NativeScript Developer Day Keynote - Todd Anglin & Burke Holland

Upload

bryant-anglinCategory

view

32download

1

College Cops Incorporated

Case Study

Bryant Anglin

Group MembersAustin Torrey

Callie Griner

Kelby Hughes

Dr. Hoyt

RMIN 5950

Spring 2014

Table of Contents1. Executive Summary………………………………………………………………………..42. Introduction…………………………………………………………………………………..63. Risk Identification and Valuation……………………………………………………8

3.1 Direct Property……………………………………………………………………………………83.1.1 Buildings……………………………………………………………………………………………………..83.1.2 Improvements and Betterments…………………………………………………………………113.1.3 Personal Property………………………………………………………………………………………12

3.2 Indirect Property……………………………………………………………………………….133.2.1 Business Interruption………………………………………………………………………………...133.2.2 Contingent Business Interruption……………………………………………………………….14

3.2.2.1 Recipient………………………………………………………………………………………………...143.2.2.2 Contributing……………………………………………………………………………………………15

3.2.3 Extra Expense……………………………………………………………………………………………153.2.4 Building Ordinance…………………………………………………………………………………….163.2.5 Leasehold Interest……………………………………………………………………………………..16

4. Liability……………………………………………………………………………………….174.1 Premises and Operations Liability………………………………………………………174.2 Products Liability………………………………………………………………………………184.3 Auto Liability……………………………………………………………………………………..194.4 Advertising Liability…………………………………………………………………………194.5 Employment Practices Liability…………………………………………………………194.6 Professional Liability…………………………………………………………………………224.7 Contractual Liability…………………………………………………………………………..22

4.7.1 Leases………………………………………………………………………………………………………224.7.2 Other Contracts…………………………………………………………………………………………23

5. Personal……………………………………………………………………………………….245.1 Workers Compensation…………………………………………………………………..…24 5.2 Business Continuation ………………………………………………………………………255.3 Employee Benefits……………………………………………………………………………..25

6. Crime…………………………………………………………………………………………..277. Other Business Risks……………………………………………………………………298. Risk Treatment…………………………………………………………………………….30

8.1 Retention…………………………………………………………………………………………..308.1.1 Retention Capability………………………………………………………………………………….308.1.2 Retention Options……………………………………………………………………………………..31

9. Insurance and Risk Financing………………………………………………………..329.1 Property Insurance…………………………………………………………………………….32

9.1.1 Direct Property………………………………………………………………………………………….329.1.2 Accounts Receivable…………………………………………………………………………………..339.1.3 Mobile Equipment……………………………………………………………………………………339.1.4 Leasehold Interest……………………………………………………………………………………..339.2 Liability Insurance…………………………………………………………………339.2.1 General Liability………………………………………………………………………………………33

2

9.2.2 Fire Legal Liability…………………………………………………………………………………..…349.2.3 Executive Liability……………………………………………………………………………………...349.2.4 Umbrella Policy………………………………………………………………………………………….34

9.3 Business Auto……………………………………………………………………………………359.4 Crime………………………………………………………………………………………………...35

9.4.1 Employee Dishonesty…………………………………………………………………………………369.4.2 Inside the Premises Theft Money and Securities………………………………………….369.4.3 Inside the Premises Robbery and Safe Burglary…………………………………………..369.4.4 Computer Fraud………………………………………………………………………………………...37

9.5 Workers Compensation and Employer’s Liability………………………………...379.6 Alternative Risk Financing………………………………………………………………….38

10. Loss Control……………………………………………………………………………….3910.1 Property…………………………………………………………………………………………..3910.2 Liability…………………………………………………………………………………………..39

10.2.1 Premises and Operations………………………………………………………………………..4010.2.2 Products Liability……………………………………………………………………………………4010.2.3 Auto Liability………………………………………………………………………………………….4110.2.4 Advertising Liability……………………………………………………………………………….4110.2.5 Employment Practices Liability……………………………………………………………….4110.2.6 Professional Liability……………………………………………………………………………….4210.2.7 Contractual Liability…………………………………………………………………………………42

10.3 Personal…………………………………………………………………………………………..4310.3.1 Workers Compensation……………………………………………………………………………4310.3.2 Business Continuation……………………………………………………………………………..45

10.4 Crime………………………………………………………………………………………………4511. Risk Management Policy Statement……………………………………………..4612. Program Organization………………………………………………………………..47

3

1. Executive Summary

College Cops Incorporated is a for-profit company that is not funded by the

government. College Cops Inc. duties are to protect faculty, students, and any person

on or around the college campus. The company also informs the people on and

around the campus of potential danger, and educates them on the proper techniques

of avoiding dangerous situations as well as what people should do if they are ever

caught in dangerous situations. College Cops Inc. has experienced tremendous

geographic growth in the past 40 years; however, the company’s risk management

and loss control policies have not grown or evolved along with the company. If

nothing is done about this, then this stagnation in policy will continue to cause

financial troubles for College Cops Incorporated, and could even lead to the

expiration of the company.

This report will lay out several recommendations and solutions to the

current problems that College Cops Inc. is facing. After a complete analysis of the

current risks and valuation of those risks, a risk treatment plan was developed to

help lower those risks. Finally, for risk administration there will be a suggested risk

management policy statement developed specifically for College Cops Inc. as well as

guidelines and suggestions for the future of administering the proposed risk

management program. College Cops Incorporated will be referred to as CCI

throughout the report.

Because of the situation that College Cops Inc. is currently facing, a large

magnitude of problems will arise if changes are not made to the company. Some

4

changes are very minor, but several sections of College Cops Inc. will require drastic

changes and/or the addition of certain policies. Although these changes may seem

difficult to implement, in the long run they will save College Cops Inc. a lot of loss.

For the betterment and survival of the company, an overall change in the risk

management program has to happen. These changes will need the full support of

the company and its employees. Without everyone on board, the new risk

management program will fail to successfully minimize losses for College Cops Inc.,

and the company will eventually succumb to its losses.

5

2. Introduction

CCI was established 40 years ago by Sullivan McGruff with the mission to

provide enhanced security services to university and college campuses across the

United States. Sullivan started the company because he was passionate about

protecting students; he felt that the protections used at the time were not sufficient.

He harnessed this passion and combined it with his experience as a campus police

officer to create the founding principles of the company. This original business plan

that Sullivan created for CCI was based on the idea that an aggressive approach to

protection is the best approach and that education is key to minimizing harm to

students. It should also be noted that Sullivan wanted CCI workforce to be

composed of former law enforcement officers and individuals with military

experience.

CCI currently offers crime prevention services, ticketing services, emergency

communication and explosive ordinance removal when necessary. The educational

aspect of the services specializes in alcohol/drug abuse education and prevention,

sexual health education and theft prevention. Because CCI offers both

prevention/protection and educational services, this really positions them as a

double threat in the private security service industry.

Sullivan’s founding principles along with the services CCI offers are what

made the first CCI contract with a school in Atlanta successful. This success allowed

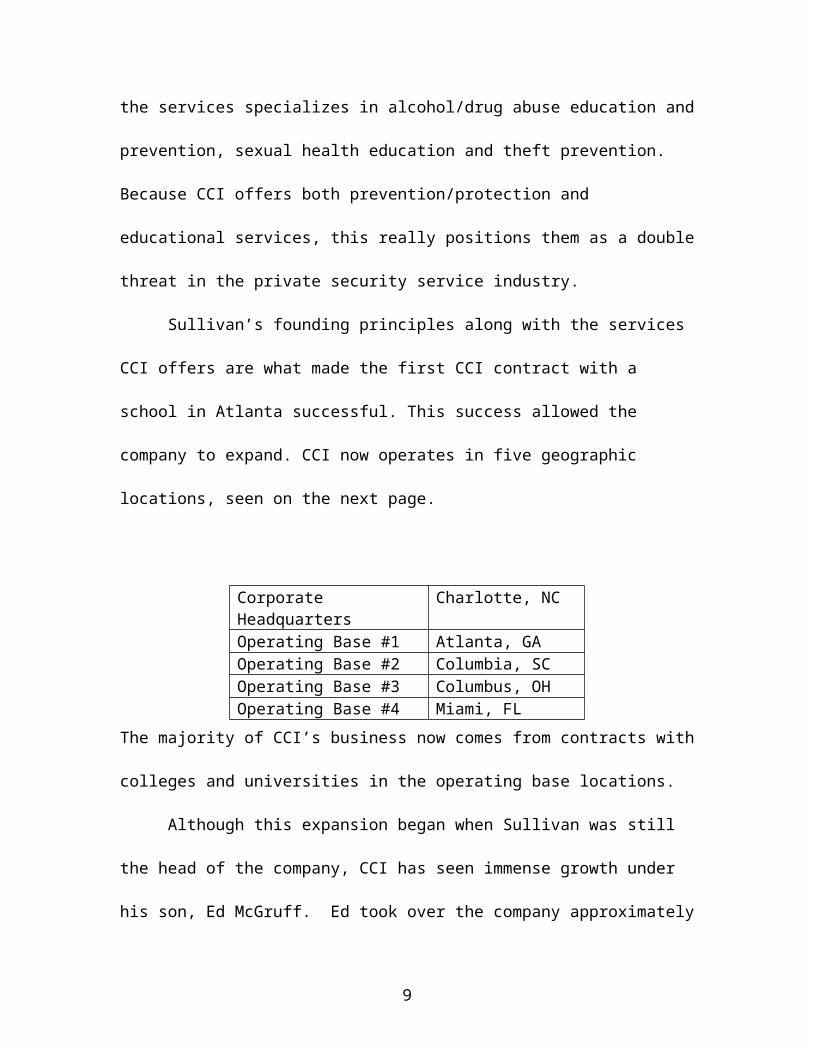

the company to expand. CCI now operates in five geographic locations, seen on the

next page.

6

The majority of CCI’s business now comes from contracts with colleges and

universities in the operating base locations.

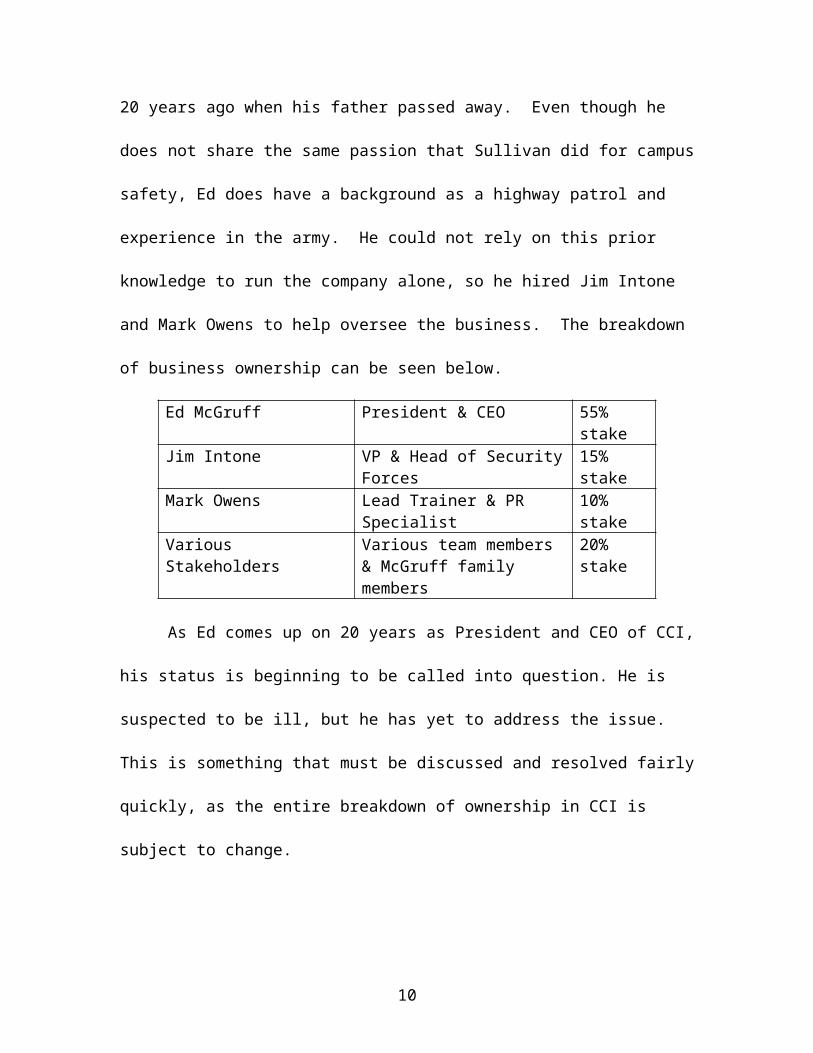

Although this expansion began when Sullivan was still the head of the

company, CCI has seen immense growth under his son, Ed McGruff. Ed took over

the company approximately 20 years ago when his father passed away. Even

though he does not share the same passion that Sullivan did for campus safety, Ed

does have a background as a highway patrol and experience in the army. He could

not rely on this prior knowledge to run the company alone, so he hired Jim Intone

and Mark Owens to help oversee the business. The breakdown of business

ownership can be seen below.

Ed McGruff President & CEO 55% stake

Jim Intone VP & Head of Security Forces 15% stake

Mark Owens Lead Trainer & PR Specialist 10% stake

Various Stakeholders Various team members & McGruff family members

20% stake

As Ed comes up on 20 years as President and CEO of CCI, his status is

beginning to be called into question. He is suspected to be ill, but he has yet to

address the issue. This is something that must be discussed and resolved fairly

quickly, as the entire breakdown of ownership in CCI is subject to change.

7

Corporate Headquarters Charlotte, NCOperating Base #1 Atlanta, GAOperating Base #2 Columbia, SCOperating Base #3 Columbus, OHOperating Base #4 Miami, FL

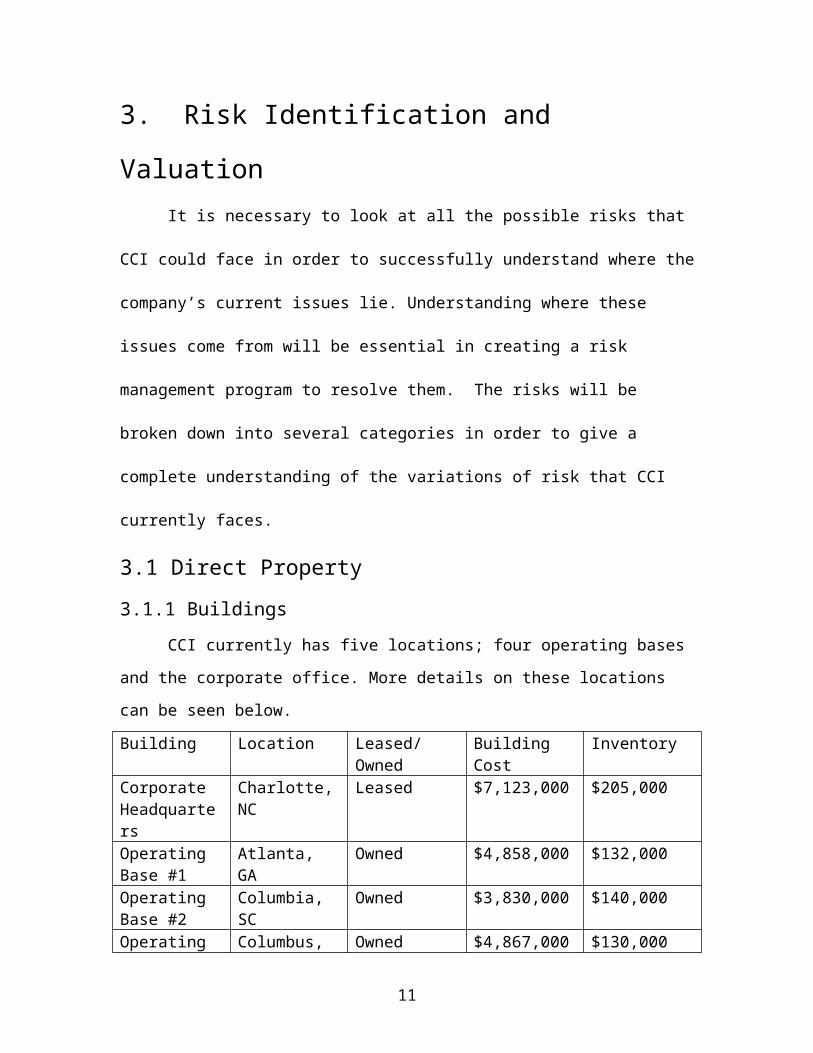

3. Risk Identification and ValuationIt is necessary to look at all the possible risks that CCI could face in order to

successfully understand where the company’s current issues lie. Understanding where

these issues come from will be essential in creating a risk management program to

resolve them. The risks will be broken down into several categories in order to give a

complete understanding of the variations of risk that CCI currently faces.

3.1 Direct Property

3.1.1 Buildings

CCI currently has five locations; four operating bases and the corporate

office. More details on these locations can be seen below.

Building Location Leased/Owned Building Cost InventoryCorporate Headquarters

Charlotte, NC Leased $7,123,000 $205,000

Operating Base #1

Atlanta, GA Owned $4,858,000 $132,000

Operating Base #2

Columbia, SC Owned $3,830,000 $140,000

Operating Base #3

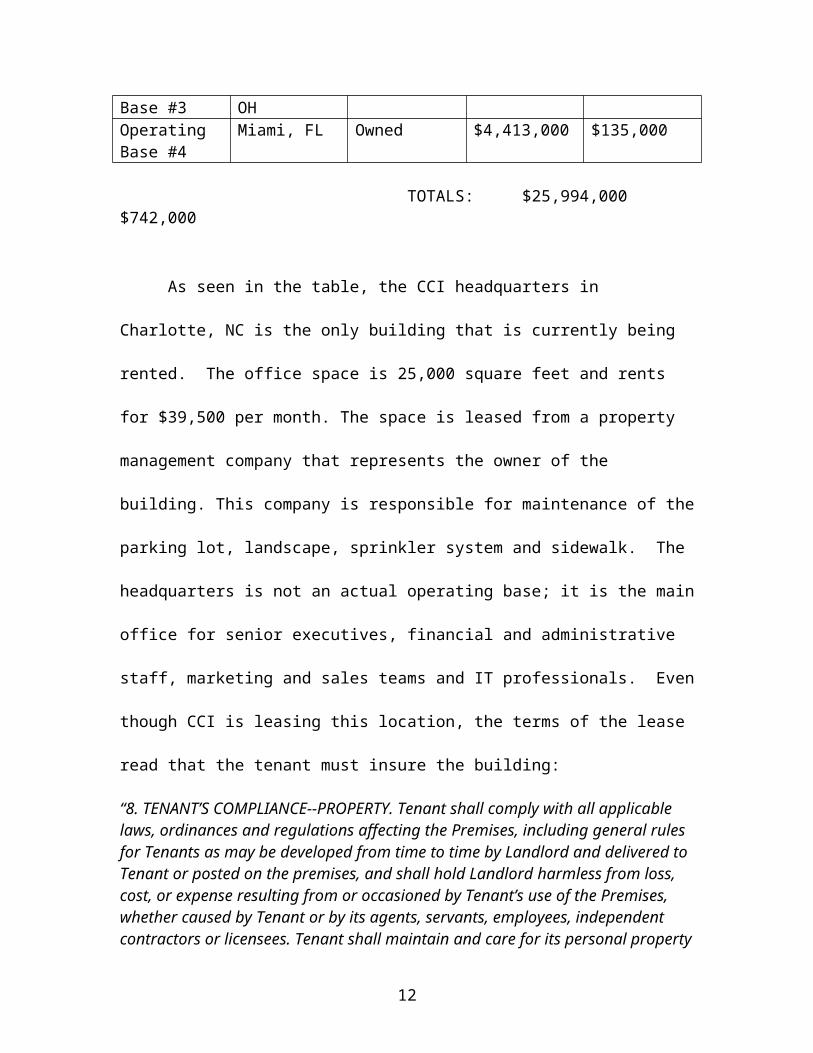

Columbus, OH Owned $4,867,000 $130,000

Operating Base #4

Miami, FL Owned $4,413,000 $135,000

TOTALS: $25,994,000 $742,000

As seen in the table, the CCI headquarters in Charlotte, NC is the only building

that is currently being rented. The office space is 25,000 square feet and rents for

$39,500 per month. The space is leased from a property management company that

represents the owner of the building. This company is responsible for maintenance

of the parking lot, landscape, sprinkler system and sidewalk. The headquarters is

not an actual operating base; it is the main office for senior executives, financial and

8

administrative staff, marketing and sales teams and IT professionals. Even though

CCI is leasing this location, the terms of the lease read that the tenant must insure the

building:

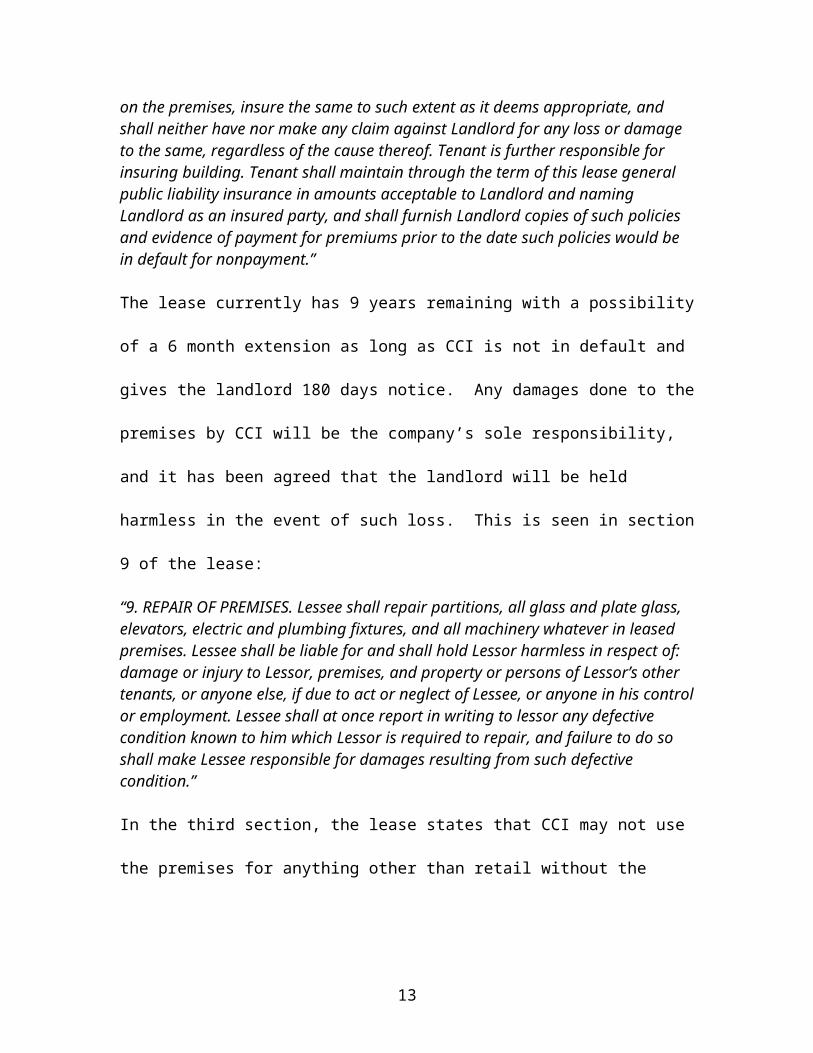

“8. TENANT’S COMPLIANCE--PROPERTY. Tenant shall comply with all applicable laws, ordinances and regulations affecting the Premises, including general rules for Tenants as may be developed from time to time by Landlord and delivered to Tenant or posted on the premises, and shall hold Landlord harmless from loss, cost, or expense resulting from or occasioned by Tenant’s use of the Premises, whether caused by Tenant or by its agents, servants, employees, independent contractors or licensees. Tenant shall maintain and care for its personal property on the premises, insure the same to such extent as it deems appropriate, and shall neither have nor make any claim against Landlord for any loss or damage to the same, regardless of the cause thereof. Tenant is further responsible for insuring building. Tenant shall maintain through the term of this lease general public liability insurance in amounts acceptable to Landlord and naming Landlord as an insured party, and shall furnish Landlord copies of such policies and evidence of payment for premiums prior to the date such policies would be in default for nonpayment.”

The lease currently has 9 years remaining with a possibility of a 6 month extension as

long as CCI is not in default and gives the landlord 180 days notice. Any damages done

to the premises by CCI will be the company’s sole responsibility, and it has been agreed

that the landlord will be held harmless in the event of such loss. This is seen in section 9

of the lease:

“9. REPAIR OF PREMISES. Lessee shall repair partitions, all glass and plate glass, elevators, electric and plumbing fixtures, and all machinery whatever in leased premises. Lessee shall be liable for and shall hold Lessor harmless in respect of: damage or injury to Lessor, premises, and property or persons of Lessor’s other tenants, or anyone else, if due to act or neglect of Lessee, or anyone in his control or employment. Lessee shall at once report in writing to lessor any defective condition known to him which Lessor is required to repair, and failure to do so shall make Lessee responsible for damages resulting from such defective condition.”

In the third section, the lease states that CCI may not use the premises for anything other

than retail without the landlords consent. CCI must stay within the scope of the business

in order to continue using the building.

9

“3. USE. Tenant may use the Premises for retail space, but for no other use without Landlord’s prior written consent. In no event shall Tenant make any use of the property which is in violation of any government laws, rules, or regulations insofar as they might relate to Tenant’s use and occupancy of the premises, nor may Tenant make any use of the premises not permitted by any restrictive covenants which apply to the Premises, or which is or might constitute a nuisance, or which increases the fire insurance premiums (or makes such insurance unavailable to Landlord) on the building. The tenant is responsible for the payment of the taxes and insurance.”

The Atlanta operating base is the first operating base that CCI opened; it is 30

years old. It is 100,000 square foot, one story, stand-alone building. It has a

complete sprinkler system, is 5 miles away from the nearest fire station and

building construction is masonry non-combustible. This would preserve the building

and its contents in the event of a fire. It should be noted that there is a fertilizer plant

located 800 yards to the south, which presents an apparent explosion risk. In the event

of an explosion, this building would be covered under the Basic Form property coverage.

The site was previously occupied by a gas station, which presents a liability risk if all

of the old chemicals and pollutants were not properly disposed of. Employees working at

this location have complained of strange smells and coughing, so the building needs to be

assessed by professional as soon as possible. This could bring about a relatively large

workers compensation claim if proven to be the reason for the employee sickness.

The CCI operating base in Columbia, SC is 80,000 square feet and the

majority of the building is over 50 years old. The building does not have sprinklers,

and the nearest fire station is 8 miles away. These unfavorable conditions make this

location prone to total loss of the building and inventory due to a fire. The current

conditions of this aged building make a total loss possible, and it is susceptible to local

building codes that could require complete destruction with a major loss. CCI has

recently considered putting a complete sprinkler system in this building. The quotes

10

received for this installation are as follows: $11,000 for the construction of the

water main, $7,000 for the water tower, a 6.5 percent city tax and an installation

cost of 85 cents per square foot. This installation would result in dramatic decreases

in property insurance rates. After running the NPV analysis shown in the Appendix,

it is highly recommended that this system be installed.

The operation base in Miami, Fl is the smallest base; it is 20,000 square feet.

The building has a complete sprinkler system. It was completely rebuilt in 1992

after Hurricane Andrew went through the area. Miami is an area that is very

susceptible to hurricane risk, which can result in the potential damages from windstorms

and flooding. Because of this, the Difference in Conditions extended coverage under the

Basic Form property policy will be recommended.

The operating base in Columbus, OH was built in 2006 and is the newest

building. It is 60,000 square feet and one story tall. It has sprinklers, was built to

code, building construction is classified as masonry non-combustible and the

nearest fire station is only one mile away. The combination of these factors makes it

very unlikely that a fire will result in a total loss.

3.1.2 Improvements and Betterments

Improvements and betterments will only apply to the CCI corporate

headquarters because it is the only building that is leased by the company. This is

specifically spelled out in the lease agreement between CCI and the leasing

company:

“6. TENANT’S BETTERMENTS AND IMPROVEMENTS. Tenant shall make no structural or interior alterations of the Premises without Landlord’s prior written consent, and any work performed by Tenant shall be done in a good and workmanlike manner, and so as not to disturb or inconvenience other Tenants in the building. Tenant shall not at

11

any time permit any work to be performed on the Premises except by duly licensed contractors or artisans, each of whom must carry general public liability insurance certificates, of which copies shall be furnished to the Landlord.”

Based on this agreement, the employees hired by CCI to provide maintenance

of the buildings are in direct violation of this clause in the lease because they are not

licensed contractors.

Even though the building owner will own any improvements that CCI could

make to the premises, because CCI has 9 years remaining, it could prove profitable

for CCI to make any advancements that they deem fit for the property. However,

they would have to get permission from the property leasing company first.

The restrictions for improvements and betterments only apply to the

location that CCI leases. All other locations are owned by CCI, so the company can

make any improvements to these buildings, as long as they follow local construction

codes. The additions and alterations that CCI makes to these owned buildings will

become part of the company’s vested interest in the value of the property. For this

reason, any changes made to the buildings should be reported to the property

insurer within thirty days of the start of construction. If CCI possesses a standard

Business and Personal Property Coverage Form, reporting these changes to the

property will be beneficial.

3.1.3 Personal Property

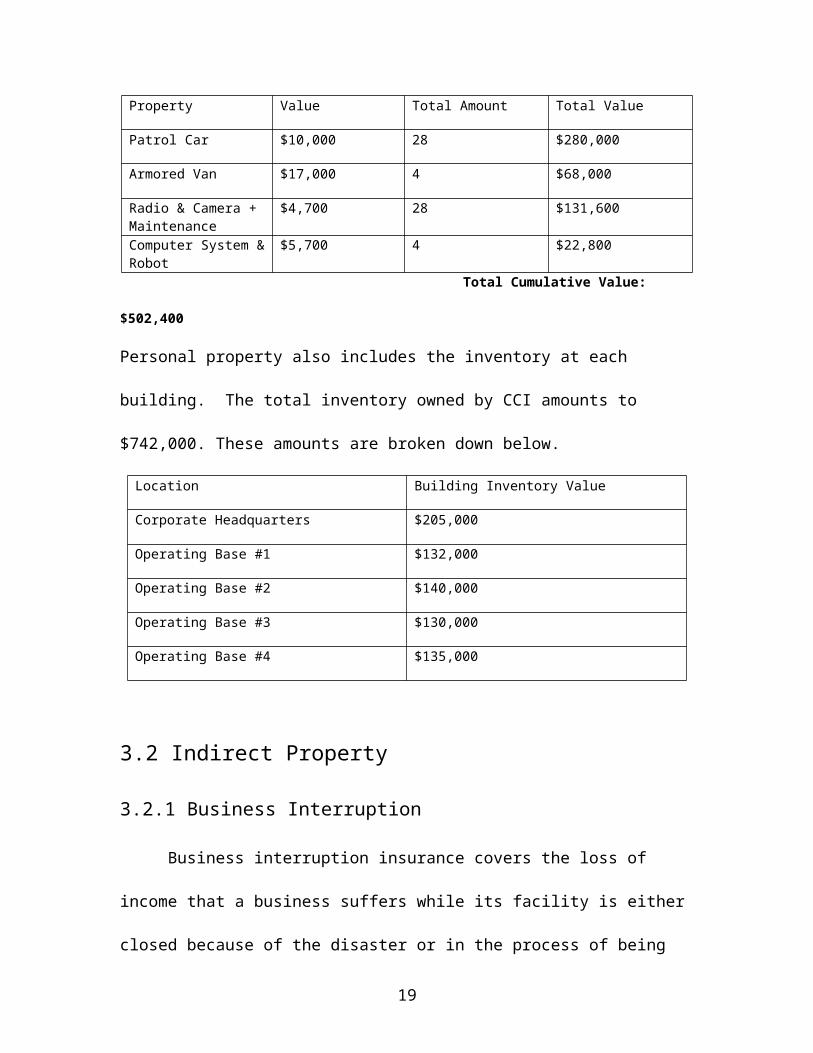

CCI has a multitude of personal property exposures, including building

inventory, vehicles, technological/computer equipment and stun guns. Because of

this multitude and the high value of this personal property, it is recommended that

12

these exposures be insured. The breakdown of the value of the personal property

held by CCI can be seen below.

Property Value Total Amount Total Value

Patrol Car $10,000 28 $280,000

Armored Van $17,000 4 $68,000

Radio & Camera + Maintenance

$4,700 28 $131,600

Computer System & Robot

$5,700 4 $22,800

Total Cumulative Value: $502,400

Personal property also includes the inventory at each building. The total inventory

owned by CCI amounts to $742,000. These amounts are broken down below.

Location Building Inventory Value

Corporate Headquarters $205,000

Operating Base #1 $132,000

Operating Base #2 $140,000

Operating Base #3 $130,000

Operating Base #4 $135,000

3.2 Indirect Property

3.2.1 Business Interruption

Business interruption insurance covers the loss of income that a business

suffers while its facility is either closed because of the disaster or in the process of

being rebuilt after it. This coverage extends until the end of the business

interruption period, which is determined by the insurance policy. For CCI the

13

business interruption period is a maximum of 7 months. This means that CCI would

have no more than 7 months to resume normal operations after a complete

shutdown.

One concern for CCI in terms of business interruption should be Ed McGruff’s

decline in health. If it is true that he has been diagnosed with cancer and has 3 years

to live, then the company must have a plan in place to restructure the CCI

management team. Ed has led CCI through nearly 20 years of impressive growth. It

will be difficult for the company to quickly transition under new management, so

the process needs to start as soon as possible.

Also, CCI is growing increasingly concerned that demand for physical

security will decrease as technology continues to become more advanced. This

presents yet another exposure for CCI and the future of the business. If this theory

is true, then CCI will have to either adjust to the market or convince the market that

their services are superior in order to stay afloat. If the company is not able to do

this, business could be severely interrupted.

3.2.2 Contingent Business Interruption

3.2.2.1 Recipient

Contingent Business Interruption insurance covers a company for any losses

experienced by a company that come due to a loss or shut down of another company

that provides some sort of support for the original company.

Right now, 80 percent of business that CCI does comes from only 5 contracts.

If any of these contracts was to go under, this would cause a huge business

interruption loss to CCI. This dependence on so few contracts is high risk for the

14

company. For example, 95 percent of the income in the Miami operating base comes

from just one contract. If this contract ended for any reason, operations would

likely shut down in the Miami location. To help mitigate this risk, CCI should

attempt to spread the company’s revenue stream over more locations.

There is also specific Business Interruption that needs to be considered for

the corporate headquarters in Charlotte. Section 7 of the lease states that if a major

loss occurs to the building, then the lease could be terminated. CCI could have to

find a new location and new lease in a short amount of time, even if the major loss

that occurs to the building is not the company’s fault.

3.2.2.2 Contributing

CCI is dependent upon an outside company to work on its radios and

cameras in the patrol cars. If this company was to suddenly go under, CCI would

need to find another company that specializes in this kind work. If any of the

equipment was to malfunction before CCI found another company, it would be

unusable and would affect employees’ abilities to do their jobs.

3.2.3 Extra Expense

Extra Expense coverage shortens the length of any interruption so that a

company can get back up and continue operations faster. Having this type of

coverage will pay for any extra expense that will facilitate a quicker recovery time

for a company. Because one loss could mean a loss of 20 percent of income for CCI,

this type of coverage would be beneficial. The longer CCI is shutdown after a loss,

the more time customers have to browse alternatives to CCI services. CCI also

provides an integral protection service for their customers. Because of the nature of

15

the business, any interruption of the services provided could lead to an increase in

crime and danger.

3.2.4 Building Ordinance

Building Ordinance coverage will cover loss caused by enforcement of

ordinances or laws regulating construction and repair of damaged buildings. The

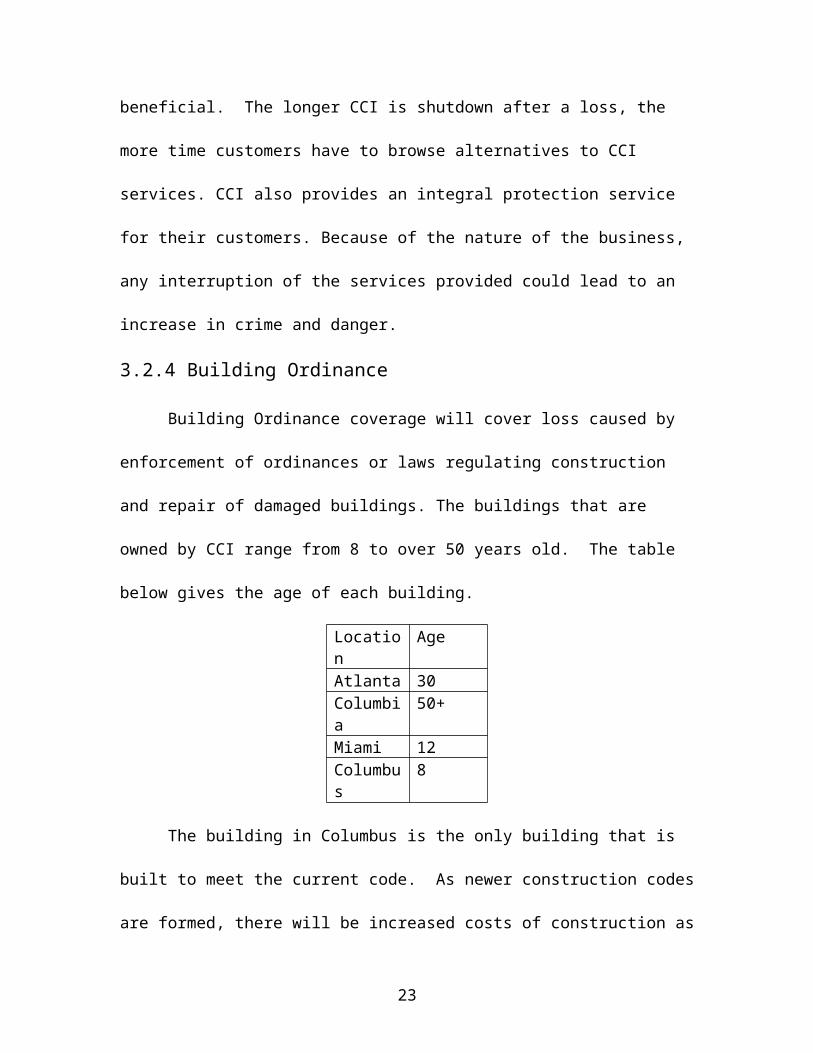

buildings that are owned by CCI range from 8 to over 50 years old. The table below

gives the age of each building.

Location AgeAtlanta 30Columbia 50+Miami 12Columbus 8

The building in Columbus is the only building that is built to meet the current

code. As newer construction codes are formed, there will be increased costs of

construction as time goes on. Because of this and the aging status of the majority of

the buildings owned by CCI, it is suggested that the company purchases ICC

Coverage C. Coverage C will cover increased cost to repair and replace buildings in

accordance with codes.

3.2.5 Leasehold Interest

Leasehold Interest coverage will cover the loss suffered by a tenant due to

termination of a favorable lease because of damage to the leased premises by a

covered cause. The space that CCI is leasing is favorable; the rate the company is

paying is $39,500 per month, while comparable properties in the Charlotte area are

renting for $42,500 a month. This presents a leasehold interest of $36,000 per year

16

for CCI. There are 9 years left on the lease. This is the amount that could be covered

if the lease was forcibly terminated.

4. Liability

4.1 Premises and Operations Liability

Premises and Operations liability provides liability coverage for potential

hazards to a business operation or the business’ premises. Because of the nature of

the business CCI is in, this type liability is a huge factor that the company needs to

take into consideration. CCI employees come into contact with people every day.

Sometimes employees are put into situations that could be dangerous. Most of the

time, employees have to use their own discretion and make split second decisions

when they are working. Recently, many of these decisions that employees have had

to make have been questionable, and some have come under public scrutiny.

In one instance, a CCI employee shot the tires on a student’s vehicle because

he thought that the student was drunk driving. In another case, a CCI employee shot

an unarmed homeless man three times because he thought the man’s milkshake was

a shotgun. In yet another instance, CCI officers used excessive force to keep students

from rushing a football field after a big win. Several students were injured, and one

suffered a broken neck. These actions taken by CCI employees are both very

extreme and unnecessary. Employees must be aware that these types of actions are

almost never okay. Lethal force should only be used in dangerous situations. CCI

employees should be trained on when to recognize if they are in a dangerous

situation. The employees are on campus to protect students; in all of these cases

17

they are doing more harm than good. Besides better training, another way to help

address this issue might be to perform background checks on employees. Originally,

CCI officers were all supposed have backgrounds in law enforcement and the

military. If CCI stayed true to this original plan, there would probably be less of

these negative incidents.

There have been other occurrences where students have been injured under

the CCI program. CCI has a “scared straight” style program that first time offenders

can opt to use in order to lessen their punishment. In one of these sessions, an

inmate stabbed a student. These sessions probably should be more closely

monitored, and students should only be coming into contact with non-violent

offenders.

CCI could be held liable for all of the above instances. Because of this, it is

recommended that CCI purchase a Commercial General Liability policy. This would

protect the company from any actions taken by its employees. While insurance will

reduce the severity of the loss for the company, the main focus should be placed on

risk control. CCI needs to make sure that its officers are trained properly to know

when it is appropriate to use excessive force to subdue an offender. There should

also be internal controls that will punish an officer who is accused of using these

methods.

4.2 Products Liability

Although CCI is a service oriented company that does not manufacture any

products, the company still could in some instances face a products liability case. If

the stun guns that CCI employees carry were to malfunction, there could be a suit

18

brought against the company. CCI should also consider its educational classes.

Anything that a student learns in this class that results in a negative action could

come back to CCI as a products liability case. It could be argued that the education

that CCI provides is the company’s product. For these reasons, CCI should think

about getting covered.

4.3 Auto Liability

As seen earlier in the report, CCI has a large amount of money invested in

automobiles. The company owns 28 patrol cars and 4 armored vans. CCI employees

are often behind the wheel while they are doing their jobs. If any accident was to

happen in these vehicles, CCI could be held liable. For this reason, CCI should protect

the company and the drivers of the patrol cars and the armored vans.

4.4 Advertising Liability

CCI is currently involved in a defamation case with a rival company. CCI ran

an ad that insinuated that the rival company was selling drugs to students. Because

CCI believes that this is actually the truth, the company believes it will win the

defamation case. However, there is concern about the high legal fees and judgment

costs. It will likely cost CCI a lot of money to prove that the statements they made

were true. CCI currently believes that its liability insurance will cover all of these

costs.

4.5 Employment Practices Liability

Employment practices liability deals with wrongful termination, sexual

harassment, discrimination, invasion of privacy, false imprisonment, breach of

19

contract, emotional distress and wage and hour law violations. CCI has faced and/or

could potentially face several of these issues.

CCI has had some questionable hiring decisions, even in the upper

management of the company. Jim Intone, VP of the company, was hired as head of

security forces despite the fact that he had been charged with assault in the past.

His aggression is probably a contributing factor to the intense behavior exhibited by

many CCI employees in the field. Mark Owens was hired because he is the CEO’s best

friend. Although his title is “Lead Trainer and Public Relations Specialist” he has no

background in PR. Being a people person has nothing to do with the practice of

public relations. The only experience he has is teaching driver’s education to high

school students. He does not appear to be qualified for the position he ahs in the

company.

The Miami and Columbus locations have had some issues with hiring

practices as well. About 90 percent of CCI employees at these locations are white

males. While these males are assigned to patrol jobs, females are almost always

assigned to desk jobs. This was addressed in a company memo that stated “… this is

done in an effort to protect our male employees.” This statement is very broad and

could be easily misunderstood. Female employees are also given degrading

uniforms that accentuate their “features”. Female employees have complained to

management that they are not comfortable in these uniforms, but the only feedback

they have gotten is that it creates “a more relaxed environment”. Basically the

company does not have a reason for the women to wear these uniforms. CCI should

either get rid of this unprofessional attire or give a better reason as to why women

20

should have to wear it. If CCI wants to be taken seriously as a security services

company, this is not the way to go. As for the reasoning that people are hired based

on the demographic makeup of the area, either CCI has not seen recent

demographics or they are just coming up with quick excuses. For example, in Miami,

70 percent of the population is Hispanic or Latino. In Columbus, while 60 percent of

the population is white, 25 percent is black. Neither area is close to 90 percent white

males.

There have also been sexual harassment complaints in the workplace.

Females have complained that Jim Intone regularly makes inappropriate jokes.

When she complained about it, he told her to work somewhere else. This is very

unprofessional. The formal CCI policy states that all employees are to be treated in a

professional manner. There is no point in having policies like this if they are not

being followed, especially by someone who manages the company. This issue needs

to be addressed immediately.

Also, it was mentioned before that employees do not have to get background

check before they are hired. Because of the nature of the job, background check

should be required. When Sullivan founded the company, he wanted all of the CCI

officers to have had experience in law enforcement and/or the military. This is

something that helped to make CCI successful, and it is something that the business

should stick to. Doing background checks would also help with the issues that CCI

has with employees. For example, if CCI required background check, then the

company would not have hired a sexual predator to teach sexual health classes.

21

If CCI does not change the company’s practices regarding hiring and

workplace behavior, then the company will be exposed to a multitude of exposures

and claims that could be brought against them. Better hiring practices and employee

policies must be adhered to.

4.6 Professional Liability

Professional liability coverage helps to protect service providing companies

such as CCI from bearing the full cost of defending against a negligence claim made

by a client. CCI has a relatively large exposure in this section. Because the company

is providing security services, if any sort of crime occurs on a campus, the university

could look to blame CCI for not doing enough to protect students. As of right now,

CCI has not had to face any accusations like this. However, because of the

orientation of the company, if something like this were to happen CCI could face a

huge loss. It is highly recommended that CCI become covered.

4.7 Contractual Liability

Contractual liability comes when a company enters into a contract with

another entity and in this contract there is a “hold harmless agreement”.

4.7.1 Leases

There is a hold harmless agreement in the lease that CCI signed for the

company headquarters in Charlotte:

“RISKS OF INJURY. The Landlord shall not be responsible for any injury which shall be sustained by the Tenant or any employee, customer, or other person who may be upon the Premises or in the said building or the entrances or appurtenances thereto. All risks of any such injury being assumed by the Tenant, who shall hold the landlord harmless and indemnified therefrom.”

22

This states that CCI will be liable for any actions that cause injury on the

leased premises.

4.7.2 Other Contracts

CCI also holds multiple contracts with different firms for the use of

intellectual property and specially licensed software. The following clause is

included in each contract:

“Lessee agrees that Lessor shall not be held responsible for any loss or damage to Lessee, its employees, its customers, or to any third party, caused directly or indirectly by the equipment. All risks of loss of the equipment and all liability for any damage or injury shall be upon Lessee and not upon Lessor. Lessee does hereby assume liability for Lessor from and against any and all liabilities, losses, damages, penalties, claims, actions, suits, costs, expenses and disbursements, including court costs and legal expenses, of whatsoever kind, and nature...any claim for patent, trademark or copyright infringement.”

This lease places all injury on CCI. The amount of technology that CCI uses for the

company offices, patrol cars and armored vans creates a large exposure. There have

been instances where CCI employees have been caught misusing the robots; any loss

resulting from this misuse would be paid for solely by CCI.

23

5. Personal

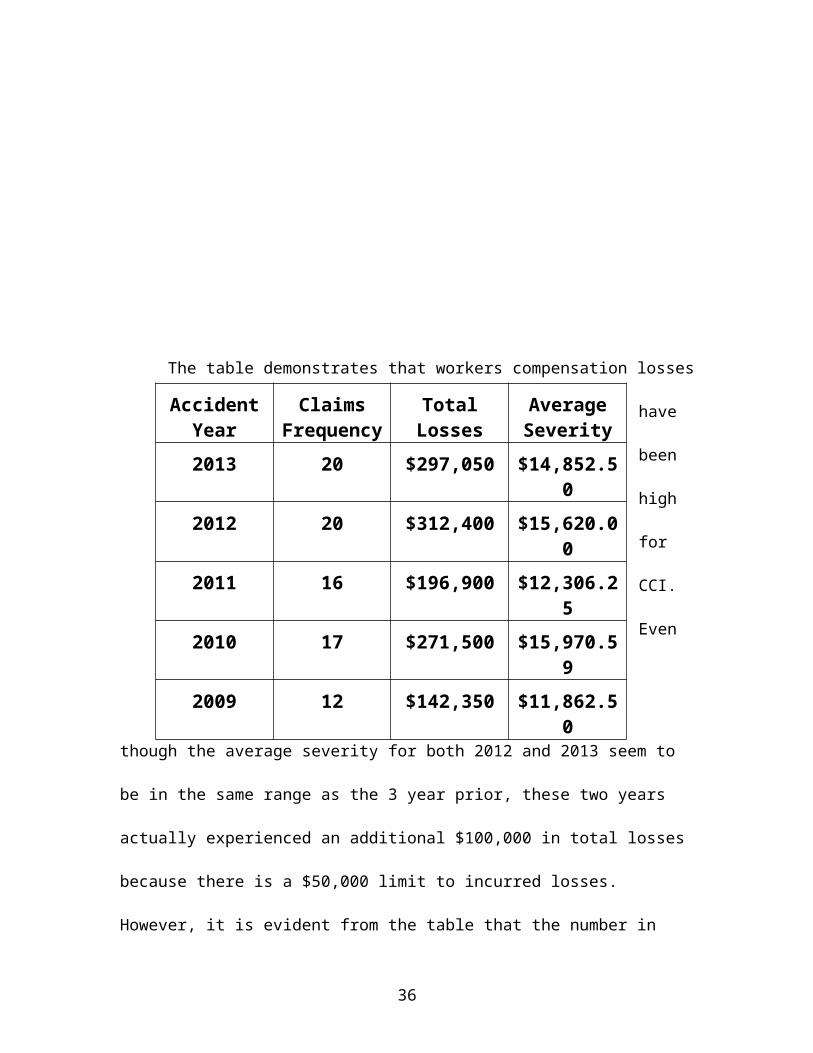

5.1 Workers Compensation

A company that is in the service industry, like CCI, can have a lot of workers

compensations claims. CCI workers are put in situations where their safety and

well- being could be compromised day in and day out. The number of claims and

losses can be seen in the table below.

The table demonstrates that workers compensation losses have been high for

CCI. Even though the average severity for both 2012 and 2013 seem to be in the

same range as the 3 year prior, these two years actually experienced an additional

$100,000 in total losses because there is a $50,000 limit to incurred losses.

However, it is evident from the table that the number in claims has slowly raised

each year. To reduce losses in the future, CCI could implement a better employee

training to teach them how to do their job more safely.

24

Accident Year

Claims Frequency

Total Losses

Average Severity

2013 20 $297,050 $14,852.50

2012 20 $312,400 $15,620.00

2011 16 $196,900 $12,306.25

2010 17 $271,500 $15,970.59

2009 12 $142,350 $11,862.50

5.2 Business Continuation

The CEO of CCI, Ed McGruff may have cancer and is only projected to live 3

more years if the rumor is found to be true. Ed is the key to holding this business

together and is the reason CCI has been very successful over the years. Ed also is the

largest shareholder owning 55% shares in the company. Prior to Ed passing away

their needs to be a plan put together involving how they will allocate his shares and

who will talk over as CEO. As of today CCI has not made a plan of action. Therefore,

the company should write a contingency plan. There isn’t a need to pay for this

insurance coverage; a strategic contingency plan work for CCI.

5.3 Employee Benefits

Having good employee benefits is not only the best way to gain great

employees but it also insures that employees will stay with that company for a

longer period of time. Most companies today want to offer the best employee

benefits in their industry. Employee benefits can consist of the following:

retirement, housing, daycare, tuition reimbursement, sick leave, disability income

protection, profit sharing, social security, gym membership, paid and non-paid

vacation, group insurance (health, dental, life, etc.).

College Cops Inc. doesn’t offer any employee benefits other than offering a

small stake in the company to employees that has been with CCI for 5 years or more.

There is no doubt that CCI should redo their employee package that they offer to

25

incoming employees as well as current employees. Most employees are interested in

retirement plans and health insurance plans.

Considering the wants of employees along with the new Affordable Care Act,

CCI must provide full time employees with sufficient health care coverage. Under

the new health care laws CCI is consider a large business and states that large

business must provide health insurance to all full time employees. Companies that

choose not to provide health coverage; will be fined by the government.

College Cop Inc. should consider offering their employees a retirement plan. I

recommend that CCI use an IRA due to its simplicity and attractiveness by

employees. Under an IRA I suggest that CCI go with a defined contribution plan. A

defined contribution plan mean that the employer will match a certain percentage of

what the employee contributes to the plan. Employees pay into the plan before their

income is taxed. This allows for the retirement plan to grow tax-free. Retirement is

not taxed until the employee draws from their retirement plan.

26

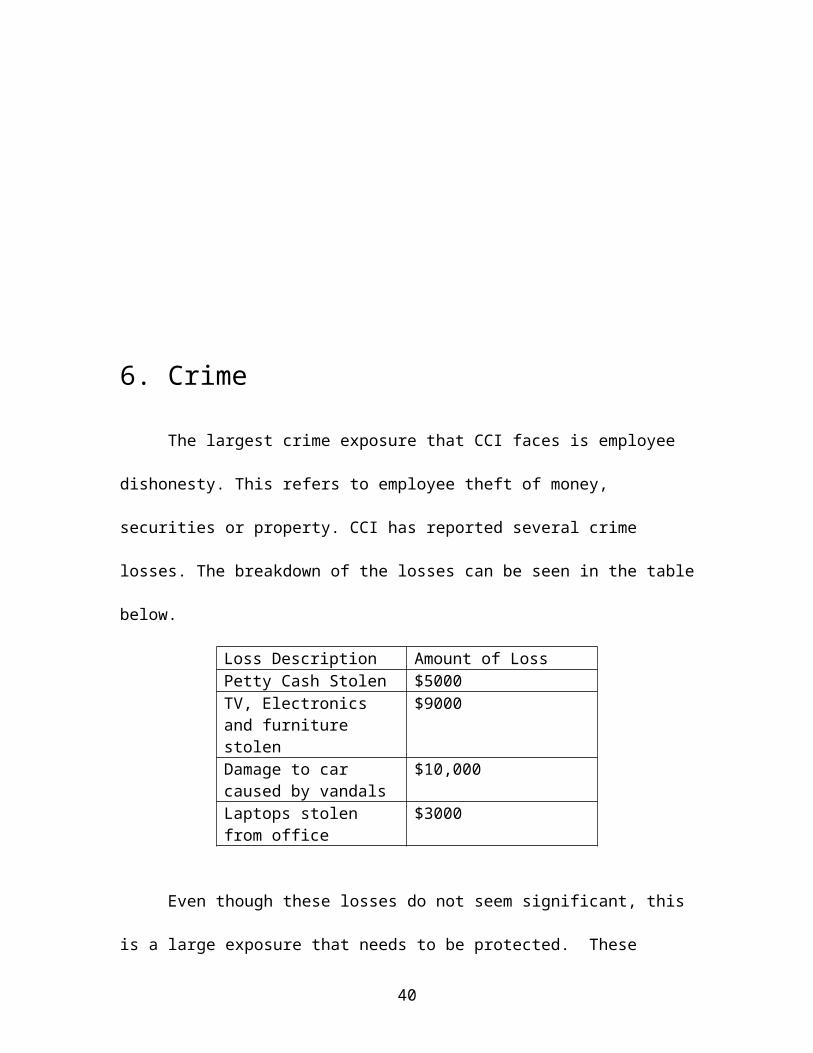

6. Crime

The largest crime exposure that CCI faces is employee dishonesty. This refers

to employee theft of money, securities or property. CCI has reported several crime

losses. The breakdown of the losses can be seen in the table below.

Loss Description Amount of LossPetty Cash Stolen $5000TV, Electronics and furniture stolen

$9000

Damage to car caused by vandals

$10,000

Laptops stolen from office

$3000

Even though these losses do not seem significant, this is a large exposure that

needs to be protected. These thefts could add up over time. Actions must be taken

to stop this kind of employee behavior. One thing CCI can do to help protects its

assets is to ensure that all property is watched by security cameras. Also, all

buildings should be monitored by a security company. These types of internal

controls are necessary to cut down on the frequency of this internal theft and

dishonesty before it becomes a bigger issue.

Another crime exposure that CCI currently is facing is cyber theft. CCI has

private, personal information as well as important business information and tools

stored in the company’s computer system. All CCI employees have easy access to

this information. There have been reports of employees taking this information and

potentially selling it to rival companies. Also, there was an instance where

thousands of student’s personal information was compromised. There are no

27

policies in place to monitor that the network is being used properly, and the only

security that the system has is a username and password selected by the employee.

Having so much sensitive information saved in one location creates a massive

exposure for CCI. This is an issue that must be addressed.

28

7. Other Business Risks

CCI faces huge reputation risk if changes are not made to the company. CCI

got most of its business from its good standing and reputation when it was first

started 40 years ago. Now, CCI is under a lot of public scrutiny for many of the

abovementioned exposures.

A security company like CCI will be unlikely to get new business if it has a

negative reputation. This also puts the company at risk to lose current business.

With technology becoming more and more prevalent in today’s society, many

colleges have considered using only technology for security purposes. If CCI has a

bad reputation, this makes the decision to go tech easy for colleges and universities.

The company will have to be at the top of its game, especially in the public eye, if it

wants to stay afloat.

29

8. Risk Treatment

8.1 Rention

Retention is when a company decided not to have insurance cover on a

certain exposure or even peril. Usually a company chooses to use retention in the

following two situations: when both frequency and severity are low, and when

severity is low but frequency is high. However, when severity is low and frequency

is high the company should not only retain the exposure but also reduce the

frequency of that exposure being a peril.

8.1.1 Retention Capability

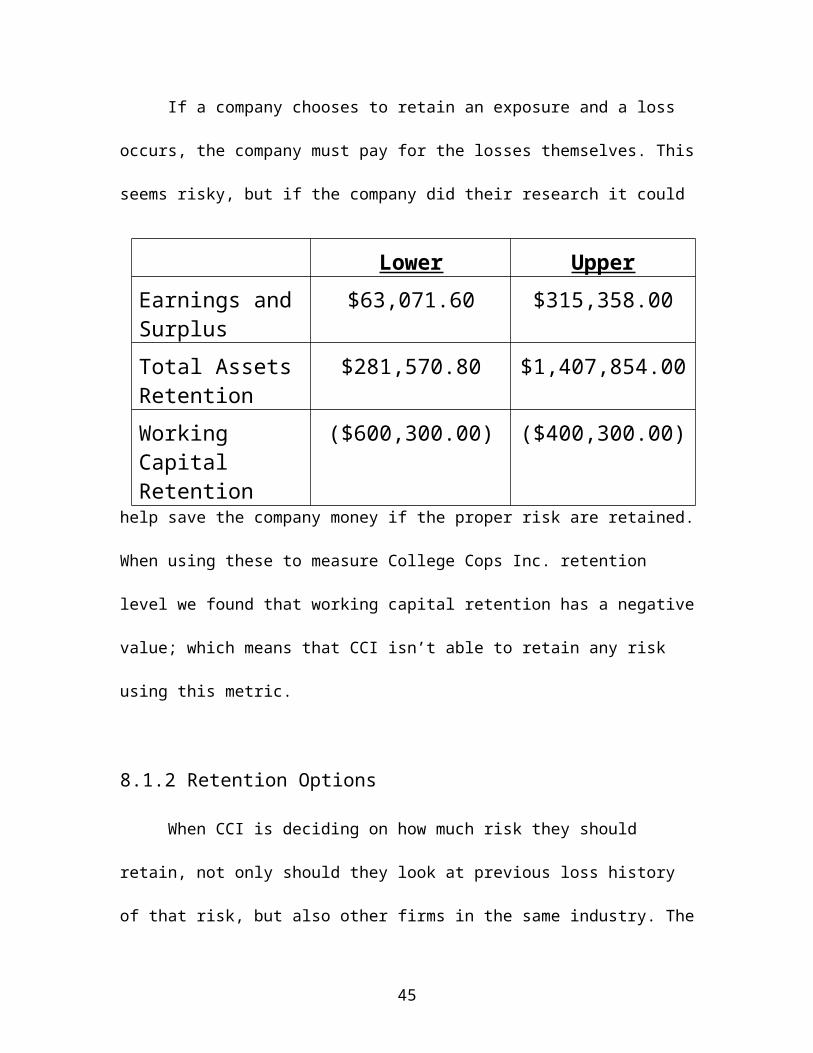

If a company chooses to retain an exposure and a loss occurs, the company

must pay for the losses themselves. This seems risky, but if the company did their

research it could help save the company money if the proper risk are retained.

When using these to measure College Cops Inc. retention level we found that

working capital retention has a negative value; which means that CCI isn’t able to

retain any risk using this metric.

30

Lower Upper

Earnings and Surplus

$63,071.60 $315,358.00

Total Assets Retention

$281,570.80 $1,407,854.00

Working Capital Retention

($600,300.00) ($400,300.00)

8.1.2 Retention Options

When CCI is deciding on how much risk they should retain, not only should

they look at previous loss history of that risk, but also other firms in the same

industry. The best way to go about comparing to industries is to compare ratios.

When calculating and comparing two ratios, CCI seems to be unfavorable to fall on

the wrong side of the ratio. Taking this into account I do not suggest that CCI retains

any risk.

9. Insurance and Risk Financing

9.1 Property Insurance

9.1.1 Direct Property

31

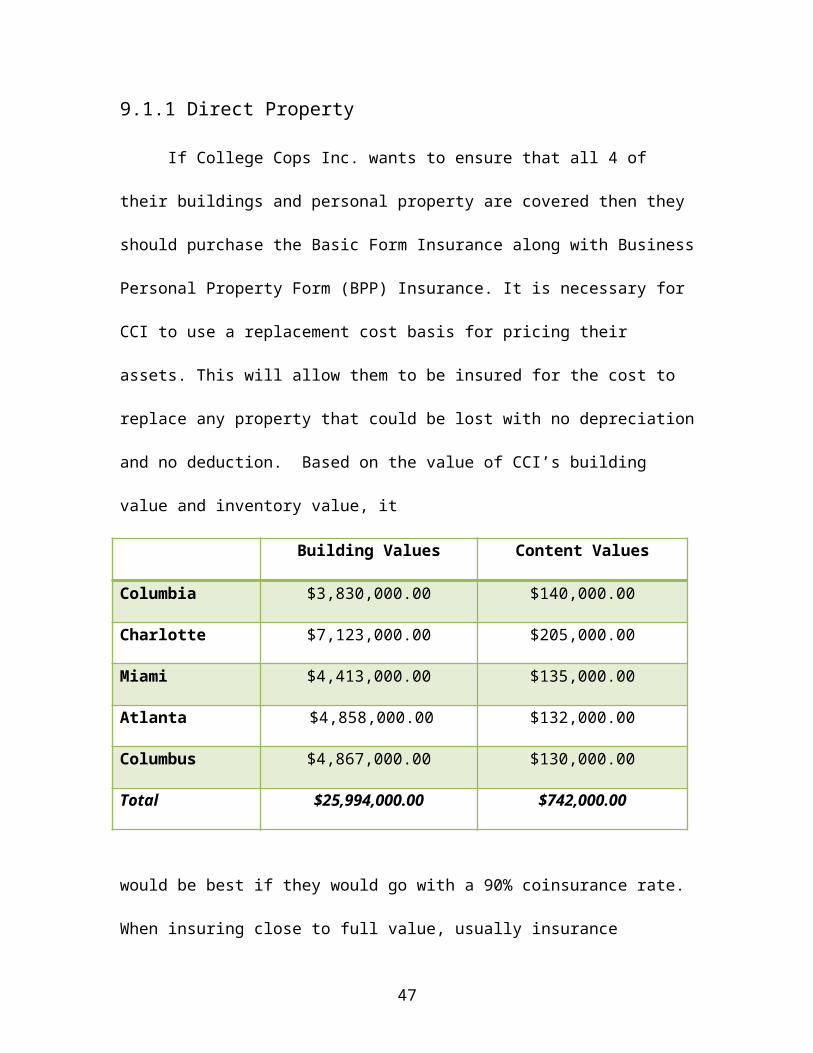

If College Cops Inc. wants to ensure that all 4 of their buildings and personal

property are covered then they should purchase the Basic Form Insurance along

with Business Personal Property Form (BPP) Insurance. It is necessary for CCI to

use a replacement cost basis for pricing their assets. This will allow them to be

insured for the cost to replace any property that could be lost with no depreciation

and no deduction. Based on the value of CCI’s building value and inventory value, it

Building Values Content Values

Columbia $3,830,000.00 $140,000.00

Charlotte $7,123,000.00 $205,000.00

Miami $4,413,000.00 $135,000.00

Atlanta $4,858,000.00 $132,000.00

Columbus $4,867,000.00 $130,000.00

Total $25,994,000.00 $742,000.00

would be best if they would go with a 90% coinsurance rate. When insuring close to

full value, usually insurance companies offer incentives. The closer CCI gets to

insure building and property to full value the lower the rate per $100 and the lower

the premium.

9.1.2 Accounts Receivable

College Cop Inc. has a 178-day collection period of funds owed to them.

Having a long collection period allows for their accounts receivables to be included

into their current assets. CCI should have accounts receivables coverage that can

32

purchase through an Inland Marine policy. This coverage will protect the insured

from losing cash that was never render by customers.

9.1.3 Mobile Equipment

The only mobile equipment that CCI has, are four robots that is in 4 separate

vans. Each of these vans is stored in separate locations. Having the robots stored in

separate locations should lower the probability of a total loss. Each of the robots is

valued at $5,700. Therefore there is no need to insure the robots to full value.

9.1.4 Leasehold Interest

CCI should add a leasehold endorsement to cover any loss of the leasehold

interest. This would take into affect if the current building being leased were

damage, making CCI rent another building at a higher monthly rate.

9.2 Liability Insurance

9.2.1 General Liability

Due to the nature CCI’s business, they face a lot of liability exposers.

Employees at CCI don’t have to act in negligence to have lawsuit filed against them.

Any result in damages or injuries during an arrest by a CCI employee could end in a

lawsuit. It is evident that liability insurance should be the main concentration of

coverage should be liability insurance. Without this coverage, CCI could get it with

and expense that wouldn’t give them a leg to stand on financially. CCI should have a

Commercial General Liability (CGL) policy, which will cover them for most occasions

that they may be found liable. CGL has three coverage’s within the policy: Coverage

33

A insures for bodily injury and property damage, Coverage B insures for personal

and advertising liability, and Coverage C is a no-fault medical expense coverage.

9.2.2 Fire Legal Liability

I recommend that CCI purchase Fire Legal Liability Coverage for the

Charlotte location. This coverage will protect the leased building if a loss incurred

due to fire.

9.2.3 Executive Liability

CCI also has a liability exposure dealing with the upper management acting in

the wrong. Executive liability could arise from many different reasons, but some of

the most common cases are wrongful termination, hiring practices, harassment, and

discrimination. CCI would be legal liable as long as the employees or up

management were representing or operating in scope of the company. In order for

CCI to protect them from these risks they would need to be covered under a

Directors and Officers policy. I recommend CCI consider a limit of $2,040,000, to

ensure that they are covered for any lawsuit that might result from upper level

managements decisions and actions.

9.2.4 Umbrella Policy

College Cops Inc. also runs the risk of being hit with an expense that exceeds

the limit of the primary coverage. This is when an Umbrella Policy is needed. An

Umbrella Policy sits above liability policies and covers the excess that exceeds the

original limit. However, CCI can’t just purchase the lowest limit to reduce their

premiums for the primary coverage. Umbrella Policy’s set what you must have in

order for the Umbrella Policy to cover the excess expenses. I recommend that CCI

34

obtain an umbrella policy with the limit of $2,000,000. The policy states that there

must be underlying limit of $500,000 for all coverages to fall under the umbrella

policy.

9.3 Business Auto

College Cops Inc. owns 32 vehicles that they use in their day-to-day

operations of the business. Being that these vehicles stay within a 100 miles radius

of their working base they are qualified as a service vehicles. CCI has had a collision

rate of 56 in their past experiences. I recommend that CCI increase their premium so

their deductible will be significantly lower. As of today they are paying a premium of

$1792.00 and their deductibles are $1,000. Under collision it would be in CCI best

interest to pay a higher premium and a lower deductible do to the amount of

collision frequency they are known for.

9.4 Crime

In order for CCI to ensure they are covered for any crime that they lead to

potential losses for the company, they will need to obtain a Commercial Crime

Policy. This coverage insures them of any crime reported against any of their

property or buildings.

9.4.1 Employee Dishonesty

One of the main reason CCI should obtain a Commercial Crime Policy is to

ensure that will be in insured for any employee dishonesty. With as many

35

employees as CCI has it is very hard to watch what every employee is doing at all

times. Employee dishonesty should be CCI’s main concern involving crime, and

because of the amount of risk exposures they have with employee dishonesty, I

recommend they be insured through Employee Dishonesty coverage.

9.4.2 Inside the Premises Theft Money and Securities

College Cops Inc. keeps some cash on hand and has had a history of petty

cash being stolen. In order to ensure that CCI is covered in the event of future cash

being stolen they would need to have a $10,000 limit on Coverage C. This would

only cost $14.10 with a $100 deductible that would yield a 6% credit. CCI hasn’t

been hit hard by a large amount of petty cash being stolen but the fact that they keep

cash on hand means I would recommend them being covered in case such event

takes place.

9.4.3 Inside the Premises Robbery and Safe Burglary

One might think that the last place a criminal would rob or steal would be a

college cops headquarters. However, CCI has lots of pricey assets that they use in

their day-to-day business operations, which would appeal to most criminals. To

ensure that CCI is covered for any robbery and safe burglary inside the premises

they would need to obtain a $75,000 limit for coverage D. This limit comes with a

$100 deductible, 6% credit, making it a $33.28 premium.

9.4.4 Computer Fraud

CCI hasn’t had any past history of computer fraud. However, CCI’s computers

and their computer systems is what keep all their valuable information that they use

during normal business operation. Any computer fraud losses could put the out of

36

commission until for day or weeks until they can get everything back in place. I

recommend that CCI protect them from this potential loss by obtaining Coverage F

in the Commercial Crime Policy. I recommend a limit of $10,000; which has a $100

deductible, 6% credit, $1.53 premium.

9.5 Workers Compensation and Employer’s Liability

As mentioned previously, College Cops Inc. struggles worker compensation.

Looking at the past workers compensation experience, CCI has produced a large

number of work related injuries. CCI is required to have workers compensation

insurance in all the states that their company resides. Therefore, it is CCI

responsibility to pay any claims that arise from employees being injured on the job

whether they were negligent or not.

I recommend that CCI implement new loss control techniques to help reduce

the frequency and severity of these reoccurring claims. I recommend CCI take ahold

of this problem by using the Grange dividend plan. The premium for the Grange

dividend plan is $508,500; which is significantly lower that the amount of worker

compensation claims they have paid out. Until CCI finds a loss control plan that

works and then implements the plan through the entire company, the number off

losses from workers compensation aren’t going to go down. However, I do believe

that if CCI would use the Grange dividend plan throughout the entire company they

will see the number of losses decrease.

9.6 Alternative Risk Financing

37

There are other way that CCI can finance their losses other than just obtain

insurance. For the building in Miami, FL, CCI could purchase a Catastrophe Bond

(Cat Bond), to cover a loss from a hurricane. They could also form a group captive

with other companies in the industry. However, I would not recommend this option

because CCI would have to spend a lot of time evaluating other company’s risk to

see if they are bringing in the same amount of risk. I feel CCI needs to focus on the

substantial amount of risk exposure they are forced to face.

38

10. Loss ControlLoss control will seek to reduce the possibility that a loss will occur and/or to

reduce the severity of the losses that do occur.

10.1 Property

Although CCI properties range in age, the majority of them can be considered

to be older buildings. This means that they will increasingly require upkeep in order

to remain safe. To reduce loss and exposure to loss on the buildings, the main loss

control measure CCI can easily apply is regular, routine maintenance. It is

recommended that CCI begin to hire contractors to do repairs and maintenance

rather than having employees do it. Because normal employees are not hired for this

type of work, they usually are not qualified for it. This will ensure that the work is

completed correctly. Also, in order for CCI to not be in violation of the lease on the

company headquarters, outside contractors need to be hired out.

In the Columbia operating base, sprinklers need to be installed immediately.

This will be the easiest way to prevent a catastrophic loss if there is a fire in the

building.

A professional needs to be hired to inspect the building in Atlanta as soon as

possible. This location was previously a gas station, and employees there have

reported a strange odor. Some have even suggested that they are falling ill because

of chemicals that have not been sufficiently wiped out. This must be checked out as

soon as possible. It could possibly save money on multiple workers compensation

claims and lawsuits in the future.

10.2 Liability

39

10.2.1 Premises and Operations

As discussed earlier, because of the service oriented industry that CCI

operates in, the company’s operations are the greatest exposure to liability. The

security services expose the company to claims of negligence, injury and excessive

force. Although these risks cannot be fully mitigated, there are steps that can be

taken to control them.

CCI needs to revamp the training program for patrol officers. It needs to be

emphasized that lethal force should only be used in dangerous situations, and

officers-in-training need to be taught and tested on what a dangerous situation is.

All patrol workers should have to pass a rigorous training course before they are

going to be allowed to interact with the public. This will help to decrease the

number of claims.

Another way to help cope with this issue is to perform background checks

before hiring employees. The cost of doing this will pay off in the long term. There

should be no employees working for CCI who have criminal backgrounds.

10.2.2 Products Liability

As previously stated, even though CCI does not manufacture any products,

the company could be held liable for malfunctioning products that employees use,

such as stun guns. For this reason, employees should be extensively trained on how

to use and properly take care of the stun guns.

Another way the CCI could possibly be held liable is through teaching. If

what a student learns in a class is considered to be a “product” in court, then CCI

could be held liable for negative outcomes from that learning experience. Because

40

of this, teachers should have some sort of past experience with both teaching and

the subject matter. These employees should also have to submit to having

background checks done before they are hired.

10.2.3 Auto Liability

As mentioned before, CCI has a large amount of money invested in

automobiles. The company owns 28 patrol cars and 4 armored vans. CCI employees

are often behind the wheel while they are doing their jobs. If any accident was to

happen in these vehicles, CCI could be held liable. For this reason, CCI should protect

the company and the drivers of the patrol cars and the armored vans. The drivers

should also be extensively trained in the operating the vehicles they will be assigned

to drive. Background checks will help to ensure that employees have a clean driving

record.

10.2.4 Advertising Liability

Although CCI is currently covered for advertising that the company might be

held liable for, CCI should consider using different advertising methods to attract

business. CCI is a unique company in that it provides security and education.

Advertisements should focus on positive aspects of the company like this instead of

bashing other security companies. This will ensure that CCI will not have to be

involved in more lawsuits than necessary.

10.2.5 Employment Practices Liability

CCI needs to significantly alter its hiring practices. Once again, background

checks need to be something that is required for every new hire. The company

41

should pay attention to the demographics it is hiring as well. Fair hiring practices

need to be adopted immediately.

Also, all employees need to be treated professionally and with respect.

Employees should be able to come to management with an issue without fear of

being fired. It is not enough to just have an employee policy; the policy must be

enforced. The employee policy needs to be strongly implemented for a successful

work environment to thrive. It is important for the success and smooth running of

the business that employees are treated well. There must be an understanding that

if a certain level of respect is not met, then there will be consequences for those

types of actions.

10.2.6 Professional Liability

As discussed earlier, because CCI provides security services, if any sort of

crime occurs on a campus, the university could look to blame CCI for not doing

enough to protect students. As of right now, CCI has not had to face any accusations

like this. However, because of the orientation of the company, if something like this

were to happen CCI could face a huge loss. It is highly recommended that CCI

become covered.

Another way to prevent something like this happening is to ensure that

employees are trained properly. There should be a continuing training plan in place

so that employees stay up to date with the latest technology and plans of action.

10.2.7 Contractual Liability

CCI has a contract to lease the headquarters in Charlotte. The contract states

that CCI will be liable for any injuries that occur on the leased site. CCI should get

42

covered to ensure that if anything happens to the property, they would not suffer

any losses.

CCI also hold leases with its software providers. This lease places all injury

on CCI. There have been instances where CCI employees have been caught misusing

the robots; any loss resulting from this misuse would be paid for solely by CCI. CCI

employees should be trained on how to properly use this type of equipment, and

there should be certain restrictions and guidelines stating how and in what

situations it can be used.

10.3 Personal

10.3.1 Workers Compensation

Looking at CCI’s past workers compensation claims it is evident that may of

their losses come from employees that are doing training exercises. It is important

for CCI to have these trainings to eliminate losses in the day-to-day business

operation. However, CCI should do a better job of monitoring the exercise trainings.

CCI should also educate their employees on the proper way to train. The charts

below show the frequency and the severity of the past workers compensation loss

experiences. It is evident that behind miscellaneous injuries that Back, Skin, Head,

43

Eye5%

Whole Body5%

Finger4%

Back11%

Skin9%

Miscellaneous18%

Head9%

Respiratory4%

Ankle4%

Foot2%

Neck4%

Collar Bone2%

Face4%

Internal 5%

Shoulder4% Hand

7%

Knee2%

Wrist2%

Arm2%

Injury Frequency

and hand are the most frequent occurring injuries.

Eye3%

Whole Body21%

Finger0%

Back13%

Skin5%

Miscellaneous9%

Head7%

Respiratory7%

Ankle1%

Foot1%

Neck7%

Collar Bone15%

Face2%

Internal 5%

Shoulder3%

Hand1%

Knee2%

Wrist0%

Arm0%

Injury Severity

As for severity, it is evident that whole body, collar bone, back, head, neck, and

respiratory have the most traumatic losses. These injuries are what cost CCI to have

to pay out a lot of money in workers compensation claims. Based on both frequency

and severity injuries, this should give CCI the adequate information they need to

know when it comes to what they need to better train their employees on, so they

44

are exercising in the proper technique. Doing this, CCI will notice a significant

amount of decrease in their workers compensation losses.

10.3.2 Business Continuation

The CEO of CCI, Ed McGruff may have cancer and is only projected to live 3

more years if the rumor is found to be true. Ed is the key to holding this business

together and is the reason CCI has been very successful over the years. Ed also is the

largest shareholder owning 55% shares in the company. Prior to Ed passing away

their needs to be a plan put together involving how they will allocate his shares and

who will talk over as CEO. As of today CCI has not made a plan of action. Therefore,

the company should write a contingency plan. There isn’t a need to pay for this

insurance coverage; a strategic contingency plan work for CCI.

10.4 Crime

Cybercrime has become highly rampant in today society. I recommend that

CCI do better about protecting their networks, due to the high amount of

confidential information they have stored in the network. CCI should not store all

their information into one network they should split the information up. They

should also have a back up network that isn’t stored inside of a computer or other

network in case if one crashes.

45

11. Risk Management Policy Statement

1. It shall be the policy of College Cops Incorporated to avoid, reduce, or transfer the risk of loss arising out of property damage, legal liability, and dishonesty in all cases in which the exposure could result in loss that would bankrupt or seriously impair the operating efficiency of the firm.

2. It shall be the policy of College Cops, Inc. to provide safe working conditions for its employees. Under no circumstances will the risk of serious injury or death of employees be considered an acceptable risk.

3. It shall be the policy of College Cops, Inc. to assume the risk of loss arising out of property damage, legal liability, and dishonesty in all cases which the exposure is so small or dispersed that a loss would not significantly affect the operations or the financial position of the firm.

4. Insurance will be purchased against all major loss exposures, which might result in loss of $75,000 aggregate self-insured retention. This amount is derived from a retention analysis using the earnings and surplus method. Insurance will be purchased through the purchase of appropriate forms of property and liability insurance against the widest range of perils and hazards available.

5. Insurance will not be purchased to cover loss exposures below the amount of $10,000 unless such insurance is required by law or by contract, or in those instances in which it is desirable to obtain special services such as inspection or claim adjustment in connection with the insurance.

6. The administration of the risk management program will be under the direction of the Human Resources director or Risk Manager if such personnel exists, such responsibility to include placement of insurance coverages, maintenance of property appraisals and inventory valuations, processing of claims and maintenance of loss records, and supervision of loss prevention activities.

7. Insurance will be placed only in insurance companies rated A+ or A in A.M Best's Policyholders Ratings. Insurance placed in any other companies will require a written report of the particulars, such report to be filed with the Board of Directors by the Insurance Administrator.

46

12. Program Organization

This risk management program must be implemented for the survival of

College Cops Incorporated. The preceding steps and suggestions will be necessary

for CCI take if the company is to continue to grow and expand at the current rapid

rate.

For this program to succeed, it is suggested that College Cops Inc. add a new

position to the upper management team. This person should have a background in

the security services industry, and he or she should also have experience in the field

of risk management.

This plan is ultimately for the betterment of the College Cops Inc., but it will

ultimately also provide benefits to shareholders, employees, customers and other

stakeholders with the company. If College Cops Incorporated follows these

instructions and adequately implements the risk management plans, the company

should thrive and expand.

47

Works Cited

1. Atkinson, Jennifer. Class Lecture. Commercial Property and Liability. University

of Georgia, Athens, GA. Fall 2013

2. Hoyt, Rob. Class Lecture. Corporate Risk Management. University of Georgia,

Athens, GA. Spring 2014.

3. Carson, James. Class Lecture. Employee Benefits. University of Georgia, Athens,

GA. Fall 2013.

48

Appendices

Workbooks Sprinkler

Premium

Ratio

Leasehold

Business Income

Analysis

Workers Compensation

Claims

Identification

Injury

Auto

49