Epic research special report of 28 sep 2015

8

DAILY REPORT 28 th SEPT. 2015 YOUR MINTVISORY Call us at +91-731-6642300 Global markets at a glance European shares ended higher on Friday after testing 2015 lows in the previous session, as concern over the global economy eased and a sell-off of car stocks began to slow. The FTSEurofirst 300 index gained 2.78% at 1,374.5 points. The blue-chip Euro STOXX 50 index climbed 3.11%. The FTSEurofirst was still down almost 1.7% this week. Euro- pean shares have been hit this week by concern over the broader risks of the emissions rigging, but the mood turned after Janet Yellen said overnight the Fed was on track to lift rates this year and U.S. GDP growth was revised upwards. The S&P 500 erased an early Fed-driven rally to close down slightly on Friday, as a selloff in biotechs offset gains in banking shares. The Nasdaq fell 1 percent, while the Nasdaq Biotech IndexI tumbled 5.1 percent and retested its low from August, when it entered bear market territory. The Dow ended solidly in positive territory, helped by shares of Nike, which hit a record high after its profit topped expectations on strong China growth. The stock, up 8.9 percent at $125, gave the biggest boost to the Dow and the S&P 500. The market started the day higher after Federal Reserve Chair Janet Yellen late Thursday said she and other Fed policymakers do not expect recent economic and financial market turmoil to significantly alter the U.S. central bank's policy, easing concerns about the world's economic health. She said she expects interest rates to be raised this year. Previous day Roundup After a consolidation in narrow range, the 50-share NSE Nifty closed marginally higher on Thursday, the expiry day for September F&O contract. The broader markets slightly outperformed benchmarks with the BSE Midcap and Small- cap indices rising 0.2% and 0.6%, respectively. Nifty rose 22.55pts to 7868.50 and Sensex gained 40.51pts at 25863.50. The market breadth was positive as about 1444 shares advanced against 1238 shares declined on BSE. Index stats The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [up 204.22pts], Capital Goods [down 171.36pts], PSU [down 64.68pts], FMCG [up 73.43pts], Realty [up 7.77pts], Power [up 0.21pts], Auto [up 16.85Pts], Healthcare [up 129.81Pts], IT [up 227.01pts], Metals [down 95.87pts], TECK [up 97.47pts], Oil& Gas [down 66.32pts]. World Indices Index Value % Change D J l 16314.68 +0.70 S&P 500 1931.34 -0.05 NASDAQ 4686.50 -1.01 FTSE 100 16109.01 +2.47 Nikkei 225 17677.12 -1.14 Hong Kong 21186.32 +0.43 Top Gainers Company CMP Change % Chg LUPIN 1,991.70 69.65 3.62 TATAPOWER 65.40 2.15 3.40 HCLTECH 956.00 28.90 3.12 INDUSINDBK 928.15 22.60 2.50 GAIL 294.00 6.70 2.33 Top Losers Company CMP Change % Chg ONGC 227.10 9.45 -3.99 NMDC 95.00 3.25 -3.31 COALINDIA 319.15 8.665 -2.64 TATAMOTORS 302.45 7.85 -2.53 TATASTEEL 215.40 5.60 -2.53 Stocks at 52 Week’s HIGH Symbol Prev. Close Change %Chg CEATLTD 1,273.90 24.45 1.96 DISHMAN 301.50 -5.55 -1.81 GMBREW 440.90 3.60 0.82 JUBILANT 380.00 14.45 3.95 MINDTREE 1,558.00 51.75 3.44 Indian Indices Company CMP Change % Chg NIFTY 7668.50 +22.55 +0.29 SENSEX 25863.50 +40.1 +0.16 Stocks at 52 Week’s LOW Symbol Prev. Close Change %Chg BHARTIARTL 332.25 -5.65 -1.67 BHEL 199.30 0.20 0.10 COALINDIA 319.15 -8.65 -2.64 HINDALCO 71.45 -1.50 -2.06 TATAMOTORS 302.45 -7.85 -2.53

-

Upload

epic-research -

Category

Business

-

view

395 -

download

2

Transcript of Epic research special report of 28 sep 2015

DAILY REPORT

28th

SEPT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

Global markets at a glance

European shares ended higher on Friday after testing 2015

lows in the previous session, as concern over the global

economy eased and a sell-off of car stocks began to slow.

The FTSEurofirst 300 index gained 2.78% at 1,374.5 points.

The blue-chip Euro STOXX 50 index climbed 3.11%. The

FTSEurofirst was still down almost 1.7% this week. Euro-

pean shares have been hit this week by concern over the

broader risks of the emissions rigging, but the mood turned

after Janet Yellen said overnight the Fed was on track to lift

rates this year and U.S. GDP growth was revised upwards.

The S&P 500 erased an early Fed-driven rally to close down

slightly on Friday, as a selloff in biotechs offset gains in

banking shares. The Nasdaq fell 1 percent, while the

Nasdaq Biotech IndexI tumbled 5.1 percent and retested its

low from August, when it entered bear market territory.

The Dow ended solidly in positive territory, helped by

shares of Nike, which hit a record high after its profit

topped expectations on strong China growth. The stock, up

8.9 percent at $125, gave the biggest boost to the Dow and

the S&P 500.

The market started the day higher after Federal Reserve

Chair Janet Yellen late Thursday said she and other Fed

policymakers do not expect recent economic and financial

market turmoil to significantly alter the U.S. central bank's

policy, easing concerns about the world's economic health.

She said she expects interest rates to be raised this year.

Previous day Roundup

After a consolidation in narrow range, the 50-share NSE

Nifty closed marginally higher on Thursday, the expiry day

for September F&O contract. The broader markets slightly

outperformed benchmarks with the BSE Midcap and Small-

cap indices rising 0.2% and 0.6%, respectively. Nifty rose

22.55pts to 7868.50 and Sensex gained 40.51pts at

25863.50. The market breadth was positive as about 1444

shares advanced against 1238 shares declined on BSE.

Index stats

The Market was very volatile in last session. The sartorial

indices performed as follow; Consumer Durables [up

204.22pts], Capital Goods [down 171.36pts], PSU [down

64.68pts], FMCG [up 73.43pts], Realty [up 7.77pts], Power

[up 0.21pts], Auto [up 16.85Pts], Healthcare [up

129.81Pts], IT [up 227.01pts], Metals [down 95.87pts],

TECK [up 97.47pts], Oil& Gas [down 66.32pts].

World Indices

Index Value % Change

D J l 16314.68 +0.70

S&P 500 1931.34 -0.05

NASDAQ 4686.50 -1.01

FTSE 100 16109.01 +2.47

Nikkei 225 17677.12 -1.14

Hong Kong 21186.32 +0.43

Top Gainers

Company CMP Change % Chg

LUPIN 1,991.70 69.65 3.62

TATAPOWER 65.40 2.15 3.40

HCLTECH 956.00 28.90 3.12

INDUSINDBK 928.15 22.60 2.50

GAIL 294.00 6.70 2.33

Top Losers

Company CMP Change % Chg

ONGC 227.10 9.45 -3.99

NMDC 95.00 3.25 -3.31

COALINDIA 319.15 8.665 -2.64

TATAMOTORS 302.45 7.85 -2.53

TATASTEEL 215.40 5.60 -2.53

Stocks at 52 Week’s HIGH

Symbol Prev. Close Change %Chg

CEATLTD 1,273.90 24.45 1.96

DISHMAN 301.50 -5.55 -1.81

GMBREW 440.90 3.60 0.82

JUBILANT 380.00 14.45 3.95

MINDTREE 1,558.00 51.75 3.44

Indian Indices

Company CMP Change % Chg

NIFTY 7668.50 +22.55 +0.29

SENSEX 25863.50 +40.1 +0.16

Stocks at 52 Week’s LOW

Symbol Prev. Close Change %Chg

BHARTIARTL 332.25 -5.65 -1.67

BHEL 199.30 0.20 0.10

COALINDIA 319.15 -8.65 -2.64

HINDALCO 71.45 -1.50 -2.06

TATAMOTORS 302.45 -7.85 -2.53

DAILY REPORT

28th

SEPT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

STOCK RECOMMENDATION [CASH]

3. BHARAT FORGE [CASH]

BHARATFORGE create bottom around 893 in last session it slipped from 925 while from last two seek it is making higher lows & finished at 903 so if it break 893 this level then it can give vertical fall so sell it below 892 for target of 882-872 use stop loss of 904

MACRO NEWS

SBI seen cutting repo rate by 25 bps on September 29.

JSW Energy may acquire 74% stake in Monnet Power

Largecap pharma, barring Dr Reddy's, overvalued

Lupin; Credit Suisse upgrades, bets on diabetes drugs

Forex reserves up $631.5 mn to $352.02 bn

USFDA denies approval to SPARC's epilepsy drug

UNSC reforms essential to make it relevant: PM

Food sector bodies demand refund of Rs 80 crore from FSSAI

Jaypee Infratech defaults in loan repayment, down-graded to default category by Care

Govt mulls higher price for ethanol

MMTC to produce, market sovereign gold coins

ITC aims Rs 18000-cr revenue from agri business by FY'21

Maruti Suzuki reaches wage settlement agreement with workers at Gurgaon & Manesar plants

Aurobindo Pharma gets US FDA nod for Caffeine Citrate.

Adani Enterprises enters into strategic pact with Chinese energy company GCL Group

India Cements sets record date as October 9 for share distribution of CSK to shareholders

Gammon India bags order worth Rs 1,710 cr from NHAI

STOCK RECOMMENDATIONS [FUTURE]

1. ONGC [FUTURE]

Despite given breakout above 235 ONGC Future faced resis-tance around 242 & at last session it finished with 3.89% loss at 228 while downside it may get support around 226 so sell around 231-233 use stop loss of 238 for target of 228-226-222.

2. GAIL [FUTURE]

GAIL Future moving in fix price range from last two weeks in last trading session it bounce from 282 level and made high of 294.55 while it 297 is upper range for it, if we see to RSI then it has positive divergence so but it in decline around 285-288 use stop loss of 281 for target of 292-296 while if it cross 296 then it may hit 300.

DAILY REPORT

28th

SEPT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

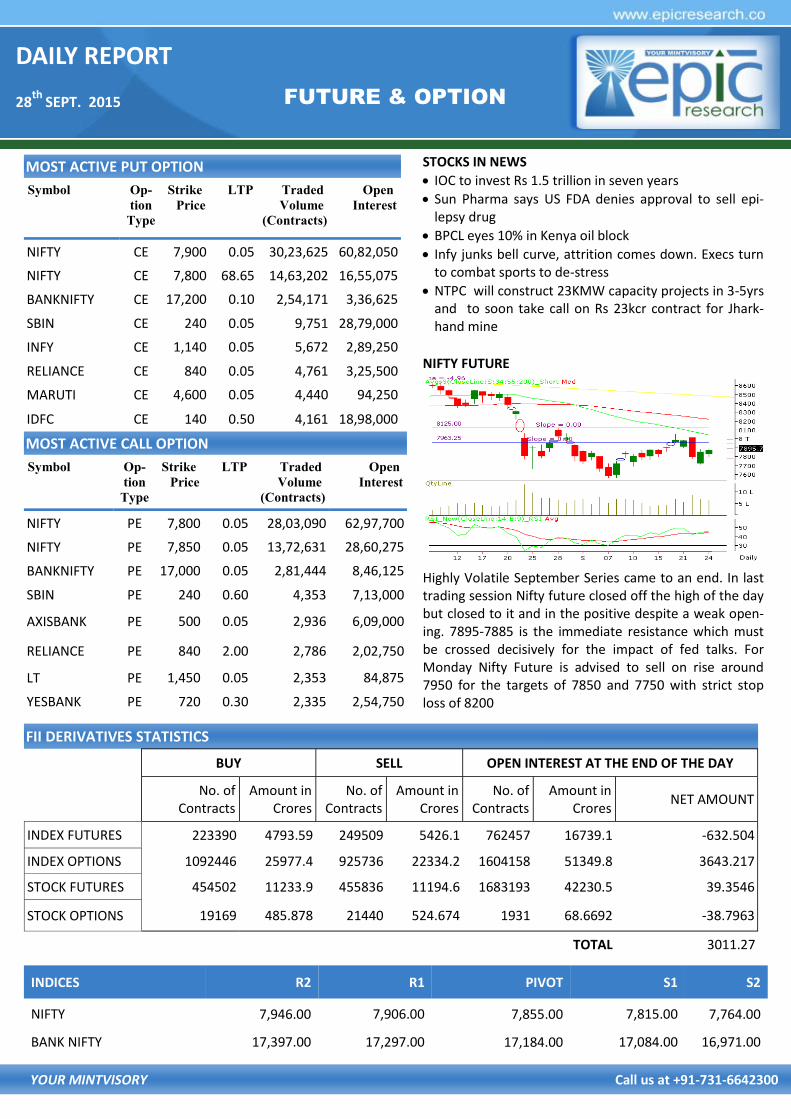

FUTURE & OPTION

MOST ACTIVE PUT OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY CE 7,900 0.05 30,23,625 60,82,050

NIFTY CE 7,800 68.65 14,63,202 16,55,075

BANKNIFTY CE 17,200 0.10 2,54,171 3,36,625

SBIN CE 240 0.05 9,751 28,79,000

INFY CE 1,140 0.05 5,672 2,89,250

RELIANCE CE 840 0.05 4,761 3,25,500

MARUTI CE 4,600 0.05 4,440 94,250

IDFC CE 140 0.50 4,161 18,98,000

MOST ACTIVE CALL OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY PE 7,800 0.05 28,03,090 62,97,700

NIFTY PE 7,850 0.05 13,72,631 28,60,275

BANKNIFTY PE 17,000 0.05 2,81,444 8,46,125

SBIN PE 240 0.60 4,353 7,13,000

AXISBANK PE 500 0.05 2,936 6,09,000

RELIANCE PE 840 2.00 2,786 2,02,750

LT PE 1,450 0.05 2,353 84,875

YESBANK PE 720 0.30 2,335 2,54,750

FII DERIVATIVES STATISTICS

BUY OPEN INTEREST AT THE END OF THE DAY SELL

No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores NET AMOUNT

INDEX FUTURES 223390 4793.59 249509 5426.1 762457 16739.1 -632.504

INDEX OPTIONS 1092446 25977.4 925736 22334.2 1604158 51349.8 3643.217

STOCK FUTURES 454502 11233.9 455836 11194.6 1683193 42230.5 39.3546

STOCK OPTIONS 19169 485.878 21440 524.674 1931 68.6692 -38.7963

TOTAL 3011.27

STOCKS IN NEWS

IOC to invest Rs 1.5 trillion in seven years

Sun Pharma says US FDA denies approval to sell epi-lepsy drug

BPCL eyes 10% in Kenya oil block

Infy junks bell curve, attrition comes down. Execs turn to combat sports to de-stress

NTPC will construct 23KMW capacity projects in 3-5yrs and to soon take call on Rs 23kcr contract for Jhark-hand mine

NIFTY FUTURE

Highly Volatile September Series came to an end. In last trading session Nifty future closed off the high of the day but closed to it and in the positive despite a weak open-ing. 7895-7885 is the immediate resistance which must be crossed decisively for the impact of fed talks. For Monday Nifty Future is advised to sell on rise around 7950 for the targets of 7850 and 7750 with strict stop loss of 8200

INDICES R2 R1 PIVOT S1 S2

NIFTY 7,946.00 7,906.00 7,855.00 7,815.00 7,764.00

BANK NIFTY 17,397.00 17,297.00 17,184.00 17,084.00 16,971.00

DAILY REPORT

28th

SEPT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

RECOMMENDATIONS

GOLD

TRADING STRATEGY:

BUY GOLD OCT ABOVE 26900 TGTS 26980,27070 SL BE-LOW 26800

SELL GOLD OCT BELOW 26700 TGTS 26620,26530 SL ABOVE 26800

SILVER

TRADING STRATEGY:

BUY SILVER DEC ABOVE 36300 TGTS 36500,36800 SL BE-LOW 36000

SELL SILVER DEC BELOW 36000 TGTS 35800,35500 SL ABOVE 36300

COMMODITY ROUNDUP Continuing its rising streak for the third straight day, gold today reclaimed Rs 27,000-mark by zooming Rs 400 to hit 1-month high of Rs 27,250 per 10 grams at the bullion market, tracking a firming trend overseas amid pick-up in jewellers' buying to meet rising wedding demand. Silver also retook the Rs 36,000-level by surging Rs 1,100 to Rs 36,500 per kg on increased offtake by industrial units and coin makers. Bullion traders said besides a firming global trend where gold soared to one-month high, continued buying by jewel-lers and retailers to meet wedding season demand largely influenced the precious metal prices. Globally, gold climbed 2.11% to USD 1,154.10 an ounce, its highest level since August 24, and silver 2.43 percent to USD 15.15 an ounce in New York in yesterday's trade. Fresh weakness in the rupee against the dollar, making imports costlier, too supported the upside, they added. In the na-tional capital, gold of 99.9 percent and 99.5 percent purity climbed Rs 400 each to Rs 27,250 and Rs 27,100 per 10 grams, respectively, a level last seen on August 25. The pre-cious metals had gained Rs 340 in the past two days. Sover-eign moved up by Rs 100 at Rs 22,500 per piece of eight grams. Tracking gold, silver ready recorded a hefty rise of Rs 1,100 to Rs 36,500 per kg and weekly-based delivery by Rs 725 to Rs 36,220 per kg. Silver coins spurted Rs 1,000 to Rs 53,000 for buying and Rs 54,000 for selling of 100 pieces. World mine production in January to July 2015 was 11.05 million tonnes which was 3.6 per cent higher than in the same period in 2014. Global refined production rose to 13.2 million tonnes up 2.6 per cent compared with the previous year with a significant increase recorded in China (up 192 kt) and India (up 51 kt). Global consumption for January to July 2015 was 13103 kt compared with 13069 kt for the same months of 2014. Chinese apparent consumption in January to July 2015 rose by 43 kt to 5337 kt which repre-sented 47.9% of global demand. EU28 production fell by 0.5% and demand was, at 1948 kt, 0.9 per cent below the January to July 2014 total. In July 2015, refined copper pro-duction was 1929.9 kt and consumption was 1869.2 kt. Oil prices pared gains on Friday after the dollar rose on ex-pectations the United States could still raise interest rates this year and after analysts from Standard & Poor's ratings cut their oil price assumptions. Weak consumer data from Japan also weighed on price. Globally traded Brent futures were at $48.33 per barrel at 0940 GMT, up just 16 cents from their last close and erasing earlier Friday gains. WTI futures were at $45.27 a barrel, up 36 cents.

DAILY REPORT

28th

SEPT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

NCDEX

NCDEX ROUNDUP

The total area sown under kharif crops as on 24th Sep-

tember, 2015 has reached to1026.23 lakh hectares as

compared to 1014.24 lakh hectare last year at this

time, witnessing a modest rise of 1.18%. The acreage

under pulses has shot up 11% while area under oil-

seeds has rose 3.50%.

The water storage available in 91 major reservoirs of

the country as on Sep 23,2015 was 95.313 BCM, which

is 60% of total storage capacity of these reservoirs.

This storage is 75% of the storage of corresponding

period of last year and 77% of storage of average of

last ten years. The total storage capacity of these 91

reservoirs is 157.799BCM which is about 62% of the

total storage capacity of 253.388 BCM which is esti-

mated to have been created in the country.

Spices fail to recover as lack of strong export demand

kept trend down for the counters. Low exports kept

sentiments weak for Guar also. Lack of strong demand

on the export front prevented any strong recovery for

Jeera even as there are expectations of exports rising

in coming weeks. With reports indicating a fall in ex-

ports, this weakened the sentiments further. Oil com-

plex traded with high volatility as Festive season de-

mand started rising in the mandis.

NCDEX INDICES

Index Value % Change

CAETOR SEED 4183 -0.19

CHANA 4632 +2.75

CORIANDER 11198 +0.63

COTTON SEED 1543 +0.46

GUAR SEED 3699 +0.11

JEERA 16050 +0.72

MUSTARDSEED 4300 +1.75

REF. SOY OIL 585.7 +1.76

TURMERIC 7420 +0.60

WHEAT 1548 -0.19

RECOMMENDATIONS

DHANIYA

BUY CORIANDER OCT ABOVE 11300 TARGET 11327 11407

SL BELOW 11273

SELL CORIANDER OCT BELOW 11150 TARGET 11123 11043

SL ABOVE 11177

GUARSGUM

BUY GUARGUM OCT ABOVE 8070 TARGET 8120 8190 SL

BELOW 8010

SELL GUARGUM OCT BELOW 7900 TARGET 7850 7780 SL

ABOVE 7960

DAILY REPORT

28th

SEPT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

RBI Reference Rate

Currency Rate Currency Rate

Rupee- $ 66.0993 Yen-100 55.0800

Euro 73.9585 GBP 100.8874

CURRENCY

USD/INR

BUY USD/INR SEP ABOVE 66.3 TARGET 66.43 66.58 SL BE-

LOW 66.1

SELL USD/INR SEP BELOW 66.1 TARGET 65.97 65.82 SL

ABOVE 66.3

EUR/INR

SELL EUR/INR SEP BELOW 74.14 TARGET 73.99 73.79 SL

ABOVE 74.34

BUY EUR/INR SEP ABOVE 74.5 TARGET 74.65 74.85 SL BE-

LOW 74.3

CURRENCY MARKET UPDATES:

Hit by month-end dollar demand from importers, the ru-

pee today dropped by another 18 paise against the Ameri-

can currency to close at 66.16, extending losses for the

fourth straight day, amid mixed global cues. Sustained for-

eign capital outflows also affected the market. FPIs sold

shares worth a net Rs 1,330.12cr yesterday, as per provi-

sional data released by the stock exchanges.

The Indian rupee resumed sharply lower at 66.20 per dollar

as against overnight level of 65.98 at the Interbank Forex

market. It hovered in a range of 66.2725 to 66.0350 per

dollar during the day, before ending at 66.16 per dollar,

showing a loss of 18 paise or 0.27 per cent. The rupee has

dropped by 49 paise or 0.75 per cent in four days.

The dollar index was down by 0.40 pct as against a basket

of six currencies. In global market, the yen rose today in

Asia because market participants sought safety amid global

economic uncertainty and ahead of a speech by U.S. Fed-

eral Reserve Chairwoman Janet Yellen.

The US dollar remained broadly lower against a basket of

currencies on Thursday, ahead of a crucial speech by Fed

Chair due later in the day. Moreover, mixed US economic

data kept the greenback under some pressure.

The euro climbed 0.58% to 1.1253 versus the dollar. The

single common currency remained supported after Euro-

pean Central Bank President said that it was too early de-

cide whether or not to add stimulus measures. On the eco-

nomic front, the German research institute Ifo earlier re-

ported that its business climate index ticked up to 108.5

this month from August's 108.4. It was the highest reading

in four months and was ahead of forecasts of 108.0.

As against the pound, the dollar was higher with GBP/USD

down 0.17% at 1.5221. The dollar pushed lower against the

yen, with USD/JPY down 0.70% at 119.41.

DAILY REPORT

28th

SEPT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

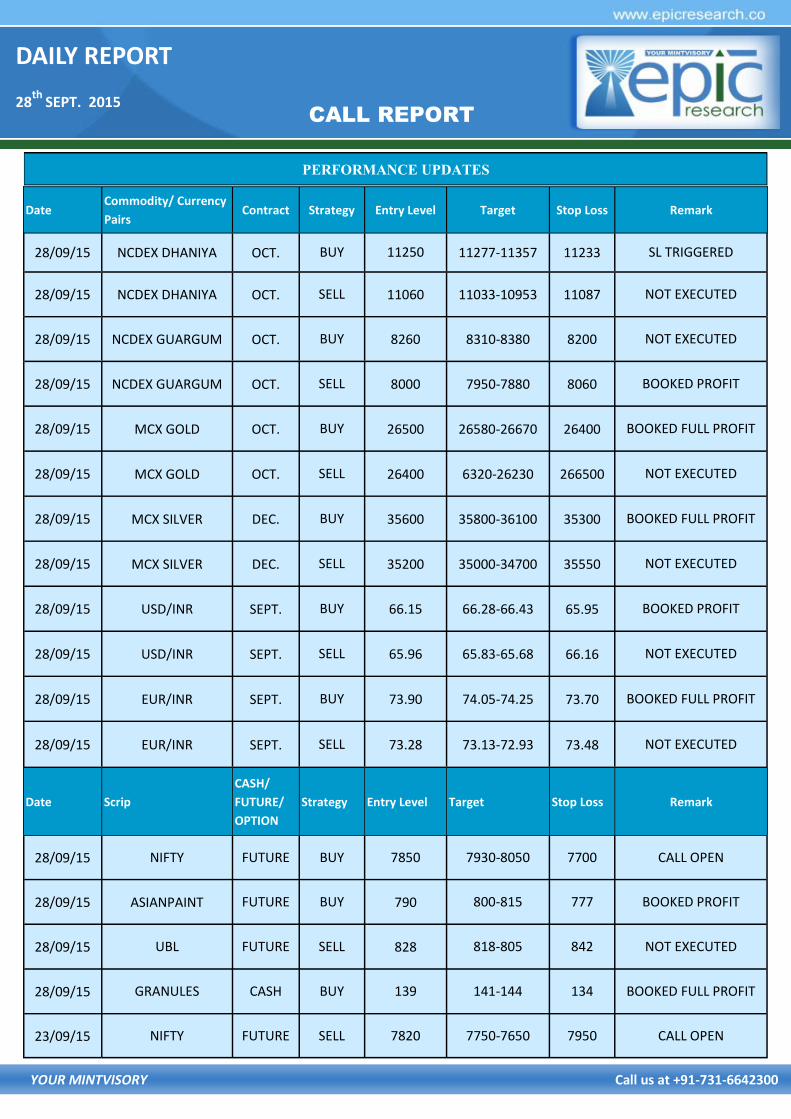

CALL REPORT

PERFORMANCE UPDATES

Date Commodity/ Currency

Pairs Contract Strategy Entry Level Target Stop Loss Remark

28/09/15 NCDEX DHANIYA OCT. BUY 11250 11277-11357 11233 SL TRIGGERED

28/09/15 NCDEX DHANIYA OCT. SELL 11060 11033-10953 11087 NOT EXECUTED

28/09/15 NCDEX GUARGUM OCT. BUY 8260 8310-8380 8200 NOT EXECUTED

28/09/15 NCDEX GUARGUM OCT. SELL 8000 7950-7880 8060 BOOKED PROFIT

28/09/15 MCX GOLD OCT. BUY 26500 26580-26670 26400 BOOKED FULL PROFIT

28/09/15 MCX GOLD OCT. SELL 26400 6320-26230 266500 NOT EXECUTED

28/09/15 MCX SILVER DEC. BUY 35600 35800-36100 35300 BOOKED FULL PROFIT

28/09/15 MCX SILVER DEC. SELL 35200 35000-34700 35550 NOT EXECUTED

28/09/15 USD/INR SEPT. BUY 66.15 66.28-66.43 65.95 BOOKED PROFIT

28/09/15 USD/INR SEPT. SELL 65.96 65.83-65.68 66.16 NOT EXECUTED

28/09/15 EUR/INR SEPT. BUY 73.90 74.05-74.25 73.70 BOOKED FULL PROFIT

28/09/15 EUR/INR SEPT. SELL 73.28 73.13-72.93 73.48 NOT EXECUTED

Date Scrip

CASH/

FUTURE/

OPTION

Strategy Entry Level Target Stop Loss Remark

28/09/15 NIFTY FUTURE BUY 7850 7930-8050 7700 CALL OPEN

28/09/15 ASIANPAINT FUTURE BUY 790 800-815 777 BOOKED PROFIT

28/09/15 UBL FUTURE SELL 828 818-805 842 NOT EXECUTED

28/09/15 GRANULES CASH BUY 139 141-144 134 BOOKED FULL PROFIT

23/09/15 NIFTY FUTURE SELL 7820 7750-7650 7950 CALL OPEN

DAILY REPORT

28th

SEPT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

NEXT WEEK'S U.S. ECONOMIC REPORTS

ECONOMIC CALENDAR

The information and views in this report, our website & all the service we provide are believed to be reliable, but we do not accept any responsibility (or

liability) for errors of fact or opinion. Users have the right to choose the product/s that suits them the most. Sincere efforts have been made to present the

right investment perspective. The information contained herein is based on analysis and up on sources that we consider reliable. This material is for per-

sonal information and based upon it & takes no responsibility. The information given herein should be treated as only factor, while making investment

decision. The report does not provide individually tailor-made investment advice. Epic research recommends that investors independently evaluate par-

ticular investments and strategies, and encourages investors to seek the advice of a financial adviser. Epic research shall not be responsible for any trans-

action conducted based on the information given in this report, which is in violation of rules and regulations of NSE and BSE. The share price projec-

tions shown are not necessarily indicative of future price performance. The information herein, together with all estimates and forecasts, can change

without notice. Analyst or any person related to epic research might be holding positions in the stocks recommended. It is understood that anyone who is

browsing through the site has done so at his free will and does not read any views expressed as a recommendation for which either the site or its owners

or anyone can be held responsible for . Any surfing and reading of the information is the acceptance of this disclaimer. All Rights Reserved. Investment

in equity & bullion market has its own risks. We, however, do not vouch for the accuracy or the completeness thereof. We are not responsible for any

loss incurred whatsoever for any financial profits or loss which may arise from the recommendations above epic research does not purport to be an invi-

tation or an offer to buy or sell any financial instrument. Our Clients (Paid or Unpaid), any third party or anyone else have no rights to forward or share

our calls or SMS or Report or Any Information Provided by us to/with anyone which is received directly or indirectly by them. If found so then Serious

Legal Actions can be taken.

Disclaimer

TIME REPORT PERIOD ACTUAL CONSENSUS

FORECAST PREVIOUS

MONDAY, SEP. 28

8:30 AM PERSONAL INCOME AUG. 0.4% 0.4%

8:30 AM CONSUMER SPENDING AUG. 0.3% 0.3%

8:30 AM CORE INFLATION AUG. 0.1% 0.1%

10 AM PENDING HOME SALES AUG. -- 0.5%

TUESDAY, SEP. 29

8:30 AM TRADE IN GOODS DEFICIT AUG. N/A -$59.1 BLN

9 AM CASE-SHILLER HOME PRICE INDEX JULY -- -0.1%

10 AM CONSUMER CONFIDENCE INDEX SEPT. 94.5 101.5

WEDNESDAY, SEP. 30

8:15 AM ADP EMPLOYMENT SEPT. -- 190,000

9:45 AM CHICAGO PMI SEPT. -- 54.5

THURSDAY, OCT. 01

8:30 AM WEEKLY JOBLESS CLAIMS SEPT. 26 N/A N/A

9:45 AM MARKIT PMI SEPT. -- 53.0

10 AM ISM SEPT. 51.1% 51.1%

10 AM CONSTRUCTION SPENDING AUG. 0.8% 0.7%

TBA MOTOR VEHICLE SALES SEPT. 17.4 MLN 17.7 MLN

FRIDAY, OCT. 02

8:30 AM NONFARM PAYROLLS SEPT. 190,000 173,000

8:30 AM UNEMPLOYMENT RATE SEPT. 5.1% 5.1%

8:30 AM AVERAGE HOURLY EARNINGS SEPT. 0.1% 0.3%

10 AM FACTORY ORDERS AUG. N/A 0.4%