Formal Theory for Comparative Politics - Stanford …stanford.edu/~avidit/teachingnotes1.pdf ·...

55

Formal Theory for Comparative Politics * Avidit Acharya † January 2013 I taught this material in the first half of a class called “Formal Modeling in Comparative Politics” to second year graduate students in the political science and economics departments at the University of Rochester. The second half of the class was mainly student presentations. * This material was taught to University of Rochester graduate students in political science and economics in the spring of 2013. † Assistant Professor of Political Science and Economics at the University of Rochester. 1

Transcript of Formal Theory for Comparative Politics - Stanford …stanford.edu/~avidit/teachingnotes1.pdf ·...

Formal Theory for Comparative Politics∗

Avidit Acharya†

January 2013

I taught this material in the first half of a class called “Formal Modeling in

Comparative Politics” to second year graduate students in the political science

and economics departments at the University of Rochester. The second half of

the class was mainly student presentations.

∗This material was taught to University of Rochester graduate students in political science and

economics in the spring of 2013.†Assistant Professor of Political Science and Economics at the University of Rochester.

1

Contents

1 Political Economy 3

1.1 Redistributive Politics (Meltzer & Richard 1981) . . . . . . . . . . . . . . . 3

1.2 Non-distortionary Taxation . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

1.3 Targetted Transfers (Lindbeck & Weibull 1987) . . . . . . . . . . . . . . . . 7

1.4 Corruption and Party Bias (Acharya, Roemer & Somanathan 2012) . . . . 9

1.5 Progressive Income Taxation (Roemer 1999) . . . . . . . . . . . . . . . . . . 11

1.6 Political Economy with Strategic Voting (Acharya 2012) . . . . . . . . . . . 15

1.7 Comparative Politics and Public Finance (Persson, Roland & Tabellini 2000) 19

2 Dynamic Methods, etc. 25

2.1 Infinite Horizon Dynamic Programming . . . . . . . . . . . . . . . . . . . . 25

2.2 Dynamic Game Theory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

2.3 Weak and Strong States (Acemoglu 2005) . . . . . . . . . . . . . . . . . . . 29

2.4 Political Transitions (Acemoglu & Robinson 2001) . . . . . . . . . . . . . . 32

2.5 Global Games (Carlsson & van Damme 1993) . . . . . . . . . . . . . . . . . 38

2.6 The Global Game of Revolution (Acharya 2009) . . . . . . . . . . . . . . . 39

2.7 Persistent Effects of Colonization in Africa (Nunn 2007) . . . . . . . . . . . 44

3 Behavioral Political Economy 49

3.1 Ideology (Benabou 2008) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

3.2 Social Identity Equilibrium (Shayo 2009) . . . . . . . . . . . . . . . . . . . . 52

2

1 Political Economy

I assume that you already know about single-peaked preferences, the single-crossing prop-

erty, sincere vs. strategic voting, and Downsian parties. You should also be somewhat

familiar with the basics of the probabilistic voting model. Finally, you should be familiar

with the difficulties in generating existence of Nash equilibrium in pure strategies when par-

ties are Downsian and the policy-space is multidimensional. If you do not know about these

things, please review your notes from previous classes and find out about them quickly!

1.1 Redistributive Politics (Meltzer & Richard 1981)

There is a unit mass continuum of individuals. Each agent has a “taste”-parameter θ.

The distribution of the taste parameter is given by the function F , which has a continuous

density f on its support [θ−, θ+]. The distribution is skewed so that the median taste

parameter θm is strictly less than the mean θ, which is quite large. Specifically, we assume

(i) 0 < θ− < θ+ < 2θ and (ii) θm < θ (A1)

What does the taste parameter capture? Assume that all individuals can produce

y(e) = e units of output by exerting e ≥ 0 units of effort, but they each dislike putting in

effort. In particular, an individual with taste parameter θ has preferences over consumption

and effort given by

u(c, e|θ) = c− e2

2θ(1)

where c is his consumption and e ≥ 0 is his effort. Thus, θ is a parameter that reflects an

agent’s propensity to work: If θ is small, then the individual has a large distaste for work,

but if it is large then he doesn’t. Because θ− > 0 all agents have some degree of distaste

for work.

Now, suppose that once the individuals make their effort decisions, the government

taxes their output at the rate τ and redistributes all of its revenue as (undirected) lump-

sum transfers. If all individuals of type θ exert e(τ, θ) units of effort when the tax rate is

τ , then the government collects

T =

∫ θ+

θ−τy(e(τ, θ))f(θ)dθ ≡ τY (2)

units of revenue. Here, Y is the total output produced. Since there is a unit mass of agents,

this is also the amount that each agent receives in return from the government. Therefore,

an individual of type θ who exerts e units of effort gets to consume

c = (1− τ)y(e) + T = (1− τ)e+ τY (3)

3

units of output. Note that because each agent is infinitesimal, he is negligible: the effort

decision e has no effect on T (or Y ).

How is the tax rate determined? We assume that prior to the agents exerting their

effort, there is a majoritarian election in which two Downsian political parties, A and B,

announce (and commit to) a tax rate τ ∈ [0, 1]. Thus, these parties compete over the issue

of fiscal policy. All voters vote sincerely for the party whose policy will give them a higher

utility. Voters who are indifferent toss a coin. If the election is tied, then each party comes

to power with probability 1/2. The party that comes to power implements its announced

policy.

So, the timing of events is as follows.

1. Parties announce τA and τB.

2. Voting takes place, and the winner is determined.

3. All agents exert effort and produce output.

4. The party in power implements the policy that it announced, so tax and redistribution

take place.

5. Consumption takes place.

A voter of type θ has preferences over tax and effort given by

(1− τ)e+ τY − e2

2θ(4)

This expression is strictly concave in effort, so we can find the optimal effort by solving the

first order condition. The solution is

e∗(τ, θ) = (1− τ)θ (5)

Here we have used the fact that the agent’s effort decision does not affect total output Y . We

can see that the agent’s optimal effort is increasing in his taste parameter θ and decreasing

in τ . The reason it is decreasing in τ is because taxes are distortionary: when agents get

to keep less of their output and their effort does not affect how much they get from the

government, they work less. We can now use the optimal effort decisions to compute total

output

Y ∗(τ) =

∫ θ+

θ−y(e∗(τ, θ))f(θ)dθ = (1− τ)θ (6)

This reflects the distortionary effect of taxation on the aggregate economy. As the tax rate

τ increases, total output decreases because agents exert less effort.

4

Figure 1: τ∗(θ)

Now let us substitute back the optimal effort e∗(τ, θ) and total output Y ∗(τ) into the

agent’s preferences in (4). This gives us the the agent’s preference over the tax rate τ :

v(τ |θ) =θ

2(1− τ)2 + τ(1− τ)θ (7)

By assumption A1(i), the above expression is strictly concave in τ for all agent types θ.

This means that we can find type θ’s most preferred tax rate τ∗(θ) by solving the first order

condition to the maximization of (7) subject to τ ∈ [0, 1]. The solution is

τ∗(θ) =

θ−θ2θ−θ if θ < θ

0 if θ ≥ θ(8)

One can see that by assumption A1(i), the optimal feasible tax rate satisfies τ∗(θ) < 1 for

all θ ∈ [θ−, θ+] and is positive only if θ < θ. By plotting τ∗(θ) one can see that the optimal

tax rate is decreasing in θ. (See Figure 1.)

Since voters’ preferences are single peaked in τ for all θ, you should immediately know

that both parties will announce the most preferred tax rate of a voter of type θm. Thus,

Downsian convergence takes place and the implemented tax rate is always

τ∗(θm) =θ − θm

2θ − θm> 0. (9)

The ratio of incomes of any two types θ and θ′ is simply y(e∗(τ, θ))/y(e∗(τ, θ′)) = θ/θ′, which

is invariant to the tax rate. Therefore, fiscal policy does not change the relative positions

of any two individuals. Then, observe that the equilibrium policy τ∗(θm) is decreasing

with the ratio of median to mean income θm/θ. Since this ratio is taken to be an inverse

5

measure of inequality, the model argues that inequality and redistribution covary, though

the relationship is not causal.

The equilibrium tax rate τ∗(θm) differs from the efficient tax rate

τ fb = 0 (10)

that maximizes total output Y ∗(τ). Thus, we have seen the first of many models that argue

that economic distortions have political causes. Here, the political cause is the class-conflict

between those who dislike to work (low θ agents) versus those who have a greater proclivity

to work (high θ agents).

Exercise. Consider the following modification to the model above. Suppose that now

tax revenue can be used for two things: to provide untargeted lump-sum transfers (as above)

and to finance a public good g that results in an additional payoff of H(g) = 1α(g)α for every

agent. Thus, agent θ’s preferences are now given by

v(c, e, g|θ) = u(c, e|θ) +H(g) (11)

where u(c, e|θ) is the function in (1). Parties compete over the linear tax rate τ and the

fraction z of total tax revenue T that is used to create the public good. Assume that g

units of the public good can be created using exactly g units of the tax revenue. Compute

the optimal z as a function of T for an agent of type θ, and show that it is independent

of θ. Then show that there exists a Nash equilibrium to the policy announcement game in

which both Downsian parties propose the same tax rate as in equation (9).

1.2 Non-distortionary Taxation

We could have, instead, started with an even simpler model in which taxes are non-

distortionary. Suppose that a unit continuum of agents are indexed by their income y which

is distributed by a function G with continuous density g on the support [y−, y+] ⊂ R+. The

mean income y is strictly greater than the median ym. Again, we have a government that

taxes at a linear rate τ and redistributes all proceeds as untargeted lump-sum transfers.

Note that tax revenues are

T =

∫ y+

y−τyg(y)dy = τy (12)

Thus an agent with income y has preferences over τ given by (1−τ)y+τy. These preferences

are single peaked in τ for every y. So, again, Downsian convergence holds and the optimal

tax rate of the median income earner is implemented. Because ym < y this optimal tax

rate is τ∗(ym) = 1.

6

The assumption that median income is lower than the mean income is one that is

empirically true for every country in the world. That we don’t observe linear tax rates

of 100% may be because of the distortionary effects of taxation that Meltzer and Richard

(1981) formalized using a model similar to that of the previous section. But many empirical

studies have estimated that the distortion must be enormous to explain why the tax rate is

as low as it is in many countries where the gap between mean and median income is very

large. (Think of Latin America.)

A large literature in political economy is concerned with explaining why more redistri-

bution does not take place. Indeed, some scholars consider it to be the most important

question in political economy.

1.3 Targetted Transfers (Lindbeck & Weibull 1987)

The Meltzer-Richard model assumes that transfers are lump-sum and untargeted. When

transfers are targeted across multiple, say three, groups then the policy space becomes

multidimensional. Here we outline a popular way to deal with the problem of existence

of pure strategy Nash equilibrium when the policy space is multidimensional: probabilistic

voting. We also assume that the two parties are maximizing vote share, which simplifies

the analysis but is not crucial to probabilistic voting models.

Assume that there is a continuum of unit mass citizens partitioned into three groups

j = 1, 2, 3, with population shares λj > 0. Two political parties must decide how to target

a resource of 1 unit across these groups. Every individual within a group receives the same

amount as every other individual in the group. Thus a policy is triple x = (x1, x2, x3) with

xj representing the amount that a member of group j receives. The parties propose (and

commit to) feasible policies xA and xB. A feasible policy x is a nonnegative vector that

satisfies the budget constraint ∑j

λjxj = 1 (BC)

Members of group j have the following preferences over policy

uj(xj) = (xj)1−α

where α ∈ (0, 1) is a parameter that reflects diminishing marginal utility. In addition a

voter from group j receives a preference shock ε in favor of party B. The shock is drawn

uniformly and independently across voters from the interval[− 1

2φj, 1

2φj

]. We will assume

that these intervals are quite large, in particular

φj <1

2∀j

7

So, a voter from group j votes for party A if and (essentially) only if

(xAj )1−α > (xBj )1−α + ε

or, ε < (xAj )1−α − (xBj )1−α ≡ ∆j(xAj , x

Bj )

Note that ∆j(xAj , x

Bj ) is strictly concave in xAj and strictly convex in xBj . Also, for all

feasible distributions xAj , xBj , the difference ∆j(xAj , x

Bj ) lies in the interval

[− 1

2φj, 1

2φj

]since ∆j(x

Aj , x

Bj ) ∈ [−1, 1] ⊂

[− 1

2φj, 1

2φj

]. So, the vote share of party A from group j is

1

2+ φj∆j(x

Aj , x

Bj )

This is because there is a continuum of voters in each group and voters are identical within

groups, so the probability that an individual voter votes for party A is also the vote share

of party A from that group. The total vote share for party A is then

V (xA, xB) =1

2+∑j

λjφj∆j(xAj , x

Bj )

which is strictly concave in each xAj since ∆j(xAj , x

Bj ) is strictly concave in xAj . The vote

share of party B is 1−V (xA, xB), which is strictly concave in each xBj . Therefore, the best

response of party A to a policy xB of party B can then be found by solving the first order

conditions of the maximization of V (xA, xB) with respect to xA, and subject to the budget

constraint (BC). These conditions are simply

λjφj(1− α)(xAj )−α = µλj , j = 1, 2, 3

where µ is the Lagrange multiplier associated with the budget constraint (BC). These

conditions imply that the ratios of distributions satisfy

xAixAj

=

(φiφj

)1/α

, i, j = 1, 2, 3

So, along with the budget constraint, we have three equations in three unknowns. There

are two ratio equations, above, since the others are redundant. (For example, the ratios

xA1 /xA2 and xA2 /x

A3 already define the ratio xA1 /x

A3 , and the reciprocal ratios.) And there is

the budget constraint (BC). Solving these three equations we find the unique best response

for party A

xAj =(φj)

1/α∑i λi(φi)

1/α, j = 1, 2, 3

which is independent of party B’s policy. By a symmetric argument, party B’s best response

is the same quantity. These mutual best responses give us the unique Nash equilibrium of

the electoral competition game between parties.

8

A few things to note about the equilibrium. Groups that are more responsive to policy

receive more from both parties. Group j is more responsive to policy when φj is higher, in

which case the preference shocks for that groups members are small and voting behavior is

mostly determined by the relative comparison of policy.

Exercise. The model above assumes that each voter in group j has a “bias” toward

party B if his realized ε is larger than 0, and a bias toward party A if the realized ε is

smaller than 0. But since there is a continuum of voters in each group, the average bias

across voters in any given group j is 0. This is because we assumed the distribution of

ε to be uniform on an interval[− 1

2φj, 1

2φj

]that is centered at 0. Suppose instead that

for a voter in group j, the bias ε is drawn uniformly from an interval[bj − 1

2φj, bj + 1

2φj

],

bj 6= 0. Now, on average, members of group j have a bias bj toward party B. Allow bj

to be positive or negative, so that they may in fact have a positive average bias towards

party A (when bj < 0). Show that there is still a unique (interior) Nash equilibrium in pure

strategies when the magnitudes of the average biases |bj | are not too large. Show that in

fact the equilibrium is the same for all small enough values of the biases bj , including the

benchmark case bj = 0 for all j. Conclude that there is policy convergence even when there

is aggregate party bias.

1.4 Corruption and Party Bias (Acharya, Roemer & So-

manathan 2012)

Now we provide a probabilistic voting model with policy divergence. To do this, we assume

that there is party bias as in the exercise above, and that the parties are maximizing

something different from their vote shares.

Consider a polity consisting of a set of citizens who belong to two different ethnic groups,

called 1 and 2. Fraction λ of the population is of group 1 while the remaining 1 − λ is of

group 2. There are two political parties, labeled A and B. Party A is identified by the

voters with group 1 and party B with group 2. If party i = A,B wins a fraction V i of the

total vote share, then it controls exactly that fraction of the government’s budget. It can

do two things with the budget: spend it on the populace, and take rents for itself. The

distribution to the citizens, however, cannot be targeted. This means that every citizen

(regardless of ethnic group) must receive the same amount of the good. Thus a party’s

policy is uni-dimensional. It is represented by a number xi, which is is the fraction of

money under party i’s control that distributes to the populace, and 1 − xi is the fraction

that it steals.

The fact that parties are associated, by the voters, with ethnic groups means that

9

(on average) voters of each ethnic group have biases in favor of their associated party.

Specifically, the payoff uij(·) to a voter of ethnic group j from voting for party i is

uA1 (xA) = xA + b1 + ε1 uA2 (xA) = xA

uB1 (xB) = xB uB2 (xB) = xB + b2 + ε2

where b1, b2 > 0 are the average biases towards the favored parties in groups 1 and 2,

and ε1, ε2 are the realizations of random variables independently drawn across voters. We

suppose that each εj is uniform over an interval[− (1− d), (1− d)

], 0 < d < 1 and we will

denote this uniform c.d.f. by F.

Facing a policy pair (xA, xB), a citizen of ethnic group 1 votes for party A if and

(essentially) only if

uA1 (xA) > uB1 (xB) ⇐⇒ ε1 < xA − xB + b1 ≡ ∆1(xA, xB)

and a citizen of ethnic group 2 votes for party A if and (essentially) only if

uA2 (xA) > uB2 (xB) ⇐⇒ ε2 < xA − xB − b2 ≡ ∆2(xA, xB)

Assuming that ∆1(xA, xB) and ∆2(xA, xB) both lie in the interval[− (1− d), (1− d)

], the

vote share of party A (and the fraction of government budget that it controls) is

V A(xA, xB) = λF(∆1(xA, xB)) + (1− λ)F(∆2(xA, xB))

=1

2+

(λ∆1(xA, xB) + (1− λ)∆2(xA, xB)

)2(1− d)

while the vote share of party B is V B(xA, xB) = 1−V A(xA, xB). Now, instead of assuming

that the parties wish to maximize their vote shares, we assume that they are venal, and

wish only to maximize the rents that they take. Then the the payoff function for party i is

Πi(xA, xB) = (1− xi) · V i(xA, xB).

Notice that party i’s payoff is strictly concave in its own policy xi. So, we can compute the

best response of party i to policy x−i of the other party −i by taking the first order condition

for the maximization of Πi(xA, xB). For the moment, we ignore the budget constraint that

xi must be a number between 0 and 1. The first order conditions for the two parties are

−V i(xA, xB) + (1− xi)∂Vi(xA, xB)

∂xi= 0, i = A,B

These are two equations in two unknowns. If the solution to these equations are numbers

xA, xB ∈ [0, 1], and the values of ∆1(xA, xB) and ∆2(xA, xB) both lie in the interior of

10

[− (1 − d), (1 − d)

]at the solution, then we have found a local Nash equilibrium (LNE).1

The solutions are

xA = d− λb1 − (1− λ)b23

xB = d+λb1 − (1− λ)b2

3.

If b1 and b2 are small, then both of these numbers lie between 0 and 1 and ∆1(xA, xB) and

∆2(xA, xB) will lie inside[− (1− d), (1− d)

]. So, we have an LNE.

Notice that the equilibrium value of xA is decreasing in b1 and increasing in b2 while

xB is increasing in b1 and decreasing in b2. As the ethnic party bias grows for the members

of group j = 1, 2, the corruption level of their party increases while the corruption level of

the other party decreases.

Exercise. The model above assumes that the parties cannot target their distribution

to the two groups as in the model of the previous section. Assume now that the parties

can target their distribution. In particular, party i can give xij to each member of group j,

keeping 1−λxi1− (1−λ)xi2 for itself. Find conditions under which a local Nash equilibrium

exists with venal parties, and compute the equilibrium. Which features of the equilibrium

are noteworthy?

1.5 Progressive Income Taxation (Roemer 1999)

There is a continuum of voters of unit mass. Income is distributed among voters according

to a continuous (atomless) probability distribution F on the support [0, 1]. A tax policy is

a triple of real numbers (a, b, c). If this policy is implemented, then a voter with income

w receives after-tax income aw2 + bw + c. Taxes are purely redistributive, so the budget

balance condition is ∫(aw2 + bw + c)dF (w) =

∫wdF (w) ≡ µ.

This implies that

c = −aµ2 − bµ+ µ where µ2 ≡∫w2dF (w).

So the budget balance condition implies that a tax policy can be denoted simply (a, b) where

c is determined residually. The after-tax income (and utility) of a voter with income w at

tax policy (a, b) is

u(a, b, w) = a(w2 − µ2) + b(w − µ) + µ

1I could in fact make the equilibrium global by assuming that the payoff were instead φuij(·),where φ > 0 is a small number in comparison to d.

11

Figure 2: The triangle OUV

Thus, a voter with income w 6= µ is indifferent between two policies (a, b) and (a′, b′) iff

aφ(w) + b = a′φ(w) + b′, where

φ(w) =w2 − µ2

w − µSo, the indifference curves of a voter with income w 6= µ are straight lines in (a, b)-space of

slope −φ(w). The indifference curves of a voter with income µ are vertical straight lines. We

further restrict a tax-policy (a, b) to satisfy the following assumptions that are maintained

throughout.

(1.) a(w2 − µ2) + b(w − µ) + µ ≥ 0 for all w

(2.) 2aw + b ≥ 0 for all w

The first assumption says that no voter can be left with a negative income. The second

condition says that after-tax income must be a nondecreasing function of income. This is

an incentive compatibility constraint that says that no voter wants to burn money.

Exercise. First, show that the conditions (1.) and (2.) above imply that the set of

admissible tax policies (a, b) coincides with the triangle OUV in Figure 2. Second, define a

tax policy to be (weakly) progressive if after-tax income as a percent of income is a (weakly)

decreasing function of income. A (weakly) regressive policy is one in which after-tax income

as a percent of income is a (weakly) increasing function of income. A proportional (or linear)

tax is one in which after-tax income as a percent of income is constant in income. Show

that a tax policy (a, b) is weakly progressive iff it lies in the triangle OUT , weakly regressive

iff it lies in the triangle OV T , and proportional iff it lies on the segment OT . Note that the

12

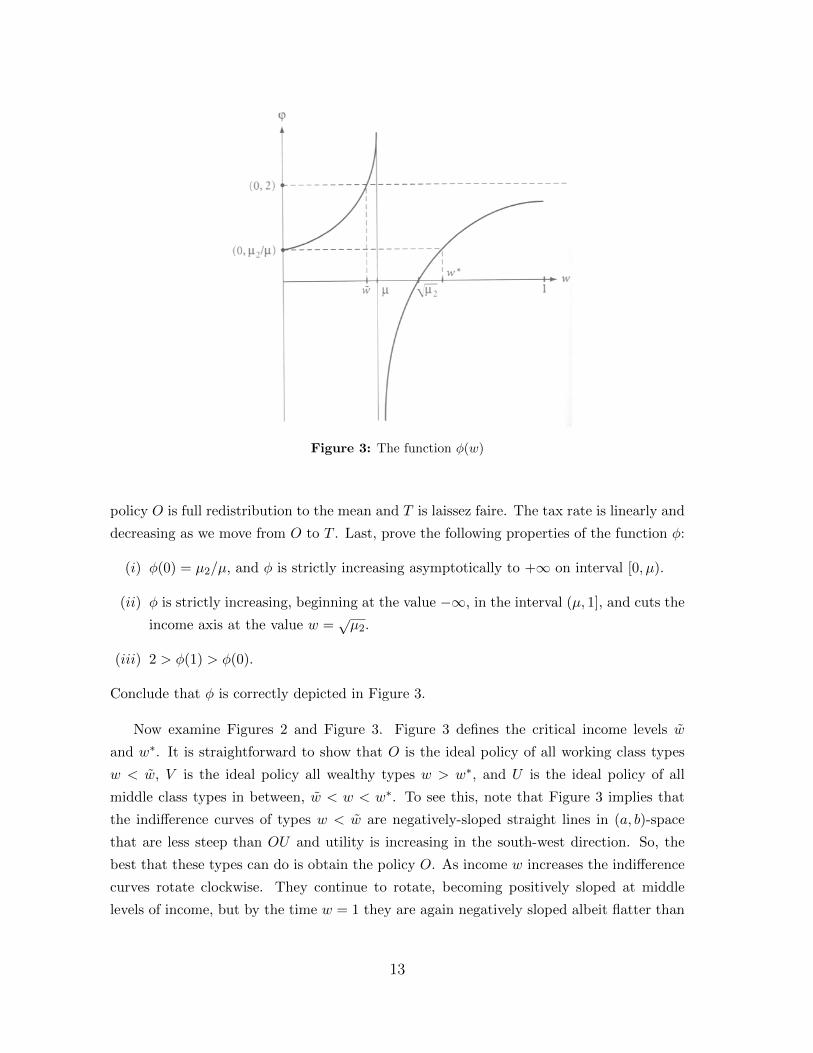

Figure 3: The function φ(w)

policy O is full redistribution to the mean and T is laissez faire. The tax rate is linearly and

decreasing as we move from O to T . Last, prove the following properties of the function φ:

(i) φ(0) = µ2/µ, and φ is strictly increasing asymptotically to +∞ on interval [0, µ).

(ii) φ is strictly increasing, beginning at the value −∞, in the interval (µ, 1], and cuts the

income axis at the value w =õ2.

(iii) 2 > φ(1) > φ(0).

Conclude that φ is correctly depicted in Figure 3.

Now examine Figures 2 and Figure 3. Figure 3 defines the critical income levels w

and w∗. It is straightforward to show that O is the ideal policy of all working class types

w < w, V is the ideal policy all wealthy types w > w∗, and U is the ideal policy of all

middle class types in between, w < w < w∗. To see this, note that Figure 3 implies that

the indifference curves of types w < w are negatively-sloped straight lines in (a, b)-space

that are less steep than OU and utility is increasing in the south-west direction. So, the

best that these types can do is obtain the policy O. As income w increases the indifference

curves rotate clockwise. They continue to rotate, becoming positively sloped at middle

levels of income, but by the time w = 1 they are again negatively sloped albeit flatter than

13

Figure 4: The triangle OUV with policies L and R

the segment OU since φ(1) < 2 (which is a fact depicted in Figure 3 and proven by you in

the Exercise above).

We suppose that there are two parties, called Left and Right, that propose policies

tL = (a, b) and tR = (a′, b′). Let Ω(tL, tR) be the set of voters that strictly prefer policy tL

to tR, and thus vote for the Left party. We assume that voters who are indifferent mix in

an arbitrary way, but as long as Left and Right propose different policies, this set of voters

is always measure zero so their behavior will not matter in determining vote shares. The

vote share of Left is thus

π(tL, tR) = F (Ω(tL, tR))

and the vote share of Right is 1 − π(tL, tR). Now, we assume that some members of each

party are policy-motivated. Specifically, some members of Left have the interest of a voter

of income wL < w in mind, whereas some members of Right have the interest of a voter of

income wR > w∗ in mind. We call such factions the Militants. The militants of party j want

to propose a policy tj that maximizes u(tj , wj). We also assume that some members of the

parties are purely office-motivated in that they care only about maximizing vote-share. We

call these fractions the Opportunists. The policy pair (tL, tR) is a Roemer-Nash equilibrium

(RNE) if it is admissible (i.e. each policy lies in the triangle OUV ) and

(L) there is no admissible policy t′L for Left such that π(t′L, tR) ≥ π(tL, tR) and u(t′L, wL) ≥u(tL, wL) with at least one inequality strict; and

(R) there is no admissible policy t′R for Right such that 1− π(tL, t′R) ≥ 1− π(tL, tR) and

u(t′R, wR) ≥ u(tR, wR) with at least one inequality strict.

14

These state that neither Left nor Right can find deviations that make their Militants better

off without making their Opportunists worse off, or make their Opportunists better off

without making their Militants worse off. We now have the following result.

Theorem 1: There exists an RNE. In particular, there is one such that Left and Right

propose distinct strictly progressive policies.

Proof: Pick a point L on the interior of segment OU and a point R on the interior of

segment UV such that the slope of LR is nearly −2, in particular pick L close to O. Look

at Figure 4 for a depiction. Suppose Left proposes the policy L and Right proposes the

policy R. Note that the set of types that vote for Left is precisely [0, w+ ε) for some small

ε. Next, since the income type wL is smaller than w, its indifference curve through the

point L is a straight line that is flatter in slope than OU . Moreover, utility is increasing in

the south-west direction. Therefore, the set of policies that make income type wL weakly

better off (than under policy L) are the policies that lie in the small shaded triangle LOQ.

But a deviation to any other policy in this triangle would strictly decrease Left’s vote share

since it would make the line LR less steep, reducing the set of types that vote for Left from

[0, w + ε) to [0, w) with w < w + ε. (Note that the triangle LOQ can really be made as

small as one wants by choosing L close enough to O.) Therefore, the equilibrium condition

(L) is satisfied. In fact, the only deviations that would increase Left’s vote share without

reducing wL’s utility, or increase wL’s utility without reducing Left’s vote share are in the

shaded cone below the point L in Figure 4; but these are not admissible deviations. A

similar argument establishes that the analogously “profitable” deviations for Right are in

the shaded cone above point R; but again these are not admissible. Hence the equilibrium

condition (R) is also satisfied, and (L,R) is and RNE. In addition, L and R are strictly

progressive policies and L 6= R.

Under some slightly stronger assumptions, and a weak refinement of RNE called strong

RNE, one can show that Left and Right propose weakly progressive policies in all strong

RNE. But the key point to highlight is that by modeling the fact of intra-party competi-

tion between Opportunist factions that care about winning and Militant factions that care

about “protecting the base,” one can generate existence of equilibrium in multidimensional

political competition while also enhancing a model’s realism.

1.6 Political Economy with Strategic Voting (Acharya 2012)

There are 2n+ 1 voters. With probability λ ∈ (0, 1/2) a voter is a high income earner, and

with probability 1−λ he is a low income earner. There are two periods and two policies. In

the first period, a status quo policy is in effect. Then, an election is held to decide whether

15

to continue with the status quo or to switch to a more redistributive policy. The policy

that wins the election is implemented in the second period. Under the more redistributive

policy, each high income voter receives a payoff yh while each low income voter receives a

payoff yl. Under the status quo policy, each high income voter has payoff yh, while each

low income voter has probability δ of receiving an opportunity to become a high income

voter. If a low income voter receives the opportunity to climb the economic ladder, and he

is talented, then he receives a payoff yh. If he is not talented, or if he does not receive the

opportunity, then his payoff is yl. Each low income voter has prior probability p ∈ (1/2, 1)

of being talented. If a voter becomes a high income earner in the first period, he remains a

high income earner in the second period. Voters who receive an opportunity to become high

income earners in the first period and are unsuccessful learn that they are untalented, and

would also be unsuccessful in the following period even if they got the opportunity again.

Voters who do not receive the opportunity in the first period do not learn whether or not

they are talented.

Voters do not directly observe δ, nor does any voter observe the consequences of the

first period policy for any other voter. Instead, voters believe that δ is a random variable

with continuous density f . Assume that there is a number ν > 0 for which

f(δ) > ν ∀δ ∈ [0, 1] (A2)

If the status quo policy is re-elected, then the value of δ in the second period is the same

as in the first. Let δ denote the expected value of δ according to f . Conditional on δ, the

expected payoff from the status quo policy for a low income voter is given by

y(δ) = (1− δp)yl + δpyh (13)

Therefore, the unconditional expected payoff to re-electing the status quo policy for a low

income voter who did not receive the economic opportunity is y(δ). His expected payoff to

electing the redistributive policy is simply yl. We will assume that

(i) yl < yl ≤ yh < yh and (ii) y(δ) < yl < y(1) (A3)

A strategy for a voter is the probability with with he votes to re-elect the status quo pol-

icy. The equilibrium concept is symmetric Bayes Nash equilibrium in weakly un-dominated

strategies. All voters are rational, so each voter casts his ballot as if he believes that his

vote will decide the election, i.e. he conditions his vote on the event that his vote is pivotal.

Call the set of voters that started off as high income earners H, the set of voters who got

the opportunity and climbed the socio-economic ladder (because they were talented) L+,

the set of voters who got the opportunity but failed to climb the socio-economic ladder

16

(because they were not talented) L− and the set of voters who did not get the opportunity

L0. The following observation is straightforward.

Lemma 1: In every equilibrium of the game, voters in H and L+ vote to re-elect the

status quo while voters in L− vote to switch to the more redistributive alternative.

Proof. Voters in H and L+ have a weakly dominant strategy to vote for the status quo,

while voters in L− have a weakly dominant strategy to vote for the more redistributive al-

ternative. Since the equilibrium concept rules out equilibria in weakly dominated strategies,

the result follows.

Let x denote the probability with which an L0 voter votes to re-elect the status quo.

Lemma 1 implies that equilibria can be identified by entirely by x. Given any symmetric

strategy x ∈ [0, 1], the unconditional probability of casting a vote for the status quo policy

(when H, L+ and L− voters play their symmetric equilibrium strategy) is

π(δ, x) = λ+ (1− λ)(δp+ (1− δ)x

)The probability that an L0 voter is pivotal is

φ(δ|x, n) =

(2n

n

)(π(δ, x))n(1− π(δ, x))n

The distribution of the state variable δ given that an L0 voter is pivotal (viewed as a function

of x and n) is

fpiv(δ|x, n) =φ(δ|x, n)(1− δ)f(δ)∫ 1

0 φ(ω|x, n)(1− ω)f(ω)dω

The expectation of δ for an L0 voter, conditional on pivotal, is

δpiv(x, n) =

∫ 1

0δfpiv(δ|x, n)dδ

Now, the next result is also straightforward.

Lemma 2: There exists a cutoff δ∗ ∈ (0, 1) such that the symmetric strategy x = 0

is part of an equilibrium iff δpiv(0, n) ≤ δ∗, the symmetric strategy x = 1 is part of an

equilibrium iff δpiv(1, n) ≥ δ∗, and the symmetric strategy x ∈ (0, 1) is part of an equilibrium

iff δpiv(x, n) = δ∗.

Proof. Follows immediately from (A2), (13), (A3)(ii) and Lemma 1.

Now note that for fixed values of x 6= p, the function π(δ, x) is a strictly monotone in δ on

the interval [0, 1]. Therefore, there is a unique number δ†(x) that minimizes |π(δ, x)− 1/2|.Now, the following mathematical result will be extremely useful.

17

Theorem 2: If x 6= p then for all ε > 0 there is N such that n ≥ N implies

|δpiv(x, n)− δ†(x)| ≤ ε

If x = p then δpiv(x, n) is a constant number between 0 and 1, for all n.

Proof. The proof of the x = p part is straightforward. For the first part, define the

function h : [0, 1]→ R by

h(π) = π(1− π)

Since π(δ, x) is continuous in its arguments, the composite function h(π(·, ·)) : [0, 1]2 → R is

continuous. Moreover, for all x 6= p, the function h(π(·, x)) : [0, 1]→ R is single peaked and

maximized by the value of δ ∈ [0, 1] that minimizes |π(δ, x) − 1/2|. Thus δ†(x) maximizes

h(π(·, x)).

Fix x 6= p and define

∆ε(x) = δ ∈ [0, 1] : |δ − δ†(x)| ≤ ε

to be an ε-neighborhood of δ†(x). Fix any ε. If ε is small enough, then ∆ε(x) 6= [0, 1]. In

this case, there exists a small number ηε ∈ (0, 1) such that

h(π(δ†(x), x))− ηε > supδ /∈∆ε(x)

h(π(δ, x))

Furthermore, define the set

Ωε(x) = ω ∈ ∆ε(x) : |h(π(δ†(x), x))− h(π(ω, x))| ≤ ηε/2

Note that the set Ωε(x) must contain a small interval I ⊂ [0, 1] that in turn contains the

number δ†(x). Let µ be the length of this interval.

We will prove that there is a number N large enough that for all n ≥ N we have∫δ∈∆ε(x)

fpiv(δ|x, n) > 1− ε.

To see this, note that if ∆ε(x) = [0, 1] then∫δ∈∆ε(x) f

piv(δ|x, n) = 1, so the above inequality

trivially holds. If ∆ε(x) 6= [0, 1] then∫δ /∈∆ε(x)

fpiv(δ|x, n)dδ =

∫δ /∈∆ε(x) φ(δ|x, n)(1− δ)f(δ)dδ∫ 1

0 φ(ω|x, n)(1− ω)f(ω)dω≤

∫δ /∈∆ε(x) φ(δ|x, n)(1− δ)f(δ)dδ∫ω∈Ωε(x) φ(ω|x, n)(1− ω)f(ω)dω

≤supδ /∈∆ε(x) φ(δ|x, n)

infω∈Ωε(x) φ(ω|x, n)

∫δ /∈∆ε(x)(1− δ)f(δ)dδ∫ω∈Ωε(x)(1− ω)f(ω)dω

≤(

supδ /∈∆ε(x) φ(δ|x, n)

infω∈Ωε(x) φ(ω|x, n)

)1

ν∫ω∈Ωε(x)(1− ω)dω

≤(

h(π(δ†(x), x))− ηεh(π(δ†(x), x))− ηε/2

)n1

12µ

2ν≤(

1− ηε1− ηε/2

)n 112µ

2ν.

18

So we can choose N large enough such that n ≥ N implies that the integral on the left

above is smaller than ε.

Finally, to prove the theorem, write

δpiv(x, n) =

∫δ /∈∆ε(x)

δfpiv(δ|x, n)dδ +

∫δ∈∆ε(x)

δfpiv(δ|x, n)dδ.

and observe that for n ≥ N , this quantity is bounded above by ε+ (δ†(x) + ε) = δ†(x) + 2ε

and bounded below by (δ†(x) − ε)(1 − ε) > δ†(x) − 2ε. Thus, the conditional expectation

δpiv(x, n) is within 2ε of δ†(x). But ε was arbitrary.

The following is an immediate corollary of Theorem 2.

Proposition 1: There exists N such that for all n ≥ N , it is (part of) an equilibrium

for all L0 voters to vote for the status quo policy with probability 1.

Proof. Suppose x = 1. Then δ†(1) = 1. So Theorem 2 implies that for n large enough

δpiv(x, n) is close to 1. So by Lemma 2, x = 1 is part of an equilibrium.

Exercise. Assume that n is large, and characterize all of the equilibria of the model.

Bonus Exercise. (Only to be done by those who took Sourav’s class last semester and

know what “information aggregation” means.) Which of the equilibria aggregate informa-

tion and which do not?

1.7 Comparative Politics and Public Finance (Persson, Roland

& Tabellini 2000)

The exposition follows that of Persson & Tabellini, Ch. 10, with some minor changes in

notation. There are three voters j = 1, 2, 3 residing in different districts. Each voter j is

represented by a legislator l = 1, 2, 3. Voter j has preferences given by

wj = y − τ + f j +H(g)

where y is his income, τ is the amount he pays in taxes, f j is the pork he receives and

H(g) is the value of a public good g, one unit of which can be produced by one unit of tax

revenue. H is a strictly concave function that you can assume to be

H(g) =z

1− α(g)1−α

19

Figure 5: The Legislative Game

Suppose that each legislator l captures rents rl from the budget. Then, the budget constraint

can be written

3τ = g +∑j

f j +∑l

rl (BC)

A policy vector is denoted q =(τ, g, (f j)j , (rl)l

), where all components are nonnegative.

The “status quo” (or “disagreement”) policy vector is the nasty one q0 =(r, 0, (0)j , (r)l

),

where r > 0. Legislators have preferences represented by

vl = rl + plR

where pl is the probability with which they are re-elected and R represents exogenously set

future rents from re-election. We assume that voters can pre-commit to threshold re-election

rules given by

pl =

1 if wj(q) ≥ wj , j = l

0 otherwise

In other words voter j asks his representative to deliver him at least utility wj . If he gets this

amount, then he re-elects the legislator; otherwise, he kicks him out of office. The timing of

the game is given by Figure 5, and summarized as follows. Nature selects a legislator a to

be the agenda setter. Voters pre-commit to the thresholds wj . The agenda setter proposes

a policy q. The entire legislature votes; if a majority vote for q then q passes, otherwise q0

is implemented. The election is held.

We will make the following three assumptions

1. R ≥ r, so the future has greater value than that of sabotaging policy today

2. R+ r− (z)1/α > 0, which will imply that pork transfer to the agenda setters district

are positive in equilibrium

20

3. 3y −R− r > 0, so that there is lots of money in the economy

4. 3y > (3z)1/α, so the socially optimal level of the public good is affordable

We first characterize the socially optimum level of public goods from the perspective of

the voters. To do this, define the social welfare function (over policies) to be the sum of

only the voters’ utility

W (q) =∑j

wj = 3(y − τ) +∑j

f j + 3H(g)

The social planner maximizes this function.

Proposition 2: At the solution to the maximization of the planner’s objective function

W (q) subject to the budget constraint (BC), we have gsp = (3z)1/α and rspl = 0 for all l.

Taxes τ must be weakly greater than gsp, but otherwise taxes and transfers, f j , j = 1, 2, 3,

are indeterminate.

Proof. Substituting the budget constraint (BC) into W (q), we get

W (q) = 3y − g +∑l

rl + 3H(g)

Clearly rspl = 0 for all l. To find the optimal g, we solve the first order condition

3H ′(g) = 3z(g)−α = 1

which gives us gsp = (3z)1/α. This is called the Samuelson level of the public good, and by

Assumption 4 above, it is affordable with a tax rate τ sp = gsp/3. Note that taxes may be

higher so long as they are given back to the districts in the form of transfers. Consequently,

the level of taxes and transfers is indeterminate.

We can now compare the equilibrium level of the public good with the planner’s optimal

level. An equilibrium of the game is a subgame perfect equilibrium in which legislators use

weakly un-dominated voting strategies. Then, the equilibrium level of the public good is

characterized in the following proposition.

Proposition 3: On every equilibrium path we have the following

g∗ = (z)1/α τ∗ = y r∗a = 3y −R− r r∗l = 0, l 6= a

fa∗ = R+ r − g∗ f j∗ = 0, j 6= a wa∗ = H(g∗) + fa∗ wj∗ = H(g∗), j 6= a

21

Proof sketch. I will sketch the argument that these are sequentially optimal on the path

of play, and you will (in the Bonus Exercise below) close the argument by proving that there

are equilibria that support this path of play (and indeed all of them support this path of

play).

We work backwards. Note that because all legislators use weakly un-dominated voting

strategies, in every equilibrium all legislators vote to pass any proposal q that gives them

a payoff least r whenever it is the case that if the proposal fails, then they will not be

re-elected. So, suppose the agenda setter proposes q∗ =(τ∗, g∗, (f j∗)j , (r

∗l )l

)when voters

use the thresholds wj∗. Then all of the legislators must vote to pass the proposal. If the

proposal does not pass, then q0 is implemented and voters in all districts receive utility

H(0) = 0 < wj∗, all j. Moreover, both legislators l 6= a receives a payoff r instead of the

payoff he would receive from q∗ which is r∗l + R = R > r by Assumption 1. The legislator

a receives a payoff r instead of the payoff r∗a +R > r by Assumptions 1 and 3, which states

that r∗a > 0. So, all vote to pass the proposal q∗.

Now, we show that it is optimal for the agenda setter a to propose q∗ when the voters

use the thresholds wj∗. Suppose a proposes a policy that gives voter j = a a payoff lower

than wa∗. Then he forgoes re-election, receiving a payoff at most 3y − r. This is because

his best deviation from q∗ is the policy τ = 1, g = f j = 0, all j and ra = 3y − r, rb = r,

rc = 0, where b is either of the other two legislators and c is the third. But by proposing q∗

he gets exactly 3y −R− r +R = 3y − r, so he is indifferent. On the other hand, it cannot

be optimal for him to give voter j = a a payoff higher than wa∗, since this eats into his

own resources (and we will show below that g∗ and fa∗ have been chosen by voter j = a

optimally).

Finally, note that it is optimal for wb∗ = wc∗ = H(g∗). If either b or c ask for more,

then q∗ will pass anyway. Likewise, it does not make sense to ask for less. Finally, voter

j = a sets wj∗ according to the following problem

maxqwa∗ = y − τ + fa +H(g)

subject to (BC) and ra ≥ 3y −R− r

In other words, he maximizes his payoff subject to the budget constraint and the incentive

constraint that legislator a wants to propose a policy that gets him re-elected. The solutions

are given in the statement of the proposition. Pork transfers to district a are positive, and

the equilibrium level of the public good is affordable by Assumptions 2 and 4 respectively.

By Assumption 3, legislator a captures positive rents.

We immediately have the following corollary.

22

Figure 6: The Congressional Committees Game

Corollary 1: The equilibrium level of the public good is lower than the Samuelson

level (social planner’s optimum):

g∗ < gsp

Bonus Exercise. (This exercise is optional.) Complete the proof of Proposition 3, i.e.

show that all equilibria of the game are path-equivalent.

Exercise. (Congressional Committees) The congressional policy game is like the game

above, except that there are two different agenda setters aτ and ag, the finance committee

and the expenditure committee, that are selected by nature at the start of the game. Voters

set their utility cutoffs wj as before. aτ proposes the tax rate τ and an up or down vote is

held. If the proposal fails then an exogenous τ0 ∈ (0, r), r < y. Then ag proposes g, (f j)j

and (rl)l subject to the budget constraint (BC) where τ here is the tax proposal that passes

or τ0 if the proposal fails to pass. Then again a vote takes place on ag’s proposal. If the

proposal fails then g = 0, f j = τ − rl ≥ 0, all j, and rl = r, all l, is implemented. Finally,

elections are held. (See Figure 6.)

Maintain Assumptions 1-4 and characterize the equilibria of the Congressional Com-

mittees game, showing in particular that the equilibrium level of the public good is unique

and under-provided, as before. Specifically,

g∗ = (z)1/α

Exercise. (Parliamentary Regimes) Now consider a parliamentary model depicted in

Figure 7. Nature selects the expenditure and finance ministers, ag and aτ . Voters set their

reservation utilities wj as before. The finance minister, aτ , proposes τ . The expenditure

minister ag proposes(g, (f j)j , (rl)l

)subject to (BC) given the proposed tax rate τ . Either

23

Figure 7: The Parliamentary Game

member of government ag or aτ can veto the aggregate proposal q =(τ, g, (f j)j , (rl)l

).

If neither does, then the proposal passes, and elections are held. If one of them vetoes,

government collapses and a legislator is selected randomly (i.e. each with probability 1/3)

to form a caretaker government. Voters then set new reservation utilities wj . The caretaker

makes an entire budget proposal q′ =(τ ′, g′, (f ′j)j , (r

′l)l

)which passes or fails by simple

majority. If it fails then the following default policy is implemented:

τ0 = r g0 = 0 rl = r, ∀l f j = 0, ∀j

Maintain Assumptions 1-4 and show that there is an equilibrium in which the level of the

public good supplied is larger than the level supplied in the congressional committees regime,

but lower than the Samuelson level, the sum total of equilibrium rents in the parliamentary

regime is larger than the sum total of equilibrium rents in the congressional committees

regime, and taxes are higher under the parliamentary regime than under the congressional

committees regime.

24

2 Dynamic Methods, etc.

I assume that you have some familiarity with this material. If you do not, please consult a

good textbook, such as Mailath and Samuelson’s (2006) Repeated Games and Reputations

and Daron Acemoglu’s (2008) Modern Economic Growth.

2.1 Infinite Horizon Dynamic Programming

We consider an infinite horizon stationary discounted dynamic programming problem as

follows. Here, I simply state the main results of dynamic programming, leaving it to you

to discover the proofs if necessary.

Suppose time is discrete and indexed by t = 0, 1, 2...,∞. Let δ ∈ [0, 1) be a discount

factor. Let X ⊆ Rm be the set of control variables. Let G : X → 2X be a correspondence

from X to itself and u : X × X → R an instantaneous reward or payoff function. The

canonical stationary dynamic program is

maxxt∞t=0

U(xt∞t=0) ≡∞∑t=0

δtu(xt, xt+1)

subject to xt+1 ∈ G(xt) for all t ≥ 0 and x0 = x ∈ X (P)

A solution to this problem may or may not exist. If it exists, then label it x∗t ∞t=0 and let

U∗ be the value of U attained at this solution, i.e. U∗ = U(x∗t ∞t=0).

For any t ≥ 0, it will be useful to define the set of feasible “plans” starting with an

initial value xt ∈ X as

Φ(xt) = xs∞s=t : xs+1 ∈ G(xs), s = t, t+ 1, ...,∞

Now define a completely new function V : X → R such that

∀x ∈ X V (x) = maxy∈G(x)

u(x, y) + δV (y) (B)

Again, such a function may or may not exist. The equality in (B) is called a “Bellman

equation” and the function V is called a “value function.”

Consider the following assumption.

Assumption A: X is compact; G is continuous, nonempty-, convex-, and compact-

valued, and it is monotone in the sense that x ≤ x′ implies G(x) ⊂ G(x′); and u is

continuously differentiable on int X×X, strictly concave, and strictly increasing in its first

m arguments; and, for all x0 ∈ X and plans xt∞t=0 ∈ Φ(x0), the following limit exists and

is finite:

limn→∞

n∑t=0

δtu(xt, xt+1)

25

Then we immediately have the following result.

Theorem A: Suppose Assumption A holds. Then:

(i) A plan x∗t ∞t=0 solving (P) exists for all starting values x∗0 = x ∈ X, and this plan

can be expressed as a recursion

x∗t+1 = π(x∗t )

where π : X → X is a continuous function (called a “policy function”).

(ii) There exists a unique, continuous, strictly concave and bounded function V that

satisfies the Bellman equation (B) and is strictly increasing in all of its arguments.

In particular, x∗t ∞t=0 is a solution to (P) if and only if

V (x∗t ) = u(x∗t , x∗t+1) + δV (x∗t+1)

And, moreover, let π be a policy function as in (i) above. If x ∈ int X and π(x) ∈int G(x) then V is differentiable at x with gradient given by

∇V (x) = ∇xu(x, π(x))

(∇x is the gradient operator applied to x, i.e. the first m arguments of u.)

The theorem implies that under Assumption A, the maximization problem in (B) is

strictly concave and the maximand is differentiable. So for any interior solution y∗ ∈ G(x),

the first order conditions are necessary and sufficient for an optimum. Optimal solutions

are characterized by the Euler equation:

∇yu(x, y∗) + δ∇V (y∗) = 0 (Euler)

where y∗ is the optimal value and ∇y is the gradient operator applied to y, i.e. the last m

arguments of u. The Euler equation is simply a first order condition. We could use it to

solve for the optimal policy y∗ if we knew the functional form of V ; but the theorem does

not tell us that.

Fortunately, we can differentiate the Bellman equation (B) with respect to x to obtain an

Envelope condition for dynamic programming. (This is essentially the same as the standard

Envelope condition that you know from optimization theory.) The optimal value y∗ in (B)

will depend on x; in particular, the theorem implies y∗ = π(x). Then, apply the implicit

function theorem to (B) to get

∇V (x) = ∇xu(x, π(x)) + [∇yu(x, π(x)) + δ∇V (π(x))]∇π(x)

26

But by the Euler equation above, the term in square brackets is 0, so we are left with

∇V (x) = ∇xu(x, π(x)) (Envelope)

which is the Envelope condition. This condition must hold for all x ∈ int X, in particular

it must hold at π(x). So, we have

∇V (π(x)) = ∇xu(π(x), π(π(x)))

We can combine this with the Euler equation to get

∇yu(x, π(x)) + δ∇xu(π(x), π(π(x))) = 0

This condition characterizes the optimal policy function π in terms of the one period reward

function u. This condition is, however, only necessary. For sufficiency, we also need what

is called a “transversality condition” but we will not discuss that here.

2.2 Dynamic Game Theory

Time is discrete and indexed by t = 0, 1, 2, ...,∞. There are I players. In each period, each

player i takes an action from the set Ai(s) ⊂ Ai ⊆ Rn. The action set is written to depend

on the state s ∈ S ⊂ Rm. The action taken by i in period t is written ait. The action profile

is at = (a1t , ..., a

It ). As usual, a−it denotes the action profile of all players other than i. Each

player i has an instantaneous utility function ui(s, a) over states s and action profiles a.

Each player’s objective at time t is to maximize the discounted payoff

U it (st) = Et∞∑j=0

δjui(st+j , at+j) (Obj)

where st+j is the state at time t + j and at+j is the action profile at that time, and Etis the expectations operator conditional on information available at time t. Since we only

work with models where all information is public, we do not index the expectation by i.

We take this expectation because we allow the state to evolve stochastically. δ ∈ (0, 1) is

the discount factor.

The state evolves according to a Markov process in which q(st+1|st, at) denotes the

probability (or density) that the state is st+1 given that the state was st today and players

chose actions at. If players use pure strategies, then a history at time t is simply

ht = (s0, a0, s1, a1, ..., st−1, at−1)

with the convention h0 = ∅. The set of all possible histories at time t is denoted Ht, and

H =⋃tH

t. Each history corresponds to a particular subgame. A (pure) strategy for player

27

i is a function

αi : H × S → Ai s.t. αi(ht, s) ∈ Ai(s) ∀s ∈ S, ∀ht ∈ Ht, ∀t

Again, α−i has the usual interpretation. A best response correspondence at time t for player

i is simply

BR(α−i|ht, st) = αi : αi maximizes (Obj) given α−i, ht and st

So, a subgame perfect equilibrium (SPE) is a strategy profile α = (α1, ..., αI), such that

αi ∈ BR(α−i|ht, st) for all histories ht ∈ Ht, states s ∈ S, players i, and periods t. A

Markov perfect equilibrium (MPE) is an SPE in which

αi(ht, st) = αi(ht′ , st) ∀ht 6= ht′ , ∀i

Theorem B: If S and Ai are finite sets, then MPE exist.

Exercise. Suppose there are I + 1 <∞ players, each with payoffs

∞∑j=0

δj log(cit+j)

at time j, where δ ∈ (0, 1) is a discount factor and cit+j denotes consumption of individual

i at time t+ j. The society owns a resource of amount Rt, which satisfies

Rt+1 = QRt −∑i

cit

where Q > 0 and R0 is given and consumptions cit must be chosen so that Rt ≥ 0 every

period. At each date t all players simultaneously announce the amount they wish to consume

cit. If∑

i cit ≤ QRt, then each individual consumes cit. If

∑i cit > QRt then QRt is equally

divided among the I + 1 players.

1. Suppose that cit are chosen by a social planner that maximizes

I+1∑i=1

∞∑j=0

δj log(cit+j)

every period t. Show that the social planner’s value function V as a function of the

resource stock R is uniquely defined, continuous, concave, and differentiable. Also

show that the saving level of the resource is π(R) = δQR.

28

2. Show that there is a symmetric MPE in which the state is the resource stock R, all

players’ consumptions are continuous in the state, the aggregate savings level in the

economy is given by

π(R) =δQR

1 + I − δI

3. Show that under this MPE, the resource stock shrinks over time.

4. Characterize the set of δ such that there exist SPEs that implement the social plan-

ner’s solution.

2.3 Weak and Strong States (Acemoglu 2005)

There is ruler who rules over a continuum of citizens of unit mass. Each citizen has an

instantaneous payoff over consumption ct and effort et in each period t, given by

u(ct, et) = ct − et (1)

Each citizen has access to the Cobb-Douglas production technology

yt =1

1− αAαt (et)

1−α (2)

where A is the level of public good in the economy. A will be determined by the investment

of the ruler. The ruler sets a linear tax rate τt on individual income yt in period t. Each

citizen can decide to hide a fraction zit of his output, which is not taxable, but hiding is

costly and ρ units are lost in the process. So given τt, the consumption of agent i is

cit =[(1− τt)(1− zit) + (1− ρ)zit

]yit (3)

where revenues are

Tt = τt

∫(1− zit)yitdi (4)

If the ruler spends Gt on the public good then the following units of it are produced to be

used in the following period

At+1 =

[(1− α)φ

αGt

]1/φ

(5)

where φ > 1 is a parameter. A0 > 0 is given. The consumption of the ruler is what is left

over:

Tt −Gt (6)

The timing of events within each period t is

1. the economy inherits At from the ruler’s choice of Gt−1

29

2. citizens exert effort eit

3. the ruler sets τt, collects revenue and decides how much to spend Gt on next period’s

public good

4. citizens decide how much of their output to hide zit

All players share a discount factor δ ∈ (0, 1) and maximize the discounted sum of their

consumption net of effort. (The ruler exerts no effort.)

Exercise. Suppose a social planner chooses effort levels eit for everyone, hiding fractions

zit for everyone, taxes τt and the public good investments Gt in every period. Suppose the

planner chooses these quantities to maximize the sum of output net of effort. Suppose the

ruler is infinitesimal (since there is a continuum of citizens, he is just another massless dot

on the continuum). Show that for all t > 0, the planner’s choices result in:

At = δ1/(φ−1) eit = δ1/(φ−1) ∀i yit =1

1− αδ1/(φ−1) ∀i

Now, we characterize the MPE. An MPE for this model is simply a set of choices(eit, τt, zit, Gt

)that depend only on the payoff relevant state At of the game, and on

prior actions within the same period, but not on actions in previous periods. The convenient

feature of MPEs is that we can use backward induction within a period.

Since citizens are small and anonymous, they maximize their current income, so

zit =

1 if τt > ρ

x ∈ [0, 1] if τt = ρ

0 if τt < ρ

(7)

So the optimal tax rate for the ruler is

τt = ρ (8)

and the citizens hide nothing so zit = 0. Citizens will thus maximize (1) subject to (2), (3),

(8) and their hiding decision zit = 0. This results in

eit = (1− ρ)1/αAt (9)

This implies that revenues from taxes are

T (At) =(1− ρ)(1−α)/αρAt

1− α(10)

30

Finally, the ruler chooses public investment Gt to maximize his consumption. The Bellman

equation for the net present value of the ruler is

V (At) = maxAt+1

T (At)−

α

(1− α)φAφt+1 + δV (At+1)

(11)

Note that Assumption A is satisfied so that this value function V (·) is strictly concave and

continuously differentiable. So the first order condition (Euler equation) for the ruler in

choosing At+1 is simplyα

1− αAφ−1t+1 = δV ′(At+1) (12)

The envelope condition is

V ′(At) = T ′(At) =(1− ρ)(1−α)/αρ

1− α(13)

Combining these two conditions, we arrive at the full characterization of the MPE:

Gt =δ(1− ρ)(1−α)/αρA [δ]

(1− α)φ(14)

where A [δ] =(δ(1− ρ)(1−α)/αρ/α

)1/(φ−1). The aggregate output in the economy is

Yt =1

1− α(1− ρ)(1−α)/αA[δ] (15)

And, the ruler’s equilibrium value function is

V ∗(At) =(1− ρ)(1−α)/αρAt

1− α+δ(φ− 1)(1− ρ)(1−α)/αρ

(1− δ)φ(1− α)A[δ] (16)

Acemoglu (2005) argues that when ρ is high “the state is ‘economically powerful’—

citizens have little recourse against high rates of taxes. In contrast, when ρ is low, the

state is ‘economically weak’ (and there is ‘limited government’), since it is unable to raise

taxes.’ Does greater economic strength lead to worse economic outcomes? The answer is

ambiguous, since ρ = 0 the ruler sets Gt = 0 and when ρ = 1 the citizens do not work.

Given the MPE, the value of ρ that maximizes output Yt above is

ρ∗ =α

φ(1− α) + α(17)

If ρ > ρ∗, the state is too powerful, whereas if ρ < ρ∗ the state is too weak. (This is the

problem of “weak states;” think of those in subsaharan Africa.)

Exercise. Let ρr be the value of ρ that maximizes the value function of the ruler from

the first period onwards, so: ρr = arg maxρ V∗(A0). Show that ρr = α. Similarly, let ρc be

the utility maximizing value of ρ for the citizens, i.e. ρc = arg maxρ U0(A0) where

U0(A0) =α

1− α(1− ρ)1/αA0 +

δ

1− δα

1− α(1− ρ)1/αA[δ]

31

Show that ρc = α/φ. Finally, let ρwm be the value of ρ that the social planner in the above

exercise would choose in period 0. Show all of the following:

0 < ρc < ρ∗ < ρr < 1 0 < ρc < ρwm < ρr < 1

The exercise shows that the citizens want state capacity to be lower than socially opti-

mal, whereas the ruler wants state capacity to be higher than socially optimal. Excessively

weak and excessively strong states are both bad; there should be a balance of power between

citizens and the ruler.

2.4 Political Transitions (Acemoglu & Robinson 2001)

Nondemocratic Politics. Time is discrete and indexed by t = 0, 1, 2, ...,∞. There is a

continuum of citizens of unit mass partitioned into two classes: the (rich) elite and (poor)

citizens. Each elite person has income yr in each period, and each poor person has income

yp in each period. Fraction 1 − λ > 1/2 of the population is poor. Mean income is y. Let

θ be the share of total income accruing to the rich. So we have

yp =(1− θ)y

1− λyr =

θy

λ(1)

You can verify that the assumption θ > λ is equivalent to the only sensible ordering

yp < y < yr (2)

We will assume that in each period t, revolution takes place ρt = 1 or it does not take

place ρt = 0. If revolution has never taken place in the past, ρt′ = 0 for all t′ ≤ t, then a

linear tax rate τt is implemented and all government revenue is redistributed as un-targeted

lump sum transfers. The function c(τt)y measures the dead-weight loss due to taxation, so

government revenues in period t are given by

Tt = τt((1− λ)yp + λyr)− c(τt)y = (τt − c(τt))y (3)

You can take the rate of dead-weight loss to be the function

c(τ) =τ2

2γ(4)

where 0 < γ < 1. If δ is a common discount factor, then at each time t, a voter of type

i = p, r has utility

uit = (1− δ)[(1− ρt)

[(1− τt)yi + (τt − c(τt))

]y + ρty

iR

](5)

32

where yiR is the payoff to an individual of type i in any every period following a revolution.

The indicator ρt indicates that revolution has taken place at some time in the past t′ ≤ t.If a revolution is attempted at time t then fraction µt of everyone’s income in that period

is destroyed. We assume that µt is an economic state variable equal to either 1 or µ in each

period, where µ ∈ (0, 1). We assume that the state is i.i.d. across periods and in particular

µt = 1 with probability 1− q and µt = µ with probability q in each period. We assume that

ypR =(1− µs)y

1− λ(6)

and yrR = 0, where s indicates the period in which revolution took place. This is tantamount

to assuming that if revolution does take place in period s then total income is smaller by

a fraction µs in every period thereafter, and citizens fully expropriate the rich and divide

the money evenly amongst themselves.

Now, the timing of events within each period t is as follows:

1. The state µt is publicly revealed.

2. If revolution has occurred in the past ρt = 1, then each agent of type i = p, r receives

yiR and the period ends. If it has never occurred in the past ρt = 0, then:

(a) An elite person sets the tax rate τt = τNt .

(b) Each citizen decides whether or not to revolt.

(c) If at least ξp ∈ (0, 1) fraction of them revolt then revolution takes place ρt = 1

and payoffs yiR are received. If revolution does not take place ρt = 0 then the

tax rate τNt is implemented and each person receives his post-fisc payoff and the

period ends.

We characterize the Markov perfect equilibrium (MPE) of the game. In an MPE all

agents can condition their behavior on the current state µt and past actions chosen by them

and others within the same period, but not in previous periods.

Let V i(R,µs) be the value to each individual of type i = p, r if there is a revolution that

took place when the state was µs ∈ 1, µ. This value is thus

V p(R,µs) =(1− µs)y

1− λV r(R,µs) = 0 (7)

Now, let us characterize value functions for i = p, r in political states N where the elite

are in power. Clearly, no citizen would ever revolt when the state is µt = 1. Therefore, in

these states, the elite will set the tax rate τNt = 0. Thus, in states µt = 1, we have the

following Bellman equations for the values of the elite and citizens

V i(N, 1) = (1− δ)yi + δ[qV i(N, 1) + (1− q)V i(N,µ)

](8)

33

We need to characterize V i(N,µ), and then we can solve for V i(N, 1) using the above

Bellman equation. The Markovian structure of the game and equilibrium concept enables

us to conduct the following analysis. Let V i(N) denote the value that would apply to

i = p, r if revolution never took place when the state is µ and the elite set τt = 0 in such

states. Then we have V i(N) = yi. Say that the revolution constraint binds if the poor

prefer to revolt, i.e. if V p(R,µ) > V p(N), which plugging in values is equivalent to

θ > µ (9)

In other words, inequality should be sufficiently high for the revolution constraint to bind.

Now suppose that when the revolution constraint binds, the elite set a tax rate τ > 0

whenever the state is µ. Therefore, the value to i when elites set tax τ in states µ and

revolution is avoided is given by the Bellman equation

V i(N,µ, τ) = (1− δ)[yi +

(τ(y − yi)− c(τ)y

)]+ δ

[qV i(N,µ, τ) + (1− q)V i(N, 1)

](10)

Citizens would like to revolt if

V p(R,µ) > V p(N,µ, τ) (11)

The elite would like to avoid revolution at all costs, but the best they can do is give each

poor citizen his most preferred tax rate τp that solves

θ − λ1− λ

= c′(τp) (12)

=⇒ τp = γ

(θ − λ1− λ

)(13)

If V p(N,µ, τp) ≥ V p(R,µ) then a revolution can be averted, but not otherwise. To derive

an expression for V p(N,µ, τp), substitute V p(N,µ, τp) = V p(N,µ) into (8) and solve with

(10) to get

V p(N,µ, τp) = yp + (1− δ(1− q))(τp(y − yp)− c(τp)y) (14)

So, revolution can be averted only if

µ ≥ θ − (1− δ(1− q))(τp(θ − λ)− (1− λ)c(τp)) (15)

So, we can define a critical value of µ, call it µ∗, such that the above inequality holds as

equality. Clearly µ∗ < θ. (Why?) If µ ≥ µ∗ then revolution can be averted, but if µ < µ∗

then it cannot. In the case where revolution can be averted, we can define the optimal tax

rate for the elite, τ∗, that averts revolution to be the one that solves

µ = θ − (1− δ(1− q))(τ∗(θ − λ)− (1− λ)c(τ∗)) (16)

34

We now have the following result:

Result: The MPE predictions of the game are unique.

1. If θ ≤ µ, the elite never redistribute and the citizens never undertake revolution.

2. If θ > µ then

(a) if µ < µ∗, promises by the elite are insufficiently credible to avoid a revolution:

If µt = 1 then the elite do not redistribute, and no revolution takes place. If

µt = µ then revolution takes place whatever the tax the elite set.

(b) if µ ≥ µ∗ the elite do not redistribute when µt = 1, and they set the tax rate

equal to τ∗ when µt = µ, which is just enough to stop a revolution. The citizens

never revolt.

Democratization. We assume that the game is exactly as before, except now the elite

have three tools at their disposal to avert the threat of revolution. As before, they can offer

a one-period concessionary tax rate τ . Alternatively, they can repress the citizens, which

is costly but always averts revolution. Finally, they can relinquish power to the citizens

by creating democracy. Like revolution, democracy is an “absorbing” political state in this

section: once it is created, the median voter (who is a poor agent, since the poor are a

majority) sets his most preferred tax rate τp in every period after. The timing is now

1. The state µt is publicly revealed.

2. If revolution has occurred at any point in the past ρt = 1, then each agent of type

i = p, r receives yiR and the period ends. If democratization has ever occurred in the

past φt = 1, then the tax rate τp given in (13) is set by the median voter and the

period ends.

3. If neither democratization nor revolution have occurred in the past ρt = φt = 0, then

the elite decide whether to repress ω = 1 or not ω = 0. If repression takes place then

each agent i = p, r gets income (1− κ)yi and the period ends. If repression does not

take place, then the elite decide whether to democratize φt = 1 or not φt = 0. If they

democratize then τp gets set by the median voter and the period ends. If they do

not, then

(a) An elite person sets the tax rate τt = τNt .

(b) Each citizen decides whether or not to revolt.

35

(c) If at least ξp ∈ (0, 1) fraction of them revolt then revolution takes place ρt = 1

and payoffs yiR are received. If revolution does not take place ρt = 0 then the

tax rate τNt is implemented and each person receives his pos-fisc payoff and the

period ends.

So, the important states are (R,µs), (N,µt) and D. The first one (R,µs) means that

revolution happened when the state was µs; the second one (N,µt) means the elite are in

power and the state is µt; and the third D means that democracy was created at some point

in the past. We characterize MPE. Again, the values V i(R,µs) are given by (7).

In state (N, 1), the elite are in power and there is no threat of revolution, so φ = ω = 0

and τN = 0. So the Bellman equation for this state is again given by (8).

The revolution constraint in states (N,µ) is again given by (9). Suppose that the elite

set tax rate τ in states (N,µ) in the event that they don’t repress. Let V i(O,µ|κ) be the

value to agent i = p, r when elites use repression to avert revolution in states (N,µ). Then

the payoff to a citizen is

V p(N,µ) = ωV p(O,µ|κ)+

(1− ω) maxρ∈0,1

[ρV p(R,µ) + (1− ρ)(φV p(D) + (1− φ)V p(N,µ, τ)] (17)

Here V p(D) is the value of democracy to a poor citizen, and V p(N,µ, τ) is the value of

receiving the concessionary tax rate τ . If the elite choose to redistribute rather than de-

mocratize in states (N,µ) then citizens get the value in (10). Revolution is then avoided

via a concessionary tax rate τ∗ solving (16) only if µ ≥ µ∗. If µ < µ∗ then the elite must

either democratize or repress.

The returns from democracy are

V p(D) = yp + τp(y − yp)− c(τp)y V r(D) = yr + τp(y − yr)− c(τp)y (18)

Democratization would prevent revolution if V p(D) ≥ V p(R,µ). This is equivalent to

µ ≥ θ − (τp(θ − λ) + (1− λ)c(τp)) (19)

The value of µ, call it µ∗∗, that equalizes this inequality is smaller than µ∗. Note that the

elite always prefer to avoid revolution via the concessionary tax rate τ instead of democra-

tizing. (Why?) To determine whether they prefer to repress rather than democratize or use

the one-period concessionary tax rate τ , let us derive their value from repression. Indeed,

we have

V i(O,µ|κ) = (1− δ)(1− κ)yi + δ[qV i(O,µ|κ) + (1− q)V i(O, 1|κ)

](20)

V i(O, 1|κ) = (1− δ)yi + δ[qV i(O,µ|κ) + (1− q)V i(O, 1|κ)

](21)

36

which takes into account that the cost of repression κ will only be incurred in states where

the revolution threat is binding. These Bellman equations imply

V i(O,µ|κ) = yi − (1− δ(1− q))κyi (22)

To understand whether or not repression occurs we compare V r(O,µ|κ) to V r(D) when

µ < µ∗∗ and to V r(N,µ, τ∗) when µ ∈ [µ∗∗, µ∗). Note that the critical value of κ that

makes V r(O,µ|κ) = V r(N,µ, τ) is

κ∗ =1

θ(λc(τ)− τ(λ− θ)) (23)

The critical value of κ that makes V r(O,µ|κ) = V r(D) is

κ∗∗ =1

1− δ(1− q)(λc(τp)− τp(λ− θ)) (24)

We now have the following

Result: In MPE, we have the following

1. If θ ≤ µ, then the revolution constraint does not bind and the elite can stay in power

without repressing, redistributing or democratizing.

2. If θ > µ, then the revolution constraint binds, and

(a) if µ > µ∗ and κ ≥ κ∗, repression is costly and the elite redistribute income in

state µ at rate τ∗ to avoid revolution

(b) if µ < µ∗ and κ < κ∗∗, or µ < µ∗∗ and κ > κ∗, or if µ > µ∗ and κ < κ∗, then

the elite use repression in state µ

(c) if µ∗∗ < µ < µ∗ and κ ≥ κ∗∗ concessions are insufficient to avoid a revolution

and repression is relatively costly, so the elite democratize the first time the

state µ is reached.

We can draw a graph to depict this result.

Exercise (Political Transitions). The game is similar to that of the previous section,

except now democracy is no longer an absorbing state. Now, in a democracy, the median

voter sets the tax rate strategically considering the incentives of the elite to mount a coup.

In each period t, there is an additional state variable ψt ∈ ψ, 1 drawn i.i.d. like µt, with

a denoting the probability that ψt equals ψ. Assume that both q and a are smaller than

1/2. If a coup is mounted in period t then all agents lose fraction ψt of their income in that

period. The game begins in the political state N with the elite in power. The timing of

events is as follows.

37

1. The state (µt, ψt) is publicly revealed.

2. If the political state is democracy D, then the citizens set a tax rate τDt ; if the political

state is nondemocracy N then the elite set a tax rate τNt .

3. In a nondemocracy N , the elite decide whether or not to repress ω and whether or not

to democratize φ. In a democracy D, they decide whether to mount a coup ζ. If they

democratize or undertake a coup, the party that comes to power decides whether to

keep the tax rate set in step 2 or set a new tax rate.

4. If the political state is nondemocracy N and ω = 0 so the citizens have not been

repressed, then the citizens decide whether or not to initiate a revolution ρ. If there

is a revolution, agents get yiR. If there is no revolution, then the tax rate set in step

2 or 3 is implemented.

Characterize the MPE and show that for some parameter values, society is able to enter

into a “consolidated democracy” where democratization takes place the first time µt = µ,

and democracy survives forever after; for other parameter values society cycles back and

forth between democracy and nondemocracy, as a result of elite’s mounting coups and

democratizing in response to revolution threats; and for yet other parameter values society

never democratizes. When is repression used? How does inequality, as measured by θ, affect

society’s likelihood of being a permanent autocracy, a consolidated democracy or a semi-

consolidated democracy that flip-flops back and forth between democracy and dictatorship?

Draw a nice picture (like the one we drew in class) to illustrate your findings.

2.5 Global Games (Carlsson & van Damme 1993)

The issues underlying this digression are so important, you cannot afford to misunderstand

them.

Probably most games that you write down will have multiple equilibria. Why do games

have multiple equilibria? What does this mean for applied game theory? Let’s begin by

writing down a two-player binary action game with payoff.