Economic Update : Tracking The World Economy,The Semiconductor Cycle And The Malaysian Economy...

8

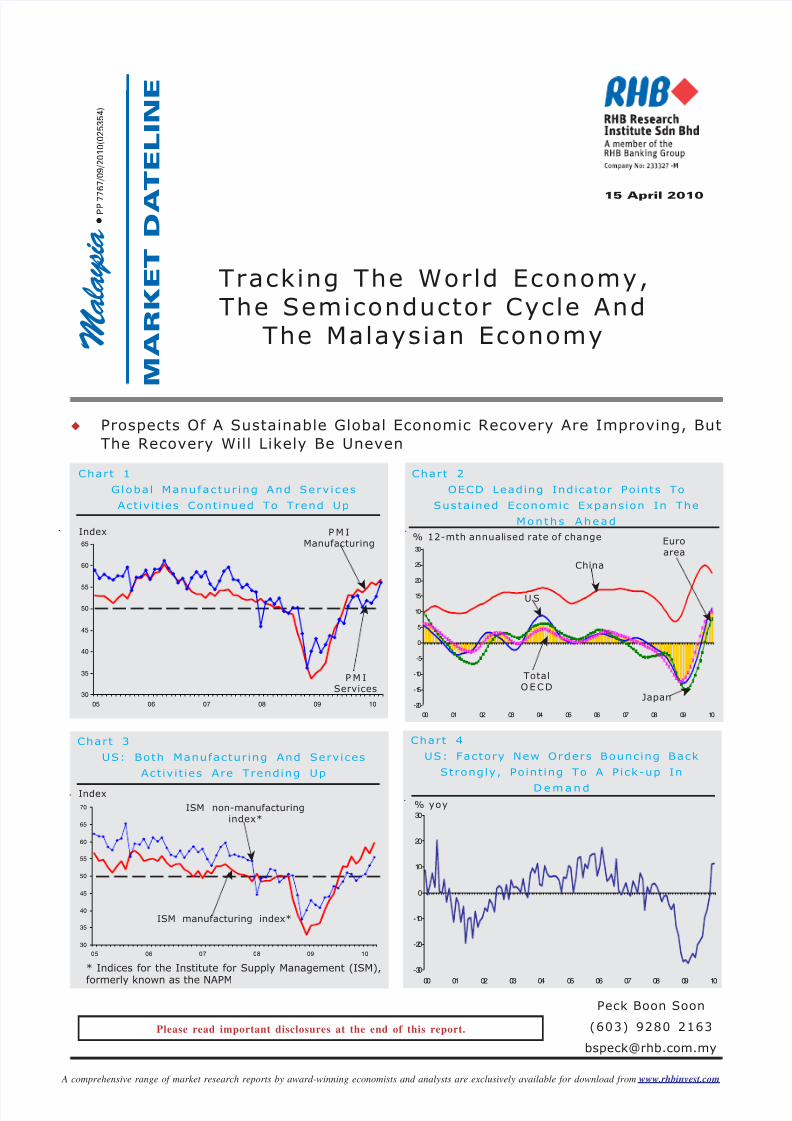

Prospects Of A Sustainable Global Economic Recovery Are Improving, But The Recovery Will Likely Be Uneven Tracking The World Economy, The Semiconductor Cycle And The Malaysian Economy Peck Boon Soon (603) 9280 2163 [email protected] Please read important disclosures at the end of this report. Chart 3 US: Both Manufacturing And Services Activities Are Trending Up Index * Indices for the Institute for Supply Management (ISM), formerly known as the NAPM ISM manufacturing index* 30 35 40 45 50 55 60 65 70 05 06 07 08 09 10 ➤ ISM non-manufacturing index* ➤ Chart 4 US: Factory New Orders Bouncing Back Strongly, Pointing To A Pick-up In Demand % yoy -3 0 -2 0 -1 0 0 1 0 2 0 3 0 0 0 01 0 2 03 0 4 0 5 06 0 7 08 0 9 10 -2 0 -1 5 -1 0 -5 0 5 10 15 20 2 5 30 00 01 0 2 03 0 4 05 0 6 07 0 8 09 1 0 Chart 2 OECD Leading Indicator Points To Sustained Economic Expansion In The Months Ahead % 12-mth annualised rate of change US ➤ China ➤ Japan ➤ Euro area ➤ Total OECD ➤ Chart 1 Global Manufacturing And Services Activities Continued To Trend Up Index 30 35 40 45 50 55 60 65 05 06 07 08 09 10 PMI Manufacturing PM I Services ➤ ➤ M a l a y s i a • • • P P 7 7 6 7 / 0 9 / 2 0 1 0 ( 0 2 5 3 5 4 ) M A R K E T D A T E L I N E 15 April 2010 A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

-

Upload

rhb-invest -

Category

Documents

-

view

223 -

download

0

Transcript of Economic Update : Tracking The World Economy,The Semiconductor Cycle And The Malaysian Economy...

8/9/2019 Economic Update : Tracking The World Economy,The Semiconductor Cycle And The Malaysian Economy -15/04/2010

http://slidepdf.com/reader/full/economic-update-tracking-the-world-economythe-semiconductor-cycle-and-the 1/8

Prospects Of A Sustainable Global Economic Recovery Are Improving, But

The Recovery Will Likely Be Uneven

Tracking The World Economy,The Semiconductor Cycle And

The Malaysian Economy

Peck Boon Soon

(603) 9280 2163

Please read important disclosures at the end of this report.

Chart 3

US: Both Manufacturing And Services

Activ it ies Are Trending Up

Index

* Indices for the Institute for Supply Management (ISM),

formerly known as the NAPM

ISM manufacturing index*

30

35

40

45

50

55

60

65

70

05 06 07 08 09 10

➤

ISM non-manufacturingindex*

➤

Chart 4

US: Factory New Orders Bouncing Back

Strongly, Point ing To A Pick-up In

D e m and

% yoy

-30

-20

-10

0

10

20

30

00 01 02 03 04 05 06 07 08 09 10

-20

-15

-10

-5

0

5

10

15

20

25

30

00 01 02 03 04 05 06 07 08 09 10

Chart 2

OECD Leading Indicator Points To

Sustained Economic Expansion In The

Months Ahead

% 12-mth annualised rate of change

U S➤

China

➤

Japan ➤

Euroarea

➤

TotalOECD

➤

Chart 1

Global Manufactur ing And Serv ices

Activ it ies Continued To Trend Up

Index

30

35

40

45

50

55

60

65

05 06 07 08 09 10

P M IManufacturing

P M IServices

➤

➤

Malaysia

• • • •

PP

7767/09/2010(025354)

MARKETDATELINE

15 April 2010

A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

8/9/2019 Economic Update : Tracking The World Economy,The Semiconductor Cycle And The Malaysian Economy -15/04/2010

http://slidepdf.com/reader/full/economic-update-tracking-the-world-economythe-semiconductor-cycle-and-the 2/8

ECONOMY IN CHARTS2

A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

Chart 9

US: The Fed Wil l Gradually Unwind Its

Quantitat ive Easing Pol icy

US$bn (Total Assets Of The Fed)

0

500

1,000

1,500

2,000

2,500

07 08 09 10

Chart 10

US: Core Inflat ion Rate Is Trending Lower,

Raising Concerns Over

Disinf lat ionary Pressure

% yoy

-3

-2

-1

0

1

2

3

4

5

6

00 01 02 03 04 05 06 07 08 09 10

CoreC P I

➤

TotalC P I

➤

Chart 8

US: Home Sales Showing Signs Of Weakness

But May Not Pose A Major Drag To The

Economy

% yoy

-60

-50

-40

-30

-20

-10

0

10

20

30

40

50

00 01 02 03 04 05 06 07 08 09 10

New homesales

➤

Existing homesales

➤

Chart 6

US: Consumer Spending Heading Up,

Underpinned By A Gradual Improvement In

Employment

% annualised

-4

-3

-2

-1

0

1

2

3

4

5

2005 2006 2007 2008 2009 2010

(Personal consumption expenditure)

Chart 5

US: Retail Sales On A Recovery Path

% yoy

-30

-20

-10

0

10

20

30

01 02 03 04 05 06 07 08 09 10

Autosales

➤

Non-autosales

➤

Total retailsales

➤

Chart 7

US: Recrui tment P ick ing Up And

Unemployment Rate Ho lding Stable

(‘000) %

-1000

-800

-600

-400

-200

0

200

400

600

00 01 02 03 04 05 06 07 08 09 10

0

2

4

6

8

10

12

Non-farm payroll(LHS)

➤

Unemploymentrate (RHS)

➤

Employment in temporaryhelp services (LHS)

➤

8/9/2019 Economic Update : Tracking The World Economy,The Semiconductor Cycle And The Malaysian Economy -15/04/2010

http://slidepdf.com/reader/full/economic-update-tracking-the-world-economythe-semiconductor-cycle-and-the 3/8

3ECONOMY IN CHARTS

A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

Chart 13

Euro land: Serv ices And Manufactur ing

Activ it ies Heading North

IndexP M I

Services

➤

30

35

40

45

50

55

60

65

00 01 02 03 04 05 06 07 08 09 10

P M IManufacturing

➤

Chart 12

China: Escalating House Prices, While

Exports Have Recovered

% yoy % yoy

-2

0

2

4

6

8

10

12

06 07 08 09 10

-40

-30

-20

-10

0

10

20

30

40

50

60House price

(LHS)

➤

Exports(RHS)

➤

Chart 15

Japan: A Sharp Recovery In Exports Lifted

Industr ia l Product ion

% yoy

-60

-40

-20

0

20

40

60

05 06 07 08 09 10

Exports

➤

I P I

➤

Chart 11

China: Manufactur ing Act iv i t ies Bouncing

Back But Investment, Though Sti l l Strong,

Is Easing

Index % yoyFixed

investment(RHS)

➤

35

40

45

50

55

60

65

05 06 07 08 09 10

10

15

20

25

30

35

ManufacturingP M I

(LHS)

➤

Chart 14

Euroland: Business Confidence Improved,

While Consumer Confidence Eased

Index Index

Consumerconfidence

(LHS)

➤

-40

-35

-30

-25

-20

-15

-10

-5

0

5

00 01 02 03 04 05 06 07 08 09 10

-40

-35

-30

-25

-20

-15

-10

-5

0

5

10

Business climateindicator

(RHS)

➤

Chart 16

Japan: Business Confidence Improved,

While Consumer Confidence Eased

Index Index

-70

-60

-50

-40

-30

-20

-10

0

10

20

30

40

01 02 03 04 05 06 07 08 09 10

0

10

20

30

40

50

60

Tankan survey(large mfg.)

(LHS)➤

Consumer confidence(RHS)

➤

8/9/2019 Economic Update : Tracking The World Economy,The Semiconductor Cycle And The Malaysian Economy -15/04/2010

http://slidepdf.com/reader/full/economic-update-tracking-the-world-economythe-semiconductor-cycle-and-the 4/8

ECONOMY IN CHARTS4

A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

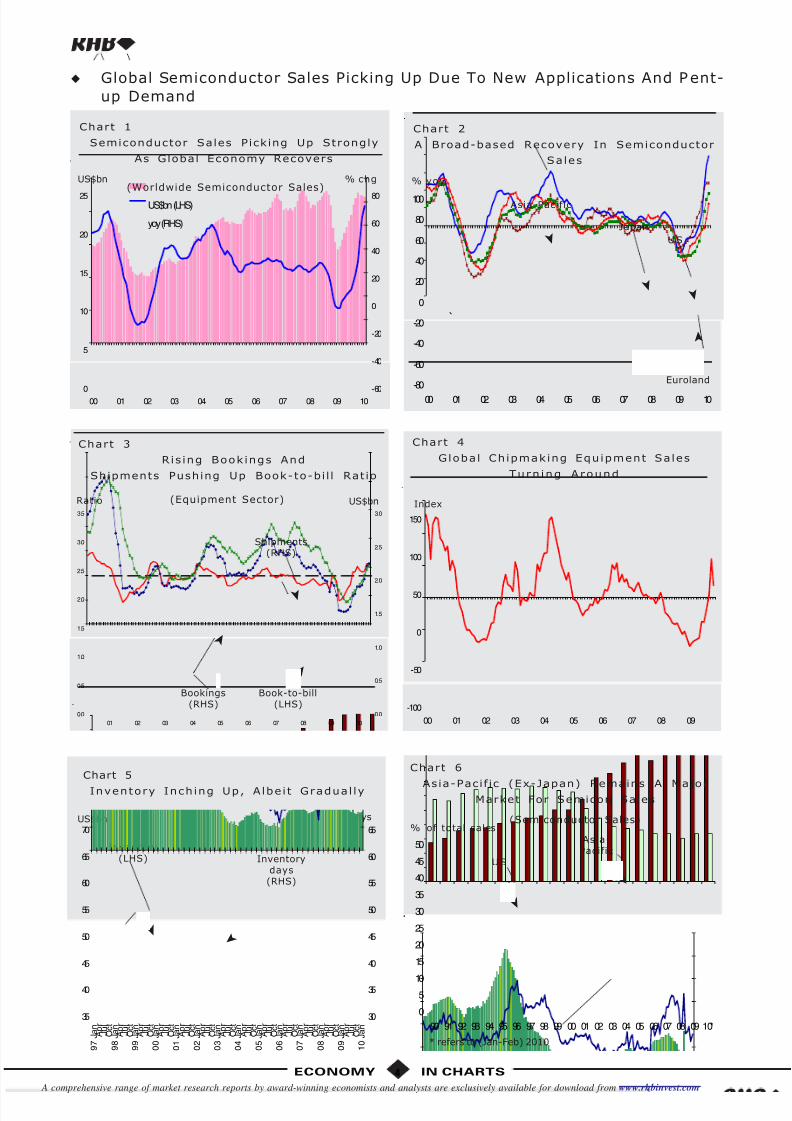

Global Semiconductor Sales Picking Up Due To New Applications And Pent-

up Demand

Chart 1

Semiconductor Sales Picking Up Strongly

As Global Economy Recovers

(Worldwide Semiconductor Sales)% chgUS$bn

0

5

10

15

20

25

00 01 02 03 04 05 06 07 08 09 10-60

-40

-20

0

20

40

60

80US$bn (LHS)

yoy (RHS)

Chart 2

A Broad-based Recovery In Semiconductor

Sales

% yoy

-80

-60

-40

-20

0

20

40

60

80

100

00 01 02 03 04 05 06 07 08 09 10

`

Asia-Pacific

➤

➤

Japan

Euroland

➤

U S

➤

Chart 5

Inventory Inching Up, Albe i t Gradual ly

US$bn Days

Inventorydays(RHS)

➤

35

40

45

50

55

60

65

70

9 7 J a n A p r

J u l

O c t

9 8 J a n A p r

J u l

O c t

9 9 J a n A p r

J u l

O c t

0 0 J a n A p r

J u l

O c t

0 1 J a n A p r

J u l

O c t

0 2 J a n A p r

J u l

O c t

0 3 J a n A p r

J u l

O c t

0 4 J a n A p r

J u l

O c t

0 5 J a n A p r

J u l

O c t

0 6 J a n A p r

J u l

O c t

0 7 J a n A p r

J u l

O c t

0 8 J a n A p r

J u l

O c t

0 9 J a n A p r

J u l

O c t

1 0 J a n

30

35

40

45

50

55

60

65

Inventory(LHS)

➤

Chart 4

Global Chipmaking Equipment Sales

Turn ing Around

Index

-100

-50

0

50

100

150

00 01 02 03 04 05 06 07 08 09

US$bn

Chart 3

Ris ing Book ings And

Shipments Pushing Up Book-to-bi l l Ratio

Ratio (Equipment Sector)

Bookings(RHS)

Book-to-bill(LHS)

Shipments(RHS)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

01 02 03 04 05 06 07 08 09 10

0.0

0.5

1.0

1.5

2.0

2.5

3.0

➤

➤

➤

Chart 6

Asia-Pacif ic (Ex-Japan) Remains A MajorMarket For Semicon Sales

% of total sales(Semiconductor Sales)

0

510

15

20

25

30

35

40

45

50

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10*

* refers to (Jan-Feb) 2010

Asia-Pacific

➤

US

➤

8/9/2019 Economic Update : Tracking The World Economy,The Semiconductor Cycle And The Malaysian Economy -15/04/2010

http://slidepdf.com/reader/full/economic-update-tracking-the-world-economythe-semiconductor-cycle-and-the 5/8

5ECONOMY IN CHARTS

A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

Malaysia : Real GDP Recovery Picking Up Momentum

Chart 2

Industr ia l Product ion And Exports

Head ing Up

% yoy

-40

-30

-20

-10

0

10

20

30

40

50

99 00 01 02 03 04 05 06 07 08 09 10

Totalexports

➤

Manufacturingproduction

➤

Chart 6

Recovery In Imports Of Intermediate InputsPoints To An Improvement In

Manufactured Exports

% yoy

Intermediateinputs

➤

Manufacturedexports

-40

-30

-20

-10

0

10

20

30

40

50

00 01 02 03 04 05 06 07 08 09 10

➤

Chart 3

Exports To China

And As ia-Pac i f ic Ex-Japan Recover ing

% yoy

-60

-40

-20

0

20

40

60

80

100

120

140

160

00 01 02 03 04 05 06 07 08 09 10

China

➤

Asia-Pacificex-Japan

➤

Chart 4

Exports To US, Euroland And Japan

Turn ing Around

% yoy

-60

-40

-20

0

20

40

60

80

00 01 02 03 04 05 06 07 08 09 10

U S

➤

Japan

➤ E U

➤

Chart 1

Leading Index Points To A Sustained

Economic Recovery

%

6 - m t h a n n u a l r a t e o f c h a n g e

%

1 2 - m t h a n n u a l r a t e o f c h a n g e

-5

0

5

10

15

20

00 01 02 03 04 05 06 07 08 09 10

-15

-10

-5

0

5

10

15

OECD leadingindex(RHS)

➤

Malaysia leading economicindex (LHS)

➤

Chart 5

A Broad-based Recovery In Exports ByP roduc t s

% yoy

E&Eexports

➤

Exports of non-E&Emanufactured goods

➤

Commodityexports

➤

-60

-40

-20

0

20

40

60

80

00 01 02 03 04 05 06 07 08 09 10

8/9/2019 Economic Update : Tracking The World Economy,The Semiconductor Cycle And The Malaysian Economy -15/04/2010

http://slidepdf.com/reader/full/economic-update-tracking-the-world-economythe-semiconductor-cycle-and-the 6/8

ECONOMY IN CHARTS6

A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

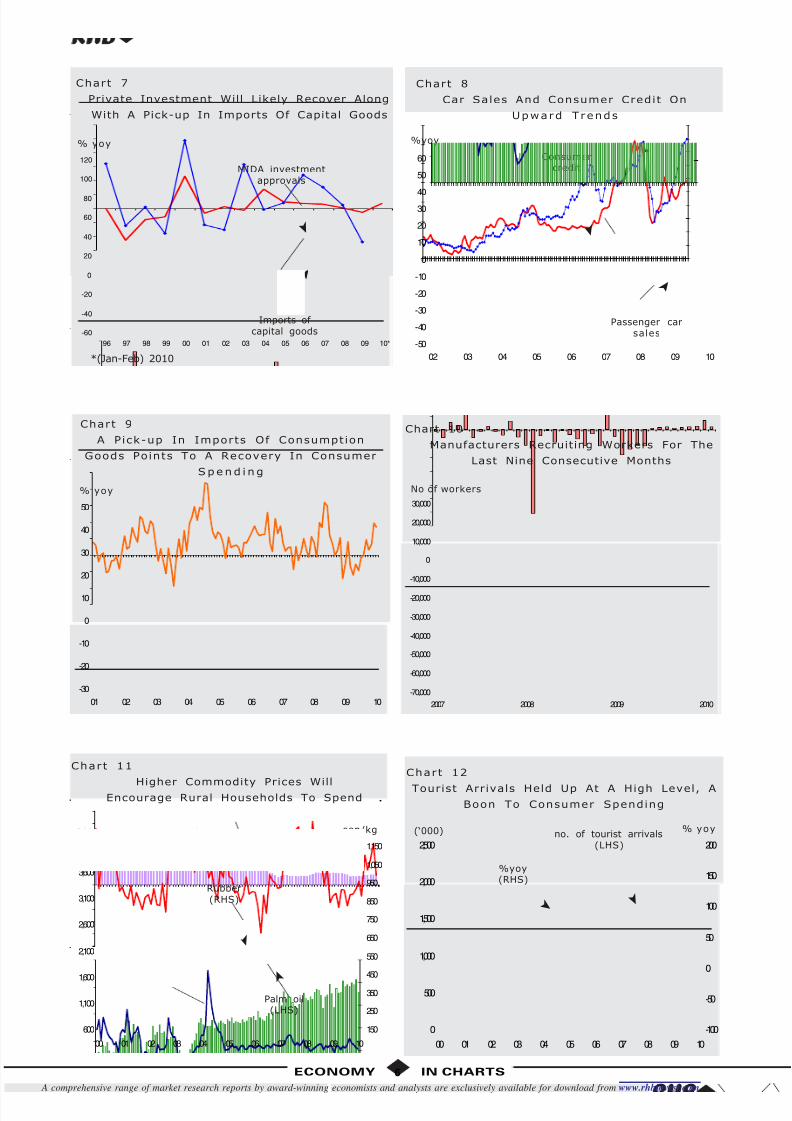

Chart 10

Manufacturers Recruiting Workers For The

Last Nine Consecutive Months

No of workers

-70,000

-60,000

-50,000

-40,000

-30,000

-20,000

-10,000

0

10,000

20,000

30,000

2007 2008 2009 2010

Chart 12

Tourist Arrivals Held Up At A High Level, A

Boon To Consumer Spending

(‘000) % yoy

➤

%yoy(RHS)

no. of tourist arrivals(LHS)

➤

0

500

1,000

1,500

2,000

2,500

00 01 02 03 04 05 06 07 08 09 10

-100

-50

0

50

100

150

200

Chart 8

Car Sales And Consumer Credit On

Upward Trends

%yoy

Consumercredit

➤

-50

-40

-30

-20

-10

0

10

20

3040

50

60

02 03 04 05 06 07 08 09 10

Passenger carsales

➤

% yoy

Chart 9

A Pick-up In Imports Of Consumption

Goods Points To A Recovery In Consumer

Spe nd i ng

-30

-20

-10

0

10

20

30

40

50

01 02 03 04 05 06 07 08 09 10

Chart 7

Private Investment Will Likely Recover Along

With A Pick-up In Imports Of Capital Goods

% yoy

*(Jan-Feb) 2010

-60

-40

-20

0

20

40

60

80

100

120

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10*

MIDA investmentapprovals

➤

Imports of capital goods

➤

Chart 11

Higher Commodity Prices WillEncourage Rural Households To Spend

RM/ tonne sen/kg

Palm oil(LHS)

➤

600

1,100

1,600

2,100

2,600

3,100

3,600

4,100

00 01 02 03 04 05 06 07 08 09 10

150

250

350

450

550

650

750

850

950

1,050

1,150

Rubber(RHS)

➤

8/9/2019 Economic Update : Tracking The World Economy,The Semiconductor Cycle And The Malaysian Economy -15/04/2010

http://slidepdf.com/reader/full/economic-update-tracking-the-world-economythe-semiconductor-cycle-and-the 7/8

7ECONOMY IN CHARTS

A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

Chart 17

Excess Liquidity Mopped Up By BNMRemains Substant ia l

RMbn

BNM bills

Excess funds mopped up by BNMfrom interbank market

Repos (estimate)

2

52

102

152

202

252

302

352

00 01 02 03 04 05 06 07 08 09 10

RM218.7bn(end-Mar)

➤

Chart 18

Smaller Current Account Surplus In TheBalance Of Payments, But Remains

Sizeable

RMbn

-20

-10

0

10

20

30

40

50

97 98 99 00 01 02 03 04 05 06 07 08 09

currentaccount in the

balance of payments

➤

% yoy(RHS)

➤

Chart 13

St imulus Spending Leading To H igher

Pub l i c Spend ing

(Federal Government Expenditure) % yoyRMbn

0

2

4

6

8

10

12

14

16

18

20

98 99 00 01 02 03 04 05 06 07 08 09

-100

-50

0

50

100

150

200

./

RMbn(LHS)

➤

%, yoy(RHS)

➤

Chart 15

Inflat ion Picking Up But Wil l Likely

Be Manageable

% yoy

-6

-4

-2

0

2

4

6

8

10

12

05 06 07 08 09 10

TotalC P I

➤

CoreC P I

➤

Chart 14

Loan Growth Acce lerat ing And Asset

Qual i ty Remain ing Stable

% of total loans % yoy

0

2

4

6

8

10

12

14

16

18

03 04 05 06 07 08 09 10

0

2

4

6

8

10

12

143-mth Gross NPLs (LHS)

6-mth Gross NPLs (LHS)

Total loan growth (RHS)

Chart 16

Normalisat ion Of Monetary Condit ions

Wil l Continue, Albeit At A Measured Pace

% p.a.

3-mthKLIBOR

O P R

➤

➤

0

1

2

3

4

5

6

7

8

00 01 02 03 04 05 06 07 08 09 10

3-mth USinterbank rate

➤

8/9/2019 Economic Update : Tracking The World Economy,The Semiconductor Cycle And The Malaysian Economy -15/04/2010

http://slidepdf.com/reader/full/economic-update-tracking-the-world-economythe-semiconductor-cycle-and-the 8/8

RHB DEALING AND RESEARCH OFFICES

MALAYSIARHB Investment Bank BhdLevel 10, Tower One, RHB Centre,Jalan Tun Razak50400 Kuala LumpurP.O. Box 1269950786 Kuala Lumpur, MalaysiaTel (General) : (603) 9285 2233

Dealing OfficeTel (Dealing) : (603) 9285 2288Fax (Dealing) : (603) 9284 7467

RHB Research Institute Sdn BhdLevel 10, Tower One, RHB Centre,Jalan Tun Razak50400 Kuala LumpurP.O. Box 1269950786 Kuala Lumpur, MalaysiaTel (Research) : (603) 9280 2160Fax (Research) : (603) 9284 8693

Lim Chee SingDirector

RHBRI is a participant of the CMDF-Bursa Research Scheme and will receive compensation for the participation.Additional information on recommended securities, subject to the duties of confidentiality, will be made available

upon request.

This report may not be reproduced or redistributed, in whole or in part, without the written permission of RHBRIand RHBRI accepts no liability whatsoever for the actions of third parties in this respect.

IMPORTANT DISCLOSURES

This report has been prepared by RHB Research Institute Sdn Bhd (RHBRI) and is for private circulation only to clients of RHBRIand RHB Investment Bank Berhad (previously known as RHB Sakura Merchant Bankers Berhad). It is for distribution only undersuch circumstances as may be permitted by applicable law. The opinions and information contained herein are based on generallyavailable data believed to be reliable and are subject to change without notice, and may differ or be contrary to opinions expressedby other business units within the RHB Group as a result of using different assumptions and criteria. This report is not to beconstrued as an offer, invitation or solicitation to buy or sell the securities covered herein. RHBRI does not warrant the accuracyof anything stated herein in any manner whatsoever and no reliance upon such statement by anyone shall give rise to any claimwhatsoever against RHBRI. RHBRI and/or its associated persons may from time to time have an interest in the securities mentionedby this report.

This report does not provide individually tailored investment advice. It has been prepared without regard to the individual financialcircumstances and objectives of persons who receive it. The securities discussed in this report may not be suitable for all investors.RHBRI recommends that investors independently evaluate particular investments and strategies, and encourages investors toseek the advice of a financial adviser. The appropriateness of a particular investment or strategy will depend on an investor’sindividual circumstances and objectives. Neither RHBRI, RHB Group nor any of its affiliates, employees or agents accepts anyliability for any loss or damage arising out of the use of all or any part of this report.

RHBRI and the Connected Persons (the “RHB Group”) are engaged in securities trading, securities brokerage, banking and financingactivities as well as providing investment banking and financial advisory services. In the ordinary course of its trading, brokerage,banking and financing activities, any member of the RHB Group may at any time hold positions, and may trade or otherwise effecttransactions, for its own account or the accounts of customers, in debt or equity securities or loans of any company that maybe involved in this transaction.

“Connected Persons” means any holding company of RHBRI, the subsidiaries and subsidiary undertaking of such a holding companyand the respective directors, officers, employees and agents of each of them. Investors should assume that the “Connected Persons” are seeking or will seek investment banking or other services from the companies in which the securities have been discussed/covered by RHBRI in this report or in RHBRI’s previous reports.This report has been prepared by the research personnel of RHBRI. Facts and views presented in this report have not been reviewedby, and may not reflect information known to, professionals in other business areas of the “Connected Persons,” including investmentbanking personnel.

The research analysts, economists or research associates principally responsible for the preparation of this research report have

received compensation based upon various factors, including quality of research, investor client feedback, stock picking, competitivefactors and firm revenues.

◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆