Epic research special report of 16 sep 2015

8

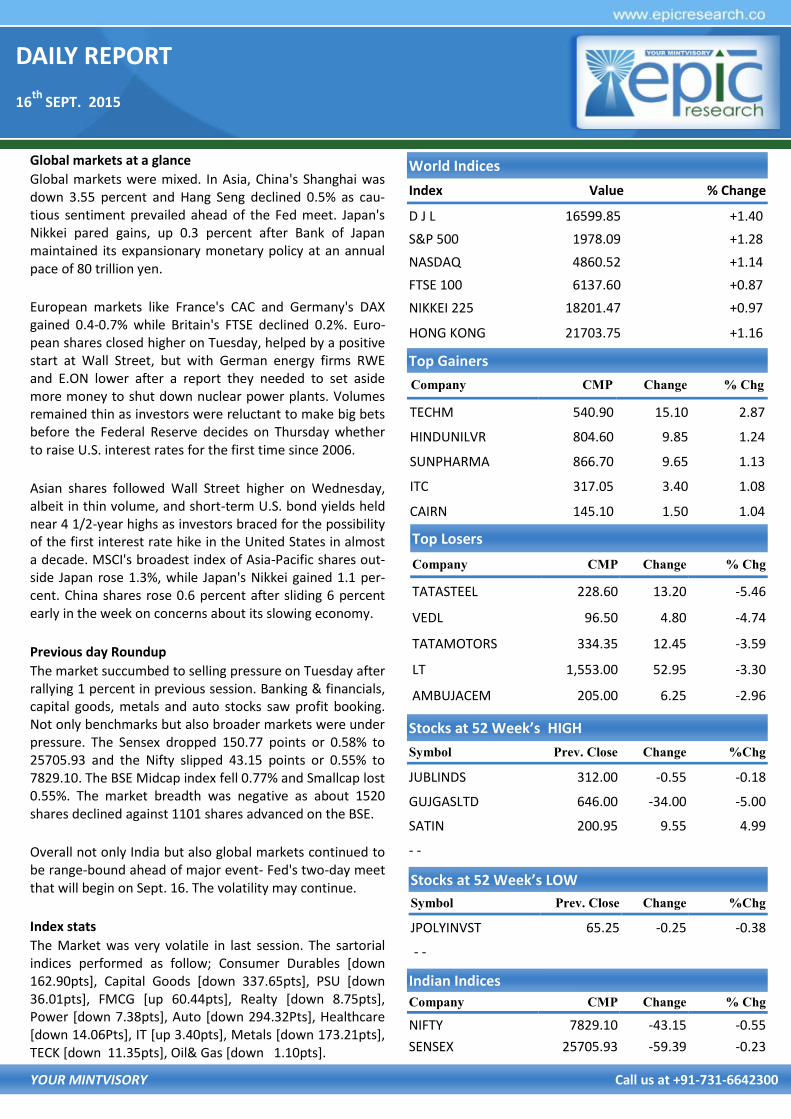

DAILY REPORT 16 th SEPT. 2015 YOUR MINTVISORY Call us at +91-731-6642300 Global markets at a glance Global markets were mixed. In Asia, China's Shanghai was down 3.55 percent and Hang Seng declined 0.5% as cau- tious sentiment prevailed ahead of the Fed meet. Japan's Nikkei pared gains, up 0.3 percent after Bank of Japan maintained its expansionary monetary policy at an annual pace of 80 trillion yen. European markets like France's CAC and Germany's DAX gained 0.4-0.7% while Britain's FTSE declined 0.2%. Euro- pean shares closed higher on Tuesday, helped by a positive start at Wall Street, but with German energy firms RWE and E.ON lower after a report they needed to set aside more money to shut down nuclear power plants. Volumes remained thin as investors were reluctant to make big bets before the Federal Reserve decides on Thursday whether to raise U.S. interest rates for the first time since 2006. Asian shares followed Wall Street higher on Wednesday, albeit in thin volume, and short-term U.S. bond yields held near 4 1/2-year highs as investors braced for the possibility of the first interest rate hike in the United States in almost a decade. MSCI's broadest index of Asia-Pacific shares out- side Japan rose 1.3%, while Japan's Nikkei gained 1.1 per- cent. China shares rose 0.6 percent after sliding 6 percent early in the week on concerns about its slowing economy. Previous day Roundup The market succumbed to selling pressure on Tuesday after rallying 1 percent in previous session. Banking & financials, capital goods, metals and auto stocks saw profit booking. Not only benchmarks but also broader markets were under pressure. The Sensex dropped 150.77 points or 0.58% to 25705.93 and the Nifty slipped 43.15 points or 0.55% to 7829.10. The BSE Midcap index fell 0.77% and Smallcap lost 0.55%. The market breadth was negative as about 1520 shares declined against 1101 shares advanced on the BSE. Overall not only India but also global markets continued to be range-bound ahead of major event- Fed's two-day meet that will begin on Sept. 16. The volatility may continue. Index stats The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [down 162.90pts], Capital Goods [down 337.65pts], PSU [down 36.01pts], FMCG [up 60.44pts], Realty [down 8.75pts], Power [down 7.38pts], Auto [down 294.32Pts], Healthcare [down 14.06Pts], IT [up 3.40pts], Metals [down 173.21pts], TECK [down 11.35pts], Oil& Gas [down 1.10pts]. World Indices Index Value % Change D J L 16599.85 +1.40 S&P 500 1978.09 +1.28 NASDAQ 4860.52 +1.14 FTSE 100 6137.60 +0.87 NIKKEI 225 18201.47 +0.97 HONG KONG 21703.75 +1.16 Top Gainers Company CMP Change % Chg TECHM 540.90 15.10 2.87 HINDUNILVR 804.60 9.85 1.24 SUNPHARMA 866.70 9.65 1.13 ITC 317.05 3.40 1.08 CAIRN 145.10 1.50 1.04 Top Losers Company CMP Change % Chg TATASTEEL 228.60 13.20 -5.46 VEDL 96.50 4.80 -4.74 TATAMOTORS 334.35 12.45 -3.59 LT 1,553.00 52.95 -3.30 AMBUJACEM 205.00 6.25 -2.96 Stocks at 52 Week’s HIGH Symbol Prev. Close Change %Chg JUBLINDS 312.00 -0.55 -0.18 GUJGASLTD 646.00 -34.00 -5.00 SATIN 200.95 9.55 4.99 - - Indian Indices Company CMP Change % Chg NIFTY 7829.10 -43.15 -0.55 SENSEX 25705.93 -59.39 -0.23 Stocks at 52 Week’s LOW Symbol Prev. Close Change %Chg JPOLYINVST 65.25 -0.25 -0.38 - -

-

Upload

epic-research-limited -

Category

Business

-

view

221 -

download

0

Transcript of Epic research special report of 16 sep 2015

DAILY REPORT

16th

SEPT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

Global markets at a glance

Global markets were mixed. In Asia, China's Shanghai was down 3.55 percent and Hang Seng declined 0.5% as cau-tious sentiment prevailed ahead of the Fed meet. Japan's Nikkei pared gains, up 0.3 percent after Bank of Japan maintained its expansionary monetary policy at an annual pace of 80 trillion yen.

European markets like France's CAC and Germany's DAX gained 0.4-0.7% while Britain's FTSE declined 0.2%. Euro-pean shares closed higher on Tuesday, helped by a positive start at Wall Street, but with German energy firms RWE and E.ON lower after a report they needed to set aside more money to shut down nuclear power plants. Volumes remained thin as investors were reluctant to make big bets before the Federal Reserve decides on Thursday whether to raise U.S. interest rates for the first time since 2006.

Asian shares followed Wall Street higher on Wednesday, albeit in thin volume, and short-term U.S. bond yields held near 4 1/2-year highs as investors braced for the possibility of the first interest rate hike in the United States in almost a decade. MSCI's broadest index of Asia-Pacific shares out-side Japan rose 1.3%, while Japan's Nikkei gained 1.1 per-cent. China shares rose 0.6 percent after sliding 6 percent early in the week on concerns about its slowing economy.

Previous day Roundup

The market succumbed to selling pressure on Tuesday after rallying 1 percent in previous session. Banking & financials, capital goods, metals and auto stocks saw profit booking. Not only benchmarks but also broader markets were under pressure. The Sensex dropped 150.77 points or 0.58% to 25705.93 and the Nifty slipped 43.15 points or 0.55% to 7829.10. The BSE Midcap index fell 0.77% and Smallcap lost 0.55%. The market breadth was negative as about 1520 shares declined against 1101 shares advanced on the BSE.

Overall not only India but also global markets continued to be range-bound ahead of major event- Fed's two-day meet that will begin on Sept. 16. The volatility may continue.

Index stats

The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [down 162.90pts], Capital Goods [down 337.65pts], PSU [down 36.01pts], FMCG [up 60.44pts], Realty [down 8.75pts], Power [down 7.38pts], Auto [down 294.32Pts], Healthcare [down 14.06Pts], IT [up 3.40pts], Metals [down 173.21pts], TECK [down 11.35pts], Oil& Gas [down 1.10pts].

World Indices

Index Value % Change

D J L 16599.85 +1.40

S&P 500 1978.09 +1.28

NASDAQ 4860.52 +1.14

FTSE 100 6137.60 +0.87

NIKKEI 225 18201.47 +0.97

HONG KONG 21703.75 +1.16

Top Gainers

Company CMP Change % Chg

TECHM 540.90 15.10 2.87

HINDUNILVR 804.60 9.85 1.24

SUNPHARMA 866.70 9.65 1.13

ITC 317.05 3.40 1.08

CAIRN 145.10 1.50 1.04

Top Losers

Company CMP Change % Chg

TATASTEEL 228.60 13.20 -5.46

VEDL 96.50 4.80 -4.74

TATAMOTORS 334.35 12.45 -3.59

LT 1,553.00 52.95 -3.30

AMBUJACEM 205.00 6.25 -2.96

Stocks at 52 Week’s HIGH

Symbol Prev. Close Change %Chg

JUBLINDS 312.00 -0.55 -0.18

GUJGASLTD 646.00 -34.00 -5.00

SATIN 200.95 9.55 4.99

- -

Indian Indices

Company CMP Change % Chg

NIFTY 7829.10 -43.15 -0.55

SENSEX 25705.93 -59.39 -0.23

Stocks at 52 Week’s LOW

Symbol Prev. Close Change %Chg

JPOLYINVST 65.25 -0.25 -0.38

- -

DAILY REPORT

16th

SEPT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

STOCK RECOMMENDATION [CASH]

3. RUSHIL [CASH]

RUSHIL made new 52 week high of 189.90 but after that it faced huge profit booking for that whole day it correct and finished around 3% loss on EOD chart it create bearish in-verted hammer which is sign of trend reversal and at last session it got around 29 time more volume as compare to average so sell it below 158 for target of 156-153-150 use stop loss of 161

MACRO NEWS

August Trade Data: Trade Deficit At $12.48Bn Vs $12.81Bn (MoM), Exports At $21.27Bn Vs $23.14Bn (MoM), Aug. Exports Lowest In Nearly 5 Years, Lowest Since Oct 2010, Imports At $33.74Bn Vs $35.95Bn (MoM)

Govt expects Rs 36Kcr investment in green energy corri-dors

Govt to ban manufacturing, import export of toxic PCBs

Havells work on wireless lighting for smartcity projects

Government likely to extend validity of environment clearance to Asian Paints' project

Bidding starts for imported LNG subsidy; 16 power com-panies in fray

Sponsors set to pour in Rs 100 crore into ISL this year; existing firms like Hero, Maruti renew pacts

Dr Reddy's signs commercialization deal with Hatchtech

Utkal D and E coal blocks allocated to Nalco

L&T; Deutsche Bank downgrades to hold, cuts target

Gujarat Gas relists at Rs 680 post merger of cos with self

Bharat Forge; BoAML cuts target on weak demand

ONGC makes another discovery in KG-D5 block Indian PC market slips 13% to 2.2 mn units in Q2. Sebi seeks greater disclosure in debt public issues of

NBFCs HC reserves order on Novartis – Cipla Patent dispute

STOCK RECOMMENDATIONS [FUTURE] 1. TECHM [FUTURE]

From last two week TECHM FUTURE trading in fix range of 548-517, before last session it made low of 517 and at last session it finished at 540 with bullish candle around 2% gain but other IT measure still trading in pressure and Index is also facing resistance at 7880 so sell on rise around 545-550 will be good with stop loss of 555.25 for target of 540-533-525. 2. ITC [FUTURE]

ITC Future create bottom around 311 at last session it fin-ished with 1% gain with bullish candle. 318 is short term re-sistance for ITC since Market is not too strong so after break-out we can’t expect big up move so buy it in decline around 313 with strict stop loss of 309.90 for target of 316-318-322+.

DAILY REPORT

16th

SEPT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

FUTURE & OPTION

MOST ACTIVE PUT OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY CE 8,000 54.60 5,87,357 49,70,900

NIFTY CE 7,900 94.20 3,58,279 32,91,825

BANKNIFTY CE 17,000 270.00 55,774 6,10,525

RELIACNE CE 880 12.90 4,913 7,04,250

TATASTEEL CE 240 5.15 4,375 19,16,000

LT CE 1,600 23.45 4,103 2,84,125

SBIN CE 240 5.65 3,944 41,89,000

WOCKPHARMA CE 1,500 38.00 3,608 1,38,500

MOST CTIVE CALL OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY PE 7,800 128.40 3,60,949 44,65,425

NIFTY PE 7,700 94.45 3,31,640 30,81,175

BANKNIFTY PE 16,000 149.45 53,440 5,21,275

RELIANCE PE 860 15.50 3,109 4,25,500

TATASTEEL PE 230 9.90 2,738 6,75,000

AXISBANK PE 480 15.50 2,157 4,80,500

LT PE 1,550 39.50 2,148 1,21,750

RELIANCE PE 840 8.60 2,108 3,02,750

FII DERIVATIVES STATISTICS

BUY OPEN INTEREST AT THE END OF THE DAY SELL

No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores NET AMOUNT

INDEX FUTURES 76021 1747.37 65418 1490.71 1074812 23113.9 256.6577

INDEX OPTIONS 509712 11579.7 601867 13301.1 4058682 96310.2 -1721.36

STOCK FUTURES 90843 2313.88 78481 1965.18 1860594 46414 348.6997

STOCK OPTIONS 63415 1538.04 63887 1549.59 108505 2633.5 -11.5434

TOTAL -1127.54

STOCKS IN NEWS ABB India bags orders worth Rs 119 crore ONGC bucks trend to build assets as oil prices ease Vedanta-Cairn India merger gets BSE, NSE approval Vedanta's Sesa Goa opens its second mining lease at

Bicholim Arvind eyeing 70% of sales from global brands in 2-3

years IOC lines up investments worth 1.7 lk cr over 7 years Arvind Infra: Circuit Filter Revised to 5% from 10% Sun Pharma to acquire US eye care co InSite Vision NIFTY FUTURE

In last trading session, a slow movement was seen in the index, it was down and moved about 80 points. Further it closed with a bear indications on daily charts but since it has resistance at current levels it may come down a little in opening hours. So we recommend you to buy it from around 7800-7820 for the targets of 7880 and 8000 with strict stop loss of 7650

INDICES R2 R1 PIVOT S1 S2

NIFTY 7,917.00 7,873.00 7,836.00 7,792.00 7,755.00

BANK NIFTY 17,017.00 16,878.00 16,779.00 16,640.00 16,541.00

DAILY REPORT

16th

SEPT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

RECOMMENDATIONS

GOLD

TRADING STRATEGY:

BUY GOLD OCT ABOVE 26150 TGTS 26230,26330 SL BE-

LOW 26050

SELL GOLD OCT BELOW 25900 TGTS 25820,25720 SL

ABOVE 26000

SILVER

TRADING STRATEGY:

BUY SILVER DEC ABOVE 34900 TGTS 35100,35400 SL BE-

LOW 34600

SELL SILVER DEC BELOW 34600 TGTS 34400,34100 SL

ABOVE 34900

COMMODITY ROUNDUP India's gold imports surged 156% on year to Rs 32261 crores in August 2015. Silver imports also surged to Rs 2364 crores, up 58.40% on year. Oil Imports At $7.36 Bn Vs $9.49 Bn (MoM) Non-oil Imports At $26.39 Bn Vs $26.46 Bn (MoM) Oil prices extended gains in early trading in Asia on Wednes-day after US prices were boosted by a stockpile draw, while a warning by OPEC producer Iraq that it may slow spending on new fields pushed up international crude. US crude fu-tures rose after industry group the American Petroleum In-stitute reported a 3.1mn-barrel crude drawdown last week. A surge in American gasoline prices was also supportive. A small increase in home steel prices is likely in the coming months, with the government having imposed a 20 per cent ‘safeguard duty’ on certain categories of import to protect local producers. The duty was imposed on Monday with immediate effect on hot-rolled flat products of non-alloy and other alloy steel, in coils of a width of 600 mm or more. Hurt by spate of cheaper imports and plummeting LME prices, domestic aluminium makers need to focus on cost competitiveness in the long run to compete against their global counterparts, analysts. Aluminium producers like Nalco, Hindalco Industries and Vedanta have been pressing for hike in import duty to 10% (from five per cent now) to counter the threat from rising imports from China and West Asia. Also, falling metal prices have eroded their competi-tive edge, forcing them to keep half of their capacities idle. Copper futures were lower in amid persistent worries about China's cooling economy and risk-aversion in the run-up to the US FOMC meeting this week, factors that are putting pressure on demand. The industrial metal fell yet again on Tuesday after the Chinese National Bureau of Statistics over the weekend showed factory production and fixed-asset investment was below expectations in August. Already run up Copper is expected to show bearish moves as there was very little backing for the rally that was seen last week. Red metal gained sharply but as the Fed meet has again come in limelight the expectations of the rally to continue has died. The FOMC begins its two-day meeting on Wednesday, which could potentially see it raise interest rates for the first time in almost a decade. This would strengthen the dollar and negatively affect dollar-denominated commodities, such as copper. MCX Copper was trading at Rs 356.80 per kg, down 0.22%. The prices tested a high of Rs 359.95 per kg and a low of Rs 355.5 per kg.

DAILY REPORT

16th

SEPT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

NCDEX

NCDEX ROUNDUP

Continuing its losing streak for the second day, carda-mom prices fell by 2.72% to Rs 827 per kg in futures trade as speculators engaged in reducing positions amid adequate stocks against subdued demand in the spot market. At the MCX cardamom for delivery in November fell by Rs 23.20, or 2.72%, to Rs 827 per kg in a business turnover of 22 lots. In a similar fashion, the spice for delivery in October traded lower by Rs 5.70, or 0.68%, to Rs 825 per kg in 169 lots. A weak trend at spot market against adequate stocks in the physical market on higher supplies from the producing belts mainly kept pressure on cardamom prices at futures trade.

Vegetable oil import during August touched 1,374,049 ton-nes, up from 1,333,480 tonnes in the same month a year ago. The overall import of vegetable oils between Novem-ber 2014 and August 2015 rose 23 per cent from 9,525,374 tonnes in August 2014 to 11,725,065 tonnes in August this year. Excessive import has put tremendous pressure on lo-cal prices. As a result, Indian oilseeds-growing farmers are in distress and losing interest in the crop. India’s dependence on imported oil has further increased to nearly 70 per cent

Wheat futures settled flat with negative note on the ac-count of strong global supplies coupled weak export de-mand in local mandies Bearish USDA report has added negative sentiments in both domestic and international market. Global wheat production is projected at 731.60mn tonnes against 726.54mn tonnes reported last month for 2015-16. Global wheat supplies for 2015/16 are raised 6.7mn tons, primarily on increased production in the EU and FSU. Partly offsetting are reductions in Canada and India. Reductions in food use are partially offsetting. The NCDEX October futures settled down at Rs 1513 per quintal

NCDEX INDICES

Index Value % Change

CAETOR SEED 4052 -1.03

CHANA 4277 -0.81

CORIANDER 10700 -1.11

COTTON SEED 2155 +0.14

GUAR SEED 3783 -4.88

JEERA 15315 -1.10

MUSTARDSEED 4266 -0.19

REF. SOY OIL 575.85 +1.76

TURMERIC 7598 -2.59

WHEAT 1515 +0.13

RECOMMENDATIONS

DHANIYA

BUY CORIANDER OCT ABOVE 11027 TARGET 11052 11132

SL BELOW 11000

SELL CORIANDER OCT BELOW 10812 TARGET 10787 10707

SL ABOVE 10839

GUARSGUM

BUY GUARGUM OCT ABOVE 8400 TARGET 8450 8520 SL

BELOW 8340

SELL GUARGUM OCT BELOW 8250 TARGET 8200 8130 SL

ABOVE 8310

DAILY REPORT

16th

SEPT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

RBI Reference Rate

Currency Rate Currency Rate

Rupee- $ 66.4383 Yen-100 55.5500

Euro 75.0487 GBP 102.4080

CURRENCY

USD/INR

BUY USD/INR SEP ABOVE 66.57 TARGET 66.7 66.85 SL BE-

LOW 66.37

SELL USD/INR SEP BELOW 66.47 TARGET 66.34 66.19 SL

ABOVE 66.67

EUR/INR

BUY EUR/INR SEP ABOVE 75.4 TARGET 75.55 75.75 SL BE-

LOW 75.2

SELL EUR/INR SEP BELOW 75.1 TARGET 74.95 74.75 SL

ABOVE 75.3

CURRENCY MARKET UPDATES: The rupee ended marginally lower by three paise at 66.36 against the US dollar today on fresh demand for the Ameri-can currency from banks and importers amidst fall in eq-uity markets despite greenback’s weakness in overseas markets. The domestic unit resumed lower at 66.35 as against yesterday’s closing of 66.33 at the Interbank Forex market and fell further to 66.48 before concluding at 66.36, showing a loss of three paise, or 0.05%. The rupee hovered in a range of 66.33 and 66.48 during the day. It had yesterday closed higher by 21 paise, or 0.32 per cent. The US dollar fell further against a basket of currencies on Tuesday, anxiously awaiting the upcoming Federal Re-serve's policy statement on Thursday. The dollar index, which measures the greenback's strength against a trade-weighted basket of six major currencies, was steady at 95.31. Meanwhile, sentiment on the dollar remained vul-nerable amid concerns that mixed U.S. economic reports and recent volatility in global financial markets will prompt the U.S. central bank to refrain from hiking interest rates on Thursday. Fed Chair said that an interest rate increase is data dependent but has also indicated that she expects to begin raising rates before the end of the year. The dollar was higher against the euro, with EUR/USD slip-ping 0.11% to 1.1305. The ZEW economic sentiment index for Germany fell to 12.1 in September from 25.0 the previ-ous month. As against the pound, dollar was steady with GBP/USD at 1.5423. The pound strengthened slightly after the U.K. Office for National Statistics reported that the consumer price index rose 0.2% last month, in line with expectations, after a 0.2% fall in July. Year-on-year, U.K. consumer prices were flat in August, in line with expecta-tions and following a 0.1% downtick the previous month. Core CPI, which excludes food, energy, alcohol and to-bacco, rose at an annualized rate of 1.0% in August, as ex-pected, after a 1.2% rise the previous month.

The dollar was lower against the yen, with USD/JPY down 0.51% at 119.63. The Bank of Japan said it had not changed its policy calling for ¥80 trillion in annual asset purchases by the central bank, to help spur inflation and stimulate growth.

DAILY REPORT

16th

SEPT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

CALL REPORT

S T O

PERFORMANCE UPDATES

Date Commodity/ Currency

Pairs Contract Strategy Entry Level Target Stop Loss Remark

15/09/15 NCDEX DHANIYA OCT. BUY 11175 11200-11280 11148 NOT EXECUTED

15/09/15 NCDEX DHANIYA OCT. SELL 11900 11875-11795 11927 SL TRIGGERED

15/09/15 NCDEX GUARGUM OCT. BUY 9010 9060-9130 8950 NOT EXECUTED

15/09/15 NCDEX GUARGUM OCT. SELL 8670 8620-8550 8730 BOOKED FULL PROFIT

15/09/15 MCX GOLD OCT. BUY 26150 26230-26330 26050 NOT EXECUTED

15/09/15 MCX GOLD OCT. SELL 25900 25820-25720 26000 NOT EXECUTED

15/09/15 MCX SILVER DEC. BUY 34900 35100-35400 34600 NOT EXECUTED

15/09/15 MCX SILVER DEC. SELL 34600 34400-34100 34900 NO PROFIT NO LOSS

15/09/15 USD/INR SEPT. BUY 66.56 66.69-66.84 66.36 NOT EXECUTED

15/09/15 USD/INR SEPT. SELL 66.43 66.30-66.15 66.63 NOT EXECUTED

15/09/15 EUR/INR SEPT. BUY 75.42 75.57-75.77 75.22 NOT EXECUTED

15/09/15 EUR/INR SEPT. SELL 75.09 74.94-74.74 75.29 NOT EXECUTED

Date Scrip

CASH/

FUTURE/

OPTION

Strategy Entry Level Target Stop Loss Remark

15/09/15 NIFTY FUTURE BUY 7800-7820 7880-8000 7650 CALL OPEN

15/09/15 KSCL FUTURE BUY 466 472-478 460 BOOKED FULL PROFIT

15/09/15 VEDL FUTURE BUY 103 104.5-106 101 NOT EXECUTED

15/09/15 DCBBANK CASH BUY 131 132.5-134.5 129 SL TRIGGERED

DAILY REPORT

16th

SEPT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

NEXT WEEK'S U.S. ECONOMIC REPORTS

ECONOMIC CALENDAR

The information and views in this report, our website & all the service we provide are believed to be reliable, but we do not accept any

responsibility (or liability) for errors of fact or opinion. Users have the right to choose the product/s that suits them the most. Sincere ef-

forts have been made to present the right investment perspective. The information contained herein is based on analysis and up on sources

that we consider reliable. This material is for personal information and based upon it & takes no responsibility. The information given

herein should be treated as only factor, while making investment decision. The report does not provide individually tailor-made invest-

ment advice. Epic research recommends that investors independently evaluate particular investments and strategies, and encourages in-

vestors to seek the advice of a financial adviser. Epic research shall not be responsible for any transaction conducted based on the infor-

mation given in this report, which is in violation of rules and regulations of NSE and BSE. The share price projections shown are not nec-

essarily indicative of future price performance. The information herein, together with all estimates and forecasts, can change without no-

tice. Analyst or any person related to epic research might be holding positions in the stocks recommended. It is understood that anyone

who is browsing through the site has done so at his free will and does not read any views expressed as a recommendation for which either

the site or its owners or anyone can be held responsible for . Any surfing and reading of the information is the acceptance of this dis-

claimer. All Rights Reserved. Investment in equity & bullion market has its own risks. We, however, do not vouch for the accuracy or the

completeness thereof. We are not responsible for any loss incurred whatsoever for any financial profits or loss which may arise from the

recommendations above epic research does not purport to be an invitation or an offer to buy or sell any financial instrument. Our Clients

(Paid or Unpaid), any third party or anyone else have no rights to forward or share our calls or SMS or Report or Any Information Pro-

vided by us to/with anyone which is received directly or indirectly by them. If found so then Serious Legal Actions can be taken.

Disclaimer

TIME REPORT PERIOD ACTUAL CONSENSUS

FORECAST PREVIOUS

MONDAY, SEP. 14

NONE SCHEDULED

TUESDAY, SEP. 15

8:30 AM RETAIL SALES AUG. 0.6%

8:30 AM RETAIL SALES EX-AUTOS AUG 0.4%

8:30 AM EMPIRE STATE INDEX SEPT. -14.9

9:15 AM INDUSTRIAL PRODUCTION AUG. 0.6^

9:15 AM CAPACITY UTILIZATION AUG. 78.0%

10 AM BUSINESS INVENTORIES JULY 0.8%

WEDNESDAY, SEP. 16

8:30 AM CONSUMER PRICE INDEX AUG. 0.1%

8:30 AM CORE CPI AUG. 0.1%

10 AM HOME BUILDERS' INDEX SEPT. 61

THURSDAY, SEP. 17

8:30 AM WEEKLY JOBLESS CLAIMS SEPT. 12 N/A N/A

8:30 AM HOUSING STARTS AUG. 1.21 MLN

8:30 AM BUILDING PERMITS AUG 1.13 MLN

8:30 AM CURRENT ACCOUNT 2Q -$113 BLN

10 AM PHILLY FED SEPT. 8.3

2 PM FOMC STATEMENT

2:30 PM JANET YELLEN PRESS CONFERENCE

FRIDAY, SEP. 18

10 AM LEADING INDICATORS AUG. -0.2%