CURRENT PATTERNS AND TRENDS IN STATE AND … · the number of states which tax intangible unless...

12

CURRENT PATTERNS AND TRENDS IN STATE AND LOCAL INTANGIBLES TAXATION** JOHN H. BOWMAN,* GEORGE E. HOFFER,* AND MICHAEL D. PRA@TT* ABSTRACT that emerged in the nineteenth century This paper presents findings from the included both tangible and intangible first broad survey of intangibles taxation personal property, as well as real prop- in a quarter-century. It provides more erty. Not long after adopting this very consistent information on intangibles tax- general form of property taxation, how- ation and more complete revenue data than ever, states began to provide for excep- previously existed. Almost all recent sub- tions. For decades, the personal property stantial changes continue the long-term share of the property tax base has dwin- decline of intangibles taxation. Twenty-two dled consistently and substantially. From states still have some intangibles taxation, 1956 to 1986, for example, Census Bu- but in only five does it account for more reau data show that personal property than one percent of state and local taxes. dropped from 25.5 percent to 15.4 percent Three states, however, recently expanded of the property tax base. Thus, personal their intangibles taxes; others had 1990 property comprises a minor component of legislative proposals to do so, and still oth- the property tax base, and intangible ers nwy consider this IZawed source to help property is only a small fraction of all close budgetary gaps. personal property.' The following sum- mary suggests some basic reasons. Both the theoretical dissatisfaction with the tax and I. Introduction its administrative weakness led to a movement among the states for special treatment of intangibles. The HIS paper reviews the current state development has taken two broad approaches: the Tof the taxation of intangible personal adoption of a partial or comprehensive system of clas- property in the United States. It is the first sifying property under which intangibles are taxed at a special low rate based either on their income or their broad survey of this tax since Blackburt@s value; and the exemption of intangibles from the (1965) survey in the Journal a quarter of property tax and the taxation of income resulting from a century ago. Following significant their ownership under general income tax laws.' change in this field, it is important to as- The long-term trend to remove intan- sess current practice. gibles from the tax base experienced re- Over the current century, the once- newed vigor in the 1980s. In the last de- dominant position of property taxation in cade, 11 states have repealed or limited state and local tax structures has eroded. the taxation of intangibles. Several fac- Relative decline of the property tax has tors help explain this acceleration. First, resulted chiefly from revenue diversifi- several adverse court decisions have ad- cation, especially by state governments, dressed inconsistencies in definitions of but narrowing of the base of the property intangible personal property. For in- tax also has played a part. For state gov- stance, several states taxed the equities ernments, sales and income taxes now of domestically (state) chartered and for- dominate, and property taxation is quite eign chartered corporations differently. insignificant. Local revenue diversifica- Successful court challenges of such incon- tion also has occurred, but to a much lesser sistencies have been mounted under the extent, and on average, property taxation e clause of the U.S. Constitution. still accounts for nearly three-fourths of commerc local government taxes (Census, 1985, Several states' legislatures have chosen 1990). repeal of their intangibles statutes over The general, ad valorem property tax amending them to conform with court de- cisions. *Virginia Commonwealth University, Richmond, VA Another factor is the continual problem 32384. of enforcement. Identification and valua- 439

Transcript of CURRENT PATTERNS AND TRENDS IN STATE AND … · the number of states which tax intangible unless...

CURRENT PATTERNS AND TRENDS IN STATE AND LOCALINTANGIBLES TAXATION**

JOHN H. BOWMAN,* GEORGE E. HOFFER,* AND MICHAEL D. PRA@TT*

ABSTRACT that emerged in the nineteenth century

This paper presents findings from theincluded both tangible and intangible

first broad survey of intangibles taxation personal property, as well as real prop-

in a quarter-century. It provides moreerty. Not long after adopting this very

consistent information on intangibles tax-general form of property taxation, how-

ation and more complete revenue data than ever, states began to provide for excep-

previously existed. Almost all recent sub-tions. For decades, the personal property

stantial changes continue the long-termshare of the property tax base has dwin-

decline of intangibles taxation. Twenty-twodled consistently and substantially. From

states still have some intangibles taxation, 1956 to 1986, for example, Census Bu-

but in only five does it account for morereau data show that personal property

than one percent of state and local taxes. dropped from 25.5 percent to 15.4 percent

Three states, however, recently expandedof the property tax base. Thus, personal

their intangibles taxes; others had 1990 property comprises a minor component of

legislative proposals to do so, and still oth-the property tax base, and intangible

ers nwy consider this IZawed source to helpproperty is only a small fraction of all

close budgetary gaps.personal property.' The following sum-mary suggests some basic reasons.

Both the theoretical dissatisfaction with the tax andI. Introduction its administrative weakness led to a movement among

the states for special treatment of intangibles. TheHIS paper reviews the current state development has taken two broad approaches: the

Tof the taxation of intangible personal adoption of a partial or comprehensive system of clas-property in the United States. It is the first sifying property under which intangibles are taxed at

a special low rate based either on their income or theirbroad survey of this tax since Blackburt@s value; and the exemption of intangibles from the(1965) survey in the Journal a quarter of property tax and the taxation of income resulting froma century ago. Following significant their ownership under general income tax laws.'change in this field, it is important to as-

The long-term trend to remove intan-sess current practice.gibles from the tax base experienced re-Over the current century, the once-newed vigor in the 1980s. In the last de-dominant position of property taxation in cade, 11 states have repealed or limitedstate and local tax structures has eroded.the taxation of intangibles. Several fac-Relative decline of the property tax hastors help explain this acceleration. First,resulted chiefly from revenue diversifi-several adverse court decisions have ad-cation, especially by state governments,dressed inconsistencies in definitions ofbut narrowing of the base of the propertyintangible personal property. For in-tax also has played a part. For state gov-stance, several states taxed the equitiesernments, sales and income taxes nowof domestically (state) chartered and for-dominate, and property taxation is quiteeign chartered corporations differently.insignificant. Local revenue diversifica-Successful court challenges of such incon-tion also has occurred, but to a much lessersistencies have been mounted under theextent, and on average, property taxation

e clause of the U.S. Constitution.still accounts for nearly three-fourths of commerclocal government taxes (Census, 1985, Several states' legislatures have chosen

1990). repeal of their intangibles statutes over

The general, ad valorem property tax amending them to conform with court de-cisions.

*Virginia Commonwealth University, Richmond, VA Another factor is the continual problem32384. of enforcement. Identification and valua-

439

440 NATIONAL TA)C JOURNAL' [Vol. XLIII

tion of intangibles always has been the tained from all 50 states and the District"Achilles heel" of tax administration for of Columbia.intangible personal property. In addition, To make the survey manageable, it wasthe desire of states with broad income necessary to limit and define the types oftaxes to harmonize the taxation of income- taxes to be studied. We include propertyproducing intangibles and other sources taxes on intangible property, whether theof income may account for at least some base and rate provisions are the same asretrenchment on the intangibles-tax front. for the other types of property or appli-Ohio provides an example, and also illus- cable only to intangibles. We also includetrates that such harmonization may come special intangibles taxes levied as a per-slowly. Legislation in the mid-1980s re- centage of income yield, such as the Mich-pealed a separate five-percent levy on the igan tax on the income from income-yields of income-producing intangibles and producing intangible assets and the taxesbrought that income under the state's imposed on dividend and interest incomegeneral income tax. This finally effected by Connecticut, New Hampshire, anda change first attempted when the state Tennessee.

3income tax was adopted in 1971. Such "income" taxes are included hereWhile most changes have narrowed the because they apply only to intangible-

taxation of intangibles, Connecticut, source income, but not to wages and sal-Florida, and Tennessee recently moved in aries and other sources of income; thesethe opposite direction, and 1990 legisla- taxes clearly single out intangibles.' Be-tive bills proposed broader intangibles cause taxes on income and on asset val-taxation in Kansas and Louisiana.' Ex- ues can be equivalent, the exact form ofpanded intangibles taxation might seem tax used generally is not relevant. Assettempting to state and local governments value tends to be the present value of ex-grappling with budgetary pressures. Bet- pected future income, so an asset yieldingter knowledge of the status of and expe- $100 income per year would have a valuerience with intangibles taxation is impor- of $1,000, if the interest rate is 10 per-tant for evaluation of both recent and cent. This asset could be taxed to yield $5prospective changes in such taxes. of revenue per year either by taxing the

income at five percent or by taxing the

11. Scope and Method capital value at five mills. Taxes on theasset value of "unproductive" (non-in-

Information on patterns and trends in come-yielding) assets, which are levied inthe taxation of intangible property was some states, are exceptions to the equiv-obtained by surveying the 50 states and alence of income and property taxes, atthe District of Columbia. First, Com- least in the short run.merce Clearing House materiaIS5 were Although excluding some taxes that inused to develop a multi-page profile of the some way fall on intangible assets whileapparent current status of intangible including others requires drawing some-property taxation in each state. This in- what arbitrary distinctions, practicalityformation then was sent to the state, ask- requires such limitation. Our general cri-ing that it be reviewed and, as necessary, terion is to exclude broad, general taxes,corrected or expanded. This approach, aside from the property tax. Thus, we omitrather than sole reliance on a survey, was general income taxes, which are found inadopted for several reasons: to reduce the most states. With bases similar to federalburden placed on state propelly tax offi- income taxes, broad income taxes include6iiilg, t"i&-@ide greater u-n-if6rmity of in- iii6bm@ fr6ii@intangibl@s, b@@t-they includeformation, and to generate a broad re- most other sources of income, as well.sponse to the.survey. Each state also was Thus, they are not viewed as intangiblesasked to indicate recent developments in taxes, per se. Similarly, broad businessintangibles taxation and to provide an es- gross receipts taxes are excluded, eventimate of revenues from such taxes. With where receipts from dealing in intangibletelephone follow-up, responses were ob- assets are included explicitly (as in New

No. 41 PATTERNS AND TRENDS IN INTANGIBLES TAXATION 441

Mexico). Finally, some states impose taxes states, moreover, coverage of intangibleson the intangible property of public util- is so limited that it stretches the point toities and/or transportation companies say such taxation is part of a generalwhere such intangibles as goodwill and/ property tax. In 16 states intangibles areor the franchise value are incorporated in taxed under a special tax (Table 1). Thevaluation of the firms as a unit. Taxes of "special" label indicates that we are notthis type also ar.--excluded from this anal- able to categorize and summarize theseysis, even when they are property taxes, taxes conveniently. As detailed below,because they do not tax intangibles per these taxes vary substantially.se. Clearly, the two taxing groups overlap.

Three states tax intangibles under both

Ill. Taxation of Intangible Personalgeneral property taxes and special taxes

Property(Louisiana, Pennsylvania, and Tennes-see). Eight of the states with special in-

Beginning prior to World War II, there tangibles taxes are states in which intan-has been a consistent decline not only in gibles are taxable under the property taxthe number of states which tax intangible unless specifically exempted. Special in-property, but also in the coverage of the tangibles taxes are imposed after ex-tax. As detailed later, although 22 states empting intangibles from general prop-continue to have some taxation of intan- erty taxation (five states), or in additiongible property (Table 1), in only seven to the general property tax (four states).states do annual revenues from these taxes Generally, the intangibles tax is the le-exceed $50 million. gal responsibility of both individuals and

corporations (Table 1). In the few states

Overviewthat hold only corporations responsible forthe tax, typically the taxes are levied on

Although intangible personal property the deposits in financial institutions or ontaxes currently are levied in less than half the capital stock of certain firm types.the states, only four-Illinois, Nevada, Connecticut, Michigan, Missouri, and NewNew York, and South Carolina-have Hampshire are the only states to limit in-constitutional prohibitions against such tangibles taxes to individuals; in each, thetaxes (Table 1). Intangibles become sub- intangibles tax base is measured at leastject to taxation, other than through a predominantly by income yield rather thanbroad-based income or gross receipts tax, asset value.in one (or both) of two ways: (1) intangi-bles are included in the property tax base Tax Baseunless specifically exempted; and (2) onlyspecifically enumerated intangibles are As we enter the 1990s, only 22 statessubject to taxation. Taxes of the first sort or their subdivisions levy any tax on in-we consider to be part of general property tangibles, per se. The intangibles tax basetaxation, while those of the second sort are has diminished even more than this fig-termed "special" taxes. ure suggests, however, because in only 13

Table 1 sheds light on the general char- states are two or more intangible prop-acter of earlier property taxation and the erty types taxed by the state and/or itserosion of that generality. Under the laws localities. Typically the tax base is de-of 29 states, intangibles are taxable un- fined as some measure of value (17 states).less specifically exempted, but only 14 of However, five states define the base onlythose now tax intangibles. Only nine states in terms of income yield (Connecticut,tax intangibles as part of the general Kansas, Michigan, Missouri, and Northproperty tax. This overstates the situa- Dakota); two use both income and asset-tion, though, because each of these places value base measures (New Hampshire andintangibles in a property class that typi- Tennessee).cally is taxed at a lower effective rate than Table 2 lists the states with at leastmost other classes .7 In several of these some type of tax considered to be an in-

@442 NATIONALTAX JOURNAL, [Vol. -XLIII

Table 1. Selected Features of Intangibles Taxation by State

State Feature' State Feature'

Alabama T, L, G, 1, C Montana TAlaska T Nebraska TArizona T Nevada EArkansas T New Hampshire L, S, ICalifornia T New Jersey

Colorado T New MexicoConnecticut L, S, I New York EDelaware North Carolina T, L, S, I, CFlorida T, L, S, 1, C North Dakota L, S, 1, CGeorgia T, L, S, I, C Ohio L, S, C

Hawaii Oklahoma TIdaho Oregon TIllinois E Pennsylvania T, L, G, S, I, CIndiana T Rhode Island L, S, CIowa L, S, C South Carolina E

Kansas L, S, I, C South DakotaKentucky T, L, G, I, C Tennessee T, L, G, S, I, CLouisiana T, L, G, S, 1, C Texas L, S, 1, CMaine Utah TMaryland Vermont

Massachusetts T VirginiaMichigan T, L, S, I Washington T, L, G, 1, CMinnesota T West Virginia T, L, G, I, CMississippi T, L, G, C Wisconsin TMissouri T, L, S, I Wyoming T., L, G, 1, C

Dist. of Columbia T

1) Key to intangibles tax features (number of states for each]:E = Taxation prohibited by state constitution [4]T = Taxable under general property tax unless specifically exempt [29)L - Tax levied [22]G = Tax levied under general property tax [9]S = Tax levied under special tax provisions (16]1 = Tax levied on individuals [18)C = Tax levied on corporations (18]

Source: CommerceClearing House State Tax Reporter and survey by authors.

tangibles tax, as delineated above, and tax base are equities and bonds. Twelvesummarizes the types of property taxed. states include both, although in severalEight states tax at least six different types states the definition for equities is ex-of intangible property (Florida, Georgia, tremely narrow. New Hampshire, for in-Kansas, Kentucky, Michigan, New stance, permits localities to tax only theHampshire, Tennessee, and West Vir- stock of nationally chartered banks asginia). Most commonly in the intangibles property.

No. 41 PATTERNSAND TRENDS IN INTANGIBLESTAXATION 443

Table 2. Details of Intangibles Tax Base by State

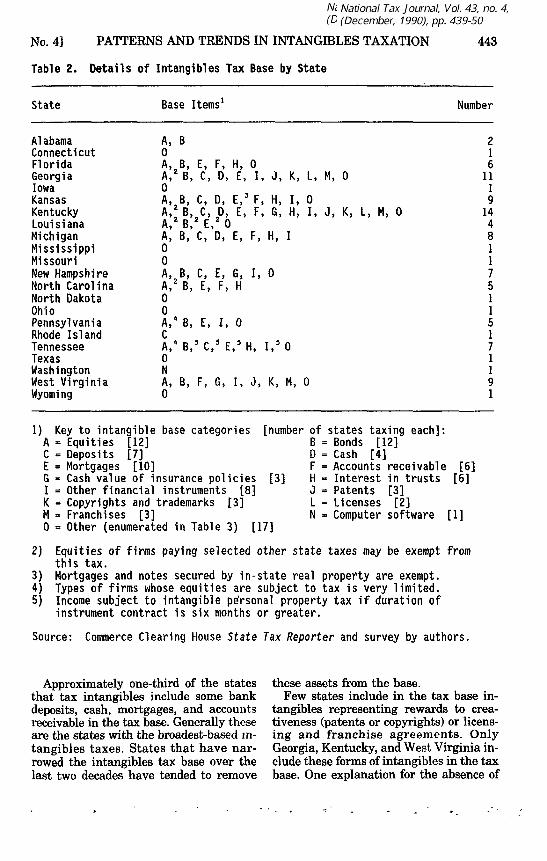

State Base Items' Number

Alabama A, B 2Connecticut 0 1Florida A B, E, F, H, 0 6Georgia A: B, C, D, E, I, J, K, L, M, 0 11Iowa 0 1Kansas iA, 8, C, D, E,' F, H, 1, 0 9Kentucky A: B C, D, E, F, G, H, I, J, K, L, M, 0 14Louisiana A 2 B: 2 E 2 0 4Michigan A, B, C, D, E, F, H, 1 8Mississippi 0 1Missouri 0 1New Hampshire A

28, C, E, G, 1, 0 7

North Carolina A: B, E, F, H 5North Dakota 0 1Ohio 0 1

4Pennsylvania A, B, E, 1, 0 5Rhode Island c 1

4 5 5Tennessee Al Bt C,5 E) Ht It5 0 7Texas 0 1Washington N IWest Virginia A, B, F, G, I, J, K, M, 0 9Wyoming 0 1

1) Key to intangible base categories [number of states taxing each]:A = Equities [12] B = Bonds [12]C = Deposits [7) 0 = Cash [4]E = Mortgages [10] F = Accounts receivable [6]G = Cash value of insurance policies [3] H = Interest in trusts (611 = Other financial instruments [8] J = Patents [3]K = Copyrights and trademarks [3) L = Licenses [2)M = Franchises [3] N = Computer software (1]0 = Other (enumerated in Table 3) [17]

2) Equities of firms paying selected other state taxes may be exempt fromthis tax.

3) Mortgages and notes secured by in-state real property are exempt.4) Types of firms whose equities are subject to tax is very limited.5) Income subject to intangible pdrsonal property tax if duration of

instrument contract is six months or greater.

Source: Commerce Clearing House State Tax Reporter and survey by authors.

Approximately one-third of the states these assets from the base.that tax intangibles include some bank Few states include in the tax base in-deposits, cash, mortgages, and accounts tangibles representing rewards to crea-receivable in the tax base. Generally these tiveness (patents or copyrights) or licens-are the states with the broadest-based in- ing and franchise agreements. Onlytangibles taxes. States that have nar- Georgia, Kentucky, and West Virginia in-rowed the intangibles tax base over the clude these forms of intangibles in the taxlast two decades have tended to remove base. One explanation for the absence of

444 NATIONAL TAX JOURNAL- [Vol. XLIII

licensing and franchise agreements from the 1980s. This group includes Iowa,the tax base is that these have grown in Massachusetts, North Carolina, and Rhodeprominence over a period in which the Island. Several other states, while nar-taxation of intangibles has been in de- rowing the tax base, also ended all statecline; to add these to the tax base would taxation of intangible property; Kansas,seem at odds with the overall direction of Mississippi, and Texas fall into this cat-intangibles taxation. The same can be said egory.of computer software. Only Washington Indiana, Virginia, and West Virginiataxes computer software as an intangible. enacted legislation under different cir-There, the Board of Tax Appeals ruled in cumstances with the intent to end all in-1989 that software-previously taxed as tangibles taxation within the state. Thetangible property-is intangible prop- Indiana legislature had enacted legisla-erty.' Although virtually all intangible tion to phase out intangibles taxation byproperty has been exempt from property 1996, but a successful court challenge oftaxation since 1931, Washington is a state the manner in which domestic and non-in which intangibles are taxable unless domestic firms were treated under the in-specifically exempt, and the 1931 ex- tangibles statutes led the legislature toempting legislation did not anticipate and repeal them retroactive to November 1988.list computer software. Virginia also de- Although under no such pressure, thefines computer software to be intangible Virginia General Assembly in 1984 re-property, but it does not tax intangibles. pealed the state tax on intangible prop-Many states, however, include commer- erty of 30 cents per $100 of market value.cially available ("canned") software in the Previously, this was a state tax, as intan-tangible property base. gible property in Virginia is reserved for

A number of intangibles-tax states have state taxation only.9some unusual levies that we assign to the The status of intangibles taxation cur-"other" category in Table 2. For these, the rently is unsettled in West Virginia. Intax base tends to be quite narrow (Table 1984, the legislature scheduled repeal of3). For instance, Missouri taxes the in- the property tax on intangibles to coin-tangible property yields of estates (in fis- cide with the reappraisal of real propertycal 1989 no revenue was collected under in the state. The reappraisal was com-this levy), Florida taxes as intangibles the pleted in 1985, but the legislature so farleaseholds on government-owned prop- has refused to ratify this reappraisal, thuserty leased to the private sector, and Ohio keeping intangibles taxation in effect.taxes the capital stock of all Ohio dealers Ohio, while not completely repealing itsin intangibles. intangibles taxes, gave up the greatest

revenue of any state in the 1980s. Overseveral years during the mid-1980s, Ohio

Recent Developments changed from broad-based taxation of in-tangibles to a much narrower tax base.

As noted, the 1980s was a decade of sig- Until 1984, the state taxed the deposits,nificant activity in intangibles taxation. shares, and capital of all financial insti-Fourteen states made significant changes, tutions. Also, unincorporated businesses,and all but three either repealed or lim- non-financial institutions, public utili-ited the extent of such taxation (Table 4). ties, and individuals paid an intangi@les(Washington joined the ranks of intangi- tax on a broadly defined group of intan-bles-tax states but, as noted, this simply gibles including financial deposits, cred-reflected a ne W- label for an old -tax.) its, moiley, stoclw, bonds, nmtgages, landChanges of particular note are discussed contracts, annuities, royalties from pat-below. ents, and other intangible property. Since

The vast majority of states which re- 1986, only a statewide uniform tax on thepealed or narrowed the intangibles tax capital of dealers in intangibles remains.base merely continued a trend predating This 8-mill tax (increased from six mills

No. 41 PATTERNS AND TRENDS IN INTANGIBLES TAXATION 445

Table 3. "Othern intangibles Subject to Taxation, by State

Connecticut: All dividend and interest income taxable when federal AGI >$54,000; also capital gains thereon

Florida: (a) Leasehold estate on government-owned property but leased to theprivate sector; (b) shares in limited partnerships which are publicly traded

Georgia: Loans secured by collateral (in addition to mortgages)

Iowa: Legal and special reserves of credit unions only

Kansas: An annual levy not to exceed 3 percent of the annual income fromselected intangibles

Kentucky: Retirement and annuity account

Louisiana: (a) Loan and finance company credit assessment based on unsecuredloan value anywhere and on loans secured by non-Louisiana property; (b)property and casualty insurance company credit assessment based on premiumswritten in Louisiana

Mississippi: Cash and selected debt instruments of banks subject to tax

Missouri: (a) Intangible income of estates; (b) dividends of farmers'cooperative credit associations

New Hampshire: (a) Income from some intangibles subject to NH state incometax; (b) stocks of national banks taxed as property by localities

North Dakota: Gross receipts from musical or dramatic compositions

Ohio: On capital stock of all Ohio dealers in intangibles

Pennsylvania: Corporate loans tax on interest paid by firms with a treasurerresident in the state

Tennessee: (a) State corp franchise tax on apportioned capital stock andsurplus; (b) selected dividend and interest income taxable subject to $1,250exemption per tax filer

Texas: (a) Intangible property of unincorporated banks; (b) apportioned valueof intangibles of certain transportation businesses, insurance companies, andfinancial institutions

West Virginia: Annuities, endowments

Wyoming: Water and reservoir rights

Source: CommerceClearing House State Tax Reporter and survey by authors.

in 1987) is divided 3/8 to the state and Estimated Revenues from the Taxation of5/8 to the localities. In fiscal 1989, gross Intangiblesrevenue from intangibles taxation was$13.4 million, compared to approximately Available information places total an-$269 million in 1981. nual intangibles tax revenues in the late

446 NATIONAL TAX-JOURNAL' [Vol. XLIII

Table 4. States with Major Intangibles Tax Changes, 1980 - 1990

State Date Nature of change

Connecticut 1990 Extended tax to nonresidentsFlorida 1990 Broadened base, increased rateIndiana 1989 RepealedIowa 1985 Virtually repealedKansas 1982 Repealed at state levelMassachusetts 1988 Repealed, blanket exemptionMississippi 1981, 1983 Repealed at state level ('81) and

for school districts ('83)North Carolina 1986 New limits imposedOhio 1983-87 Tax on most intangible property repealed;

rate increased for remaining tax ondealers in intangibles (1987)

Rhode Island 1988 Repealed on net worth of corporationTennessee 1986 Broadened baseTexas 1985 New limits imposedVirginia 1984 RepealedWashington 1989 Computer software ruled to be intangible

and, since not specific:lly exempted bystatute, is taxable as uch'

West Virginia ? Repealed by 1984 law, once reappraisal hasbeen ratified by General Assembly-2

1) Previously taxed as tangible property2) As of September 1990, the 1985 reappraisal has not been ratified

Source: Commerce Clearing House State Tax Reporter and survey by authors.

1980s (generally fiscal 1989) at nearly $1.5 Virginia) accounted for 83 percent of thebillion, with state revenues more than local total.three times those of localities (Table 5, Table 5 also relates revenues from com-columns 1-3). While 13 states taxing in- bined state and local intanfibles taxes totangible property at the state level re- total state and local taxes to show theported annual revenues totaling over $1.1 relative importance of the intangibles taxbillion, two states, Connecticut and Flor- in the late 1980s and, where possible, inida, accounted for 69 per cent of the to- the early 1960s. In the later period, fortal.10 each of the 21 states reporting intangi-

Fifteen states also were able to report bles revenue data, intangibles taxes ac-revenues generated by the local taxation counted for a small portion of total taxof intangibles. As with state-level taxa- revenue (column 4)-one-half percent ortion, the bulk of the local revenues were less in 14, and less than one percent inconcentrated in a few states. Although 15 all but five (Connecticut, Florida, Ken-states -r@o;ited total annual 166a-!*reve- t , New- Ham@sVirci, an(i Tbiiiiess-ee).nues of $315 million, 45 per cent of the Of these five, all but one (Kentucky) haverevenues were generated in two states, no broad-based income tax, but three ofNorth Carolina and Pennsylvania, and six the remaining four (all but Florida) taxstates (Georgia, Louisiana, North Caro- dividend and interest income.lina, Pennsylvania, Tennessee, and West The 1963 survey (Blackburn, 1965) re-

No. 41 PATTERNS AND TRENDS IN INTANGIBLES TAXATION 447

Table 5. Estimated Annuil Intangibles Taxation Revenue by State and by Levelof Government in Late 1980s and Revenue Significance, Late 1980s' and 1963 2

Tax in Late 1980s (Millions) Total As Percent of Allby Level of Government - State and Local Taxes

State State Local Total Late J,94QS 19-63(1) (2) (3) (4) (5)

Alabama 3 $ 2.2 $ 15.3 $ 17.5 .2190/.Connect@cut 384.9 384.9 4.146Florida 402.9 402.9 1.425 2.014%Georgia 24.0 24.0 .170Iowa 0.5 0.5 1.0 .015Kansas 9.9 9.9 .166Kentuckyr' 77.1 4.3 81.4 1.126Louisiana 24.0 24.0 .253Michigan 118.0 118.0 .489Mississippi 0.2 0.2 .004Missouri 0.0 0.0 .000 .696New Hampshire 36.2 10.8 47.0 2.127North Caroliga 84.9 84.9 .654 1.783NortD Dakota 0.1 0.1 .007Ohio 5.1 8.3 13.4 .057 1.868Pennsylvania 8.6 56.6 65.2 .246Rhode Island 8.0 8.0 .325Tennessee 95.5 42.0 137.5 1.540 2.092Texas 0.1 0.1 .000Washington 1.4 4.2 5.6 .049West Virginia 30.0 30.0 .908 1.638Wyoming NA NA NA NA

TOTALS $1,140.5 $315.1 $1,455.7

l@ Data for latestb@ear available (1987, 1988, or1989)

gusually FY 1989.2 1963 data are ( ackburn, 1965) and (Census Bureau, 1 85, Table 24).3 Residents gain lifetime exemption from the intangibles tax on non-Alabama

securities by paying a one-time registration fee of $ 25 per $100 parvalue; estimated $1 million annual revenue from this iee is included here.

4) In Florida, of the $402.9 million in revenues, $289.7 million wasgenerated by the annual tax and $113.2 million by a nonrecurring tax.

5) While the monies and credits tax on the reserves of credit unions islocally administered, 501/.of the receipts go to the Iowa General Fund.

6) Varied local tax rates preclude an exact estimate of annual local revenue.In FY 1988, rates ranged from $.19 to $.38 per $100 of assessed value1[$2.27 billion). If all bank shares were taxed at the minimum, localitieswould have collected $4.3 million; this lower-bound estimate is used here.

7 Missouri reports zero revenue from each of two intangibles taxes in 1989.Only two firms pay the North Dakota copyright tax, so exact revenues couldnot be released. However, annual total collections are under $100,000.9)State tax in Ohio is shared with local governments, as shown here.

Ported intangibles revenue data for six of the late 1980s in each of these six statesthe states in Table 5 (Florida, Missouri, (columns 4 and 5). In the earlier period,North Carolina, Ohio, Tennessee, and five of these derived from 1.6 to 2.1 per-West Virginia). The relative importance cent of state and local tax revenue fromof intangibles taxes already was small by intangibles taxes; however, none of the fivethe early 1960s, but it declined further by obtained more than 1.5 percent from this

448 NATIONAL TAX 4OURNAL [Vol. XLIII

source in the late 1980s. The sixth state gible instruments. Finally, simplicity suf-with data for both years, Missouri (where fers when intangible property is taxed. Thethe intangibles base is very selective), de- potential for significant tax evasion ne-rived 0.7 percent of state and local tax cessitates incurring relatively high ad-revenue from intangibles in the early ministrative costs to assure reasonable1960s, but reports zero revenue for the levels of tax compliance. Moreover, manylater period. forms of intangibles are difficult to value.

Thus, a key policy concern is that many

IV. Summary and Conclusion intangibles represent tangible (real orpersonal) properties that are in the tax

With few exceptions, developments of base. Separate taxation of such intangi-the last quarter-century have continued bles results in double taxation. The samethe secular decline in intangibles taxa- issue is presented, however, by the si-tion. Nonetheless, three states have multaneous existence of property taxes onbroadened their intangibles tax bases and income-producing assets and income taxesa few have increased their rates. Recent on the incomes generated by those assets.legislative bills in a few other states have In general, such double taxation seemssought to expand intangibles taxes, and least objectionable when the paired taxes-more states no doubt will be tempted by (1) on the asset values of tangible prop-this revenue source (among others) as erty and of representative intangibles, orbudgets grow tighter. Should the long-term (2) on the asset values and the incomedecline of this tax continue, or should leg- flows from those assets-are levied byislators rediscover intangibles as a viable different government units, both of whichtax source? provide services to the taxpayers said to

In general, public finance economists be double-taxed." But true double taxa-favor broad tax bases over narrow bases. tion diminishes both equity and effi-Often, broad-based taxes are supported by ciency.both major tax criteria-efficiency (both To the extent that intangible values areneutrality and ease of administration and not reflected in values of tangible prop-compliance) and equity. Evaluation erty or in taxable income flows under in-against these criteria suggests, however, come taxes, however, a separate levy onthat a property tax including intangibles intangibles is appropriate. Such gaps inin the base may not be preferable to one coverage seem less likely for broad in-exempting intangibles. come taxes than for property taxes. Broad

Several considerations suggest exclud- use of state (and even local) income tax-ing intangibles from the tax base. First, ation, therefore, diminishes the case forincluding intangibles in the property tax separate taxation of intangible assets, es-base in many instances is inequitable be- pecially at the state level.cause it effectively double-taxes the same Recent patterns and trends of intangi-asset. For example, mortgages and cor- bles taxation generally are consistent withporate stocks are paper claims to tangible minimizing double taxation. Three of theassets that also are part of the property states narrowing intangibles taxation intax base. Also, many forms of intangible the last decade are among the most re-property rather easily can escape detec- cent adopters of personal income taxestion by assessors. Thus, a broad intangi- (Indiana in 1963, Ohio and Rhode Islandbles tax may engender evasion that is in 1971). And the three states broadeningsufficiewy widespread as to p:roa4ce se- intou *bles taxation have Q41v, narrow-rious horizonal inequity. Second, if double based personal income taxes (Connecticuttaxation results from including intangi- and Tennessee) or no personal income taxbles in the base, efficiency, as well as eq- (Florida). Moreover, four of the five statesuity, of property taxation is diminished. with the greatest reliance upon intangi-The resulting higher taxes create biases bles taxes (Connecticut, New Hampshire,against decisions, such as the corporate Florida, and Tennessee) have no broad-form of organization, that generate intan- based personal income tax. For three of

No. 4] PATTERNS AND TRENDS IN INTANGIBLES TAXATION 449

the four (all but Florida), it is the tax on broadened intangibles taxation in those states. Also,

dividend and interest income of individ- a 1989 Virginia law required a study of the equityand economic effects of the classification of personal

uals that produces their relatively high prpety and t.ati. of the classes at diff,@rentrates,intangibles tax reliance. All three of these including the zero rate on intangibleshave corporate income taxes, but their 5CommerceClearing House, State Tax Reporter,

relatively high-yielding intangibles taxes looseleaf service for each state (Chicago, Illinois:Conukigrce Cle@armg H(tW, coptinuqkisly-upd4ted).

do not apply to cbrporatf-dns. 61t is a bit of an overstatement to say that all threeThere is, however, some overlapping. Of states' income taxes apply only to intangible-source

the other two states in the top five, Flor- income; Connecticut also taxes gains from the sale of

er- capital assets using the same capital gains base asida has a corporate income tax but no p the federal income tax (ACIR, 1990, p. 52).sonal income tax while Kentucky has both 'Wyoming is an exception in that intangibles arepersonal and corporate income taxes. Both part of Class 3 which, under classification adopted inFlorida and Kentucky have relatively 1988, encompasses most property, including residen-

broad intangibles tax bases applicable to tial d agricultural real estate.8Ruthe Ridder v. WashirWton Mutual Savings Bank,

both individuals and corporations. Docket No 33595, February 10, 1989.As for future changes, states seeking 9In 1989, out of concern for disparity in the mamer

additional revenue generally should look in which different types of property are taxed, the

to other sources. The decline in the role General Assembly directed the Department of Taxa-tion to study the equity and economic impact of per-

of intangibles taxation has not been with- sonal property clawification and the (bfferential taxesout reason. imposed upon the various classes, including intangi-

bles."The Connecticut levy is a tax on dividend and in-

ENDNOTES terest income, and on the federal capital gains base,of individuals reporting federal a4justed gross in-

**We gratefully acknowledge our debts to the Fed_ comes over $54,000. The tax on capital gains is in-

eration of Tax Administrators for encouragement and cluded in the revenue figure given here.assistance in connection with the survey reported here, "Fiscal 1988 is the latest period for which aggre-

to the state tax officials who responded to the survey, gate state and local tax collections are available on acomparable basis for each state (Census Bureau, 1990,and to two anonymous reviewers and the editor of this Table 17). This should produce some overstatement of

Journal, whose comments have improved the paper. the importance of intangibles taxes, since most of theIn addition, comments by Arthur D. Lynn, Jr., were intangibles revenue data are for fiscal 1989. Simi-esvecially beneficial.ly larly, 1963 intangibles revenue are related to 1962Thiis counts all state-assessed property (large total state and local tax revenues because 1963 datapublic

utility property) as personal property, which is are not readily available (Census Bureau, 1985, Ta-a bit of an overstatement but the data needed to de- ble 24).termine the@personal sha@ are not available. Intan- 12 Indeed, in such circumstances, it does not seemgible property accounts f6r a very small percentage of meaningful to talk of "double taxation" even if eachtotal personal property value in these numbers (less governmental unit uses exactly the same form of taxthan 0.02 percent) partly because only three of the on the same base.states still taxing intangible property reported as- 13 Careful consideration of the relative defensibilitysessed values for such property (Census Bureau, 1989, of intangibles taxes in different situation is providedTables A and 14. by Groves (1967).'Milton C. Taylor, "Taxation of Intangible PersonalProperty in Michigan," in Michigan Tax Study StaffPapers, Harvey E. Brazer, ed (Lansing, Michigan:State of Michigan, 1958), p. 394. SELECTED BIBLIOGRAPHY

'A major complicating factor was the intangiblestax earmarking and, thus, the need to fashion an ac- Advisory Commission on Intergovernmental Rela-ceptable state aid for local revenue replacment (Ko- tions. Significant Features of Fiscal Federalism,sydar and Bowman, 1972, pp. 388-89). Volume 1, Budget Processes and Tax Systems, Re-

'Effective January 1, 1986, Tennessee broadened port M-169 Washington, D.C.: Government Print-the intangibles tax base to include the dividends on ing Office, 1990all equities except those of financial institutions. Pre- Aronson, J Richard. "Intangible Taxes-A Wiselyviously, the dividends on most Tennessee corpora- Neglected Revenue Source for States." National Taxtions were not subject to intangibles taxation. Con- Journal, 19 (June 1966): 194-86.necticut extended its capital gains tax realized from Blackburn, John 0. "Intangible Taxes-A Neglectedthe sale of in-state real estate to nonresidents effec- Revenue Source for States." National Tax Journal,tive with the 1990 tax year. Effective July 1, 1990, 18 (June 1965): 214-18.Florida brought publicly traded shares in limited Groves, Harold M. "Property Taxation of Intangi-partnerships into the intangibles tax base and in- bles." Property Taxation USA

,Richard W. Lind-

creased the tax rate. Legislation introduced in 1990 holm, ed. Madison, Wisconsin: University of Wis-in the Kansas and Louisiana legislatures would have consin Press, 1967, pp. 117-30.

450 NATIONAL TAX JOURNAL [Vol. XLIII

"Intangible Personal Property Tax." Final Report of Book ofreadings, Harold M. Groves, ed. New York,the Pennsylvania Tax Commission. Harrisburg, New York: Henry Holt and Co., 1947, pp. 58-65.Pennsylvama: Pemisylvania Tax Comniission, 1981, Sanders, Joe C. "A Defense of Personal Property Tax-pp. 28-35. ation." The Property Tax: Problems and Potentials.

"Intangible Personal Property Tax." StaffReport, The Princeton, New Jersey: Tax Institute of America,State and Local Tax Structure of Ohio, Frederick D. 1967, pp. 331-41.Stocker, ed. Columbus, Ohio: Ohio Tax Study Com- Stohlgren, Kurt. "The Nature and Taxability of Com-mission, 1967, pp. 180-90. puter Software." Washburn Law Journal, 22 (Fall

Jaffee, Bruce L. "The Indiana Intangibles Tax: The 1982):103-19.Tax Nobody Pays?" Indiana Business Review (July- Taylor, Milton C. "Taxation of Intangible PersonalAugust 1973): 3-7. Property in Michigan." Michigan Tax Study Staff

Jaffee, Bruce L. "State Taxation of Intangibles: The Papers, Harvey E. Brazer, ed. Lansing, Michigan:Problem of Evasion." Public Finance Quarterly, 6 State of Michigan, 1958, pp. 393-413.(October 1978): 485-502. Tunick, David C. and Schechter, Dan S. "State Tax-

Kosydar, Robert J. and Bowman, John H. "Moderni- ation of Computer Programs; Tangible or Intangi-zation of State Tax Systems: The Ohio Experience." ble?" Taxes--The Tax Magazine (January 1985): 54-National Tax Journal, 25 (September 1972): 379- 77.90. U.S. Bureau of the Census. Government Finances in

Lynn, Arthur D. "Trends in Taxation of Personal 1987-1988. Washington, D.C.: Government Print-Property." The Property Tax: Problems and Poten- ing Office, 1990.tials. Princeton, New Jersey: Tax Institute of U.S. Bureau of the Census. @987 Census of Govern-America, 1967, pp. 321-30. ments, Volume 2, Taxable Property Values. Wash-

Menchik, Paul L. "The Intangibles Tax." Michigan's ington, D.C.: Government Printing Office, 1989.Fiscal and Economic Structure, Harvey E. Brazer U.S. Bureau of the Census 198'-' Census of Govern-and Deborah S. Laren, eds. Ann Arbor, Michigan: ments, Vol. 6, No. 4, Historical Statistics on Gov-University of Michigan Press, 1982, pp. 619-46. ernmental Finances and Employment. Washington,

Noonan, Albert W. "Improvements in Personal Prop- D.C.: Government Printing Office, 1985.erty Taxation." Viewpoints on Public Finance: A