China’s Logistics Industry Update 2012 - Fung · PDF fileChina’s Logistics...

46

China’s Logistics Industry Update 2012 June 2012 Li & Fung Research Centre 1

Transcript of China’s Logistics Industry Update 2012 - Fung · PDF fileChina’s Logistics...

China’s Logistics Industry Update 2012

June 2012Li & Fung Research Centre

1

In this issue:

2

I. Industry Overview

3

Total Logistics Value in China

Billion yuan % Share in total

Total logistics value 158,400(+12.3% yoy)

100

Including:‐ Agricultural products 2,600 1.6‐ Industrial products 143,600 90.2‐ Imported products 11,200 7.0‐ Recycled materials 600 0.4‐ Commercial and personal products 200 0.1

4

• China’s logistics industry demonstrated robust growth in 2011. The total logistics value1 reached 158,400 billion yuan, up by 12.3% year‐on‐year (yoy) in real terms

• Manufacturing sector remains key to China’s economy. The logistics value of industrial products accounted for a substantial share of 90.2% of the total logistics value in 2011

China’s total logistics value by category, 2011

Source: China Federation of Logistics & Purchasing

1 Total logistics value is defined as the total value of products being produced in or entering the country during the recording period. It reflects the market size of, and total demand for logistics services of a country [China Federation of Logistics & Purchasing (CFLP)]

Logistics Demand Coefficient and Total Value‐added of the Logistics Industry

5

Logistics demand coefficient, 2007 – 2011 The total value‐added of the logistics industry, 2010 and 2011

• A steady growth of the logistics market in China is also reflected by 2 other parameters: logistics demand coefficient1 and value‐added of the logistics industry

• The larger the two values, the larger is the market• In 2011, the logistics demand coefficient was 3.4, up from 3.2 in 2010. And the

value‐added was 3,200 billion yuan, up by 13.9% yoy in real terms• These increases denote a growing logistics market in China

Source: China Federation of Logistics & Purchasing Source: China Federation of Logistics & Purchasing

Unit 2010 2011

Total value‐added

Billion yuan 2,700 3,200

% yoy growth % 13.1 13.9

Share in GDP % 6.9 6.8

Share in tertiary industry % 16 15.7

1 Logistics demand coefficient refers to the logistics value‐to‐GDP ratio

Industry Overview

6

Logistics Cost

7

The total logistics cost as a percentage of GDP, 2007 – 2011

• Efficiency of the logistics industry is reflected by the total logistics cost as a percentage of GDP. The lower the ratio, the more efficient is the logistics sector

• The ratio has been decreasing over the past few years; it stayed at 17.8% in 2011• This ratio is still twice the ratios observed in other developed countries; there is huge room

for improving the efficiency of China’s logistics industry • The total logistics cost recorded 8,400 billion yuan in 2011, up by 18.5% yoy• In terms of cost structure, transportation cost accounted for the highest portion in the total

logistics cost, while the proportion has been decreasing over the last few years

Source: China Federation of Logistics & Purchasing

Share in total logistics cost 2007 2008 2009 2010 2011

Management 12.7% 12.7% 11.8% 12.7% 12.0%

Inventory 32.9% 34.7% 32.9% 33.8% 35.0%

Transportation 54.4% 52.6% 55.3% 53.5% 53.0%

The total logistics cost and its composition, 2007 – 2011

Source: China Federation of Logistics & Purchasing

Average Inventory Period of Industrial and Commercial Enterprises

8

• According to the 9th National Survey on Logistics Market by the National Development and Reform Commission (NDRC) and Nankai University in 2010, more surveyed enterprises kept their average inventory period with less than 2 months compared with the previous year

• In 2010, the average inventory period of industrial enterprises dropped to one and a half months; that of commercial enterprises even reduced to less than 40 days, reflecting an overall improvement in logistics efficiency in China

Average inventory period of industrial enterprises, 2009 – 2010

Average inventory period of commercial enterprises, 2009 – 2010

2009 2010

Average inventory period: 48.94 days

Average inventory period: 45.88 days

2009 2010

Average inventory period: 40.11 days

Average inventory period: 38.03 days

Source: National Development and Reform Commission, and Nankai University Source: National Development and Reform Commission, and Nankai University

World Ranking

9

• The logistics efficiency level in China can also be reflected in the global logistics performance index• The Logistics Performance Index by World Bank measures the logistics efficiency of different economies• In the 2012 exercise, China ranked 26 among 155 assessed economies, showing an improvement of

logistics efficiency as compared with the 2010 record• Developed or high‐income territories such as Singapore, Hong Kong and Finland topped the chart. A

number of European countries have shown a drop in their rankings, largely due to the global economic downturn and the lingering European debt crisis

Logistics Performance Index, 2012Economy Rank in 2012 Rank in 2010 Economy Rank in 2012 Rank in 2010 Economy Rank in 2012 Rank in 2010

Singapore 1 2 Austria 11 19 South Korea 21 23

Hong Kong SAR 2 13 France 12 17 Norway 22 10

Finland 3 12 Sweden 13 3 South Africa 23 28

Germany 4 1 Canada 14 14 Italy 24 22

Netherlands 5 4 Luxembourg 15 5 Ireland 25 11

Denmark 6 16 Switzerland 16 6 China 26 27

Belgium 7 9 United Arab Emirates 17 24 Turkey 27 39

Japan 8 7 Australia 18 18 Portugal 28 34

United States 9 15 Taiwan 19 20 Malaysia 29 29

United Kingdom 10 8 Spain 20 25 Poland 30 30

Source: World Bank

Industry Overview

10

Top Logistics Enterprises in China

11

• In 2011, CFLP ranked the top 50‐local logistics enterprises in China, based on their annual sales revenue in 2010. Tables above show the top‐20 ranking

• All of the top‐50 registered an annual sales revenue over 1.5 billion yuan in 2010• In terms of scope of business, 26 out of the top‐50 are integrated logistics enterprises. 22

specialize on transportation and the rest provides warehouse services• Most of the top‐20 enterprises recorded double digit growth in their 2010 annual sales

revenue. Some are new faces in the top‐20, reflecting that Mainland logistics enterprises are facing increasing competition in the high growth logistics market

Top 20 Mainland logistics enterprises by sales revenue, 2010Ranking in

2010Ranking in

2009 Logistics enterprises 2010 (billion yuan)

% yoy growth

1 1 China Ocean Shipping (Group) Company 中國遠洋運輸集團總公司

143.6 37.3

2 2 SINOTRANS & CSC Holdings Co. Ltd中國外運長航集團有限公司

91.6 27.9

3 3 China Shipping (Group) Company 中國海運集團總公司

64.2 43.9

4 6 Xiamen Xiangyu Group Co. Ltd 廈門象嶼集團有限公司

25.7 51.4

5 7 China Railway Material Company 中鐵物資集團有限公司

22.7 61.0

6 5China National Materials Storage and Transportation Corporation (CMST) 中國物資儲運總公司

22.0 23.8

7 ‐ Hebei Logistics Industry Group Co., Ltd. 河北省物流產業集團有限公司

16.4 ‐

8 10 Henan Coal and Chemical Industry Group Co. Ltd. 河南煤業化工集團國龍物流有限公司

16.2 83.9

9 9 China Petroleum Transportation Corporation 中國石油天然氣運輸公司

14.6 45.9

10 14 The S.F. Express Company 順豐速運(集團)有限公司

11.4 76.4

Ranking in 2010

Ranking in 2009 Logistics enterprises 2010

(billion yuan)% yoy growth

11 12 China Railway Container Transport Co. Ltd 中鐵集裝箱運輸有限責任公司

10.6 29.4

12 ‐ Anji Automotive Logistics Company 安吉汽車物流公司

10.0 ‐

13 11 Shuohuang Railway Development Co. Ltd. 朔黃鐵路發展有限責任公司

9.6 9.2

14 16 International Cargo Transport Limited of China 中國國際貨運航空有限公司

8.6 60.9

15 47 China Minmetals Logistics Corporation 五礦物流集團有限公司

8.0 ‐

16 13 China Railway Express Co. Ltd 中鐵快運股份有限公司

7.7 6.4

17 17 Yunnan Logistics Industry Group 雲南物流產業集團有限公司

7.5 45.0

18 15 Beijing Huayou Natural Gas Co. Ltd, CNPC 北京華油天然氣有限責任公司

7.1 16.3

19 ‐ SITC International Holdings Company Ltd. 海豐國際控股有限公司

6.03 ‐

20 18 SINOPEC Pipeline Transport & Storage Co. 中國石油化工股份有限公司管道儲運分公司

6.01 34.4

Source: China Federation of Logistics & PurchasingSource: China Federation of Logistics & Purchasing

Keen Competition in China~ Four types of large‐scale logistics enterprises

12

Types Selected Enterprises Pros Cons Latest Development

State‐owned ‐Sinotrans‐COSCO‐China Post

‐Large‐in‐scale‐Pan‐China network‐Good relationship with governments

‐Overstaffing‐Low operational efficiency ‐Not customer‐oriented

‐Improve efficiency by merger and acquisition

The new breed(Private‐owned or joint venture)

‐PG Logistics‐JC Trans‐SF Express

‐Clear market segment in terms of locations, services and targeted customers‐Relatively efficient‐Rapid growth

‐Limited fixed assets‐Lack of funding for market expansion‐Constrained by internal management and company structure

‐Form strategic partnership with other competitive counterparts or investors

The spin off(logistics subsidiary of large‐scale enterprise)

‐Midea‐Haier

‐With specialist knowhow‐Good network coverage

‐Difficult to develop external client base‐Future strategic plan and positioning affected by mother company

‐Operate independently from mother company

Foreign players ‐FedEx‐DHL‐UPS‐TNT

‐Strong overseas network‐Good logistics operation knowhow‐Widespread adoption of IT

‐Relatively weak domestic network in China‐Limited scope of business in China ‐High operating cost in China

‐Expand their Mainland market by merging or forming strategic partnership with local players

Note: Pros and cons, and latest development may not apply to the enterprises listed in the table aboveSource: Internet sources; complied by Li & Fung Research Centre

Performance of Chinese Logistics Enterprises

13

• 42.1% of the surveyed logistics enterprises recorded a profit margin of 5‐10%, while 28.6% indicated that their profit margin was between 3‐5% in 2010.

• Average profit margin reached 5.4% in 2010, slightly higher than the previous year. • Overall, the profitability of logistics enterprises in China is still low. Heavy tax burden, high

toll fees, expensive fuel costs and rising labour wages are trimming the profit margin of Chinese logistics enterprises. For details, challenges facing the logistics enterprises are shown in Section II

Profit margin of Chinese logistics enterprise, 2010

2009Average profit margin: 5.32%

2010Average profit margin: 5.40%

ProfitMargin

Source: National Development and Reform Commission, and Nankai University

Performance of Chinese Logistics Enterprises (cont’d)

14

• In 2010, 77.8% of the surveyed logistics enterprises utilized over 70% of the capacity of their vehicles, while 80.4% of them used over 70% of the capacity of their warehouses.

• Average utilization rate of vehicles and warehouses both increased in 2010, indicating an improvement in the efficiency of logistics enterprises

Utilization rate of vehicles of logistics enterprises

Utilization rate of warehouses of logistics enterprises

2009Average utilization rate:

77.96%

2010Average utilization rate:

81.04%

Source: National Development and Reform Commission, and Nankai University Source: National Development and Reform Commission, and Nankai University

2009Average utilization rate:

78.52%

2010Average utilization rate:

80.81%

Utilization rate

Utilization rate

Performance of Chinese Logistics Enterprises (cont’d)

2008 2009 2010Global positioning system 2 1 1

Barcode system 3 3 2

Electronic data interchange 1 2 3

Radio frequency identification 5 4 4

Automated sorting system 6 6 5

Electronic ordering system 4 5 6

% of adoptionBarcode system 57.9%Radio frequency identification 53.8%Electronic data interchange 46.4%Electronic ordering system 35.1%Global positioning system 20.8%Automated sorting system 13.9%Others 4.5%

15

• In 2010, 80.3% of the surveyed logistics enterprises applied Global Positioning System (GPS) in their operations, while 74.6% and 70.8% of the surveyed enterprises adopted barcode technology and Electronic Data Interchange (EDI) system, respectively

• When asked which kind of information technology applications the surveyed enterprises would consider to invest in the future, barcode technology, Radio Frequency Identification (RFID) and EDI system were the most mentioned

Major IT applications adopted by logistics enterprises, 2008 – 2010

Future adoption of IT applications by logistics enterprises

Source: National Development and Reform Commission, and Nankai University Source: National Development and Reform Commission, and Nankai UniversityNote: multiple responses allowed

Industry Overview

16

Outsourcing Rate of Industrial and Commercial Enterprises

17

• Although the outsourcing rate of logistics operations of Chinese industrial and commercial enterprises is still lower than the similar records in the developed countries, the rate has been rising over the last few years

• The outsourcing rate climbed up to 63.3% in 2010. This reflects that a growing number of Chinese enterprises recognized the benefits of outsourcing and started to outsource non‐core functions to third parties

Outsourcing rate of Chinese industrial and commercial enterprises, 2006 – 2010

Source: National Development and Reform Commission, and Nankai University

Outsourcing Level of Logistics Functions and Numbers of Logistics Service Providers

18

• Enterprises are becoming more receptive to the idea of outsourcing and are more willing to outsource a significant proportion of their logistics functions. They could reduce transaction costs by outsourcing their logistics functions to an optimal number of LSPs

• In 2010, 69.4% of the surveyed industrial and commercial enterprises outsourced more than 50% of their logistics functions by volume; over 40% of the surveyed enterprises even outsourced more than 80% of their logistics functions by volume

• Besides, 74% of the surveyed enterprises outsourced their logistics functions to 2 – 5 LSPs

Outsourcing level of logistics functions of the surveyed enterprises, 2010

Number of logistics service providers (LSPs) contracted with the surveyed enterprises, 2010

Outsourcing level

Number ofLSPs

Source: National Development and Reform Commission, and Nankai University Source: National Development and Reform Commission, and Nankai University

Types of Logistics Service(s) Outsourced

2009 2010

Transportation 42.6% 47.8%

Distribution 38.3% 43.1%

Warehousing 15.5% 16.3%

Logistics information management 15.6% 16.2%

Packaging & processing 13.5% 14.6%

Logistics system design 10.7% 11.5%

Inventory management 5.4% 5.9%

Others 2.1% 2.3%

% to be outsourced

Logistics information management 38.9%

Logistics system design 25.6%

Packaging & processing 17.8%

Warehousing 12.8%

Inventory management 9.1%

Distribution 8.3%

Transportation 4.1%

19

• Traditional functions such as transportation and distribution were the most popular services the surveyed enterprises outsourced

• When asked which services the surveyed enterprises would consider to outsource in the future, logistics information management and logistics system design were the most mentioned

• It reveals that Chinese enterprises are becoming more open to outsource more advanced logistics functions to LSPs

Types of logistics services outsourced Types of logistics services to be outsourced in the future

Source: National Development and Reform Commission, and Nankai University Source: National Development and Reform Commission, and Nankai UniversityNote: multiple responses allowed Note: multiple responses allowed

Industry Overview

20

Latest Development of Transport Infrastructure

2010(billion yuan)

% yoy growth

Highway 1,276 20.9

Railway 750 12.5

Water 208 24.4

Air 89 46.3

Total 2,322 19.1

21

• A comprehensive transportation network is the foundation for the development of logistics industry.

• Improving transport infrastructure has always been a priority for the government in China. The networks of the four modes of transport (road, railway, water and air) have been expanding over years

• The total fixed assets investment in the logistics industry grew by 19.4% to 3,070 billion yuan in 2010; Investment in transportation accounted for 75.7% of the total fixed assets investment in the logistics industry in 2010

Fixed assets investment in four major modes of transport in China, 2010

Capacity of transport infrastructure in China, 2010

Source: National Bureau of Statistics of China

For more information on the four modes of transport in China, please refer to our Newsletters –An Update on the Transport Infrastructure Development in China, 2011: Road (Issue 87), Water (Issue 88), Air (Issue 92) and Rail (Issue 93)http://www.lifunggroup.com/eng/knowledge/research.php?report=china&version=archive&category=logistics

Unit 2010 % yoy growth

Length of highway '000 km 4,008 3.8

‐ Length of expressway '000 km 74 13.8

Length of railway '000 km 91 6.7

Length of navigable inland waterway '000 km 124 0.4

Number of airports each 175 6.1

Source: National Bureau of Statistics of China

Traffic Volume

Total freight traffic

(million tonnes)

Total freight tonne‐kilometers (billion tonne‐km)

Mode of transport 2010 % yoy

growth 2010 % yoygrowth

Road 24,480.5 15.0 4,339.0 16.7

Railway 3,642.7 9.3 2,764.4 9.5

Water 3,789.5 18.8 6,842.8 18.9

Air 5.6 26.4 17.9 41.8

22

• Both passenger and freight traffic recorded steady increases in 2010• Road remained the major mode of transport to dispatch both passengers and freight in

China• Among the four modes of transport, air had the most impressive growth rates in terms of

passenger traffic (up by 16.1% yoy in 2010) and total passenger‐km (up by 19.7% yoy in 2010)

• Again, growth rates of the air transportation were the highest for freight traffic: freight traffic up by 26.4% yoy and freight tonne‐km up 41.8% yoy in 2010

Passenger services in China Freight services in ChinaTotal passenger

traffic (million persons)

Total passenger kilometers

(billion passenger‐km)

Mode of transport 2010 % yoy

growth 2010 % yoy growth

Road 30,527.4 9.8 1,502.1 11.2

Railway 1,676.1 9.9 876.2 11.2

Water 223.9 0.3 7.2 4.3

Air 267.7 16.1 403.9 19.7

Source: National Bureau of Statistics of China Source: National Bureau of Statistics of China

II. Challenges

23

Challenges ‐ External Economic Environment• Fewer export orders require less logistics services, e.g. reduced demand

for transporting raw materials in China and exporting goods out of China

• Major factors affecting the export volume in China include:– Volatile global economy

• The European debt crisis• Sluggish recovery of the US economy • Social instabilities in the Middle East and North Africa

– Trade protectionism against China– RMB appreciation – Increasing cost of production in China

24

Challenges ‐ Infrastructure• Infrastructure projects on airports, ports and railway are now putting in

place in China. However, infrastructure development mainly concentrates in coastal areas. Inland China still lags behind

• More and more coastal enterprises sourced from/ relocated to inland China. Due to different nature of goods, imbalance movement of traffic is common between coastal and inland areas. For example, raw materials are transported to inland by truck, while final high‐end products are exported directly to overseas markets by air. Return of empty load trucks to coastal cities is costly and environmental unfriendly

• Warehouses in China are sub‐standard, e.g.:– Lack of temperature controlled storage for goods that required cold chain facilities– Not enough loading docks for trucks; wastage of turnaround time– Inefficient manual operation and low adoption of warehouse management technology– Low visibility level of inventory control and no real time information sharing

• Land hoarding practices in China are very common. Landlords reserve part of sites for self use and lease out the rest as warehouse for profit; however, warehouse design may not suit the needs of LSPs

25

Challenges ‐ Transportation• High toll fees are imposed by local governments for recovering the

construction costs of roads and bridges. The toll charges may account for 30 to 40% of transport costs of trucking firms

• Many cities pose specific requirements on in‐town trucking services, e.g., – Operators must obtain specific license(s) to operate in‐town trucking services.

However, the number of licenses granted to trucking firms are affected by limited quota. Some companies, failed to get proper licenses, may either pay higher cost to hire licensed trucking firms to convey the goods or operate without license with a risk of being fined

– Limitation on loading time inside city reduces operational flexibility

• Increasing fuel cost is another headache for logistics operators. To strive for a living, overloading trucks are commonly found in China. Road accidents occur easily and roads are often blocked for clearance. Severe traffic jam makes no guarantee for on‐time delivery

• Vehicles used by small operators are mostly open trucks or those simply covered by canvas. Product damage and security are big issues

26

Challenges ‐ Logistics Cost• Rising wages, rentals, water and electricity fees increase the burden of

logistics operators – Promoting domestic market is one of the key issues in the 12th Five‐year plan.

To encourage domestic spending, minimum wage levels in many provinces have already increased by more than 10%. For many enterprises, the persistently increment in labour costs is a great challenge

– Rentals and land costs are increasing on the Mainland

• Many small‐ and medium‐sized operators often find it hard to secure cheaper finance; thus, it is challenges for them to equip better facilities, adopt sophisticated IT applications or extend their network to more cities

27

Challenges ‐ Fragmented Logistics Sector• China’s logistics market remains highly fragmented; there are large number

of small‐scale local LSPs. These logistics firms possess local knowhow and offer services at affordable prices. However, no single trucking firm possesses nationwide network with full coverage to all cities and villages. High transaction costs are often incurred, as enterprises have to deal with numerous of logistics operators

• Some small‐scale local LSPs may not adapt to modern logistics practices. Their service standard may not always comply with the requirements listed in the standard operation procedures. It takes time to establish mutual trust and standardized processes

• The sub‐standard logistics services also explain the self‐management mentality of enterprises. Low level in outsourcing logistics functions may hinder the growth of China’s logistics sector

28

Challenges ‐ Human Resources• Insufficient supply of logistics manpower is a critical issue. Although

there are increasing number of graduates in in logistics and transport in China, the labour supply is far less than the demand in China. And labour shortage also leads to high turnover rates in the competitive labour market

• Many practitioners lack modern management knowledge and skill sets to satisfy the increasingly demanding clients

• Many foreign companies have set up their businesses in China and sought for LSPs with local experiences. Staff of local firms usually possess hands‐on operational experience, however, many of them fail to communicate with the potential clients in foreign languages. Other the other hand, many are well‐educated, but lack the relevant experience and soft skills. As a result, local firms may easily lose the contracts to foreign LSPs in China

29

Challenges ‐ Government and Regulations• Lack of high‐level coordination among government departments leads to

multiple jurisdictions– The Ministry of Railways still retains as a separate ministry from the Ministry of

Transport, which have consolidated civil aviation, postal services, communications and urban public transportation since 2008. It is still a long way to develop intermodal transportation between rail and other transport modes

• Imperfect regulations and lack of standardization on logistics operation deter a healthy development of the industry

– To provide all‐round logistics services in China, LSPs need to apply various operating licenses; these licenses are often issued by various government departments. Application for the licenses may be costly and the process may be quite lengthy

– Also, enterprises have to pay multiple taxes to different government bodies at different rates, adding further cost burden to LSPs

30

III. Government Policies

31

Government PoliciesOpinions of the State Council on the releasing plans for adjusting and accelerating the logistics industry (The Opinions)《國務院關於印發物流業調整和振興規劃的通知》

32

Launch date August 2011

Launch by The State Council

Key highlights

• Premier Wen Jiabo highlighted 8 measures to promote a healthy development of the logistics industry in the committee meeting of the State Council in June 2011, including: 。Reduce tax burden of logistics enterprises。Enhance policy support on land use allocation in favour of logistics industry。Promote a better operation environment for trucking services。Improve the management of logistics enterprises。Encourage integration of logistics facilities and resources。Promote the innovation and application of logistics technology。Increase the inputs to logistics industry。Support the development of agricultural products logistics

• In August 2011, the State Council promulgated The Opinions. On top of the 8 measures mentioned, another measure was added: 。Enhance the coordination between stakeholders, accelerate the functions and management of government in promoting logistics industry

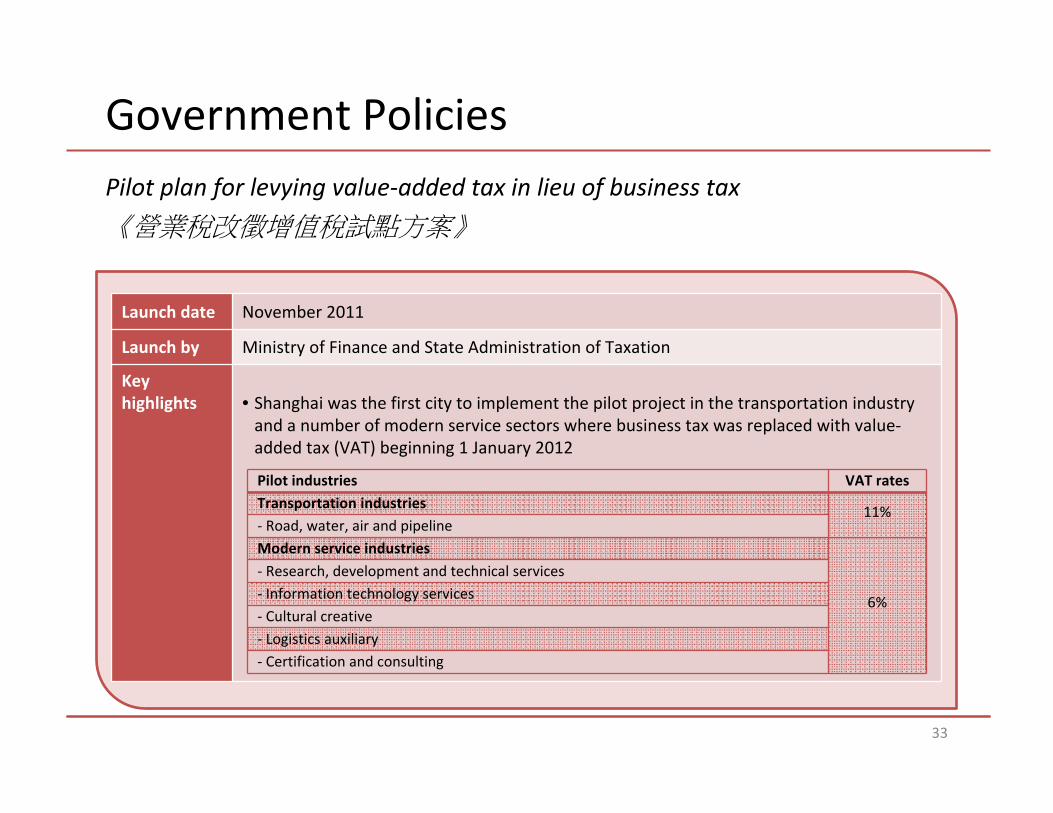

Government PoliciesPilot plan for levying value‐added tax in lieu of business tax 《營業稅改徵增值稅試點方案》

33

Launch date November 2011

Launch by Ministry of Finance and State Administration of Taxation

Key highlights • Shanghai was the first city to implement the pilot project in the transportation industry

and a number of modern service sectors where business tax was replaced with value‐added tax (VAT) beginning 1 January 2012

Pilot industries VAT ratesTransportation industries 11%‐ Road, water, air and pipelineModern service industries

6%

‐ Research, development and technical services‐ Information technology services‐ Cultural creative‐ Logistics auxiliary‐ Certification and consulting

Government PoliciesNotice on urban land use tax policy for bulk commodity storage facilities of logistics enterprises 《關於物流企業大宗商品倉儲設施用地城鎮土地使用稅政策的通知》

34

Launch date February 2012

Launch by Ministry of Finance and State Administration of Taxation

Key highlights • From 1 January 2012 to 31 December 2014, a 50% reduction of current urban land use

tax will be applied to the land for bulk commodity storage facilities owned by logistics enterprises (whether self‐used or leased out)

• Land for bulk commodity storage facilities refer to the area of land for storage facilities exceeding 6,000 sq m

IV. Special Topic: Retail Logistics in China

35

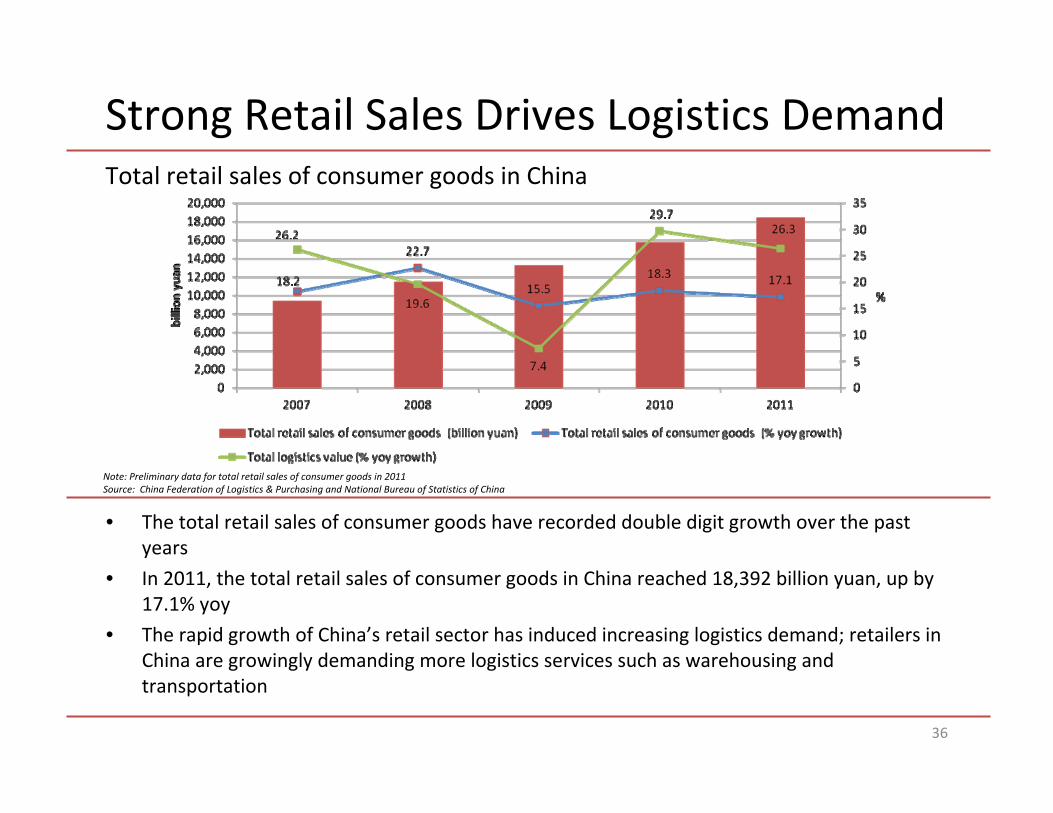

Strong Retail Sales Drives Logistics Demand

36

• The total retail sales of consumer goods have recorded double digit growth over the past years

• In 2011, the total retail sales of consumer goods in China reached 18,392 billion yuan, up by 17.1% yoy

• The rapid growth of China’s retail sector has induced increasing logistics demand; retailers in China are growingly demanding more logistics services such as warehousing and transportation

Total retail sales of consumer goods in China

Note: Preliminary data for total retail sales of consumer goods in 2011Source: China Federation of Logistics & Purchasing and National Bureau of Statistics of China

Logistics Cost Composition Varies among Different Consumer Goods

% of transportation cost in total

logistics cost (%)

% of interest cost in total

logistics cost (%)

% of storage cost in total logistics

cost (%)

% of management cost in total

logistics cost (%)

% of packing/ processing/

distribution cost in total logistics cost

(%)Retailing in department stores,

supermarket and etc. 55.5 6.2 2.0 26.8 7.4

Food, beverage and tobacco products retailing 58.7 4.1 1.0 24.0 12.0

Apparel and daily commodity products retailing 46.1 3.8 11.5 22.3 6.8

Pharmaceutical products and equipment retailing 30.4 1.0 12.6 28.5 20.4

37

• According to a logistics survey conducted jointly by the National Development and Reform Commission, the National Bureau of Statistics and China Federation of Logistics and Purchasing in 2011, logistics cost components of different consumer goods varied considerably among the surveyed retail enterprises

• Transportation cost accounted for the highest portion of the total logistics cost of all surveyed retailers• However, other cost components varied significantly among retailers across different industry segments.

E.g. the surveyed pharmaceuticals retailers generally bore higher storage cost and packing, processing and distribution cost than the surveyed apparel retailers due to the fact that pharmaceutical products often require temperature‐controlled storage and distribution facilities

Composition of total logistics cost

Source: National Development and Reform Commission, National Bureau of Statistics and China Federation of Logistics and Purchasing

Retail Logistics Process is Complex• Key benchmarks for effective store

operation and logistics management include:

– 5R of delivery: Right place, right quantities, right quality, right time and right price

– Accurate inventory control – Just‐in‐time replenishment of stocks

• Logistics processes and requirements vary among different consumer products, for instance:

– Well pick and pack, sorting processes, and effective distribution mechanisms for handling fast moving consumer goods (FMCG)

– Temperature controlled storage and transportation are crucial when handling fresh and frozen foods

– Warehouse management and inventory control are important in fashion logistics

The case for L’Oréal in China• L’Oréal is one of the world’s leading cosmetics

enterprises• The Group has a retail network of more than

200,000 selling points in China• The retail channels and corresponding

distribution practices for L’Oréal brands can be very different and complex, depending on their target consumer segments

38

Retail channels Distribution practices

High‐end cosmetics brands (e.g. Lancome and Kiehl’s)

• Sold in sales counters of prominent areas of department stores

• The frequency of inventory replenishment is fairly high• Each batch of delivery usually covers a wide range of items but with small quantities

Mid‐range cosmetics products (e.g. Maybelline, Garnier, Vichy and L’Oréal Paris

• Sold in hypermarkets, which provide larger storage space for the retailers

• Each batch of delivery is larger in quantity• Replenishment of the cosmetics products is less frequent

Professional product line(e.g. Kérastase)

• Mainly distributed via hair salons

• Customized logistics services , subject to specific need of individual customer

Reverse Logistics Remains a Key Element in Retail Logistics• Reverse logistics has become

increasingly critical in China’s retail logistics market in recent years

• As pricing, quality and cycle time become more or less the same among retailers, reverse logistics can be a distinct differentiator

• The reverse logistics flow normally requires extra storage capacity and handling process, some retailers in China choose to outsource the reverse logistic process to LSPs

Reverse logistics• What is it?

– the management of all the logistics activities involved in the flow of goods in the opposition direction of the primary logistics flow

• Why reverse flows?– Return or exchange of products by

consumers– Unsalable goods returned by retailers

to distribution centers or suppliers– Withdrawal of problematic goods by

suppliers– Return of damaged goods to

suppliers due to mishandling in the processes of storage or distribution

39

IV. Special Topic: Retail logistics in China

40

Self‐owned and Operated Logistics Facilities are Common among Large‐scale Retailers in China• More large‐scale retailers in China are

setting up their own logistics facilities to better manage the logistics flows of their operations

• According to China Chain Store and Franchise Association, 60% of retail enterprises in China operated their own logistics facilities in 2010

The case for RT‐Mart• Taiwan‐based RT‐Mart (大潤發), one of the

leading hypermarket chains in China, has set up its own informatized logistics system and distribution centers in China

• Functions of their informatized logistics system: – Allow seamless information transmission

between hypermarkets and their respective regional headquarters

– Provide sales data analysis and determine the optimal inventory levels via the warehouse management system (WMS)

– Capable to process purchase orders instantly via the inventory replenishment system

• Benefits of the adoption of the informatized logistics system:

– Able to adjust product mix, inventory level and pricing in real time

– Enhance the responsiveness to the changes in market demand

– Enhance the overall sales performances of the hypermarkets

41

Source: China Chain Store and Franchise Association

Proportion of retail enterprises who owned & Proportion of retail enterprises who owned & operated their logistics facilities, 2010operated their logistics facilities, 2010

Self‐owned and Operated Logistics Facilities are Common among Large‐scale Retailers in China (cont’d)Cold chain logistics in China• Setting up cold chain facilities generally

involves much higher capital investments • According to “China Cold‐Chain Logistics

Development Report (2010)”, the cost of setting up cold chain storages and refrigerated trucks in China can be three to five times higher than building normal warehouses and trucks

• In China, small‐ and medium‐sized logistics enterprises are rarely capable to provide integrated cold chain logistics services with nationwide network coverage

• To ensure the food quality and safety, more large‐scale food processing enterprises have established their own logistics subsidiaries to manage cold chain logistics processes

The case for Zhongpin Inc.• Zhongpin Inc. (眾品集團) is one of the

leading enterprises in agricultural processing industry in China

• The Group have set up a logistics subsidiary to provide distribution, storage, processing and other value‐added services for internal clients since 2004

• Now, the logistics subsidiary has also served as a third party cold chain logistics service provider for its downstream partners, such as Zhengzhou Sanquan Foods Co. Ltd. (三全食品) and Zhengzhou Synear Food Co. Ltd. (思念食品)

42

Third‐party retail logistics development gathers paceGrowing number of international LSPs have entered retail logistics businesses•Retailers both at home and abroad are increasingly demanding for sophisticated logistics services on the Mainland•There are ample opportunities for international LSPs to expand their foothold in China’s retail logistics market

Local small‐ and medium‐sized LSPs have a strong presence in lower‐tier cities and rural market•More large‐scale retailers have accelerated their expansion into second‐ and third‐tier cities and the rural market in recent years•Instead of using their own logistics arms, they resort to competent local LSPs to distribute their products in remote regions

The case for Nike Inc.• Nike Inc., a famous international sport

wear enterprise, has set up a logistics center in Taicang, Suzhou in early 2011.

• The operation of this 200,000m2 logistics facility has been outsourced to Hong‐Kong based Li & Fung Ltd., the world’s leader in consumer goods design, development, sourcing and distribution.

• Orders from all Nike’s retail outlets can be efficiently and accurately processed in this centralized logistics center with the adoption of state‐of‐the‐art technologies such as WMS and voice picking technology

• The logistics operation services provided by Li & Fung greatly enhance Nike’s responsiveness to customers’ needs and increase overall efficiency

43

Online Retailing is Growing Fast in China; yet, Logistics Remains the Biggest Bottleneck• The logistics crunches have constrained

the development of online retailing and increased the logistics costs of online retailers

• Huge number of orders generated by online retailing have overloaded many express delivery companies

• According to a survey conducted by the State Post Bureau, on‐time delivery of China’s express delivery services remained dissatisfactory to over half of the respondents; around 52% of the complaints were related to delay of delivery

• To enhance the service quality, some online retailers strive for providing one‐stop‐shop logistics services to their customers

• Establish own logistics facilities – Vancl (凡客誠品), a pure‐click apparel

retailer, has established its own express delivery company, Rufengda (如風達)

– Rufengda provides last‐mile delivery services to its customers. They have a very strong network covering more than 1,200 cities on the Mainland

– Door‐to‐door delivery lead time of Vancl is within 24 hours

• Partner with other LSPs – Tmall (天貓), the dominant player in

China’s business‐to‐consumer (B2C) market, is a case in point

– Tmall provides one‐stop‐shop logistics services to its larger‐scale online sellers via its strategic partners such as warehousing services providers, express delivery companies as well as IT solutions providers

44

One‐stop‐shop logistics services

Government Supports in Retail Logistics

Launch date Name of Policy Launch by

July 2010 Development plan of cold‐chain logistics for agricultural product 《農產品冷鏈物流發展規劃》 NDRC

March 2011 Development plan of commercial logistics 《商貿物流發展專項規劃》 MOC, NDRC and ACFSMC

May 2011 Outline of development plan of national pharmaceutical circulation industry (2011‐2015) 《全國藥品流通行業發展規劃綱要(2011‐2015)》 MOC

August 2011Opinions of the State Council on the releasing plans for adjusting and accelerating the logistics industry 《國務院關於印發物流業調整和振興規劃的通知》* Based on a set of eight measures announced by the State Council in June 2011

The State Council

October 2011 Guiding opinions of development of e‐Commerce in 12th Five Year Plan 《十二五電子商務發展指導意見》 MOC

October 2011 Guiding opinions of accelerating the construction of tracking system for meat and vegetable circulation during 12th Five Year Plan period 《關於“十二五”期間加快肉類蔬菜流通追溯體系建設的指導意見》

MOC

November 2011 Pilot plan for levying value‐added tax in lieu of business tax 《營業稅改徵增值稅試點方案》 MOF and SAT

December 2011 Opinions of the general office of the State Council on strengthening the construction of circulation system for agricultural product 《國務院辦公廳關於加強鮮活農產品流通體系建設的意見》

The State Council

January 2012 Guiding opinions of MOC on accelerating the development of retail industry during 12th Five Year Plan period 《商務部發佈關於“十二五”時期促進零售業發展的指導意見》

MOC

February 2012 Notice on urban land use tax policy for bulk commodity storage facilities of logistics enterprises 《關於物流企業大宗商品倉儲設施用地城鎮土地使用稅政策的通知》

MOF and SAT

March 2012 Guiding opinions of accelerating the collaboration and development of express services and online retailing《關於促進快遞服務與網絡零售協同發展的指導意見》

SPB and MOC

45

• To create a more regulated and transparent environment for the development of the retail logistics market, the Chinese government has put in place a number of supportive policies in the past few years

Government policies related to retail logistics:Government policies related to retail logistics:

ACFSMC – All China Federation of Supply and Marketing CooperativesMOC – Ministry of CommerceMOF – Ministry of Finance

NDRC – National Development and Reform CommissionSAT – State Administration of TaxationSPB – State Post Bureau

For More InformationLi & Fung Research Centre10/F, LiFung Tower, 888 Cheung Sha Wan Road, Kowloon, Hong Kong

Tel: 2300 2470 Fax: 2635 1598Email: [email protected]://www.lifunggroup.com/

© Copyright 2012 Li & Fung Research Centre. All rights reserved.Though Li & Fung Research Centre endeavours to have information presented in this document as accurate and updated as possible, it accepts no responsibility for any error, omission or misrepresentation. Li & Fung Research Centre and/or its associates accept no responsibility for any direct, indirect or consequential loss that may arise from the use of information contained in this document.

46