetitorstotheDOCSISworld.Thereisasignificant

$100

$1,000

$10,000

CY05 CY07 CY09 CY11 CY13 CY15

CMTSRevenueperDownstreamChannel-10yrView

$0

$200

$400

$600

$800

$1,000

$1,200

CY11 CY12 CY13 CY14 CY15

RevenueperDownstreamChannel- 5yearview

CMTS CCAP CMC EdgeQAM

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 25

effortatCableLabstofinalizetheDOCSISFull-duplexspecification.ThisissignificantasitenablessymmetricGbpsservices.ItalsorequiresanN+0/FTTLAplantforoperation.Andwithfiberpushingdeeper,DOCSISwillalsoseespectrumextendedasdescribedin[CLOONAN_2016].FTTLAcouldenable25GbpsDOCSISsystemswhileFTTCmightenable100Gbpsorhigher.

Finally,muchindustryworkisgoingintoSoftwareDefinedNetworks(SDN)andNetworkFunctionVirtualization(NFV).ThiswillhelpdrivethevirtualizationofDOCSISplatforms.

DOCSIShasseenmoreinnovationinlastcoupleyearsthanprevioustwodecadescombined.ThisshouldhelpcontinuethedownwardpressureonDOCSIScosts.

So,whatisthecostimpactofthispay-as-you-growphilosophy?Toanalyzethis,ahypotheticalcaseisconsideredthatstartswith16-bonded3.0channelsinYear0.TheDOCSIScapacityisthenroughlydoubledeveryotheryeartokeepupwithnetworktrafficgrowthasdescribedearlierinthispaper.Attheendof8years,theDOCSISsystemhasreached32-bonded3.0channelswith4x192MHzOFDMchannels.Thisrepresentsadatarateof~8.6Gbpswhichispracticallyidenticalto10GEPON.ThiscapacitygrowthisshowninFigure18.Thecapacityhasgrownbyafactorof14overthe8years.

Figure18–DOCSISCapacityMigrationExample

AscanbeseeninFigure18,mostofthenetworkcapacityisaddedinlateryears.SomemaysaythatthetotalDOCSIScostswillendupbeing14timestheYear0costsusingtoday’sDOCSISprices.Let’stakealookattheimpactoncostperbitofdelayingthosecapacitypurchases.Thisisvastlydifferentthan10GEPONwheretheentirecapacitymustbepurchasedupfront.

Therearetwoimportantfactorsthatwillaffecttheoverallcost.ThesearethecontinuingdeclineofCMTS/CCAPpricesandtheeffectofNPV.TheseareshowninFigure19.

0

2000

4000

6000

8000

10000

Y0 Y2 Y4 Y6 Y8

Mbp

s

Year

DOCSISCapacityoverTime

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 26

Figure19–DOCSISChannelCosts,NPVOveran8YearPeriod

ForfutureDOCSIScosts,arangeofvaluesareconsidered.Ononeend,acontinuationofthe25%peryeardeclineisassumed.Ontheotherend,aslowingto15%peryearisused,similartowhathasbeenexperiencedintheEQAMmarket.ThisisshownontheleftofFigure18.NotethatbyYear8whenthelargestamountofDOCSIScapacityisadded,DOCSISChannelcostsareprojectedtobe10%to27%oftheoriginalYear0costs.

TherighthandsideofFigure19showsthecostimpactofNPVfor8%and12%costofcapital.NotethatbyYear8,theNPVisbetween$0.36and$0.51ontoday’s$1.BothofthesefactorsworktogethertoreducethecostperbitofDOCSIS.ThiscausestherelativecostperDOCSISbittofallasshownontherightinFigure20.Onecaselooksat15%ayearDOCSISpricedeclineswith8%costofcapitalwhiletheothercaseuses25%ayearand12%respectively.ByYear8,therelativecostperDOCSISbitintoday’sdollarshasfallentosomewherebetween4%and14%oftheoriginalcostforthelargestpurchasesofDOCSISresources.

Figure20–DOCSISWeightedCostperBit

TheweightedaverageoftheDOCSISinvestmentsovertheentireeightyearperiodisshownontheleftinFigure20.Theinitialinvestmentof16DOCSISchannelsinYear0isusedasabaselineandassignedavalueof100.IftheentireDOCSIScapacityis

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Y0 Y2 Y4 Y6 Y8Year

DSDOCSISChannelCostsoverTime

15.0%

25.0%

0.00

0.20

0.40

0.60

0.80

1.00

Y0 Y2 Y4 Y6 Y8Year

NetPresentValueof$1.00

8.0%

12.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Y0 Y2 Y4 Y6 Y8Year

RelativeCostperBit

15%/8%

25%/12%

100

1,435

643

395

0

250

500

750

1000

1250

1500

TotalInvestmentFactoringCostDeclines&NPV

Initial=100

0%/0%

15%/8%

25%/12%

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 27

purchasedupfrontinYear0,itwouldcostmorethan14Xtheinitialinvestment.However,factoringdownstreamchannelcostreductionsandNPVreducestotalinvestmentfor8.6Gbpstotherangeof4xto6.4xtheinitialinvestment.

Thisshowsthebenefitsofpay-as-you-growoverinitialupfrontinvestmentofthefullcapacity.Somefolkswillarguethatthecostperbitismuchlessfortechnologylike10GEPON.Therearesomecaveatswiththislineofthought.Inreality,costperbitisactuallycostperbandwidthorcapacity.

Let’stakealookatthevalidityofthismetric.Fromautilizationperspective,itwasnotedthatresidentialsubscribersarebarelyconsuming1Mbpsonaverageasdiscussedearlierinthispaper.Fora32subGPONsystem,thisis~1%utilization,whilea64sub10GEPONisbeingutilizedlessthanone-halfof1%!So,isthisavalidmetricif99%+ofbitsaregoingunused?!

Whataboutpeakspeeds?Streamingvideoisthedominantresidentialapplicationtoday.AdaptiveBitRate(ABR)protocolsoperateoptimallywhengiven2-3Xaveragevideorate.Sothedominantapplication,evenwith4KUHDstreams,caneasilyhandleacoupleUHDstreamswitha100Mbpsservicetier.Theneedforwidespread2.5Gor10Gburstratesarestillonthehorizon.

WhileCostperBitisaninterestingdatapoint,oneshouldnotusethisinisolation.AlsoconsiderTotalCostofOperation(TCO)andcostpersubscriberaswellwhencomparingsolutions.

CONCLUSIONInsummary,SelectiveSubscriberMigrationstrategyisasensibleapproachforanHFCtoFTTxtransition.MovingtoptierstoFTTxcanbuyHFCextradecadesfor80-95%ofsubscribersintheflagshipbasic/economytiers.Tmaxdominatesforthenext5-7years,soitismoreimportanttoincreasetheHFCcapacitytoatleast1GHzspectrumratherthansplitnodes.However,Tavgfinallycatchesup8-10+yearsfromnow;andSGsizereductionscomebackintovogue.OperatorsshouldpushfiberdeepenoughtoenableSelectiveFTTxfortoptiersondemandandbepreparedforthenextroundofSGsplits.

Tounderstandwhatthebestoptionistoenablethismigration,thepaperanalyzedindetail5veryuniquerealnodesthatvariedfromsparseruralnodetoaverydenseurbannode.Designworkwasthendoneonthesefivenodesforeachofthefollowingscenarios:

• “Businessasusual”1GHzactivedropinupgradewithnodesplitasneeded• FiberDeep–FTTLA• FTTC• FTTP

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 28

Theresultsshowthatthereissignificantcostvariationsfromusecasetousecase.Everyoperatormustlookateachindividualscenariotodeterminewhatisbestforthatsituation.However,sometrendsdidemergethatshouldhelpguidetheoperators.ThefiberdeepapproachessuchasFTTLAprovidesomesignificantbenefitssuchas:

1. MaximizesDOCSIS3.1performancea. Datacapacitythatmatches10GbpsPON

2. ProvidesexcellentsteppingstonetoFTTPon-demanda. SelectiveSubscriberMigrationtoFTTPasneededb. Onaverage,fiberislessthan1000’fromanytap

3. ProvidesfinegranularityforoptimizingDOCSISSGsizesa. SameSGsizesasPON:~30-60homesb. MaximizeDOCSISCMTS/CCAPresources

4. Reducesmaintenance,power,andoperationalexpensescomparedtotoday’sHFC

5. Futureproofarchitecturea. N+0enablesDOCSISFull-duplex(FDX)andextendedspectrumb. ThesenewtechnologiespromisetodoforDOCSIS&cablewhatG.fastis

attemptingtodoforDSLandtwistedpair.

TheFTTLAanalysisshowsthatitisaneffectivefiberdeepFTTxmigrationstrategythatisaneconomicalsteppingstonetoFTTP.ItcanadddecadestothelifeofthevastmajorityofcustomersremainingonHFCwhileenablingaselectivemigrationofthetoptierstoFTTP.OtherN+0fiberdeepapproacheswerenotexplicitlydiscussedinthispaperbutareexpectedthattheywouldshowsimilarcostsandbenefitsasFTTLA.

ACKNOWLEDGEMENTSTheauthorswouldliketogratefullyacknowledgetheassistanceofStuartEastmanandmembersofhisteamwhohelpedimmenselywithanalyzing,dissecting,andcreatingdataandmaterialfortheusecasesthatarethebackboneofthispaper.WealsowouldliketoacknowledgeVenkMutalikforhisinputsonFTTLAandotherfiberdeeparchitecturalchoices.

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 29

ABBREVIATIONSABR AdaptiveBitRateASC ActiveSplitter-CombinerBAU BusinessasUsualBcast BroadcastBps BitsPerSecondCAA CentralizedAccessArchitectureCAGR CompoundedAnnualGrowthRateCAPEX CapitalExpenseCCAP ConvergedCableAccessPlatformCM CableModemCMTS CableModemTerminationSystemCPE ConsumerPremiseEquipmentD3.1 DataOverCableServiceInterfaceSpecification3.1DAA DistributedAccessArchitectureDCA DistributedCCAPArchitectureDEPI DownstreamExternalPHYInterfaceDNA DistributedNodeArchitectureDOCSIS DataOverCableServiceInterfaceSpecificationDS DownstreamDWDM DenseWaveDivisionMultiplexingE2E EndtoendEPON EthernetPassiveOpticalNetwork(akaGE-PON)EQAM EdgeQuadratureAmplitudeModulatorFD FiberDeepFDX FullDuplex(i.e.DOCSIS)FEC ForwarderrorcorrectionFTTC FibertotheCurbFTTH FibertotheHomeFTTLA FibertotheLastActiveFTTP FibertothePremiseFTTT FibertotheTapFTTx Fibertothe‘x’where‘x’canbeanyoftheaboveGbps GigabitsPerSecondGHz GigahertzGPON Gigabit-PassiveOpticalNetworkHFC HybridFiber-CoaxHP HomesPassedHPON HybridPassiveOpticalNetwork

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 30

HSD HighSpeedDataI-CCAP IntegratedConvergedCableAccessPlatformIEEE InstituteofElectricalandElectronicsEngineersIEQ IntegratedEdgeQAMLDPC LowDensityParityCheckFECCodeMAC MediaAccessControlinterfaceMACPHY DCAinstantiationthatplacesbothMAC&PHYintheNodeMbps MegaBitsPerSecondMDU MultipleDwellingUnitMHz MegahertzMSO MultipleSystemOperatorN+0 Node+0activesNcast NarrowcastNFV NetworkFunctionVirtualizationNPV NetPresentValueNSI NetworkSideInterfaceOBI OpticalBeatInterferenceODN OpticalDistributionNetworkOFDM OrthogonalFrequencyDivisionMultiplexingOFDMA OrthogonalFrequencyDivisionMultiplexingAccess(Upstream)OLT OpticalLineTerminationONU OpticalNetworkUnitOOB OutofBandOPEX OperatingExpenseOTT OvertheTopPHY PhysicalinterfacePNM ProactiveNetworkMaintenancePON PassiveOpticalNetworkQAM QuadratureAmplitudeModulationQoE QualityofExperienceQoS QualityofServiceRF RadiofrequencyRFoG RFOverGlassROI ReturnonInvestmentR-OLT RemoteOLTRPD RemotePHYDeviceR-MACPHY RemoteMAC-PHYR-PHY RemotePHYRX ReceiveSDN SoftwareDefinedNetworkSG ServiceGroup

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 31

SCTE SocietyofCableTelecommunicationsEngineersSNR SignaltoNoiseRatioTaFDM TimeandFrequencyDivisionMultiplexingTavg AveragebandwidthpersubscriberTCO TotalCostofOperationTmax MaximumSustainedTrafficRate–DOCSISServiceFlow

parameterTX TransmitUHD UltraHighDefinitionUS UpstreamVOD VideoondemandWDM WavelengthDivisionMultiplexing

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 32

RELATEDREADINGS• TheYinandtheYangofaMovetoAllFiber:TransformingHFCtoanAllFiber

NetworkWhileLeveragingtheDeployedHFCAssets–ThispaperprovidescriticalinsightsintotheinnovationsthatenableOBIfreeRFoGtransmissionsanddiscussesintrinsiccapabilitiesofHybridPON(HPON)technology,explaininghowthistechnologyworkswithexistingHFCanalogandQAMvideoandD3.0andD3.1signalswhilealsobeingcompletelytransparentwithtraditionalPONstandardssuchasthe10GEPON,1GEPON,GPONandXGPON1.

• PoweringPONwithHFC-AHybridforaNewGeneration–Inthepast10-15years,fiber-to-the-premises(FTTP)networkshavebeendeployedinmanyregionsoftheworld.Thispapercomparesthetotalend-to-endcostsandthroughputofthemostcommontypesofPONsanddemonstrateshowtheHFCnodecanbeusedtoenablecableoperatorstodeliverHFCandfiber-to-the-premises(FTTP)servicessimultaneouslyfromthesamenode.

• ComparingtheDOCSIS3.1andHFCEvolutiontotheFTTHRevolution–Thispaperdescriberstheexistingnetworkmigrationoptionsincludingdifferentmigrationpathsfortheexistingcoax-to-the-home(CTTH)networksupportingmoreIP/datacapacitywithDOCSIS3.0/3.1overHFC.

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 33

MEETONEOFOUREXPERTS:JohnUlmJohnUlmholdsthepositionofEngineeringFellow,BroadbandSystemsforARRISwithintheNetworkSolutionsCTOgroup.InthisroleheinvestigatesAdvancedTechnologiesforBroadbandSystemsincludingstrategictechnicaldirectionsformultiscreenservicesandbandwidthexpansion.RecentactivitiesincluderesearchintonextgenerationCCAParchitectures;HFCtoFTTxmigrationincludingHybridPON(HPON),distributedaccessarchitecturessuchasRemote-CCAPandRemote-PHY;nextgenerationprotocolsincludingDOCSIS3.1andNG-EPON;andMulti-screenIPVideosolutionsincludingmulticast-assistedABR.John’sthreedecadesintheBroadbandindustrybeganasdesigner,architect,andMACprotocoldeveloperatLANcity,pioneeringtheindustry’sfirstcablemodemsystems.HewasprimaryauthorfortheCableIndustry’sDOCSIS1.0and1.1specificationsthatdroveearlycablemodemsuccess.HealsospenttimeasNetworkProcessorarchitectforNortelandasseniortechnicalconsultanttotheBroadbandindustrywithYASCorp. JohnholdsaBSEEandMSEEfromRPIandhasamultitudeofpapersandpatentstohisname.

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 34

REFERENCES(1) [AYHAM_2014]“TheSpectralEfficiencyofDOCSIS3.1Systems,”AyhamAl-Bannaet.al.,SCTECableTecExpo’14,SCTE,2014

(2) [AYHAM_2015]“Measurement-BasedEoLStochasticAnalysisandDOCSIS3.1SpectralGain”;AyhamAl-Bannaet.al.,TheNCTACableShowSpringTechnicalForum,INTX2015

(3) [CLOONAN_2014]“PredictionsontheEvolutionofAccessNetworkstotheYear2030&Beyond”;T.Cloonan,M.Emmendorfer,J.Ulm,A.Al-Banna,S.Chari,TheCableShowNCTA/SCTETechnicalSessionsSpring2014

(4) [CLOONAN_2015]“LessonsfromTelcoandWirelessProviders:ExtendingtheLifeoftheHFCPlantwithNewTechnologies,”TomCloonanet.al.,TheNCTACableShowSpringTechnicalForum,May,INTX2015

(5) [CLOONAN_2016]“UsingDOCSIStoMeettheLargerBandwidthDemandofthe2020decadeandBeyond”TomCloonan,AyhamAl-Banna,FrankO’Keeffe;TheNCTACableShowSpringTechnicalForum,INTX2016

(6) [CL_D3.1_PHY]Data-Over-CableServiceInterfaceSpecificationsDOCSIS3.1PhysicalLayerSpecification;CM-SP-PHYv3.1-I05-150326,CableLabs

(7) [CL_RMACPHY]Data-Over-CableServiceInterfaceSpecificationsDCA-RemoteMACPHY;RemoteMAC-PHYTechnicalReportCM-TR-R-MACPHY-V01-150730,CableLabs

(8) [EMM_2014]“Nielson’sLawvs.NielsonTVViewershipforNetworkCapacityPlanning,”MikeEmmendorfer,TomCloonan;TheNCTACableShowSpringTechnicalForum,April,2014

(9) [EMM2_2014]“ASide-by-sideComparisonofCentralizedvsDistributedAccessArchitectures”,MikeEmmendorferet.al.,2014SCTESpringTechnicalForum,SCTE

(10) [EMM_2015]“ComparingtheDOCSIS3.1andHFCEvolutiontotheFTTHRevolution”MikeEmmendorfer;2015SCTESpringTechnicalForum,SCTE

(11) [EMM2_2015]“EstimatingDownstreamPerformanceandDOCSIS3.1CapacityinCAAandDAASystems”,MikeEmmendorferet.al,TheNCTACableShowSpringTechnicalForum,INTX2015

(12) [EMM_2016]“AnEconomicAnalysisofBrownfieldMigrationCTTHvs.FTTH”,MikeEmmendorfer,TheNCTACableShowSpringTechnicalForum,INTX2016

Copyright2016–ARRISEnterprisesLLC.Allrightsreserved. 35

(13) [EMM2_2016]“AComparisonofCentralizedvs.DistributedAccessArchitectureforPON”,MichaelEmmendorfer,SebnemZorluOzer;TechnicalForum,INTX2016

(14) [IHS_2010-16]“IHSTechnology(formerlyInfonetics)CableBroadbandHardwareQuarterlyMarketTracker”from1Q2010through1Q2016

(15) [ULM_2013]“CCAPCaseStudy:EnablingConvergedVideo+DatathruSpace&PowerSavings”JohnUlm,SaifRahman,JorgeSalinger,JeffFinkelstein,2013SCTECable-TecExpo

(16) [ULM_2014]“IsNielsenReadytoRetire?LatestDevelopmentsinBandwidthCapacityPlanning”,JohnUlm,T.Cloonan,M.Emmendorfer,J.Finkelstein,JPFioroni;2014SCTECable-TecExpo

(17) [ULM2_2014]“ScalingTraditionalCCAPToMeetTheCapacityNeedsOfTheNextDecade”JohnUlm,TomCloonan;2014SCTECable-TecExpo

(18) [ULM_2015]“HFCTransformationtoFTTP:TheRoleofRFoG,PONandHybridsolutions”,JohnUlm,VenkMutalik;2015SCTECable-TecExpo

(19) [ULM_2016]“GivingHFCaGreenThumb:ACaseStudyonAccessNetworkandHeadendEnergy&SpaceConsiderationsforToday&FutureArchitectures”JohnUlm,ZoranMaricevic;2016SCTECable-TecExpo

(20) [ULM2_2016]“AddingtheRightAmountofFibertoYourHFCDiet:ACaseStudyonHFCtoFTTxMigrationStrategies”,JohnUlm,ZoranMaricevic;2016SCTECable-TecExpo

(21) [VENK_2015]“TheYinandtheYangofaMovetoAllFiber:TransformingHFCtoanAllFiberNetworkwhileLeveragingtheDeployedHFCAssets”;VenkMutalik,MarcelShemmann,ZoranMaricevic,JohnUlm;2015INTXNCTASpringTechnicalForum

(22) [VENK_2016]“Cable’sSuccessisinitsDNA:DesigningNextGenerationFiberDeepNetworkswithDistributedNodeArchitecture”VenkMutalik,ZoranMaricevic;2016SCTECable-TecExpo

(23) [ZORLU_2015]“FromOBIandSNRtoOoklaandNetflix:HowNetworkImpairmentsaffectCustomerPerceptions:TheroleofLeadingandLaggingIndicatorsasWeEvolveHFCtoFTTP”;SebnemZorluOzer,Ph.D.,VenkMutalik,A.Vieira,Ph.D.,J.Chrostowski;SCTECable-TecExpo2015