Dem&sup(1)

40

Fall ‘ 97 Principles of Microeconomics slide 1 This is a PowerPoint presentation on elementary supply and demand. A left mouse click or the enter key will add and element to a slide or move you to the next slide. The back space key will take you back an element or slide. If you wish to exit the presentation, the escape key will do it! R. Larry Reynolds 1997

Transcript of Dem&sup(1)

Fall ‘ 97 Principles of Microeconomics

slide 1

This is a PowerPoint presentation on elementary supply and demand. A left mouse click or the enter key will add and element to a slide or move you to the next slide. The back space key will take you back an element or slide. If you wish to exit the presentation, the escape key will do it!

R. Larry Reynolds 1997

Fall ‘ 97 Principles of Microeconomics

slide 2

Demand and Supply· Markets as allocative mechanism require:

· nonattenuated property rights [exclusive, enforceable, transferable]

· “voluntary” transactions· Markets include all “potential buyers and

sellers”· behavior of buyers is represented by “demand”

[benefits side of model]

· behavior of sellers is represented by “supply” [cost side of model]

Fall ‘ 97 Principles of Microeconomics

slide 3

Markets, Supply and Demand

· markets include all potential buyers and sellers· geographic boundaries of market· markets defined by nature of product

and characteristics of buyers· conditions of entry into market· markets, competition and substitutes

Fall ‘ 97 Principles of Microeconomics

slide 4

Demand· Definition: “A schedule of the quantities

of a good that buyers are willing and able to purchase at each possible price during a period of time, ceteris paribus. [all other things held constant]”

· Demand can also be perceived as a schedule of the maximum prices buyers are willing and able to pay for each unit of a good.

Fall ‘ 97 Principles of Microeconomics

slide 5

Demand Function· Is the functional relationship between the

price of the good and the quantity of that good purchased in a given time period [UT], income, other prices and preferences being held constant.

· A change in income, prices of other goods or preferences will alter [‘shift’] the demand function.

Fall ‘ 97 Principles of Microeconomics

slide 6

Quantity demanded· A change in the price of the good under

consideration will change the “quantity demanded.”

· Q = f (P, holding M, Pr , preferences constant); where: M = income

Pr = prices of related goods • ∆P causes a change in X [∆Q], this is a “change in

quantity demanded”

Fall ‘ 97 Principles of Microeconomics

slide 7

Change in demand· If M, Pr, or preferences change, the demand

function [relationship between P and Q] will change.

· These are sometimes called “demand shifters”· Be sure to understand difference between a

“change in demand” and a “change in quantity demanded”· change in demand --- shift of the function· change in quantity demanded --- move on the function

Fall ‘ 97 Principles of Microeconomics

slide 8

“Law of Demand”

· Theory and empirical evidence suggest that the relationship between Price and Quantity is an inverse or negative relationship

· At higher prices, quantity purchased is smaller, or at lower prices the quantity purchased is greater.

Fall ‘ 97 Principles of Microeconomics

slide 9

An example of hot chocolate:There is a coffee cart in the building that primarily serves the individuals who work in the building. The market is defined to some extent by the geography of the building. Individuals who buy the hot chocolate rarely come from other buildings to purchase a cup. During the time period [UT]under consideration [8:00-9:00am on a week day ] the incomes and preferences of buyers are unlikely to change. The prices of coffee, lattes, etc. can be controlled by the vendor and the price of soft drinks from the machines remains constant. The number of workers in the building remain at a constant level.

Under these circumstances, we observe the number of cups of hot chocolate [H] sold each morning as the price [P] is changed. From these observations the demand relationship is estimated.

Fall ‘ 97 Principles of Microeconomics

slide 10

Cups of Hot Chocolate [H] purchased

each day between 8 -9 am

price per cup

cups

purchased

A 0 20 .

B $ . 5 0 15 .

C $ . 7 5 12 . 5

D $ 1 . 0 0 10 .

E $ 1 . 2 5 7 . 5

F $ 1 . 5 0 5 .

G $ 1 . 7 5 2 . 5

H $ 2 . 0 0 0

The demand relationship can be demonstrated as atable:

Demand is a schedule ofquantities that will be purchased at a schedule

of prices during a given time period, cet. par.As the price is increased,the quantity purchased decreases.

∆Q < 0[-7.5]

∆P > 0[+.75]

This demand relationship can be expressed as an equation:P = 2 - .1Q or Q = 20 - 10P: [Q = f (P, . . .) but we graph P onthe Y axis and Q on the X axis.]

Fall ‘ 97 Principles of Microeconomics

slide 11

The demand relationship can be expressed as a table(previous slide) or an equation [either P = 2 - .1Q or Q = 20 - 10P]

The data from the table or equation can be graphed:

QUANTITY{CUPS/UT}

PRIC

E

2 4 6 8 10 12 14 16 18 20 22 24

.25

.50

.75

1.001.251.50

1.75 2.00 2.25

$

.....

.

Demand

P = $2, Then Q = 0 P = $1.75, then Q = 2.5

P = $1.50, then Q = 5P = $1.25, Q = 7.5

P = $1, then Q = 10P = 0, then Q = 20

The demand function can be represented as a table, an equation or a graph.

Fall ‘ 97 Principles of Microeconomics

slide 12

QUANTITY

{CUPS/ UT}

PRIC

E

2 4 6 8 10 12 14 16 18 20 22 24

.25

.50

.75

1.001.251.50

1.75 2.00 2.25

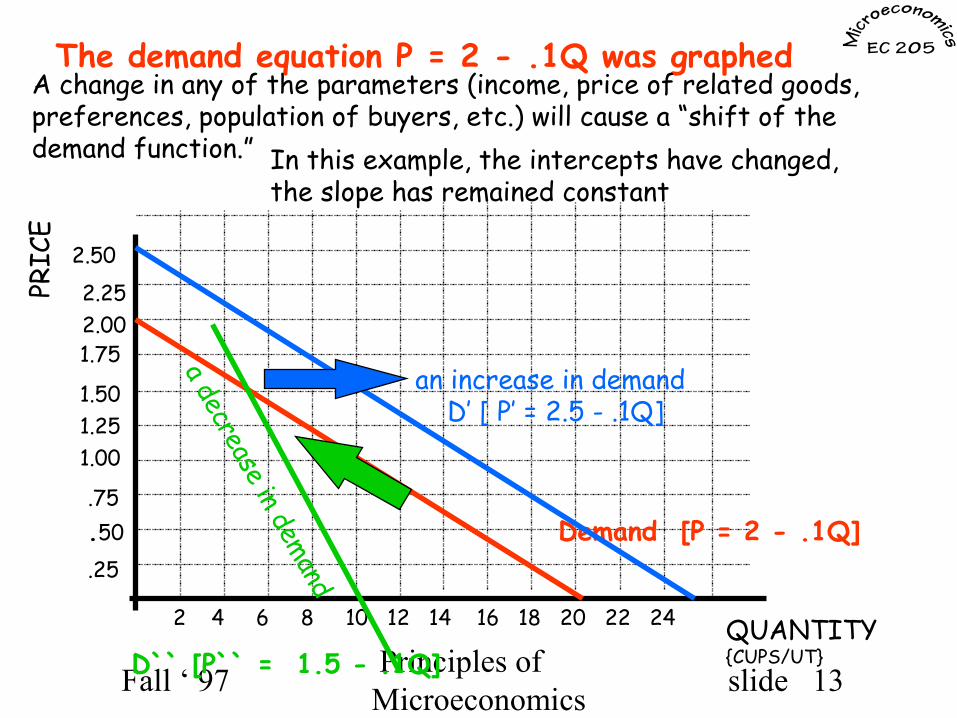

The demand equation P = 2 - .1Q was graphed

Demand [P = 2 - .1Q]

A change in “quantity demanded” is a movement on the demand function caused by a change in the independent variable [ price].

∆P from $1.50 to $1 causes ∆Q from 5 to 10 units

5

..A

Β

A change in quantity demanded is a move from point A to B “on the demand function”

caused by a change in the price!

Fall ‘ 97 Principles of Microeconomics

slide 13

QUANTITY{CUPS/UT}

PRIC

E

2 4 6 8 10 12 14 16 18 20 22 24

.25

.50

.75

1.001.251.50

1.75 2.00 2.25

The demand equation P = 2 - .1Q was graphed

Demand [P = 2 - .1Q]

A change in any of the parameters (income, price of related goods,preferences, population of buyers, etc.) will cause a “shift of the demand function.”

2.50

an increase in demand D’ [ P’ = 2.5 - .1Q]

In this example, the intercepts have changed,the slope has remained constant

a decrease in demandD`` [P`` = 1.5 - .1Q]

Fall ‘ 97 Principles of Microeconomics

slide 14

QUANTITY{CUPS/UT}

PRIC

E

2 4 6 8 10 12 14 16 18 20 22 24

.25

.50

.75

1.001.251.50

1.75 2.00 2.25

2.50

Demand [P = 2 - .1Q]

A change in the parameters [income, Pr, preferences, population, etc.] might alter the relationship by changing the slope

an increase in the slope P = 2 - .25Q

buyersare lessresponsiveto ∆P

a decrease in the slope

P` = 2- .048076923Q

buyers are more responsive to ∆P

A change in demand refers to a movement or shift of the entire demand function

Fall ‘ 97 Principles of Microeconomics

slide 15

Demand [P = 2 - .1Q]

An increase in demand

QUANTITY{CUPS/UT}

PRIC

E

2 4 6 8 10 12 14 16 18 20 22 24

.25

.50

.75

1.001.251.50

1.75 2.00 2.25

2.50

D2 [an increase in demand]

increase

results in a larger quantity beingpurchased at each price

Q = 7.5

In this case, an increase in demand resultsin an increase in the amount that will be purchased at a price of $1.25. At this price the Quantity purchased increases from 7.5to 18. An increase in demand!

Fall ‘ 97 Principles of Microeconomics

slide 16

QUANTITY[steak /UT]

PRIC

E

2 4 6 8 10 12 14 16 18 20 22 24

.25

.50

.75

1.001.251.50

1.75 2.00 2.25

2.50

Demand [P = 2 - .1Q]

Effect of a change in the price of a substitute

If the price of a substitute, like chicken, increasesbuyers will buy more steak at each price of steak

Demand for steak increases when

the price of chicken increases

If the price of chicken decreases, the buyers will want less steak at each possible price of steak; the demand for steak decreases!

D2

a decrease

in the demand

for steak

Fall ‘ 97 Principles of Microeconomics

slide 17

Complementary goodsTwo goods may be complimentary, i.e. the two goods are “used together. [tennis rackets and tennis balls or CD’s and CD Players]An increase in the price of CD’s will tend to reduce the demand [shift the demand function to the left] for CD Players

CD’s/UT

PCD’s

Dcd

CD Playersper UT

Pplayers

Dplayer

P2

P1

Y1Y

As the price of CD’s increases from P1 to P2, the quantity of CD’s decreases from Y1

to Y.

As people buy fewerCD’s, the demand forCD players decreases.

D’player

At the same price, Ppl , the demand

is reducedfrom Dto D’.

X1X

Ppl

Fall ‘ 97 Principles of Microeconomics

slide 18

Compliments and Substitutes

· Substitutes:· if the price of a substitute increases, the

demand for the good increases.· if the price of a substitute decreases, the

demand for the good decreases.· Compliments:

· if the price of a compliment increases, the demand for the good decreases.

· if the price of a compliment decreases, the demand for the good increases.

Fall ‘ 97 Principles of Microeconomics

slide 19

Demand Summary· “Law of Demand” holds that usually as the

price of a good increases, individuals will buy less of it.

· The nature of this relationship is influenced by a variety of other variables;· income, preferences, prices of related

goods, and other circumstances· as these circumstances change, the

demand relationship changes or “shifts.”

Fall ‘ 97 Principles of Microeconomics

slide 20

Demand Summary [cont. . . ]

· A “change in demand” means the relationship between price and quantity was altered by a change in some other variable [a demand “shifter”] The demand “shifts.”

· A “change in quantity demanded” is a change in the quantity bought that was caused by a change in the price of the good. There is a movement on the demand function.

Fall ‘ 97 Principles of Microeconomics

slide 21

Supply· Supply is defined as a schedule of

quantities of a good that will be produced and offered for sale at a schedule of prices during a given time [UT], ceteris paribus.

· Generally, producers are willing to offer greater quantities of a good for sale at higher prices; a positive relationship between price and quantity supplied.

Fall ‘ 97 Principles of Microeconomics

slide 22

Supply Schedule

Observation Price QuantitySupplied

A $1 6

B $2 10

C $3 14

D $4 18

E

F $5 22

Q

P

2 4 6 8 10 12 14

$1

$2

$3

$4$5

A supply schedule can be displayed as a table.

The information can be representedon a graph by plotting each price quantity combination.

. . . .supply

Both the graph and the tablerepresent a supply relationship: Q = 2 + 4P

Fall ‘ 97 Principles of Microeconomics

slide 23

Change in Quantity Supplied

· A change in the price of the good causes a change in the “quantity supplied.”

· The change in the price of the good causes a “movement on the supply function,” not a change or “shift of the supply function.”

Fall ‘ 97 Principles of Microeconomics

slide 24

Supply Schedule

Observation Price QuantitySupplied

A $1 6

B $2 10

C $3 14

D $4 18

E

F $5 22

supply

Q/ut

P

$1

$2

$3

$4

$5

2 4 6 8 10 12 14 16

A change in the price “causes” achange in the “quantity supplied.”This can be represented by a “movement” on the supply function in the graph

∆P from $1 to $3

∆P “causes” the quantity suppliedto increase from 6 to 14.

∆P$1

$3“CAUSES” ∆Q

This is a change in “quantitysupplied.” Not to beconfused with a “change insupply!”

Fall ‘ 97 Principles of Microeconomics

slide 25

“Change in Supply”· A change in supply [like a change in demand]

refers to a change in the relationship between the price and quantity supplied.

· A change in supply is “caused” by a change in any variable, other than price, that influences supply

· A change in supply can be represented by a shift of the supply function on a graph

Fall ‘ 97 Principles of Microeconomics

slide 26

“Change in Supply” [cont. . . ]

· There are many factors that infuence the willingness of producers to supply a good.· technology· prices of inputs· returns in alternative choices· taxes, expectations, weather, number of

sellers, . . .· Qs = fs (P, Pinputs, technology, . . .)

Fall ‘ 97 Principles of Microeconomics

slide 27

“Change in Supply” [cont. . . ]

· Qs = fs (P, Pinputs, technology, number of sellers, taxes, . . .)

· A change in the price [P] causes a “change in quantity supplied;”

· a change in any other variable causes a “change in supply”

Fall ‘ 97 Principles of Microeconomics

slide 28

Supply Schedule

Observation Price QuantitySupplied

A $1 6

B $2 10

C $3 14

D $4 18

E

F $5 22

Q

P

$1

$2

$3

$4

$5

2 4 6 8 10 12 14 16

Given the supply schedule,

supply

An increase in the pricesof inputs would make itmore expensive to produceeach unit of output, therefore, the supply decreases

481216

20

The decreased quantityat each price “shifts” thesupply curve to the left!

new

supp

ly fu

nctio

n a shift to the leftis a decrease in supply

The development of a “new”technology that reduces thecost of production will “shift”the supply function to the right

an in

crea

se in

su

pply

Fall ‘ 97 Principles of Microeconomics

slide 29

Equilibrium

· Equilibrium: 1. a state of rest or balance due to the equal action of opposing forces. 2. equal balance between any powers, influences, [Webster’s Encyclopedic Unabridged Dictionary of the English Language]

· In a market an equilibrium is said to exist when the forces of supply [sellers] and demand [buyers] are in balance: the actions of sellers and buyers are coordinated. The quantity supplied equals the quantity demanded!

Fall ‘ 97 Principles of Microeconomics

slide 30

10 20 30 40 50 60 70 80 90 100 110 120 130

10

20304050

60

708090

100Px

[Pr

ice]

Qx/ UT

Given a demandfunction [whichrepresents thebehavior or choicesof buyers,

Demandand a supply functionthat represents the

behavior of sellers,

Supp

lyWhere the quantity that people want to buy is equal to the quantity that the producers want to sell, there is an equilibrium quantity.

60

The price that coordinates the preferences of the buyers and sellersis the equilibrium price.

$70

At the equilibrium price of $70, the quantity supplied is equal tothe quantity demanded.

Fall ‘ 97 Principles of Microeconomics

slide 31

10 20

30 40

50 60

70 80

90 100 1

10 120 1

30

2030

4050

6070

8090

100

Px

[Pric

e]

Qx/ UT

DemandSu

pply

When the price is greater than the equilibrium price, the amount that sellers want to sell at that price [quantity supplied] exceeds the amount that buyers are willing to purchase [quantitydemanded] at that price. The price is “too high.”

60

$70

equi

libri

um p

rice

equilibrium quantity

At a Price of $90 the quantity supplied is 80,

$90

80

the quantity demanded is 35

35

At $90 there is a surplusof 45 units [80-35=45]

surplus = 45

Fall ‘ 97 Principles of Microeconomics

slide 32

10 20

30 40

50 60

70 80 9

0 100 1

10 120 1

30

1020

3040

5060

7080

9010

0

Px

[Price

]

Qx/ UT

DemandSu

pply

60

$70

$90

8035

At a price of $90 a surplusof 45 units exists

surplus = 45

Suppliers have more to sell than buyers will purchase at a price of $90.

To get rid of these unsold units [inventory], the

sellers lower the price.

lower price

As the price of the good is reduced, the quantity supplied decreases.

Quantitysupplieddecreases

The quantity demanded increases as the price falls.

Quantitydemandedincreases

As the price moves toward equilibrium, quantity supplied and quantity demanded are brought into equilibrium.

.

.

Fall ‘ 97 Principles of Microeconomics

slide 33

10 20 30 40 50 60 70 80 90 100 110 120 130

10

20304050

60

708090

100Px

[ P

r ice

]

Qx/ UT

Demand

Supp

ly

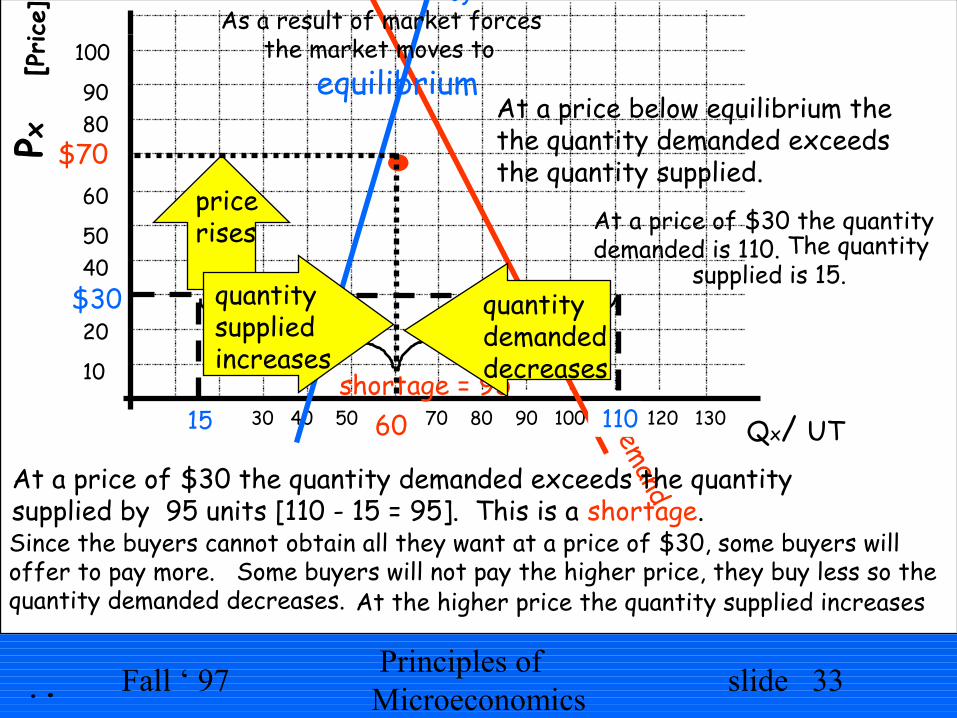

At a price below equilibrium thethe quantity demanded exceedsthe quantity supplied.

.

At a price of $30 the quantitydemanded is 110.

$30

110

The quantity supplied is 15.

15

At a price of $30 the quantity demanded exceeds the quantity supplied by 95 units [110 - 15 = 95]. This is a shortage.

shortage = 95

.

Since the buyers cannot obtain all they want at a price of $30, some buyers will offer to pay more. Some buyers will not pay the higher price, they buy less so the quantity demanded decreases.

pricerises

quantity demandeddecreases

At the higher price the quantity supplied increases

quantitysupplied increases

As a result of market forces the market moves to

equilibrium.

60

$70

Fall ‘ 97 Principles of Microeconomics

slide 34

10 20 3

0 40 5

0 60 7

0 80 9

0 100 11

0 120 13

0

1020

3040

5060

7080

90100

Px

[Pric

e]

Qx/ UT

DemandSu

pply

60

$70

The market for good X is in equilibrium at Px = $70

An increase in the price of a substitute [good Y] causes the demand for good X to increase.

demand increases

D2

As a result of the increased demand,market forces push Px up.

pricerises

$89

equilibriumquantityincreases

80

The increase in the demand for good X results in an increase in both the equilibrium price and quantity.

Identify other factors that couldincrease demand!

Fall ‘ 97 Principles of Microeconomics

slide 35

Demand

10 20 30 40 50 60 70 80 90 100 110 120 130

10

20304050

60

708090

100Px

[P

r ice

]

Qx/ UTSu

pply

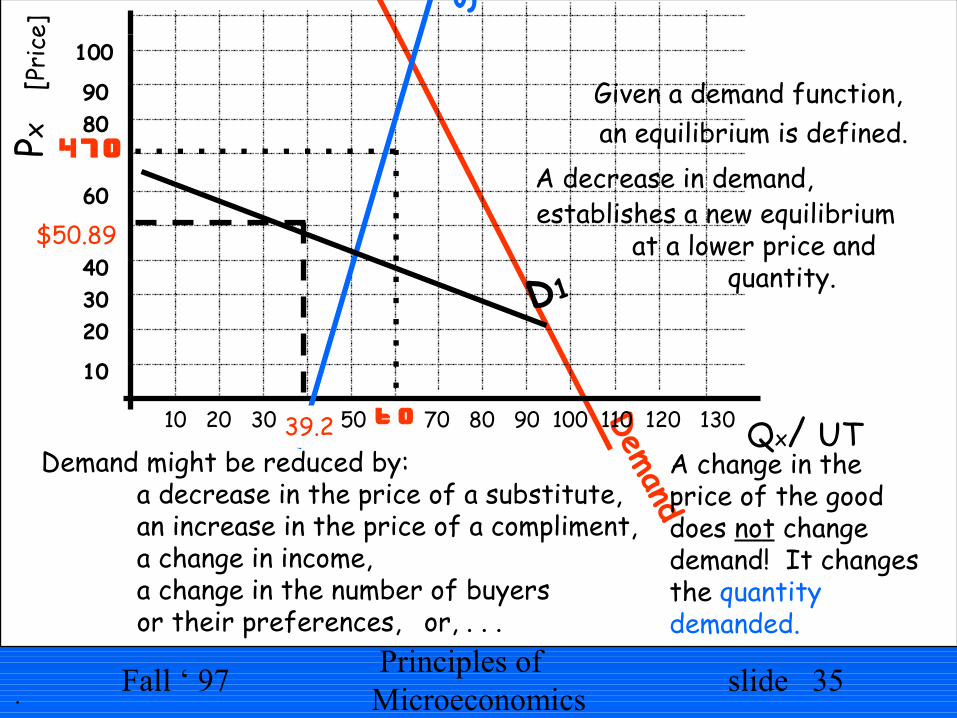

Given a demand function,an equilibrium is defined.

6 0

$70A decrease in demand,

D1

$50.89

39.2

establishes a new equilibriumat a lower price and

quantity.

Demand might be reduced by:a decrease in the price of a substitute,an increase in the price of a compliment,a change in income,a change in the number of buyers or their preferences, or, . . .

.

A change in the price of the gooddoes not changedemand! It changesthe quantity demanded.

Fall ‘ 97 Principles of Microeconomics

slide 36

10 20 3

0 40 5

0 60 7

0 80 9

0 100 11

0 120 13

0

1020

3040

5060

7080

9010

0

Px

[Pric

e]

Qx/ UT

DemandSu

pply

60

$70

Given an equilibrium condition in a market,

supplyincreases

an increase in supply willincrease the equilibriumquantity and decreaseequilibrium P.

S2

price falls$50

Quantity increases

86Identify factors that increase supply: 1. fall in price of inputs 2. improved technology 3. increase in number of sellers 4. fall in return in alternative

uses of inputs 5. or, . . .

Fall ‘ 97 Principles of Microeconomics

slide 37

10 20 30 40 50 60 70 80 90 100 110 120 130

10

20304050

60

708090

100

Px

Qx/ UT

Demand

Supp

ly

6 0

$70

A decrease in supply

decrease in supply

S1

price rises

$90

quantitydecreases

35

causes the equilibrium price to increaseand equilibrium quantity to decrease. What forces might cause the

supply to decrease?1. an increase in the prices

of inputs2. increase in returns from

alternative actions3. problems in technology [regulations, . . . ]4. decrease in number of sellers or producers

Fall ‘ 97 Principles of Microeconomics

slide 38

Qx/ UT10 20 30 40 50 60 70 80 90 100 110 120 130

10

20304050

60

708090

100Px

When demand and supply both shift, the resultant effect on eitherequilibrium price or quantity will be indeterminate.

DemandSu

pply

6 0

$70

demandincreases

D2results ina market force to increase Q

and increase price

supplyincreases

S2

results ina market force to increase Q

and decrease price

Both the increase in demand and supply increase quantity;

increase

increase

100

equilibrium Q increases.

The increase in demand pushes price up.

+∆P

The increase in supply pushes price down.

price mightgo up or downor stay the same -∆P

The change in price may be positive or negative, it depends on the magnitude of the shifts in and slopes of demand and supply.

If both supply and demand decrease,the ∆P will be indeterminate and the equilibrium Q will decrease.

Fall ‘ 97 Principles of Microeconomics

slide 39

10 20 30 40 50 60 70 80 90 100 110 120

10

20304050

60

708090

100

Qx/ UT

Demand

Supp

ly60

$70

Price

A decrease in supply

decrease in supplyS1

pushesprice up

reducesquantity

35

tends to increase P and reduce Q.

An increase in demand

an increase indemand tends D2

to pushprice up

and increaseQ

tends to increase both P and Q.Result is that Price will rise, Quantity may increase, decrease or stay the samedepending on the magnitudes of the shifts and slopes of supply and demand.

In this example,the price increases to$105.

$105

49the quantity decreases to 49

When supplyincreases anddemand decreases,the price willfall but thechange in Q will beindeterminate!

Fall ‘ 97 Principles of Microeconomics

slide 40

Supply and Demand Analysis· Supply and demand is a simplistic model that

provides insights into the effects of events that are related to a specific market.

· Whether an event will tend to cause the price of a good to increase or decrease is of importance to decision makers.

· To estimate the magnitude of price and quantity changes more sophisticated models are needed.

![Tic Normal Sup Informe Final[1]](https://static.fdocuments.net/doc/165x107/5563443fd8b42a5c7b8b552e/tic-normal-sup-informe-final1.jpg)